Biological Skin Substitutes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

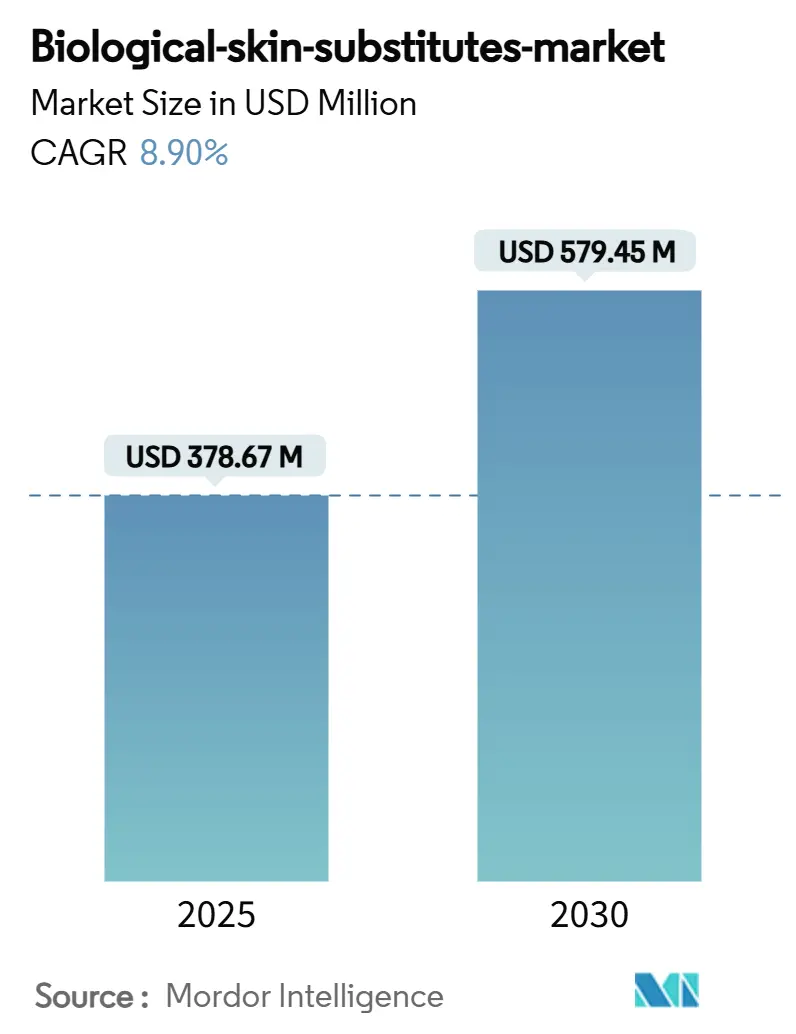

| Market Size (2025) | USD 378.67 Million |

| Market Size (2030) | USD 579.45 Million |

| Growth Rate (2025 - 2030) | 8.90% CAGR |

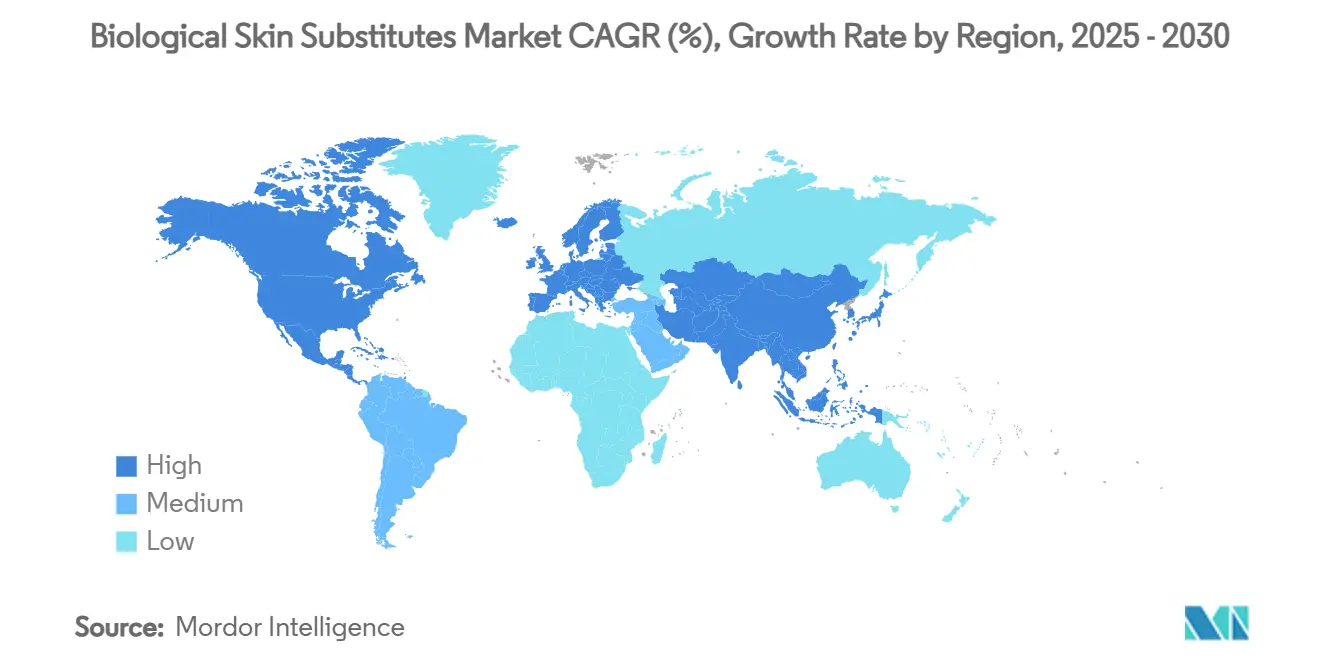

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biological Skin Substitutes Market Analysis by Mordor Intelligence

The biological skin substitutes market size stands at USD 378.67 million in 2025 and is forecast to reach USD 579.45 million by 2030, advancing at an 8.9% CAGR over the period. Growing use of advanced wound-care solutions, wider clinical acceptance of engineered tissues, and steady regulatory approvals underpin current demand momentum. Greater attention to evidence-based reimbursement, combined with military-funded innovations that quickly migrate into civilian care, increases the addressable patient pool and reinforces the premium positioning of products with robust clinical data. Investments in 3-D bioprinting, autologous cell-harvesting systems, and omega-3-rich xenografts broaden the therapeutic arsenal while constraining commodity offerings that lack proven outcomes. At the same time, stricter Local Coverage Determinations in the United States and similar policy shifts in Europe channel volume toward products that deliver measurable savings through faster healing and lower complication rates. These parallel forces of innovation, regulation, and value-based purchasing collectively drive the biological skin substitutes market toward higher-quality, data-driven consolidation.

Key Report Takeaways

- By source material, human allografts held 42.5% revenue share in 2024, whereas cell-based constructs record the highest projected CAGR at 13.4% through 2030.

- By product type, acellular matrices accounted for 48.3% of the biological skin substitutes market size in 2024; bioengineered 3-D skin is forecast to advance at an 18.2% CAGR to 2030.

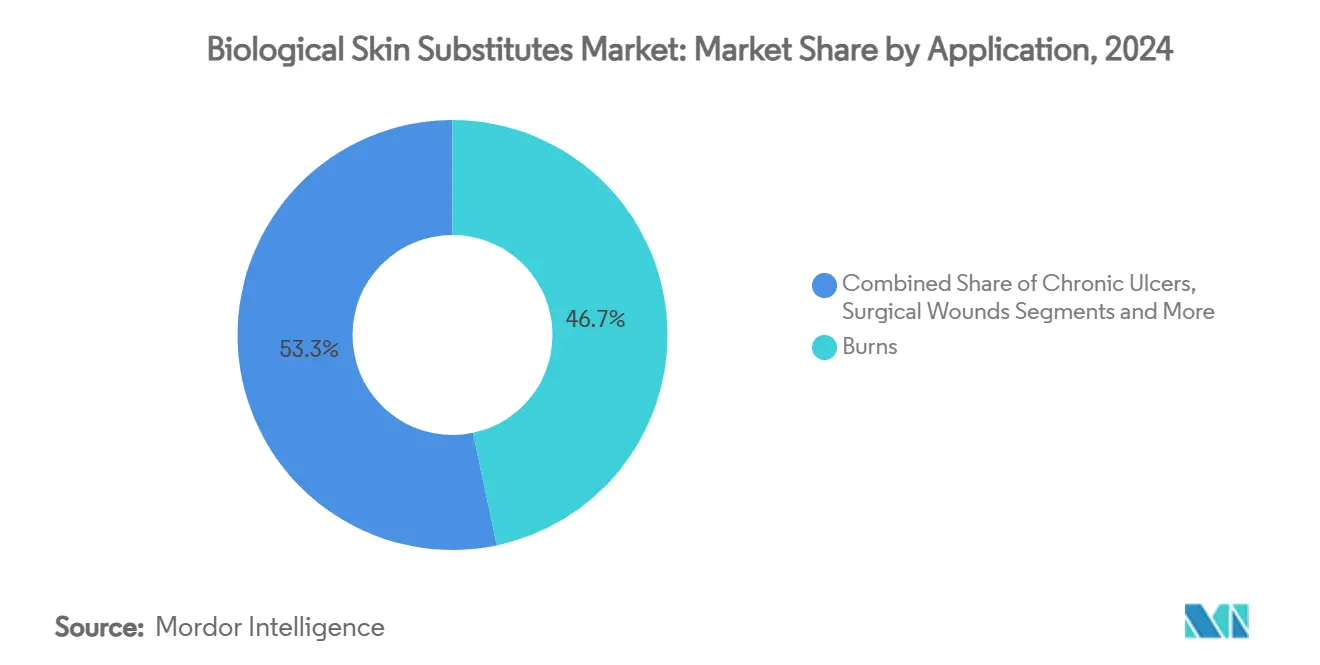

- By application, burns maintained 46.7% share of the biological skin substitutes market size in 2024, while pediatric congenital defects rise at a 15.5% CAGR between 2025-2030.

- By end user, hospitals represented 55.1% share in 2024, whereas military and defense facilities expand quickest at a 14.7% CAGR through 2030.

- By geography, North America captured 39.6% of the biological skin substitutes market share in 2024, while Asia-Pacific posts the fastest regional expansion at a 12.4% CAGR to 2030.

Global Biological Skin Substitutes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic wounds & burns | +2.10% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing geriatric & diabetic population | +1.80% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Favorable reimbursement in developed markets | +1.30% | North America & Europe | Short term (≤ 2 years) |

| Military combat-care R&D adoption | +0.90% | North America, with spillover to allied nations | Medium term (2-4 years) |

| Veterinary reconstructive surgery uptake | +0.60% | Global, led by developed markets | Long term (≥ 4 years) |

| 3D bioprinting for on-site custom grafts | +1.40% | Global, early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds & Burns

Ten point five million Medicare beneficiaries currently live with chronic wounds, imposing USD 28 billion in direct annual costs.[1]Centers for Medicare & Medicaid Services, “Skin Substitute Grafts… L39760,” cms.gov Clinical studies confirm that tissue-engineered skin shortens healing times and cuts infection-related readmissions, prompting hospitals to integrate biologics into routine protocols. Breakthroughs such as fully functional laboratory-grown skin containing hair follicles and glands underscore a shift toward regenerative rather than protective therapies. Health-system focus on total episode cost, not device price alone, accelerates uptake because faster closure reduces downstream expenditures for long-term care. As diabetic foot ulcer incidence climbs, surgical teams increasingly specify substitutes that can be applied in outpatient settings, broadening access beyond burn units. Together, these factors cement chronic wounds as a durable demand engine within the biological skin substitutes market.

Increasing Geriatric & Diabetic Population

Global aging deepens comorbidity profiles and elevates the prevalence of non-healing ulcers, especially in Asia Pacific, where senior cohorts grow fastest.[2]World Health Organization, “Resolution WHA77.4: Strengthening Safe, Ethical and Timely Access to Human Cells, Tissues and Organs,” who.int Elderly diabetic patients require more complex interventions because vascular insufficiency slows spontaneous recovery, making advanced grafts an essential rather than optional modality. Regulatory pathways that allow certain human-cell-based products to reach the market under less stringent requirements expand supply but heighten quality variability. Consequently, hospitals screen suppliers for proven safety to avoid sepsis or graft failure in frail patients. Personalized constructs that account for patient-specific factors, such as collagen content or growth-factor dosage, become a competitive differentiator. The demographic surge, therefore, sustains long-run volume growth and steers R&D toward bespoke therapies, reinforcing revenue visibility for the biological skin substitutes market.

Favorable Reimbursement in Developed Markets

The United States now limits coverage to 26 skin-substitute grafts that meet rigorous clinical-outcome thresholds, effectively lifting well-validated brands above commodity peers. Medicare permits up to eight applications over a 12-16-week episode, providing ample reimbursement headroom for complex wounds while capping overuse. Europe follows suit through the Tissues and Cells Directive, obligating manufacturers to show safety and efficacy before national payers authorize payment. Premium products that demonstrate higher closure rates secure formulary preference despite higher list prices because hospitals capture savings through shorter length of stay. The shift bolsters revenue certainty and drives continued investment in post-market surveillance to protect formulary status. Evidence-based reimbursement thus rewards data-rich players and accelerates market consolidation, elevating overall quality across the biological skin substitutes market.

Military Combat-Care R&D Adoption

The 2025 Military Burn Research Program allocates USD 650 million to skin-substitute innovations suited for austere environments.[3]Congressionally Directed Medical Research Programs, “2025 Military Burn Research Program,” cdmrp.health.mil Projects include pirfenidone-infused patches that minimize hypertrophic scarring and omega-3 fish-skin xenografts that outperform cadaveric skin in deep burns. Battlefield prototypes emphasize portability, shelf stability, and rapid application, specifications that later translate into trauma-center procurement criteria. Civilian burn units adopt defense-validated products because they arrive with robust survival and functional-outcome data from high-acuity cases. This defense-to-civilian technology flow expands volume, giving suppliers a dual-market revenue stream that reinforces their R&D budgets. Military investment, therefore, exerts a multiplier effect on commercial demand within the biological skin substitutes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biological substitutes | -1.70% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Disease-transmission & immune-rejection risk | -0.80% | Global, with stricter oversight in developed markets | Medium term (2-4 years) |

| Regulatory ambiguity in cross-border tissue trade | -0.60% | Global, affecting international supply chains | Medium term (2-4 years) |

| Cold-chain logistics gaps in emerging markets | -0.40% | Asia-Pacific, Middle East & Africa, South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biological Substitutes

Rapid revenue escalation from USD 1 billion in 2019 to nearly USD 7 billion in 2024 raised payer scrutiny, leading CMS to propose a 90% spending cut on skin-substitute reimbursement for 2026. Analysts attribute cost inflation to products cleared under less-rigorous pathways that command premium prices without matching clinical benefit. Hospitals in resource-constrained regions defer purchases or switch to older dressings, slowing geographic expansion. Evidence-based coverage rules may curb commoditized offerings, but near-term revenue could dip as formularies rationalize inventories. Suppliers that combine strong data with manufacturing efficiency will better defend price points, whereas high-cost, low-evidence products risk delisting. Affordability therefore remains the most immediate brake on global penetration of the biological skin substitutes market.

Disease-transmission & Immune-Rejection Risk

The FDA’s 2025 draft guidance on sepsis and tuberculosis vigilance in tissue products heightens compliance obligations for processors. Additional donor-screening steps and validated sterilization methods raise operating costs, particularly for small tissue banks. End-users remain wary of allogeneic grafts when autologous or xenograft alternatives reduce immunogenicity, channeling demand away from traditional cadaveric skin. Emerging fish-skin matrices sidestep human-to-human disease risk but introduce questions about long-term biocompatibility and cultural acceptance. Heightened safety oversight, therefore, tempers growth by elongating product-launch timelines and elevating quality-control expenditures, slightly dampening the CAGR projection for the biological skin substitutes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Material: Allografts Anchor Volume, While Cell-Based Constructs Accelerate

Allografts generated 42.5% of the biological skin substitutes market size in 2024, reflecting long clinical tenure and insurer familiarity. Early processing ensures low antigenicity, which keeps readmission rates manageable and preserves surgeon confidence. Market share stability is reinforced by national tissue-bank networks that guarantee supply continuity and traceability. Parallel evidence shows that cell-based constructs are advancing at a 13.4% CAGR to 2030, which is the fastest within this segment. Ex vivo expansion of autologous keratinocytes and fibroblasts facilitates full-thickness coverage with minimal donor skin, appealing to burn centers seeking to reduce surgical morbidity.

Laboratory breakthroughs such as stem-cell-derived skin complete with appendages position cell-based products for future volume gains. Gene-edited grafts now deliver 81% closure rates in dystrophic epidermolysis bullosa, validating targeted molecular repair. Xenografts, particularly omega-3 fish-skin sheets, secure Medicare coverage for specialized indications, offering a pathogen-reduced alternative to porcine dermis. Composite matrices that combine acellular scaffolds with autologous cells bridge mechanical robustness and biological signaling. Collectively, these advances diversify material choice and keep procurement teams engaged, sustaining competitive dynamics inside the biological skin substitutes market.

By Product Type: Acellular Matrices Hold the Lead As 3-D Prints Gain Ground

Acellular matrices represented 48.3% of the market share for biological skin substitutes in 2024, anchored by established supply chains and broad label indications. Decellularization preserves dermal architecture while reducing immunogenicity, combining off-the-shelf convenience with predictable integration profiles. Bioengineered 3-D skin captures the growth spotlight with an 18.2% CAGR forecast, empowered by bedside printers that lay vascularized layers in a single pass. Hospitals adopting this modality report shorter operating times and lower donor-site morbidity, supporting premium pricing.

Cellularized matrices balance active signaling with cold chain demands, targeting chronic ulcer clinics. Spray-on formulations retain niche roles in field care where rapid coverage is paramount. Innovations such as Cohealyx, a collagen-based dermal matrix, promise quicker graft readiness and reduced hospital stays, adding competitive friction. As the payers reward measured outcomes, product-type differentiation hinges on quantifiable healing metrics and cost-of-care reductions, influencing purchasing behavior across the biological skin substitutes market.

By Application: Burns Remain Dominant While Pediatric Demand Surges

Burn indications held 46.7% of the biological skin substitutes market size in 2024, capitalizing on standardized military and civilian protocols that mandate biological coverage for deep-partial and full-thickness injuries. Consistent R&D funding ensures a steady pipeline of materials that improve functional and cosmetic recovery, reinforcing segment resilience. Pediatric congenital defect treatment registers the fastest growth at 15.5% CAGR as clinicians adopt biologics tailored for fragile skin and immature immune systems. The case series using fish-skin grafts achieved 95% coverage without infection, driving confidence in xenograft safety profiles.

Chronic ulcers in diabetic and vascular-compromised patients exhibit rising complexity; surgeons favor matrices that release growth factors over extended periods. Surgical-traumatic wounds and aesthetic procedures form complementary niches, benefiting from outcomes data generated in high-acuity burn and pediatric settings. Diversified application breadth cushions suppliers against cyclical fluctuations and amplifies the total addressable biological skin substitutes market.

By End User: Hospitals Anchor Volume, Defense Medicine Drives Pace

Hospitals accounted for 55.1% biological skin substitutes market share in 2024, supported by integrated procurement and multidisciplinary wound teams. Their position is bolstered by centralized reimbursement processes that facilitate bulk purchasing and clinical-protocol standardization. Military and defense facilities, however, exhibit the fastest expansion at 14.7% CAGR through 2030 because of sizable combat-readiness budgets and rapid technology transfer mandates. Deployed medics require shelf-stable matrices and portable application systems, accelerating vendor innovation cycles.

Ambulatory surgical centers gain moderate traction as payers shift suitable cases out of inpatient wards to cut costs. Specialized burn centers and wound-care clinics maintain high procedure volumes, often serving as reference sites for new product evaluations. Emerging veterinary demand, enabled by companion-animal insurance coverage, broadens the customer base and lengthens product life cycles. These diverse channels collectively underpin robust demand for the biological skin substitutes market.

Geography Analysis

North America generated 39.6% of global revenue in 2024, underpinned by advanced trauma networks, supportive reimbursement, and concentrated clinical research. Stricter CMS coverage criteria prune low-evidence offerings but funnel higher volumes toward products demonstrating superior closure rates. Funding from the Military Burn Research Program accelerates technology maturation, while coordinated FDA and Health Canada policies facilitate bi-national distribution. Leading companies base manufacturing and R&D hubs in the United States, ensuring rapid clinician feedback loops that hasten iterative product upgrades.

Asia-Pacific ranks as the fastest-growing region with a 12.4% CAGR projected through 2030, propelled by aging populations and expanding health-insurance penetration. China’s investment in tricopolymer scaffolds and bilayered substitutes positions domestic firms as global exporters. Japan’s super-aged society drives hospital demand for regenerative approaches that reduce lengthy wound-care hospitalizations. India’s vast diabetic ulcer patient pool represents future upside once cold-chain and reimbursement gaps narrow. Continued regulatory alignment under WHO guidance further strengthens import and export clarity, boosting confidence among multinational suppliers and reinforcing positive momentum for the biological skin substitutes market.

Europe posts steady mid-single-digit growth, aided by the European Tissues and Cells Directive that standardizes safety and quality benchmarks. Germany, France, and the United Kingdom lead adoption due to well-funded health systems and established burn-care networks. Southern and Eastern European markets follow as EU funds modernize emergency care infrastructure. Middle East & Africa and South America remain nascent but attractive over the long term; high burn prevalence and limited local production create unmet need. Supplier partnerships with NGOs and disaster-relief agencies seed initial volume and lay groundwork for eventual commercial expansion.

Competitive Landscape

The biological skin substitutes market shows moderate fragmentation with a cluster of mid-sized incumbents and a rising cohort of technology disruptors. Integra LifeSciences reported USD 380.8 million Q3 2024 revenue, reflecting resilient demand despite earlier supply constraints. Organogenesis expanded manufacturing capacity by 122,000 square feet, signaling confidence in long-term demand and proactive mitigation of capacity bottlenecks. Smith & Nephew integrates acquired regenerative assets into its advanced wound-management portfolio, broadening value-added bundles for hospital customers.

Disruptive entrants spotlight autologous cell-harvesting and 3-D bioprinting solutions that reduce operating-room time and donor-site morbidity. AVITA Medical’s RECELL system received regulatory clearance for smaller wounds, targeting trauma centers seeking procedural speed. Kerecis leverages omega-3-rich fish skin to offer immunologically inert grafts with documented faster closure, securing quick Medicare contractor approvals. LifeNet Health’s Dermacell Porous demonstrates 135% higher healing relative to standard care and has already secured coverage under forthcoming Local Coverage Determinations.

Competition now hinges on clinical-outcome data, supply reliability, and cost-offset evidence rather than raw material source alone. Suppliers with integrated tissue banking, cGMP manufacturing, and post-market surveillance infrastructure command stronger bargaining power with group purchasing organizations. Ongoing consolidation suggests a gradual shift toward an oligopolistic structure centred on evidence-rich brands, further elevating quality expectations across the biological skin substitutes market.

Biological Skin Substitutes Industry Leaders

Integra LifeSciences

Organogenesis Holdings

Smith & Nephew

MIMEDX Group

Zimmer Biomet (Derma Sciences)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kerecis obtained rapid Medicare Administrative Contractor approval for new medical fish-skin products.

- April 2025: AVITA Medical launched Cohealyx, a collagen matrix designed to shorten graft-readiness times.

- April 2025: LifeNet Health unveiled Dermacell Porous, entering Medicare coverage under new LCD guidelines.

- January 2025: Stanford Medicine received FDA approval for genetically engineered skin grafts that achieved 81% healing in epidermolysis bullosa patients.

Global Biological Skin Substitutes Market Report Scope

| Human Allografts |

| Animal Xenografts |

| Cell-based Constructs |

| Composite / Hybrid |

| Autografts |

| Acellular Matrices |

| Cellularized Matrices |

| Bioengineered 3-D Printed Skin |

| Spray-on Skin Substitutes |

| Others |

| Burns |

| Chronic Ulcers (Diabetic, Venous, Pressure) |

| Surgical & Traumatic Wounds |

| Pediatric Congenital Defects |

| Cosmetic & Aesthetic Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Burn Care & Wound Care Centers |

| Military & Defense Medical Facilities |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source Material | Human Allografts | |

| Animal Xenografts | ||

| Cell-based Constructs | ||

| Composite / Hybrid | ||

| Autografts | ||

| By Product Type | Acellular Matrices | |

| Cellularized Matrices | ||

| Bioengineered 3-D Printed Skin | ||

| Spray-on Skin Substitutes | ||

| Others | ||

| By Application | Burns | |

| Chronic Ulcers (Diabetic, Venous, Pressure) | ||

| Surgical & Traumatic Wounds | ||

| Pediatric Congenital Defects | ||

| Cosmetic & Aesthetic Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Burn Care & Wound Care Centers | ||

| Military & Defense Medical Facilities | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected biological skin substitutes market size by 2030?

It is forecast to reach USD 579.45 million, reflecting an 8.9% CAGR from 2025.

Which region is growing fastest in the biological skin substitutes market?

Asia-Pacific leads with a projected 12.4% CAGR through 2030, driven by aging populations and improving healthcare infrastructure.

Which product category currently holds the largest biological skin substitutes market share?

Acellular matrices command 48.3% revenue share in 2024.

What factor is expected to have the greatest positive impact on future market growth?

Rising incidence of chronic wounds and burns contributes approximately +2.1 percentage points to forecast CAGR.

How are reimbursement changes influencing competitive dynamics?

Stricter coverage policies now favor products with published clinical-outcome data, prompting consolidation toward evidence-rich brands.

Why are military research programs significant for market innovation?

Defense-funded projects deliver shelf-stable, rapid-application grafts that migrate into civilian trauma care, expanding overall market demand.

Page last updated on: