Orthopedic Biomaterials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

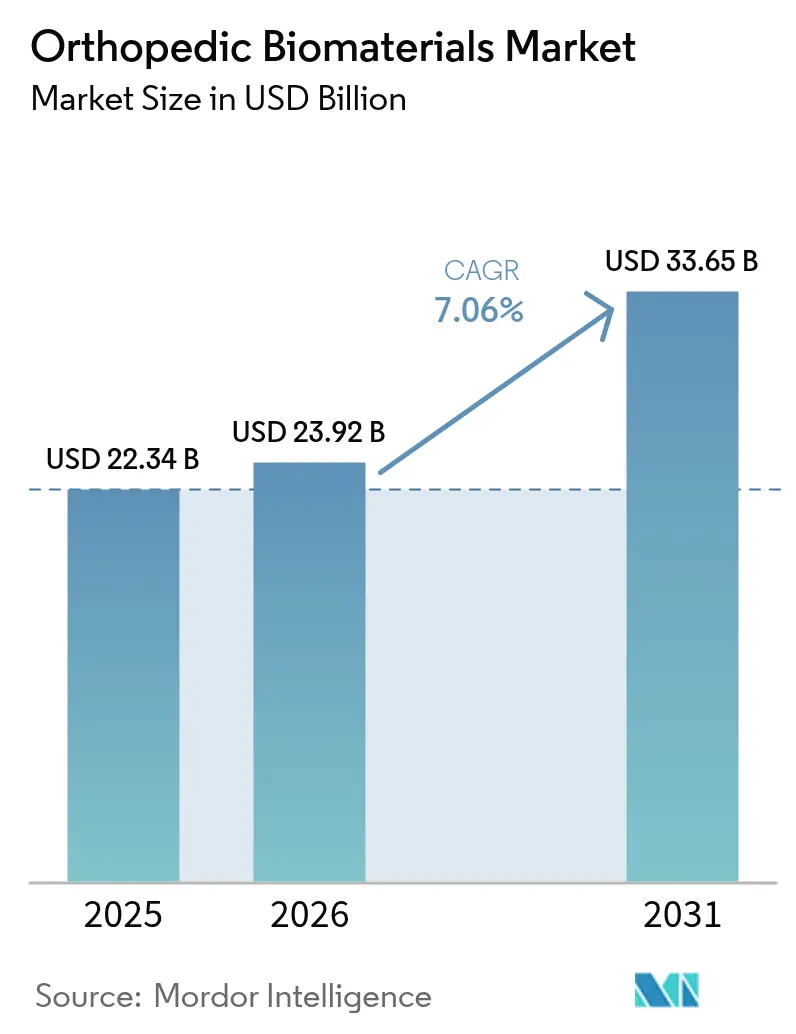

| Market Size (2026) | USD 23.92 Billion |

| Market Size (2031) | USD 33.65 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

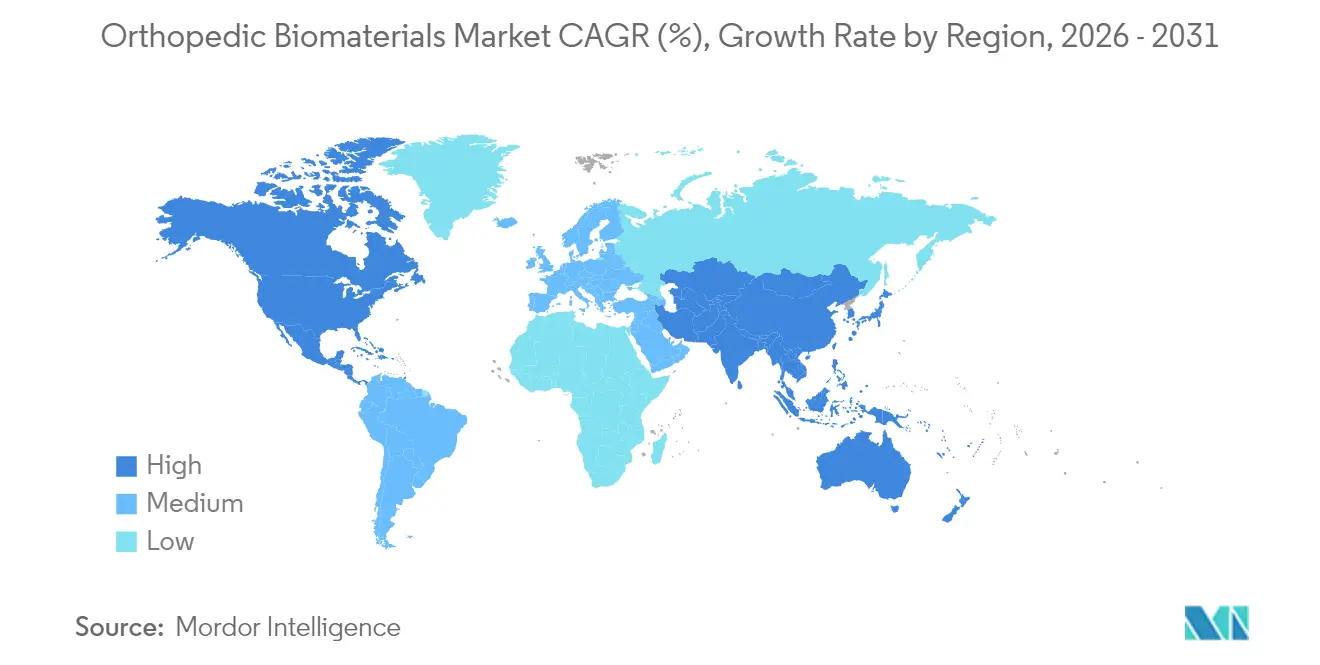

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Biomaterials Market Analysis by Mordor Intelligence

Orthopedic Biomaterials market size in 2026 is estimated at USD 23.92 billion, growing from 2025 value of USD 22.34 billion with 2031 projections showing USD 33.65 billion, growing at 7.06% CAGR over 2026-2031.

Growth stems from a confluence of demographic aging, surging osteoarthritis prevalence, steady sports- and traffic-injury incidence, and rapid technological progress in patient-specific and bioactive implants. Regulatory catalysts such as the U.S. FDA’s breakthrough device program shorten launch timelines for novel biomimetic materials [1]FDA, “Medical Device Supply Chain Resiliency Initiative,” fda.gov , while hospital demand for post-pandemic backlog reduction sustains procedural volumes. Companies leverage additive manufacturing to deliver fit-for-purpose components that reduce revision risk, and sustainability mandates push the supply base toward biodegradable formulations. Persistent supply chain stresses and tighter reimbursement scrutiny temper, but do not derail, the forward trajectory of the orthopedic biomaterials market.

Key Report Takeaways

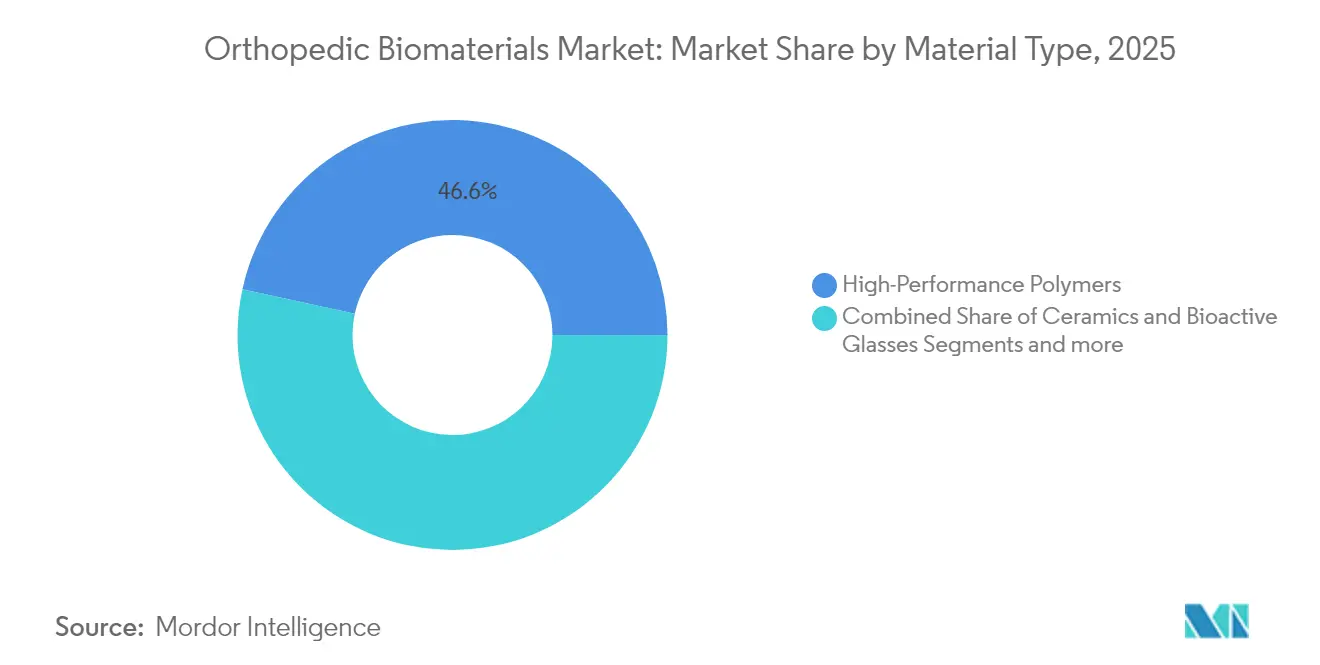

- By material type, high-performance polymers led with a 46.58% revenue share in 2025, while ceramics and bioactive glasses are projected to grow at a 7.82% CAGR through 2031.

- By application, joint reconstruction held 38.25% of the orthopedic biomaterials market share in 2025; orthobiologics are forecast to expand at an 8.03% CAGR to 2031.

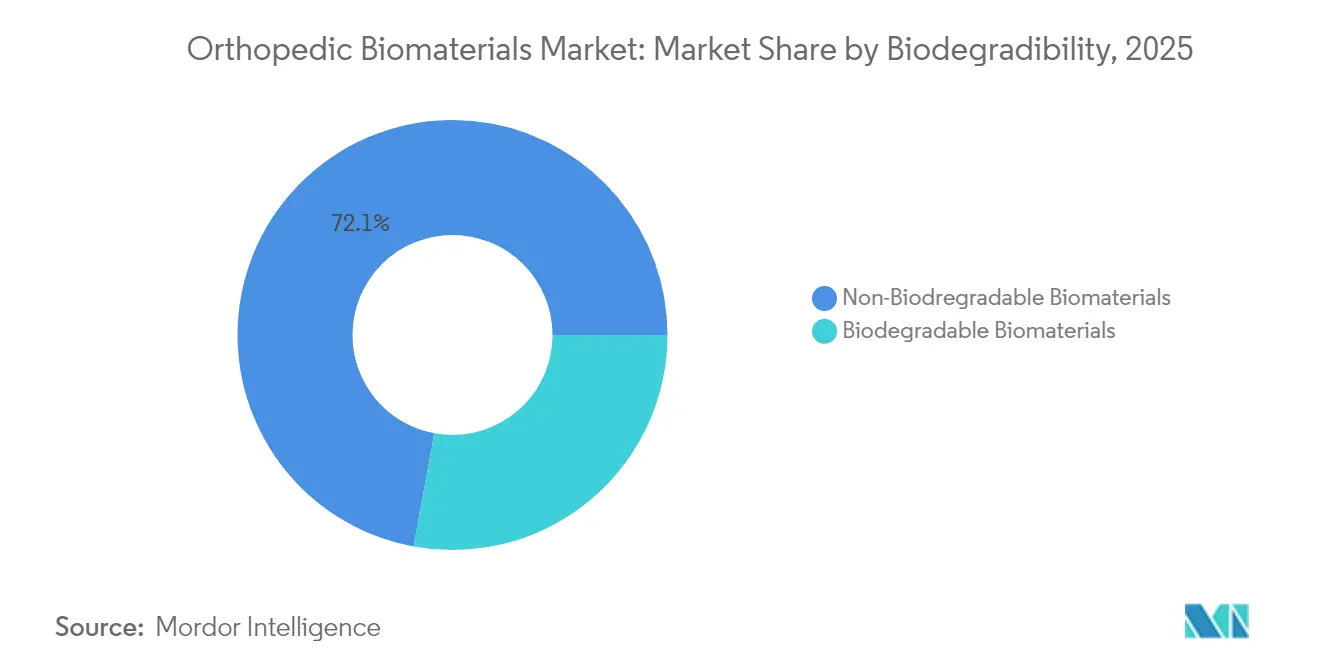

- By biodegradability, non-biodegradable biomaterials accounted for 72.10% of the orthopedic biomaterials market size in 2025, whereas biodegradable biomaterials are advancing at an 7.88% CAGR through 2031.

- By condition, osteoarthritis represented 37.20% of the orthopedic biomaterials market size in 2025; bone tumors are projected to register an 7.86% CAGR between 2026-2031.

- By geography, North America commanded 39.90% of revenue in 2025, while Asia-Pacific is forecast to rise at an 7.98% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Orthopedic Biomaterials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-linked osteoarthritis burden | +2.1% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Sports & road-injury up-trend in emerging markets | +1.8% | APAC core, spill-over to LATAM & MEA | Medium term (2-4 years) |

| 3-D printed patient-specific implants adoption | +1.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rapid FDA breakthrough device designations for biomimetic materials | +1.2% | Global, led by U.S. pathway | Short term (≤ 2 years) |

| Hospital PPP tenders in LATAM & MENA favouring local sourcing | +0.8% | LATAM & MENA | Medium term (2-4 years) |

| Circular-economy push for bio-resorbable materials | +0.6% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Linked Osteoarthritis Burden

Global life expectancy gains intersect with lifestyle factors to lift osteoarthritis prevalence, creating enduring demand for joint reconstruction solutions. Nearly 50% of post-menopausal women are expected to develop the condition by 2045, and knee osteoarthritis cases could rise 75% by 2050 [2]Arthritis Research & Therapy editorial board, “Projected Osteoarthritis Growth to 2050,” arthritis-research.biomedcentral.com . Parallel growth in revision hip and knee arthroplasty volumes amplifies requirements for durable, wear-resistant biomaterials. Elevated body-mass index contributes to more than 20% of global cases, coupling metabolic stress with mechanical wear and accelerating formulation of high-strength, low-debris polymers that extend implant longevity.

Sports & Road-Injury Up-Trend in Emerging Markets

Urbanization and motorization raise musculoskeletal trauma incidence across many lower-income regions. In Kenyan hospitals, road accidents account for 59.4% of orthopedic admissions, with 85% of victims in the 15-64 age bracket [3]BMC Musculoskeletal Disorders editors, “Road Trauma Injury Burden in Kenya,” bmcmusculoskeletdisord.biomedcentral.com . Comparable patterns in Ghana show vehicular crashes comprising 42% of injuries. Rising elective sports participation also expands reconstruction volumes among younger patients, prompting suppliers to tailor polymer-ceramic composites that balance mechanical resilience with accelerated bone in-growth.

3-D Printed Patient-Specific Implants Adoption

Additive manufacturing unlocks mass-customization for complex anatomies. The FDA cleared the restor3d total talus device in 2024, demonstrating 96.3% survivorship and validating individualized workflows. Modeling studies indicate patient-matched knees could cut readmissions 62% and revisions 39% by 2026, trimming cumulative costs by USD 38 billion. Titanium remains the prime metal in orthopedic printing due to favorable modulus and biocompatibility. Adoption challenges persist around reimbursement alignment and long-term durability evidence, yet surgeon demand for bespoke components keeps momentum strong.

Rapid FDA Breakthrough Device Designations for Biomimetic Materials

The breakthrough pathway shortens feedback loops between developers and regulators. Recent designations span bone graft substitutes such as NOVOSIS PUTTY and meniscal scaffolds from OrthoPreserve, signaling agency confidence in biomimetic platforms. Zimmer Biomet’s Oxford Cementless Partial Knee achieved U.S. approval with 94.1% ten-year survival, proving novel porous apps can excel without cement. Accelerated review trims costs and encourages venture investment, especially for osteoconductive PEEK and bioactive glass hybrids that mirror natural bone behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Procedure down-coding & reimbursement erosion | -1.6% | North America, expanding to EU | Short term (≤ 2 years) |

| Post-implant infection litigations increasing insurer scrutiny | -1.2% | Global, concentrated in litigious markets | Medium term (2-4 years) |

| Raw-material supply volatility | -0.9% | Global supply chains | Short term (≤ 2 years) |

| Talent shortage in orthobiologic R&D labs | -0.7% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Procedure Down-Coding & Reimbursement Erosion

Payers tighten documentation demands, forcing hospitals to justify every orthopedic indication. Medicare now requires proof of failed conservative care before authorizing total knees, extending pre-operative timelines. Payment bands fluctuate widely; complex trauma reimbursements range from USD 9,496 to USD 50,639 under MS-DRG codes, adding budgeting uncertainty for providers. Device firms must therefore demonstrate cost-offset claims and supply evidence dossiers to maintain coder compliance.

Post-Implant Infection Litigations Increasing Insurer Scrutiny

Periprosthetic infection rates of 0.5-3% for primary implants and up to 20% for revisions spur lawsuits and recall expenses. Elutia’s FiberCel recall triggered more than USD 17 million in legal outlays, illustrating the financial stakes. Insurers respond by elevating coverage thresholds and requiring stringent sterilization proof, raising liability coverage costs throughout the orthopedic biomaterials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymer Dominance Amid Ceramic Momentum

High-performance polymers generated the largest revenue slice in 2025, reflecting 46.58% share, anchored by strong uptake in acetabular cups and spinal cages. Evonik’s VESTAKEEP Fusion illustrates how adding biphasic calcium phosphate turns PEEK bioactive without sacrificing mechanical strength. The orthopedic biomaterials market size for polymers is projected to expand steadily as surface-enhanced variants tackle historical osseointegration limits. Ceramics and bioactive glasses, while smaller today, post a brisk 7.82% CAGR through 2031 as surgeons capitalize on innate osteoconductivity and radiolucency. Hybrid designs that bond polymer cores to ceramic coatings blend load tolerance with bone affinity, marking a shift toward materials that participate in healing rather than merely occupy space.

The metals category faces renewed scrutiny tied to stress shielding and nickel hypersensitivity. Zimmer Biomet’s Tivanium alloy targets allergy mitigation with low-nickel chemistry. Niche disruptors such as silicon nitride pursue antibacterial surfaces and thermal stability, with Sintx claiming sole FDA-cleared status for the compound. Calcium-phosphate cements retain hospital favor for moldable bone void fillers, yet ongoing research into controlled-resorption magnesium alloys foreshadows future movement toward fully degradable load-sharing constructs.

By Application: Reconstruction Stronghold Meets Biologic Surge

Joint reconstruction retained 38.25% revenue in 2025 as hip and knee arthroplasty volumes remained high among aging populations. Nonetheless, orthobiologics outpace all other uses with an 8.03% CAGR, propelled by evidence that bioinductive patches such as Smith+Nephew’s REGENETEN cut rotator-cuff re-tear rates 68% versus conventional repair. The orthopedic biomaterials market size attributed to biologics is set to widen as payers warm to regeneration that delays or avoids replacement surgery.

Spinal and trauma fixation implants continue reliable growth thanks to rising high-energy impacts in emerging economies. Viscosupplementation, once confined to mild osteoarthritis, is being repositioned as an adjunct to postpone arthroplasty among active seniors. Convergence arises as hardware manufacturers embed growth factors within plates or nails, creating integrated constructs that stabilize fractures while stimulating callus formation.

By Biodegradability: Resorbable Uptake Accelerates

Non-biodegradable options delivered 72.10% of sales in 2025 due to their track record in heavy load paths, yet biodegradable biomaterials advance at an 7.88% CAGR, confirming a decisive sustainability pivot. Magnesium screws achieve complete resorption after 52 weeks while maintaining union rates, eliminating secondary removal surgery. Orthopedic biomaterials market share for resorbables improves as hospital green-procurement policies emphasize circular economy compliance.

Poly-lactic-co-glycolic acid devices demonstrate over 90% bone replacement at 2-4.5 years in pediatric pelvis cases. Material recycling pilots show polymer implants can be processed through extrusion, whereas metal frames re-enter supply via powder metallurgy, though contamination control remains pivotal. Patient surveys reveal 90% acceptance of recycled braces, providing market pull for design-for-recycling initiatives.

By Condition: Osteoarthritis Scale Versus Oncology Growth

Osteoarthritis dominated 37.20% of revenue in 2025, buoyed by 595 million global sufferers. Yet bone tumors display the fastest 7.86% CAGR as early imaging and survivorship gains lift surgical intervention rates. PEEK cages increasingly replace titanium in metastatic spine cases, facilitating post-op radiotherapy with fewer artifacts. Orthopedic biomaterials market size for oncology uses remains modest today but draws R&D funding for patient-specific segmental replacements.

Trauma management stays essential in fast-growing cities, while osteoporosis devices gain ground among post-menopausal women facing fracture risk. Rheumatoid arthritis needs smaller, inflammation-resistant constructs, creating a micro-niche for thin-strut polyurethanes that minimize synovial abrasion.

Geography Analysis

North America held 39.90% of 2025 revenue, anchored by advanced surgical robotics and comprehensive insurance cover. The orthopedic biomaterials market benefits from technology showcases such as the VELYS robotic knee and KINCISE 2 automated hip system that refine component alignment. Yet payer documentation tightening and raw-material supply warnings issued by the FDA underscore profit-margin pressure. Hospital groups increasingly weigh device selection on lifetime value metrics, encouraging vendors to present cost-in-use evidence alongside clinical data.

Asia-Pacific posters an 7.98% CAGR to 2031 on the back of rapid aging and expanding middle-class insurance coverage. Domestic manufacturers scale additive manufacturing labs to cut import reliance, while governments streamline approval pathways for 3-D printed implants. Markets such as India roll out price ceilings to widen access, pushing multinationals to localize production and adjust channel strategies. Country-level diversity remains high, with Japan’s mature regulatory oversight contrasting with evolving frameworks in fast-growing Southeast Asian nations.

Europe grows steadily through 2030 as the EU Medical Device Regulation tightens traceability and accelerates eco-design mandates. Hospitals pilot cradle-to-grave tracking of orthopedic components, paving the way for higher biodegradable uptake. Middle East & Africa endorse public-private collaborations to raise theater capacity; the GCC alone spends USD 43.9 billion annually on medical devices. Latin America fosters clinical-trial tourism; Chile hosted 33 orthopedic device studies in 2023, up from 20 in 2021. Local manufacturing incentives in Brazil aim to narrow price gaps between imported and domestic knee implants, supporting regional supplier emergence.

Competitive Landscape

Competition is moderate-to-high, with the top eight firms spanning full portfolios while niche players exploit material or digital specializations. Stryker deepened capabilities by purchasing Artelon for synthetic graft augmentation and Vertos Medical for minimally invasive lumbar decompression. Zimmer Biomet broadened allergy-safe offerings with the Persona metal-alternate knee approved in March 2025. Johnson & Johnson invests in AI-guided navigation that links implant libraries with intra-operative analytics to differentiate on workflow efficiency.

Specialists such as Globus Medical push expandable cages that optimize endplate contact, while Exactech focuses on extremity systems where bespoke geometry outperforms standard shapes. Silicon-nitride pioneer Sintx leverages proprietary processing to deliver bacteriostatic surfaces in spinal interbodies, carving a premium niche. The orthopedic biomaterials industry also sees alliances between materials scientists and software vendors to embed sensor arrays that track healing strain, foreshadowing data-as-a-service monetization.

White-space lies in biodegradable load-bearing constructs and emerging-market price points. Talent shortages in bioprocess engineering and analytical testing pose barriers to scaling cell-based orthobiologics, as highlighted by the Alliance for Regenerative Medicine workforce survey. Vendors that cultivate manufacturing excellence, regulatory fluency, and sustainability credentials are best positioned to widen share through 2030.

Orthopedic Biomaterials Industry Leaders

Koninklijke DSM N.V

Zimmer Biomet

Stryker

Invibio Ltd

Evonik Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zimmer Biomet received FDA clearance for the Persona Revision SoluTion Femur, the first metal-alternative knee revision implant for patients sensitive to nickel, cobalt, and chromium.

- March 2025: Smith+Nephew unveiled the TESSA Spatial Surgery System, pending FDA clearance, to guide ACL reconstruction with real-time tracking and augmented reality.

- January 2025: Stryker divested its U.S. spine implant line to Viscogliosi Brothers, forming VB Spine and sharpening focus on core orthopedic innovations.

- January 2024: Enovis closed its USD 1 billion acquisition of LimaCorporate, adding 3-D printed Trabecular Titanium platforms to its reconstruction suite.

Global Orthopedic Biomaterials Market Report Scope

As per the scope, orthopedic biomaterial comprises ceramics, calcium phosphate cement, metals, and polymers, widely used in joint replacement, spine implants, Orth biologics, bioresorbable tissue fixation, and many more. The Orthopedic Biomaterials Market is Segmented By Material Type (Polymers, Ceramics & Bioactive Glasses, Calcium Phosphate Cement, Metal, and Others), By Application (Orthobiologics, Joint Replacement/Reconstruction, Viscosupplementation, Orthopedic Implants, Others), and Geography. (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| High-Performance Polymers |

| Ceramics and Bioactive Glasses |

| Calcium-Phosphate Cements |

| Metals and Metal Alloys |

| Others |

| Orthobiologics |

| Joint Reconstruction |

| Viscosupplementation |

| Spinal and Trauma Fixation Implants |

| Others |

| Non-Biodregradable Biomaterials |

| Biodegradable Biomaterials |

| Osteoarthritis |

| Osteoporosis |

| Bone Tumors |

| Rheumatoid Arthritis |

| Trauma Management |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | High-Performance Polymers | |

| Ceramics and Bioactive Glasses | ||

| Calcium-Phosphate Cements | ||

| Metals and Metal Alloys | ||

| Others | ||

| By Application | Orthobiologics | |

| Joint Reconstruction | ||

| Viscosupplementation | ||

| Spinal and Trauma Fixation Implants | ||

| Others | ||

| By Biodegradability | Non-Biodregradable Biomaterials | |

| Biodegradable Biomaterials | ||

| By Condition | Osteoarthritis | |

| Osteoporosis | ||

| Bone Tumors | ||

| Rheumatoid Arthritis | ||

| Trauma Management | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the orthopedic biomaterials market?

The market stands at USD 23.92 billion in 2026 and is projected to reach USD 33.65 billion by 2031.

Which material category dominates revenue?

High-performance polymers lead with 46.58% of 2025 sales, owing to versatility in joint and spinal implants.

Why are biodegradable implants gaining traction?

They eliminate secondary removal surgeries and support circular-economy goals, fueling an 7.88% CAGR through 2031.

Which region is growing fastest?

Asia-Pacific posts the highest regional CAGR at 7.98%, driven by demographic aging and expanded healthcare access.

What is the biggest restraint facing suppliers?

Reimbursement erosion from procedure down-coding reduces hospital spending power and pressures manufacturers to prove economic value.

How are companies differentiating in a competitive landscape?

Leaders integrate additive manufacturing, AI-enabled surgical guidance, and bioactive surface technologies to improve outcomes and capture share.

Page last updated on: