Surgical Tourniquets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

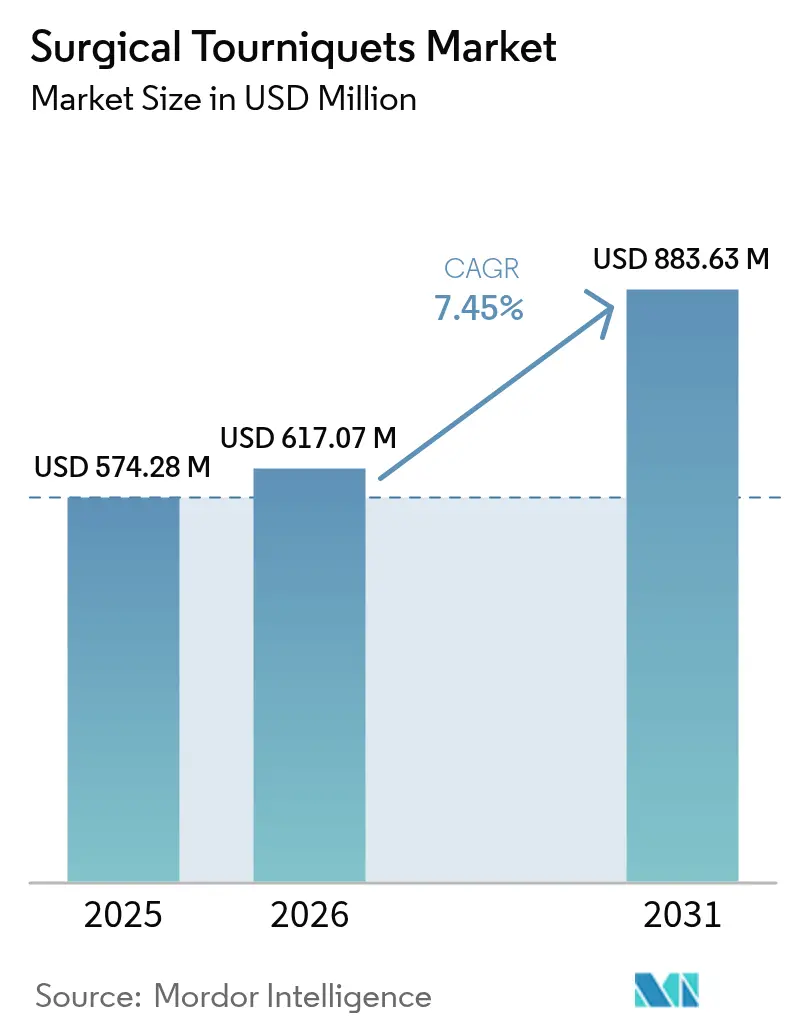

| Market Size (2026) | USD 617.07 Million |

| Market Size (2031) | USD 883.63 Million |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Tourniquets Market Analysis by Mordor Intelligence

The surgical tourniquets market size was valued at USD 574.28 million in 2025 and estimated to grow from USD 617.07 million in 2026 to reach USD 883.63 million by 2031, at a CAGR of 7.45% during the forecast period (2026-2031). Momentum stems from three intersecting forces: rising trauma caseloads linked to road accidents, sustained modernization of military medical corps, and quick uptake of limb-occlusion-pressure (LOP) technology that lowers the incidence of nerve injury during surgery. Emergency medical services now integrate tourniquet deployment into pre-hospital protocols after conflict data proved a 57.1% success rate in combat scenarios. Market penetration also benefits from infection-control mandates that heighten demand for single-use cuffs and from console-based systems that automate pressure adjustment, reducing litigation exposure for hospitals and ambulatory surgery centers.

Key Report Takeaways

- By product type, pneumatic systems retained 53.88% of the surgical tourniquets market share in 2025, while disposable sterile cuffs are advancing at an 8.51% CAGR to 2031.

- By application, lower-limb orthopedic surgery held 62.24% of the surgical tourniquets market size in 2025; trauma & battlefield stabilization is forecast to expand at a 9.01% CAGR through 2031.

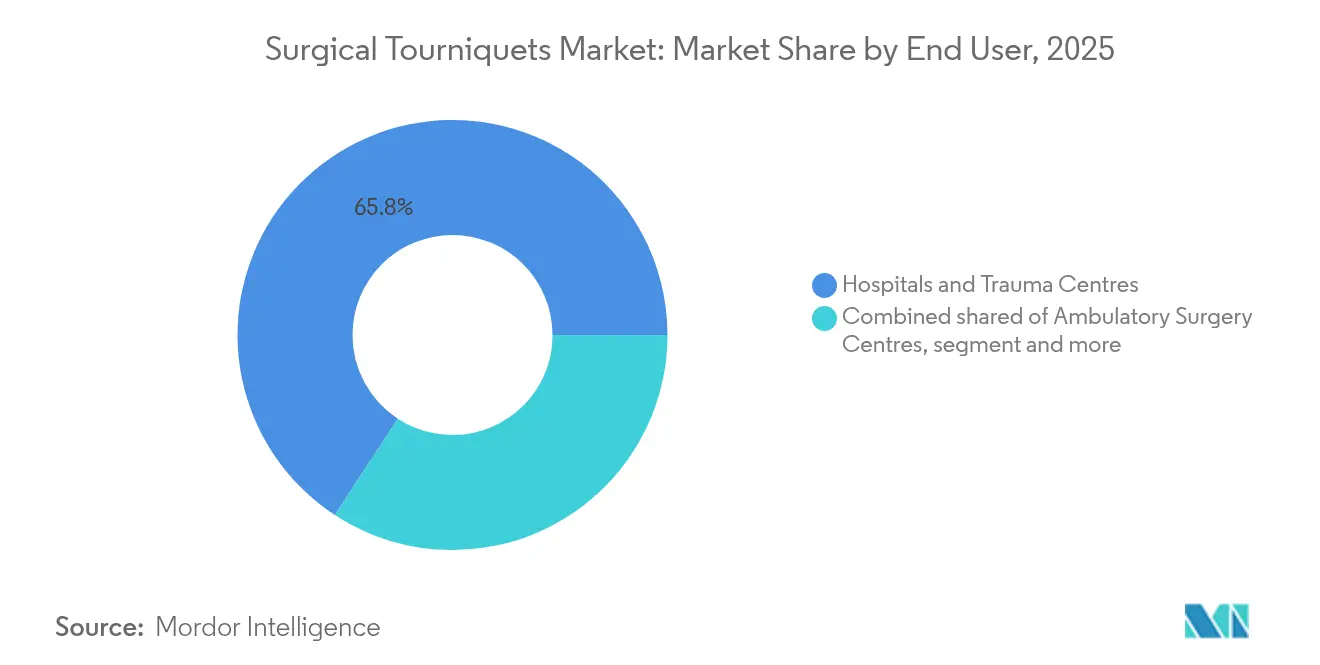

- By end user, hospitals and trauma centers accounted for 65.78% revenue share in 2025, whereas military medical units are set for a 8.89% CAGR to 2031.

- By technology, multi-channel consoles commanded 46.30% revenue in 2025; integrated pressure-feedback software is projected to grow at 9.26% CAGR through 2031.

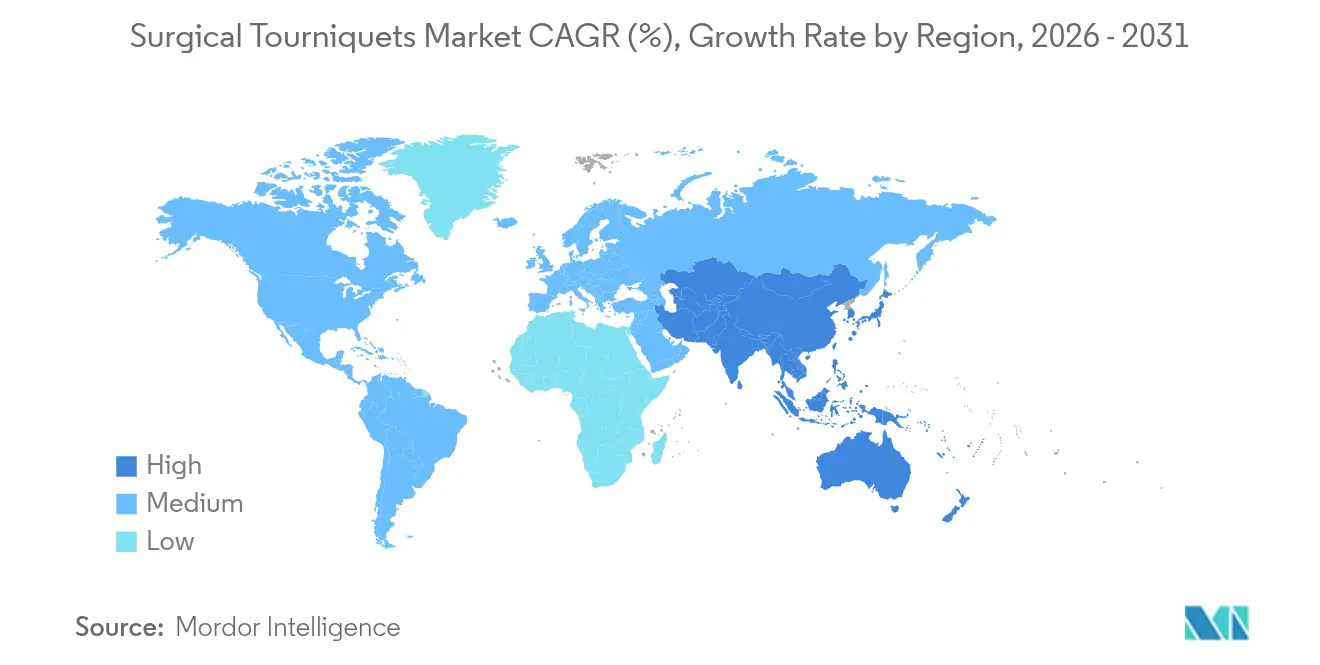

- By geography, North America led with 47.05% revenue share in 2025, yet Asia-Pacific is the fastest-growing region at 9.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Surgical Tourniquets Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising trauma & road-accident surgeries | +1.8% | Global, with concentration in APAC emerging markets | Medium term (2-4 years) |

| Growth in elective Orthopedic & joint-replacement volumes | +2.1% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Expansion of hospitals & ASC capacity in emerging economies | +1.5% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Adoption of LOP-smart tourniquet systems to cut nerve injuries | +1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Military demand for compact field tourniquets | +0.7% | North America, Europe, select APAC markets | Short term (≤ 2 years) |

| Shift to blood-sparing outpatient arthroplasty protocols | +0.3% | North America & Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Trauma & Road-Accident Surgeries

Military casualty data, notably from the Russia–Ukraine conflict, validated tourniquet efficacy and spurred civilian EMS adoption. Field studies show mass-casualty tourniquet placement times under two minutes, a capability increasingly embedded in paramedic curricula worldwide.[1]SJTREM Editorial Board, “Rapid tourniquet deployment in mass casualty events,” sjtrem.biomedcentral.com The Combat Application Tourniquet consistently achieves superior arterial occlusion when applied over clothing, a critical advantage for first responders wearing protective gear. Civilian uptake accelerates via STOP THE BLEED campaigns, and county EMS agencies in Texas deployed abdominal aortic junctional devices in 2025 for non-compressible hemorrhage control.[2]EMS1 Staff, “Texas EMS adopts abdominal aortic junctional tourniquets,” ems1.com Evidence across 4,095 civilian trauma cases shows a 52% mortality reduction without higher amputation risk when tourniquets are used pre-hospital. This cross-sector momentum widens the surgical tourniquets market beyond operating rooms into pre-hospital care.

Growth in Elective Orthopedic & Joint-Replacement Volumes

Private hospital networks in India alone are adding up to 2,500 beds in fiscal 2025, with 11–12% revenue growth that lifts joint-replacement caseloads. Aging demographics and broader insurance coverage support higher procedure volumes, while medical tourism now contributes 10–12% of hospital top lines across Asia-Pacific. Study data reveal that tourniquet use in total knee arthroplasty cuts intraoperative blood loss but slightly increases postoperative bruising.[3]BMC Musculoskeletal Disorders Editors, “Tourniquet outcomes in total knee arthroplasty,” bmcmusculoskeletdisord.biomedcentral.comConsequently, surgeons gravitate to pressure-feedback consoles that calibrate inflation to LOP readings, mitigating tissue-related complications. Silicone ring designs also gain favor because they extend surgical fields, a benefit in bilateral knee work.

Hospital & ASC Capacity Expansion in Emerging Markets

Leading Indian chains—Apollo, Max Healthcare, and Aster DM Healthcare—collectively plan 17,800 new beds, underpinned by USD 1.75 billion in announced capital outlays. ASEAN regulators have adopted a unified medical-device directive that speeds registration and scales the total addressable market for tourniquet suppliers. As purchasing departments migrate to bundled operating-room packages, consoles with integrated tourniquets, suction, and fluid-management systems become procurement norms. Training and after-sales support now weigh heavily in tender scoring, favoring vendors with regional service hubs. These conditions accelerate the surgical tourniquets market in emerging economies.

Adoption of LOP-Smart Tourniquet Systems to Cut Nerve Injuries

Peer-reviewed trials show LOP-calibrated protocols reduce average inflation pressure to 152 mmHg without changing surgical field quality. Stryker’s SmartPump uses EvenAIRe sensors for continuous adjustment, while Zimmer Biomet’s A.T.S. 5000 algorithmically tailors pressure to limb circumference. Hospitals adopting these systems report fewer nerve-injury claims, lowering malpractice premiums. Real-time data logging also satisfies emerging medico-legal standards that demand documented pressure profiles for every tourniquet case. As a result, smart consoles transition from premium niche to standard requirement, reinforcing growth in the surgical tourniquets market.

Restraints Impact Analysis of Surgical Tourniquets Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nerve-/tissue-damage litigation risk | -1.4% | North America & Europe primarily | Short term (≤ 2 years) |

| Shortage of staff trained in optimal pressure management | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Move toward tourniquet-less arthroscopy & TKA techniques | -1.1% | North America & Europe core, expanding globally | Medium term (2-4 years) |

| Cost spike from single-use & re-processing regulations | -0.9% | Global, with regulatory focus in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nerve-/Tissue-Damage Litigation Risk

Meta-analyses show tourniquet use during ACL reconstruction elevates postoperative drainage by 100 ml and increases short-term pain, sharpening plaintiff arguments in malpractice suits. Cardiac-cycle efficiency drops markedly during inflation under general anesthesia, adding peri-operative risk factors. Insurers are now pricing premiums against hospital adoption rates of pressure-feedback consoles. Legal precedents increasingly oblige facilities to log pressure duration, prompting procurement of devices with automated audit trails. Vendors that bundle extended warranties and indemnification clauses gain an edge as hospitals hedge liability in the surgical tourniquets market.

Shortage of Staff Trained in Optimal Pressure Management

Fast-growing hospitals often lack certified peri-operative technologists, leading to default use of fixed 250–300 mmHg settings that heighten complication risk. Advanced consoles include limb-specific presets, but staff unfamiliar with LOP calculations underutilize these features. Continuous education programs face time and budget constraints, especially in APAC where bed expansion outpaces workforce development. Manufacturers that offer e-learning modules and on-site workshops report higher customer retention. Conversely, facilities that defer training see elevated rates of nerve injury, which undermines confidence and slows conversion to next-generation tourniquet consoles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Surgical Tourniquets Market Segment Analysis

By Product Type:

Pneumatic Systems Dominate Despite Disposable InnovationPneumatic devices controlled 53.88% of the surgical tourniquets market in 2025 owing to reliable inflation control and established surgeon preference. Disposable sterile cuffs, however, are growing at an 8.51% CAGR as infection-control guidelines push operating rooms toward single-use supplies. Re-usable cuffs now face performance audits that track cross-contamination events, amplifying the shift.

Hospitals that migrated to single-use cuffs during pandemic conservation mandates report 27% lower sterilization labor cost. Simultaneously, intelligent cuffs embedded with RFID facilitate automatic pairing with smart pumps, ensuring pressure accuracy logs match individual patients. Waterproof drape innovations further reduce skin burns in knee arthroscopy, improving patient satisfaction and accelerating adoption.

By Application:

Lower-Limb Procedures Lead While Trauma Applications AccelerateLower-limb orthopedic surgery accounted for 62.24% of the surgical tourniquets market size in 2025, supported by sustained growth in knee and hip replacements. Nonetheless, trauma and battlefield care registers the highest CAGR at 9.01%, thanks to new military field kits and EMS protocols that stipulate tourniquet use within two minutes of extremity hemorrhage.

Combat casualty research sparked design improvements such as junctional abdominal devices for pelvic bleeding, broadening indication scope. Concurrently, upper-limb demand remains stable through wrist reconstruction and micro-vascular flap procedures, while plastic surgeons adopt silicone ring systems to expand incision visibility without raising pressure.

By End User:

Hospital Dominance Challenged by Military ExpansionHospitals and trauma centers represented 65.78% revenue share in 2025 as bulk buyers of multi-channel consoles and audit-compliant software. Military and defense medical units, however, are set to outpace all others at a 8.89% CAGR because of defense modernization budgets and the proven 57.1% combat success rate of tourniquets.

Defense buyers prioritize ruggedized, lightweight kits deployable under extreme weather. Meanwhile, ambulatory surgery centers invest in consoles paired with blood-loss-estimation AI to support same-day discharge models. Sports clinics and expeditionary medicine teams create a tail market for compact belt-pack tourniquet kits.

By Technology:

Multi-Channel Systems Prevail as Smart Integration AdvancesMulti-channel consoles retained 46.30% value share in 2025 because they manage multiple limbs in complex orthopedic reconstructions. Smart pressure-feedback modules are projected to log a 9.26% CAGR, propelled by evidence that LOP-based algorithms secure 90% bloodless fields at lower pressures while trimming nerve-injury incidence.

Hybrid consoles now integrate cloud connectivity for real-time analytics, allowing biomedical engineers to monitor seal integrity and schedule preventive maintenance remotely. The tourniquet systems industry thus migrates from hardware-centric propositions to data-rich service models that align with hospital digital-strategy roadmaps.

Geography Analysis

North America Surgical Tourniquets Market

North America’s 47.05% share in 2025 rests on advanced trauma systems, defense procurement, and early approval pathways such as FDA 510(k) expedited reviews, but it also sees a nascent shift toward tourniquet-less protocols in select orthopedic centers. Regional sales therefore tilt toward consoles with adaptive pressure curves that reassure surgeons wary of litigation. Texas county EMS adoption of junctional tourniquets for non-compressible bleeds underscores continuing growth in pre-hospital niches. Corporate consolidation, illustrated by Stryker’s USD 4.9 billion Inari Medical purchase, extends competitive breadth into thrombectomy—a logical adjacency to bleeding-control technologies.

APAC Surgical Tourniquets Market

Asia-Pacific records the fastest CAGR at 9.43%, fueled by USD 1.75 billion bed-expansion programs across Indian hospital networks and by regulatory harmonization that eases device approvals across ASEAN. Medical-tourism inflows fortify procedure volumes, while government initiatives such as e-medical visas for 167 countries further widen access. Domestic manufacturing drives price competition; India’s Make-in-India framework encourages local sourcing, which presses multinationals to establish joint ventures or risk market share erosion.

EMEA and South America Surgical Tourniquets Market

Europe maintains steady uptake under cohesive medical-device regulations and growing preference for premium LOP consoles. Ulrich medical allocated EUR 5 million in 2024 to scale production, reporting a 12% revenue uplift to EUR 150 million—evidence that medium-sized players can prosper in specialized niches. Middle East and Africa funnel petro-revenues into trauma-center upgrades, and South America’s private-hospital groups cautiously phase in smart consoles, though macroeconomic volatility remains a headwind. Collectively, these dynamics distribute growth pockets that vendors must navigate with agile channel strategies to capture share in the surgical tourniquets market.

Regulatory Landscape

Regulation for surgical tourniquets is anchored in medical-device frameworks that differentiate pneumatic consoles/cuffs and manual extremity tourniquets by intended use, sterility, and measurement claims. In the United States, pneumatic tourniquets are classified by the FDA under 21 CFR 878.5910 as Class I (general controls) and are generally exempt from 510(k) premarket notification, which shifts emphasis toward core controls such as establishment registration and device listing, labeling, and quality-system expectations.

In Europe, the EU Medical Device Regulation (Regulation (EU) 2017/745) governs classification and conformity assessment, with manual-use extremity tourniquets commonly falling under Class I pathways when they are non-sterile, non-measuring, and non-reusable (Annex VIII). Even where self-certification applies, manufacturers still need to maintain technical documentation and post-market surveillance, and EU UDI requirements reinforce traceability expectations that support the market shift toward documented pressure profiles and audit-ready use records in clinical settings.

Value Chain Analysis

The value chain spans raw materials (rubber compounds, synthetic textiles, plastics, and electronic components for pneumatic control units), component processing, and assembly into cuffs, tubing, and console-based systems with pressure-control software. For pneumatic systems, FDA Class I status under 21 CFR 878.5910 lowers premarket friction compared with higher-risk device classes, but manufacturers still operate under documented processes that support material traceability, lot controls, and consistent performance of pressure-regulation and safety features.

Commercialization flows through a mix of direct sales to large hospital groups and trauma centers, often tied to capital equipment tenders for multi-channel consoles, and distributor channels that broaden reach to smaller hospitals and ambulatory surgery centers. Aftermarket and reverse logistics differ by product type: single-use sterile cuffs move through high-velocity consumables replenishment aligned with infection-control policies, while reusable cuffs depend on reprocessing workflows and, in some cases, refurbishment cycles that can change total cost of ownership and purchasing decisions. Supply-chain sensitivity is higher for smart consoles that rely on specialized electronics, making availability of microprocessors and sensor components a practical constraint for advanced pressure-feedback platforms.

Competitive Landscape

The market sits at a moderate concentration level. Stryker and Zimmer Biomet headline the leader cohort, leveraging acquisitions and algorithmic pressure control to differentiate. Stryker’s SmartPump embeds EvenAIRe sensors that modulate inflation in milliseconds, while Zimmer Biomet’s A.T.S. 5000 employs Personalized Pressure Technology that individualizes occlusion settings. Both firms bundle cloud dashboards that feed usage analytics back to quality-improvement teams.

Ulrich medical’s EUR 5 million capacity expansion in Germany exemplifies European mid-tier commitment to specialty gear, enabling faster lead times and localized customization. In the disposable cuff segment, Dynarex introduced the DynaSafety line in 2024, bringing textured, non-pinching materials to the emergency-response channel. Delfi Medical advances single-use cuffs with integrated fill lines and matched limb sleeves, solving sizing errors that once plagued high-BMI patients.

Disruptive threats loom from thrombectomy advances such as milli-spinner devices that secure 90% clot-removal rates, potentially cutting tourniquet demand in certain vascular surgeries. Yet even here, cross-selling opportunities arise because vendors with vascular portfolios can position tourniquets as complementary for limb-sparing procedures. The interplay of innovation, litigation risk, and regional procurement norms keeps competitive intensity high, shaping strategic choices in the surgical tourniquets market.

Surgical Tourniquets Industry Leaders

Ulrich Medical

AneticAid Ltd

Zimmer Biomet

Hammarplast Medical AB

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Surgical Tourniquets Market Companies Covered in this Report

- Stryker

- Zimmer Biomet

- ulrich medical

- Hammarplast Medical

- Anetic Aid

- VBM Medizintechnik

- Delfi Medical Innovations

- Daesung Maref

- HemaClear (OHK Medical Devices Inc.)

- DESSILLIONS & DUTRILLAUX

- Riester

- SAM Medical

- Tactical Medical Solutions

- CAT Resources (C-A-T)

- Dynarex

- Medline Industries Ltd.

Market Opportunities and Future Outlook

Opportunities concentrate on safety standardization and automation that reduce variability in cuff selection and inflation-pressure decisions. In April 2025, AORN updated clinical guidance for pneumatic tourniquet safety, reinforcing standardized preoperative assessment, cuff selection, and safe pressure determination, which supports demand for systems that embed protocols into workflows and simplify documentation for hospitals and ambulatory surgery centers managing litigation exposure.

Technology whitespace is visible in adaptive, sensor-driven control that moves beyond static pressure settings toward personalized occlusion. Commercial platforms such as Stryker SmartPump and Delfi Medicals Personalized Tourniquet System illustrate the direction of travel toward minimum effective pressure with continuous sensing, while June 2026 peer-reviewed work in Frontiers in Medical Technology described an automated pneumatic tourniquet evaluated on an adaptive testing platform that achieved hemorrhage control in under one minute and addressed cuff slippage through control logic. These proof points, together with growing single-use cuff adoption driven by infection-control mandates, keep product development focused on integrated pressure-feedback software, audit trails, and easier-to-use designs where staffing and LOP training gaps persist.

Recent Industry Developments in Surgical Tourniquets Market

- June 2026: Researchers published a Frontiers in Medical Technology study describing an automated pneumatic tourniquet evaluated using an adaptive testing platform that achieved hemorrhage control in under one minute and incorporated control logic to address cuff slippage. The work reinforces R&D focus on sensor-driven, semi-automated pressure control that reduces dependence on operator technique. It also supports the shift toward designs that can be validated for faster deployment and more consistent performance across varied clinical users.

- April 2025: AORN released an updated guideline for pneumatic tourniquet safety, emphasizing standardized patient assessment, cuff selection, and safe inflation pressure determination. The update strengthens hospital demand for consoles and cuffs that support protocol adherence through features such as guided setup and pressure documentation. Vendors that align device workflows and training materials to AORN-aligned practices gain procurement advantages in risk-managed perioperative environments.

- January 2024: ulrich medical invested EUR 5 million to expand production capacity in Ulm, Germany, adding manufacturing capability for its surgical portfolio. The investment improved lead-time resilience for European supply and signaled ongoing commitment by mid-sized players to specialized surgical equipment. Expanded capacity also supports faster fulfillment for hospital tenders where delivery reliability and service continuity influence purchasing decisions.

Surgical Tourniquets Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the global value of devices used to temporarily restrict blood flow during limb procedures in an operating or procedural setting, where controlled pressure supports a clearer surgical field and a safer workflow.

Scope exclusions: This sizing does not count first-aid elastic tourniquets, hemostatic dressings, or veterinary-use tourniquets.

Segments Covered in This Report

- By Product Type

- Pneumatic Tourniquet Systems

- Intelligent LOP-controlled Systems

- Elastic / Silicone-ring Tourniquets

- Disposable / Sterile Cuffs

- Re-usable Cuffs

- Accessories

- By Application

- Lower-Limb Orthopedic Surgery

- Upper-Limb Orthopedic Surgery

- Trauma & Battlefield Stabilisation

- Other Surgical Specialities

- By End User

- Hospitals & Trauma Centres

- Ambulatory Surgery Centres

- Military / Defence Medical Units

- Other End Users (Sports clinics, EMS)

- By Technology

- Single-Channel (1-cuff) Consoles

- Multi-Channel (2-4 cuff) Consoles

- Integrated Pressure-Feedback Software

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to assemble the fact base around procedure volumes, device usage norms, and safety expectations that shape demand. We relied on public sources such as the US FDA databases and FDA safety communications, the US CDC where relevant for procedure setting context, and OECD health statistics to triangulate hospital activity signals across countries.

To avoid sizing on assumptions alone, we also reviewed clinical and practice context from peer-reviewed orthopedic and vascular surgery journals, along with perioperative care guidance from professional associations. For market structure and the supplier footprint, we checked annual reports, investor presentations, and reputable press coverage, and we supplemented financial context using paid subscriptions for company financials and news intelligence. Patent databases were also reviewed to confirm the direction of technology and device components. This list is not exhaustive, and many other public sources were referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how often tourniquets are used by procedure type, how purchasing decisions are handled in hospitals and ambulatory centers, and how pricing varies based on system configuration, cuff type, and the accessory mix. We conducted interviews with a balanced set of manufacturers, distributors, and clinical stakeholders across major regions, so gaps from desk research could be closed and key assumptions checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 43% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 21% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links limb surgery volumes and tourniquet adoption rates by care setting, and then converts that into system and cuff consumption using replacement cycles and typical cuffs-per-system usage. Where public data is thinner, assumptions are kept explicit and then stress-tested through primary feedback.

To keep totals realistic, results are corroborated with selective bottom-up checks, such as supplier revenue checkpoints, sampled average selling prices by product class, and channel discussions on the split between reusable systems and single-use cuffs. Key model inputs include orthopedic and trauma procedure counts, ambulatory surgery center utilization trends, reusable system installed base and service life, cuff and accessory replacement frequency, and observed price bands by region after currency normalization. For forecasting, scenario analysis is used around procedure growth and adoption, and the central case is tuned using expert consensus on how safety protocols and device mix are likely to evolve over the next few years.

Data Validation & Update Cycle

Outputs are checked against independent signals such as procedure growth, hospital procurement patterns, and observed pricing ranges, so the final numbers are not driven by a single indicator. Any sharp changes by region or product class are reviewed, and then re-checked with follow-up calls when variance cannot be explained by known shifts.

Before sign-off, the model and assumptions go through multi-step analyst reviews, with attention to unit consistency, currency timing, and year-to-year continuity. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory actions, meaningful pricing swings, or notable technology shifts. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Surgical Tourniquets Market Size Compared With Other Published Estimates

Published market sizes for surgical tourniquets can look far apart even when everyone is referring to the same clinical need, because the counted product set and the timing of the base year often differ. The split in scope also changes whether reusable systems are treated separately from recurring cuff and accessory demand, and whether ASP movement is assumed uniformly across regions.

The table reflects that variation in scope boundaries and year alignment, and in Mordor Intelligence's model the total is limited to surgical tourniquet systems plus dedicated cuffs and essential accessories used for limb surgery and trauma stabilization, with first-aid elastic bands and veterinary use excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 617.07 M (2026) | |

| Global Publisher A | USD 933.20 M (2026) | Uses a broader definition that can pull in adjacent tourniquet categories and a wider recurring-consumables basket, which raises the 2026 total even if procedure volumes are similar. |

| Global Publisher B | USD 593.07 M (2026) | Applies a narrower product and end-user cut, and tends to lean on conservative ASP progression in early forecast years, which keeps the 2026 value lower. |

Taken together, the comparison indicates that the biggest drivers are what gets counted as a surgical tourniquet product set and how pricing and replacement behavior are converted into yearly revenue. By keeping inputs tied to observable procedure activity and repeatable usage assumptions, we can explain the total in clear steps and make updates clean when new signals emerge.

Key Questions Answered in the Report

What is the current value of the surgical tourniquets market?

The surgical tourniquets market stands at USD 617.07 million as of 2026, with a forecast to reach USD 883.63 million by 2031.

Which product segment is growing the fastest?

Disposable sterile cuffs lead growth with an 8.51% CAGR through 2031, driven by infection-control requirements and single-use mandates.

Why are limb-occlusion-pressure (LOP) systems important?

LOP systems individualize inflation pressure, lowering average pressures to 152 mmHg and cutting nerve-injury claims, which reduces hospital liability and improves patient outcomes.

Which region will add the most new demand?

Asia-Pacific shows the highest CAGR at 9.43% thanks to large-scale hospital expansions and medical-tourism inflows, notably in India and ASEAN markets.

How are legal risks influencing equipment purchases?

Rising litigation over nerve damage compels hospitals to purchase consoles with automated pressure feedback and comprehensive data logging, shifting demand toward smart tourniquet technologies.

Page last updated on: