Total Wrist Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

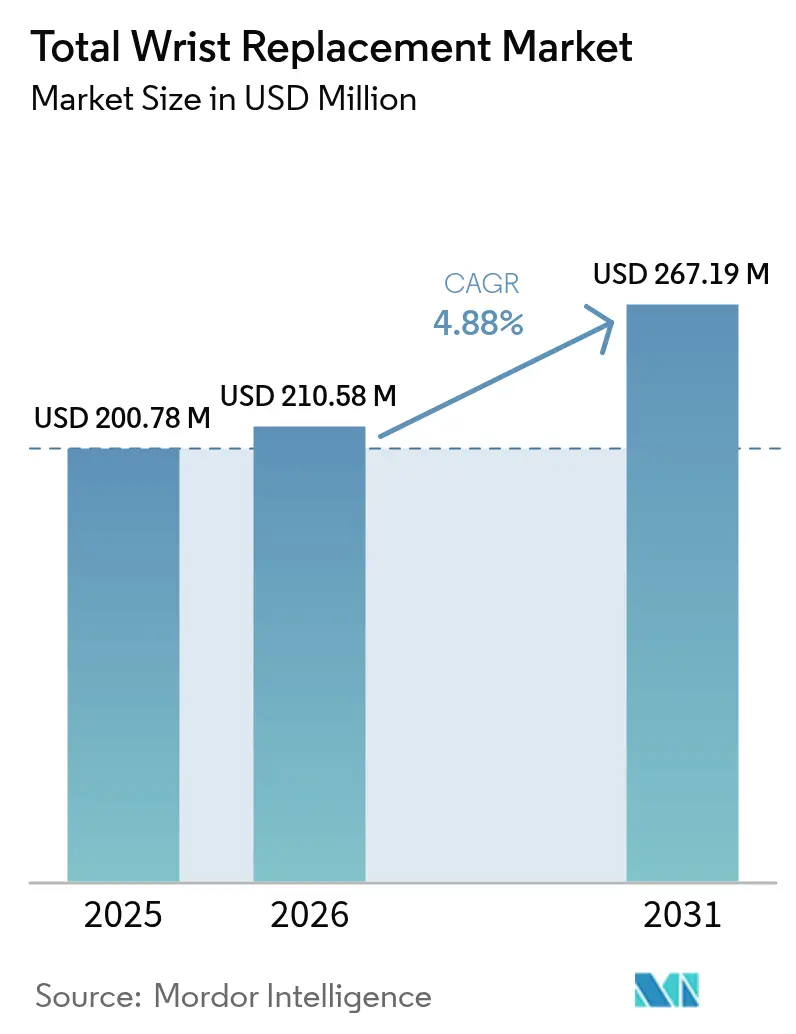

| Market Size (2026) | USD 210.58 Million |

| Market Size (2031) | USD 267.19 Million |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

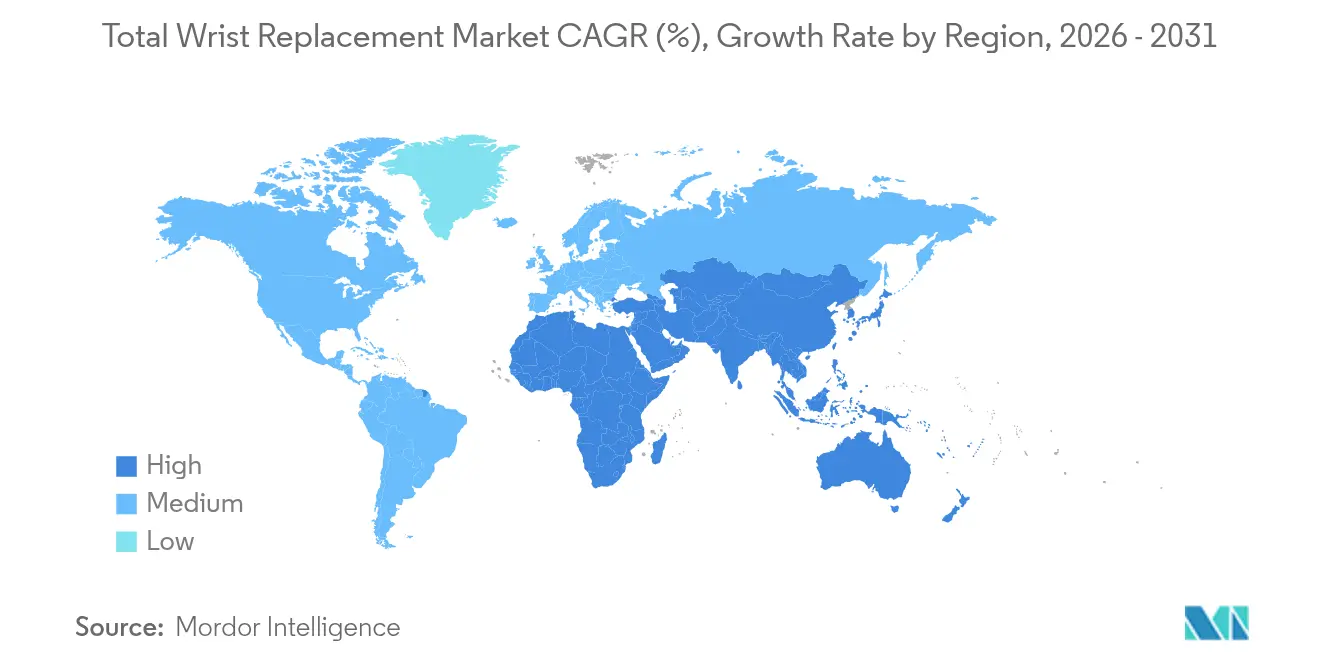

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Total Wrist Replacement Market Analysis by Mordor Intelligence

Total Wrist Replacement Market size in 2026 is estimated at USD 210.58 million, growing from 2025 value of USD 200.78 million with 2031 projections showing USD 267.19 million, growing at 4.88% CAGR over 2026-2031.

The transition from experimental procedures to routine motion-preserving solutions reflects fourth-generation implants that achieve more than 90% five-year survivorship, a performance level that encourages wider surgeon adoption while supporting patient demand for functional recovery over fusion solutions. Bundled payment models across major payers have already trimmed Medicare joint-replacement episode costs by 20.8%, creating cost visibility that favors outpatient pathways and drives procedure migration to ambulatory surgical centers. Material science also propels differentiation: cobalt-chromium alloys keep the lead through proven strength, yet ceramic components gain pace as surgeons look to minimize metal-ion release risks. Geographically, North America remains the revenue anchor, but rapid procedure uptake in China, Japan, and India positions Asia for the fastest expansion through 2030.

Key Report Takeaways

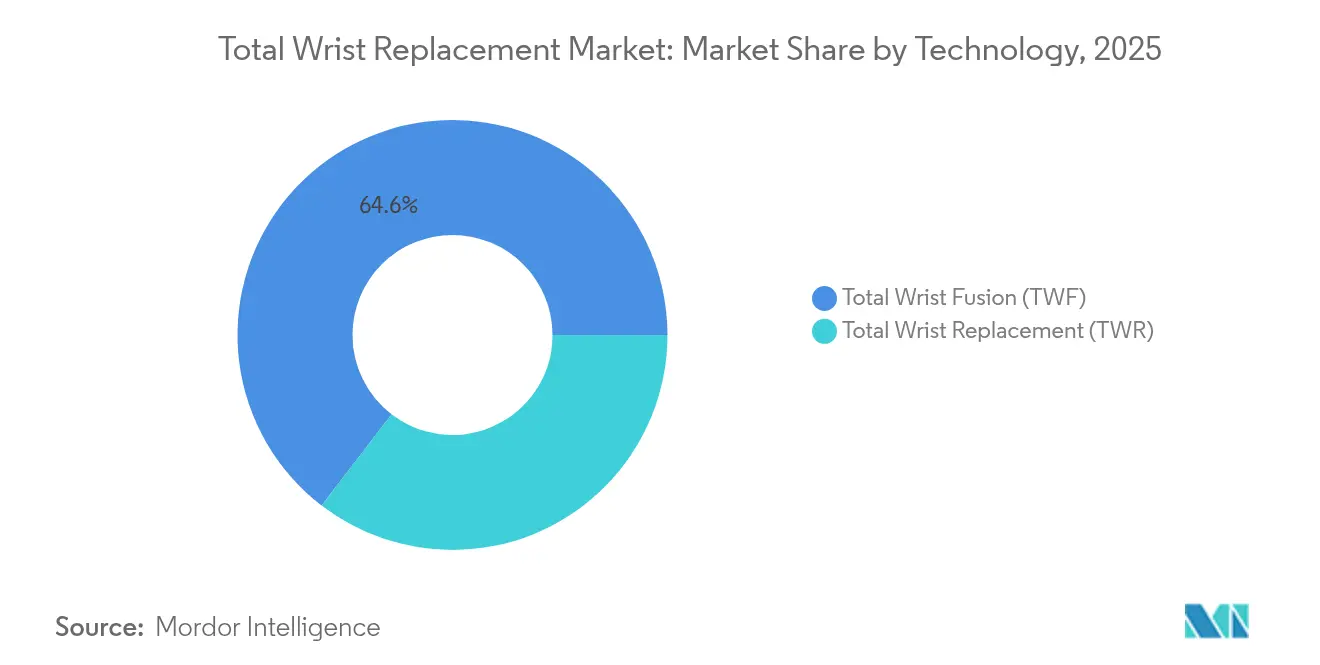

- By technology, total wrist fusion held 64.58% of the total wrist replacement market share in 2025, whereas total wrist replacement is set to climb at a 7.21% CAGR through 2031.

- By material, cobalt-chromium alloys captured 57.88% revenue in 2025, while ceramic-based components will expand at an 8.12% CAGR to 2031.

- By end user, hospitals accounted for 67.95% of the total wrist replacement market size in 2025; ambulatory surgical centers are forecast to grow at 9.68% CAGR up to 2031.

- By geography, North America dominated with 39.35% revenue in 2025, whereas Asia is projected to register the strongest 9.20% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Total Wrist Replacement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of rheumatoid & osteoarthritis | +1.2% | North America, Europe, high visibility in Asia-Pacific | Long term (≥ 4 years) |

| Advancements in 4th-generation modular implants | +0.9% | North America, Europe | Medium term (2-4 years) |

| Preference for motion-preserving procedures | +0.7% | North America, Europe, spillover into Asia-Pacific | Medium term (2-4 years) |

| Expansion of outpatient/ASC arthroplasty | +0.8% | North America, early adoption in Europe | Short term (≤ 2 years) |

| Emergence of 3-D-printed patient-specific devices | +0.6% | North America, Europe, pilot use in Asia | Long term (≥ 4 years) |

| Bundled-payment models rewarding outcomes | +0.5% | North America, selective uptake in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Rheumatoid & Osteoarthritis

Rheumatoid arthritis affects 2.5 million individuals in the United States, and wrist arthritis is present in 13.6% of the general population, expanding the clinical pool eligible for arthroplasty.[1]R. Berbrayer, “Epidemiology of Wrist Arthritis,” eMedicine, medscape.com Shifting demographics and sedentary work habits bring the earlier onset of pathology that pushes treatment demand among younger, economically active patients. Comparative studies confirm that arthroplasty delivers better functional results than arthrodesis in rheumatoid cohorts despite slightly different complication profiles, strengthening the procedure’s value proposition. Disease-modifying antirheumatic therapies now prolong joint integrity, yet prolonged survival raises the lifetime need for motion-preserving interventions. In practice, the Universal Total Wrist prosthesis improved Disabilities of the Arm, Shoulder and Hand (DASH) scores by 29% while cutting pain scores from 66.3 to 6.7, an outcome that resonates with patient-reported priorities.

Advancements in 4th-Generation Modular Implants

Fourth-generation systems provide four-year survival rates above 90%, dwarfing the 42% mid-term results seen in first-generation devices.[2]C. Tomori, “Advances in Modular Wrist Systems,” Current Orthopaedic Practice, journals.lww.com Modular trays let surgeons tailor component sizes intraoperatively, minimizing malalignment risk and enabling easier staged revisions. The Freedom prosthesis, for instance, receives patient satisfaction scores of 8.7/10, but radiographic lucency in one-third of implants underlines the need for annual surveillance. Enhanced kinematics via semi-constrained ellipsoidal joints distribute load more evenly across the radiocarpal interface. Titanium-nitride coatings on CoCrMo and Ti6Al4V alloys virtually eliminate detectable ion release, responding to long-term biocompatibility concerns

Preference for Motion-Preserving Procedures

Total wrist arthroplasty restores roughly 50% of physiologic motion, whereas fusion eliminates it entirely, a distinction that matters to patients engaged in fine-motor or athletic activities. Surveys indicate that 91% of revision arthroplasty recipients report no or mild pain, indicating a willingness to accept revision risk to preserve motion. Advancing simulation modules and e-learning streamline surgeon education, shortening the learning curve and widening access. Regionally, the Asia Pacific Wrist Association has become a conduit for cadaveric courses and technique workshops that accelerate adoption of arthroplasty across emerging markets. Shared decision-making platforms further amplify patient demand patterns that favor motion-preserving options.

Expansion of Outpatient/ASC Arthroplasty

Same-day discharge rates for elective total joint arthroplasty are climbing as multimodal pain pathways shrink length of stay and as payer policy changes roll out. Hand procedures performed in ASCs cost 25-30% less than hospital equivalents, yet maintain complication rates below 2.5%, satisfying value-based purchasing criteria. Medicare’s Comprehensive Care for Joint Replacement (CJR) model, covering 324 hospitals through 2024, directly incentivizes episode cost control and spurs site-of-service shifts. With 6,308 ASCs operating in 2023, mainly in dense urban centers, competitive forces now make high-acuity hand cases a strategic growth lane. Robotics and AI analytics further underpin precision and peri-operative monitoring, letting surgeons replicate inpatient standards in lower-cost venues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure & Device Cost / Limited Reimbursement | -0.8% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| High Revision & Complication Rates | -0.6% | Global, with regional variation in surgical expertise | Medium term (2-4 years) |

| Regulatory Caution After Device Withdrawals | -0.4% | North America & Europe, with spillover to global markets | Medium term (2-4 years) |

| Sparse Long-Term Evidence for Novel Biomaterials | -0.3% | Global, with emphasis on developed markets requiring evidence-based adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Cost / Limited Reimbursement

U.S. payers have yet to publish national coverage determinations for total wrist arthroplasty, obliging surgeons to secure prior authorization case by case. Several private insurers label the operation experimental outside rheumatoid indications, enforcing restrictive criteria that limit patient throughput. Device prices remain elevated relative to hip and knee counterparts because smaller volumes offer fewer economies of scale, while regulatory hurdles raise commercialization costs. Bundled payment contracts push providers toward lower implant expenditures unless superior outcomes justify premium components. In many emerging markets, state payers favor high-volume orthopedic interventions over niche wrist procedures, delaying reimbursement inclusion.

High Revision & Complication Rates

Five-year revision-free survival sits at 71%, dropping to 60% by 10 years, far below hip and knee benchmarks, deterring surgeons and payers alike.[3]N. Yoshida, “Revision Rates in Wrist Arthroplasty,” PubMed, pubmed.ncbi.nlm.nih.gov Complication profiles span loosening, dislocation, and infection; revision attempts carry 50% complication rates and 21.6% re-revision risk. Device withdrawals such as the Maestro system by Zimmer Biomet illustrate how liability exposure trims product offerings despite satisfactory mid-term survival data. Complex wrist anatomy, coupled with low procedure volumes, elongates the learning curve, elevating early failure rates in inexperienced hands. FDA recalls of oxidation-prone inserts further raise caution during purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fusion Dominance Amid Arthroplasty Innovation

Total Wrist Fusion represented 64.58% revenue in 2025, illustrating surgeon trust in reliable pain control and predictable union. In contrast, arthroplasty rises at a 7.21% CAGR as fourth-generation devices prove durable beyond the rheumatoid cohort and into osteoarthritis as well as post-traumatic indications, enlarging the candidate base. The 3D-printed microporous titanium prosthesis (3DMT-Wrist) lowered pain from 66.3 to 6.7 while tripling grip strength, reinforcing momentum behind motion-preserving platforms.

Clinical meta-analyses place arthroplasty complications at 19%, nearly matching the 17% rate seen in fusion among rheumatoid cases, eroding historical perceptions of high failure risk. Seven-year survival of 97% achieved by the Re-motion system underscores progress, though one-third of recipients still face secondary interventions. Artificial-intelligence guidance now offers millimeter-level accuracy on screw trajectory and component alignment, enhancing reproducibility. As evidence solidifies, the total wrist replacement market size for arthroplasty is set to expand faster than any other technology segment through 2031.

By Material: Ceramic Innovation Challenges Metal Dominance

Cobalt-chromium alloys captured 57.88% revenue in 2025 thanks to fatigue strength and decades of clinical familiarity. Ceramics, however, are climbing at an 8.12% CAGR because they curtail wear debris and remove metal-ion exposure, aligning with rising patient safety expectations. Titanium alloys, enhanced with atomic-layer TiO₂ coatings, resist fretting corrosion and extend service life.

Novel high-performance ceramics exhibit lower wear rates and improved osseointegration, supporting wider indication use. Ti-33Mo-0.2C alloys now reach ultimate tensile strength of 960 MPa without compromising biocompatibility. Additive manufacturing lets engineers produce trabecular-like scaffolds that encourage bone in-growth, translating dorsal plate technology from trauma to arthroplasty shells. Against this backdrop, the total wrist replacement market size for ceramics is positioned to carve out substantial incremental revenue despite today’s metal dominance.

By End User: Hospital Expertise Meets ASC Efficiency

Hospitals controlled 67.95% of 2025 revenue, reflecting the multi-disciplinary resources needed for complex wrist implantation and potential revision. Yet ambulatory surgical centers march forward at 9.68% CAGR as enhanced-recovery protocols improve pain control and anesthesia techniques, allowing safe same-day discharge for carefully selected cases. Hand surgery in ASCs costs 25-30% less than hospital surgery while posting sub-3% complication rates, answering payer imperatives for value.

Specialty orthopedic clinics occupy an agile middle ground, offering concentrated expertise without tertiary-hospital overhead. CMS value-based models drive volume from inpatient DRGs toward such outpatient settings, while robotics and imaging platforms deliver OR precision in compact footprints. Consequently, the total wrist replacement market share of hospitals is predicted to slip gradually as ASCs capture complex but protocolized cases over the forecast window.

Geography Analysis

North America maintains leadership with 39.35% revenue in 2025, supported by Medicare initiatives such as CJR that reduce average episode costs and create stable reimbursement for complex wrist implants. Consolidated centers of excellence draw volume nationally, while FDA 510(k) clarity lowers the hurdle for incremental implant upgrades. ASC expansion, driven by payer pressure, accelerates site-of-service conversions without diminishing patient safety metrics.

Asia-Pacific records the fastest 9.20% CAGR through 2031. China’s high procedure volume, together with local manufacturing capability, now positions domestic implants ahead of imported counterparts, dramatically tightening price-performance ratios. Knowledge-sharing through the Asia Pacific Wrist Association plus multinational fellowship exchanges quickly diffuse surgical best practices. Japan and India further elevate regional numbers thanks to national insurance expansion and private-sector hospital networks.

Europe posts moderate, steady growth. The market benefits from methodical adoption following rigorous registry feedback loops that benchmark survivorship and complication metrics. The completion of Enovis’s EUR 800 million purchase of LimaCorporate in 2024 brought additional 3D-printed expertise into continental portfolios, supporting take-up of trabecular titanium designs. Cross-border research consortia, combined with pan-EU medical-device directives, provide an integrated pathway for advanced implants while preserving patient safety obligations.

Competitive Landscape

Total wrist replacement competition remains moderately concentrated. Orthopedic multinationals leverage design, marketing, and distribution synergies from hip and knee lines to defend share in this smaller segment. Zimmer Biomet’s exit of the Maestro system despite 90–100% five-year survival rates highlights how liability and recall exposure temper new-product risk appetite. Market leaders increasingly differentiate via survivorship publications, surgeon training academies, and digital navigation tools that uplift technical accuracy.

Strategic consolidation is gathering pace. Enovis absorbed LimaCorporate for EUR 800 million in 2024 to create a USD 1 billion reconstruction unit with advanced 3D-printed trabecular titanium. AI-driven guidance systems embedded in leading platforms offer intra-operative feedback, reducing component malposition and potentially lowering early failure rate. Meanwhile, regional manufacturers in China and India secure local tenders by pairing lower cost with government-mandated localization targets.

White-space opportunities lie in patient-specific instrumentation, robotic enablers for limited surgical fields, and ultra-wear-resistant ceramics. Companies that prove durability and provide robust revision pathways while educating surgeons will extend their lead as procedure volumes climb in outpatient settings globally. The total wrist replacement market therefore rewards scale, clinical data transparency, and capability to engage expanding ASC networks.

Total Wrist Replacement Industry Leaders

Zimmer Biomet

Johnson and Johnson

Stryker Corporation

Smith & Nephew plc

Enovis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zimmer Biomet announced first quarter 2025 net sales of USD 1,909.1 million, representing a 1.1% increase, while updating full-year revenue guidance to reflect the acquisition of Paragon 28, focusing on foot and ankle orthopedic segments. The company showcased innovations at the AAOS annual meeting, including advancements in hip and knee products that may influence wrist replacement offerings.

- April 2025: Smith+Nephew reported Q1 2025 revenue of USD 1,407 million with 3.2% underlying revenue growth in Orthopaedics, highlighting strong performance in knee and hip implants and new product launches including innovations in surgical robotics and implant systems. The CATALYSTEM Primary Hip System and LEGION Medial Stabilized inserts received FDA clearance, indicating ongoing advancements in their product portfolio.

- February 2025: Zimmer Biomet reported fourth quarter net sales of USD 2.023 billion, a 4.3% increase, and announced an agreement to acquire Paragon 28, focusing on the foot and ankle orthopedic segment. The company received FDA approvals for various products, including the Oxford Cementless Partial Knee and the OsseoFit Stemless Shoulder System.

- January 2024: Enovis Corporation completed its acquisition of LimaCorporate S.p.A. for approximately EUR 800 million, enhancing its position in the global orthopedic reconstruction market and adding a portfolio of innovative surgical solutions, including 3D printed Trabecular Titanium implants.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we look at the total wrist replacement market as all surgical systems, implants, and related disposables designed to fully substitute the radiocarpal joint, restoring motion for severe arthritis or trauma. The definition limits measurement to first-time implant revenue that originates from original equipment makers and their authorized distributors across every major care setting worldwide.

Scope Exclusion: The study leaves out partial arthrodesis kits, external fixation hardware, and nonsurgical wrist therapies.

Segmentation Overview

- By Technology

- Total Wrist Replacement (TWR)

- Total Wrist Fusion (TWF)

- By Material

- Cobalt–Chromium Alloys

- Titanium Alloys

- Stainless Steel

- Ceramic-based Components

- Polymer Components

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Orthopedic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted interviews with orthopedic surgeons, procurement heads at public hospitals, and day surgery center managers across North America, Europe, and high-growth Asian nations. Their inputs refined adoption rates, average selling prices, typical revision intervals, and the pace at which wrist fusion is still preferred over total replacement.

Desk Research

Our analysts began with open datasets that track joint procedures and arthritis prevalence, such as the United States National Inpatient Sample, Eurostat hospital activity files, the Global Burden of Disease study, and device clearance notices from the FDA and EMA. Trade bodies like the American Academy of Orthopaedic Surgeons and Arthritis Foundation helped size candidate pools, while customs and shipment feeds from UN Comtrade revealed the cross-border flow of cobalt- and titanium-based implants. Financial clues from D&B Hoovers and short news bursts gathered through Dow Jones Factiva anchored revenue splits. This list is illustrative only, and many additional sources informed subsequent validation.

Market-Sizing & Forecasting

Top-down modeling starts with recorded wrist arthroplasty volumes that we reconstruct from procedure codes, prevalence cohorts, and treatment penetration, which are then multiplied by region-specific ASPs to arrive at 2025 revenue. Bottom-up checks roll up sampled manufacturer earnings and channel audits to tighten totals. Key variables include diagnosed rheumatoid and osteoarthritis counts, elective-surgery backlogs, reimbursement shifts, 3-D printed implant approvals, and median implant price erosion. A multivariate regression blended with ARIMA trend extension projects each driver to 2030, while scenario analysis gauges upside from faster outpatient migration. Data gaps in low-reporting countries are bridged through weighted proxies drawn from comparable care systems before final aggregation.

Data Validation & Update Cycle

We run variance scans that flag every five-percent swing, route anomalies through a two-analyst peer review, and re-contact field sources when triggers emerge. Reports refresh each year, with mid-cycle updates pushed after material regulatory or recall events, so clients always see the latest baseline.

Why Our Total Wrist Replacement Baseline Commands Reliability

Published estimates rarely match because firms pick different device mixes, procedure definitions, pricing corridors, and update rhythms. We acknowledge these moving pieces upfront to explain why numbers diverge.

Key gap drivers include whether fusion systems sit inside scope, how aggressively future ASP compression is assumed, the choice of 2023 versus 2025 as the base year, and the cadence at which currency translation is updated. We rely on the latest surgical volumes, whereas several peers still extrapolate older inpatient data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 200.78 million (2025) | Mordor Intelligence | - |

| USD 186.4 million (2023) | Global Consultancy A | Omits emerging Asia and uses outdated surgical counts |

| USD 183.85 million (2023) | Industry Research Journal B | Values reflect hospital procurement only, excluding ancillaries |

| USD 192.2 million (2024) | Regional Consultancy C | Blends wrist fusion with replacement and mixes spot exchange rates |

The comparison shows that when scope, currency, and data vintage are aligned, our 2025 baseline sits logically between earlier and broader estimates, giving decision-makers a balanced, fully traceable view they can trust.

Key Questions Answered in the Report

What is the current size of the total wrist replacement market?

The total wrist replacement market is valued at USD 210.58 million in 2026 and is forecast to reach USD 267.19 million by 2031.

Which technology segment is growing fastest?

Total wrist replacement procedures are advancing at a 7.21% CAGR, outpacing fusion despite the latter’s larger 2025 base.

Why are ceramic components gaining share?

Ceramics lower wear debris and eliminate metal-ion exposure, driving an 8.12% CAGR growth within the material segment.

Which region leads the market, and which grows fastest?

North America leads with 39.35% revenue, while Asia-Pacific is advancing at 9.20% CAGR through 2031.

How does outpatient migration influence the market?

Ambulatory surgical centers show 25-30% lower costs and <3% complication rates, supporting a 9.68% CAGR for procedures performed outside hospitals.

What are the main barriers to wider adoption?

High device costs, reimbursement hurdles, and a 71% five-year revision-free survival rate compared with hip and knee replacements remain primary challenges.

Page last updated on: