Tissue Nanotransfection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

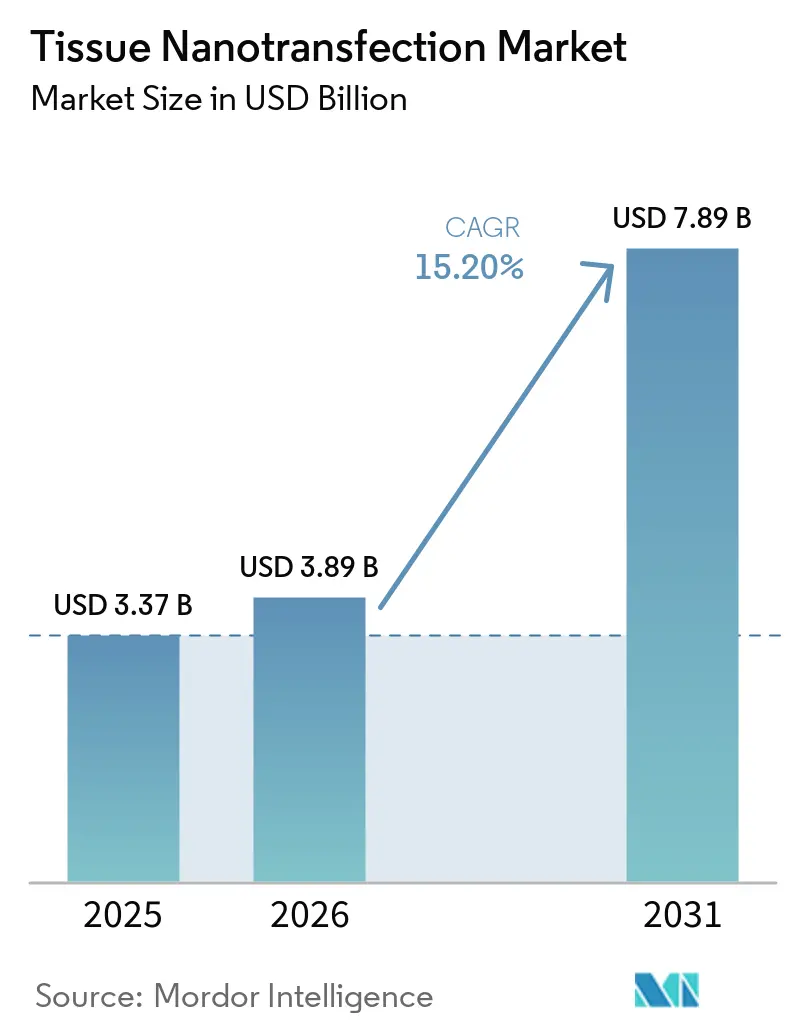

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 15.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Nanotransfection Market Analysis by Mordor Intelligence

The Tissue Nanotransfection Market size was valued at USD 3.37 billion in 2025 and is estimated to grow from USD 3.89 billion in 2026 to reach USD 7.89 billion by 2031, at a CAGR of 15.20% during the forecast period (2026-2031).

The tissue nanotransfection market is advancing due to its ability to deliver plasmid DNA, mRNA, and gene-editing cargo directly into living tissue within one second using silicon-based nanochannel and hollow microneedle structures. This eliminates the need for viral vectors, reducing concerns about immunogenicity and insertional mutagenesis. The market is also driven by increasing investments from major life sciences companies in non-viral in vivo delivery platforms that support localized cell engineering and regenerative medicine programs. Advancements in chip architecture, particularly the shift from flat nanochannel devices to hollow microneedle formats, have improved tissue contact and delivery precision. Additionally, research in wound healing, vascular repair, nerve repair, and stroke models highlights the market's potential to expand across therapeutic applications without relying on ex vivo cell expansion, simplifying manufacturing and treatment processes.

Key Report Takeaways

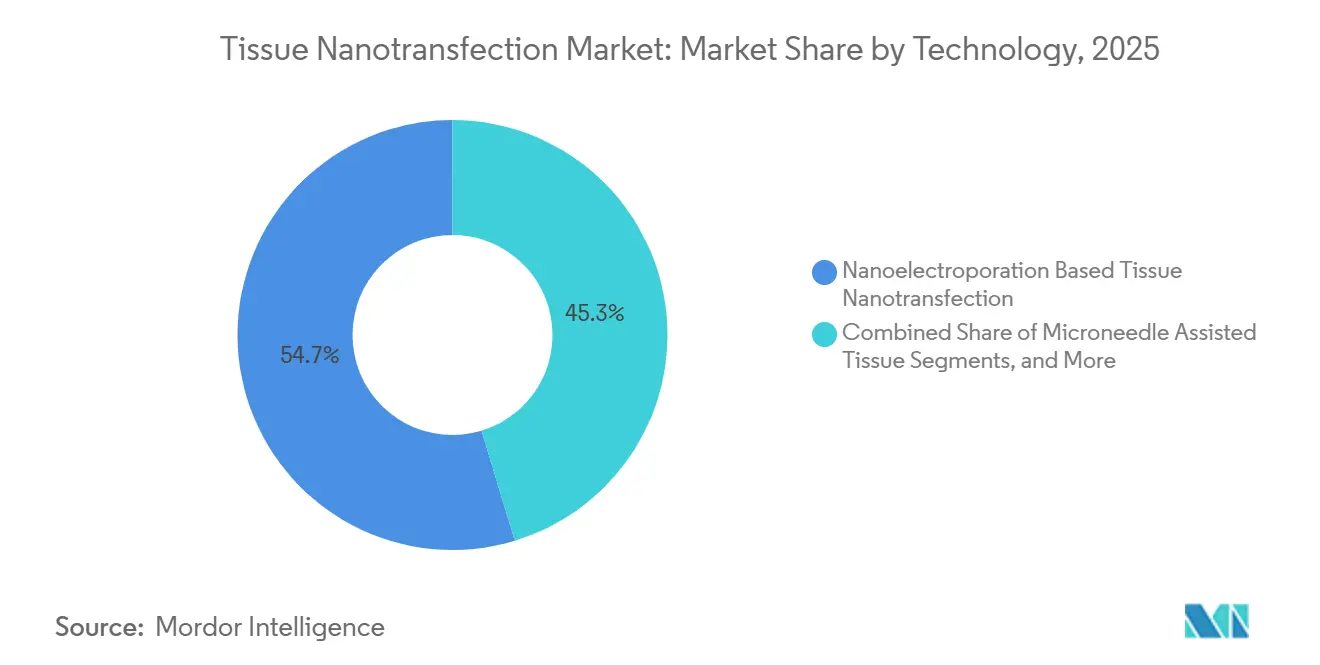

- By technology, nanoelectroporation-based tissue nanotransfection led with 54.67% revenue share in 2025, while microneedle-assisted tissue nanotransfection is forecast to expand at a 16.99% CAGR through 2031.

- By application, oncology and tumor microenvironment reprogramming accounted for 33.56% share in 2025, while neurological repair is projected to record the highest CAGR of 17.95% through 2031.

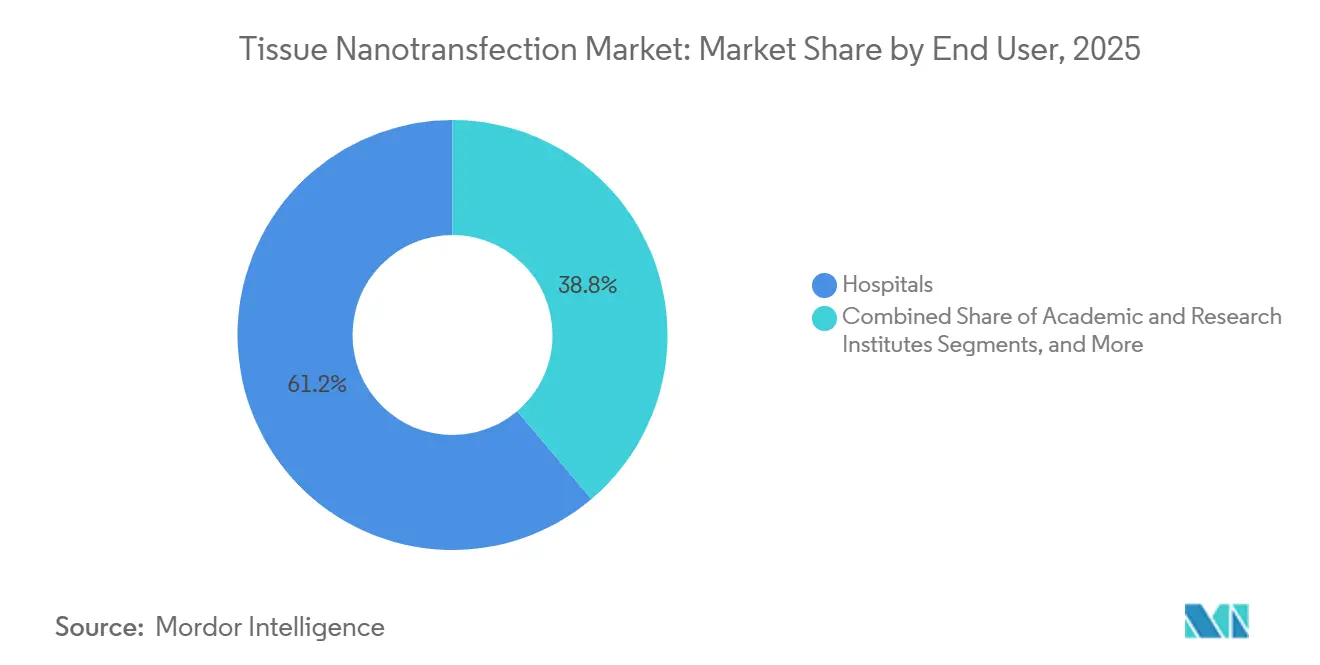

- By end user, hospitals held 61.20% of the tissue nanotransfection market in 2025, while academic and research institutes are expected to advance at a 17.55% CAGR through 2031.

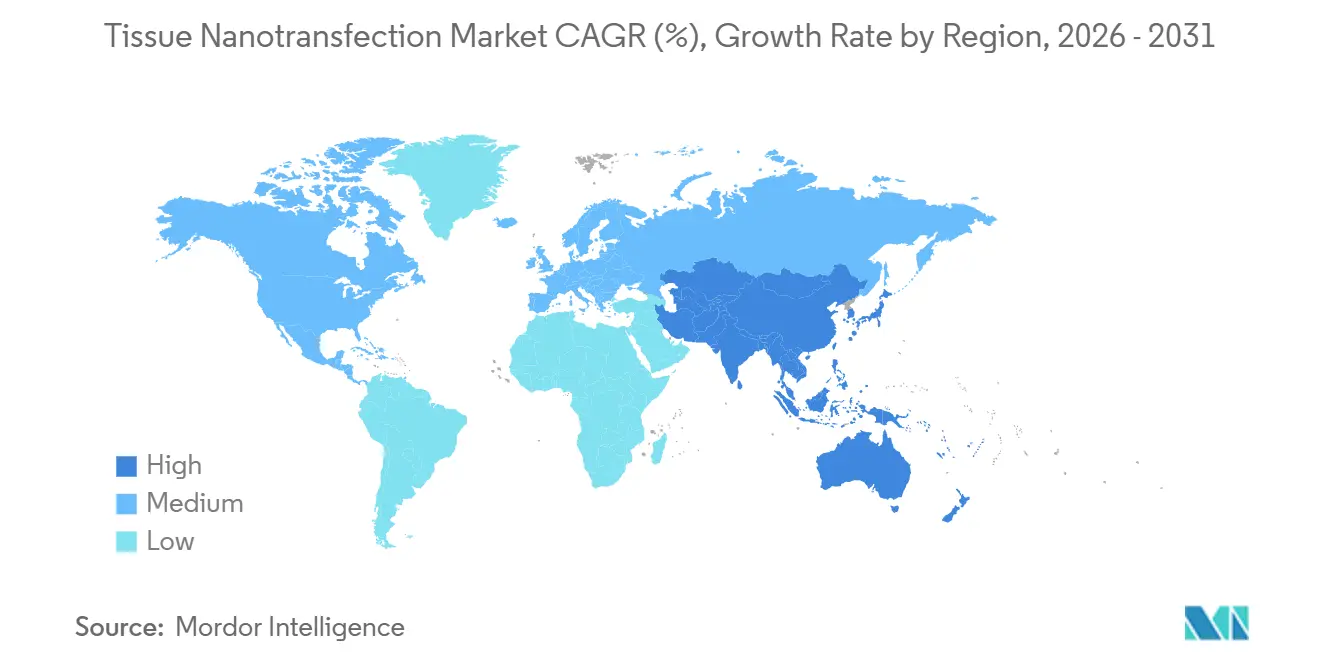

- By geography, North America captured 42.33% share in 2025, while Asia-Pacific is expected to grow at a 16.26% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tissue Nanotransfection Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for non-viral in vivo gene delivery | +4.2% | Global, with strongest momentum in North America and Europe | Short term (≤ 2 years) |

| Increasing clinical interest in localized tissue reprogramming | +3.6% | North America and Asia-Pacific, with early traction in Europe | Short term (≤ 2 years) |

| Advances in silicon hollow-needle and nanochannel chip fabrication | +2.8% | North America and East Asia | Medium term (2-4 years) |

| Expanding use cases across wound healing, vascular, and oncology applications | +2.0% | Global, with added relevance in wound care and regenerative medicine centers | Medium term (2-4 years) |

| Growing translation from academic proof-of-concept to clinical development | +1.6% | North America and Europe | Medium term (2-4 years) |

| AI-guided pulse optimization and semiconductor-scale manufacturing | +1.8% | East Asia and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Non-Viral In Vivo Gene Delivery

The tissue nanotransfection market is benefiting from a broader industry shift toward non-viral delivery methods. Researchers and developers are increasingly seeking ways to introduce genetic material into tissues without the complications often associated with viral systems. Tissue nanotransfection employs a brief electrical pulse alongside a silicon-based chip to directly transfer plasmid DNA, mRNA, and similar materials across cell membranes at the treatment site. This localized delivery approach not only sidesteps the use of viral vectors but also minimizes systemic exposure. Furthermore, it facilitates repeatable in situ reprogramming in tissues accessible through topical or surgical means. In a significant move underscoring this trend, AbbVie inked a deal to acquire Capstan Therapeutics for up to USD 2.1 billion in June 2025, bolstering its foothold in RNA-centric in vivo cell engineering. The tissue nanotransfection market is increasingly shedding its image as merely an academic curiosity. It's now being recognized as a viable platform for applications ranging from wound care and vascular repair to nerve repair and other tissue-centric initiatives.

Increasing Clinical Interest in Localized Tissue Reprogramming

The tissue nanotransfection market is witnessing a boost from heightened interest in localized tissue reprogramming. Published studies consistently demonstrate that targeted gene delivery can modify repair responses at injury sites, all without the need for cell harvesting. For instance, in preclinical studies related to strokes, using intracranial tissue nanotransfection with EFF factors not only reduced infarct volume but also enhanced functional recovery in murine models. Similarly, in models of peripheral nerve injuries, delivering vasculogenic genes via tissue nanotransfection led to improved vascularization and better grip outcomes over a 20-week span. In wound healing, studies have highlighted tissue nanotransfection's ability to reactivate angiogenic signaling, thereby accelerating healing in diabetic scenarios. Collectively, these findings signal a shift for the tissue nanotransfection market, moving from academic validation to concrete application-driven development.

Advances in Silicon Hollow-Needle and Nanochannel Chip Fabrication

The tissue nanotransfection market is bolstered by advancements in chips and devices, leading to more controlled, reproducible, and adaptable delivery methods across various tissues. Recent studies highlight a transition from TNT1.0 flat nanochannel chips to the more advanced TNT2.0 hollow microneedle designs. This evolution not only enhances the chip-tissue contact but also optimizes delivery depth and efficiency.[1]Frontiers in Bioengineering and Biotechnology, “Tissue Nanotransfection and Cellular Reprogramming in Regenerative Medicine and Antimicrobial Dynamics,” Frontiers in Bioengineering and Biotechnology, frontiersin.org These chips, crafted from silicon through cleanroom techniques like deep reactive ion etching and lithography, allow the tissue nanotransfection market to leverage established semiconductor manufacturing expertise, sidestepping the need for a completely new production setup. Additionally, a 2025 Engineering study showcased the efficacy of MXene hydrogel microneedles in a diabetic model, achieving 98% wound re-epithelialization by day 10. Broader evidence from preclinical studies indicates that dissolving microneedles often achieve, or even surpass, transfection results compared to traditional subcutaneous or intramuscular routes.[2]Nanomaterials Editorial Team, “Tissue Nanotransfection Silicon Chip and Related Electroporation-Based Technologies for In Vivo Tissue Reprogramming,” Nanomaterials, mdpi.com

AI-Guided Pulse Optimization and Semiconductor-Scale Manufacturing

The tissue nanotransfection market relies heavily on precise adjustments of voltage, pulse duration, waveform, and tissue contact. As the industry scales, AI-driven optimizations could play a pivotal role in enhancing performance. Currently, setting these protocols is often based on empirical methods and varies by tissue type. This variability not only hampers standardization but also complicates efforts to make the tissue nanotransfection market more universally applicable across different centers. At the 2026 ASGCT Annual Meeting, Dyno Therapeutics demonstrated the potential of integrating advanced AI models with high-throughput in vivo experiments. This synergy can refine delivery designs for various tissue targets and is indicative of future pulse optimization endeavors. On the manufacturing front, the tissue nanotransfection market stands to benefit from the semiconductor-level production expertise prevalent in North America and East Asia.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited clinical evidence and early-stage human adoption | -3.2% | Global, with added caution in Europe and conservative Asia-Pacific markets | Short term (≤ 2 years), Medium term (2-4 years) |

| Complex protocol optimization across tissue types and cell lines | -1.8% | Global, especially in research-led institutions | Medium term (2-4 years) |

| GMP sterility, yield, and device reproducibility challenges | -1.5% | Global, with greater impact where chip fabrication capacity is limited | Medium term (2-4 years), Long term (≥ 4 years) |

| Reimbursement and regulatory uncertainty for first-in-class devices | -1.7% | Europe, North America, and Asia-Pacific | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Evidence and Early-Stage Human Adoption

The tissue nanotransfection market faces challenges due to limited clinical evidence compared to extensive preclinical studies. As of 2026, research primarily focuses on wound healing, stroke, and peripheral nerve injuries in animal models, with insufficient long-term human safety and efficacy data. This lack of evidence impacts hospital and payer support, as they require more than mechanistic data for routine adoption.[3]Engineering Editorial Team, “MXene Hydrogel Microneedles with Nitric Oxide and HIF-1α Plasmid Controllable Releasing for Wound Healing,” Engineering, engineering.org.cn Additionally, the market encounters a learning curve at the point of care, where success depends on precise device placement, tissue preparation, pulse selection, and operator consistency. Biological uncertainty also persists, as reprogrammed cells must maintain their intended phenotype in dynamic tissue environments. Until these issues are resolved with stronger clinical follow-ups and standardized protocols, market growth will likely remain gradual.

Reimbursement and Regulatory Uncertainty for First-in-Class Devices

The tissue nanotransfection market faces a complex reimbursement and regulatory environment, positioned between active medical device logic and biologic cargo delivery. In the U.S., accelerated regenerative pathways aid development but do not ensure payer support or clear commercial access post-market. In Europe, stringent combination product regulations and higher clinical evidence requirements extend development timelines and increase costs for programs in wound care, neurology, oncology, and vascular repair. Manufacturing challenges, including sterile packaging, reproducibility, traceability, and device consistency, further complicate GMP scale-up. Without clear evaluation and payment standards, smaller developers may struggle to fund trials, establish manufacturing systems, and enter multiple global markets simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Nanoelectroporation Entrenched, Microneedle Platforms Accelerating

In 2025, Nanoelectroporation Based Tissue Nanotransfection held a 54.67% share of the tissue nanotransfection market within its technology segment. This dominance reflects the field's reliance on the foundational silicon nanochannel architecture, supported by extensive validation, consistent use in regenerative models, and a well-defined technical identity. The technology enables direct cargo transfer via nanoscale structures with brief electrical stimulation, offering a localized delivery method distinct from systemic non-viral carriers and bulk electroporation approaches. Nanoelectroporation remains the benchmark in the market, even as competing device designs advance.

Microneedle Assisted Tissue Nanotransfection is projected to grow at a 16.99% CAGR through 2031, making it the fastest-growing technology in the tissue nanotransfection market. Its growth is driven by improved tissue contact, easier penetration of surface layers, and versatile designs like dissolving, hydrogel, and hollow microneedles. A 2025 review highlighted that 83% of preclinical dissolving microneedle studies achieved transfection efficacy comparable to or better than traditional methods. While other formats remain relevant, the market will likely continue to center on established nanochannel systems and rapidly advancing microneedle platforms.

By Application: Distributed Therapeutic Landscape with Neurological Repair as the Breakout Segment

In 2025, Oncology and Tumor Microenvironment Reprogramming accounted for 33.56% of the market, highlighting the broad application base of tissue nanotransfection. This diversity mitigates risks by spanning areas like wound healing, vascular repair, nerve repair, and oncology. Neurological Repair is expected to grow at a 17.95% CAGR through 2031, driven by evidence of improved nerve vascularization, better recovery outcomes, and promising stroke-related studies. Despite being in early clinical stages, neurological applications are becoming a key focus in the market.

Wound Healing and Skin Repair remains a practical entry point due to the accessibility of skin, measurable healing outcomes, and high unmet needs in chronic wounds. Vascular and Ischemic Tissue Repair also holds potential, leveraging revascularization principles to address ischemic conditions. Musculoskeletal regeneration remains relevant, with studies showing gene delivery via tissue nanotransfection supports muscle repair. Oncology, while smaller, offers opportunities through in situ reprogramming of tumor-associated cells. Together, these applications provide breadth, with neurological repair and wound care emerging as key development areas.

By End User: Hospitals Anchor Current Adoption, Research Institutes Drive Future Pipeline

In 2025, hospitals captured 61.20% of the market, reflecting the need for controlled settings with trained operators, calibrated equipment, and defined workflows. Hospitals remain the primary base for tissue nanotransfection due to their ability to manage procedural quality and post-treatment monitoring. Academic and Research Institutes are forecast to grow at a 17.55% CAGR through 2031, as much of the field’s innovation originates from university-led work. This dynamic positions hospitals for current use and research institutes as drivers of future advancements.

Biotech and pharmaceutical companies are not yet the largest end-user group but are showing increasing interest as the market aligns with regenerative medicine strategies. Specialty clinics are emerging in advanced wound care, where local tissue access and repeat procedures fit the technology's logic. Other end users, such as translational medicine programs, may gain importance over time, but adoption will remain concentrated in settings capable of managing procedural quality and device reproducibility. Expansion is expected to progress outward from hospitals and research centers.

Geography Analysis

In 2025, North America dominated the tissue nanotransfection market, holding a significant 42.33% share. This leadership stems from a strong academic foundation, early translational efforts, and a regulatory framework that supports advanced regenerative products, despite reimbursement uncertainties. The U.S. plays a key role, driving major studies and translational initiatives. North American hospital networks also leverage critical safety data, such as findings from the 2025 Wound Healing Society, which demonstrated preserved mitochondrial bioenergetics and cytoskeletal integrity in gene-transfected skin tissue. This combination of scientific expertise, translational activity, and clinical infrastructure secures North America's leading position in the market.

Asia-Pacific is projected to grow at a 16.26% CAGR through 2031, making it the fastest-growing region in the tissue nanotransfection market. The region's strength in semiconductor fabrication aligns with the silicon chip processes used in device manufacturing. South Korea and Taiwan are key players, with mature microfabrication ecosystems supporting device scale-up. Additionally, advancements in regenerative medicine and gene delivery research drive demand for localized delivery tools, enabling their transition from research to application. These factors position Asia-Pacific as a critical growth region, despite varying clinical adoption across countries.

In 2025, Europe, the Middle East and Africa, and South America collectively held the remaining market share. Europe has a strong scientific base and expertise in wound care and regenerative medicine, but stringent evidence requirements can delay commercialization. Germany and the U.K. are notable for their active clinical work in electroporation and translational applications. In the Middle East and Africa, adoption is expected to grow in high-investment health systems, while other areas remain in earlier stages of readiness. South America, though nascent, benefits from research links and improving biotech capacity. These regions, while not market leaders, are positioned for growth as clinical and reimbursement clarity improves.

Competitive Landscape

The tissue nanotransfection market remains fragmented, with no single company emerging as a clear leader. Competition is primarily between large, diversified healthcare firms with regenerative capabilities and smaller, research-focused entities honing in on tissue nanotransfection expertise. This dynamic keeps the market open, but commercial leadership will hinge on the ability to integrate device performance, biological cargo strategy, manufacturing quality, and clinical evidence. Major players like Johnson & Johnson and AbbVie bring essential scale, financing, and infrastructure, positioning them to absorb or partner with emerging tissue nanotransfection initiatives. For instance, J&J’s announcement in February 2026 of a USD 1 billion investment in a next-generation cell therapy manufacturing facility in Pennsylvania underscores the commitment of these giants to bolster their production and development base for future regenerative platforms.

In the tissue nanotransfection market, competition extends beyond the device itself. Companies aiming for prominence must navigate application focus, clinical workflow design, sterile manufacturing, and protocol standardization. Opportunities abound for innovations like deeper tissue access tools, co-packaged reagent-device offerings, and software-assisted procedure controls to ensure consistent documentation across centers. Such innovations are crucial, as hospitals and payers will assess the market not just on mechanisms but also on reproducibility, training demands, and evidence quality. While smaller specialists may swiftly pivot in design and focus, larger entities can accelerate their scaling due to established commercial systems and regulatory teams. This strategic allure of the tissue nanotransfection market heightens the likelihood of partnerships or acquisitions determining the eventual leaders.

Recent strategic moves highlight how adjacent players are aligning with pivotal themes in the tissue nanotransfection market. Similarly, Johnson & Johnson’s June 2026 USD 1 billion acquisition of Firefly Bio demonstrates interest in oncology mechanisms that can transform tissue-level treatment strategies. Organogenesis, in April 2026, reported that its PuraPly AM achieved primary endpoints in a diabetic foot ulcer trial, emphasizing the importance of strong wound care evidence in regenerative settings. While no single company currently leads the tissue nanotransfection market, these moves indicate where capital, clinical focus, and commercial strategies are heading. As the market evolves, competition is expected to intensify around wound care and localized repair before expanding into broader regenerative and oncologic applications.

Tissue Nanotransfection Industry Leaders

Novartis AG

Zimmer Biomet Holdings, Inc.

Integra LifeSciences Holdings Corporation

NanoBio Corporation

NanoSonic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Global Tissue Nanotransfection Market Report Scope

As per the scope of the report, tissue nanotransfection (TNT) is a regenerative medical technique that uses a tiny chip to reprogram living skin cells into other types of cells (like blood vessels or nerve cells) directly in the body. It delivers genetic code using a painless, split-second electrical spark to heal and repair damaged organs.

The tissue nanotransfection market is segmented by technology, application, end-user, and geography. By technology, the market includes nanoelectroporation-based tissue nanotransfection, microneedle-assisted tissue nanotransfection, related electroporation-based platforms, and other nanotransfection technologies. By application, the market is segmented into wound healing and skin repair, vascular and ischemic tissue repair, neurological repair, musculoskeletal and muscle regeneration, oncology and tumor microenvironment reprogramming, and other applications. By end-user, the market is categorized into hospitals, specialty clinics, academic and research institutes, biotech and pharmaceutical companies, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Nanoelectroporation Based Tissue Nanotransfection |

| Microneedle Assisted Tissue Nanotransfection |

| Related Electroporation Based Platforms |

| Other Nanotransfection Technologies |

| Wound Healing and Skin Repair |

| Vascular and Ischemic Tissue Repair |

| Neurological Repair |

| Musculoskeletal and Muscle Regeneration |

| Oncology and Tumor Microenvironment Reprogramming |

| Other Applications |

| Hospitals |

| Specialty Clinics |

| Academic and Research Institutes |

| Biotech and Pharmaceutical Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Nanoelectroporation Based Tissue Nanotransfection | |

| Microneedle Assisted Tissue Nanotransfection | ||

| Related Electroporation Based Platforms | ||

| Other Nanotransfection Technologies | ||

| By Application | Wound Healing and Skin Repair | |

| Vascular and Ischemic Tissue Repair | ||

| Neurological Repair | ||

| Musculoskeletal and Muscle Regeneration | ||

| Oncology and Tumor Microenvironment Reprogramming | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Academic and Research Institutes | ||

| Biotech and Pharmaceutical Companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the tissue nanotransfection market?

The tissue nanotransfection market is valued at USD 3.89 billion in 2026 and is forecast to reach USD 7.89 billion by 2031, growing at a CAGR of 15.20% during 2026-2031.

Which technology segment leads tissue nanotransfection adoption?

Nanoelectroporation Based Tissue Nanotransfection leads the technology mix with a 54.67% share in 2025, supported by the strongest body of published validation and technical familiarity.

Which application is growing the fastest in tissue nanotransfection?

Neurological Repair is the fastest-growing application, with a projected CAGR of 17.95% through 2031, supported by published nerve repair and recovery data.

Why is North America leading in this field?

North America held 42.33% share in 2025 because of its stronger academic base, earlier translational activity, and more developed regenerative medicine infrastructure.

What is driving interest in tissue nanotransfection over older delivery approaches?

Interest is rising because tissue nanotransfection supports local non-viral delivery, avoids ex vivo cell expansion, and fits several tissue-directed repair settings such as wound healing and nerve regeneration.

What is the main barrier to wider adoption?

The main barrier is still limited human clinical evidence, along with reimbursement uncertainty and the need for tighter protocol standardization across tissues and care settings.

Page last updated on: