Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

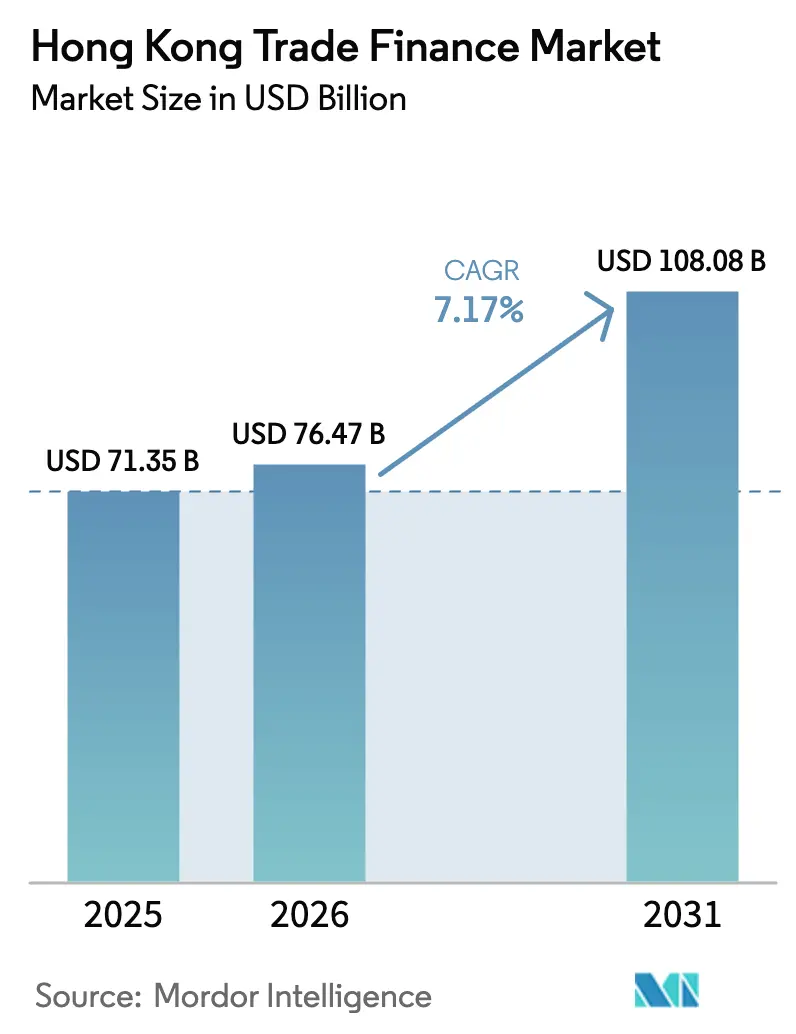

| Base Year Market Size (2025) | USD 71.35 Billion |

| Market Size (2026) | USD 76.47 Billion |

| Market Size (2031) | USD 108.08 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Trade Finance Market Analysis by Mordor Intelligence

The Hong Kong Trade Finance Market size is expected to grow from USD 71.35 billion in 2025 to USD 76.47 billion in 2026 and is forecast to reach USD 108.08 billion by 2031 at 7.17% CAGR over 2026-2031.

This growth trajectory rests on accelerating digital adoption, the rise of renminbi-denominated settlement, and policy backstops that de-risk lending to smaller exporters. Blockchain platforms are compressing letter of credit processing cycles, freeing compliance staff for higher-margin business, while tokenization pilots convert illiquid collateral into tradable assets[1]eTradeConnect, “About eTradeConnect,” etradeconnect.net. Government extensions of guarantee schemes continue to absorb default risk, sustaining demand from small and medium-sized enterprises even as Mainland trade volumes soften. Meanwhile, the top banks contend with margin pressure from Basel III liquidity rules and heightened anti-money-laundering scrutiny, which together reduce appetite for low-yield documentary instruments. Non-bank platforms and insurers are exploiting these constraints, drawing fresh liquidity into payables and supply-chain finance pools.

Key Report Takeaways

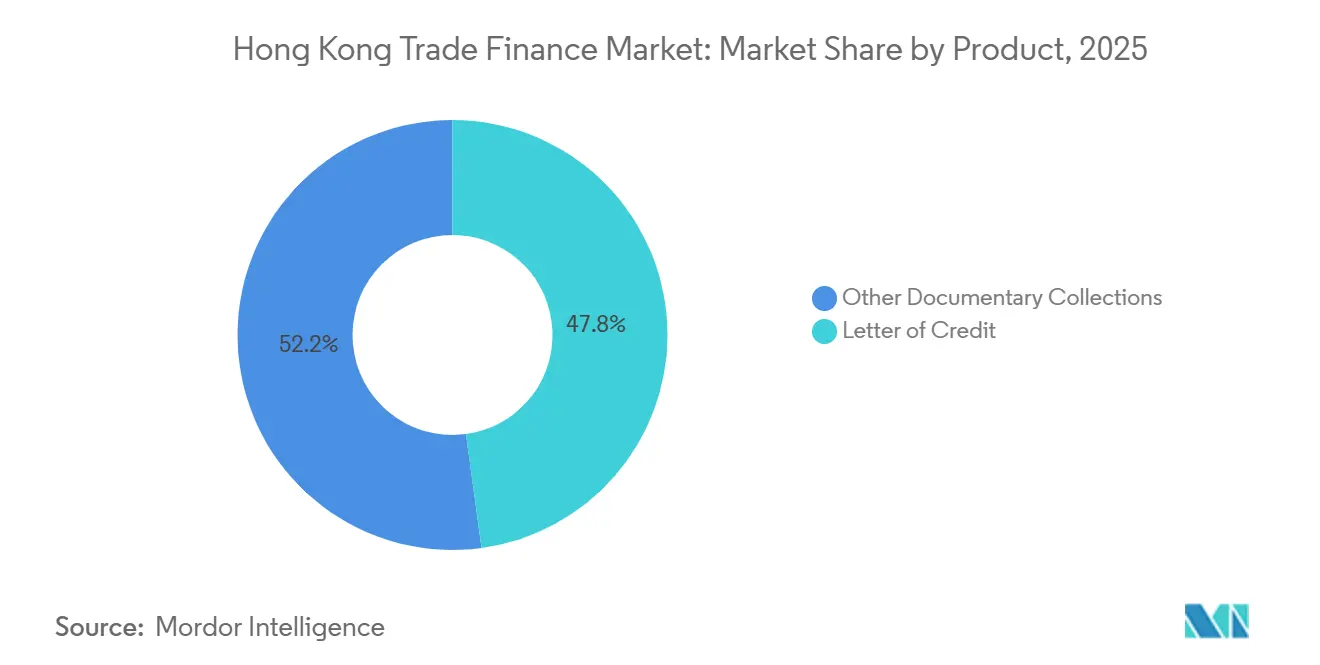

- By product category, documentary instruments led with 47.84% of Hong Kong trade finance market share in 2025; payables and supply-chain finance solutions are forecast to expand at a 10.45% CAGR through 2031.

- By service provider, banks held 84.78% of the Hong Kong trade finance market share in 2025, while fintech-enabled platforms were projected to record the highest CAGR at 9.87% through 2031.

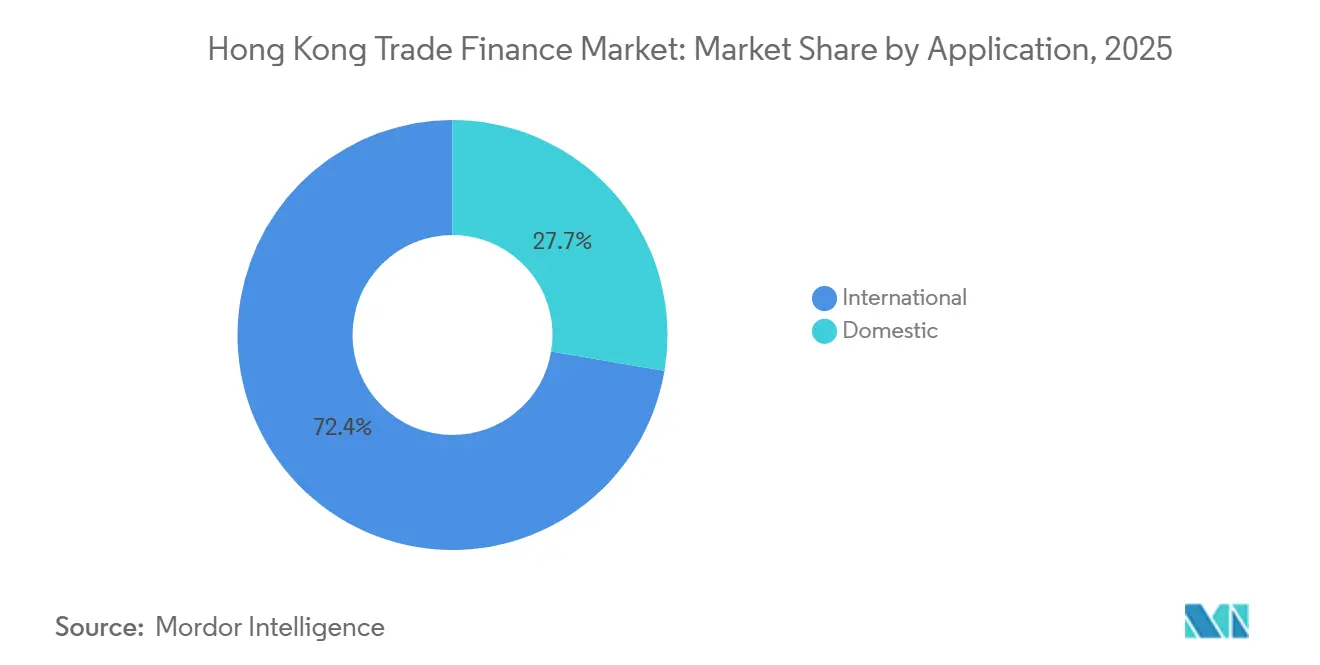

- By application, international transactions accounted for 72.35% of the Hong Kong trade finance market size in 2025 and are projected to advance at a 10.23% CAGR through 2031.

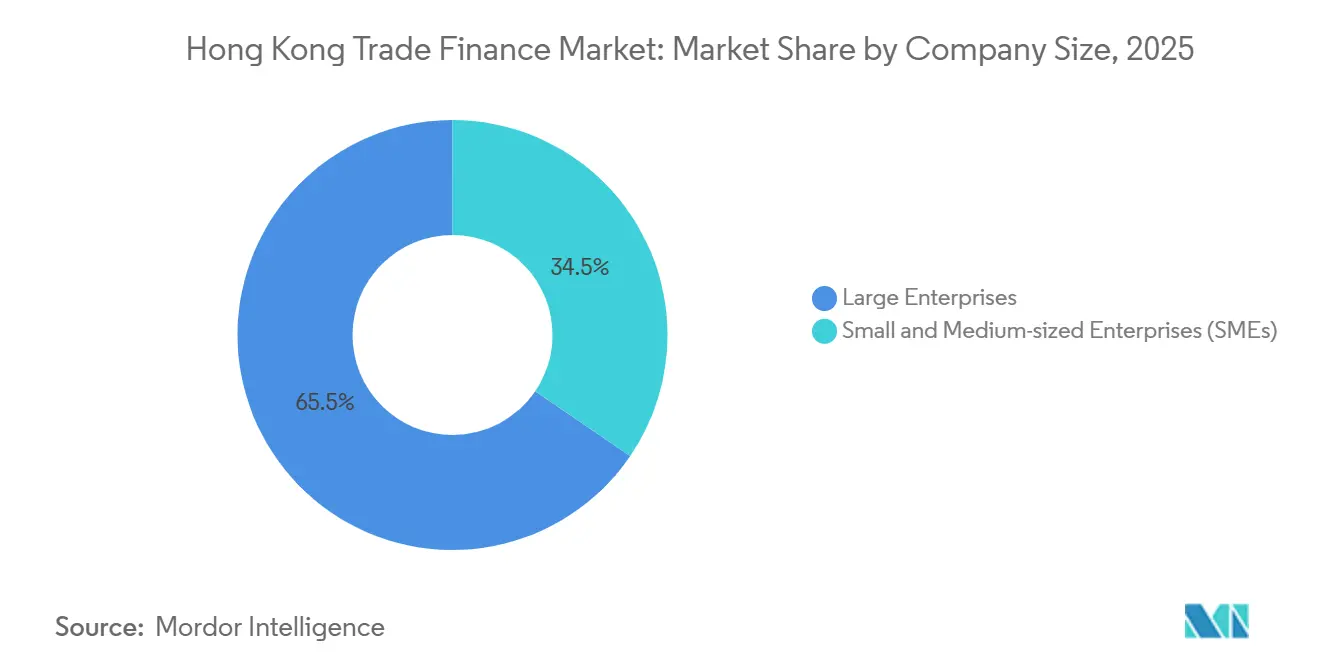

- By company size, SMEs are projected to expand at an 11.43% CAGR to 2031, supported by the fact that Large Enterprises accounted for 65.48% of the Hong Kong trade finance market size in 2025.

- By financing structure, structured trade finance captured a 59.48% share of the Hong Kong trade finance market size in 2025 and is growing at a 10.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hong Kong Trade Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of documentary trade flows | +1.8% | Global, concentrated in APAC and Europe | Medium term (2 – 4 years) |

| Expansion of RMB-denominated trade settlement | +1.5% | APAC core, spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Government SME-guarantee schemes extension | +1.2% | Hong Kong domestic | Short term (≤ 2 years) |

| Cross-boundary Wealth & Trade Connect programmes | +1.0% | Greater Bay Area | Medium term (2 – 4 years) |

| Tokenization of trade assets and gold collateral | +0.9% | Early adoption in APAC and the Middle East | Long term (≥ 4 years) |

| Rise of ESG-linked trade-finance facilities | +0.8% | Global, led by Europe and APAC | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Digitization of Documentary Trade Flows

Blockchain platforms in Hong Kong have reduced the average processing time for letter of credit from several days to under a day, providing a direct boost to working capital for importers. By mid-2025, the eTradeConnect consortium had processed numerous transactions and achieved interoperability with Contour, facilitating cross-border credits worth millions of United States dollars. In 2024, the Hong Kong Monetary Authority announced the Commercial Data Interchange initiative, which is streamlining digital bills of lading across multiple jurisdictions. This move reduces courier costs and mitigates document-fraud losses. Artificial intelligence vendors such as Traydstream are transforming compliance checks, reducing manual review time significantly, and creating a more level competitive landscape for mid-tier banks. These advancements in efficiency are particularly beneficial for small and medium enterprises, which previously relied on slower documentary collections for access to credit.

Expansion of RMB-Denominated Trade Settlement

Renminbi settlement through Hong Kong increased in 2025, reflecting hedging demand against dollar volatility and cheaper funding via the Hong Kong Monetary Authority’s RMB Trade-Financing Liquidity Facility. The People’s Bank of China expanded bilateral currency swaps to multiple jurisdictions, enabling direct RMB settlement for Belt and Road projects and reducing reliance on dollar nostro balances[2]People’s Bank of China, “RMB Internationalization,” pbc.gov.cn. Banks have seen a growing proportion of RMB-denominated trade, led by commodity traders in Southeast Asia. Banks lacking RMB clearing licenses face margin pressure as corporates arbitrage spreads between dollar and RMB-linked facilities. This trend positions Hong Kong as a leading offshore liquidity pool for RMB-denominated sukuk, tapping Gulf Cooperation Council demand for sharia-compliant Chinese exposure.

Government SME-Guarantee Schemes Extension

The Special 100% Loan Guarantee under the SME Financing Guarantee Scheme now runs through mid-2026, covering loans per borrower[3]Hong Kong Monetary Authority, “Commercial Data Interchange,” hkma.gov.hk. Since the 2025 budget announcement, the scheme has supported numerous SME facilities, keeping non-performing loan ratios near pre-pandemic levels despite softer exports. Banks disclosed a notable rise in SME trade-finance originations, with pricing advantages over unsecured loans. The guarantee tiers have broadened supply-chain finance to second-tier suppliers lacking audited statements. However, the 2026 expiry introduces refinancing risk that could trigger restructurings if external demand remains muted.

Cross-Boundary Wealth & Trade Connect Programmes

By the end of 2025, the Wealth Management Connect scheme recorded significant cumulative flows, and its infrastructure is being adapted to securitize trade receivables for institutional investors. Greater Bay Area manufacturers can now distribute RMB-denominated invoices to Hong Kong asset managers seeking yields. A pilot Trade Connect extension allows Mainland exporters to pledge Hong Kong dollar receivables for onshore working-capital loans, creating a two-way liquidity corridor. Early participants report reduced borrowing costs for manufacturers. The initiative addresses the mismatch between long payment terms and immediate cash-flow needs.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contraction in Mainland-related trade lending | –1.2% | Hong Kong and Pearl River Delta | Short term (≤ 2 years) |

| Tightening Basel III capital and liquidity rules | –0.9% | Global, acute in APAC and Europe | Medium term (2 – 4 years) |

| Heightened trade-based money-laundering scrutiny | –0.7% | Cross-border corridors | Short term (≤ 2 years) |

| Diminishing U-line trucking and border logistics capacity | –0.4% | Hong Kong-Mainland crossings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Contraction in Mainland-Related Trade Lending

Hong Kong’s merchandise trade declined during the first nine months of 2025 amid slower Chinese exports and supply-chain shifts toward Southeast Asia. Letter of credit and pre-shipment finance, once a core component of bank balance sheets, are steadily shrinking. HSBC reported a sequential contraction in its Greater China trade-finance book during the third quarter of 2025, redeploying capital toward wealth-management activities[4]HSBC, “Trade and Receivables Finance,” hsbc.com. Smaller Mainland banks have increasingly consolidated dollar-clearing activities through state-owned institutions, reducing fee income opportunities for Hong Kong correspondent banks. The Hong Kong Monetary Authority observed a rise in trade-finance non-performing loans in mid-2025, reflecting mounting pressure on exporters facing extended payment terms.

Tightening Basel III Capital & Liquidity Rules

The full implementation of Basel III in early 2024 increased capital intensity for trade-finance assets, as banks are now required to hold additional high-quality liquid assets against contingent liabilities. Documentary trade products have also attracted higher operational-risk charges related to cyber and process vulnerabilities, prompting banks to exit lower-margin client relationships. Standard Chartered reduced trade-finance risk-weighted assets during 2025, prioritizing supply-chain-finance structures that generate recurring foreign-exchange and transaction-banking revenues. Non-bank lenders and trade-credit insurers, which are not subject to Basel capital rules, have gained share in smaller transactions but lack the balance-sheet capacity to support large commodity trades. Regulators are consulting on potential capital relief for institutions adopting blockchain-based verification frameworks, signaling a possible easing of capital pressure for digitally enabled trade-finance models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Documentary Instruments Face Digital Substitution

Letter of credit controlled 47.84% of Hong Kong trade finance market share in 2025, anchored by regulatory mandates in emerging markets and commodity flows, but segment growth remains low as corporates migrate to open-account terms. Payables and supply-chain finance solutions are expected to grow rapidly at a 10.45% CAGR over the forecast period, driven by multinational buyers extending payment terms and using investment-grade ratings to offer suppliers early-payment discounts. Receivables finance, including factoring and forfaiting, is capturing share as fintech platforms cut transaction costs, unlocking invoice-level liquidity for SMEs. Guarantees and insurance products are gaining relevance amid elevated counterparty risk, encouraging firms to hedge exposures in volatile jurisdictions. Corporations are increasingly adopting blended product strategies to optimize costs and speed.

Fintech innovation is accelerating documentary substitution by digitizing bills of lading and embedding artificial-intelligence compliance checks, further shrinking processing times. Tokenization promises secondary-market liquidity, deepening investor appetite for structured receivables. However, guaranteed documents remain critical where legal or sovereign risk prompts importers to demand bank intermediation. Banks, therefore, maintain hybrid offerings, integrating blockchain verification into letter of credit workflows to defend their core franchises. As digital standards mature, the Hong Kong trade finance market is set to tilt decisively toward open-account structures, while maintaining a residual base of documentary instruments in high-risk corridors.

By Service Provider: Fintech Platforms Erode Bank Dominance

Banks commanded 84.78% of the Hong Kong trade finance market in 2025 due to their balance-sheet capacity and correspondent networks, yet fintech platforms are growing at a 9.87% CAGR by unbundling documentation, credit assessment, and liquidity provision. Trade-finance companies target SME niches with faster approval cycles, and insurers underwrite receivables for corporates lacking bank facilities. Logistics firms and commodity exchanges are entering via warehouse receipt financing, creating a modular ecosystem in which specialized providers collaborate via APIs. HSBC and Standard Chartered now supply liquidity to eTradeConnect and Contour rather than attempt to build competing rails.

Regulatory technology interfaces, such as the Commercial Data Interchange, reduce onboarding friction, inviting smaller banks to syndicate deals without large compliance teams. Insurtech innovations lower premium costs, incentivizing corporates to substitute credit insurance for letter of credit. The competitive landscape is therefore shifting from vertical integration to horizontal collaboration, with banks focusing on distribution while platforms supply origination and risk analytics. As tokenization scales, non-bank investors will gain easier access to short-duration assets, further chipping at bank share.

By Application: International Flows Dominate Despite Onshoring

International trade finance accounted for 72.35% of the Hong Kong trade finance market size in 2025, reflecting the territory’s deep role in transshipment and renminbi clearing. Growth at a 10.23% CAGR is underpinned by direct RMB settlement between Mainland exporters and buyers in Southeast Asia, the Middle East, and Africa. Cross-border e-commerce boosts small-ticket financing as platforms enable SMEs to export directly to consumers. Domestic trade finance grows steadily, aided by guarantee schemes but constrained by Hong Kong’s limited manufacturing base.

International demand benefits from tokenized receivables, which enable global investors to finance Asian supply chains. Dollar liquidity remains abundant, but corporates increasingly arbitrage into RMB or Hong Kong dollar funding to reduce costs and hedging complexity. Domestic financing relies on shorter-tenor products tailored to retail and wholesale distribution, with banks automating credit decisions based on point-of-sale and tax data. Nonetheless, international corridors will continue to dominate value, given Hong Kong’s legal infrastructure and currency convertibility.

By Company Size: SME Segment Accelerates on Guarantee Backstops

Large enterprises held 65.48% market share in 2025, leveraging diversified funding and favorable pricing; however, SMEs are projected to grow at 11.43% CAGR through 2031, buoyed by the 100% guarantee scheme and digital onboarding models. Hang Seng Bank reported that a growing share of new SME facilities originated online, reflecting machine-learning credit scoring based on transactional data. Fintech factoring platforms enable SMEs to monetize single invoices quickly, thereby improving working-capital efficiency. Trade-credit-insurance uptake increased as SMEs hedged buyer risk in unfamiliar jurisdictions. Expiry of the guarantee program in June 2026 creates refinancing uncertainty that could temper growth in the second half of the year.

Large corporates are pushing supply-chain finance deeper into vendor tiers, using reverse factoring to secure just-in-time supply and embed ESG metrics. They also anchor tokenized receivable programs that trickle liquidity to smaller suppliers. SMEs remain vulnerable to demand shocks and logistics disruptions so that policy continuity will shape segment resilience. If guarantee coverage narrows, insurance and fintech lenders may gain additional share by filling the liquidity gap.

By Financing Structure: Structured Products Capture Commodity Flows

Structured trade finance accounted for a 59.48% share in 2025 and is forecast to grow at a 10.65% CAGR, supported by commodity traders’ demand for pre-export and warehouse-receipt facilities. Non-structured open-account lending continues to advance as corporates favor speed and simplicity. Hong Kong’s gold market underpins gold-backed loans and tokenized receivables. Tokenization lowers custodian fees and enables real-time collateral valuation, enhancing investor appetite for structured assets. Insurance-wrapped unsecured facilities are gaining traction as banks transfer default risk to insurers, broadening credit availability.

Regulatory support via Project Ensemble is expected to accelerate structured adoption by standardizing digital asset frameworks. Deep-tier supply-chain finance, where second-tier suppliers pledge purchase orders from investment-grade anchors as collateral, is scaling rapidly, aided by guidance from the Asian Development Bank on legal enforceability. Non-structured lending still suits repeat buyers with strong payment history, but collateralized structures will dominate commodity segments given price volatility and longer transit times.

Geography Analysis

Asia-Pacific represented the largest share of Hong Kong's trade finance market in 2025, anchored by the Greater Bay Area and intra-ASEAN supply chains. Trade corridors linking Hong Kong to Vietnam, Thailand, and Indonesia are expanding as manufacturers diversify sourcing. Bilateral currency swaps enable direct renminbi settlement for Belt and Road projects, lowering dollar dependence. Japan and South Korea sustain steady demand for performance guarantees tied to capital goods exports, but mature banking systems limit growth potential. Australia and New Zealand present niche demand for commodity-backed structured finance, particularly iron ore and agricultural shipments.

The Middle East and Africa are expected to grow rapidly through 2031, driven by Gulf sovereign funds seeking RMB assets and Hong Kong’s roll-out of Islamic trade-finance windows offering sharia-compliant alternatives. Free-trade zones in the United Arab Emirates and Saudi Arabia are offering Hong Kong dollar receivables finance at attractive spreads, boosting cost competitiveness. Sub-Saharan Africa presents a significant opportunity due to the trade-finance gap, though its frail legal systems introduce risks. Insurers are broadening political-risk coverage to ease deal-making. Banks in Hong Kong are focusing on infrastructure imports, often backed by Chinese contractors and capitalizing on available export-credit agency guarantees.

Trade in Europe and North America holds a moderate share of the global market. European importers are increasingly using renminbi settlements for Chinese goods, using Hong Kong's clearing system to avoid foreign-exchange spreads and relying on the RMB liquidity facility. In North America, the focus is on financing commodities, with energy exports from Canada and agriculture from the United States. However, growth faces challenges from strong competition within domestic banking. South America's presence is limited, but Brazil's soybean and Argentina's beef exports are being financed through documentary credits and cargo insurance to counteract potential risks from counterparties.

Competitive Landscape

Market concentration is moderate, with the top five banks controlling half of the assets, yet they are also confronting non-bank disruptors. HSBC and Standard Chartered dominate large-enterprise and commodity segments, but both are trimming risk-weighted assets to meet Basel III targets while partnering with fintechs for document verification. Bank of China (Hong Kong) and Hang Seng Bank leverage Mainland ties to capture renminbi settlement, though spreads compress as corporates arbitrage funding costs. Mid-tier banks such as DBS, Citi, and OCBC Wing Hang differentiate through API connectivity that embeds trade finance within corporate treasury platforms.

European banks, including BNP Paribas and Crédit Agricole, focus on structured commodity finance yet face eroding share as Asian banks offer competitive RMB loans. Blockchain-based networks create white space for smaller institutions to syndicate risk without building full compliance infrastructures. eTradeConnect and Contour together streamlined document flows for new SME originations.

Insurers, including Allianz Trade and Coface, monetize credit intelligence underwriting receivables banks deem too granular and now hold a growing market share in low-risk corridors. Project Ensemble’s regulatory sandbox signals official backing for tokenized instruments, rewarding early adopters and intensifying competition. As digital assets gain acceptance, liquidity is poised to shift toward platforms that offer transparency, speed, and fractional investment entry points.

Hong Kong Trade Finance Industry Leaders

HSBC

Bank of China (Hong Kong)

Standard Chartered

Hang Seng Bank

DBS Bank (Hong Kong)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Standard Chartered Bank (Hong Kong) and Ant International launched a blockchain-based tokenized deposit solution for real-time, 24/7 multi-currency settlements (SGD, HKD, CNH, USD) on Ant’s Whale platform, enhancing global corporate treasury liquidity under Hong Kong’s HKMA Project Ensemble.

- September 2025: HSBC expanded its tokenized deposit offering to support cross-border USD and local currency payments, facilitating corporate clients’ real-time settlement between Hong Kong and Singapore and paving the way for broader corporate blockchain treasury use.

- September 2025: Hong Kong and Singapore advanced a regulated "token corridor" for digital assets and tokenized payments. By integrating frameworks for stablecoins and tokenized deposits, they established seamless channels for real-time cross-border finance, reinforcing Asia's strategy to drive digital finance adoption.

- August 2025: DBS Bank rolled out tokenized structured financial products, including blockchain-based structured notes and tokenized instruments, broadening investor access and signaling institutional adoption of tokenized finance solutions.

Hong Kong Trade Finance Market Report Scope

Trade finance encompasses the various financial tools and products businesses utilize to streamline international trade and commerce. It plays a crucial role in simplifying transactions for importers and exporters. The report covers a thorough knowledge of market segmentation, product types, current market trends, market dynamics modifications, growth possibilities, and examination of market size and projections for different segments.

The Hong Kong Trade Finance Market Report is Segmented by Product (Documentary, Non-Documentary), Service Provider (Banks, Trade Finance Companies, Insurance Companies, Other Service Providers), Application (Domestic, International), Company Size (Large Enterprises, SMEs), and Financing Structure (Structured, Non-Structured).

By Product

| Documentary | Letter of Credit |

| Other Documentary Collections | |

| Non-Documentary | Receivables Finance (Factoring, Forfaiting, Invoice Discounting) |

| Payables / Supply-Chain Finance (Reverse Factoring, Dynamic Discounting) | |

| Direct Lending / Open Account-Based Finance (Trade Loans, Buyer's / Seller's Credit) | |

| Guarantees (Performance, Bid, Financial Guarantees) | |

| Insurance Products (Trade Credit Insurance, PRI, ECA Cover) |

By Service Provider

| Banks |

| Trade Finance Companies |

| Insurance Companies |

| Other Service Providers |

By Application

| Domestic |

| International |

By Company Size

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

By Financing Structure

| Structured Trade Finance |

| Non-Structured Trade Finance |

| By Product | Documentary | Letter of Credit |

| Other Documentary Collections | ||

| Non-Documentary | Receivables Finance (Factoring, Forfaiting, Invoice Discounting) | |

| Payables / Supply-Chain Finance (Reverse Factoring, Dynamic Discounting) | ||

| Direct Lending / Open Account-Based Finance (Trade Loans, Buyer's / Seller's Credit) | ||

| Guarantees (Performance, Bid, Financial Guarantees) | ||

| Insurance Products (Trade Credit Insurance, PRI, ECA Cover) | ||

| By Service Provider | Banks | |

| Trade Finance Companies | ||

| Insurance Companies | ||

| Other Service Providers | ||

| By Application | Domestic | |

| International | ||

| By Company Size | Large Enterprises | |

| Small and Medium-sized Enterprises (SMEs) | ||

| By Financing Structure | Structured Trade Finance | |

| Non-Structured Trade Finance | ||

Key Questions Answered in the Report

What is the current value of the Hong Kong trade finance market?

The Hong Kong trade finance market size is USD 76.47 billion in 2026.

How fast will the sector grow over the next five years?

The market is forecast to reach USD 108.08 billion by 2031, expanding at a 7.17% CAGR.

Which product category is expanding the quickest?

Payables and supply-chain finance solutions are projected to grow at a 19.35% CAGR through 2031.

How are SMEs being supported in accessing trade finance?

A government-backed 100% loan guarantee covering loans up to USD 1.15 million (HKD 9 million) runs through June 2026, boosting SME lending.

What role does tokenization play in Hong Kong trade finance?

Tokenization pilots are converting receivables and gold-backed assets into digital securities, lowering ticket sizes and enhancing secondary-market liquidity.

Page last updated on: