Tattoo Removal Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

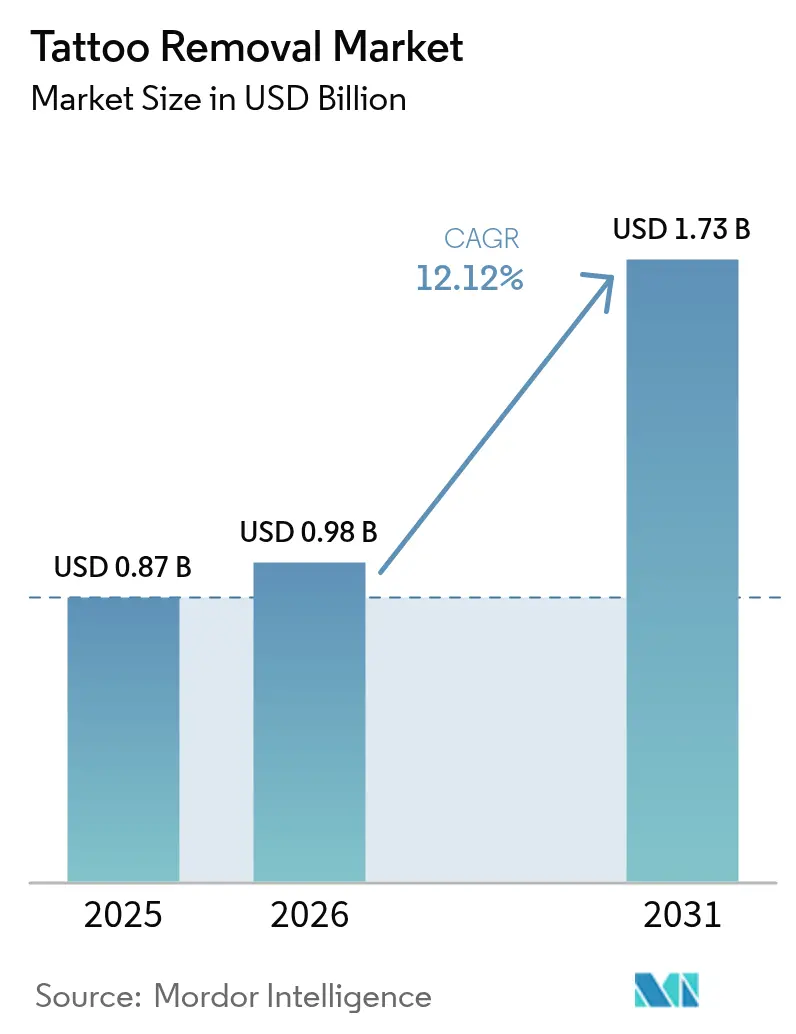

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

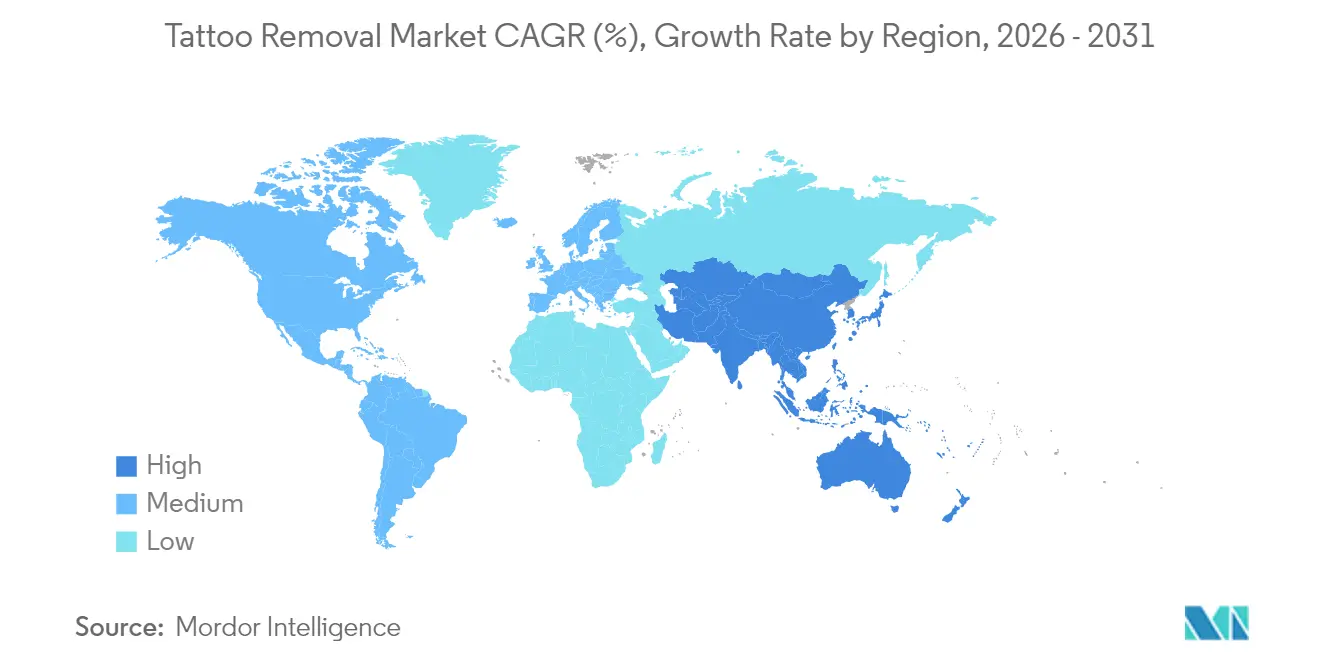

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tattoo Removal Market Analysis by Mordor Intelligence

The Tattoo Removal Market size was valued at USD 0.87 billion in 2025 and estimated to grow from USD 0.98 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 12.12% during the forecast period (2026-2031). This healthy rise mirrors a shift in consumer attitudes that now favor reversible body art, stricter workplace appearance rules, and steady gains in medical-aesthetic spending. Multi-wavelength picosecond lasers are reducing treatment times and enhancing clearance rates, while the government's efforts to restrict unsafe ink chemicals are prompting many consumers to opt for professional removal rather than at-home solutions. Clinic networks are proliferating across major cities, capitalizing on the growing disposable income of young adults who view skin “reset” procedures as an investment in employability and self-branding. At the same time, private-pay economics remain a barrier for some, keeping premium providers in a strong position.

Key Report Takeaways

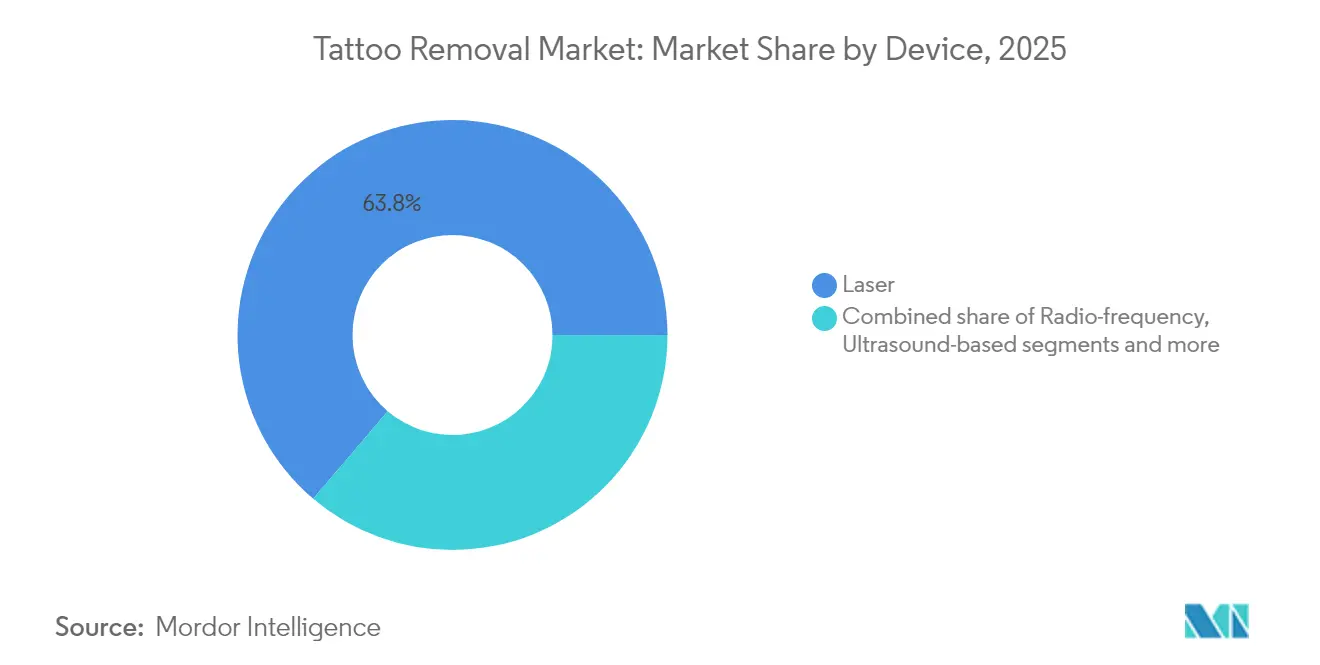

- By device, laser devices held 63.78% of tattoo removal market share in 2025; high-intensity focused ultrasound is projected to grow at a 13.34% CAGR to 2031.

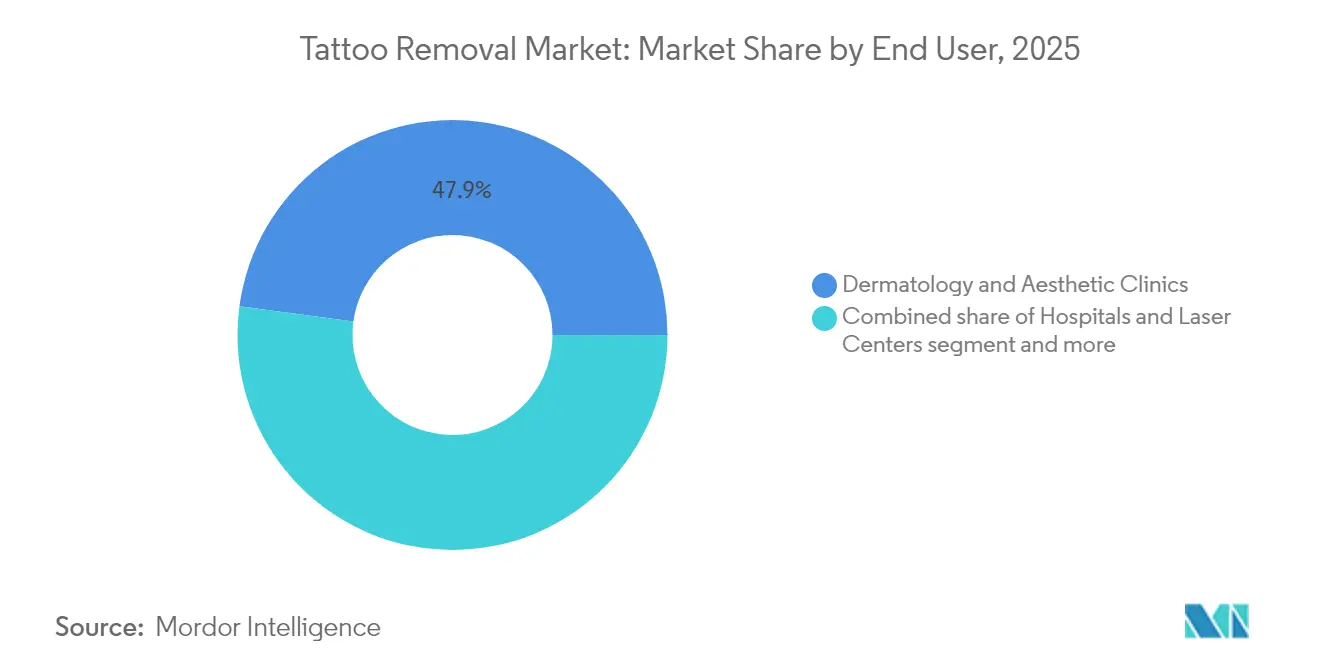

- By end user, dermatology and aesthetic clinics led with 47.86% revenue share in 2025, while medical spas are forecast to expand at a 13.85% CAGR through 2031.

- By geography, North America commanded 39.76% share of the tattoo removal market in 2025; Asia Pacific is anticipated to post the fastest 13.7% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tattoo Removal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of tattoo regret among millennials and Gen Z | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Shifting lifestyle aesthetics toward "clean-skin" look | +1.8% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Growing disposable income in emerging APAC economies | +2.3% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Continuous technological advancements in multi-wavelength laser platforms | +1.9% | Global | Short term (≤ 2 years) |

| Rapid expansion of dermatology and aesthetic clinic chains in urban centers | +2.0% | Global, with early gains in major metropolitan areas | Medium term (2-4 years) |

| Employment-screening policies refraining tattoos | +1.4% | North America & EU primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Tattoo Regret Among Millennials and Gen Z

One-quarter of tattooed adults report regret, and younger cohorts account for most removal inquiries, reinforcing a steady, demographically driven funnel for the tattoo removal market. Career shifts, identity evolution and greater buying power combine to turn removal into a planned life-cycle event rather than a last-minute remedy. Clinics note that women and recent graduates represent a sizable share of consultations, suggesting sustained demand as this cohort ages. This trend is amplified by social media influence and changing workplace expectations that make tattoo removal a strategic career investment rather than purely aesthetic choice.

Shifting Lifestyle Aesthetics Toward “Clean-Skin” Look

Minimalist beauty trends championed on Instagram and TikTok have redefined what “fresh” and “professional” appearance means across cultures. Dermatological surveys show 68% of removal patients cite “style evolution” over regret as the main trigger. In Asia Pacific, longstanding preferences for unmarked skin converge with Western “clean girl” sensibilities, generating a common aesthetic language that favors tattoo fading or complete erasure. Influencers regularly post before-and-after reels, demystifying downtime and normalizing multiple-session commitments. Clinics capitalize by packaging removal with skin-brightening regimens, positioning the service as part of a broader wellness journey instead of a corrective measure alone.

Growing Disposable Income in Emerging APAC Economies

Asia Pacific’s rising middle class is fuelling parallel surges in tattoo adoption and removal. Local clinics leverage competitive pricing and Western-style marketing to attract young professionals who can now afford multi-session packages. Spending on aesthetic services outpaces regional GDP growth, underscoring income elasticity for appearance-focused treatments. Rising disposable incomes in China, India, and Southeast Asia are coinciding with Western aesthetic influences that drive both tattoo adoption and subsequent removal decisions. The demographic dividend in these markets creates a large population of young professionals who view tattoo removal as a career advancement investment.

Continuous Technological Advancements in Multi-Wavelength Laser Platforms

Picosecond lasers deliver 74.3% complete clearance rates and cut sessions by nearly half compared with older Q-switched systems. New devices integrate up to four wavelengths, allowing operators to target stubborn blue-green inks safely and more profitably. R&D pipelines feature low-energy, high-frequency prototypes that promise shorter downtimes. These technological advances are creating competitive advantages for early adopters while driving down treatment costs through improved efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High overall treatment cost due to multi-session protocols | -1.7% | Global, particularly impactful in emerging markets | Medium term (2-4 years) |

| Post-procedure adverse events and scarring risk | -1.2% | Global | Short term (≤ 2 years) |

| Limited reimbursement coverage and absence of insurance support | -1.5% | North America & EU primarily | Long term (≥ 4 years) |

| Insufficient skilled laser operators in lower-income and rural regions | -0.9% | Global, concentrated in rural and developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Overall Treatment Cost Due to Multi-Session Protocols

Removal remains a premium out-of-pocket service. The American Society of Plastic Surgeons pegs average session fees at USD 697, and most patients need 5-8 visits for satisfactory clearance. Financing plans help, yet the cumulative burden restricts uptake among lower-income groups. Payment plan availability and package discounts are emerging as competitive differentiators, but the fundamental cost barrier limits market expansion to higher-income segments. The cost challenge is particularly acute for large or complex tattoos that may require 10-20 sessions, pushing total costs into luxury purchase territory that excludes broad market participation.

Limited Reimbursement Coverage and Absence of Insurance Support

Classified as elective, tattoo removal receives negligible insurer backing in major markets, keeping the tattoo removal market heavily private-pay. Without clinical evidence linking removal to health improvement, public programs are unlikely to shift coverage in the near term. The reimbursement limitation also prevents tattoo removal from being positioned as preventive care for employment or psychological well-being, constraining market expansion arguments. This restraint is likely to persist unless medical evidence emerges linking tattoo removal to measurable health or economic benefits that justify insurance coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: Laser Dominance Faces Ultrasound Disruption

Laser systems represented 63.78% of tattoo removal market revenue in 2025, validating decades of clinical use and multiple FDA clearances. The tattoo removal market size for laser platforms is projected to keep expanding, yet ultrasound devices are charting the fastest 13.34% CAGR as practitioners test non-thermal pigment fragmentation. Picosecond technology is resetting performance benchmarks, especially for multicolor artwork, which historically needed double-digit sessions. Manufacturers such as Cutera, Candela and Fotona have added multi-wavelength modes that address diverse ink profiles in fewer passes, enhancing clinic productivity. High-intensity focused ultrasound, though niche, appeals to darker skin phototypes that face higher post-inflammatory hyperpigmentation risk with thermal lasers. Radio-frequency combinations remain minor but attractive for clinics offering concurrent skin tightening.

Competitive dynamics inside the laser segment increasingly revolve around service contracts, software upgrades and consumable sales rather than hardware alone. Vendors supply clinics with training packages and marketing toolkits, fostering long-term loyalty and differentiating their offerings. Intellectual-property disputes over pulse-duration engineering continue, indicating a technology arms race not yet settled.

By End User: Medical Spas Challenge Clinical Dominance

Dermatology and aesthetic clinics controlled 47.86% of tattoo removal market revenue in 2025, reflecting clinician trust and advanced diagnostic skills. Yet medical spas are expanding at 13.85% CAGR, propelled by customer-centric environments and bundled cosmetic packages. The tattoo removal market size within medical spas is expected to widen as non-physician operators gain certification under supervised protocols. Chains leverage retail storefronts and social-media outreach to lower patient acquisition costs, chipping away at traditional clinic leadership.

Hospitals and laser centers still handle complex cases—large tattoos, immune-compromised patients or pigment-related complications—where medical risk profiles demand physician oversight. Niche operators offering mobile or pop-up removal services address convenience-oriented customers but face regulatory scrutiny regarding laser safety and waste disposal.

Geography Analysis

North America held 39.76% of tattoo removal market revenue in 2025, aided by a 32% adult tattoo prevalence in the United States and a well-developed aesthetic-device distribution network. Federal oversight provides predictable clearance pathways, giving consumers confidence in treatment safety. Financing programs that spread multi-session costs over 12-18 months also boost accessibility. Growth now tilts toward secondary cities where clinic density was previously sparse, although saturation in tier-one metros could slow regional CAGR.

Europe’s market benefits from robust consumer-safety regulations and high aesthetic spending. The European Directorate for the Quality of Medicines & HealthCare promotes stringent tattoo ink oversight,and a 2024 ban on 4,000 hazardous chemicals, including Blue 15 and Green 7 pigments, spurred many long-term wearers to schedule removals. Germany, France, the United Kingdom and Italy anchor demand, with Southern and Eastern markets showing catch-up potential as clinic infrastructure expands.

Asia Pacific is poised for the quickest 13.7% CAGR through 2031. Rising disposable income among China, India and Southeast Asia’s young urbanites fuels both tattoo adoption and subsequent removal. Competitive service pricing—far below North American levels—helps democratize access. Regulatory frameworks vary, but large private hospital groups and franchised med-spa chains are rolling out accredited laser suites, signalling a scale game similar to that seen in facial aesthetics. Australia, Japan and South Korea remain premium sub-markets favoring U.S.-made picosecond devices and shorter protocols.

Competitive Landscape

The tattoo removal market is moderately fragmented. Industry incumbents such as Cutera, Candela Medical, Fotona and Cynosure-Lutronic compete with emerging disruptors boasting energy-efficient platforms. Cutera’s Chapter 11 restructuring to trim USD 400 million in debt reflects rising R&D costs and pricing pressure.[3]Source: StockTitan, “Can Cutera's Chapter 11 Filing Transform USD 400M Debt Into a Fresh Start?” stocktitan.net Multi-wavelength versatility, software-driven parameter presets and after-sales training have become key differentiators.

Strategic alliances are on the rise. Device makers are partnering with clinic chains for revenue-sharing models that align hardware placement with patient volume growth. Alternative energy modalities are carving out white-space niches: academic spin-offs are commercializing ultra-low-energy pico pulses that promise shorter downtimes.

Barriers to entry include capital intensity, regulatory approvals and the need for certified operators. Nonetheless, private-equity capital keeps flowing into roll-ups of regional med-spa groups, signalling confidence in consolidated patient pipelines and cross-selling synergies. Premium-priced sessions, bundled treatment plans and adjunct skin-rejuvenation offerings sustain attractive margins despite rising competition.

Tattoo Removal Industry Leaders

Alma Lasers Ltd

Lumenis LTD

Cutera, Inc.

Hologic, Inc (CynoSure Inc)

Asclepion Laser Technologies Gmbh

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Hahn & Co. closed the merger of Cynosure with Lutronic, forming “Cynosure Lutronic” to accelerate global innovation.

- March 2024: Reveal Lasers launched Karma, a dual-wavelength 532/1064 nm Nd:YAG platform for tattoo removal and skin rejuvenation.

- January 2024: Quanta System introduced Discovery PICO with VarioPulse, delivering up to 1.8 GW peak power for multicolor clearance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global tattoo removal market as the total annual revenue earned by licensed hospitals, dermatology clinics, medical spas, and specialized laser centers from procedures that fully erase or partially lighten permanent decorative or cosmetic tattoos through laser, radio-frequency, ultrasound, surgical excision, or dermabrasion treatments.

Scope exclusions include revenues from home-use fading creams, DIY laser pens, temporary tattoos, and sales of capital equipment to providers, which sit outside this market.

Segmentation Overview

- By Device

- Laser

- Radio-frequency

- Ultrasound-based

- Other Devices

- By End User

- Hospitals and Laser Centers

- Dermatology and Aesthetic Clinics

- Medical Spas

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews were completed with dermatologists, medical-spa managers, laser-platform product specialists, and reimbursement advisors across North America, Europe, Asia-Pacific, and the Gulf. These discussions clarified typical session counts, emerging picosecond premium pricing, and regional acceptance barriers, enabling us to close data gaps and fine-tune model assumptions.

Desk Research

Analysts first gathered publicly available procedure and pricing data from tier-1 bodies such as the American Society for Dermatologic Surgery, United States FDA 510(k) laser approvals, Eurostat outpatient statistics, and Japan's MHLW medical service fee schedules. Trade-association papers from the International Aesthetic & Laser Association, peer-reviewed work in Lasers in Surgery and Medicine, and shipment records for Q-switched systems pulled from Volza helped size device installed bases and regional adoption curves. Financial snapshots on leading clinic chains were extracted through D&B Hoovers, while news archives on Dow Jones Factiva provided recent expansion moves. This list is illustrative; many other credible sources were consulted during evidence gathering.

Market-Sizing & Forecasting

A top-down prevalence model begins with adult tattoo incidence by country, layers the share expressing 'tattoo regret,' and multiplies by removal-seeking and treatment-completion rates to derive annual session volumes, which are then valued at blended average charges. Bottom-up cross-checks use sampled provider procedure logs, laser-room utilization surveys, and average selling price multiplied by unit volumes for key chains. Core variables include tattoo prevalence trends, regret sentiment, average sessions per removal, price per session trajectory, clinic density growth, and picosecond-laser penetration. Multivariate regression supported by ARIMA smoothing projects these drivers to 2030, with scenario analysis applied for economic downturn or rapid technology uptake. Data voids in immature markets are bridged by proximate country proxies that share tattoo culture and income bands.

Data Validation & Update Cycle

Outputs face three tiers of review: automated variance flags, senior-analyst peer checks, and research-manager sign-off. Anomalies versus external benchmarks trigger re-contact with interviewees. Mordor refreshes the model every year and issues interim revisions after material regulatory or technology events, ensuring users always receive the most current baseline.

Why Mordor's Tattoo Removal Market Baseline Stands Reliable

Published estimates diverge because firms mix devices with services, apply divergent price stacks, or freeze models for years.

By restricting scope to provider revenue streams and pairing the prevalence build-up with real-world price audits, Mordor delivers a figure that decision-makers can trace back to transparent levers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.87 billion (2025) | Mordor Intelligence | - |

| USD 1.29 billion (2025) | Regional Consultancy A | Combines after-care product sales and tele-consult packages, inflating totals |

| USD 4.34 billion (2021) | Global Consultancy B | Merges device revenues with procedure fees and uses older currency bases |

| USD 0.14 billion (2022) | Trade Journal C | Covers only hardware sales, omitting clinical service income |

The comparison shows that numbers swing wide when scope or base year drifts. Mordor's disciplined variable selection, annual refresh cadence, and dual-layer validation keep its tattoo removal baseline balanced, reproducible, and ready for confident strategic use.

Key Questions Answered in the Report

What is the current size of the tattoo removal market?

The tattoo removal market is valued at USD 0.98 billion in 2026 and is projected to reach USD 1.73 billion by 2031 at a 12.12% CAGR.

Which device technology leads the tattoo removal market?

Laser platforms dominate, holding 63.78% of 2025 revenue, although ultrasound systems are growing the fastest at a 13.34% CAGR.

Why is Asia Pacific the fastest-growing region?

Rising disposable income, dense urbanization and expanding clinic chains are driving a 13.7% CAGR in the region between 2026-2031.

How much does professional tattoo removal cost?

The American Society of Plastic Surgeons lists an average per-session fee of USD 697, with most patients needing 5-8 treatments.

Are tattoo removal procedures covered by insurance?

In most markets removal is deemed elective, so consumers typically pay out-of-pocket, though some clinics offer financing plans.

What are the main risks associated with tattoo removal?

Potential adverse events include scarring, pigment changes and incomplete clearance; proper device selection and trained operators mitigate most issues.

Page last updated on: