Tissue Sectioning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

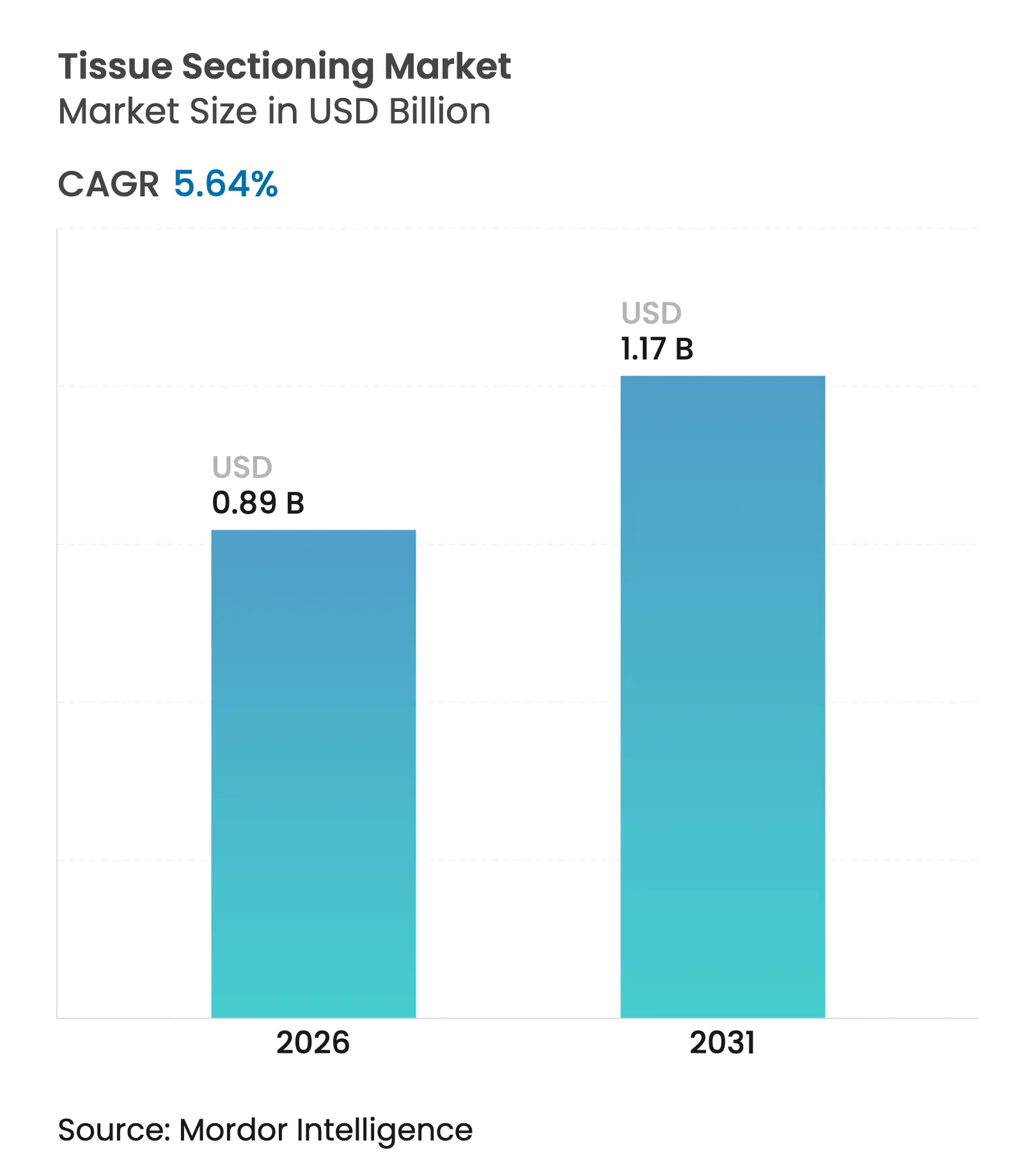

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 5.64 % CAGR |

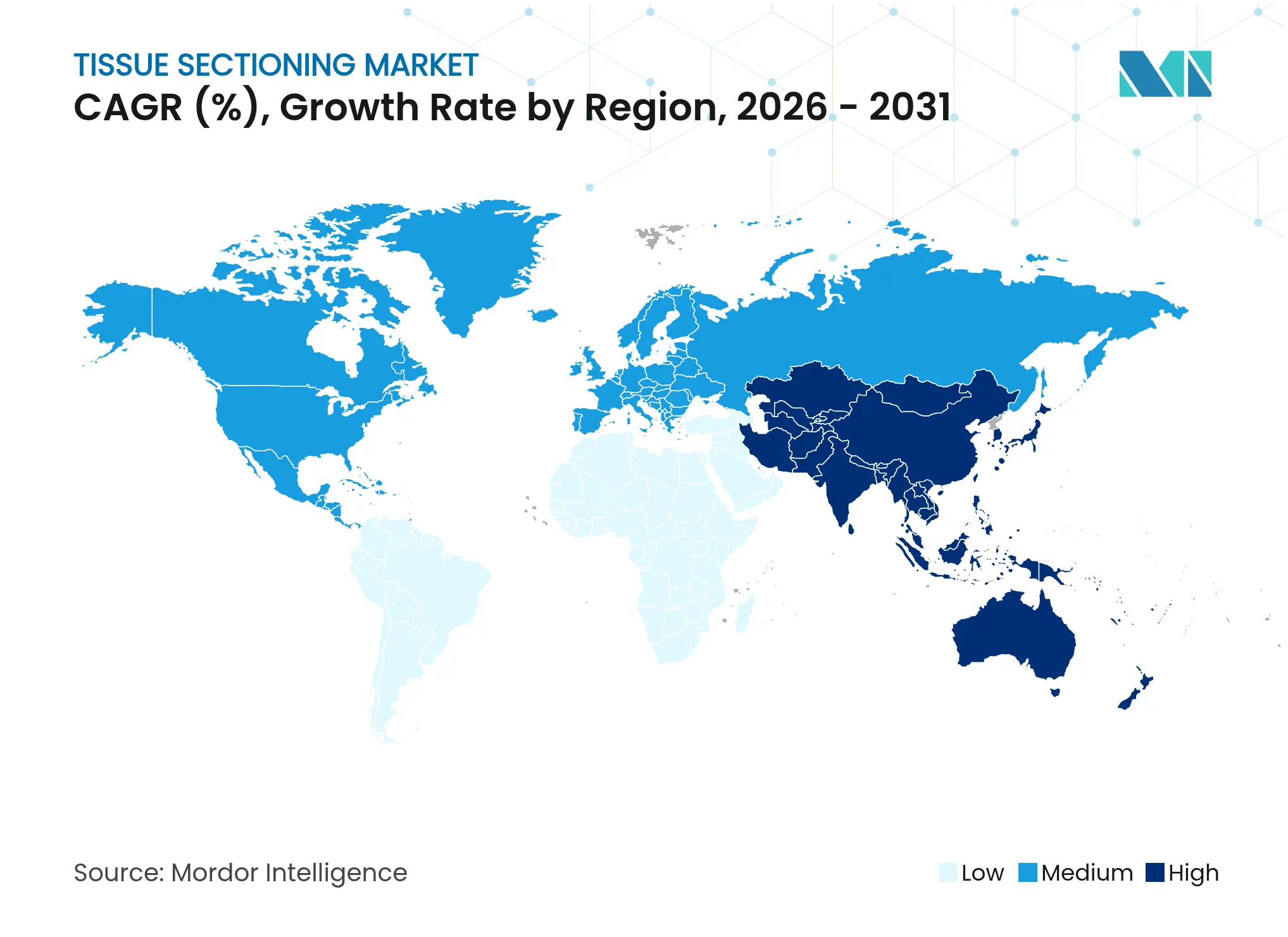

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Tissue Sectioning Market Analysis by Mordor Intelligence

The tissue sectioning market size was valued at USD 0.84 billion in 2025 and estimated to grow from USD 0.89 billion in 2026 to reach USD 1.17 billion by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). Robust demand stems from oncology’s shift toward high-throughput, AI-enabled histology, the growing penetration of automated microtomy, and regulatory clarity that accelerates digital pathology adoption. Intensifying cancer incidence, with about 20 million new cases in 2022 and a projected 35 million by 2050, is magnifying slide-volume requirements and underpinning long-term capital spending on automated sectioning platforms. Workforce shortages—histotechnologist vacancy rates reached 8.37% in 2024—are another structural catalyst pushing laboratories toward robotics, predictive maintenance, and “dark-lab” concepts that promise quality gains at lower operating cost. Vendors able to integrate spatial biology and AI analytics directly into sectioning hardware are carving durable competitive moats as precision medicine and companion diagnostics become mainstream. North America presently dominates the tissue sectioning market with 41.56% revenue contribution, but Asia-Pacific is the fastest-growing arena, expanding at a 6.54% CAGR due to rapid infrastructure build-outs and a rising cancer burden.

Key Report Takeaways

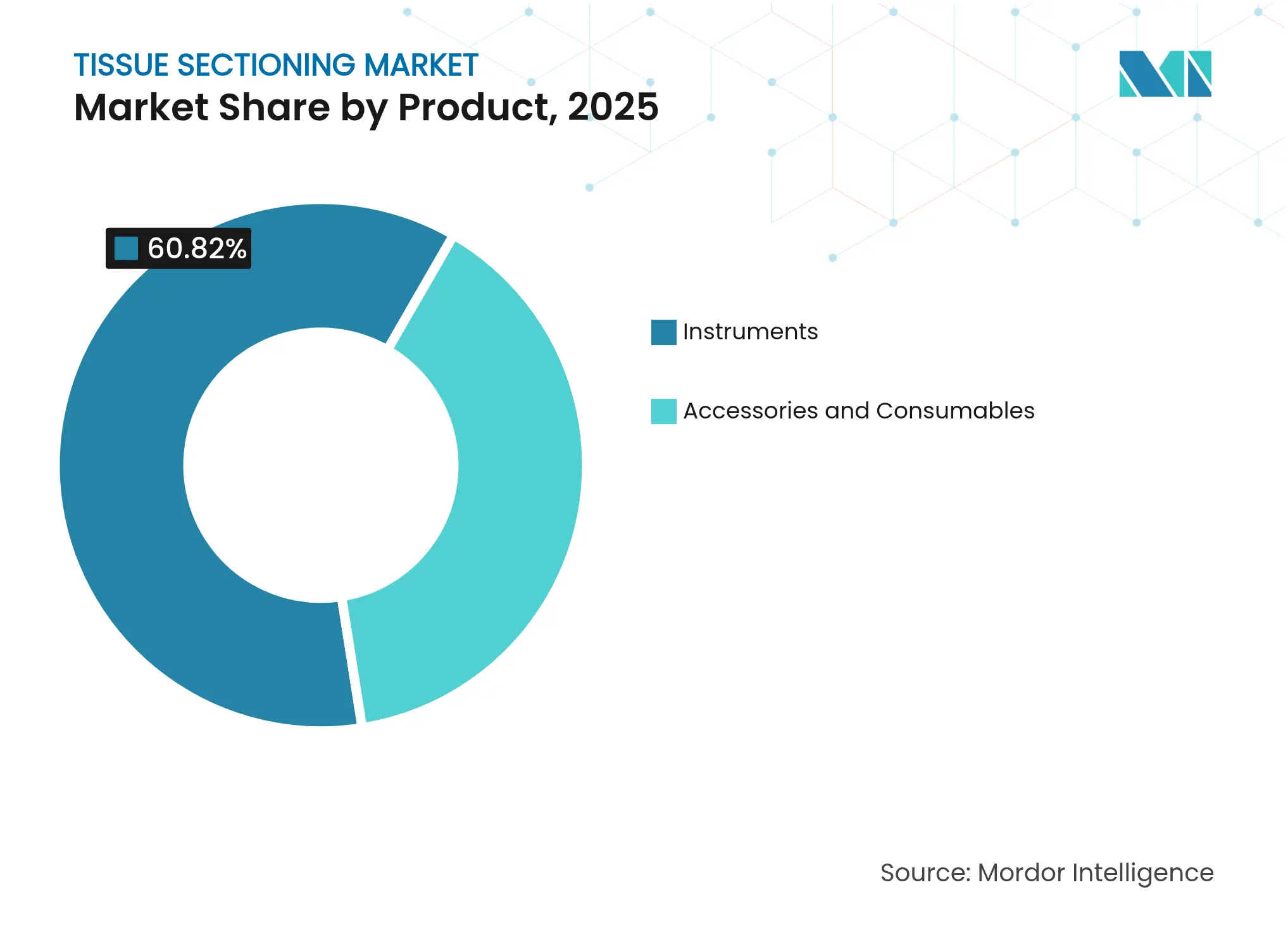

- By product, instruments captured 60.82% revenue share in 2025; accessories and consumables are projected to rise at a 7.34% CAGR through 2031.

- By technology, automatic systems held 48.10% of the tissue sectioning market share in 2025, while the same category posts the swiftest 7.62% CAGR to 2031.

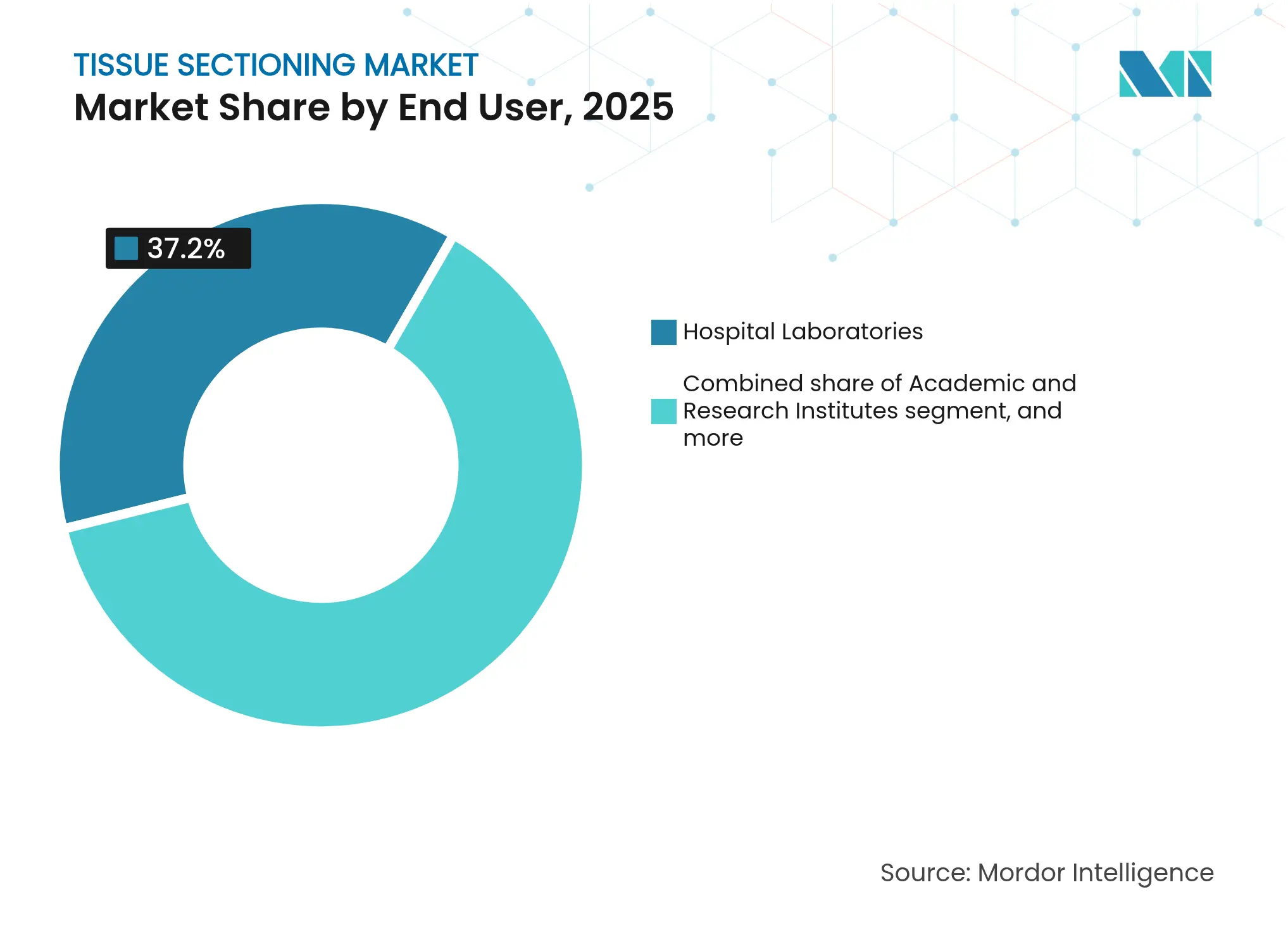

- By end user, hospital laboratories commanded 37.20% share of the tissue sectioning market size in 2025, whereas contract research organizations record the highest 8.21% CAGR through 2031.

- By application, disease diagnosis accounted for a 71.85% share of the tissue sectioning market in 2025 and research applications are advancing at an 8.55% CAGR toward 2031.

- By geography, North America led with 41.10% revenue share in 2025; Asia-Pacific is forecast to accelerate at a 6.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tissue Sectioning Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Incidence Of Cancer Worldwide Rising Incidence Of Cancer Worldwide | +1.8% | Global, highest in aging populations across North America, Europe, Asia-Pacific | Long term (≥ 4 years) | % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, highest in aging populations across North America, Europe, Asia-Pacific | Impact Timeline:Long term (≥ 4 years) |

Growing Adoption Of Precision Medicine And Companion Diagnostics Growing Adoption Of Precision Medicine And Companion Diagnostics | +1.2% | North America and EU leading, Asia-Pacific following | Medium term (2–4 years) | |||

Technological Advancements In Tissue Sectioning And Digital Pathology Systems Technological Advancements In Tissue Sectioning And Digital Pathology Systems | +1.0% | Global, early uptake in developed markets | Medium term (2–4 years) | |||

Increasing Healthcare Expenditure And Laboratory Automation Investments Increasing Healthcare Expenditure And Laboratory Automation Investments | +0.8% | Asia-Pacific core, spill-over to Middle East & Africa and South America | Long term (≥ 4 years) | |||

Expansion Of Diagnostic Infrastructure In Emerging Economies Expansion Of Diagnostic Infrastructure In Emerging Economies | +0.6% | Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) | |||

Government Funding And Reimbursement Support For Histopathology Services Government Funding And Reimbursement Support For Histopathology Services | +0.4% | Primarily North America and EU | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Cancer Worldwide

Escalating cancer prevalence is the single largest volume driver for the tissue sectioning market. Lung malignancies alone generated 2.5 million diagnoses in 2022, topping incidence and mortality tables. This momentum is not merely quantitative; precision oncology protocols now demand higher slide numbers per case to support multiplex biomarker panels. The American Cancer Society expects more than 2 million new U.S. cases in 2025, sustaining pressure on histology capacity[1]American Cancer Society, “Global Cancer Facts & Figures 2024,” cancer.org. Regional variability is stark—Australia shows the highest per-capita rates, while Western Africa remains lowest—leading vendors to stagger inventory and training strategies. Automated microtome suppliers gain the most from this throughput surge because laboratories must reconcile volume growth with shrinking staff pools.

Growing Adoption of Precision Medicine and Companion Diagnostics

Precision medicine workflows are shrinking acceptable tissue input while widening analytical breadth. Guardant360 Tissue, launched in 2025, delivers DNA-RNA profiling while requiring 40% fewer slides, illustrating labs’ need to extract maximum data from minimal biopsies. Spatial biology combinations, such as Bio-Techne’s protease-free RNAscope workflow, merge morphology with multiomics, expanding adjacent revenue pools for sectioning consumables and imaging-embedded instruments. As antibody-drug conjugates proliferate, pathology demands quantitative rather than subjective scoring; integrated slide scanners within microtomes are gaining favor to support algorithmic HER2 or PD-L1 assessment. Medicare’s reimbursement of complex molecular panels lowers financial barriers, further lifting utilization.

Technological Advancements in Tissue Sectioning and Digital Pathology Systems

FDA’s 2023 decision to classify digital pathology algorithms as Class II devices unlocked a clearer 510(k) pathway, encouraging rapid software innovation. The result is a pipeline of platforms, such as PathPresenter’s 2025-cleared Clinical Viewer, that bolt onto sectioning hardware for end-to-end digitization. Robotics vendors like Clarapath secured USD 36 million to commercialize SectionStar, an autonomous microtome that converts paraffin blocks to finished slides with minimal human touch. Stanford’s microDicer and microGrater prototypes push precision to sub-millimeter dissection, paving the way for uniform organoid preparation in drug screening. AI is migrating from image analysis to equipment self-calibration and predictive maintenance, compelling buyers to treat software roadmaps as core procurement criteria.

Increasing Healthcare Expenditure and Laboratory Automation Investments

National funding vehicles are underwriting infrastructure upgrades. The U.S. NIH Basic Instrumentation Grant offers up to USD 350,000 for high-spec ultramicrotomes, accelerating academic adoption[2]National Institutes of Health, “S10 Basic Instrumentation Grant,” nih.gov. NSW Government approved a statewide pathology hub at Westmead in June 2025, showcasing public-sector commitment to centralized, automated diagnostics[3]NSW Government, “Statewide Pathology Hub Announcement,” health.nsw.gov.au. Automation promises tangible savings: vendors cite 10–15% lower operating costs and 20–30% shorter turnaround times once manual trimming and slide drying are replaced by conveyor-based workflows. Dark-lab pilots illustrate how continuous-flow tissue sectioning can overcome staff shortages without compromising quality metrics.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost Of Advanced Tissue Sectioning Instruments And Maintenance High Cost Of Advanced Tissue Sectioning Instruments And Maintenance | -1.4% | Global, strongest in emerging markets and small laboratories | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, strongest in emerging markets and small laboratories | Impact Timeline:Medium term (2–4 years) |

Shortage Of Skilled Histotechnologists And Pathologists Shortage Of Skilled Histotechnologists And Pathologists | -0.9% | North America and EU first, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

Stringent Regulatory And Quality Compliance Requirements Stringent Regulatory And Quality Compliance Requirements | -0.6% | Global, most stringent in EU and U.S. markets | Medium term (2–4 years) | |||

Proliferation Of Alternative Non-Invasive Diagnostic Modalities Proliferation Of Alternative Non-Invasive Diagnostic Modalities | -0.5% | Global, particularly in developed healthcare systems | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Advanced Tissue Sectioning Instruments and Maintenance

Automated platforms command premium pricing compounded by semiconductor and medical-grade polymer shortages. Smaller labs often lack capital budgets for USD 200,000 microtomy suites and face protracted return-on-investment cycles. Inflationary pressure on ethylene oxide sterilization sharpens cost burdens, pushing many independent practices toward mergers that create scale in procurement. Vendors are countering with leasing, consumables-bundled subscriptions, and software-as-a-service updates that spread payments while ensuring regulatory compliance. Yet uptake remains sluggish in low-income geographies where diagnostic demand rises fastest, limiting near-term penetration.

Shortage of Skilled Histotechnologists and Pathologists

Retirement of 27.13% of supervisory staff by 2028 will deepen an existing skills gap. Training pipelines cannot replenish the deficit quickly; in the U.K., only 3% of departments meet staffing benchmarks, echoing shortages evident in Canada and Germany. Rural regions endure week-long slide backlogs, eroding clinician confidence and amplifying burnout. Automation alleviates workload but initial deployment requires experienced technologists—a paradox that lengthens rollout timelines. Credentials vary across jurisdictions, restricting worker mobility that might otherwise ease hot-spot strain.

Segment Analysis

By Product: Instruments Dominate Amid Consumables Momentum

In 2025 instruments accounted for 60.82% of revenue, anchoring the tissue sectioning market. Rotary and cryostat microtomes remain indispensable for routine and frozen diagnostics, while ultramicrotomes ride a research resurgence in neuroscience and materials science. Demand for single-use blades, microtome adhesive films, and embedding cassettes is rising faster than capital equipment because throughput expansion magnifies consumables burn rate. Accessories and consumables expand at a 7.34% CAGR, highlighting a strategic pivot to recurring revenue streams and post-installation service contracts. Vendors embed RFID tracking in cassettes and slides to curb specimen mix-ups, supporting regulatory compliance and chain-of-custody documentation. Tissue processors now feature cloud dashboards that alert users to reagent exhaustion, minimizing downtime. Integrated paraffin dispensers and slide dryers reduce manual handling, a critical benefit when staff turnover is high. As laboratories embrace lean methodologies, consumables-bundled service agreements offer predictable cost structures and inventory assurance.

The digital adjacency widens margins: scanner-ready slides with barcodes integrate smoothly into AI workflows, while pre-analytical QC dyes help software identify tissue folds. Companies offering proprietary blade geometries lock in customers through performance claims tied to equipment warranties. Environmental regulations spur interest in low-xylene reagents, opening green premium niches. Collectively these trends suggest that consumables growth will outpace hardware upgrades beyond 2030, further shifting vendor focus toward lifetime value rather than one-time sales.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Automation Becomes the New Normal

Automatic systems held 48.10% of tissue sectioning market share in 2025 and simultaneously register the fastest 7.62% CAGR, underscoring a decisive pivot toward lights-out workflows. Integrated diagnostic chains that link cassette printing, block trimming, slicing, and slide labeling improve reproducibility and reduce error rates to below 0.2%. Semiautomatic models serve price-sensitive buyers upgrading from manual tools; many platforms are modular, allowing incremental automation as budgets permit. Manual microtomes persist mainly in teaching settings and field hospitals but are losing ground each budget cycle.

AI overlays now calibrate blade angle and slice thickness in real time, reacting to paraffin hardness variations that once demanded expert judgment. Predictive maintenance algorithms flag impending motor wear weeks before failure, boosting uptime beyond 98%. Software-defined instruments also ease regulatory submissions because firmware updates can address performance deviations without mechanical intervention. Laboratories benchmark return on investment not only on labor savings but also on measurable quality—automation reduces repeat cuts and slide recolor, saving consumables. As cloud connectivity becomes standard, cybersecurity certification emerges as a purchase criterion, especially for hospital IT departments wary of ransomware exposure.

By End User: Hospitals Hold Sway While CROs Surge

Hospital laboratories retained 37.20% of revenue in 2025, benefiting from proximity to clinicians and insurance reimbursement flows. These labs are under acute staffing pressure, motivating early adoption of high-capacity inline sectioning gear that can process ≥ 1,200 blocks per shift. In contrast, contract research organizations enjoy the fastest 8.21% CAGR as pharmaceutical pipelines expand biomarker-rich oncology assets requiring specialized tissue analytics. CROs differentiate with GLP-compliant digital chains and rapid turnaround, often guaranteed within 48 hours. Academic and research institutes remain innovation testbeds, validating emerging spatial techniques and feeding discoveries into commercial vendor pipelines. Clinical reference labs operate as volume hubs for small hospitals, often negotiating national consumables contracts that influence supplier share.

Outpatient surgery centers represent an incipient niche; their growth aligns with value-based care models that push procedures outside hospitals. These centers favor compact, user-friendly microtomes because histology is ancillary to surgical throughput. Across all end users, procurement decisions increasingly hinge on interoperability with lab information systems and AI viewers, favoring vendors with open APIs and strong cybersecurity postures.

Note: Segment shares of all individual segments available upon report purchase

By Application: Diagnosis Leads, Research Rises

Disease diagnosis accounted for 71.85% of 2025 revenue and remains the spine of the tissue sectioning market. Oncologists rely on rapid frozen section results during surgery, and kidney biopsies demand ultra-thin, artifact-free slices for rejection scoring. Yet research applications, growing at an 8.55% CAGR, are capturing budget share as drug developers intensify preclinical and translational studies. Spatial biology assays require serial sections of identical quality to map RNA-protein co-expression, increasing slide-per-specimen ratios. AI-enhanced virtual immunostaining cuts reagent cost and time, but still depends on consistent physical sections for algorithm training.

Hybrid workflows where a single specimen feeds both diagnostic and exploratory protocols raise throughput complexity; automated split-path systems that duplicate blocks or generate alternate slice sets are therefore gaining traction. Preclinical safety studies in toxicologic pathology also lift demand for ultramicrotomy to assess subcellular effects of novel therapeutics. The technological cross-pollination between diagnostic and research domains enlarges the ecosystem for consumables tailored to advanced imaging and multiomics.

Geography Analysis

North America, holding 41.10% of 2025 sales, benefits from mature reimbursement frameworks, early digital pathology approvals, and integrated health networks that rapidly scale automation pilots. FDA clearance of algorithmic viewers spurred hospital groups such as Mayo Clinic and Northwell to invest in end-to-end robotic sectioning lines paired with AI triage viewers. Venture funding pipelines remain strong, with U.S. startups raising > USD 100 million since 2024 for robotics and software that augment traditional hardware.

Asia-Pacific is the fastest-growing region at a 6.39% CAGR through 2031. China’s tier-3 hospitals are shifting from manual to semiautomatic microtomes, supported by domestic manufacturing incentives that shorten delivery times and meet language localization needs. India’s private oncology chains adopt subscription models where vendors charge per processed block, eliminating capital barriers. Japan and South Korea focus on high-precision ultramicrotomy for regenerative medicine research, reinforcing demand for premium equipment. Southeast Asian nations, including Indonesia and Vietnam, deploy compact automatic units in regional pathology hubs to widen access outside metropolitan centers.

Europe exhibits steady but slower expansion as budgetary austerity measures temper capital expenditure. Nonetheless, the region’s strict waste-management and chemical safety rules spur interest in xylene-free processing and energy-efficient cryostats. The EU’s In Vitro Diagnostic Regulation compels manufacturers to supply comprehensive performance data, raising barriers to entry and favoring established brands. Middle East & Africa and South America represent early-stage markets characterized by sporadic tenders and donor-funded projects. Governments there prioritize infection disease testing, yet rising non-communicable disease prevalence is expected to unlock demand for modern tissue sectioning capabilities during the forecast horizon.

Competitive Landscape

Market Concentration

The tissue sectioning market is moderately fragmented. Top vendors leverage integrated portfolios that span cassetting, microtomy, staining, scanning, and AI analytics. Danaher’s Leica Biosystems division sits at the center of this value chain, drawing on the parent company’s USD 24 billion life-sciences revenue base to cross-sell sectioning instruments alongside digital pathology software. Thermo Fisher Scientific supports continual innovation through an annual USD 1.3 billion R&D budget, reinforcing its premium positioning in automated cryostats and rotary microtomes.

Strategic alliances intensify competitive differentiation. Leica’s January 2025 investment in Indica Labs fuses Aperio scanners with HALO AP analytics, producing a hardware-software bundle optimized for companion diagnostics. Guardant Health’s multiomics tissue test illustrates how assay developers influence equipment requirements, driving co-development with instrument makers on slide quality metrics. Clarapath exemplifies disruptive entrants that focus on full automation; backing from Northwell Health and investors accelerates commercialization of lights-out microtomy lines.

Regional manufacturers exploit cost advantages, particularly in China, where local brands undercut imported systems by up to 30% while adhering to evolving quality standards. However, global players offset price gaps with service networks and validated AI partnerships. The competitive frontier is shifting toward data ecosystems: vendors offering cloud platforms that aggregate slide metadata and integrate into laboratory information systems secure long-term annuity streams through analytics subscriptions and algorithm marketplaces.

Tissue Sectioning Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NSW Government approved a statewide pathology hub at Westmead Hospital Precinct, slated to process 3.5 million tests annually.

- May 2025: Labcorp agreed to acquire select anatomic pathology assets from Incyte Diagnostics, expanding oncology coverage in the U.S. Pacific Northwest.

- April 2025: Guardant Health launched Guardant360 Tissue, a DNA-RNA multiomics panel requiring 40% fewer slides and reporting within two weeks.

- January 2025: Leica Biosystems and Indica Labs formed a strategic investment to co-develop a combined scanner-AI platform for biomarker discovery.

- November 2024: Danaher partnered with Yale’s Dr. David Rimm to create a quantitative HER2 assay enabling precise antibody-drug conjugate patient selection.

- September 2024: Stanford researchers unveiled microDicer and microGrater, robotic tools producing uniform tumor organoids for therapy screening.

Table of Contents for Tissue Sectioning Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence of Cancer Worldwide

- 4.2.2Growing Adoption of Precision Medicine and Companion Diagnostics

- 4.2.3Technological Advancements in Tissue Sectioning and Digital Pathology Systems

- 4.2.4Increasing Healthcare Expenditure and Laboratory Automation Investments

- 4.2.5Expansion of Diagnostic Infrastructure In Emerging Economies

- 4.2.6Government Funding and Reimbursement Support for Histopathology Services

- 4.3Market Restraints

- 4.3.1High Cost of Advanced Tissue Sectioning Instruments and Maintenance

- 4.3.2Shortage of Skilled Histotechnologists and Pathologists

- 4.3.3Stringent Regulatory and Quality Compliance Requirements

- 4.3.4Proliferation of Alternative Non-Invasive Diagnostic Modalities

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers/Consumers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitute Products

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Instruments

- 5.1.1.1Cryostat Microtomes

- 5.1.1.2Rotary Microtomes

- 5.1.1.3Sliding Microtomes

- 5.1.1.4Ultramicrotomes

- 5.1.1.5Vibrating Microtomes

- 5.1.1.6Tissue Processors

- 5.1.1.7Other Instruments (Paraffin Dispensers, Slide Warmers, Tissue Baths)

- 5.1.2Accessories & Consumables

- 5.2By Technology

- 5.2.1Automatic

- 5.2.2Semiautomatic

- 5.2.3Manual

- 5.3By End User

- 5.3.1Academic & Research Institutes

- 5.3.2Clinical Laboratories

- 5.3.3Hospital Laboratories

- 5.3.4Pharmaceutical & Biotechnology Companies

- 5.3.5Contract Research Organizations (CROs)

- 5.3.6Ambulatory Surgery Centers (ASCs)

- 5.4By Application

- 5.4.1Disease Diagnosis

- 5.4.2Translational & Pre-clinical Research

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1AGD Biomedicals (P) Ltd

- 6.3.2Amos Scientific Pty Ltd

- 6.3.3Boeckeler Instruments Inc.

- 6.3.4Danaher Corporation

- 6.3.5Diapath S.p.A.

- 6.3.6LLS ROWIAK LaserLabSolutions GmbH

- 6.3.7Sakura Finetek Japan Co. Ltd

- 6.3.8SLEE Medical GmbH

- 6.3.9SM Scientific Instruments Pvt. Ltd

- 6.3.10Thermo Fisher Scientific Inc.

- 6.3.11Milestone Medical Srl

- 6.3.12Bioevopeak Co. Ltd

- 6.3.13MEDIMEAS Instruments

- 6.3.14Histo-Line Laboratories

- 6.3.15Micros Productions GmbH

- 6.3.16CellPath Ltd

- 6.3.17Cardinal Health Inc.

- 6.3.18Epredia (PHC Group)

- 6.3.19Merck KGaA (Sigma-Aldrich)

- 6.3.20StatLab Medical Products

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Tissue Sectioning Market Report Scope

As per the scope of the report, tissue sectioning is the process of cutting thin slices, known as sections or slides, from biological tissues for microscopic examination. These sections study tissue structure, composition, and pathology at a cellular level, aiding in various fields such as pathology, biomedical research, and drug development.

The tissue sectioning market is segmented by product (instruments and accessories and consumables), technology (automatic, semiautomatic, and manual), end user (academic and research institutes, clinical laboratories, hospital laboratories, and pharmaceutical and biotechnology companies), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market sizes and forecasts in terms of value (USD) for the above segments.