Tissue Processing Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 418.20 Million |

| Market Size (2031) | USD 623.90 Million |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

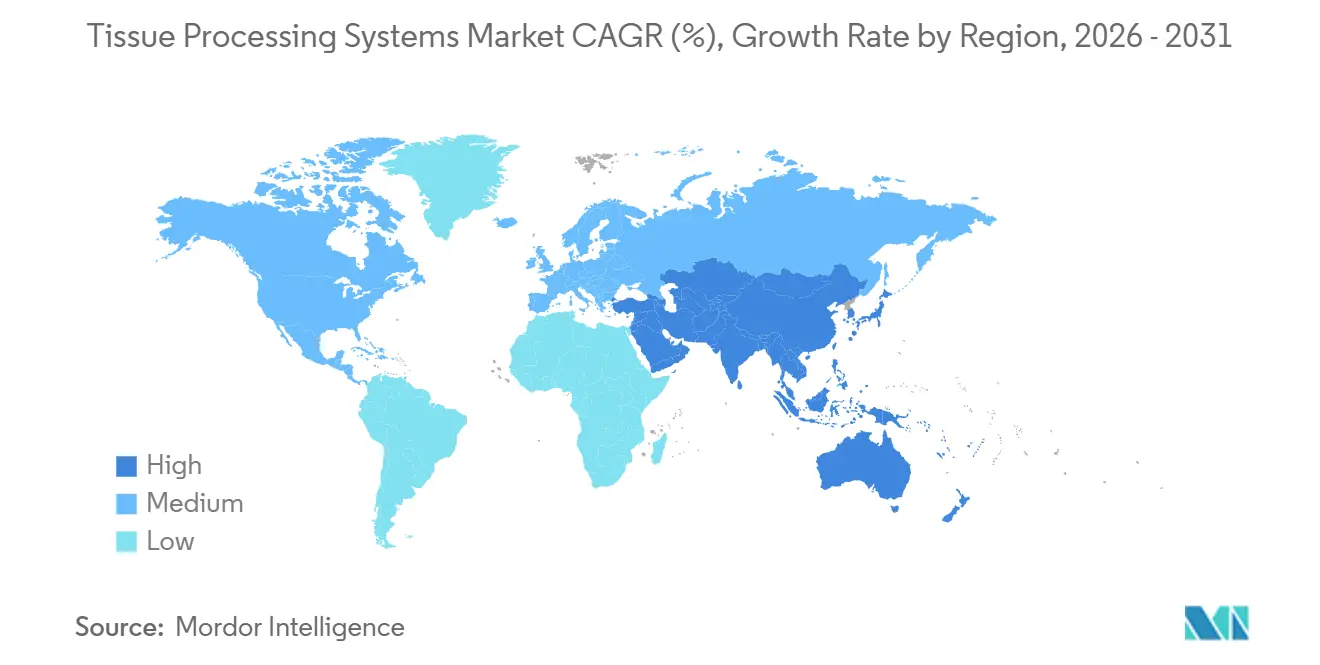

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Processing Systems Market Analysis by Mordor Intelligence

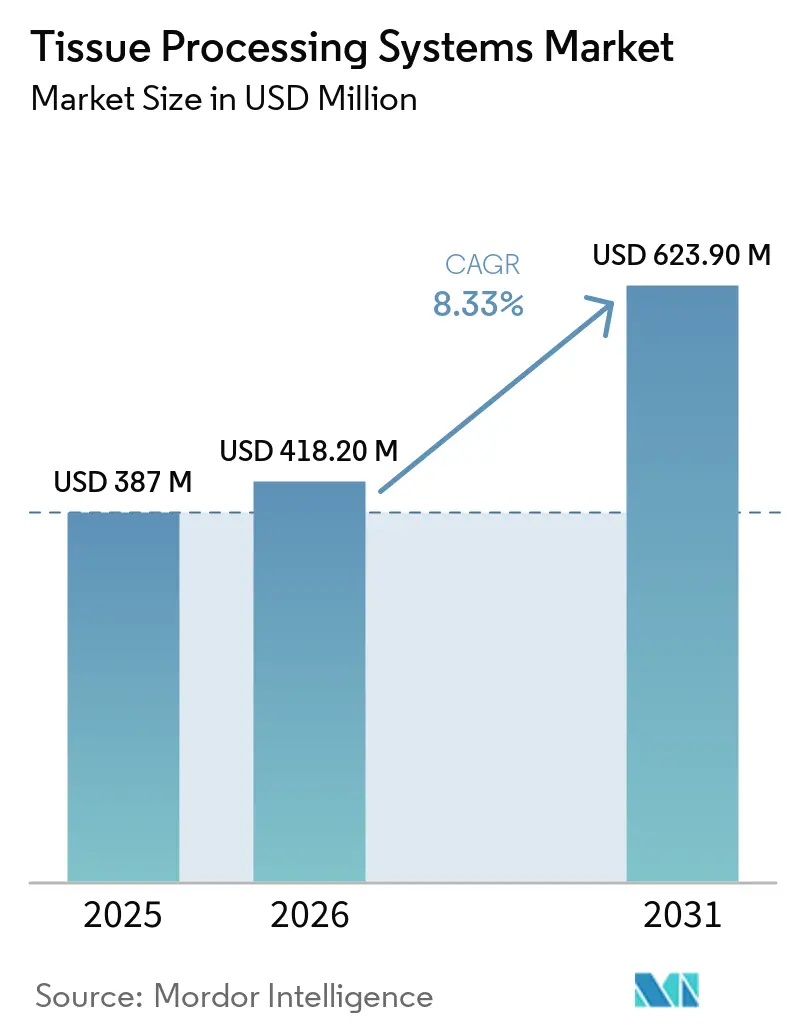

The Tissue Processing Systems Market size is expected to increase from USD 387 million in 2025 to USD 418.20 million in 2026 and reach USD 623.90 million by 2031, growing at a CAGR of 8.33% over 2026-2031.

Solid growth reflects three reinforcing factors. First, an expanding cancer burden is lifting global biopsy volumes, with the World Health Organization forecasting 30.5 million cases by 2050 [1]World Health Organization, “Cancer Fact Sheet,” WHO, who.int. Second, regulators are tightening turnaround-time and traceability rules, typified by the Centers for Medicare & Medicaid Services’ CLIA order QSO-25-10, which mandates electronic audit trails for every pre-analytical step. Third, hospital and reference-lab consolidation is concentrating procurement into multi-site tenders that favor fully integrated hardware and reagent bundles, accelerating equipment standardization across large fleets.

Key Report Takeaways

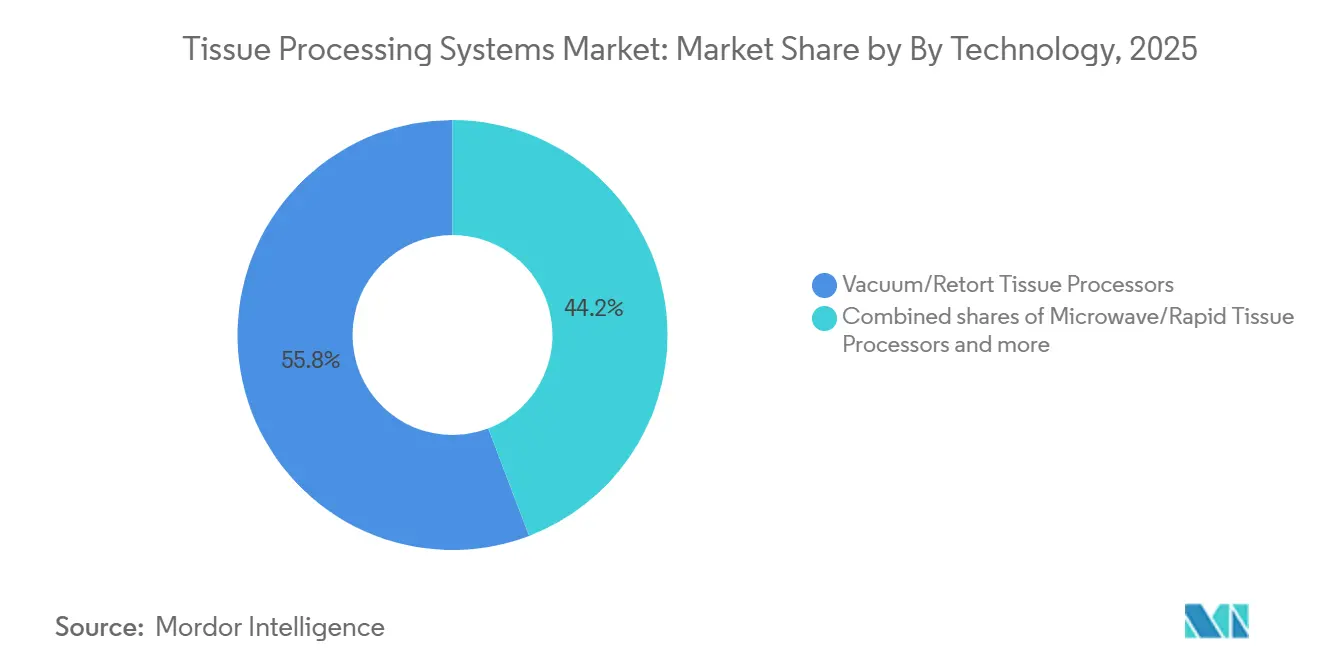

- By technology, vacuum or retort systems held 55.80% of the tissue processing systems market share in 2025, yet microwave or rapid systems are advancing at an 8.87% CAGR through 2031.

- By product, fully automated platforms led with 53.80% revenue share in 2025, while the same category is growing at an 8.68% CAGR.

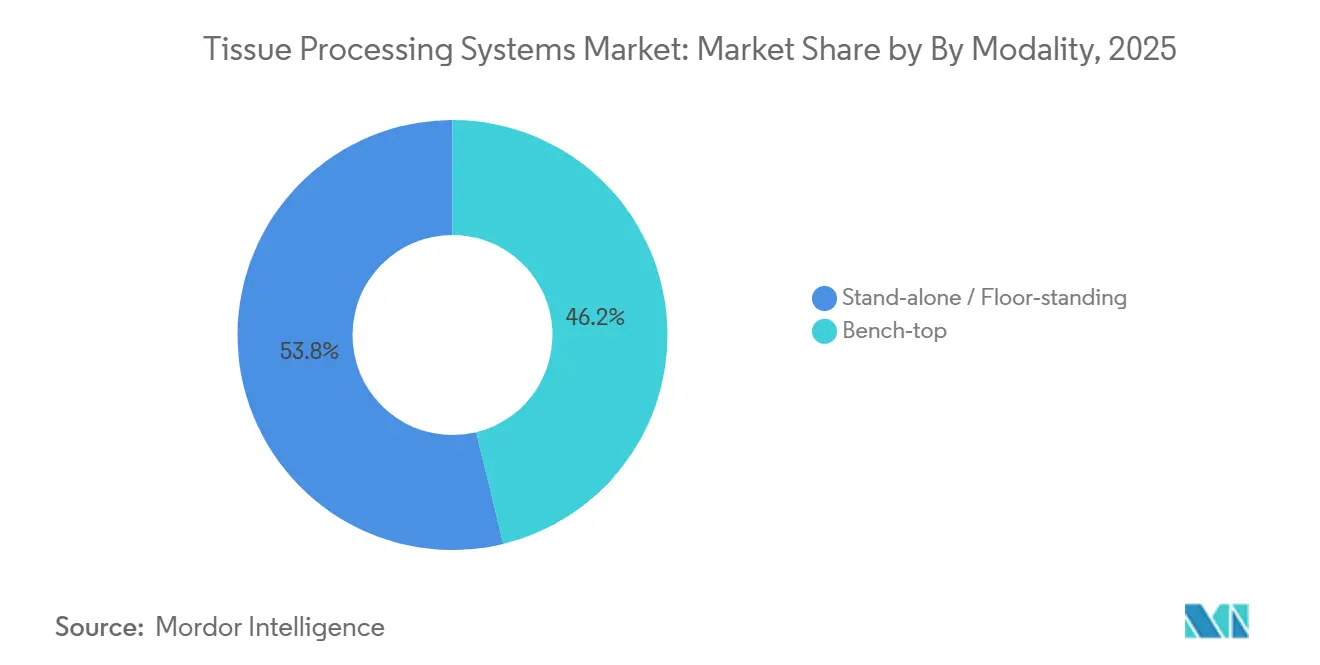

- By modality, stand-alone or floor-standing modalities commanded 53.80% of 2025 revenue and are expanding at an 8.81% CAGR.

- By end user, hospitals accounted for 43.18% of 2025 sales, yet diagnostic laboratories are forecast to post the highest growth at an 8.67% CAGR.

- By geography, North America contributed 38.19% in 2025, and Asia-Pacific is projected to grow at an 8.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tissue Processing Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cancer and chronic disease burden | +2.1% | Global, peak growth in APAC and aging OECD economies | Long term (≥ 4 years) |

| Push for lab automation and LIS integration | +1.8% | North America and Europe first, APAC following | Medium term (2-4 years) |

| Faster turnaround mandates | +1.5% | U.S., EU cancer centers, select APAC tertiary hospitals | Short term (≤ 2 years) |

| Xylene-free or formalin-reduced workflows | +1.2% | EU, North America, Australia-NZ | Medium term (2-4 years) |

| Dual-retort continuous-flow architectures | +0.9% | North American and EU reference labs, APAC mega-hospitals | Short term (≤ 2 years) |

| Multi-site consolidation and tendering | +0.7% | U.S. health systems, EU frameworks, Singapore and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer and Chronic Disease Burden Elevates Biopsy Volumes and Histology Workloads

The Global Burden of Disease Study estimated worldwide cancer incidence at 18.5 million cases in 2023 and projects a 65% increase to 30.5 million by 2050, thereby directly increasing cassette throughput in pathology laboratories [2]Institute for Health Metrics and Evaluation, “Global Burden of Disease Study 2023,” IHME, healthdata.org. Precision oncology protocols now demand three to five blocks per patient for biomarker panels such as PD-L1 or HER2, tripling work per case compared with hematoxylin-and-eosin-only routines. China’s clinical-trial ecosystem logged a 22% annual rise in oncology studies in 2024, with each trial generating 50-200 biopsies, prompting Beijing and Shanghai centers to install dual-retort processors that handle 300-400 cassettes per eight-hour shift. Across OECD markets, people older than 65 will account for 25% of the population by 2030, and this cohort already represents 60% of cancer diagnoses, stretching histology capacity. Serial-biopsy monitoring of inflammatory bowel and autoimmune liver disease added 12 million cases in 2025, raising utilization above 85% at many labs.

Push for Lab Automation and LIS/Digital Integration to Lift Throughput and Quality in Core Histology

Modern laboratory information systems orchestrate end-to-end specimen flow. Tissue processors now stream real-time temperature and reagent-consumption data via HL7 FHIR, feeding dashboards that predict maintenance windows and prompt just-in-time reagent restocks. In 2025, Agilent bundled its processors with digital pathology partners, cutting ID errors by 40% at Mayo Clinic’s two-million-slide operation. CMS order QSO-25-10 enforces electronic audit trails, obliging any Medicare-billing lab to retire isolated manual processors that lack connectivity. FlexLIS, launched in 2025, reroutes cassettes to under-used instruments and flags anomalies before embedding, slashing overall turnaround 30% at pilot sites.

Faster Turnaround Time Mandates Accelerate Rapid or Microwave Processor Adoption

Emergency departments and intraoperative suites need same-day answers. Microwave processors compress 12-hour cycles into 90 minutes without compromising antigen integrity for 95% of immunohistochemistry panels, as verified in multiple 2024-2025 validation papers [3]Journal Editorial Board, “Microwave Tissue Processing Validation,” Journal of Clinical Pathology, jcp.bmj.com. The U.K. National Health Service requires 75% of suspected-cancer patients to receive a confirmed diagnosis within 28 days, driving hospitals to place rapid processors near theaters. U.S. centers such as Johns Hopkins reduced reliance on frozen sections by 30% after installing dedicated microwave suites. Though microwave systems cost 40-60% more upfront, they allow departments to curb costly overnight staffing once routine blocks clear before evening shifts.

Shift to Xylene-Free or Formalin-Reduced Workflows to Meet Occupational-Health and Sustainability Targets

Xylene carries a permissible exposure limit of 100 ppm under OSHA, yet spot checks in community hospitals often exceed 150 ppm during reagent swaps, triggering ventilation upgrades priced at USD 200,000-500,000. Xylene-free substitutes such as d-limonene or aliphatic hydrocarbons eliminate that hazard and reduce waste-disposal costs 30-40%, because regulators classify them as non-hazardous. Leica’s HistoCore PEGASUS Plus, released in 2025, uses closed-system delivery that cuts airborne fumes by 90%. Procurement policy amplifies the effect; the U.K. NHS Anatomical Pathology Automation framework assigns 15% of scoring weight to green metrics. Cedarwood oil and supercritical CO₂ alternatives show equal staining quality for routine H&E and most antibodies, but still exhibit modest penetration due to higher cost and additional validation cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and lifecycle costs (service, reagents, downtime risk) constrain adoption | -1.4% | Global, most acute in price-sensitive emerging markets (South Asia, Sub-Saharan Africa, Latin America) | Medium term (2-4 years) |

| Shortage of skilled histotechnologists limits complex protocol utilization at scale | -1.1% | North America (15-20% vacancy rates), EU (aging workforce), select APAC markets (India, Southeast Asia) | Long term (≥ 4 years) |

| Regulatory and chemical-safety compliance adds validation/documentation burden | -0.8% | EU (REACH enforcement), North America (OSHA/CLIA), Australia/NZ (stringent OH&S frameworks) | Medium term (2-4 years) |

| Protocol validation hurdles for rapid/microwave on sensitive tissues/biomarkers | -0.6% | Global, particularly impacting academic medical centers and pharma/biotech CROs requiring molecular diagnostics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Costs Constrain Adoption

A modern dual-retort processor lists at USD 150,000-250,000, and annual service can add 15% of that figure. Medium-sized community hospitals face a 3- to 5-year payback period, while reimbursement for histopathology has remained flat since 2020. Refurbished units cut upfront costs but increase downtime risk because parts for seven-year-old platforms may take 6 weeks to source, an unacceptable delay for single-processor sites. Reagent lock-in deepens the bill: xylene-free chemistries from leading vendors cost 25% more than bulk xylene and cannot be cross-used on rival machines, removing competitive-bidding leverage. The NHS in Wales excluded processors from a GBP 34.4 million managed-service package in 2025, precisely to avoid volatile reagent escalations.

Shortage of Skilled Histotechnologists Limits Complex Protocol Uptake

The American Society for Clinical Pathology pegged U.S. histotechnologist vacancies at 15-20% in its 2024 survey. Microwave workflows require constant oversight to tune power and fixation by specimen type, yet many labs run with a single technologist per shift who already handles embedding and microtomy. 40% of U.S. staff will reach retirement age by 2030, threatening a brain drain of troubleshooting knowledge. India added more than 2,000 pathology labs from 2023-2025 but still lacks 15,000 trained technologists, forcing continued reliance on manual processors that trade throughput for easier operation. Each reagent or protocol swap triggers 30-60 days of validation, demanding scarce expert time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Vacuum Dominance Persists as Microwave Gains Momentum

Vacuum or retort processors delivered 55.80% of 2025 revenue, anchored by proven parity with xylene methods and overnight reliability. The tissue processing systems market size for this segment is advancing at a steady pace as refurb units cascade into smaller hospitals. Microwave systems are tracking an 8.87% CAGR because emergency departments want same-day answers and academic centers build rapid suites to cut frozen-section backlogs. Validation research confirmed 95% biomarker integrity after microwave cycles, easing earlier doubts about epitope loss.

Continuous-flow dual-retort architectures help vacuum systems stay relevant by shaving queue times and automating reagent swaps. Milestone’s EVO platform processes 400 cassettes per shift and supports xylene-free chemistries, narrowing the functional gap with microwave alternatives. Sakura’s VIP 6 AI adds viscosity monitoring, cutting reprocess rates by significantly. With histotechnologist overtime surpassing USD 50 per hour in many U.S. markets, the capital premium for microwave units can be offset within two years through labor savings.

By Product: Automation Drives Rapid Consolidation Toward Fully Integrated Platforms

Fully automated processors captured 53.80% of 2025 sales. The tissue processing systems market share advantage stems from integrated barcode tracking, predictive maintenance, and cloud dashboards that enable a single technologist to supervise multiple runs. CMS order QSO-25-10 accelerates that shift by forcing audit-trail capability for Medicare labs. Semi-automated units retain a foothold among mid-tier hospitals yet face erosion as secondary-market automated systems hit similar price points. Manual devices linger in veterinary and small research labs.

Epredia’s E1000 Dx processes 1,500 samples a day and uses RFID-based reagent management that automatically orders supplies when a 2-day supply is available, smoothing cash flow for high-volume reference labs. In Asia-Pacific, hospital chains equipping for medical-tourism accreditation install fully automated lines to satisfy College of American Pathologists benchmarks, helping the region outpace global growth. Robotic loaders, such as Sakura’s SmartConnect, reduce manual handling by 80%, which is vital in geographies with 20% vacancy rates.

By Modality: Bench-Top Units Win Space-Constrained Sites, Floor-Standing Systems Dominate Volume

Stand-alone floor units accounted for 53.80% of the 2025 value and grew at an 8.81% CAGR, as dual-retort models increase run capacity and slash per-cassette reagent costs through bulk tanks. Bench-top microwaves, though smaller in revenue, are expanding in dermatopathology clinics, where floor space costs USD 50-100 per square foot per year. NHS procurement in 2025 specified modular bench-top units for district hospitals, using distributed processing to shorten specimen transit and hit new 28-day cancer targets.

Leica’s HistoCore PEGASUS Plus floor system lowers fume exposure 90% with closed cartridges, satisfying strict EU occupational-health rules. Milestone’s EVO One bench-top processor needs only a 24-inch footprint yet handles 60 cassettes per cycle, enabling small clinics to in-source work previously outsourced at USD 8-12 per specimen. Modality choice now hinges on reagent-cost strategy; floor units use bulk stock that cuts per-cassette spend 25% while bench-tops trade higher consumable prices for zero waste on expired chemicals.

By End User: Diagnostic Laboratories Outpace Hospitals on Outsourcing Wave

Hospitals owned 43.18% of 2025 sales because intraoperative consultations must remain on-site. Still, diagnostic laboratories will post an 8.67% CAGR as health systems outsource routine blocks to regional hubs, illustrated by NHS Wales’ GBP 34.4 million managed-service deal in 2025. Research and academic institutes deploy dual-retort systems to meet stringent FDA or EMA trial documentation, while pharma or biotech firms expand in-house histology for biomarker discovery.

Diagnostic labs amortize equipment across 50,000-200,000 cassettes per year, compared with 10,000-30,000 in many hospitals, allowing them to price aggressively while still funding automation. Sakura’s SmartConnect robotics allows one technologist to run four processors, adding cost leverage. Hospitals retain an advantage in urgent STAT cases, yet rising labor costs push them toward hybrid models in which routine work is outsourced while high-acuity specimens remain on campus. Pharma users adopt xylene-free reagents faster due to corporate green targets and the absence of legacy workflows.

Geography Analysis

North America accounted for 38.19% of the 2025 value, with the United States accounting for nearly four-fifths. The region’s consolidation wave, typified by Labcorp’s May 2025 acquisition of Incyte diagnostics assets, is harmonizing protocols and negotiating reagent bulk discounts. CMS CLIA order QSO-25-10 forces full digital traceability, vaulting automation investment ahead of simple capacity gains. Leica partnered with Histofy in 2025 to embed predictive QC into HistoCore PEGASUS Plus, showing the region’s appetite for AI-driven analytics. Canada and Mexico lag because of lower per-capita spend and limited adoption outside academic centers. Persistent 15-20% technologist vacancies keep automation on the front burner.

Asia-Pacific is forecast to post an 8.59% CAGR to 2031, outpacing all other regions. China leads due to a 22% annual rise in oncology trials that demand high-throughput dual-retort systems. India’s private hospital chains install automated lines to attract international patients and secure College of American Pathologists stamps, yet staffing shortfalls slow protocol validation. Japan’s over-65 share will hit 35% by 2030, spurring demand, though reimbursement caps temper capital budgets. Australia and South Korea act as early adopters of xylene-free chemistries because procurement frameworks award 15% weight to environmental criteria.

Europe holds a diversified mid-tier position. The U.K. NHS Anatomical Pathology Automation framework, worth GBP 40 million over eight years, anchors large upgrades across England and Wales. Germany and France follow with university hospital investments, while Eastern Europe sees fresh capacity, as in MedLife’s USD 2.1 million automated lab opened in Romania in 2025. The Middle East and Africa cluster around centers of excellence such as Saudi Arabia’s King Faisal Specialist Hospital, which unveiled a USD 50 million AI-enabled lab in 2024. South America remains nascent; Brazilian and Argentine labs rarely surpass 5,000 cassettes a year, limiting automation ROI, though donor-funded projects in Ethiopia and the Gulf Cooperation Council bring select modern units to public labs.

Competitive Landscape

Leica Biosystems, Sakura Finetek, and Epredia jointly capture majority share, giving the tissue processing systems market a moderately concentrated profile. Each vendor fields full-line portfolios, from processors to embedding stations and proprietary reagents that lock users into consumable contracts for five-plus years. Competition revolves around three levers: exclusive xylene-free chemistries that command significant premiums over commodity xylene; digital pathology interoperability via HL7 FHIR and DICOM-WSI; and service bundles that convert capital outlay into leasing fees with uptime guarantees.

Agilent’s USD 950 million purchase of Biocare Medical in March 2026 brings 300 antibodies and slides the company into full control of the pathology workflow, threatening to commoditize stand-alone processor makers through reagent-equipment bundling. Leica’s September 2025 tie-up with Histofy injects AI that predicts protocol failure hours before run completion, lowering re-process rates 25%. Epredia’s FDA-cleared E1000 Dx embeds RFID reagent management that auto-orders supplies, winning multi-site reference labs who chase working-capital gains.

Smaller challengers target niches. Milestone’s bench-top microwave processors fit dermatopathology clinics with 50-150 cassettes per day. Diapath pushes xylene-free validation support, saving clients 30-60 days of trial work. Software-only newcomers bolt AI QC onto legacy fleets, carving recurring revenue without hardware replacement. The College of American Pathologists does not accredit brands but requires documented validation for any protocol change, effectively raising switching costs and insulating incumbents.

Tissue Processing Systems Industry Leaders

Leica Biosystems

Sakura Finetek USA, Inc

Epredia

MEDITE Medical GmbH

Bio-Optica Milano S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Agilent Technologies announced a USD 950 million purchase of Biocare Medical to integrate antibodies and digital pathology into its tissue workflow.

- February 2026: Epredia partnered with Mindpeak to add AI QC to its digital pathology suite across the EU.

- February 2026: Leica Biosystems launched the CM1950 cryostat with RFID tracking that meshes with HistoCore PEGASUS Plus data streams.

Global Tissue Processing Systems Market Report Scope

As per the scope of the report, a tissue processing system is an automated laboratory instrument used in histopathology to prepare biological tissue specimens for microscopic examination. These systems automate the sequential steps required to preserve cellular structure and morphology, transforming fresh samples into stable blocks suitable for thin sectioning.

The tissue processing systems market is segmented by technology, product, modality, end users, and geography. By technology, the market is segmented into vacuum/retort tissue processors, microwave/rapid tissue processors, and others. By product, the market is segmented into fully automated, semi‑automated, and manual. By modality, the market is segmented into stand‑alone / floor‑standing and bench‑top. By end users, the market is segmented into hospitals, diagnostic laboratories, research & academic institutes, and pharma/biotech & CRO. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Vacuum/Retort Tissue Processors |

| Microwave/Rapid Tissue Processors |

| Other |

| Fully Automated |

| Semi‑automated |

| Manual |

| Stand‑alone / Floor‑standing |

| Bench‑top |

| Hospitals |

| Diagnostic Laboratories |

| Research & Academic Institutes |

| Pharma/Biotech & CRO |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Vacuum/Retort Tissue Processors | |

| Microwave/Rapid Tissue Processors | ||

| Other | ||

| By Product | Fully Automated | |

| Semi‑automated | ||

| Manual | ||

| By Modality | Stand‑alone / Floor‑standing | |

| Bench‑top | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Research & Academic Institutes | ||

| Pharma/Biotech & CRO | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the tissue processing systems market in 2031?

The market is expected to reach USD 623.9 million by 2031, reflecting an 8.33% CAGR over 2026-2031.

Which technology is growing fastest within tissue processors?

Microwave or rapid systems are expanding at an 8.87% CAGR in 2025, due to same-day biopsy protocols in emergency and oncology centers.

Why are fully automated tissue processors gaining share?

They integrate barcode tracking and predictive maintenance, which eases staffing shortages and meets new CLIA electronic audit requirements.

Which region is forecast to grow quickest?

Asia-Pacific is projected to post an 8.59% CAGR through 2031, led by China’s booming oncology trial activity and India’s hospital build-out.

Page last updated on: