3D Bioprinted Human Tissue Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

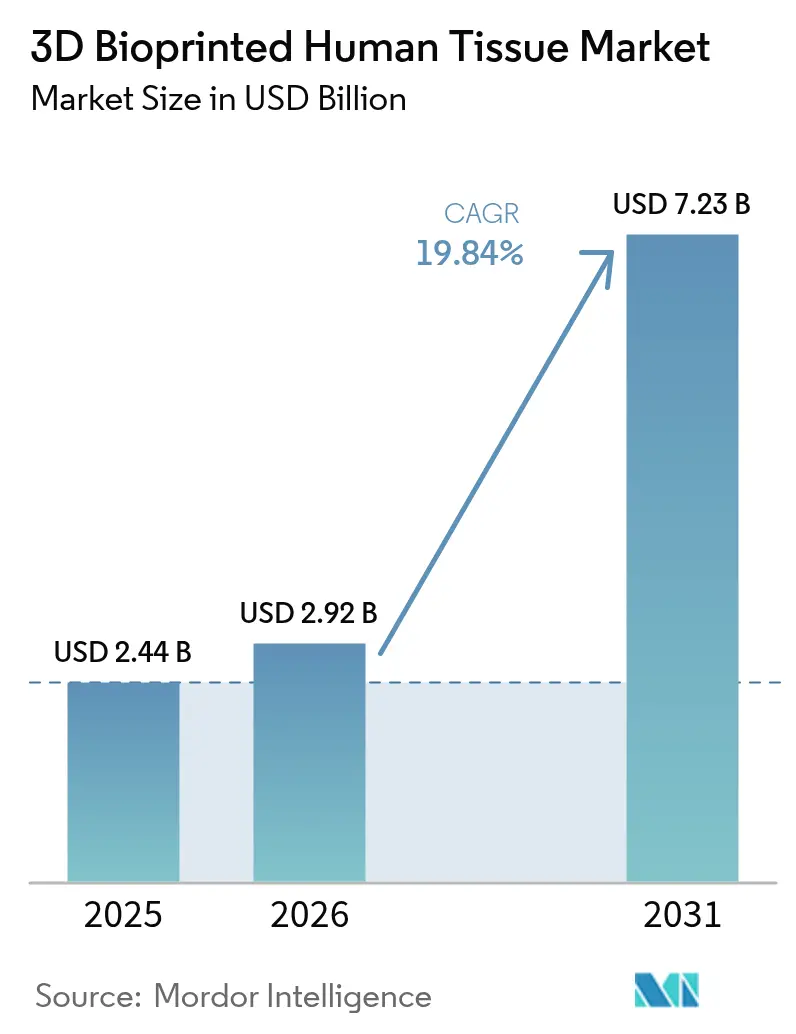

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 19.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

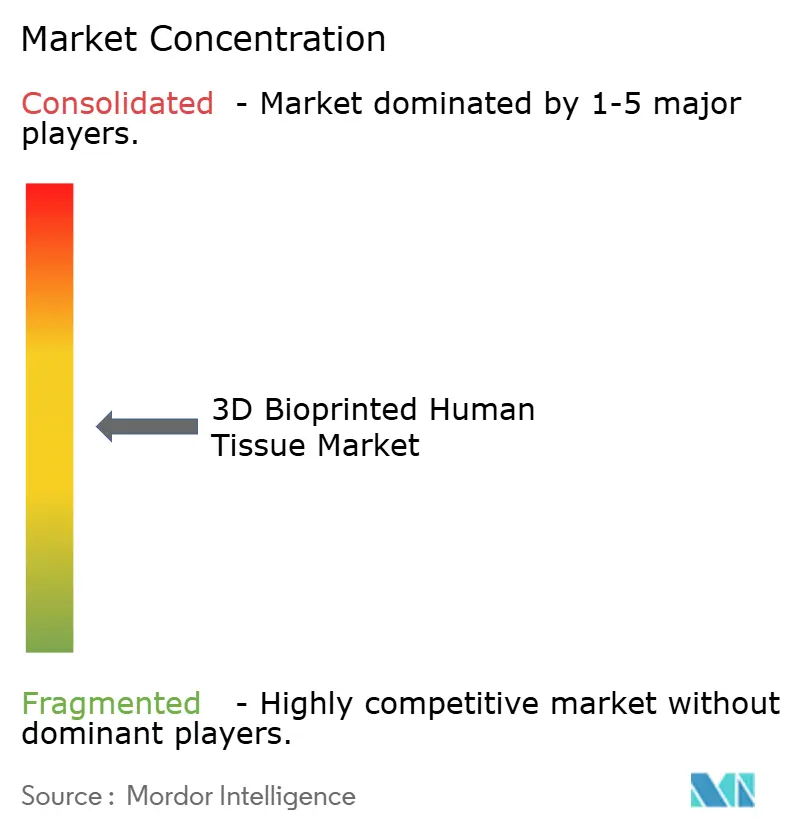

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

3D Bioprinted Human Tissue Market Analysis by Mordor Intelligence

The 3D bioprinted human tissue market size was valued at USD 2.44 billion in 2025 and estimated to grow from USD 2.92 billion in 2026 to reach USD 7.23 billion by 2031, at a CAGR of 19.84% during the forecast period (2026-2031). The current growth trajectory stems from clearer regulatory frameworks, rapid advances in stem-cell–based bioinks, and record venture funding that is pushing laboratory concepts toward routine clinical practice. In December 2024, the US FDA cleared PrintBio’s 3DMatrix, the first resorbable surgical mesh fabricated entirely by additive manufacturing, validating regulatory confidence in bioprinted medical devices. Europe is following suit; a refined Advanced Therapy Medicinal Products (ATMP) framework from the European Medicines Agency specifies classification routes for cell-laden constructs, lowering regulatory ambiguity for commercial developers. Large pharmaceutical groups are accelerating the adoption of printed tissue models to cut late-stage failure rates, while hospital systems view patient-specific implants as a long-term answer to transplant shortages. Collectively, these factors have shifted the narrative from proof-of-concept toward scalable manufacturing, opening substantial white-space opportunities for platform suppliers that can combine printing hardware, qualified bioinks, and regulatory documentation in a single package.

Key Report Takeaways

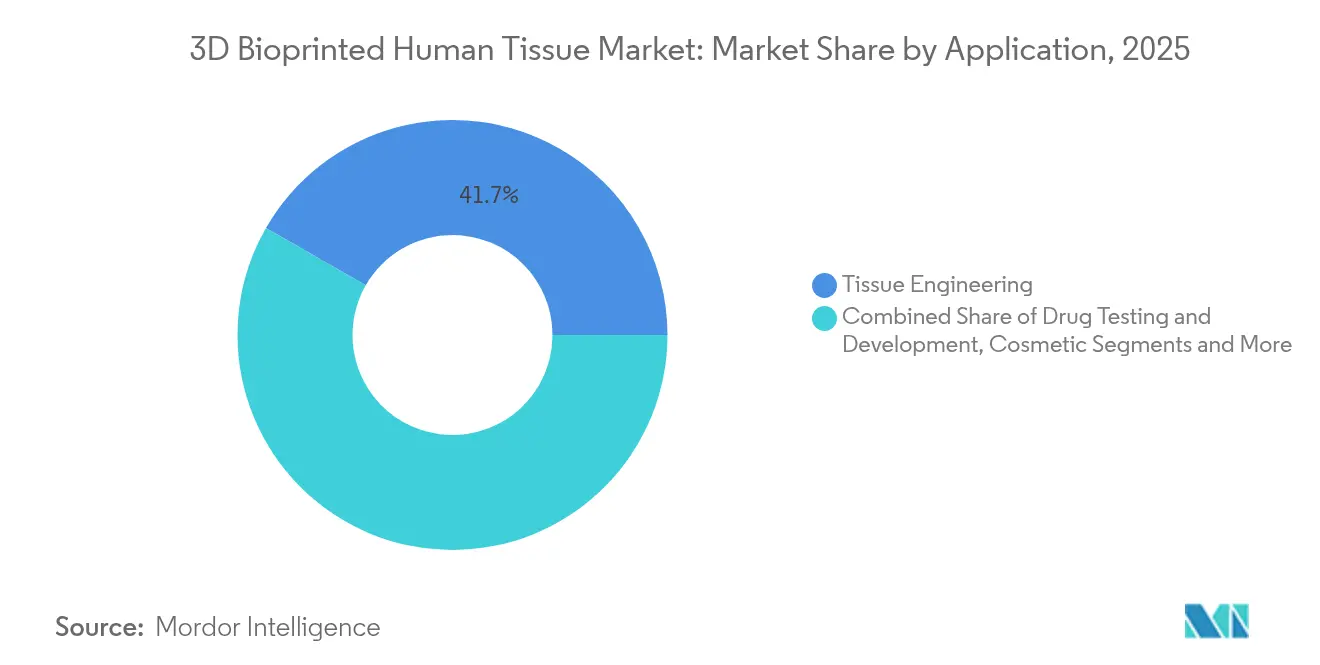

- By application, tissue engineering led with 41.72% revenue in 2025, whereas drug testing and development are projected to expand at a 27.85% CAGR through 2031.

- By technology, extrusion systems held the top 37.54% share in 2025; hybrid/4D systems record the fastest 30.15% CAGR to 2031.

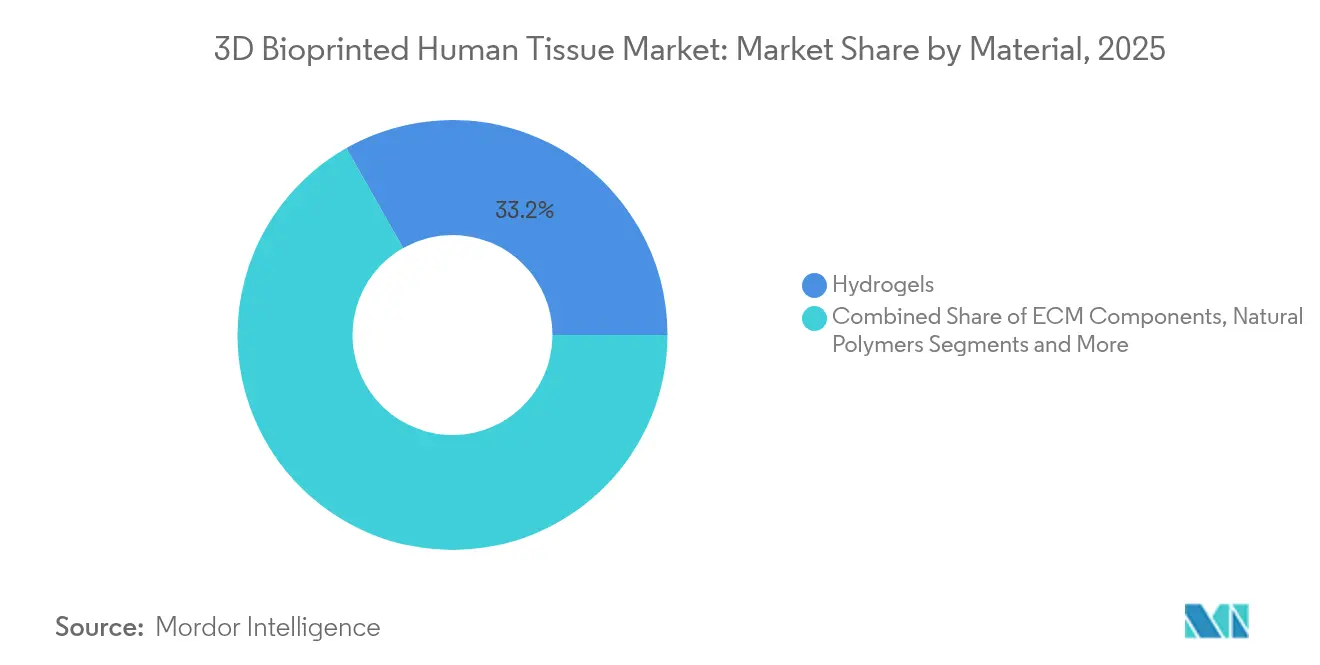

- By material, hydrogels commanded 33.22% of the 3D bioprinted human tissue market share in 2025, while living-cell bioinks grew at a 26.1% CAGR.

- By end-user, pharmaceutical and biotechnology companies captured 46.15% of the 3D bioprinted human tissue market size in 2025 and are advancing at a 24.9% CAGR.

- By region, North America maintained a 48.55% share in 2025; Asia Pacific posts the fastest 22.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Bioprinted Human Tissue Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for regenerative medicine solutions | +4.20% | North America & Europe | Long term (≥ 4 years) |

| Escalating investment in bioprinting R&D | +3.80% | North America & Europe; spill-over to Asia Pacific | Medium term (2-4 years) |

| Advances in stem-cell and biomaterial technologies | +3.10% | US, Germany, Japan | Medium term (2-4 years) |

| Strategic collaborations and industry partnerships | +2.70% | Global pharma hubs | Short term (≤ 2 years) |

| Government funding and grant initiatives | +2.40% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Rising prevalence of chronic disease and trauma injuries | +2.90% | Ageing high-income markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Regenerative Medicine Solutions

Organ shortages now leave more than 100,000 patients on US transplant waiting lists, prompting regulators to endorse translational research that can create functional tissue substitutes.[1]National Academies of Sciences, “Report on Organ Shortage and Bioprinting Solutions,” nationalacademies.org The FDA’s December 2024 clearance of Symvess, an acellular tissue-engineered vessel for vascular trauma, underscored this shift toward printed grafts. Japan’s Kyoto University Hospital subsequently reported 100% sensory improvement 48 weeks after autologous Bio 3D nerve conduit implantation, marking the first human trial of a fully printed peripheral-nerve graft. Vascularization remains the main biological hurdle; Carnegie Mellon University’s FRESH printing method now builds perfusable constructs at the organ scale, greatly improving nutrient diffusion and cell survival. As regulatory clarity rises and clinical success stories mount, regenerative medicine will remain the single most powerful growth catalyst over the next decade.

Escalating Investment in Bioprinting Research and Development

Series-B and Series-C funding rounds routinely surpass USD 50 million, led by Aspect Biosystems, which announced CAD 165 million (USD 120 million) for printed-tissue therapeutics in January 2025. Nuclera raised USD 75 million in October 2024 for its desktop protein bioprinter, reflecting a broader move to shrink printing platforms onto benchtops while maintaining GMP capabilities. Pharmaceutical alliances add non-dilutive capital; CN Bio’s multi-year organ-on-chip collaboration with Pharmaron is expected to integrate printed liver, lung, and gut models into global discovery workflows. Capital intensity is therefore no longer a prohibitive barrier for agile innovators, but access to scale-up funds now determines competitive positioning.

Advances in Stem-Cell and Biomaterial Technologies

Stony Brook University’s TRACE process demonstrated direct writing of collagenous elements with physiological architecture, merging mechanical integrity with biofunctionality in a single pass. Concurrently, partnerships between FluidForm and Merck showed higher viability for induced-pluripotent-stem-cell-derived cardiomyocytes, signaling a step toward functional myocardium patches. On the materials side, UPM Biomedicals introduced FibGel, a birch-wood-derived nanocellulose hydrogel that meets regulatory requirements for renewable sourcing without sacrificing print fidelity. These converging breakthroughs lower the cost per construct while broadening the palette of bioactive inks.

Increasing Strategic Collaborations and Industry Partnerships

CollPlant’s rhCollagen bio ink is being combined with Stratasys’ polymer printers to develop resorbable breast implants aimed at a USD 3 billion reconstruction market, highlighting how joint development shortens time-to-clinic. Organovo monetized non-core liver assets via a USD 10 million intellectual property sale to Eli Lilly in February 2025, using cash inflows to accelerate high-margin kidney programs. As regulatory expectations tighten, bioprinting specialists increasingly pursue revenue-sharing deals with pharma groups that can fund pivotal trials and navigate global distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs | -2.80% | Global; acute in emerging markets | Medium term (2-4 years) |

| Regulatory and ethical uncertainty | -2.10% | Varies by jurisdiction | Long term (≥ 4 years) |

| Manufacturing scale-up and standardization gaps | -1.90% | Commercial applications worldwide | Medium term (2-4 years) |

| Shortage of skilled workforce | -1.60% | Severe in APAC & emerging regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of Bioprinting Platforms

Industrial-grade printers range between USD 500,000 and USD 2 million, while GMP-compliant cleanrooms add multimillion-dollar overheads, limiting entry by small institutes. Proprietary bioinks often cost 10-50× standard media, and shortages of experienced tissue-engineering scientists inflate labor budgets. Contract development and manufacturing organizations (CDMOs) are emerging to spread CapEx across multiple clients, exemplified by Biological Lattice Industries’ pay-per-print model launched after a USD 1.8 million seed round. Even so, investors remain cautious until equipment-as-a-service models achieve meaningful utilization rates.

Regulatory and Ethical Uncertainty Surrounding Bioprinted Tissues

The EU’s ATMP regulation classifies constructs by cellular content, scaffolding, and intended use, forcing developers to prepare multiple dossiers before final product designation.[2]European Medicines Agency, “Advanced Therapy Medicinal Products: Updated Framework,” ema.europa.eu In the United States, draft FDA guidance outlines performance-based testing for printed implants but has yet to propose standardized validation for living tissues, extending timelines for complex products.[3]US Food & Drug Administration, “FDA Clears PrintBio 3DMatrix Resorbable Surgical Mesh,” fda.gov Ethical debates over patient-specific stem cells add review cycles in certain jurisdictions, especially where genetic editing might be involved. Lack of harmonized global standards, therefore, prolongs cross-border trials and increases compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Drug Testing Redefines Commercial Priorities

Drug testing and development captured 27.85% CAGR through 2031, eroding the historical dominance of tissue engineering that still accounts for the largest absolute revenue pool. Pharmaceutical users increasingly cite bioprinted liver and gut models as key to cutting attrition in late-stage trials, a shift reinforced by regulatory pressure to reduce animal studies. POSTECH’s artificial lung model exemplifies how printed constructs replicate disease states more faithfully than two-dimensional cell cultures, accelerating antiviral research. Cosmetic and reconstructive surgery applications gained momentum once CollPlant successfully printed 200 cc breast implants, moving aesthetic indications from concept to pre-clinical validation. Food safety and cultured-protein applications remain small but highly publicized following the FDA’s first pre-market consultation on cell-based foods in July 2025.

Rising adoption in pharmacology has reshaped supplier roadmaps: many platform providers now bundle printer hardware with validated liver, cardiac, and kidney bioinks to target CROs and pharma innovation centers. These end-users demand multi-tissue arrays that allow parallel testing of toxicity, metabolism, and efficacy across organ systems. Meanwhile, regenerative orthopedics continues to secure public grants as governments seek printed cartilage and bone grafts that reduce donor-site morbidity. Collectively, application diversification supports a broad revenue base, though near-term margin expansion is concentrated in contract drug-testing services.

By Technology: Hybrid Systems Challenge Extrusion Dominance

Extrusion printers still generated 37.54% of 2025 revenue because of proven reliability, broad material compatibility, and favorable cost-of-ownership. Nonetheless, hybrid and 4D configurations are growing 30.15% a year as they combine extrusion with light-based curing or acoustic positioning to deposit multiple bioinks with microscale precision. Stanford University used algorithm-generated vascular lattices to accelerate print times 200-fold, illustrating why hybrid platforms excel at perfusable tissues. Ink-jet modalities maintain relevance in high-throughput screening, while laser-assisted systems dominate applications requiring <20 µm resolution such as corneal stroma.

In vivo printing technologies, such as Caltech’s ultrasound-guided deposition, highlight a future where therapeutic material is formed directly inside patients, bypassing graft maturation ex vivo. Printer OEMs now integrate closed-loop imaging and AI-driven feedback to correct deposition in real time, enhancing construct fidelity and reducing batch failure. As validation datasets accumulate, industry analysts expect hybrid printers to overtake extrusion for high-value therapeutic tissues before 2030, though extrusion retains an edge in low-complexity scaffolds and educational markets.

By Material: Living Cells Narrow the Gap With Hydrogels

Hydrogels retained 33.22% revenue share in 2025, supported by deep regulatory familiarity and scalable manufacturing. Innovations such as UPM’s nanocellulose FibGel show the category’s adaptability, offering renewable feedstock and tunable mechanical strength. The living-cell segment, however, is expanding 26.1% annually as stem-cell viability rises above 90% post-print, making functional constructs feasible for clinical implantation. Extracellular-matrix-based bioinks deliver biochemical cues that enhance cell maturation and are gaining traction in cardiac and hepatic models.

Programmable living materials now incorporate genetically-engineered cells that respond to biochemical or optical triggers, adding therapeutic function beyond structural repair. Synthetic polymers remain indispensable for load-bearing orthopedic implants, while natural polymers such as alginate dominate low-temperature extrusion applications. Advanced bioinks increasingly blend multiple material classes to balance mechanical integrity, biodegradability, and cellular compatibility. Suppliers able to certify material provenance and endotoxin levels gain preferred-vendor status among GMP facilities.

By End-User: Pharmaceutical Firms Anchor Demand

Pharmaceutical and biotechnology companies accounted for 46.15% of 2025 revenue and continue to post a 24.9% CAGR. Their purchasing criteria emphasize validated multi-organ panels, throughput, and regulatory documentation aligned with ICH safety guidelines. Academic institutes, once the primary customers, now focus on early-stage innovation rather than volume purchases, although they still influence material-science breakthroughs. Hospitals remain a small but strategic segment as printed implants secure more device clearances; early adopters are large teaching centers with in-house clinical research units.

Contract research organizations integrate bioprinted models into toxicology and ADME workflows, creating recurring consumable demand. Equipment vendors increasingly provide service contracts that bundle printer leasing, reagent subscriptions, and regulatory-compliance support. The resulting ecosystem blurs traditional supplier-client lines, with several pharma companies investing directly in printer start-ups to secure supply of bespoke tissues for pipeline candidates.

Geography Analysis

North America contributed 48.55% of global revenue in 2025, underpinned by the FDA’s proactive stance on printed devices and a venture ecosystem that routinely funds nine-digit rounds. Academic centers at Stanford, Carnegie Mellon, and the University of Pittsburgh anchor intellectual property output, while companies such as Redwire leverage microgravity bioprinting on the International Space Station to solve vascularization challenges in organ fabrication. Federal grants from the National Institutes of Health complement private venture capital, ensuring a balanced funding mix even as operational costs and talent shortages persist.

Europe ranks second in value thanks to a harmonized ATMP pathway and generous Horizon Europe funding calls. Germany’s machine-tool heritage accelerates adoption in industrial biomedical printing, whereas the United Kingdom’s post-Brexit regulatory regime maintains alignment with EMA quality benchmarks to preserve market access. Scandinavian nations champion sustainable bio-based inks, reflecting broader EU green-deal ambitions that favor circular-economy solutions in medical manufacturing.

Asia Pacific posts the fastest 22.4% CAGR through 2031, propelled by China’s Five-Year Plan incentives for biomanufacturing and the rapid licensing of hospital-based printing labs. Japan’s aging population drives demand for cartilage and vascular grafts, leveraging local excellence in materials science. South Korea applies consumer-electronics precision to desktop bioprinters, while India grows as an outsourcing hub for cost-sensitive pre-clinical testing. Regional challenges include patchy IP enforcement and varying ethical guidelines, yet localized manufacturing clusters are emerging around Shanghai, Yokohama, and Bengaluru.

Competitive Landscape

Market structure remains moderately fragmented. BICO retains a broad portfolio across printers, bioinks, and automation, reporting SEK 2.2 billion in 2025 revenue. Stratasys extends polymer expertise into medical implants via CollPlant’s rhCollagen inks, illustrating how traditional additive leaders partner for biological know-how. Enovis’ EUR 800 million acquisition of LimaCorporate adds 3D-printed titanium orthopedics, signaling vertical integration among device majors.

Start-ups differentiate through platform specialization: Aspect Biosystems focuses exclusively on printed pancreatic and liver tissues, while Biological Lattice Industries competes on affordability through modular printers priced below USD 100,000. Pharmaceutical firms such as Eli Lilly acquire IP blocks—Organovo’s FXR liver model—securing exclusive disease models and reinforcing supplier dependence. Competitive advantage increasingly shifts from raw print speed to validated clinical data sets and regulatory dossiers.

Strategic alliances serve as force multipliers. CN Bio’s tie-up with Pharmaron embeds printed organ-on-chip models into global discovery pipelines, creating high-volume reagent pull-through. CollPlant and Stratasys co-develop implants, sharing development risk while accessing each other’s distribution. Overall, industry players that combine robust IP, scalable GMP manufacturing, and multidomain collaborations command premium valuations.

3D Bioprinted Human Tissue Industry Leaders

-

Organovo

-

Stratasys Ltd.

-

Prellis Biologics

-

Materialise NV

-

Oceanz 3D printing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stanford researchers generated vascular networks 200× faster than previous iterations, enabling rapid fabrication of organ-scale constructs.

- June 2025: Stony Brook University unveiled the TRACE process for direct collagen printing with native-like architecture.

- May 2025: Caltech demonstrated ultrasound-guided in vivo 3D printing for localized drug and cell delivery.

- April 2025: CN Bio signed a long-term organ-on-chip collaboration with Pharmaron to integrate printed tissues into global drug-discovery workflows.

- February 2025: Enovis completed the EUR 800 million acquisition of LimaCorporate to expand its 3D-printed orthopedic portfolio.

Global 3D Bioprinted Human Tissue Market Report Scope

3D bioprinted human tissue refers to tissue made by 3D bioprinting. A 3D bioprinter uses a layer-by-layer 3D bioprinting method, depositing bioinks or biomaterials to create 3D tissues or structures used for medicine or tissue engineering. This technology is being applied to regenerative medicine to address the need for tissues and 3D-printed organs for transplant.

The 3D Bioprinted Human Tissue Market is Segmented by Application (Tissue Engineering, Cosmetic Surgery, Drug Testing and Development, Food Testing, and Other Application Types) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value in USD million for the above segments.

| Tissue Engineering |

| Drug Testing & Development |

| Cosmetic & Reconstructive Surgery |

| Food Safety & Novel Foods |

| Other Applications |

| Extrusion-based |

| Ink-jet |

| Laser-Assisted |

| Microfluidic & Acoustic |

| Magnetic Levitation |

| Hybrid / 4D |

| Living Cells |

| Hydrogels |

| Extracellular-Matrix Components |

| Synthetic Polymers |

| Natural Polymers |

| Others |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Hospitals & Surgical Centres |

| Contract Research Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Tissue Engineering | |

| Drug Testing & Development | ||

| Cosmetic & Reconstructive Surgery | ||

| Food Safety & Novel Foods | ||

| Other Applications | ||

| By Technology | Extrusion-based | |

| Ink-jet | ||

| Laser-Assisted | ||

| Microfluidic & Acoustic | ||

| Magnetic Levitation | ||

| Hybrid / 4D | ||

| By Material | Living Cells | |

| Hydrogels | ||

| Extracellular-Matrix Components | ||

| Synthetic Polymers | ||

| Natural Polymers | ||

| Others | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Hospitals & Surgical Centres | ||

| Contract Research Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the 3D bioprinting market?

The 3D bioprinting market is valued at USD 2.92 billion in 2026 and is projected to reach USD 7.23 billion by 2031.

Which segment is growing the fastest?

Drug testing and development applications are expanding at a 27.85% CAGR, outpacing all other use cases as pharmaceutical companies pivot toward printed tissue models for preclinical studies.

Why are hybrid bioprinters gaining popularity?

Hybrid and 4D systems integrate multiple deposition and curing techniques, enabling dynamic tissue responses and faster vascularization, which drives a 30.15% CAGR through 2031.

Which region offers the highest growth potential?

Asia Pacific leads in growth with a 22.4% CAGR, supported by Chinese industrial policy, Japanese materials science, and expanding healthcare investment across the region.

What are the primary barriers to wider adoption?

High capital costs for GMP facilities, regulatory complexity across jurisdictions, and shortages of skilled bioprinting scientists collectively restrain rapid commercial scale-up.

Page last updated on: