Nanocomposites In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 11.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

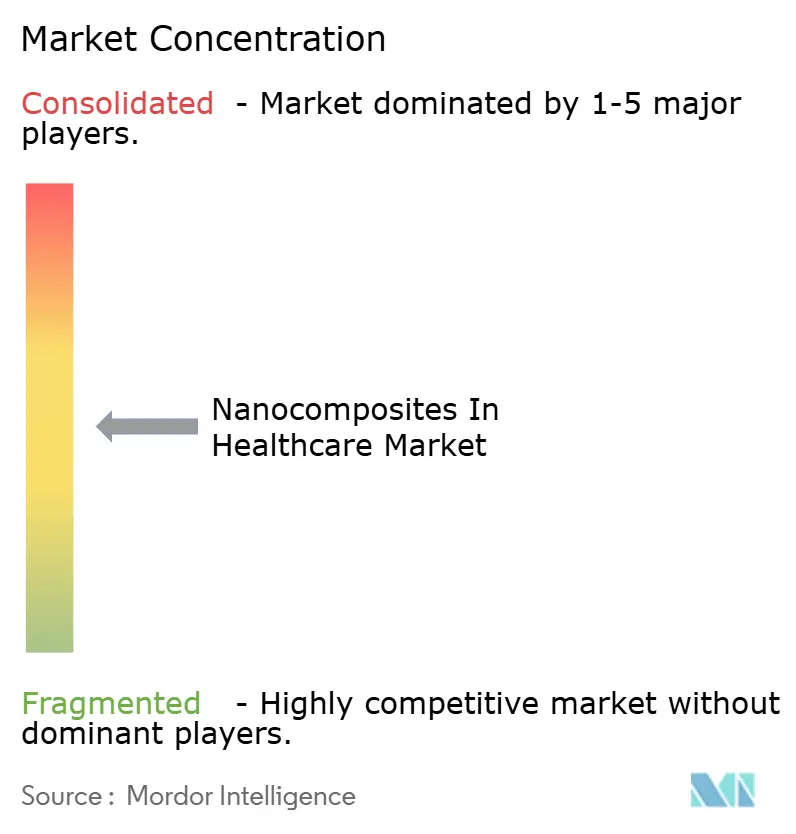

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nanocomposites In Healthcare Market Analysis by Mordor Intelligence

The Nanocomposites In Healthcare Market size is projected to be USD 1.19 billion in 2025, USD 1.33 billion in 2026, and reach USD 2.29 billion by 2031, growing at a CAGR of 11.55% from 2026 to 2031.

The market is being shaped by tighter hospital-acquired infection control protocols, wider clinical use of precision drug delivery systems, and material science progress that is replacing conventional biomedical polymers with multifunctional nanocomposite platforms. The nanocomposites in healthcare market also benefits from aging populations and rising rates of chronic musculoskeletal disorders, cancer, and metabolic disease, which are widening the base for implant, diagnostic, and therapeutic use cases. Its position between advanced materials science and clinical medicine gives the nanocomposites in healthcare market broad demand support, but it also places the market under some of the toughest qualification and validation standards in the healthcare value chain. Competitive activity in the nanocomposites in healthcare market remains moderate to high because large specialty material suppliers compete with smaller nanomaterial specialists that move faster in product development, even if they still operate at a smaller commercial scale. The nanocomposites in healthcare market also faces slower commercialization when laboratory proof of concept must move through case-by-case regulatory review, and that friction is made harder by input cost volatility for high-purity carbon nanotubes and specialty ceramic nanopowders.

Key Report Takeaways

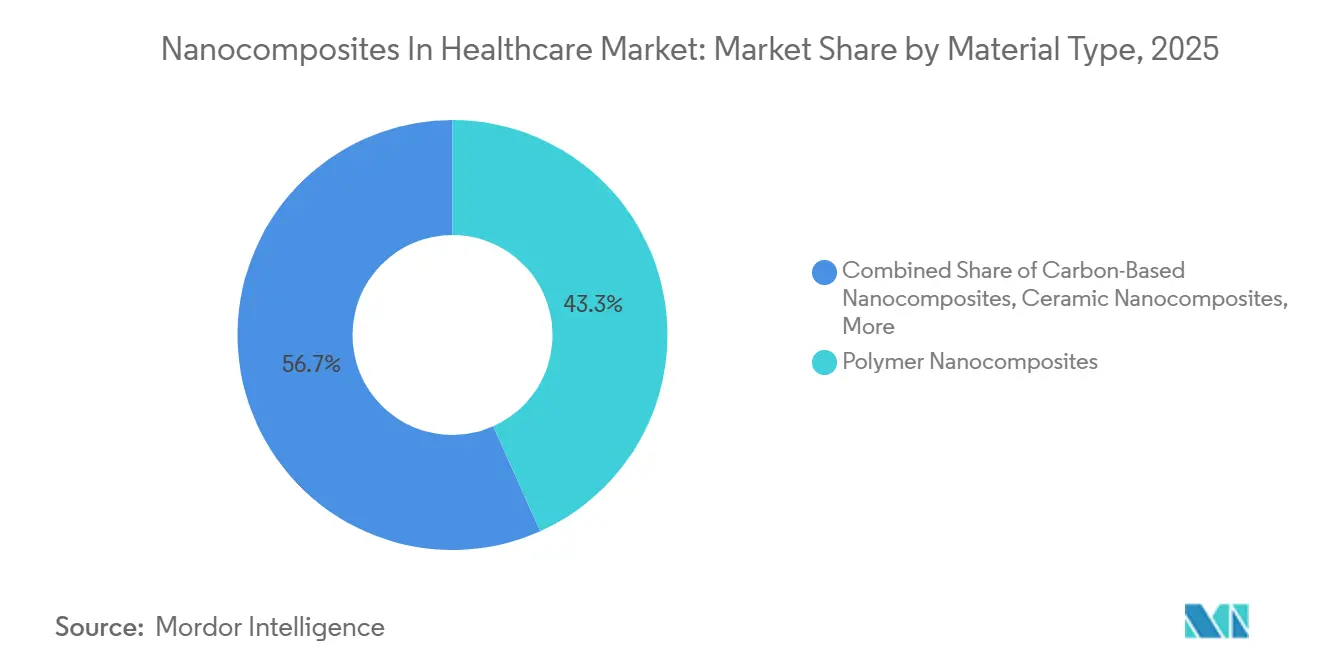

- By material type, polymer nanocomposites held 43.31% of revenue in 2025, while carbon-based nanocomposites are projected to advance at a 12.38% CAGR through 2031.

- By application, medical implants and prosthetics accounted for 32.24% of revenue in 2025, while tissue engineering and regenerative medicine is forecast to grow at a 14.52% CAGR through 2031.

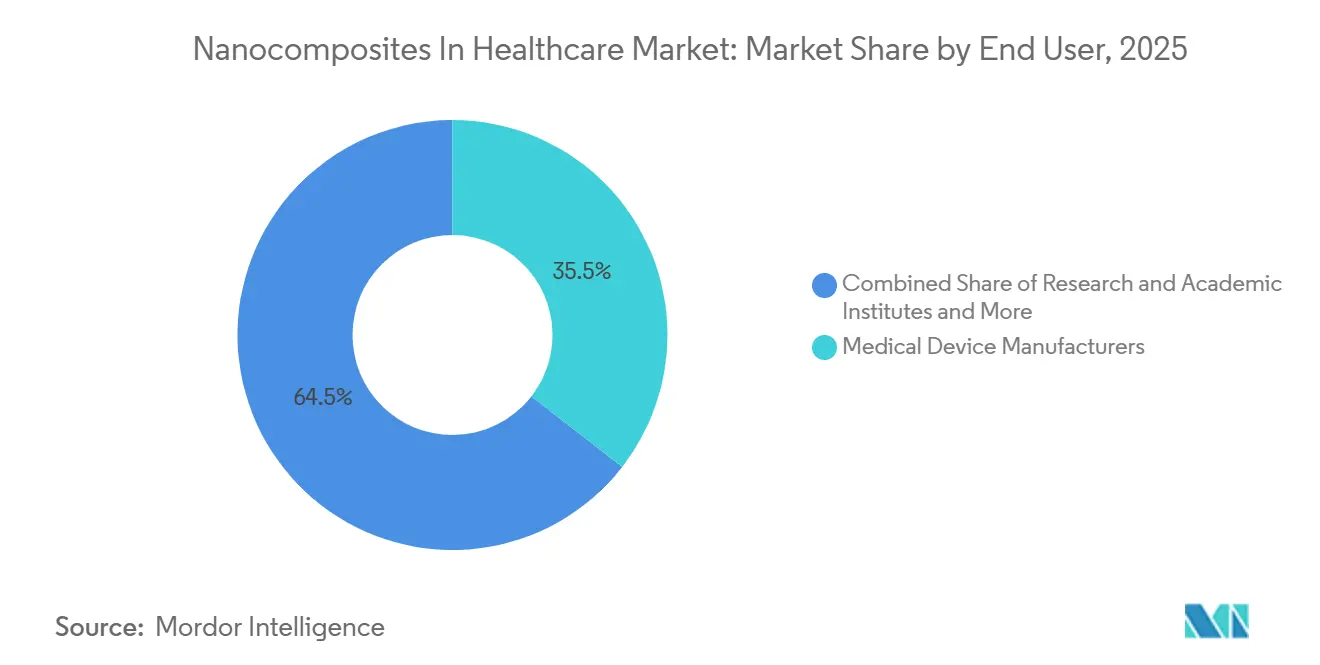

- By end user, medical device manufacturers held 35.52% of the nanocomposites in healthcare market share in 2025, while research and academic institutes are projected to expand at a 12.25% CAGR through 2031.

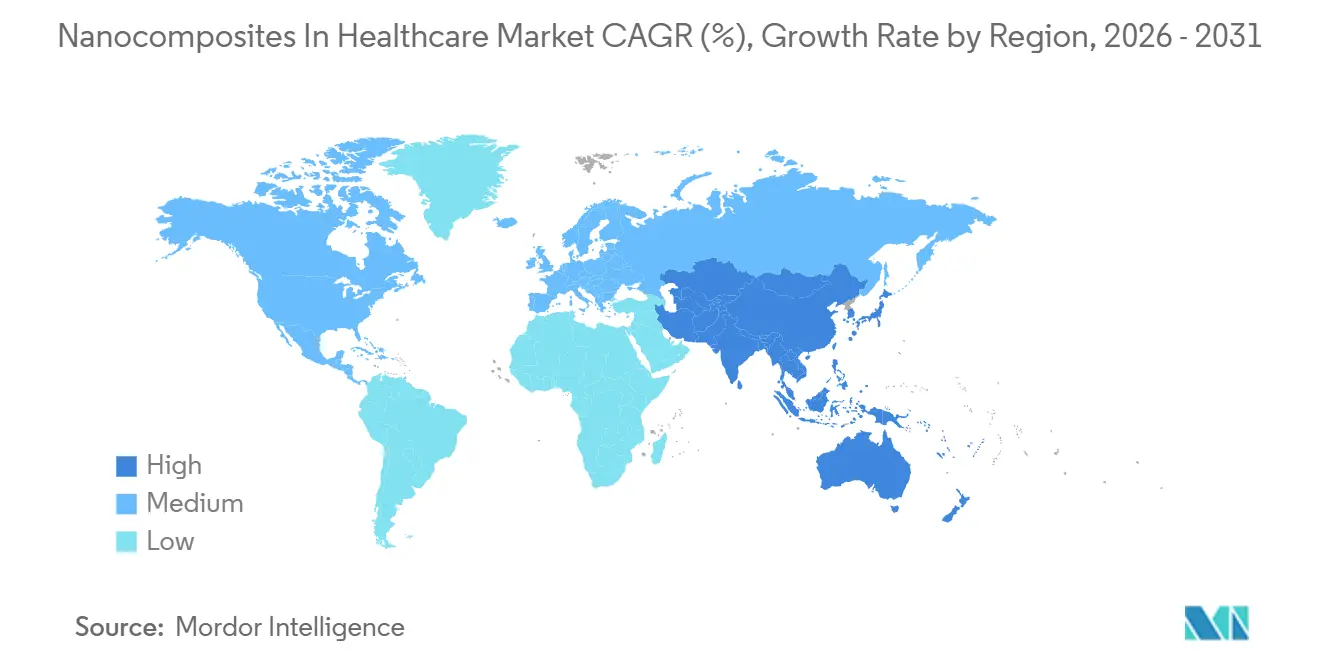

- By geography, North America held 35.22% of revenue in 2025, while Asia-Pacific is expected to grow at a 12.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nanocomposites In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Use Of Antimicrobial Nanocomposite Coatings In Medical Devices | +1.8% | Global, with concentrated near-term gains in North America and Western Europe | Medium term (2-4 years) |

| Demand For Lightweight, High-Strength Materials In Implants And Wearables | +1.5% | Global, with high activity in North America, EU, and APAC medtech hubs | Medium term (2-4 years) |

| Growth In Precision Drug Delivery And Targeted Therapeutics | +2.1% | Global, APAC and North America leading clinical adoption | Long term (≥ 4 years) |

| Expansion Of Biosensors And Point-Of-Care Diagnostics | +1.7% | Global, with fastest growth in Asia-Pacific and Middle East emerging healthcare markets | Medium term (2-4 years) |

| Rising Hospital Focus On Infection Control And Surface Functionalization | +1.3% | North America and EU core, with spillover to GCC and South Korea | Short term (≤ 2 years) |

| Scale-Up Of Biocompatible Polymer And Hybrid Nanocomposite Platforms | +1.4% | Global, North America and EU currently lead, APAC accelerating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Use of Antimicrobial Nanocomposite Coatings in Medical Devices

The nanocomposites in healthcare market is seeing stronger demand for antimicrobial device coatings because prosthetic joint infections affected 1% to 3% of total joint replacement procedures and represented 13% to 31% of all revision surgeries in 2025. Silver nanoparticle multilayer coatings on titanium alloy and cobalt-chromium-molybdenum implant surfaces showed strong antibacterial activity against Staphylococcus aureus and Pseudomonas aeruginosa while maintaining in vivo biocompatibility after 3 months, with higher microvessel density and no systemic inflammatory response. Boron nitride nanosheet reinforced chitosan coatings on magnesium implants also showed suppression of biofilm formation without creating antimicrobial resistance, which gives antibiotic-free infection management a more credible clinical route. Pressure to reduce hospital-acquired infections is also pushing the nanocomposites in healthcare market toward smart catheter coatings that release antimicrobials in response to bacterial pH shifts, which changes procurement expectations for urological and vascular devices. This shift matters because the nanocomposites in healthcare market is moving from passive surface protection to dynamic infection control, and recent work on biofilm-related device challenges supports that change in design direction[1]“Advances in Nanotechnology for Addressing Biofilm-Related Challenges in Medical Devices,” Nanotechnology, iopscience.iop.org.

Demand for Lightweight, High-Strength Materials in Implants and Wearables

The nanocomposites in healthcare market is also benefiting from the need for implant materials that can better balance tissue-like compliance with long-term mechanical strength. Ti-based nanocomposites that combine hydroxyapatite and nanostructured titania showed better corrosion resistance, stronger osseointegration potential, and measurable antimicrobial performance, which means they solve multiple clinical problems at the same time. PLA and nano-hydroxyapatite composite coatings made through green electrospinning on titanium created a bioactive nanofibrous surface for bone regeneration, and the work confirmed successful filler integration and controlled degradation behavior. In wearables, carbon composites and nanostructured hydrogels are improving sensor conformability and biocompatibility, while machine learning is increasingly being layered onto those sensing systems for continuous chronic disease monitoring. The nanocomposites in healthcare market is likely to keep attracting development spending here because the mismatch between existing implant materials and natural tissue stiffness remains unresolved, especially at cartilage and neural interfaces.

Growth in Precision Drug Delivery and Targeted Therapeutics

The nanocomposites in healthcare market has some of its strongest translational momentum in drug delivery because conventional delivery systems often fail to reach the required local concentration without systemic toxicity. PLGA-based multifunctional nanosystems have moved furthest in commercialization, and several FDA-approved formulations created a regulatory base for later submissions, with Doxil standing as a recognized example of efficacy and toxicity reduction through nanocomposite-enabled delivery. Polydopamine-based nanocomposite hydrogels with nanoparticle drug carriers also achieved multistage controlled release in bone defect repair, which improved drug stability and local therapeutic concentration beyond what passive systems can deliver. The nanocomposites in healthcare market still faces a key translation barrier because the protein corona effect can change targeting efficiency in vivo in ways that in vitro tests do not predict well. That makes regulatory review more demanding, and it helps explain why oncology remains the main clinical focus while wound care, central nervous system disease, and metabolic disease still represent open space for future nanocomposite delivery platforms.

Expansion of Biosensors and Point-of-Care Diagnostics

The nanocomposites in healthcare market is gaining support from biosensors because nanocomposite platforms are pushing point-of-care diagnostics toward laboratory-grade sensitivity. Metal nanocomposite and microfluidic hybrid systems have demonstrated very high detection capability, and MXene-gold nanoparticle sensor designs enabled point-of-care monitoring of multiple serum biomarkers at clinically relevant precision. Field-effect transistor platforms with nanocomposite bio-interfaces reached attomolar detection for endometrial cancer biomarkers HE4 and CA125 directly in unprocessed serum, and the architecture has already been adapted into a portable point-of-care prototype. Graphene oxide and conductive polymer biosensors are also addressing biofouling, which was a major reason many earlier point-of-care systems struggled in real biological samples. Even so, the nanocomposites in healthcare market still meets a compliance gap here because FDA De Novo and 510(k) pathways do not yet sit alongside standardized ISO protocols that are specific to nanocomposite functionalized sensing surfaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of GMP-Grade Manufacturing And Dispersion Control | -1.5% | Global, most severe for clinical-stage SMEs in North America and Europe | Short term (≤ 2 years) to Medium term (2-4 years) |

| Regulatory Uncertainty Around Nanotoxicology And Long-Term Biocompatibility | -1.9% | Global, EU and US most affected due to high regulatory scrutiny under MDR Rule 19 and FDA guidance | Long term (≥ 4 years) |

| Limited Clinical Evidence And Slow Translation From Lab To Device Approval | -1.2% | Global, most pronounced in Asia-Pacific markets where regulatory harmonization with FDA and EMA is incomplete | Long term (≥ 4 years) |

| Reproducibility Challenges Across Batches And Sterilization Cycles | -0.8% | Global, disproportionate impact on polymer and hybrid nanocomposite platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of GMP-Grade Manufacturing and Dispersion Control

The nanocomposites in healthcare market continues to face a cost barrier because GMP-compliant production requires much more than successful lab synthesis. Batch-to-batch variability at the nanoscale demands extensive in-process analytical monitoring to satisfy quality system requirements under 21 CFR 820 and comparable EU quality management standards. Small differences in particle size or drug loading can force deficiency letters and rework because protocols that work in lab-scale nanoprecipitation or emulsification often do not translate directly to commercial equipment. Silver nanoparticle integration into polymer matrices shows the problem clearly because agglomeration lowers antimicrobial performance, while high silver use and chemical reducing agents raise purification complexity and unit cost. This makes the nanocomposites in healthcare market harder for smaller clinical-stage companies to scale because GMP qualification can add 12 to 24 months to product development programs.

Regulatory Uncertainty Around Nanotoxicology and Long-Term Biocompatibility

The nanocomposites in healthcare market also moves more slowly because neither the United States nor the European Union offers a dedicated nanomedicine approval pathway. The FDA still reviews nanomaterial-containing drugs under existing frameworks and relies on guidance such as the 2022 document on drug products that contain nanomaterials, which provides structure but not full procedural certainty for portfolio planning[2]U.S. Food and Drug Administration, “Drug Products, Including Biological Products, That Contain Nanomaterials, Guidance for Industry,” U.S. Food and Drug Administration, fda.gov. In Europe, MDR 2017/745 Rule 19 classifies nanomaterial-containing devices by exposure potential into Class IIa, IIb, or III, but harmonized nanotoxicology testing standards are still not aligned across member states. Developers also have to characterize long-term in vivo behavior such as protein corona dynamics, complement activation risk, and biodistribution in organs like the liver, spleen, and kidney, and those methods are still not standardized. The result is that the nanocomposites in healthcare market carries both scientific uncertainty and regulatory uncertainty at the same time, especially for early-stage companies working under Quality by Design expectations tied to critical quality attributes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymer Dominance Anchors Market, Carbon Platforms Accelerate

Polymer nanocomposites accounted for 43.31% of the nanocomposites in healthcare market share in 2025, which kept them in the leading material position. That lead came from long clinical use of biocompatible polymer matrices such as PLGA, PEEK, polycaprolactone, and chitosan. The nanocomposites in healthcare market still favors polymers because these materials have a stronger body of peer-reviewed evidence and clearer FDA precedent across approved products. Silver nanoparticle based polymer nanocomposites also kept attracting interest in wound care, medical coatings, and tissue engineering, and recent work on green synthesis improved control over particle morphology and matrix dispersion. Carbon-based nanocomposites are projected to grow at a 12.38% CAGR from 2026 to 2031, making them the fastest-growing material category in the nanocomposites in healthcare market.

That momentum reflects the fact that carbon nanotube and graphene derivatives combine electrical conductivity with structural reinforcement, which is increasingly important in neural scaffolds, bone cements, and electrochemical biosensors. Research from JAIST showed that graphene oxide and bacterial component hybrid nanocomposites produced synergistic photothermo-chemo-immunotherapy outcomes in cancer models, which broadened the value of carbon platforms beyond structural roles alone[3]Soudamini Sai Vimala Veera Chintalapati and Eijiro Miyako, “Hybrid Nanoarchitectonics with Bacterial Component-Integrated Graphene Oxide for Cancer Photothermo-Chemo-Immunotherapy,” Carbon, jaist.ac.jp. Metal oxide nanocomposites remain concentrated in antimicrobial surface functionalization and imaging contrast use, while ceramic nanocomposites serve load-bearing orthopedic and dental applications where polymers cannot meet the same mechanical threshold. Hybrid and multifunctional nanocomposites are becoming more important because the nanocomposites in healthcare market increasingly values platforms that can sense, deliver, and support tissue within a single design. EU MDR compliance and ISO 10993 biocompatibility requirements also strengthen the position of polymer and ceramic systems that already carry better characterized safety data packages.

By Application: Implant Scale Masks Regenerative Medicine's Rapid Emergence

Medical implants and prosthetics accounted for 32.24% of the nanocomposites in healthcare market size in 2025, which made them the largest application area. This position came from high global volumes in orthopedic and dental procedures and from the long-standing use of nanocomposite coatings to improve osseointegration, reduce infection risk, and control corrosion. Drug delivery systems and diagnostic devices and biosensors followed as the next largest application areas, with drug delivery gaining share as nanocomposite lipid nanoparticle and polymer-based systems move through clinical development in oncology and infectious disease. Wound care and antimicrobial dressings also benefited from hospital infection control spending, and chitosan-zinc oxide nanocomposite dressings together with self-healing nanocomposite hydrogels already showed commercial and clinical-stage validation. Tissue engineering and regenerative medicine is projected to grow at a 14.52% CAGR through 2031, making it the fastest-rising application in the nanocomposites in healthcare market.

This split between the largest segment and the fastest-growing one shows that the nanocomposites in healthcare market still depends on implants for present revenue, even as regenerative medicine builds the next wave of demand. A 2026 review on polymeric nanocomposites for tissue engineering highlighted AI-based scaffold design, clinical-use collagen nerve conduits, and stimuli-responsive 4D nanocomposites as major near-term enablers for this application area. Carbon nanotube reinforced hydroxyapatite and silk fibroin scaffolds for bone repair, along with electrospun PCL and carbon nanotube nerve conduits, also demonstrated functional recovery with clear translational potential. Other applications such as dental restorative materials, ophthalmic devices, and cardiovascular stent coatings remain at an earlier stage, but they are expected to gain more weight after 2028 as their regulatory dossiers mature. That leaves the nanocomposites in healthcare market with a broad application pipeline, but one that still commercializes at different speeds by clinical use case.

By End User: Device Manufacturers Lead, Research Activity Drives the Innovation Pipeline

Medical device manufacturers held 35.52% of the nanocomposites in healthcare market share in 2025, which kept them as the largest end-user group. Their role as the main integrators of nanocomposite materials into FDA- and CE-marked finished products means they largely determine which material categories reach commercial production scale. For suppliers in the nanocomposites in healthcare market, qualification with this customer group remains a core strategic requirement because approved device platforms create durable procurement relationships. Pharmaceutical and biotechnology companies represented the second-largest end-user base, supported by investment in nanocomposite-enabled drug delivery for oncology, vaccines, infectious disease, and gene therapy. Hospitals and clinics also matter as active end users in wound care and infection control, but their purchases often move through group purchasing organization models rather than direct long-term supplier contracts.

Research and academic institutes are projected to grow at a 12.25% CAGR through 2031, which makes them the fastest-growing end-user segment in the nanocomposites in healthcare market. That figure matters because it signals that discovery-stage work is still expanding and will continue feeding the future device and therapeutics pipeline. The Chinese Academy of Sciences held 23,400 nanopatents as of 2025 and stood as the largest global patent holder by organization, while biomedicine remained one of 4 main focus domains in China’s nanotechnology white paper. Hokkaido University researchers also developed a photoresponsive nanocomposite platform for peri-implantitis treatment in 2024 that combined minocycline, hyaluronan, and carbon nanohorns for sustained antimicrobial action from a single administration. Other end users include veterinary medical device manufacturers and CDMOs, both of which are gradually expanding their capabilities in response to pipeline demand from the broader nanocomposites in healthcare market.

Geography Analysis

North America held 35.22% of the nanocomposites in healthcare market share in 2025, which made it the largest regional market. The region benefits from mature regulatory systems, a dense base of medical device manufacturers, strong specialty material supply, and high spending on implantable devices and advanced diagnostics. The United States also provides relatively established review pathways for nanocomposite-containing devices and drug products through 510(k), PMA, and other existing routes, even though review standards remain demanding. DuPont’s February 2026 launch of the Liveo C6-8XX USP Class VI liquid silicone rubber series for healthcare applications points to continued commercial activity in North American medical materials. DuPont’s April 2026 launch of Liveo Pharma TPE Overmolded Assemblies for biopharmaceutical fluid handling adds to that pattern and shows active product positioning across adjacent healthcare manufacturing needs.

Europe held the second-largest share in the nanocomposites in healthcare market in 2025. Germany, the United Kingdom, and France remain the key demand centers because they combine academic research strength, a large orthopedic and cardiovascular device base, and rising compliance investment under EU MDR. BASF expanded its Ultrason portfolio in March 2026 with the biomass-balanced PPSU grade Ultrason P 3010 BMB for medical technology, which shows that sustainability criteria are beginning to influence high-performance medical material decisions in the region. Europe also stands out because Rule 19 compliance is forcing upstream qualification spending faster than in many other regions, which raises near-term cost but also increases future entry barriers. The rest of Europe, including Scandinavia and Eastern European medtech hubs, is gaining gradual importance as manufacturing capacity broadens beyond the traditional Western European base.

Asia-Pacific is projected to grow at a 12.65% CAGR from 2026 to 2031, making it the fastest-growing regional segment in the nanocomposites in healthcare market. China, Japan, South Korea, and India are the main growth contributors. China’s nanotechnology strategy has already translated into 43% of global nanopatents, with biomedicine listed as a priority domain, and that is helping build a more local supply ecosystem for nanocomposite intermediates. Japan’s academic and industry pipeline is also advanced, and JAIST researchers reported bacterial-adjuvant liquid metal nanocomposites for photothermal cancer immunotherapy in 2025 with complete tumor elimination in murine colorectal cancer models after a single near-infrared irradiation cycle. India and South Korea continue to develop as complementary growth markets, while the Middle East and Africa and South America remain earlier-stage regions where demand is more concentrated in wound care, infection control, and drug delivery channels.

Competitive Landscape

The nanocomposites in healthcare market is moderately fragmented, with large specialty chemical and biomaterial groups such as BASF, Evonik, DuPont, Arkema, and Cabot competing alongside smaller nanomaterial specialists such as Nanocyl, Nanophase Technologies, PlasmaChem, ZyVex Technologies, and NanoSonic. The larger companies bring scale, broader platform portfolios, and stronger regulatory experience. The smaller firms compete more on focused formulation capability and faster innovation cycles. This creates a two-speed structure in the nanocomposites in healthcare market, where scale advantages and technical agility do not always sit with the same suppliers.

A clear strategy pattern in the nanocomposites in healthcare market is the move toward compliance-ready medical grades, tighter control over nanoparticle supply, and co-development partnerships with clinical-stage customers. Evonik’s Endexo additive technology is a useful example because it is positioned as a surface-modifying additive that helps reduce thrombosis, bacterial adhesion, and biofouling across catheters, stents, and connectors without forcing customers to redesign their entire production process. DuPont has also continued investing in the Liveo biomaterial portfolio for implants, drug delivery, and biopharmaceutical processing, which supports a strategy built on compliance-grade materials rather than commodity competition. BASF’s 2026 Ultrason expansion shows another strategic direction, where medical-grade performance is being paired with sustainability positioning for OEM customers. These moves show that the nanocomposites in healthcare market is not competing only on raw material properties, because commercial success also depends on qualification risk, documentation quality, and fit with existing manufacturing lines.

Technology also plays a direct role in differentiation across the nanocomposites in healthcare market. AI-assisted scaffold design, microfluidic nanoparticle synthesis, and process analytical tools for real-time monitoring are helping both large and small companies strengthen their manufacturing quality arguments. White-space opportunity remains strongest in ceramic and hybrid nanocomposites for regenerative medicine and in nanocomposite-functionalized biosensor surfaces for point-of-care diagnostics, because neither area has a single company with a dominant application-specific position today. ISO 13485 and ISO 10993 compliance increasingly works as a competitive filter, since companies with existing biocompatibility data packages can move through new customer development cycles faster. That means the nanocomposites in healthcare market still looks fragmented on the surface, but the practical ability to convert technical promise into approved medical use is concentrated among suppliers with stronger regulatory and manufacturing depth.

Nanocomposites In Healthcare Industry Leaders

Arkema Group

Evonik Industries AG

Cabot Corporation

Nanocyl SA

Showa Denko Materials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BASF introduced Ultrason P 3010 BMB, a biomass-balanced polyphenylsulfone (PPSU) grade with 20% bio-circular feedstock attribution, certified under ISCC PLUS, for medical technology and other high-performance applications. The move positions BASF to meet growing sustainability specifications from medical device OEMs while retaining full material performance.

- February 2026: DuPont launched the Liveo C6-8XX Liquid Silicone Rubber (LSR) series, a USP Class VI range of medical-grade, two-part silicone elastomers in 30 to 70 Shore A hardness, supporting medical device applications including non-implant and short-term implant healthcare components with validated biocompatibility.

Global Nanocomposites In Healthcare Market Report Scope

As per the scope of the report, nanocomposites in healthcare are materials composed of a matrix (such as a polymer, ceramic, or metal) integrated with nanoscale reinforcements or fillers, typically less than 100 nanometers in size. These nanomaterials enhance the properties of the composite, such as strength, biocompatibility, antimicrobial activity, and controlled drug release. In healthcare, nanocomposites are used in various applications including drug delivery systems, tissue engineering, medical implants, and diagnostic devices.

The segmentation for the nanocomposites in healthcare market is categorized by material type, application, end user, and geography. By material type, the market includes polymer nanocomposites, carbon-based nanocomposites, metal oxide nanocomposites, ceramic nanocomposites, and hybrid and multifunctional nanocomposites. By application, it covers medical implants and prosthetics, drug delivery systems, wound care and antimicrobial dressings, diagnostic devices and biosensors, tissue engineering and regenerative medicine, and other applications. By end user, the segmentation includes medical device manufacturers, pharmaceutical and biotechnology companies, hospitals and clinics, research and academic institutes, and other end users. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Polymer Nanocomposites |

| Carbon-Based Nanocomposites |

| Metal Oxide Nanocomposites |

| Ceramic Nanocomposites |

| Hybrid and Multifunctional Nanocomposites |

| Medical Implants and Prosthetics |

| Drug Delivery Systems |

| Wound Care and Antimicrobial Dressings |

| Diagnostic Devices and Biosensors |

| Tissue Engineering and Regenerative Medicine |

| Other Applications |

| Medical Device Manufacturers |

| Pharmaceutical and Biotechnology Companies |

| Hospitals and Clinics |

| Research and Academic Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Polymer Nanocomposites | |

| Carbon-Based Nanocomposites | ||

| Metal Oxide Nanocomposites | ||

| Ceramic Nanocomposites | ||

| Hybrid and Multifunctional Nanocomposites | ||

| By Application | Medical Implants and Prosthetics | |

| Drug Delivery Systems | ||

| Wound Care and Antimicrobial Dressings | ||

| Diagnostic Devices and Biosensors | ||

| Tissue Engineering and Regenerative Medicine | ||

| Other Applications | ||

| By End User | Medical Device Manufacturers | |

| Pharmaceutical and Biotechnology Companies | ||

| Hospitals and Clinics | ||

| Research and Academic Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and future size of nanocomposites in healthcare?

The nanocomposites in healthcare market is valued at USD 1.33 billion in 2026 and is projected to reach USD 2.29 billion by 2031 at a CAGR of 11.55%.

Which material type leads this space today?

Polymer nanocomposites led with a 43.31% share in 2025 because of stronger clinical validation, better regulatory precedent, and broad use across implants, coatings, and delivery systems.

Which application is growing the fastest through 2031?

Tissue engineering and regenerative medicine is the fastest-growing application, with a projected CAGR of 14.52% from 2026 to 2031.

Which end users matter most for commercial adoption?

Medical device manufacturers held the largest end-user share at 35.52% in 2025, while research and academic institutes are expanding fastest at 12.25% CAGR through 2031.

Which region leads demand and which one is growing fastest?

North America led with 35.22% share in 2025, while Asia-Pacific is forecast to record the fastest growth at a 12.65% CAGR through 2031.

What is the biggest challenge slowing broader adoption?

High GMP manufacturing cost, dispersion control issues, and regulatory uncertainty around nanotoxicology and long-term biocompatibility remain the main barriers to faster scale-up.

Page last updated on: