Carpal Tunnel Release Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

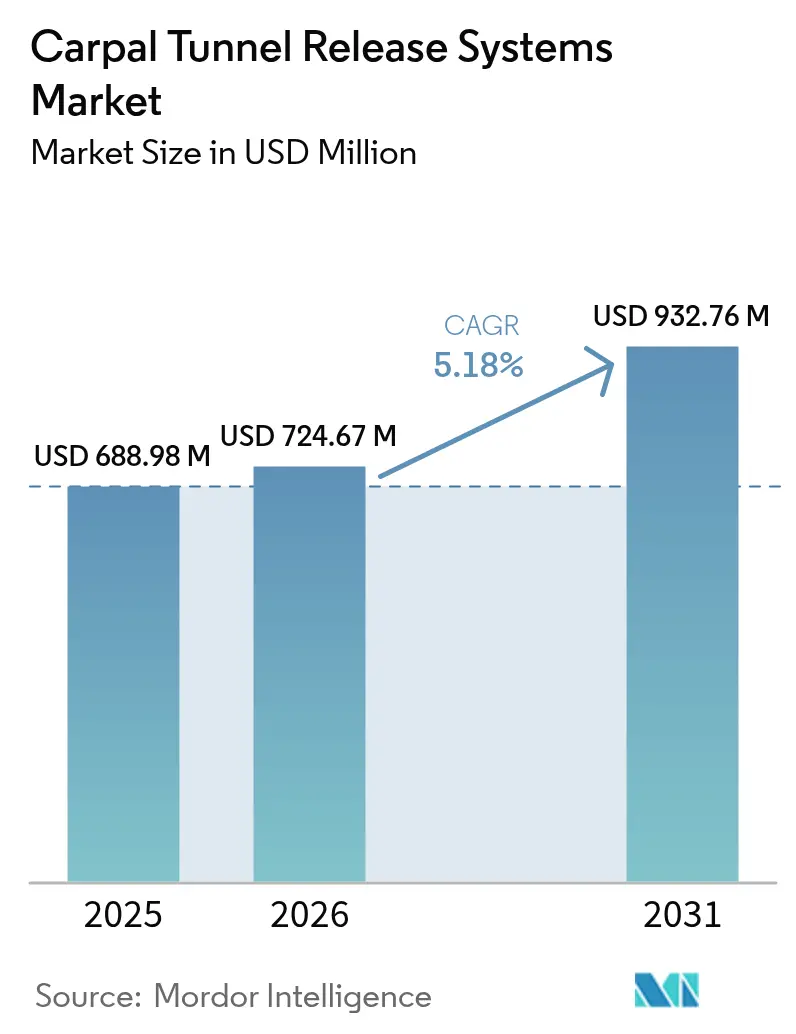

| Market Size (2026) | USD 724.67 Million |

| Market Size (2031) | USD 932.76 Million |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

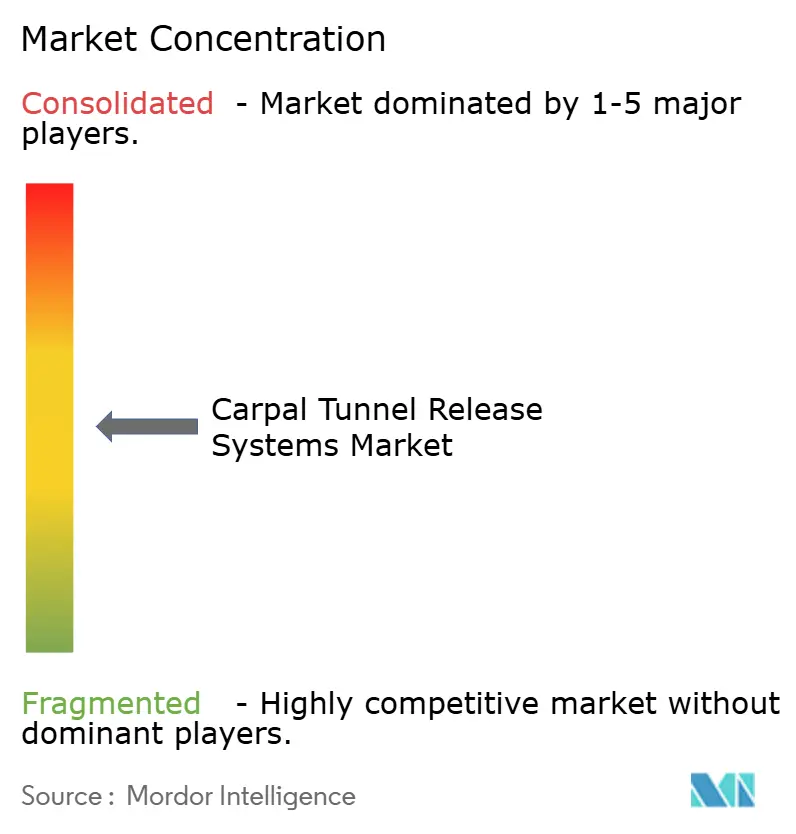

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carpal Tunnel Release Systems Market Analysis by Mordor Intelligence

The Carpal Tunnel Release Systems Market size was valued at USD 688.98 million in 2025 and is estimated to grow from USD 724.67 million in 2026 to reach USD 932.76 million by 2031, at a CAGR of 5.18% during the forecast period (2026-2031).

Rising median-nerve decompression demand from an aging workforce, growing surgeon preference for minimally invasive techniques, and payer support for ultrasound-guided approaches are the prime growth levers. Endoscopic solutions drive adoption by shortening recovery times. At the same time, office-based wide-awake surgery models cut facility fees and anesthesia costs by an estimated USD 750 million each year in the United States alone. Technological innovations, including AI-enabled nerve mapping, disposable optics, and single-use instrumentation, further strengthen the value proposition for outpatient settings. Regionally, North America leads due to robust reimbursement and specialist density. Yet, Asia-Pacific is set to outpace all other regions as healthcare access broadens and awareness of minimally invasive options rises.

Key Report Takeaways

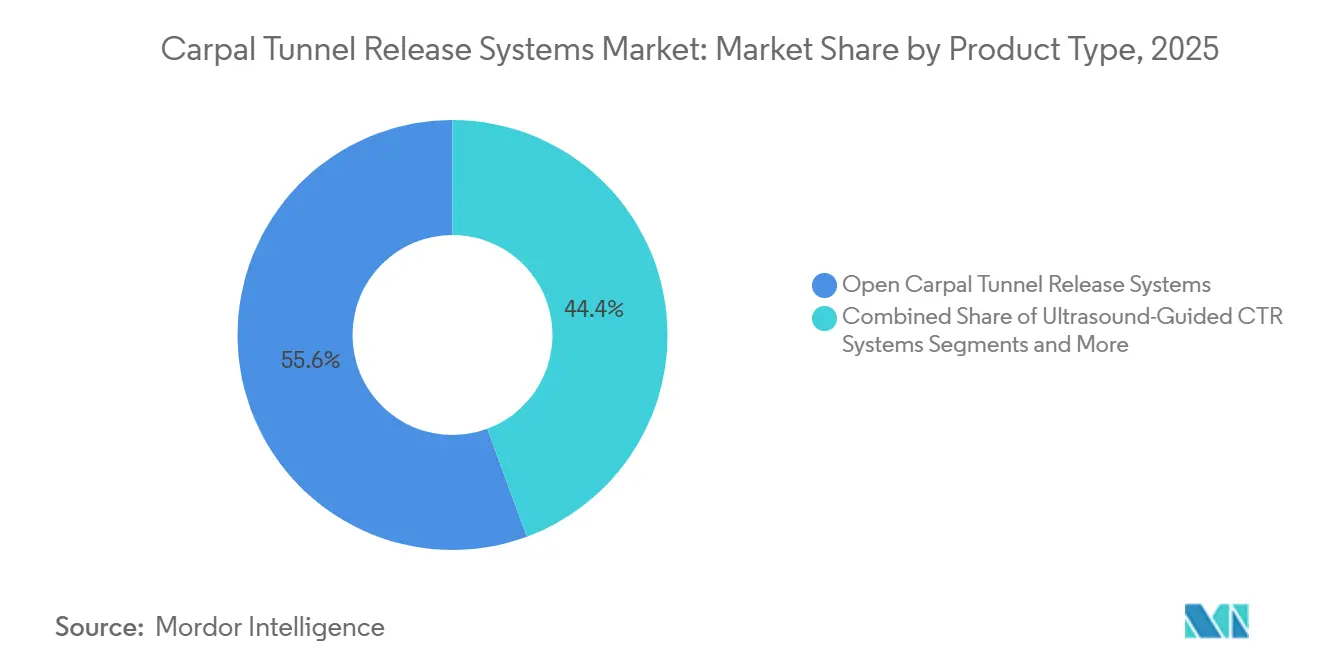

- By product type, endoscopic solutions accounted for 55.64% of the carpal tunnel release systems market share in 2025, while ultrasound-guided systems are forecast to accelerate at a 5.63% CAGR to 2031.

- By end user, hospitals accounted for 48.15% of the carpal tunnel release systems market in 2025, whereas ambulatory surgical centers are advancing at a 5.78% CAGR through 2031.

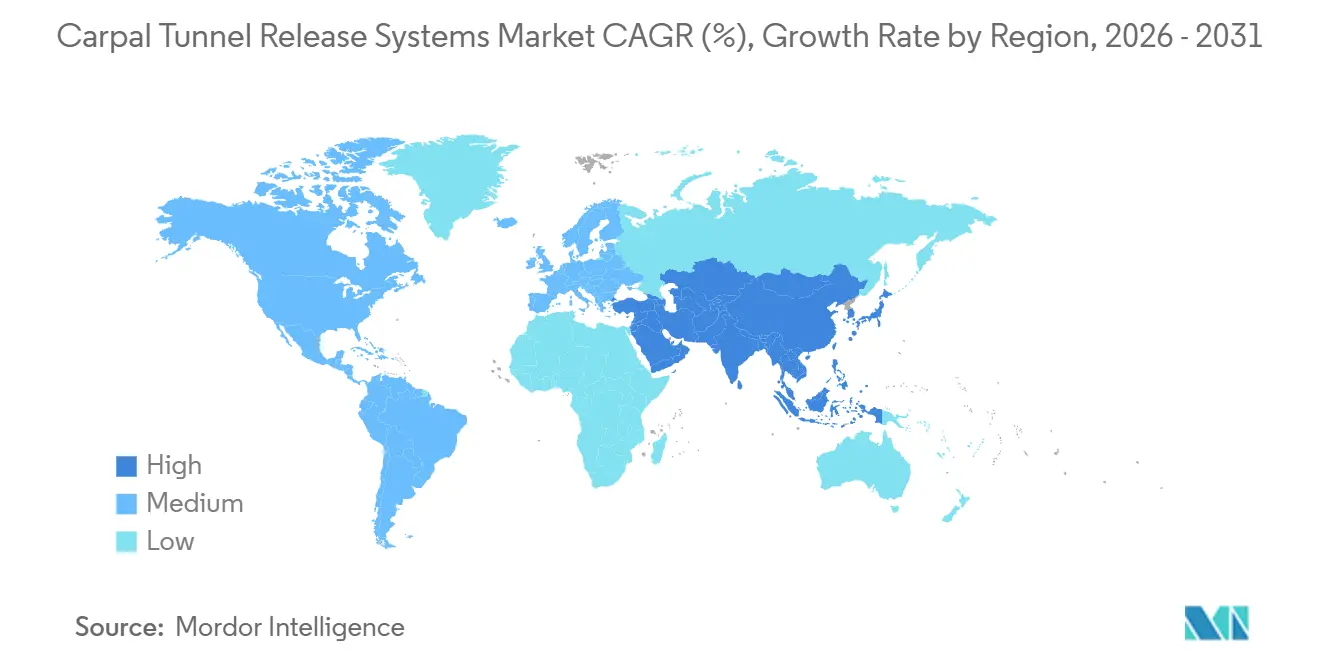

- By geography, North America led with 39.84% revenue share in 2025; Asia-Pacific is projected to rise at a 5.93% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carpal Tunnel Release Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging workforce driving CTS incidence | +1.2% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Shift to outpatient & office-based CTR | +1.0% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Reimbursement expansion for ultrasound CTR | +0.9% | United States, select EU markets | Short term (≤ 2 years) |

| Ai-enabled pre-operative nerve mapping | +0.6% | North America, academic EU and Asia-Pacific centers | Medium term (2-4 years) |

| Disposable single-use endoscopes | +0.7% | Global, early North America and Northern Europe | Medium term (2-4 years) |

| AI-powered ergonomic-injury prevention | +0.5% | North America, Western Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Workforce Driving CTS Incidence

Workers aged 45-60 experience the highest rates of carpal tunnel syndrome, a demographic fact closely tied to postponed retirement ages and more prolonged exposure to repetitive tasks. Tissue aging reduces tendon elasticity and increases vulnerability to median-nerve compression, making ergonomic programs insufficient for many patients. As 3.8% of the global population is affected, the persistent patient pipeline underpins robust procedure volumes and, by extension, sustained demand for the carpal tunnel release systems market. Developed economies remain epicenters because of their older labor forces, but industrializing Asian nations are quickly converging. Employers’ awareness of productivity losses fosters corporate adoption of early-intervention pathways, ensuring that surgical demand continues even with preventive measures in place.

Shift to Outpatient & Office-Based CTR Procedures

Endoscopic releases enable same-day discharge, with patients resuming light activities in a matter of days versus weeks for open surgery.[1]Source: MUSC Health Hand Center, “Treating Carpal Tunnel Syndrome Outside the OR,” muschealth.org Wide-awake local-anesthetic protocols further compress total procedure time, allowing more cases per surgical day and reducing costs for payers. This configuration unlocks revenue opportunities for ambulatory surgery centers and office suites that can market convenience alongside equivalent clinical outcomes. Such settings reinforce adoption of disposable kits that eliminate re-processing, thereby strengthening infection-control compliance while streamlining logistics.

Reimbursement Expansion for Ultrasound-Guided CTR

Following ECRI’s 2024 “Favorable” evidence rating, U.S. Medicare and multiple private insurers expanded coverage for ultrasound-guided releases. The multicenter ROBUST trial showed 94% patient satisfaction and a median two-day return to normal activities, providing the clinical footing for payers to justify procedural reimbursement.[2]BMC Musculoskeletal Disorders, “Carpal Tunnel Syndrome Incidence and Prevalence in Working-Age Populations,” bmcmusculoskeletdisord.biomedcentral.com Coverage variability remains, but positive cost-utility analyses accelerate alignment, particularly as outpatient settings document fewer resource inputs and comparable outcomes to standard endoscopy.

Surge in Ergonomic-Injury Prevention Programs

Corporate ergonomic strategies now integrate AI computer-vision tools that flag wrist-strain exposure in real time, enabling proactive rotation or tool redesign. These programs target reduced workers ' compensation claims, yet do not fully offset age-related degeneration, so surgical volume declines have not materialized. Instead, early identification funnels higher-risk employees to specialty clinics sooner, often shortening conservative-treatment phases and indirectly supporting the carpal tunnel release systems market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Post-operative pillar pain & litigation risk | –0.8% | Global, acute in U.S. litigation environment | Short term (≤ 2 years) |

| Shortage of hand surgeons in emerging economies | –0.6% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Capital-cost barrier for ultrasound systems | –0.5% | Emerging markets, small ASCs in developed economies | Medium term (2-4 years) |

| Supply-chain fragility in medical-grade optics | –0.4% | Global, with Asia-Pacific component bottlenecks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Operative Pillar Pain & Litigation Risk

Pillar pain occurs in 7-48% of release procedures and may linger up to a year, fueling dissatisfaction and malpractice exposure, especially in litigious regions. While endoscopic routes demonstrate somewhat lower incidence, they do not eliminate the syndrome. Preoperative sensory-profile assessments can stratify risk, yet add time and cost. Surgeons may hesitate to adopt new devices if perceived incremental benefits fail to outweigh legal hazards, temporarily dampening uptake.

Shortage of Hand Surgeons in Emerging Economies

Hand-surgery fellowships cluster in high-income countries, creating workforce gaps where demand is escalating fastest. Patients in rural Asia-Pacific often face month-long waitlists or must travel to tertiary centers, delaying intervention and permitting symptom progression. Scalability depends on training pipelines that include simulation-based curricula and tele-mentoring; lacking these, device sales remain constrained beyond major metropolitan hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ultrasound Guidance Redefines Adoption Curves

Endoscopic solutions captured 55.64% of the carpal tunnel release systems market share in 2025, underlining sustained surgeon preference for minimally invasive visualization with sub-15-mm incisions. The carpal tunnel release systems market for endoscopic devices is set to compound, thanks to the launch of disposable kits that eliminate sterilization overhead. Single-portal variants offer reduced learning curves, while two-portal systems deliver broader visual fields for complex ligament anatomy. Ultrasound-guided platforms, although representing a smaller absolute base, are logging the fastest CAGR at 5.63% because they enable proper office-suite procedures without general anesthesia. AI-assisted imaging overlays streamline ligament-division path planning, narrowing skill-gap barriers for early adopters. Open systems remain for revision cases complicated by adhesions, and mini-invasive knife-light kits offer hybrid cost-saving alternatives that combine tactile feedback with LED illumination.

In parallel, price competitiveness intensifies as manufacturers introduce tiered configurations ranging from reusable scopes for high-volume centers to single-use blades packaged for remote ambulatory sites. The United States, benefiting from insurers’ facility-fee incentives, is the principal source of revenue. Yet, growth hotspots are shifting to high-population countries such as India and China, where industrial job growth is accelerating CTS incidence. Product differentiation now emphasizes software upgrades as much as hardware refinements, underscoring an ecosystem view that links diagnostics, surgical guidance, and postoperative analytics into an integrated workflow.

By End User: Ambulatory Facilities Outpace Hospitals on Growth

Hospitals still comprise 48.15% of 2025 device purchases, mainly because complex or revision cases require full perioperative teams and overnight observation. The carpal tunnel release systems market size in acute-care settings will grow modestly as reimbursement shifts, capital budgets tighten, and technology migrates outward. In contrast, ambulatory surgical centers are driving momentum, expanding at a 5.78% CAGR as payers and patients favor lower out-of-pocket costs and the convenience of same-day discharge. Local anesthetic protocols underpin throughput: an ASC can complete four ultrasound-guided releases in the same time it takes to perform two open cases under general anesthesia.

Specialty clinics and office suites are carving out a share by focusing solely on upper-extremity disorders and often marketing transparent, all-inclusive package pricing. These environments gravitate toward single-use disposables that sidestep central-sterile bottlenecks. Furthermore, migration aligns with surgeons' lifestyle preferences, which favor predictable schedules over inpatient on-call rotations. Regulatory frameworks, notably the United States Food and Drug Administration’s 21 CFR 882.1320, provide device-filed pathways that accommodate diverse practice settings without demanding reclassification, thereby smoothing market transition.

Geography Analysis

North America generated 39.84% of total 2025 revenues, driven by comprehensive insurance coverage and a dense network of fellowship-trained hand surgeons. Its continued leadership is supported by early adoption of AI-enabled ultrasound systems and an ecosystem that rapidly validates real-world evidence through multicenter registries. Europe maintains steady uptake through public payer mechanisms and standardized clinical guidelines; however, state budget caps temper the penetration of premium-priced kits moderately.

Asia-Pacific, forecast to grow at a 5.93% CAGR, is the fastest-growing region as demographic aging converges with industrial workplace expansion. Government insurance expansions in South Korea and pilot device-rental programs in India reduce upfront costs for private clinics, further stimulating procedure volumes. Vietnam’s Ministry of Health approving MicroAire endoscopic units for national-level hospitals exemplifies regional policy endorsement. China’s urban-worker insurance pool now reimburses endoscopic procedures, prompting procurement by high-tier public hospitals and cascading procedural familiarity to county-level facilities.

Latin America exhibits mixed dynamics: Brazil’s supplemental insurance market funds minimally invasive releases, but device import duties slow broader adoption. The Middle East and Africa remain nascent; Gulf countries invest in tertiary orthopedic centers, whereas Sub-Saharan nations still rely on humanitarian missions for specialist surgeries. Manufacturers view these regions as long-tail opportunities necessitating hybrid sales models that blend capital-equipment leasing with surgeon-training scholarships.

Competitive Landscape

The carpal tunnel release systems industry displays moderate fragmentation: the key suppliers are Arthrex, Stryker, and CONMED anchor the scene with broad endoscopic portfolios complemented by surgeon-education platforms. Sonex Health differentiates itself through ultrasound-guided hand-piece innovation validated by independent ECRI review. MicroAire leverages agile scope designs attractive to resource-constrained hospitals, while AI-centric entrants offer SaaS decision-support overlays that ride atop existing imaging infrastructures.

Strategic plays revolve around disposables that assure every procedure yields incremental revenue versus semi-fixed capital amortization. Partnerships with ASC chains broaden distribution channels and facilitate on-site device trials that convert to multi-year supply contracts. Intellectual-property fences tighten as companies secure patents for sensor-based ligament-thickness mapping and haptic-feedback blade assemblies. M&A outlook centers on startups holding FDA 510(k) clearances for AI imaging modules, offering established players bolt-on capabilities to round out full-cycle solutions.

Carpal Tunnel Release Systems Industry Leaders

Arthrex, Inc.

MicroAire Surgical Instruments, LLC.

Trice Medical

Smith & Nephew plc

Integra LifeSciences Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: California Sports and Rehab addressed the growing demand for precise clinical diagnostics in Southern California. The practice emphasized its specialized infrastructure designed to deliver comprehensive diagnostic services for nerve and muscle dysfunctions, including carpal tunnel syndrome.

- August 2025: NanoScopic Release System received a Bronze Edison Award for its innovative compact endoscopic approach designed for use in standard ambulatory suites.

- February 2025: The U.S. Army Institute of Surgical Research and MIT Lincoln Laboratory introduced an AI-powered ultrasound nerve-block platform capable of autonomously identifying peripheral nerves during regional anesthesia.

Global Carpal Tunnel Release Systems Market Report Scope

As per the scope of the report, carpal tunnel release is a surgery used to treat and potentially heal the painful condition known as carpal tunnel syndrome. A proper diagnosis of carpal tunnel syndrome is the primary reason to have carpal tunnel surgery. Carpal tunnel release is generally an outpatient procedure, which means that one can go home the same day as the surgery if all goes well. There are two types of carpal tunnel release surgery, i.e., open and endoscopic.

The carpal tunnel release systems market is segmented by product type, end user, and geography. By product type, the market is segmented into open carpal tunnel release system and endoscopic carpal tunnel release system. By end user, the market is segmented into hospitals, ambulatory surgical centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Open Carpal Tunnel Release Systems |

| Endoscopic Carpal Tunnel Release Systems |

| Ultrasound-Guided CTR Systems |

| Mini-invasive Kit-based CTR Systems |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Open Carpal Tunnel Release Systems | |

| Endoscopic Carpal Tunnel Release Systems | ||

| Ultrasound-Guided CTR Systems | ||

| Mini-invasive Kit-based CTR Systems | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the carpal tunnel release systems market by 2031?

The market is forecast to reach USD 932.76 million by 2031, translating into a 5.18% CAGR from 2026.

Which product category is growing fastest?

Ultrasound-guided systems are expanding at a 5.63% CAGR, supported by payer coverage gains and office-based workflow advantages.

Why are ambulatory centers gaining share?

They eliminate hospital facility fees, enable wide-awake local-anesthetic protocols, and can save U.S. insurers USD 750 million annually.

How prevalent is post-operative pillar pain?

Between 7% and 48% of patients experience pillar pain, which can persist up to a year and is a key deterrent to certain techniques.

Which region offers the highest growth potential?

Asia-Pacific is the fastest-growing territory at a 5.93% CAGR, driven by aging demographics and expanding healthcare access.

How is AI transforming the field?

AI tools automate ultrasound diagnosis, map ligament-division paths, and predict pillar-pain risk, improving accuracy and reducing procedure time.

Page last updated on: