Tissue Engineering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

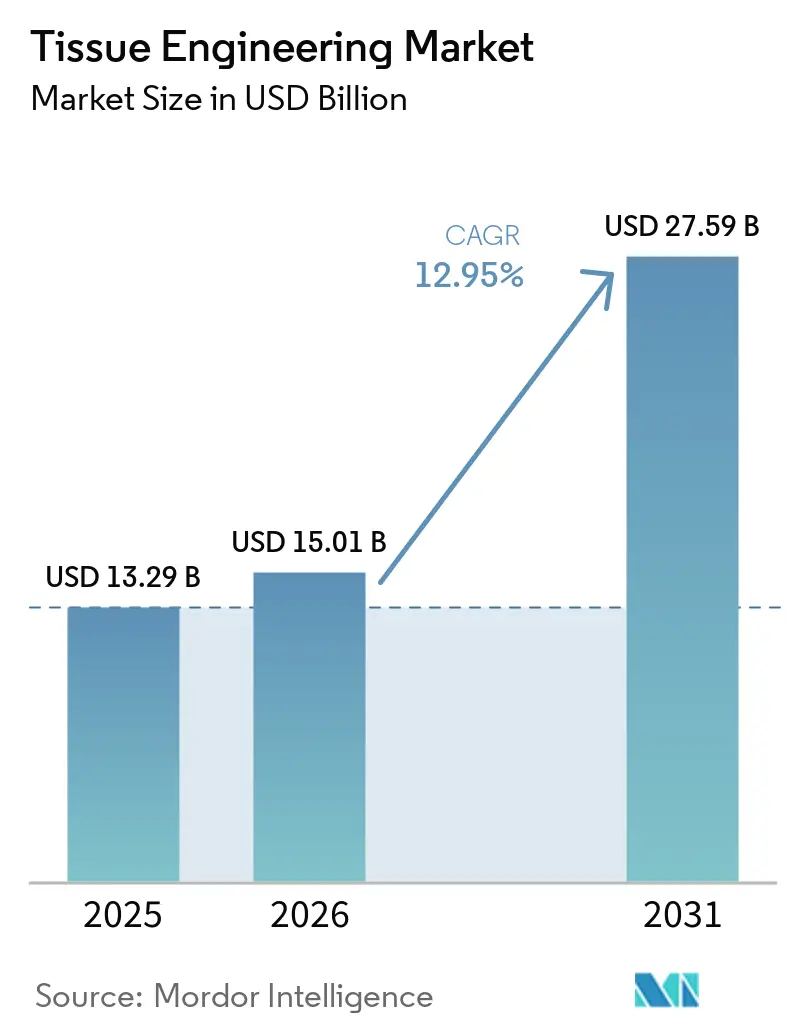

| Market Size (2026) | USD 15.01 Billion |

| Market Size (2031) | USD 27.59 Billion |

| Growth Rate (2026 - 2031) | 12.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Engineering Market Analysis by Mordor Intelligence

The Global Tissue Engineering Market size is projected to be USD 13.29 billion in 2025, USD 15.01 billion in 2026, and reach USD 27.59 billion by 2031, growing at a CAGR of 12.95% from 2026 to 2031.

This expansion rests on the convergence of modernized regulatory frameworks, breakthroughs in scaffold design, and a widening set of clinical indications. Synthetic polymers remain the volume backbone of the Tissue Engineering market because of mature manufacturing infrastructure, but hybrid composites are attracting capital faster as next-generation performance requirements strengthen. Demand dynamics favor orthopedic, musculoskeletal, and trauma applications, yet vascular indications are pacing the future growth curve as military and civilian trauma cases surge.

Key Report Takeaways

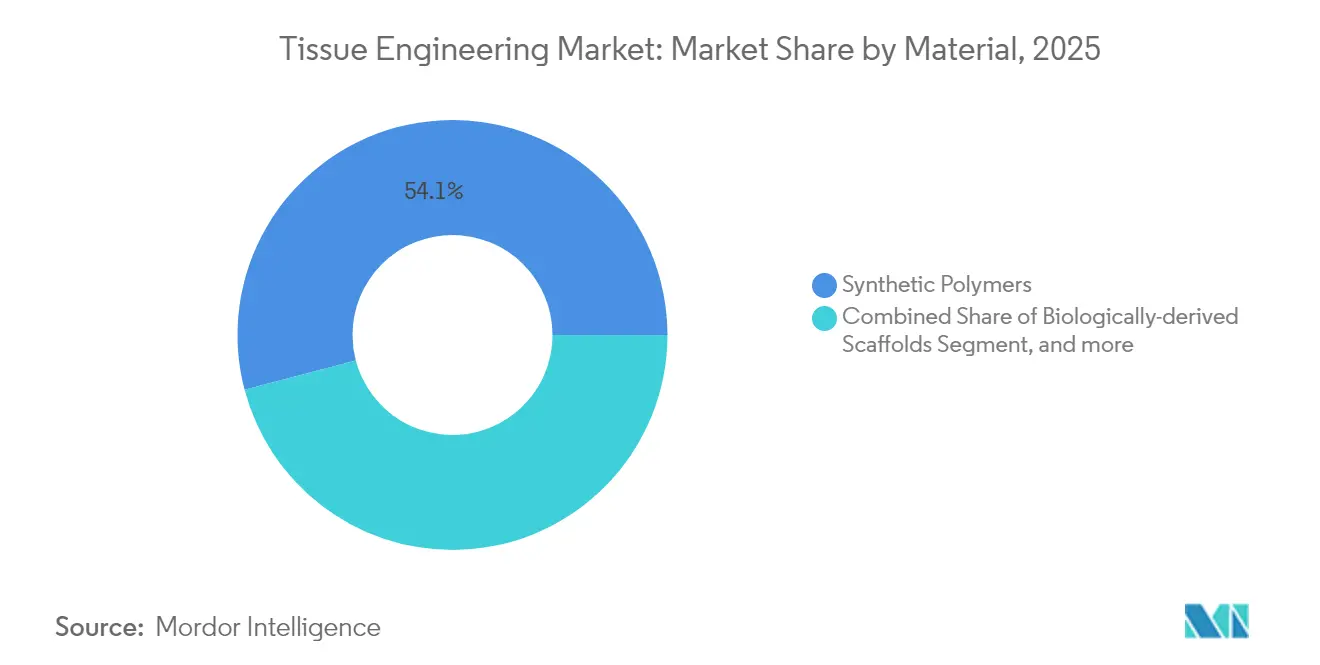

- By material type, synthetic polymers held 54.10% of the Tissue Engineering market share in 2025, whereas hybrid/composite materials are set to grow at a 14.05% CAGR through 2031.

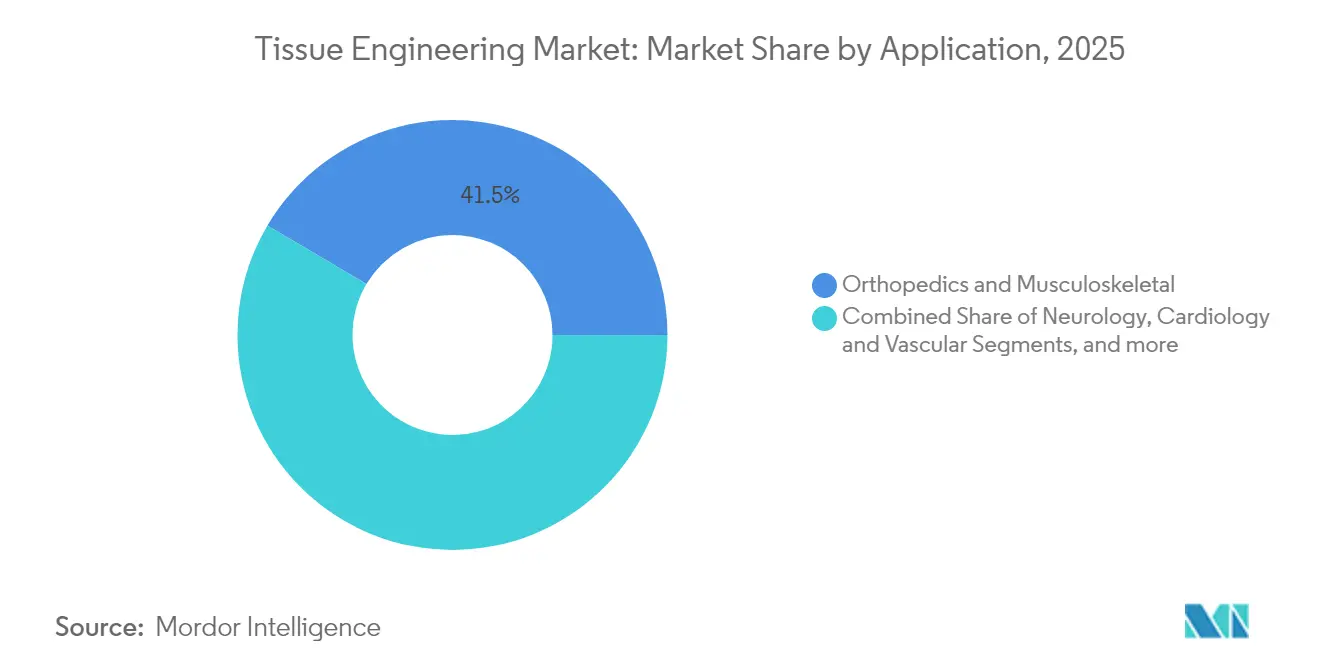

- By application, orthopedic and musculoskeletal solutions commanded 41.50% of the Tissue Engineering market size in 2025; cardiology and vascular solutions are forecast to advance at a 13.75% CAGR to 2031.

- By end user, hospitals and surgical centers controlled 62.70% revenue in 2025, while specialty regenerative clinics are expanding at 13.55% CAGR through 2031.

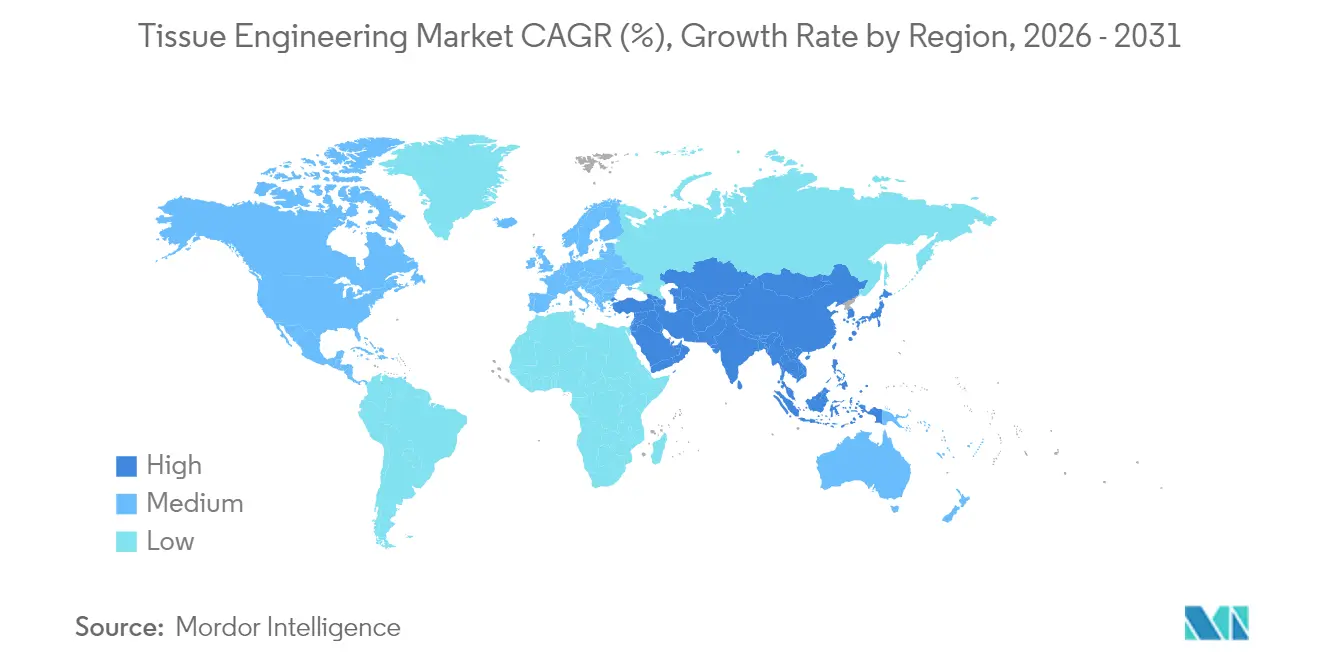

- By geography, North America captured 45.10% of the Tissue Engineering market share in 2025, whereas Asia-Pacific is on track for the fastest 13.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tissue Engineering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases & trauma injuries | +2.0% | Global, acute in aging North America & Europe | Medium term (2-4 years) |

| Expanding public-private funding pools for regenerative medicine | +1.8% | Global, concentrated in US NIH, EU Horizon, China national plans | Long term (≥ 4 years) |

| Rapid advances in 3-D bioprinting & scaffold design | +1.5% | North America & Europe leading; Asia-Pacific accelerating | Short term (≤ 2 years) |

| Accelerated regulatory pathways | +1.2% | FDA leadership, EMA harmonization, Asia-Pacific frameworks | Medium term (2-4 years) |

| Corporate ESG Mandates Replacing Animal Testing with Human-cell Tissue Models | +0.9% | Global, Developed Economies, Developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases & Trauma Injuries

Degenerative joint disease, cardiovascular complications, and large-scale trauma are lifting baseline demand for regenerative solutions, strengthening the tissue engineering market. Osteoarthritis alone affects 595 million people worldwide, creating a sizable cohort for cartilage repair scaffolds. Field experience from military conflicts has confirmed the utility of off-the-shelf engineered grafts such as Symvess in austere settings. In January 2025, UC Irvine researchers introduced lipocartilage, a flexible skeletal tissue substitute that may broaden indications in reconstructive surgery[1]Phys.org Staff, “3-D Printed Collagen Structures Break Speed Barrier,” phys.org Source: Science Daily Editors, “Lipocartilage Offers New Option for Skeletal Repair,” sciencedaily.com. Clinical evidence is maturing quickly; recent trials reported 96.3% survivorship of 3-D printed talus replacements and 100% union in complex hindfoot reconstructions when platelet-rich fibrin coatings were employed, reinforcing surgeon confidence in tissue-engineered implants.

Expanding Public-Private Funding Pools for Regenerative Medicine

Government and mission-driven capital flows are intensifying around biomanufacturing, positioning the Tissue Engineering market for long-term supply expansion. A 2024 National Academies report quantified sizeable US federal commitments to scale advanced therapy manufacturing and highlighted persistent bottlenecks in growth-factor production[2]National Academies Press, “Emerging Technologies to Advance Regenerative Medicine Manufacturing,” ncbi.nlm.nih.gov. Multilateral projects under Europe’s Horizon program and China’s strategic biotech blueprint are channeling funds into pilot facilities, while venture investors continue favoring platform technologies with clear regulatory visibility. Funding tailwinds are also prompting collaborations that target bioprocess standardization, an effort expected to unlock nearly 50 metric tons of global capacity by 2028.

Rapid Advances in 3-D Bioprinting & High-Throughput Scaffold Design

Hardware, software, and biomaterial innovations are compressing design-to-clinic timelines, accelerating innovation across the tissue engineering market. In June 2025, Stanford engineers debuted an algorithm that outputs organ-scale vascular networks suitable for bioprinted constructs. Stony Brook University’s TRACE method overcame collagen gelation speed limits, enabling intricate collagenous structures with embedded cells. The University of Pittsburgh’s CHIPS system now yields perfusable scaffolds that promote self-organizing tissue morphogenesis, while the Terasaki Institute refined a light-based 3-D printing technique that optimizes cellular orientation. Together, these milestones reduce prototyping costs, elevate reproducibility, and facilitate patient-specific implants—advantages that conventional machining and molding lack.

Accelerated Regulatory Pathways

Modern policy blueprints are lowering uncertainty for developers and investors within the tissue engineering market. The FDA’s May 2025 roadmap to phase out animal testing prioritizes organoid models and advanced computational methods, aligning directly with Tissue Engineering market stakeholders[3]US Food & Drug Administration, “Humacyte Receives Marketing Authorization for Symvess,” fda.gov. Europe’s ATMP regulation is gradually harmonizing dossier requirements, although national implementation remains uneven. In Asia-Pacific, regulators are clarifying product classifications to ease market entry barriers, with Japan’s PMDA issuing additional guidance on scaffold-only devices in early 2025. Streamlined documentation and adaptive trial designs are emerging as core mechanisms that shorten overall time-to-approval.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy & procedure costs | -1.5% | Global, acute in cost-sensitive regions | Short term (≤ 2 years) |

| Fragmented reimbursement coverage architecture | -0.9% | US private payers, EU national variations, limited Asia-Pacific coverage | Medium term (2-4 years) |

| Supply-chain shortages of cGMP-grade growth factors & cytokines | -0.5% | Global, regionally variable | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy and Procedure Costs

Complex good-manufacturing workflows and stringent quality controls keep unit prices above conventional graft alternatives. For instance, the newly approved Symvess is priced around USD 29,500 per unit, reflecting both high-grade biomaterials and extensive clinical validation requirements. Growth factors and cytokines necessitate cGMP production environments; efforts to substitute food-grade inputs show promise but remain in early validation. Capital outlays for dedicated biomanufacturing infrastructure often sit beyond the reach of start-ups, compelling partnerships or contract manufacturing agreements to manage fixed costs. Over the medium term, platform standardization and rising production volumes are expected to compress cost curves

Fragmented Reimbursement Coverage Architecture

Payer adoption lags scientific progress creating friction within the tissue engineering market. In the United States, Category III CPT codes, NTAP requests, and state-level Medicaid reviews impose multi-layered hurdles that can delay broad coverage by two or more years after FDA approval. Europe’s single-payer systems weigh cost-effectiveness differently by country, forcing companies to pursue sequential launches. Asia-Pacific markets amplify complexity; many insurers restrict coverage to legacy solutions or require local data. These reimbursement headwinds slow uptake even when clinical benefits are clear, making early health-economic modeling a necessity for market strategy teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Hybrid Composites Drive Next-Generation Scaffold Performance

Synthetic polymers led with a 54.10% share of the Tissue Engineering market in 2025, underpinned by cost-efficient scale, regulatory familiarity, and established surgeon comfort. Polylactic acid and polycaprolactone dominate today’s orthopedic and soft-tissue scaffolds, and mounting evidence from 3-D printed bone models is reinforcing their clinical staying power. Hybrid composites, however, are the fastest-growing segment at a 14.05% CAGR. These constructs merge synthetic durability with biologic cues by integrating bioactive ceramics, growth factors, or natural polymers into a single matrix, a capability that broadens the functional design landscape. The Tissue Engineering market size for hybrid composites is forecast to widen steadily as hospitals validate improved mechanical strength and integration profiles in human trials.

Biologically derived scaffolds are also advancing as decellularized extracellular matrix processes mature and regulators issue clearer documentation checklists. Innovations such as UPM Biomedicals’ injectable nanocellulose hydrogel FibGel signal a shift toward sustainable, plant-based inputs news. Consistency remains the gating factor; batch-to-batch variability can derail multicenter trial outcomes, so new quality-control analytics are gaining priority. As standardization improves, biologically derived matrices are expected to secure a solid mid-tier share of the Tissue Engineering market.

By Application: Cardiovascular Solutions Accelerate Through Trauma Adoption

Orthopedic and musculoskeletal interventions claimed 41.50% of the Tissue Engineering market share in 2025, anchored by well-accepted surgical protocols and solid reimbursement pathways. Surgeons now deploy tri-element-doped scaffold inserts for osteosarcoma resection sites, while lipocartilage research suggests a future avenue for flexible skeletal repairs. Extensions into dental and cranio-maxillofacial indications are leveraging similar growth-factor delivery systems, further reinforcing volume momentum.

Cardiovascular and vascular trauma solutions are outpacing all other indications at a 13.75% CAGR. Symvess stands as the first purely acellular large-diameter graft cleared for extremity trauma, and early site reports note 67% primary patency at 30 days fda.gov. Stanford’s 2025 vascularized organoid platform now supplies preclinical screens that accelerate the discovery of adjunctive biologics. These achievements position cardiovascular applications as the focal point for next-wave growth within the broader Tissue Engineering market size.

By End User: Specialty Clinics Emerge as Adoption Leaders

Hospitals and surgical centers controlled 62.70% of 2025 revenue because complex tissue-engineering procedures rely on multidisciplinary teams, advanced imaging suites, and intensive post-operative care. Integrated regenerative medicine programs within large academic medical centers streamline patient eligibility assessments and scaffold-sourcing logistics, reinforcing hospital dominance. Yet, their committee-based technology adoption often slows the introduction of novel implants.

Specialty regenerative clinics are expanding at 13.55% CAGR and now function as early-adopter sandboxes. Lean operations allow them to pilot personalized implants and point-of-care bioprinting protocols ahead of hospital standardization cycles. Research institutes remain influential in proof-of-concept trials, but their direct procedure volumes are smaller. As regulatory clarity improves, specialty clinics are likely to capture a rising portion of elective orthopedic and dermatological procedures, tightening competition across provider types within the Tissue Engineering market.

Geography Analysis

North America retained 45.10% of the Tissue Engineering market share in 2025 and benefits from the FDA’s responsive pathways, deep venture capital pools, and established reimbursement codes. The region’s hospitals moved quickly to integrate Symvess into trauma protocols, and multiple academic centers are now partnering with Defense Department programs to accelerate next-generation vascular graft deployment. Canada contributes niche cGMP manufacturing and favorable R&D tax credits, whereas Mexico offers lower-cost assembly options that complement supply chains.

Europe posts steady growth while refining its Advanced Therapy Medicinal Product regulatory framework. Germany, France, and the United Kingdom remain research powerhouses, yet multi-payer reimbursement negotiations can delay clinical adoption. Several EU member states are launching consortia to pool purchasing volumes for advanced biologics, a move expected to ease budgetary hurdles and increase procedure counts starting 2027.

Asia-Pacific is the fastest-rising region with a projected 13.98% CAGR through 2031. China’s 14th Five-Year Plan earmarked substantial funds for tissue-engineering pilot plants, and the National Medical Products Administration has introduced guidance to clarify scaffold-only and combination-product categories. Japan’s aging demographics drive high demand for cartilage and vascular implants, while its PMDA agency provides fast-track review channels that shorten time-to-market for qualified devices. India’s private hospital chains are investing in modular bioprinting labs to capture inbound medical-tourism flows, expanding the regional footprint of the Tissue Engineering market. Regulatory harmonization remains the critical variable; initiatives to align GMP audits and dossier templates across ASEAN economies could unlock additional adoption over the next five years.

Competitive Landscape

The Tissue Engineering market shows moderate concentration, with no single scaffold technology dominating all indications. Legacy orthopedic suppliers like Integra LifeSciences and Zimmer Biomet wield distribution reach and surgical training resources that smaller firms lack, yet specialized entrants are carving out niches. Humacyte’s focus on acellular human-derived grafts has already reshaped competitive benchmarks in vascular trauma, and the company’s manufacturing modularity lends itself to license-out partnerships.

Strategic positioning is gravitating toward platform approaches that extend from discovery software to pilot-scale biofabrication lines. Biological Lattice Industries epitomizes this model by coupling the BioLoom multi-tool bioprinter with cloud-based design software, an architecture that targets democratization of tissue manufacturing. In contrast, traditional device firms are layering AI-guided mesh optimization onto existing polymer portfolios to protect incumbency. Competitive differentiation now hinges on reproducible biomanufacturing and timely clinical-economic proof rather than material novelty alone.

Partnership structures are multiplying across the value chain. Scaffold developers increasingly secure contract bioprocess capacity to sidestep plant construction costs, while hospitals are co-investing in on-site mini-fabs to localize time-critical implants. IP landscapes remain fragmented, leading to growing cross-licensing deals. Overall, the next five years should witness selective consolidation around companies capable of pairing scalable manufacturing with distinct clinical franchises, holding the Tissue Engineering market in a balanced, innovation-driven rivalry.

Tissue Engineering Industry Leaders

Zimmer Biomet

B. Braun Melsungen AG

Integra Lifesciences

AbbVie (Allergan)

Becton, Dickinson and Company (C.R. Bard)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stanford scientists cultured vascularized heart and liver organoids with integrated blood vessels, removing long-standing size constraints for organoids and boosting their translational potential.

- December 2024: FDA granted market clearance to Humacyte’s Symvess, the first acellular tissue-engineered vessel indicated for extremity vascular trauma.

- October 2024: UPM Biomedicals introduced FibGel, the first injectable nanocellulose hydrogel sourced from birch wood, offering customizable stiffness and full biocompatibility.

- October 2024: Uni.Fund spearheaded a USD 1.8 million pre-seed funding round for Biological Lattice Industries. The funds will propel the advancement of BioLoom, a multi-tool 3D bioprinter, and the Loominus Studio software platform. The company's mission is to democratize biofabrication technologies, particularly for tissue engineering applications Business Wire

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global tissue engineering market as commercial products and services that combine living cells with natural, synthetic, or hybrid scaffolds to restore, replace, or enhance human tissues across orthopedic, cardiovascular, neurological, dermatological, dental, and other clinical uses.

Scope Exclusion: Pure cell-therapy products without an engineered scaffold or matrix lie outside this assessment.

Segmentation Overview

- By Material

- Synthetic Polymers

- Biologically-derived Scaffolds

- Hybrid / Composite

- By Application

- Orthopedics & Musculoskeletal

- Neurology

- Cardiology & Vascular

- Skin & Integumentary

- Dental & Cranio-maxillofacial

- Others

- By End User

- Hospitals & Surgical Centers

- Research & Academic Institutes

- Specialty Regenerative Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We supplement desk work through interviews with biomaterial scientists, hospital procurement heads, contract manufacturers, and reimbursement specialists across North America, Europe, and Asia-Pacific. Their insights verify adoption rates, price corridors, and regulatory pacing, allowing Mordor Intelligence to refine model assumptions and close data gaps.

Desk Research

Mordor analysts begin with structured searches across high-credibility, open sources such as the U.S. National Institutes of Health, Eurostat, the World Health Organization, the U.S. FDA 510(k) database, and trade bodies like the American Academy of Orthopaedic Surgeons. Market fundamentals are enriched with company 10-Ks, investor decks, import-export ledgers, and clinical-trial registries, which help link procedure counts to implant demand. Paid repositories, D&B Hoovers for company revenue splits and Questel for scaffold patent flows, supply granular validation when public data thin out. This list is illustrative; many additional references support fact-finding and clarification.

Market-Sizing & Forecasting

A top-down demand pool is constructed from procedure volumes, prevalence-to-treated ratios, and average selling prices, which are then cross-checked with selective supplier roll-ups and channel feedback. Key variables like orthopedic implant surgeries, chronic wound incidence, scaffold material cost trends, research funding outlays, and 3D-bioprinter installations drive annual estimates. Multivariate regression, stress-tested through scenario analysis, projects values to 2030. Where bottom-up inputs lack depth, interpolation is guided by regional ASP surveys and capacity utilization signals.

Data Validation & Update Cycle

Outputs pass variance and outlier checks against external series, after which senior reviewers sign off. Reports refresh each year, with interim adjustments when material events, such as major approvals or safety recalls, occur, and a final analyst pass ensures clients receive the most current view.

Why Mordor's Tissue Engineering Baseline Inspires Greater Trust

Published sizes often diverge because firms choose different scope boundaries, pricing ladders, and update rhythms.

Key gap drivers include varying inclusion of regenerative adjuncts, divergent ASP inflation paths, and less frequent refresh cycles in some studies, which can inflate or compress headline values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.29 B (2025) | Mordor Intelligence | |

| USD 22.13 B (2025) | Global Consultancy A | Broader regenerative medicine scope and unverified hospital charge data |

| USD 13.02 B (2025) | Industry Report B | Excludes hybrid scaffold materials and relies on limited interview depth |

| USD 5.40 B (2025) | Trade Journal C | Counts only scaffold hardware, uses conservative ASP baselines, and five-year-old currency factors |

The comparison shows how disciplined scope selection, annual refreshes, and dual-layer validation let Mordor Intelligence offer a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Tissue Engineering market?

The market is valued at USD 15.01 billion in 2026 and is forecast to reach USD 27.59 billion by 2031.

Which material type dominates revenue?

Synthetic polymers held 54.10% of revenue in 2025, reflecting mature manufacturing and surgeon familiarity.

Which application segment is growing the fastest?

Cardiovascular and vascular trauma solutions are expanding at a 13.75% CAGR through 2031, driven by recent FDA approvals.

Why is Asia-Pacific considered the fastest-growing region?

Government research grants, expanding clinical infrastructure, and evolving regulatory clarity push regional growth at a 13.98% CAGR.

What is the main cost barrier to broader adoption?

High cGMP manufacturing and procedure costs keep unit prices above conventional grafts, delaying payer coverage.

Page last updated on: