Tokenized Securities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

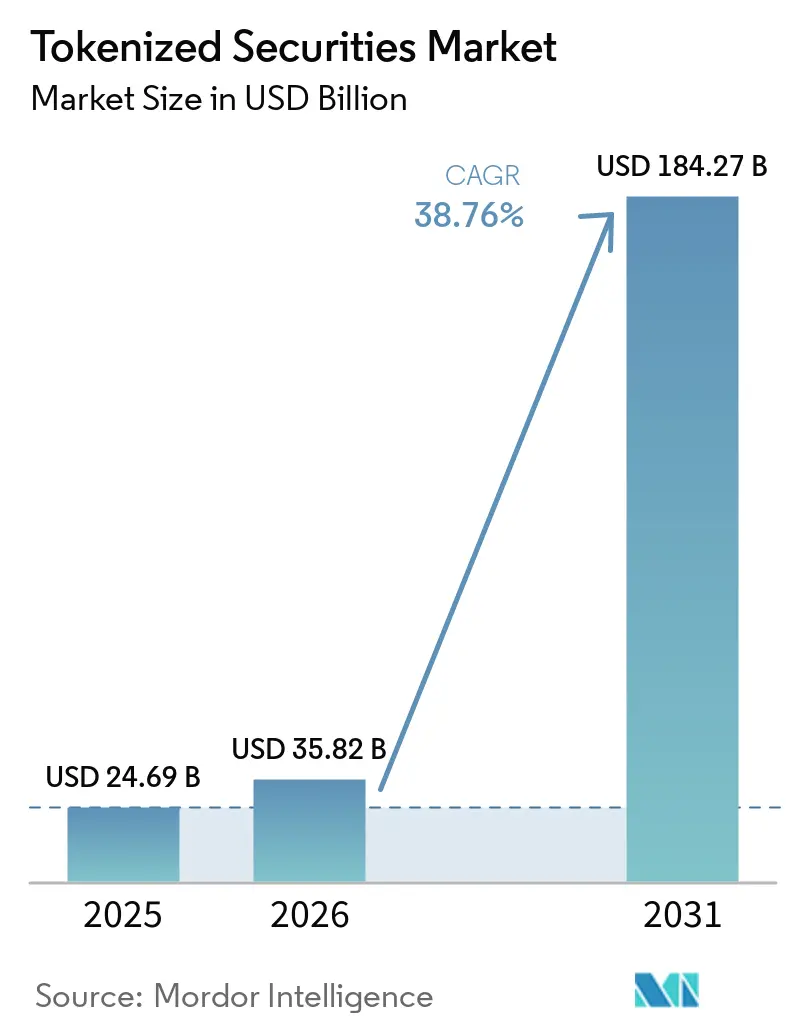

| Market Size (2026) | USD 35.82 Billion |

| Market Size (2031) | USD 184.27 Billion |

| Growth Rate (2026 - 2031) | 38.76% CAGR |

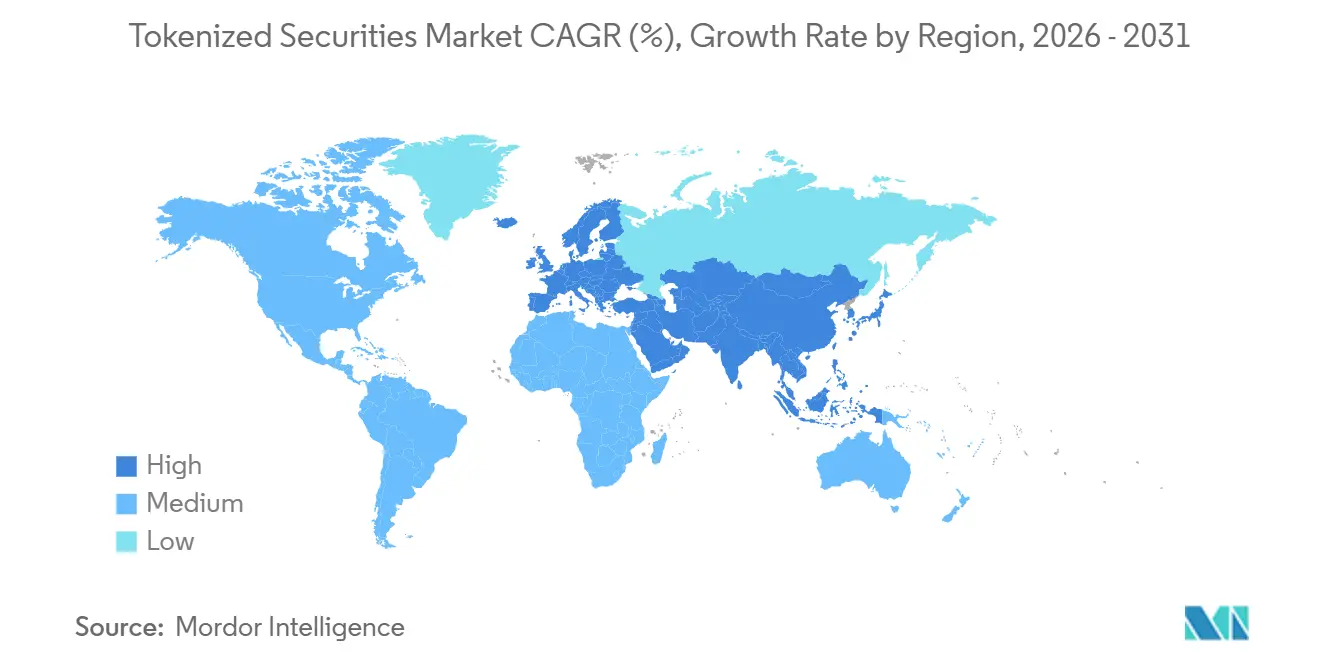

| Fastest Growing Market | Europe |

| Largest Market | North America |

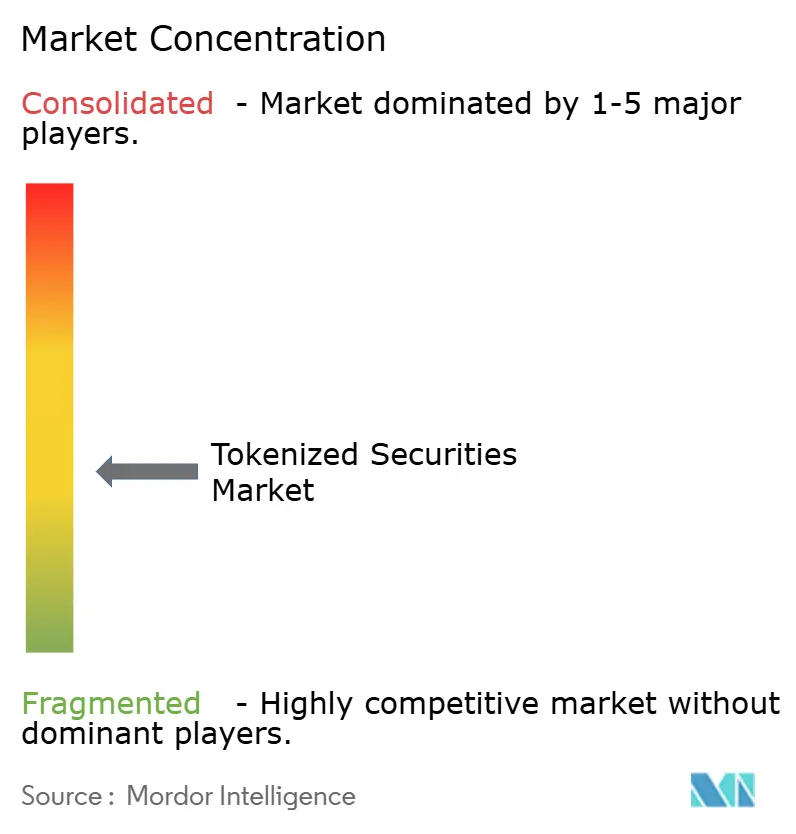

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tokenized Securities Market Analysis by Mordor Intelligence

The Tokenized Securities Market size is expected to increase from USD 24.69 billion in 2025 to USD 35.82 billion in 2026 and reach USD 184.27 billion by 2031, growing at a CAGR of 38.76% over 2026-2031.

The tokenized securities market is moving into a more formal stage of adoption because the March 2026 Securities and Exchange Commission and Commodity Futures Trading Commission interpretive release defined digital securities as the crypto-asset category that must comply with full United States securities law, which reduced a major legal barrier for institutional programs. The December 2025 authorization for DTCC to tokenize Russell 1000 constituents, select ETFs, and United States Treasuries under a 3-year pilot, followed by planned live trading in 2026, provides the tokenized securities market with a practical route from legal clarity to large-scale infrastructure deployment. Growth also reflects a shift in use cases, because institutions are no longer viewing tokenization only as a new issuance format and are increasingly using it for collateral mobility, cash management, and settlement efficiency across regulated products. Europe is also adding momentum through tokenization frameworks in the United Kingdom and wider wholesale market reforms, which broaden the opportunity set for issuers and service providers in the tokenized securities market. The main limits remain cross-border regulatory mismatch, operational vulnerabilities in smart contracts and oracle design, and thin liquidity outside the largest products, so market expansion will depend on stronger interoperability and clearer legal ownership standards

Key Report Takeaways

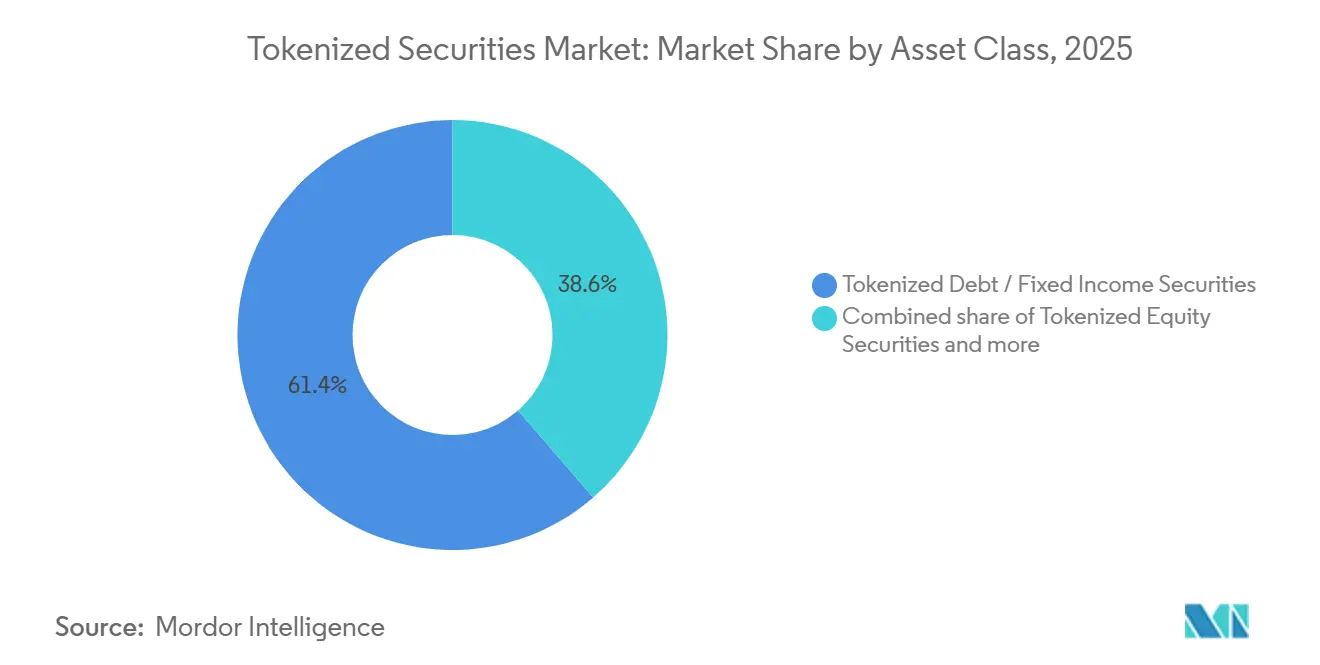

- By asset class, debt and fixed income captured 61.36% of the tokenized securities market share in 2025, while equity securities are projected to grow at 46.21% CAGR through 2031.

- By investor type, institutional investors held 91.48% of the tokenized securities market share in 2025, while retail investors are forecast to expand at a 48.72% CAGR through 2031.

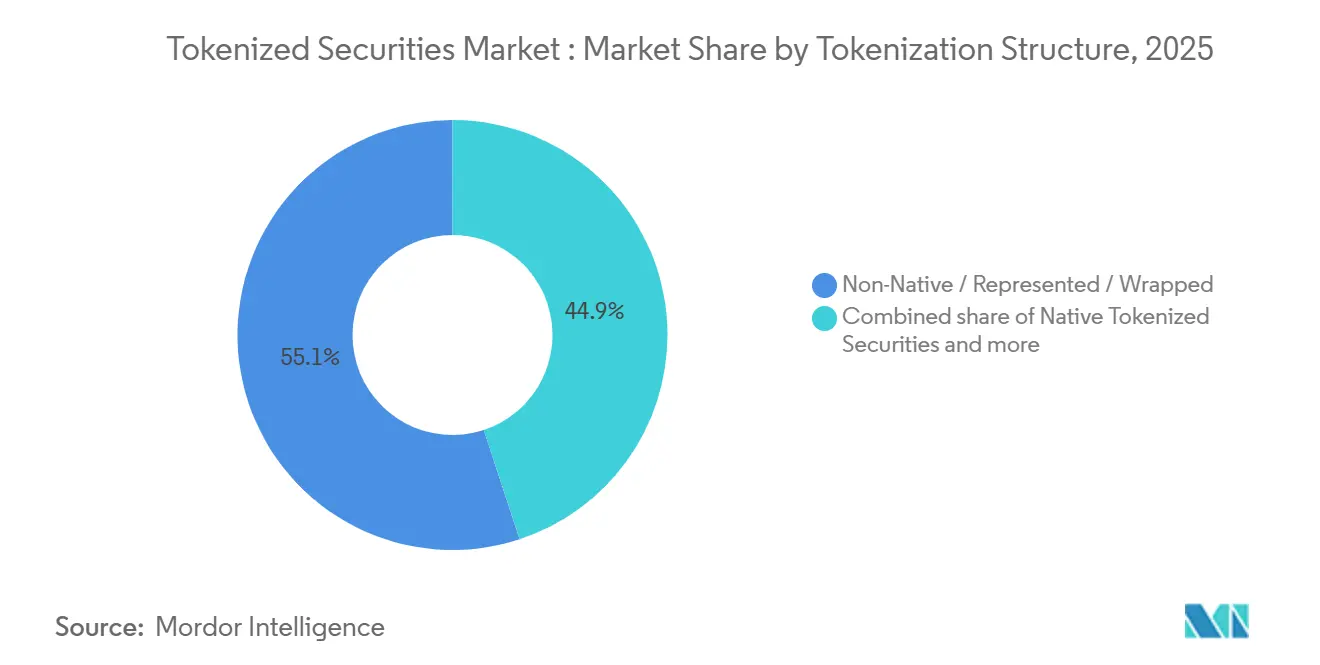

- By tokenization structure, non-native, represented, and wrapped formats accounted for 55.07% of the tokenized securities market size in 2025, while native tokenized securities are projected to grow at 43.67% CAGR through 2031.

- By issuer type, traditional financial institutions held 68.44% of the tokenized securities market share in 2025, while crypto-native and specialized tokenization platforms are forecast to record the highest CAGR of 45.83% through 2031.

- By geography, North America captured 67.34% of the tokenized securities market share in 2025, while Europe is projected to grow at 44.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tokenized Securities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Clarity in Major Financial Centers | +7.2% | North America, Europe, Singapore | Short term (≤ 2 years) |

| Rising Institutional Allocation to Tokenized Funds and Public Securities | +8.1% | Global | Short term (≤ 2 years) |

| Demand for Fractional Access to Premium Securities and Funds | +4.5% | Global, early gains in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments | +6.4% | North America, Europe | Short term (≤ 2 years) |

| Infrastructure Convergence Between Market Utilities, Banks, and Digital Asset Platforms | +5.2% | North America, Europe, Singapore | Medium term (2-4 years) |

| 24/7 Secondary Market Demand from Digitally Native Investors | +3.8% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Clarity in Major Financial Centers

The March 2026 SEC and CFTC interpretive release resolved a central legal uncertainty in the tokenized securities market by defining digital securities as the crypto-asset category subject to full United States securities law obligations. One day later, the SEC approved Nasdaq to trade tokenized and traditional shares on unified order books with identical execution priority, signaling that on-chain and off-chain securities can be treated with functional parity within regulated exchange infrastructure. In Singapore, the revised Guide on the Tokenization of Capital Markets Products raised securities compliance expectations across issuance, trading, custody, and settlement, thereby strengthening the operating framework for institutions seeking end-to-end compliance clarity[1]Monetary Authority of Singapore, “Guide on the Tokenization of Capital Markets Products,” mas.gov.sg. Taken together, these actions narrow the old cost advantage of loosely regulated offshore venues because major financial centers now offer clearer rules and more credible operating conditions. That shift is accelerating internal approval cycles across banks, asset managers, and long-term institutional allocators in the tokenized securities market.

Rising Institutional Allocation to Tokenized Funds and Public Securities

Institutional participation in the tokenized securities market is rising because large firms are now launching regulated products rather than limiting activity to pilots. J.P. Morgan Asset Management launched MONY in December 2025 as its first tokenized money market fund, and it followed that with JLTXX in 2026, which broadened the range of tokenized liquidity products available to qualified investors[2]J.P. Morgan Asset Management, “J.P. Morgan Asset Management Launches Its First Tokenized Money Market Fund,” am.jpmorgan.com. Goldman Sachs and BNY also launched a tokenized money market fund solution in July 2025, demonstrating that large financial institutions are treating tokenized fund shares as usable capital-market infrastructure rather than as experimental wrappers. The demand driver is not only about product access; institutions also want tokenized securities that can move more efficiently through collateral, treasury, and settlement workflows. As a result, the tokenized securities market is drawing capital from operating functions that sit outside traditional portfolio allocation buckets.

Demand for Fractional Access to Premium Securities and Funds

Fractional access is expanding the addressable base of the tokenized securities market by lowering the practical entry point for investors who previously could not access premium securities and funds through conventional channels. Binance announced United States stock trading in 2026 with fractional access from USD 5 and introduced bStocks tokenized securities through an ADGM-registered SPV, demonstrating how consumer-facing distribution can expand access to regulated economic exposure[3]Binance, “Binance Launches US Stocks Trading and Previews bStocks Tokenized Securities,” prnewswire.com . This trend matters beyond retail because smaller family offices and treasuries can also benefit when products are distributed in smaller ticket sizes and through digital rails. It also pressures older distribution models, since a tokenized product can reduce dependence on multiple intermediaries in administration, transfer, and clearing. Over time, that shift can support broader participation in the tokenized securities market if investor protection and eligibility controls keep pace with access expansion.

Growing Use of Tokenized Treasuries as Collateral and Cash Management Instruments

The tokenized securities market is gaining support from a core use case in institutional finance: the use of tokenized Treasuries and fund shares as collateral and for cash management. GFMA reported that JPMorgan's Kinexys platform had processed more than USD 1.5 trillion in intraday repo transactions since inception and was averaging USD 2 billion per day, indicating that blockchain-based workflows are already operating at meaningful capital markets volume. Goldman Sachs and BNY designed their tokenized money market fund solution so that digital ownership records could support collateral use, thereby moving tokenization from investment exposure to treasury efficiency[4]Goldman Sachs, “BNY and Goldman Sachs Launch Tokenized Money Market Funds Solution,” goldmansachs.com. This matters because collateral mobility is often more valuable to institutions than a small improvement in portfolio yield. As that utility spreads, the tokenized securities market becomes more embedded in repo, margin, and liquidity operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Fragmentation Across Jurisdictions | -3.2% | Global, especially cross-border EU-United States and Asia-Pacific flows | Medium term (2-4 years) |

| Smart-Contract, Oracle, and Custody Risk | -2.1% | Global | Short term (≤ 2 years) |

| Limited Standardization of Legal Ownership and Transfer Rights | -2.0% | Cross-border markets, Asia-Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Thin Liquidity Outside a Few Flagship Products | -1.8% | All regions outside North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Across Jurisdictions

The tokenized securities market still faces a major cross-border limit because regulatory frameworks are becoming clearer within jurisdictions faster than they are becoming compatible across jurisdictions. The OECD noted in January 2025 that differing legal treatments across markets threaten settlement finality and can trap liquidity within national or regional silos, thereby directly weakening one of the main efficiency claims behind tokenization. MAS also clarified in June 2025 that digital token service providers would face a stricter licensing bar under the next phase of Singapore's regime, which shows that compliance thresholds can rise sharply even in innovation-friendly centers. The practical result is that firms often need separate legal entities, licensing structures, and control frameworks to distribute similar products into different regions. That raises cost, slows rollout, and limits how quickly the tokenized securities market can scale across borders.

Smart-Contract, Oracle, and Custody Risk

Operational risk remains a real restraint because tokenized securities depend on smart contracts, pricing inputs, and custody controls that must all work correctly under stress. OWASP identified Oracle manipulation as one of the top vulnerabilities in its 2025 smart contract risk framework, highlighting the danger of single-source pricing feeds in products that depend on automated valuation or collateral actions. The Securities and Exchange Commission's (SEC) November 2025 technical framework for tokenized collateral required at least 3 independent oracle feeds, median aggregation, cryptographic attestation, and failover mechanisms, which shows that regulators already treat oracle design as a core control issue rather than a technical detail. Custody risk adds another layer, because key management, recovery design, and operational segregation must all withstand disruption at an institutional scale. Until these controls are tested across more live products, risk committees will continue to treat parts of the tokenized securities market with caution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Fixed Income Anchors the Market, Equities Define the Next Wave

Debt and fixed income accounted for 61.36% of the tokenized securities market in 2025, making it the leading asset class by a wide margin. This segment gained scale first because short-duration Treasuries and money market instruments are easier to value, regulate, and position as collateral-grade assets within institutional workflows. The DTCC pilot authorized in late 2025 includes United States Treasuries and major ETFs, which reinforces the role of fixed income as the operational bridge between existing post-trade systems and tokenized issuance models. Product launches from J.P. Morgan Asset Management, Goldman Sachs, and BNY also support this pattern, as tokenized money-market and Treasury-linked structures are already being used to improve liquidity management and settlement flexibility. In practice, fixed income remains the anchor of the tokenized securities industry because it offers the clearest path from proof of concept into repeat institutional use.

Equity securities are the fastest-growing asset class, and the tokenized securities market size for this segment is projected to expand at 46.21% CAGR through 2031. Growth is accelerating because the required infrastructure for order-book integration, shareholder communications, and corporate action handling is now becoming more credible at a regulated scale. The SEC approval that allows Nasdaq to trade tokenized and traditional shares on a unified order book is a major step because it creates a template for listed equity tokenization within a familiar exchange environment. Proxy voting support is also improving, as shown by Ondo Finance's integration with Broadridge for more than 250 tokenized stocks and ETFs, which addresses one of the practical gaps that had slowed equity adoption. Fund shares and collective investment products also benefit from this infrastructure buildout. In contrast, other tokenized securities, such as private credit and real-asset-linked products, are likely to grow more gradually until secondary trading and legal transfer standards improve.

By Investor Type: Institutional Capital Dominates, Retail Rails Now Opening

Institutional investors held 91.48% of the tokenized securities market in 2025, underscoring the concentration of early demand among qualified and regulated participants. The product structure of the tokenized securities market still reflects that base, because many offerings require KYC and AML screening, wallet allowlisting, and ongoing compliance checks before investors can subscribe or transfer holdings. J.P. Morgan Asset Management's MONY and JLTXX are clear examples, as both products sit within controlled distribution and reporting environments aimed at serious liquidity management use cases rather than open retail access. Institutional dominance also persists because legal ownership clarity, collateral eligibility, and operational continuity matter more to large allocators than novelty. For now, the tokenized securities industry remains led by institutions that can absorb compliance complexity and demand robust operational controls.

Retail investors are the fastest-growing investor group, and their participation in the tokenized securities market is forecast to rise at 48.72% CAGR through 2031. This shift is being supported by consumer-facing platforms that are opening fractional exposure to public securities and funds through wallet-based or app-based channels. Binance's 2026 launch of fractional United States stock access at USD 5 and its planned bStocks structure illustrate how retail distribution is moving from concept to live product design. Retail expansion also increases the operating burden on issuers and platforms, as investor communication, suitability reviews, and identity verification must scale across a much larger user base. As that user base grows, the tokenized securities market will need stronger rules around disclosures, trading windows, dispute resolution, and treatment of corporate actions for non-institutional holders.

By Tokenization Structure: Wrapped Formats Lead, Native Architecture Gains Ground

Non-native, represented, and wrapped structures accounted for 55.07% of the tokenized securities market in 2026, which makes the digital twin model the current operating standard. This model remains attractive because it can fit into existing custody and settlement arrangements with less legal disruption than a fully native issuance model. The tradeoff is that it adds another intermediary layer between the holder and the underlying security, which can create insolvency and recourse questions if the tokenization platform or custodian fails. The SEC highlighted this concern in January 2026, warning that third-party tokenization models may not always grant token holders direct rights against the original issuer. Even with that risk, wrapped formats continue to lead the tokenized securities market because they offer the fastest route into regulated deployment without requiring legal systems to change all at once.

Native tokenized securities are the fastest-growing structure, projected to grow at a 43.67% CAGR through 2031. Their appeal lies in the fact that ownership records, transfer logic, and lifecycle events can be embedded directly into the distributed ledger infrastructure rather than layered on top of legacy registers after the fact. DTCC's planned commercial launch in October 2026 is important because it points toward a model in which DTC-custodied assets can be tokenized while preserving traditional investor safeguards, thereby narrowing the gap between native design and mainstream infrastructure. Native models are likely to benefit most in jurisdictions that give blockchain-based records stronger legal standing and clearer recognition in settlement and ownership law. Hybrid structures will remain relevant in cross-border issuance, but over time, the tokenized securities market is likely to favor native or near-native, well-regulated models.

By Issuer Type: Banks Control Issuance Volume, Crypto-Native Platforms Reshape the Stack

Traditional financial institutions held 68.44% of the tokenized securities market in 2026, reflecting their advantages in established balance sheets, custody networks, and long-standing regulatory relationships. Large banks and asset managers also control many of the products that have moved fastest from pilot into production, especially in tokenized money market funds and Treasury-linked structures. J.P. Morgan Asset Management's MONY and JLTXX, along with the Goldman Sachs and BNY money market fund solution, show how incumbents are using tokenization to extend familiar liquidity products into digital channels rather than replacing existing business models outright. This incumbent strength matters because the tokenized securities market still requires trusted issuance, custody, and compliance functions that many newer firms are only beginning to build. For that reason, banks continue to control issuance volume even as the technology stack becomes more open.

Crypto-native and specialized tokenization platforms are the fastest-growing issuer cohort, forecast to expand at a 45.83% CAGR through 2031. Their role is growing because they move faster on product design, wallet integration, transfer automation, and support for on-chain investor functionality than most incumbent institutions. Ondo Finance's April 2026 partnership with Broadridge is a good example, as it added proxy voting and access to governance materials for holders of more than 250 tokenized stocks and ETFs, helping close a gap between tokenized wrappers and traditional investor rights. These platforms are still operating alongside incumbent financial institutions rather than displacing them. Still, they are reshaping the service layer that supports issuance, transfer, and investor administration in the tokenized securities market. Public sector issuers and corporates remain smaller contributors because legal ownership complexity and compliance setup costs still favor specialist or bank-led issuance channels.

Geography Analysis

North America captured 67.34% of the tokenized securities market share in 2025, which made it the clear regional center of activity. The region benefits from the depth of the United States market infrastructure, the concentration of major asset managers and market utilities, and a sequence of regulatory approvals that now support issuance, trading, and settlement more coherently. DTCC received authorization for its tokenization service in December 2025 and confirmed live-pilot trading and commercial-launch milestones in 2026, which will give North America a strong institutional operating base. The SEC and CFTC interpretive release and the Nasdaq approval in March 2026 added legal and exchange-level clarity, which further strengthened the region's first-mover position. This combination means the tokenized securities market in North America is already moving from pilot activity toward production-grade implementation.

Europe is the fastest-growing regional segment, and the tokenized securities market size in this geography is projected to expand at 44.25% CAGR through 2031. Growth is being supported by a more active policy agenda around wholesale market tokenization, fund tokenization, and digital asset infrastructure. In the United Kingdom, the FCA issued PS26/7 in May 2026 and set the Blueprint model as the operating framework for tokenized authorized funds, providing firms with a clearer path to launch and supervision. The Bank of England and FCA also set out a shared vision for tokenization in wholesale markets in May 2026, which supports longer-term changes in settlement and payments infrastructure. Europe still faces classification and interoperability frictions, but the policy direction is making the region more attractive for the tokenized securities market.

Asia-Pacific accounts for a smaller share today, but it remains one of the most important regions for future expansion in the tokenized securities market. Singapore set a high compliance benchmark with its revised tokenization guide and the 2025 clarification of the licensing regime for digital token service providers, making it a reference market for institutional-grade issuance and servicing. In Japan, SBI Holdings announced its first security token bond series for individual investors in February 2026, indicating that retail-facing security token products are also beginning to develop under regulated local structures. The Middle East is also emerging through ADGM-linked distribution structures such as Binance's planned bStocks framework. At the same time, South America remains at an earlier exploratory stage in the tokenized securities market.

Competitive Landscape

The tokenized securities market remains moderately fragmented, with scale spread across asset managers, banks, infrastructure utilities, and specialist tokenization platforms rather than concentrated in a single control point. Incumbent institutions hold an advantage in assets under management, regulated distribution, and balance sheet trust, while digital-native firms are moving faster on on-chain functionality, wallet access, and investor workflow design. DTCC's tokenization service is one of the clearest examples of incumbent strategy because it extends a systemically important post-trade role into digital asset infrastructure with support from more than 50 market participants. Nasdaq's unified order-book approval is another example, bringing tokenized securities into mainstream exchange operations rather than treating them as a separate market silo. This competitive shape means the tokenized securities market is being built through overlap between legacy market power and newer platform capabilities.

Competition is also defined by product strategy. J.P. Morgan Asset Management expanded from MONY to JLTXX between late 2025 and 2026, which shows a deliberate move to build a broader tokenized liquidity suite across private placement and registered fund structures. Goldman Sachs and BNY chose a different route by building tokenized money-market fund infrastructure around digital ownership records and collateral use, tying tokenization more closely to treasury and post-trade workflows. Ondo Finance's partnership with Broadridge adds another layer of competition by focusing on investor rights, proxy voting, and communications, which are essential to broader public securities adoption. These moves show that the tokenized securities market is not being shaped by a single winning model, but by multiple attempts to control the links among issuance, custody, administration, and trading.

White-space opportunities remain, especially in secondary market-making outside tokenized Treasuries, cross-border compliance services, and infrastructure supporting non-United States equity tokenization with strong legal rights. Firms that can simplify ownership verification, address transfer restrictions, and support multi-jurisdictional servicing should have room to grow as the tokenized securities market broadens. At the same time, the scale advantage of incumbents is likely to persist, as large institutions increasingly adopt tokenization through their existing client and infrastructure franchises. That balance should keep competition active without producing extreme consolidation in the near term.

Tokenized Securities Industry Leaders

Securitize

Ondo Finance

Broadridge Financial Solutions, Inc.

DTCC

Tokeny Solutions SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DTCC announced plans to facilitate initial, limited production trades of tokenized assets in July 2026 and a full commercial service launch in October 2026, with over 50 firms, including BlackRock, Circle, Anchorage Digital, and Fireblocks, joining the industry working group

- May 2026: J.P. Morgan Asset Management launched its second tokenized money market fund (JLTXX) on Ethereum, a registered fund investing in United States Treasuries and overnight repos and accessible alongside MONY through the Morgan Money platform, expanding JPMorgan's tokenized liquidity suite across private placement and registered fund structures

- April 2026: Ondo Finance announced a partnership with Broadridge Financial Solutions, enabling holders of over 250 tokenized stocks and ETFs to participate in proxy voting and access regulatory filings and governance communications through Broadridge's investor communications infrastructure, the first such capability for third-party tokenized public securities.

- March 2026: SEC approved Nasdaq's proposal to trade tokenized and traditional shares on unified order books under the DTC Pilot, covering Russell 1000 constituents, major ETFs, and United States Treasuries, with identical execution priority for both share forms.

Global Tokenized Securities Market Report Scope

| Tokenized Equity Securities |

| Tokenized Debt / Fixed Income Securities |

| Tokenized Fund Shares / Collective Investment Schemes |

| Other Tokenized Securities |

| Institutional Investors |

| Retail Investors |

| Native Tokenized Securities |

| Non-Native / Represented / Wrapped |

| Hybrid Structures |

| Traditional Financial Institutions |

| Crypto-Native / Specialized Tokenization Platforms |

| Public Sector & Development Institutions |

| Corporate Issuers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Asset Class | Tokenized Equity Securities | |

| Tokenized Debt / Fixed Income Securities | ||

| Tokenized Fund Shares / Collective Investment Schemes | ||

| Other Tokenized Securities | ||

| By Investor Type | Institutional Investors | |

| Retail Investors | ||

| By Tokenization | Native Tokenized Securities | |

| Non-Native / Represented / Wrapped | ||

| Hybrid Structures | ||

| By Issuer Type | Traditional Financial Institutions | |

| Crypto-Native / Specialized Tokenization Platforms | ||

| Public Sector & Development Institutions | ||

| Corporate Issuers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of tokenized securities by 2031?

The tokenized securities market is projected to reach USD 184.27 billion by 2031 from USD 35.82 billion in 2026, at a CAGR of 38.8% during 2026-2031.

Which asset class currently leads global adoption?

Debt and fixed income led with 61.36% share in 2025, mainly because Treasuries and money market instruments are easier to regulate, value, and use as collateral.

Which investor group is growing the fastest?

Retail investors are forecast to expand at 48.72% CAGR through 2031, even though institutional investors still held 91.48% of the market in 2025.

Why is North America ahead in tokenized securities adoption?

North America held 67.34% share in 2025 because of deep United States capital markets infrastructure, DTCC pilot progress, and clearer SEC and CFTC treatment of digital securities.

What is the main risk slowing wider adoption?

The largest constraints are regulatory fragmentation across jurisdictions, legal uncertainty around ownership rights in some structures, and limited liquidity outside a few flagship products.

Which structure is expanding the fastest?

Native tokenized securities are projected to grow at 43.67% CAGR through 2031, although wrapped and represented formats still led with 55.07% share in 2026.

Page last updated on: