Nanotechnology Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

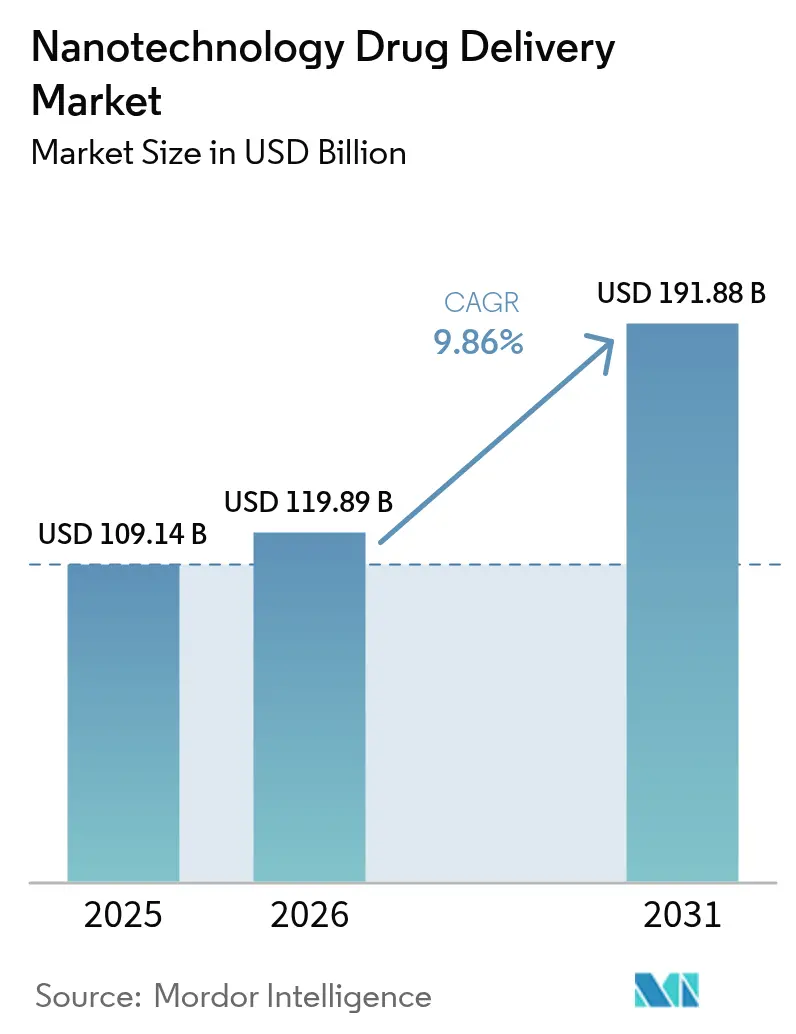

| Market Size (2026) | USD 119.89 Billion |

| Market Size (2031) | USD 191.88 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

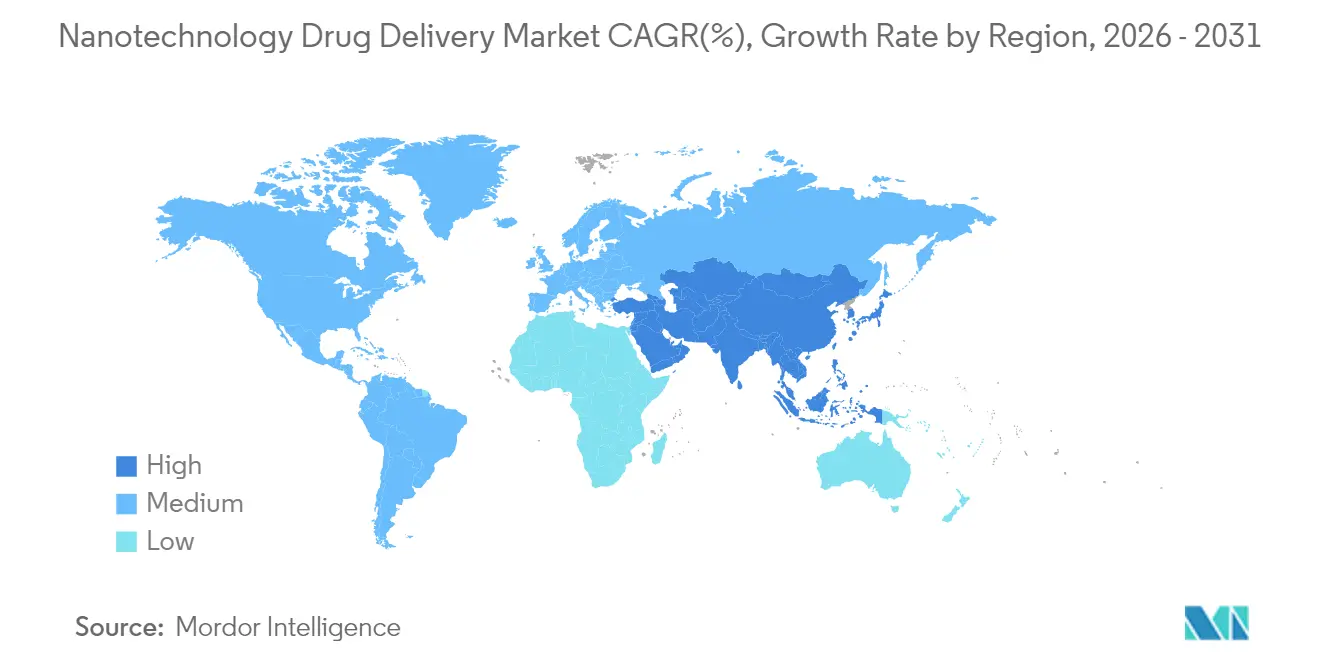

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

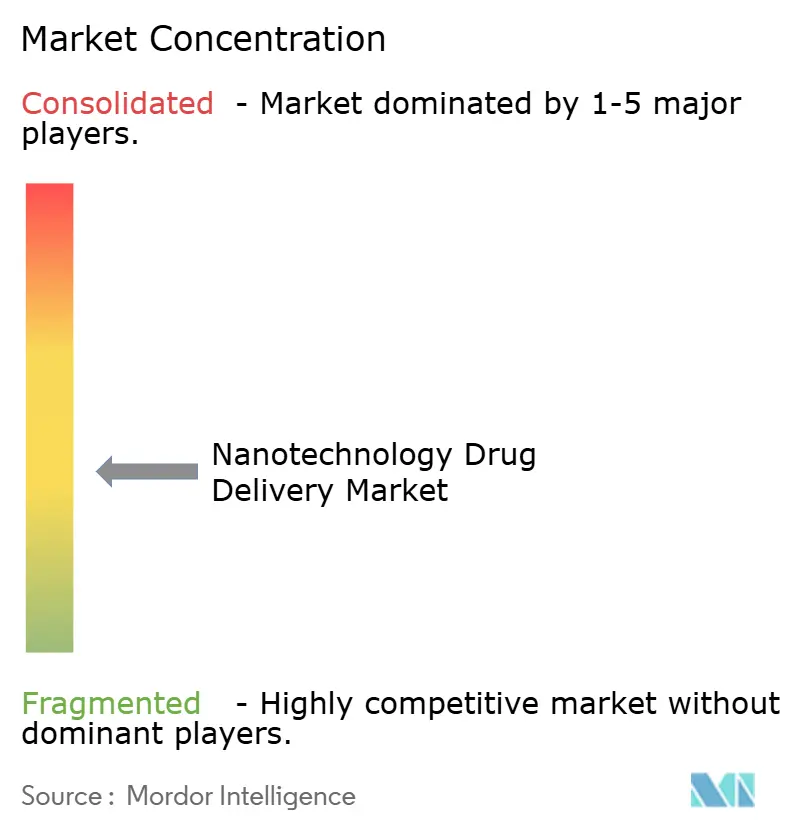

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nanotechnology Drug Delivery Market Analysis by Mordor Intelligence

nanotechnology drug delivery market size in 2026 is estimated at USD 119.89 billion, growing from 2025 value of USD 109.14 billion with 2031 projections showing USD 191.88 billion, growing at 9.86% CAGR over 2026-2031. This momentum reflects tighter alignment between advanced manufacturing, clearer regulatory pathways, and accumulating clinical proof that nano-enabled carriers improve drug targeting and safety profiles. Growth is further propelled by surging demand for lipid nanoparticles, which already account for one-third of revenue, as well as by the pharmaceutical sector’s pivot toward genetic medicine and other complex biologics. Oncology continues to anchor revenues as providers seek premium, precision-based formulations that address tumor heterogeneity, while gene therapy and mRNA programs lead the pace of expansion. Regionally, North America keeps its lead thanks to entrenched R&D spending and fast-moving regulators, yet Asia Pacific is rising fastest on the back of generous public funding and rapid capacity build-outs. Routes of administration are also diversifying as pulmonary delivery begins to challenge intravenous dominance amid improved inhalation devices and formulation science driving higher deposition efficiency. Longer term, platform consolidation around scalable lipid and polymer systems promises to shift competitive dynamics as manufacturing know-how becomes a critical differentiator within the nanotechnology drug delivery market.

Key Report Takeaways

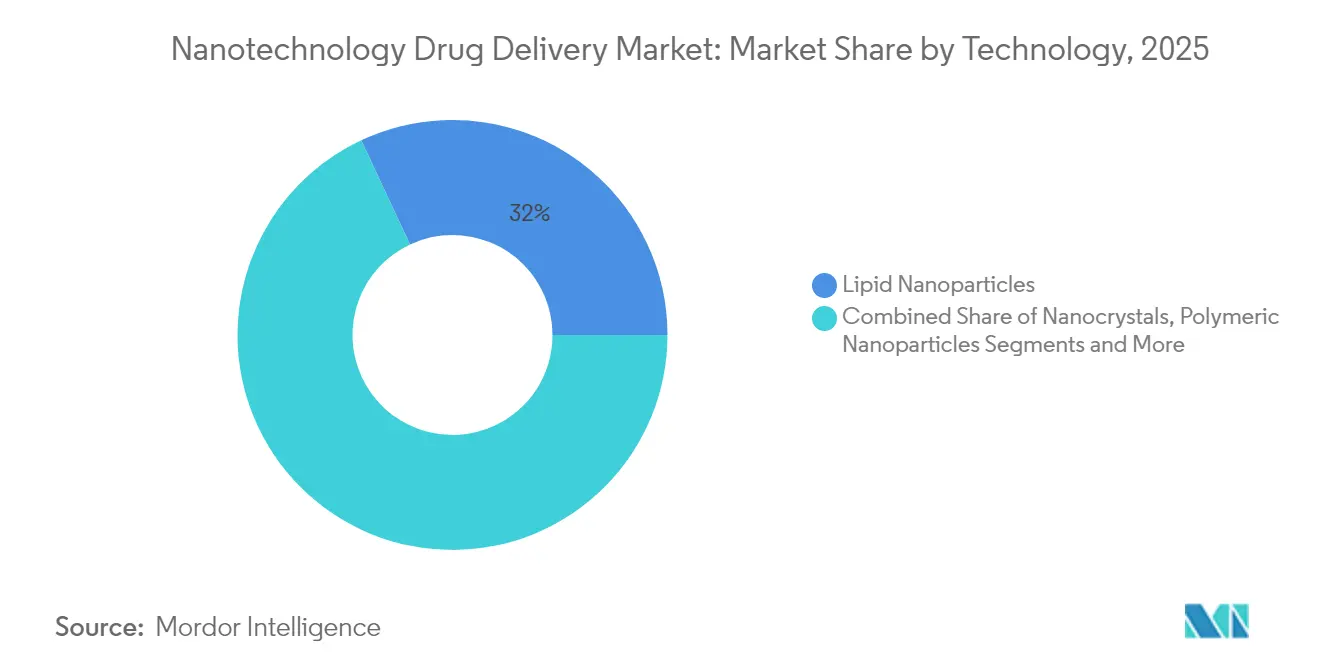

- By technology, lipid nanoparticles captured 31.98% of the nanotechnology drug delivery market share in 2025, while polymeric platforms are forecast to advance at a 13.02% CAGR to 2031.

- By application, oncology held 43.12% revenue share in 2025; gene therapy and mRNA delivery are set to expand at a 13.21% CAGR through 2031.

- By route of administration, intravenous delivery commanded 49.05% share of the nanotechnology drug delivery market size in 2025, whereas pulmonary delivery is projected to grow at 13.74% CAGR over the same horizon.

- By end-user, pharmaceutical and biotechnology companies accounted for 50.78% of 2025 revenue, while contract research and manufacturing organizations are growing fastest at 12.22% CAGR.

- By geography, North America led with 39.21% share in 2025, yet Asia Pacific is slated to register a 12.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nanotechnology Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Cancer, Genetic & Cardiovascular Diseases | +2.1% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Growing Pipeline Of Nano-Enabled Biologics & Gene Therapies | +1.8% | North America & EU leading, APAC emerging | Medium term (2-4 years) |

| Rapid Advances In Scalable Lipid-Nanoparticle (LNP) Manufacturing | +1.5% | Global, with manufacturing hubs in North America, Europe, APAC | Short term (≤ 2 years) |

| Hospital Demand For Personalized/Precision Dosing Platforms | +1.2% | North America & EU core, selective APAC markets | Medium term (2-4 years) |

| Venture Investment In Programmable Nanocarriers & Stimuli-Responsive DDS | +0.9% | North America & EU concentrated, emerging in APAC | Long term (≥ 4 years) |

| Government Nanomedicine Mega-Grants | +0.7% | National programs in US, EU, China, with spillover effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cancer, Genetic & Cardiovascular Diseases

Accelerating incidence of cancer, rare genetic disorders, and chronic heart conditions is enlarging the addressable pool of patients who need more precise dosing and tissue targeting. Growing life expectancy and better diagnostics add to case volumes, reinforcing the call for nano-enabled formulations that can navigate biological barriers while reducing toxic spillover. In cardiovascular care, nanoparticles are being designed to hone in on atherosclerotic plaques, a capability that broadens therapeutic windows for potent agents. Researchers at Oregon State University reported a 94% jump in targeting accuracy when nanoparticles were used to quell inflammatory cascades in preclinical models, underscoring how disease burden is turning into concrete commercial demand. Successful outcomes in one therapeutic area often spark spill-over interest in adjacent fields, speeding adoption curves across the healthcare system. As hospital formularies observe superior efficacy and safety records, demand for nano-formulations grows, strengthening the revenue base for the nanotechnology drug delivery market.

Growing Pipeline of Nano-Enabled Biologics & Gene Therapies

Messenger RNA vaccines validated the commercial and regulatory feasibility of lipid nanoparticle delivery, triggering a wave of venture funding and strategic deals aimed at next-generation gene therapies. Large drug makers are partnering with academic labs to refine encapsulation chemistries that protect fragile molecules and promote endosomal escape. Pfizer’s collaboration with UT Southwestern on RNA payload technologies typifies the collaboration model intended to cut translation times from bench to bedside. As more candidates clear mid-stage trials, comfort within regulatory agencies rises, diminishing approval risk and widening the funnel for nano-based therapeutics across oncology, rare diseases, and metabolic disorders. Pipeline growth thus reinforces demand for specialized manufacturing capacity, supporting longer-term revenue visibility for suppliers operating in the nanotechnology drug delivery market.

Rapid Advances in Scalable Lipid-Nanoparticle Manufacturing

Continuous processing, microfluidic mixers, and in-line analytics now permit real-time control of particle size and encapsulation efficiency, dismantling a historic scale-up bottleneck. Danaher’s acquisition of Precision Nanosystems created an end-to-end offering that spans early research to GMP production, providing drug makers with a turnkey route to globally harmonized supply. Wacker’s EUR 107 million mRNA center adds capacity for more than 200 million vaccine doses annually, demonstrating that capital is flowing into dedicated nano plants rather than retrofitting legacy lines.[1]Wacker Chemie AG, “WACKER Opens mRNA Competence Center in Halle an der Saale, Germany,” wacker.com Lower unit costs make nano formulations viable for chronic therapies, moving the technology beyond niche, high-priced indications and broadening the commercial canvas for the nanotechnology drug delivery market.

Hospital Demand for Personalized/Precision Dosing Platforms

Clinicians are gravitating toward nanoparticle formulations that trim adverse events and unlock higher dose intensities. Hospital pharmacy committees weigh formulary additions on both clinical and operational grounds, giving preference to nano drugs that shorten hospital stays or reduce readmissions. Theranostic particles able to signal their location in real time let physicians fine-tune regimens mid-course, improving outcomes. A Journal of Nanobiotechnology study showed enzyme-responsive nanoparticles could concentrate chemotherapy in tumors with 94% precision, capturing physician interest in real-world oncology settings.[2]Journal of Nanobiotechnology, “Enzyme-sequential responsive core-satellite nanomedicine enables activatable imaging-guided chemotherapy,” jnanobiotechnology.biomedcentral.com The link between measurable clinical benefit and operating-cost reduction accelerates procurement decisions, lifting demand in the nanotechnology drug delivery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CMC & GMP Compliance Cost For Nano-Formulations | -1.4% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Uncertain Long-Term Nano-Toxicology Data | -1.1% | Global regulatory concern, varying regional standards | Long term (≥ 4 years) |

| Scale-Up Bottlenecks For Microfluidic-Based Production | -0.8% | Manufacturing hubs in North America, Europe, APAC | Medium term (2-4 years) |

| Limited Reimbursement Pathways For Nano-Formulated Generics | -0.6% | North America & EU primarily, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CMC & GMP Compliance Cost for Nano-Formulations

Nano drugs often require bespoke production suites, particulate monitoring, and advanced analytics that push fixed costs well above those of conventional injectables. Detailed characterization of particle size, zeta potential, and surface chemistry must be maintained across shelf life, adding complexity. The FDA’s 2024 guidance on nanomaterial drug products emphasizes rigorous in-process testing, which many smaller firms struggle to afford.[3]Food and Drug Administration, “Considerations for Drug Products That Contain Nanomaterials,” fda.gov High compliance costs can delay launch timelines and discourage follow-on formulations, moderating expansion in the nanotechnology drug delivery market.

Uncertain Long-Term Nano-Toxicology Data

While acute toxicity signals are often benign, questions persist over long-term accumulation in the reticuloendothelial system. Regulators seek extensive biodistribution and clearance studies, adding both time and cost. A review in Discover Nano highlighted the fragmented nature of current assays and called for harmonized protocols across particle classes. Until longitudinal data mature, conservative risk-benefit evaluations may slow broader adoption within the nanotechnology drug delivery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Lipid Platforms Drive Commercial Adoption

Lipid nanoparticles generated 31.98% of 2025 revenue and remain the anchor of the nanotechnology drug delivery market. A blend of clinical validation and compatible excipient supply chains keeps adoption high, with a forecast 12.61% CAGR to 2031. News of successful mRNA vaccines normalized lipid-based design across therapeutic categories, prompting CDMOs to expand dedicated lines and secure long-term contracts. Polymeric systems, while second in share, excel at modulating release profiles in chronic therapies and show promise in multi-payload constructs. Nanocrystals are carving a space for poorly soluble drugs, whereas dendrimers appeal to researchers focused on multivalent ligand display despite heavier synthetic workloads. Quantum dots retain an imaging niche but face regulatory headwinds due to heavy-metal cores. Process scalability and regulatory precedent will continue to separate front-runner platforms from experimental niches, guiding capital allocation inside the broader nanotechnology drug delivery market.

By Application: Oncology Leadership Faces Gene Therapy Challenge

Oncology accounted for 43.12% revenue in 2025 because cancer care often rewards innovations that enable higher dose intensities or localized release. Liposomal reformulations of chemotherapeutics remain an enduring revenue stream. Gene therapy and mRNA indications are advancing at 13.21% CAGR, emblematic of the industry’s shift toward molecular-level interventions. Neurology programs are gathering momentum by harnessing nano carriers to cross the blood–brain barrier, while anti-inflammatory candidates gradually displace systemic steroids in rheumatoid settings. Cardiovascular trials remain smaller but stand to broaden if plaque-targeting nanoparticles validate in Phase III. Collectively, these tracks create a diversified opportunity set that stabilizes cash flow across the nanotechnology drug delivery market.

By Route of Administration: Pulmonary Delivery Gains Momentum

Intravenous lines dominated 49.05% of the nanotechnology drug delivery market size in 2025 owing to familiar hospital workflows. Yet pulmonary delivery is on course for the quickest gains: a 13.74% CAGR through 2031 supported by dry-powder inhalers that improve alveolar deposition. Oral nano capsules aspire to elevate adherence in chronic conditions, although gastrointestinal degradation remains a design hurdle. Transdermal nano emulsions continue to target dermatology and pain management, offering controlled surface delivery that minimizes systemic exposure. Together these routes dilute supply-chain risk and extend nano-enabled care into outpatient settings, supporting volume growth in the nanotechnology drug delivery market.

By End-user: Contract Manufacturing Gains Strategic Importance

Pharmaceutical and biotechnology companies controlled 50.78% of 2025 sales by virtue of marketing authorizations, but they increasingly outsource particle engineering and fill-finish work. CDMOs are rewarded with a 12.22% CAGR for investing in clean-room facilities and GMP analytics. Hospital compounding caters to individualized doses for ultra-rare disorders, yet capital barriers often steer production toward specialized suppliers. Academic centers drive discovery, passing transfers to industry partners as scale requirements emerge. This interlinked ecosystem underpins the resilience and specialization evident in the nanotechnology drug delivery market.

Geography Analysis

North America captured 39.21% of global revenue in 2025 and remains a magnet for first-in-human studies thanks to clear FDA guidance and dense venture funding networks. Canada bolsters the regional picture with generous R&D credits and pragmatic regulators who often coordinate with their US counterparts. The nanotechnology drug delivery market benefits here from predictable reimbursement systems that reward innovation while ensuring pharmacovigilance.

Europe maintains traction through Horizon Europe grants and national co-funding that knits academia and industry into translational pipelines. Germany’s chemical clusters supply excipients and surfactants, while the Benelux region offers clinical trial infrastructure. Together these attributes support a robust nanotechnology drug delivery market despite pricing pressure from centralized procurement.

Asia Pacific is the fastest-growing territory, posting a 12.54% CAGR that is reshaping supply chains. China anchors regional expansion by financing cGMP nano parks and rolling out supportive IP reforms, positioning itself as a cost-effective manufacturing hub. Japan’s materials science prowess advances lipid and polymer libraries, whereas South Korea’s conglomerates integrate device and drug development to shorten timelines. India targets global export markets with generic nano injectables. These developments collectively increase manufacturing velocity, lifting the overall nanotechnology drug delivery market.

Latin America and the Middle East currently post modest revenue but exhibit growing demand for advanced formulations that fit local disease burdens. Brazil and Saudi Arabia, for example, have signaled intent to localize vaccine and nano-therapeutic production, laying groundwork for future market growth.

Competitive Landscape

The competitive set spans global pharmaceutical majors, mid-sized biotech innovators, and early-stage start-ups. Larger companies wield experienced regulatory teams and global distribution, enabling them to run multi-center trials and launch across geographies. Smaller players differentiate through specialized carrier designs, quick iteration cycles, and academic collaborations.

Technology advantages revolve around scalable manufacturing and proven CMC packages. CDMOs with continuous nanoparticle mixers and inline PAT instrumentation command premium multipliers, as sponsors prefer de-risked supply. Patent filings around carbon nanostructure-based delivery systems hint at next-generation payload architectures. Bristol Myers Squibb’s partnership with Cellares shows how automation is being hard-wired into production to contain cost and reduce cycle times. Market entry barriers therefore grow steeper, guiding the nanotechnology drug delivery market toward a moderately consolidated future while still leaving room for breakthrough technologies to disrupt incumbent positions.

Nanotechnology Drug Delivery Industry Leaders

Pfizer

Bristol Myers Squibb

Novartis

Merck Co& Inc

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nanobiotix presented positive clinical trial outcomes for JNJ-1900 in pancreatic cancer treatment, underscoring the therapeutic promise of nano-enabled formulations in diseases with limited options.

- June 2024: Wacker Biotech completed its EUR 107 million mRNA competence center capable of producing over 200 million vaccine doses annually, boosting European preparedness for future outbreaks while expanding oncology capacity.

- February 2024: CPI’s RNA Centre of Excellence received GMP certification, becoming the United Kingdom’s only open-access site able to produce lipid-encapsulated mRNA for clinical trials and emergency response.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nanotechnology drug delivery market as all revenue generated from therapeutics whose active compound is carried, protected, or released by intentionally engineered materials between one and one hundred nanometers, including lipid nanoparticles, polymeric particles, dendrimers, micelles, nanocrystals, quantum dots, and related hybrid structures that reach systemic or localized circulation. These platforms must deliver an approved or clinical-stage pharmaceutical payload and exclude purely diagnostic nano-agents.

Scope exclusion: Formulations used solely for imaging, surface-coated medical devices, and generic macro-scale controlled-release drugs are outside our numbers.

Segmentation Overview

- By Technology

- Nanocrystals

- Polymeric Nanoparticles

- Lipid Nanoparticles / Liposomes

- Polymeric Micelles

- Dendrimers

- Quantum Dots

- Others

- By Application

- Oncology

- Neurology

- Cardiovascular

- Anti-inflammatory / Immunology

- Anti-infective

- Ophthalmology

- Others

- By Route of Administration

- Intravenous

- Oral

- Pulmonary

- Transdermal & Topical

- Others

- By End-user

- Pharmaceutical & Biotechnology Companies

- Contract Research & Manufacturing Organizations

- Hospitals & Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct interviews and short surveys with formulation scientists at multinational and mid-size pharma, regulatory reviewers, CMO business-development heads, and hospital pharmacists across North America, Europe, and key Asia-Pacific hubs. These discussions quantify real-world pricing spreads, scale-up yields, and expected indication launches that secondary data only hint at.

Desk Research

We begin with open datasets from regulators such as the US FDA, European EMA, and Japan's PMDA that list nano-enabled Investigational New Drug filings and approvals, followed by trade flows in UN Comtrade that reveal bulk lipid nanoparticle volumes. Academic literature indexed in PubMed and Web of Science supplies failure rates and dosage benchmarks, while national science agencies (for example, the US NSF Nano Initiative) offer funding signals. Company 10-Ks, investor decks, and press releases clarify commercialization timelines, and patent analytics from Questel plus news screening via Dow Jones Factiva help us map emerging modalities. This list is illustrative; many other public and paid sources were reviewed for corroboration.

Market-Sizing & Forecasting

A top-down build starts with country-level nano-therapy sales reported by regulators and customs, which are then adjusted for off-invoice rebates and clinical-trial supply. Results are cross-checked through selective bottom-up roll-ups of CMO lipid nanoparticle capacity, sampled average selling price times batch volumes, and pipeline progression ratios. Inputs that move the model most include: - number of approved nano-therapies and their weighted ASP per milligram - phase II/III trial counts and historic success probabilities - prevalence of target oncologic and gene-therapy cohorts - national R&D spending on nanomedicine - regulatory review turnaround times. Forecasts deploy a multivariate regression blended with scenario analysis that ties these drivers to macro health-spend trends; where supplier data are sparse, gap fills use conservative midpoint estimates vetted during expert calls.

Data Validation & Update Cycle

Outputs pass a multi-step peer review, anomaly screens against independent spend indices, and senior sign-off. We refresh models every twelve months, issuing rapid interim revisions when approvals, safety events, or currency swings shift fundamentals.

Why Mordor's Nanotechnology Drug Delivery Baseline stands apart

Published estimates vary because firms choose different payload scopes, assume divergent success rates, and refresh at unequal cadences.

Key gap drivers include whether diagnostics are bundled with therapeutics, how contract manufacturing revenue is treated, and the rigor of currency normalization before aggregating regional figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 109.14 Bn | Mordor Intelligence | - |

| USD 108.08 Bn | Regional Consultancy A | Includes diagnostic nano-agents and double-counts imaging contract work |

| USD 105.95 Bn | Global Consultancy B | Inflates 2024 values to 2025 without FX harmonization; omits CMO revenues |

| USD 107.65 Bn | Industry Association C | Applies a blanket 40 percent hospital markup instead of segment-specific ASP tracking |

Taken together, the comparison shows that Mordor's disciplined scope, dual-path modeling, and annual refresh create a transparent, repeatable baseline stakeholders can trust when sizing investments or benchmarking strategy.

Key Questions Answered in the Report

What is the current size of the nanotechnology drug delivery market?

The nanotechnology drug delivery market reached USD 119.89 billion in 2026 and is projected to climb to USD 191.88 billion by 2031.

Which technology segment leads revenue generation?

Lipid nanoparticles lead with 31.98% market share in 2025, owing to their proven performance in mRNA vaccines and adaptable chemistry.

Why is Asia Pacific the fastest-growing region?

Robust government funding, large-scale manufacturing investments, and expanding domestic demand are driving a 12.54% CAGR in Asia Pacific.

What application area is expanding most quickly?

Gene therapy and mRNA delivery are advancing at a 13.21% CAGR through 2031 as more clinical candidates enter late-stage trials.

How are contract manufacturing organizations influencing the market?

CDMOs provide specialized GMP capacity and advanced analytics, supporting a 12.22% CAGR in their segment as sponsors outsource complex production.

What remains the largest hurdle for broad adoption of nano-formulations?

High CMC and GMP compliance costs, alongside unresolved long-term toxicology questions, continue to raise development expenses and regulatory scrutiny.

Page last updated on: