Topical Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 134.27 Billion |

| Market Size (2031) | USD 186.42 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

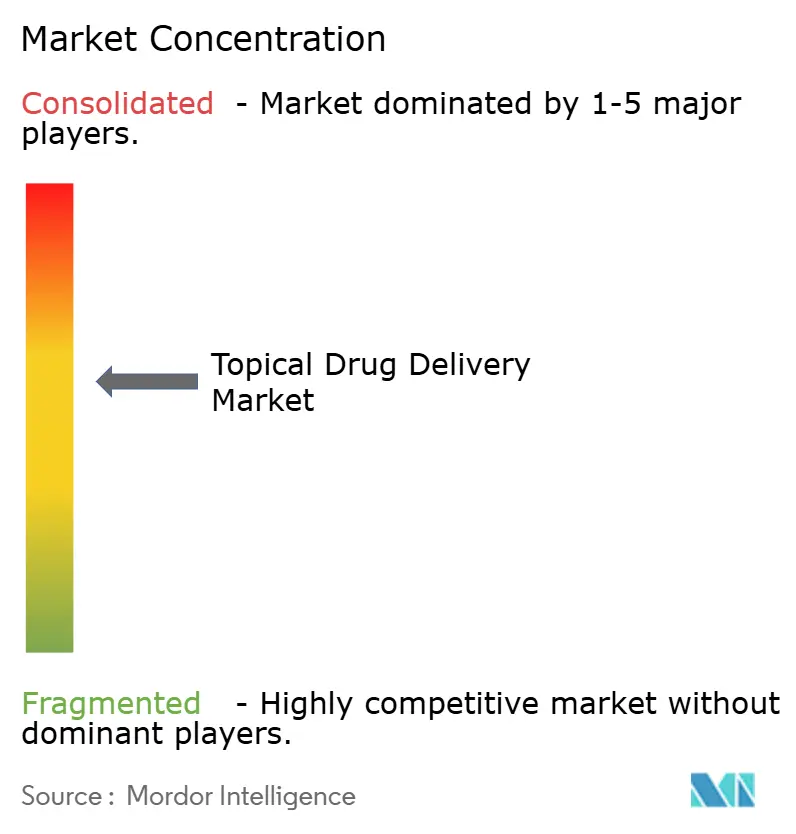

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Topical Drug Delivery Market Analysis by Mordor Intelligence

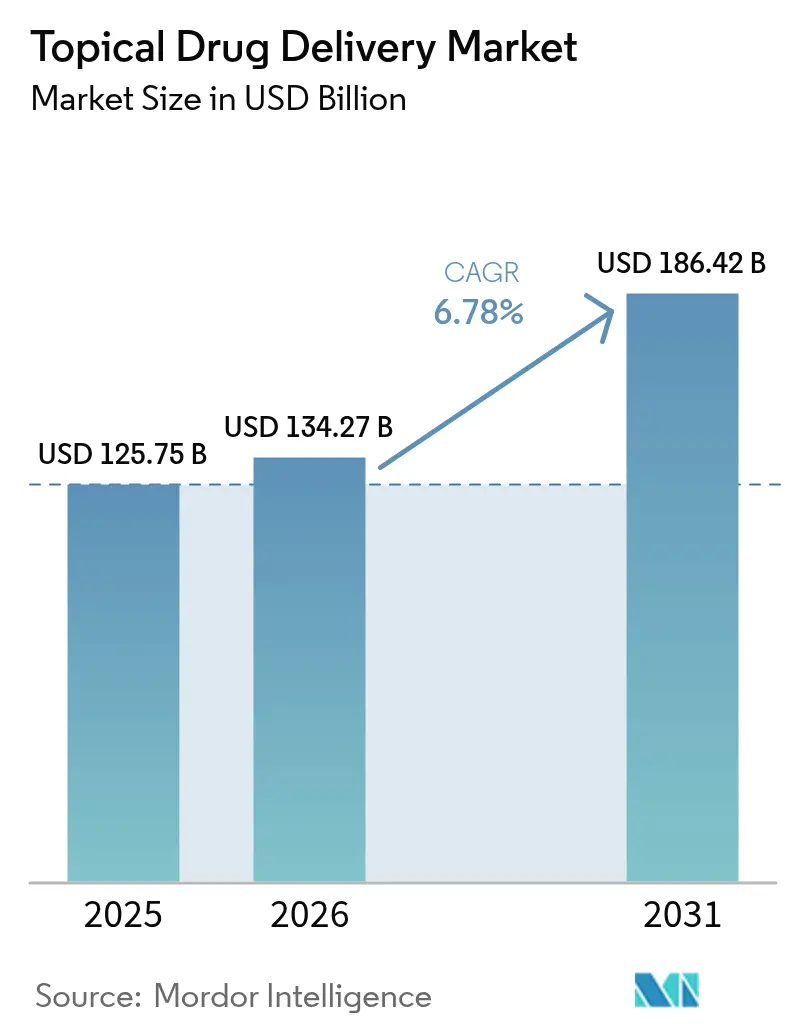

The topical drug delivery market size in 2026 is estimated at USD 134.27 billion, growing from 2025 value of USD 125.75 billion with 2031 projections showing USD 186.42 billion, growing at 6.78% CAGR over 2026-2031. This expansion reflects the shift from conventional creams and ointments toward precision-engineered patches, microneedle arrays, and smart, sensor-enabled devices that improve dosing accuracy and treatment adherence. Strong demand for non-invasive chronic-disease therapies, regulatory support for non-opioid pain solutions, and rapid progress in biologic formulations collectively sustain momentum. Companies also benefit from the steady launch pace of targeted dermatology drugs and the broadening role of connected health ecosystems that allow clinicians to monitor patient compliance remotely. Against this backdrop, the topical drug delivery market continues to attract both large pharmaceutical manufacturers and agile biotechnology firms that specialize in delivery platforms.

Key Report Takeaways

- By route of administration, dermal delivery led with 44.71% of topical drug delivery market share in 2025, while nasal delivery is projected to advance at a 9.12% CAGR through 2031.

- By product, traditional formulations accounted for 70.45% of topical drug delivery market size in 2025, whereas the devices segment is expanding at an 8.07% CAGR to 2031.

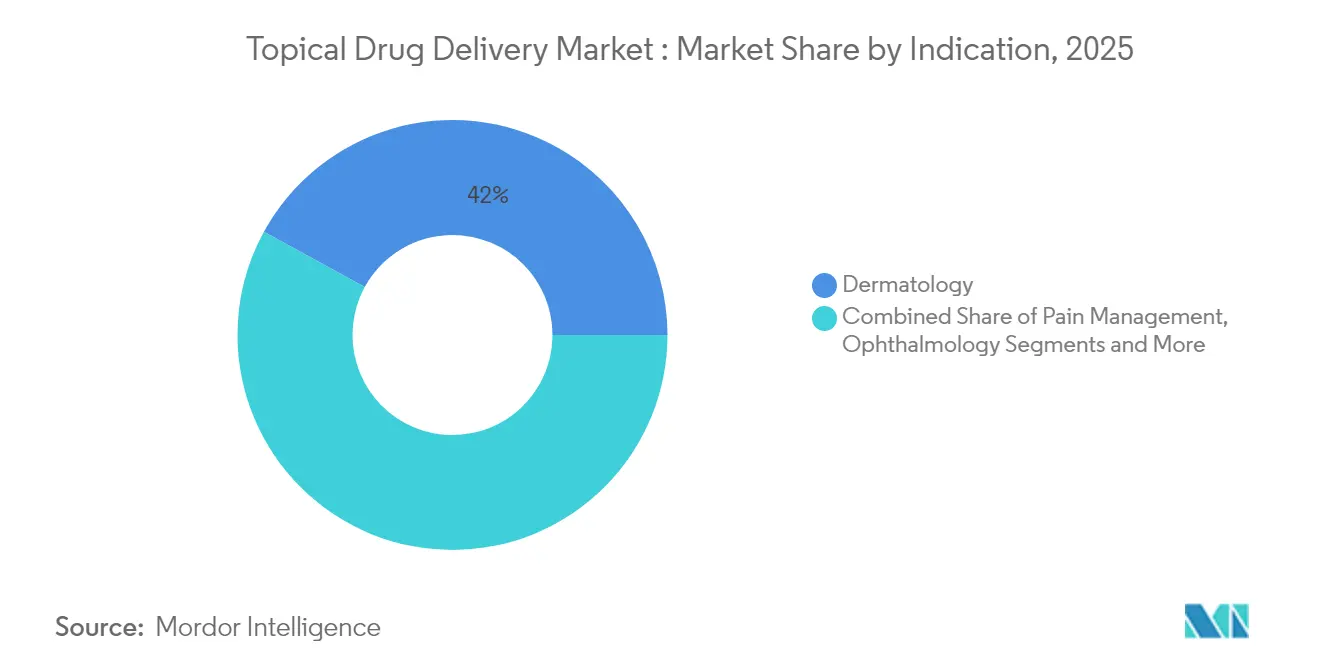

- By indication, dermatology dominated with 42.03% revenue share in 2025; pain management is set to rise at a 9.94% CAGR between 2026-2031.

- By end-user, hospitals held 35.02% of topical drug delivery market share in 2025, but the home-care segment is growing the fastest at a 8.96% CAGR.

- By geography, North America commanded 38.31% of topical drug delivery market share in 2025, while Asia-Pacific is expected to record the highest regional CAGR of 9.18% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Topical Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence Of Chronic & Infectious Skin Diseases | +1.2% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption Of Transdermal Patches In Pain & Hormone Therapy | +1.8% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Rising Geriatric Population | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Demand For Self-Administration & Home-Care–Friendly Formats | +1.5% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Polymeric Microneedle Breakthroughs Enabling Large-Molecule Delivery | +0.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Smart/Connected Patches Driving Longitudinal Dosing Compliance | +0.7% | North America & developed APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High prevalence of chronic & infectious skin diseases

Chronic skin disorders such as psoriasis and atopic dermatitis remain among the ten most common health conditions worldwide. Psoriasis alone affected more than 40 million people in 2024, spurring steady prescription growth for topical biologics. Galderma’s Nemluvio, approved in December 2024, demonstrated superior itch reduction in trials with 1,900 patients, underscoring how IL-31 antagonists reshape moderate-to-severe atopic dermatitis management. Artificial-intelligence skin-mapping tools now guide personalized regimens, while multimodal vision models trained on two million images boost diagnostic accuracy in clinics.[1]Siyuan Yan, “A Multimodal Vision Foundation Model for Clinical Dermatology,” Nature Medicine, nature.com Together, epidemiologic pressure and technology convergence position chronic-disease care as a long-duration growth engine for the topical drug delivery market.

Rapid adoption of transdermal patches in pain & hormone therapy

The United States Food and Drug Administration cleared Journavx (suzetrigine) in January 2025 as the first non-opioid patch indicated for moderate to severe acute pain.[2]Office of the Commissioner, “FDA Approves Novel Non-Opioid Treatment for Moderate to Severe Acute Pain,” U.S. Food and Drug Administration, fda.gov The decision signals regulatory willingness to back novel, non-addictive analgesics. In hormone therapy, Bayer’s elinzanetant New Drug Application targets vasomotor symptoms for the 1.2 billion global menopausal population anticipated by 2030. New adhesive chemistries such as Medherant’s TEPI platform deliver uniform doses over extended wear periods, driving patient preference for patches over oral regimens. As a result, transdermal modalities continue to capture share within the broader topical drug delivery market.

Rising geriatric population

Older adults tend to favor simple, non-invasive options that limit systemic exposure and drug-drug interactions. Dissolving microneedle patches now compensate for age-related dermal thinning, improving absorption of large molecules. Sensor-integrated bandages capable of streaming wound-healing data to clinicians illustrate how electronic textiles extend remote monitoring and support independent living. As populations age across North America, Europe, Japan, and China, geriatric care needs reinforce the long-term demand curve for the topical drug delivery market.

Demand for self-administration & home-care-friendly formats

Healthcare systems encourage at-home therapy to relieve clinic capacity constraints and cut costs. Smartphone-enabled Spatiotemporal On-Demand Patches let users time their own doses while supplying adherence data to providers. Home-care already shows the highest end-user CAGR in the topical drug delivery market, supported by rapid deployment of Bluetooth-equipped wearables that pair with telehealth platforms. Roll-to-roll manufacturing lowers production costs for smart patches, paving the way for personalized packaging at pharmacy level.[3]Khasha Ghaffarzadeh, “Pilot Factory for Roll-to-Roll Processing of Next-Generation Smart Wearable Patches,” Wevolver, wevolver.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Price Controls On Topical Corticosteroids | -0.8% | Global, with higher impact in Europe & emerging markets | Medium term (2-4 years) |

| Frequent Contamination-Driven Product Recalls & Warning Letters | -0.6% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Limited Skin Permeation Of Biologics Without Enhancers | -0.4% | Global, affecting premium product segments | Long term (≥ 4 years) |

| ESG-Driven Phase-Out Of Petrolatum Bases In Europe | -0.3% | Europe primary, with spillover to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent global price controls on topical corticosteroids

Many governments have tightened reference pricing schemes, compressing margins on mainstream corticosteroid products and restricting cash flow available for novel delivery research. Patent expiries in 2025 for several branded formulations further intensify low-price competition, particularly in high-volume emerging markets. Suppliers are forced to re-engineer cost structures even as complex biologic pipelines demand higher R&D investment, creating a squeeze that could moderate growth in certain segments of the topical drug delivery market.

Frequent contamination-driven product recalls & warning letters

Current Good Manufacturing Practice lapses led the FDA to issue several warning letters in 2024-2025, including notices to Chem-Tech and AnuMed International for sterility violations. Endo USA’s late-2024 recall of Adrenalin Chloride Solution illustrates how quality breaches interrupt supply and erode patient confidence. Although manufacturers with robust systems may capture share, the broader market faces near-term drag from compliance costs and supply disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Dermal leadership under pressure from nasal acceleration

Dermal deliveries captured 44.71% of topical drug delivery market share in 2025, reflecting broad clinical familiarity and patient comfort. The topical drug delivery market size attached to dermal routes is forecast to expand steadily as biologics and smart patches penetrate dermatology and systemic indications. Nasal delivery, however, is registering the fastest 9.12% CAGR to 2031 as intranasal sprays for migraine, respiratory infections, and neurologic rescue therapy gain traction. A growing pipeline of antisense oligonucleotides formulated for the nasal cavity demonstrates commercial enthusiasm. Digital health integration now extends to dermal routes through sensor-equipped patches that relay dose records to electronic health records, while connected inhalers offer similar feedback loops for pulmonary applications. Ophthalmic therapy benefits from preservative-free multi-dose bottles that reduce ocular surface damage, and pulmonary devices leverage vibrating mesh technology to improve deep-lung deposition.

The convergence of microneedles with nasal and dermal platforms is widening access to large molecules. Smart interfaces guide users through app-based tutorials, lowering administration errors. Meanwhile, rectal and oral-mucosal routes maintain niche relevance for palliative care and buccal vaccine delivery, respectively. Across all pathways, formulation scientists increasingly employ permeation enhancers, nanoemulsions, and in situ gels to meet dosing targets without compromising safety. This broad toolbox strengthens each route’s ability to address emerging clinical needs, reinforcing the long-term diversification of the topical drug delivery market.

By Product: Formulations dominate while devices inject pace

Traditional creams, gels, lotions, and sprays represented 70.45% of topical drug delivery market size in 2025. Their entrenched physician acceptance and manufacturing scale keep volumes high. Semi-solids such as foams are popular with patients who prefer quick absorption, whereas liquids thrive in ophthalmology and nasal care where metered-dose applicators enhance accuracy. Solid films and powders remain small but essential for on-the-go wound care and pediatric dosing.

The devices category—comprising patches, microneedle arrays, smart bandages, and drug-eluting dressings—shows an 8.07% CAGR and is the clear momentum play. Solventum’s V.A.C. Peel and Place system lowered hospital-labor time by 61% and treatment costs by 41% during clinical rollout. Programmable microneedle patches for weight-management agents such as Semaglutide demonstrate that devices can unlock monthly dosing cycles impossible with traditional creams. As electronics costs fall and flexible circuits mature, hybrid “formulation-plus-device” products blur category boundaries, adding value through monitoring and data capture.

By Indication: Dermatology still rules but pain management gains speed

Dermatologic disorders anchored 42.03% of 2025 revenue thanks to high prevalence and continuous new-product flow. The segment benefits from biologics that treat atopic dermatitis, psoriasis, and vitiligo more effectively than older steroids. Pain management, advancing at a 9.94% CAGR, is propelled by urgent demand for non-opioid options such as suzetrigine patches. Ophthalmology grows on the back of innovations like netarsudil mesylate for glaucoma, while respiratory care leverages nanosuspension inhalers to cut corticosteroid dose requirements. Hormone replacement remains a sizable opportunity as menopause treatments move toward once-daily or weekly transdermal regimens. Central nervous system disorders and metabolic diseases populate the pipeline, indicating further diversification of clinical indications addressed by the topical drug delivery industry.

By End-User: Hospital volume holds, home-care races ahead

Hospitals accounted for 35.02% of topical drug delivery market share in 2025, reflecting complex cases that require physician supervision, especially for biologic infusions and advanced wound therapies. Specialty clinics concentrate on dermatology and pain medicine, using AI-driven imaging to tailor therapy plans and document outcomes. The home-care channel, expanding at 8.96% CAGR, benefits from telehealth reimbursement and rising comfort with self-treatment devices. Bluetooth-enabled patches transmit adherence logs, allowing clinicians to intervene remotely before non-compliance escalates. Pharmacies and ambulatory surgical centers round out distribution, stocking both mass-market generics and high-value specialty kits.

Geography Analysis

North America maintained a 38.31% revenue share in 2025, backed by deep R&D pipelines, high healthcare expenditure per capita, and fast regulatory turnarounds for break-through devices. The United States drives patch adoption through value-based reimbursement that rewards fewer hospital visits. Canada shows strong demand for biosimilar creams within its single-payer scheme, while Mexico’s private-sector clinics increasingly stock smart dressings for diabetic ulcer care.

Asia-Pacific shows the fastest 9.18% CAGR, even as venture funding fell 22% in 2024. China funds domestic microneedle startups and supports large-scale GMP plants that supply domestic and export demand. Japan faces accelerated aging, boosting sales of easy-to-apply analgesic patches. India’s respiratory portfolio, led by Cipla, expanded 17.9% year over year and demonstrates rising domestic appetite for specialty devices. South Korea approved Rhopressa ophthalmic solution to address rising glaucoma prevalence, while Australia promotes remote monitoring solutions for rural patients.

Europe registers steady growth and leads in sustainability legislation, prompting rapid petrolatum replacement in Germany and the Nordic region. France and the United Kingdom pilot AI-linked dermatology networks that feed real-world evidence to regulators. Eastern Europe grows off a lower base but exhibits strong demand for generics, making it a target for contract manufacturers operating within the topical drug delivery industry. South America and the Middle East & Africa remain smaller today but represent future upside as healthcare infrastructure matures and digital-health connectivity widens.

Regulatory Landscape

In the United States, generic approvals for complex topical semisolids and liquids are being shaped by the FDA final guidance on Physicochemical and Structural (Q3) Characterization of Topical Drug Products Submitted in ANDAs, published in March 2026. The guidance sets out how applicants characterize formulation microstructure (including rheology and phase behavior) and positions Q3 as part of an integrated bioequivalence package alongside in vitro release testing (IVRT) and in vitro permeation testing (IVPT), which raises the analytical bar for topical generics.

For topical drug delivery products that incorporate device elements, such as transdermal patches, microneedle arrays, and connected dressings, compliance expectations increasingly cover both drug and device quality systems. The FDA Quality Management System Regulation (QMSR), effective February 2, 2026, further aligns device quality requirements with ISO 13485:2016, which is relevant for manufacturers and suppliers supporting combination products that combine topical formulations with delivery hardware and electronics.

Value Chain Analysis

The topical drug delivery value chain connects API and excipient suppliers, including polymers, lipids, and adhesive chemistries, with specialized equipment providers for semi-solid handling and high-shear mixing. Formulation developers then convert actives into creams, gels, sprays, or patch-compatible matrices. CDMOs and device-focused manufacturing partners support scale-up, analytical method development, and GMP production, while contract packaging organizations enable unit-dose and child-resistant formats. 3PL and wholesalers handle cold-chain or controlled storage where required.

As device-led formats gain share, value is shifting toward partners that can integrate drug, adhesive, and device engineering under regulated quality systems. Recent collaboration patterns reflect this: Raphas partnered with Hosokawa Micron (July 2026) on microneedle-patch production using biodegradable polymer nanocomposite encapsulation, and Praxis Precision Medicines and Remagine Labs (July 2026) announced a collaboration and license agreement focused on an iontophoretic transdermal patch approach. On the generics side, the FDA March 2026 Q3 guidance increases demand for advanced characterization and performance testing (IVRT/IVPT), reinforcing the role of analytically capable CDMOs in moving development through to ANDA submissions.

Competitive Landscape

The field is moderately fragmented. Large multinationals such as Johnson & Johnson, Galderma, and Bayer retain breadth across indications, while specialists like Medherant and MC10 focus on delivery hardware. Galderma’s Nemluvio, projected to exceed USD 2 billion in annual sales, showcases the payoff when biologic innovation aligns with topical formats. Johnson & Johnson’s TAR-200 device reported 83.5% complete response in bladder-cancer trials, signifying growing cross-indication use of controlled-release platforms.

M&A activity centers on technology access. Solventum, spun out of 3M at an USD 8.2 billion valuation, is carving a niche in low-touch wound care that leverages proprietary adhesives and negative-pressure know-how. Patent filings, such as the halobetasol propionate-lidocaine combination (US20240358716A1), underscore the race to lock in differentiation through intellectual property. Quality-related FDA enforcement nudges weaker players to exit or sell assets, nudging consolidation upward. At the same time, barriers remain modest enough for start-ups to enter with targeted devices, keeping competitive intensity high in segments like microneedle manufacturing and sensor-embedded patches.

Topical Drug Delivery Industry Leaders

Bayer AG

Galderma Holding SA

GlaxoSmithKline PLC

Johnson & Johnson

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is emerging around non-steroidal, targeted dermatology therapies delivered as creams and ointments that aim to reduce reliance on topical corticosteroids amid price controls and long-term safety concerns. This is reinforced by several 2026 regulatory and pipeline signals, including the FDA approval of ADQUEY (difamilast 1%) ointment in February 2026 for mild-to-moderate atopic dermatitis in adults and pediatric patients aged 2 and older. The FDA also expanded pediatric approval for Arcutis ZORYVE (roflumilast) cream 0.3% in June 2026 down to age 2 for plaque psoriasis, while the EMA CHMP issued a positive opinion in June 2026 for Incyte Opzelura (ruxolitinib) cream in adults with moderate atopic dermatitis.

Outside dermatology, the most tangible opportunities concentrate in advanced delivery platforms that translate complex molecules into user-friendly, home-care-compatible regimens, consistent with faster movement in devices and home-care settings. Clinical activity continues to support platform diversification, including first-patient-dosed activity for a skin-restricted topical JAK inhibitor ointment for vitiligo (Lynk Pharmaceuticals, June 2026) and initiation of a Phase 1/2 study for a topical cream in actinic keratosis (Rubedo Life Sciences, January 2026). At the same time, the technical threshold for complex topical generics is rising under the FDA’s March 2026 Q3 characterization framework, which creates room for CDMOs and developers with strong microstructure analytics, IVRT/IVPT capability, and scalable patch or microneedle manufacturing.

Recent Industry Developments

- July 2026: Galderma received a Complete Response Letter from the US FDA for its Biologics License Application for RelabotulinumtoxinA following a manufacturing site inspection. The company indicated it initiated corrective and preventive actions, highlighting how manufacturing readiness and inspection outcomes can affect launch timelines and capacity planning for complex therapeutic portfolios.

- June 2026: Bayer completed its acquisition of Perfuse Therapeutics, adding PER-001, an intravitreal implant program that uses sustained-release drug delivery for eye diseases including glaucoma and diabetic retinopathy. The deal reflects continued strategic interest in long-acting local delivery technologies that can reduce dosing burden in chronic ophthalmology care.

- September 2024: Solventum introduced its Peel and Place extended-wear wound-care dressing, reporting reductions in application time and care costs during clinical rollout. The launch supports broader adoption of advanced dressings in hospitals and home-care settings by linking product design to workflow efficiency and total cost of care.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the topical drug delivery market is measured as the value of drug products and delivery systems that administer an active ingredient onto skin or other accessible surfaces for local or systemic effect, including OTC and prescription therapies.

Scope exclusions: Cosmetic-only skin care products with no drug claim, and non-topical delivery such as oral solids and injectables, are excluded from this sizing.

Segmentation Overview

- By Route of Administration

- Dermal

- Ophthalmic

- Nasal

- Oral Mucosal

- Otic

- Rectal

- Vaginal

- Pulmonary (Inhalational)

- Others

- By Product

- Formulations

- Solid (powders, films)

- Semi-Solid

- Creams

- Ointments

- Gels & Pastes

- Liquid (solutions, sprays)

- Foams

- Devices

- Transdermal Patches

- Microneedle Patches

- Inhalers & Nebulisers

- Metered-Dose Sprayers

- Formulations

- By Indication

- Dermatology (Eczema, Psoriasis, Acne)

- Pain Management (Musculoskeletal, Neuropathic)

- Ophthalmology (Dry-eye, Glaucoma)

- Respiratory (Asthma, COPD)

- ENT & Nasal Infections

- Hormone Replacement Therapy

- CNS Disorders (Migraine, Parkinson’s)

- Others

- By End-User

- Hospitals

- Specialty Clinics & Dermatology Centers

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the ground rules for what counts as topical delivery and then to collect stable reference series that help anchor volumes and pricing. We typically start with public health and medicine sources, including US FDA databases and guidance pages, the US National Library of Medicine (Drug Labels), the World Health Organization, and the US CDC, to capture disease and treatment context that drives topical use.

To cross-check demand direction, we also rely on peer-reviewed dermatology and pharmaceutics journals, trade association publications, customs and trade statistics where relevant for finished dosage forms, and company annual reports and investor presentations that discuss portfolio mix and sales trends. Patent databases are used selectively to understand formulation and device activity, for example penetration enhancers and patch-related filings. A paid subscription for company financials and news is then used to verify timelines and reported mix shifts. This desk source list is illustrative and not exhaustive, and additional public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold and used as topical drug delivery across major regions, and on correcting desk assumptions on pricing and adoption. We spoke with a mix of formulation and device stakeholders, distributors, and clinical and commercial respondents so that changes in prescription behavior, OTC switching, and channel splits could be captured and reconciled.

Because market reporting practices vary by dosage form and route, the discussions were also used to confirm which adjacent categories should be excluded or counted separately, and to pressure-test the forecast drivers before the final model was signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 17% | Managers: 54% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started from a demand-pool build that uses treated-patient and therapy-use signals, where disease prevalence and treatment rates are translated into topical therapy volume by dosage form and typical pack usage. That top-down build was then checked with selective bottom-up approximations, including sampled brand and category revenue roll-ups, channel checks on OTC versus prescription mix, and a price times volume sanity check for high-usage categories.

Key inputs used in the model included diagnosed dermatology burden and flare patterns that affect repeat purchases, prescription to OTC switching behavior, route mix between dermal and transdermal products, typical pack sizes and application frequency, and ASP movements tied to generic entry and product upgrades. When bottom-up inputs were missing for smaller categories, gaps were handled using proxy pricing and penetration rates derived from adjacent, better-covered product groups and then validated through expert feedback.

For the forecast, scenario analysis was applied around a base case that reflects likely adoption changes by route and dosage form, supported by short series smoothing for stable sub-categories where demand is less sensitive to new launches. Assumptions on growth drivers, including chronic skin condition management, aging-related care, and patch usage in selected therapies, were reviewed with primary respondents so the final curve remained realistic by region.

Data Validation & Update Cycle

Outputs were validated through stepwise triangulation, where totals were compared against independent signals such as reported product mix comments, regional demand direction, and price evolution patterns, and then rechecked for arithmetic consistency across routes and end users. When large variances showed up, the model was reopened and the underlying assumptions were revisited, followed by targeted re-contacts with experts to confirm what changed.

Before sign-off, a separate analyst review is completed to spot anomalies that can come from scope overlap, double counting, or currency timing, and corrections are documented for traceability. Reports are refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is performed so clients receive the most current view.

Mordor Intelligence's Topical Drug Delivery Market Size Compared Against Other Published Estimates

Published market numbers for topical drug delivery can look far apart even when the topic is described similarly, because the counted routes, included product types, and year definitions are not consistent across sources. Differences also come from how pricing is handled for generics versus branded therapies, and from whether OTC demand is modeled using real usage assumptions or treated as a simple uplift.

The largest gaps usually show up when some estimates pull in adjacent non-topical delivery routes, expand the scope to broader drug delivery categories, or apply aggressive growth curves from launch-heavy years into the full forecast. Currency conversion timing and refresh cadence can also move the headline value, particularly in a market with fast mix shifts between dermal, transdermal, and mucosal routes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 134.27 B (2026) | |

| Industry Publisher A | USD 136.35 B (2025) | Uses a different base year and a wider route lens in its segmentation language, which can pull in adjacent delivery routes and inflate the comparable topline if not normalized to strictly topical products. |

| Industry Publisher B | USD 177.82 B (2025) | Counts a broader set of revenues across topical product types and applies a shorter historical window, which can lift the 2025 number if OTC-heavy categories and wider product definitions are included together. |

The spread in values is largely explained by base-year choice and what each source considers topical versus adjacent delivery routes, followed by how pricing and OTC volume are converted into revenue. By keeping the counted scope tight to drug-labeled topical therapies and checking price and volume assumptions against expert feedback, the resulting estimate stays more comparable across regions and product forms, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the topical drug delivery market?

The topical drug delivery market size stands at USD 134.27 billion in 2026 and is projected to hit USD 186.42 billion by 2031.

Which route of administration is growing fastest?

Nasal delivery is registering the highest CAGR of 9.12% through 2031 due to growing use in neurologic and respiratory therapies.

Why are smart patches important for patient adherence?

Smart, sensor-equipped patches record dose-timing, stream data to clinicians, and can adjust release profiles automatically, reducing missed or incorrect doses.

How are ESG policies affecting topical formulations in Europe?

New sustainability rules are phasing out petrolatum, prompting companies to reformulate with bio-based excipients and invest in new manufacturing lines.

What segments present the strongest growth opportunities?

Pain management, with a 9.94% forecast CAGR, and home-care delivery settings, with a 8.96% CAGR, stand out as the most dynamic opportunities within the topical drug delivery market.

Page last updated on: