Tire Manufacturing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.17 Billion |

| Market Size (2030) | USD 2.68 Billion |

| Growth Rate (2025 - 2030) | 4.37% CAGR |

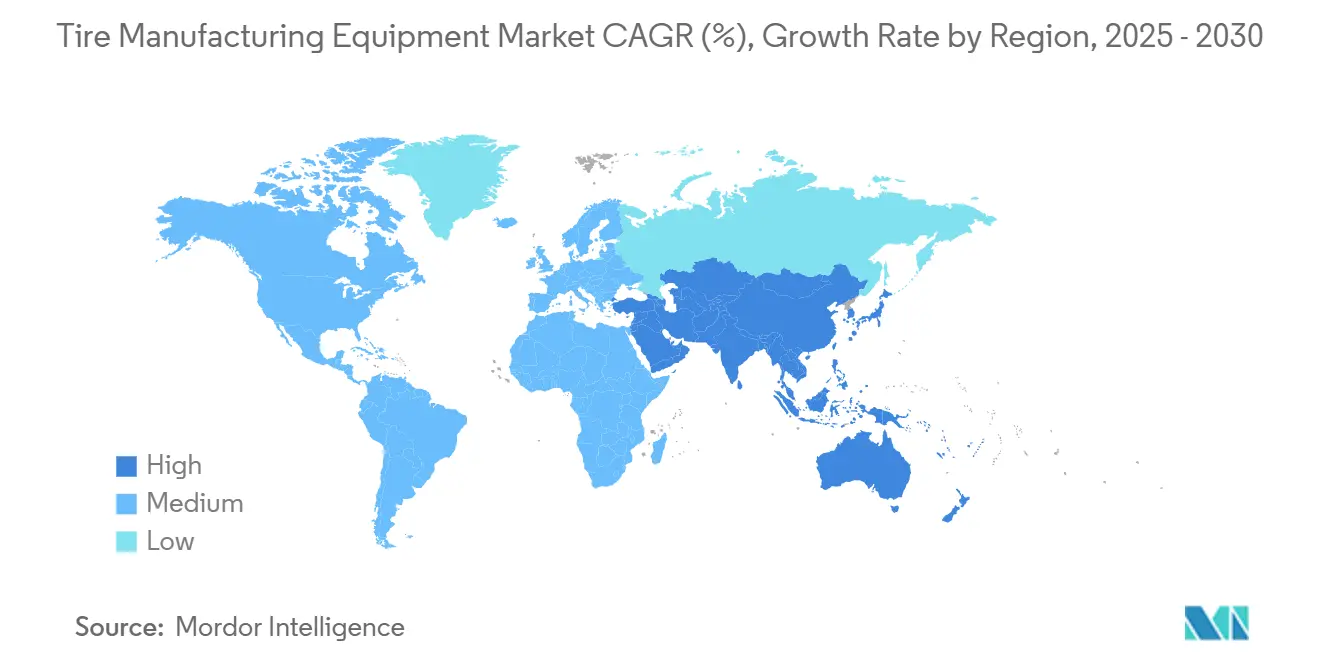

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tire Manufacturing Equipment Market Analysis by Mordor Intelligence

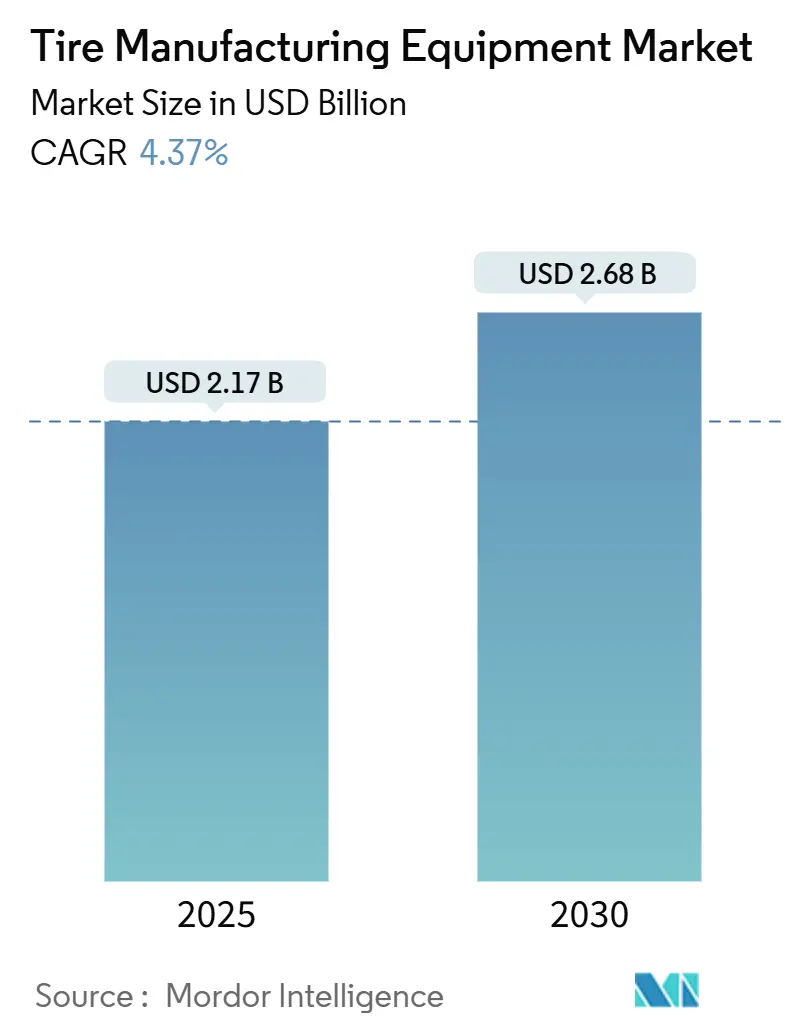

The Tire Manufacturing Equipment Market size is estimated at USD 2.17 billion in 2025, and is expected to reach USD 2.68 billion by 2030, at a CAGR of 4.37% during the forecast period (2025-2030). This growth trajectory reflects a maturing global landscape in which investment priorities shift from sheer capacity expansion toward automation that protects margins while meeting new environmental and product‐mix demands. The industry benefits from the steady recovery of global vehicle production, a rapidly widening electric-vehicle fleet that requires specialized tires, and intensive adoption of Industry 4.0 architectures that raise productivity and reduce scrap. Regional dynamics remain pivotal: Asia-Pacific sustains its manufacturing heft, the Middle East and Africa capture the fastest incremental gains through greenfield projects, and North America and Europe focus on technology upgrades that strengthen compliance and energy efficiency. Competitive strategies center on modular equipment platforms and software partnerships that unlock predictive maintenance and flexible, small-batch capabilities.

Key Report Takeaways

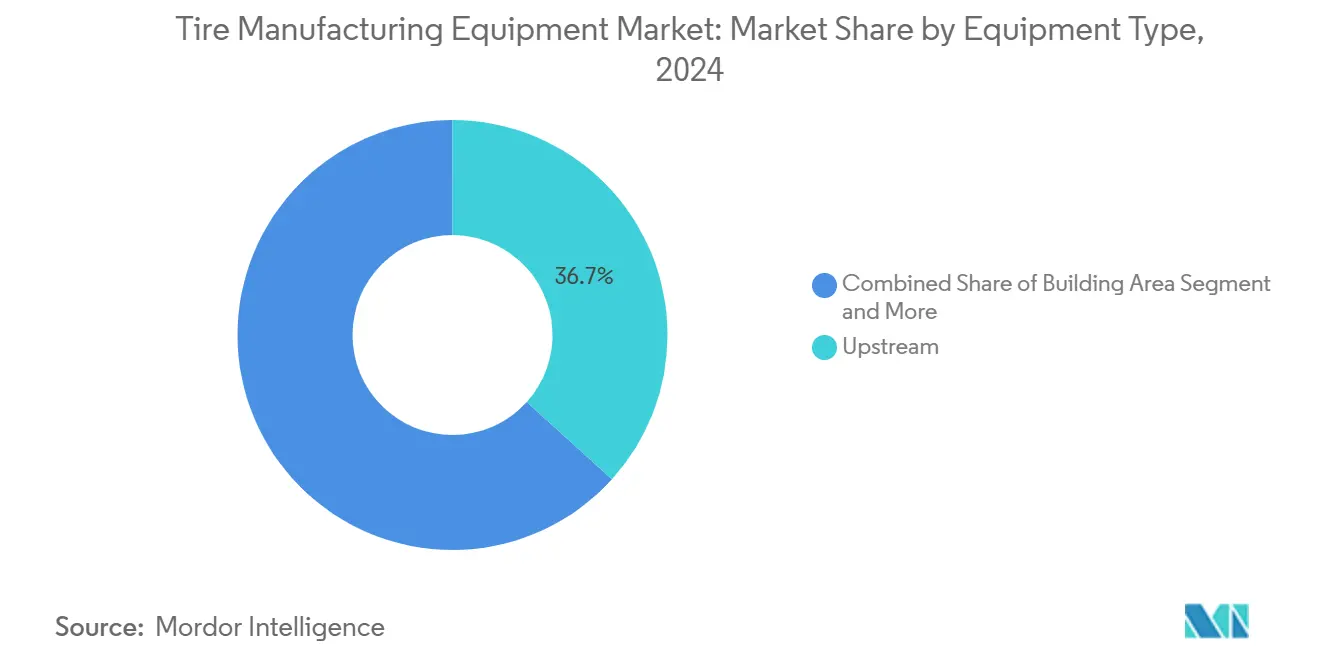

- By equipment type, upstream processing led with 36.71% of the tire manufacturing equipment market share in 2024, while curing and inspection systems are projected to expand at a 4.45% CAGR through 2030.

- By tire design, radial machinery held 78.15% of the tire manufacturing equipment market size in 2024, and the same category is also forecast to log the highest 4.48% CAGR to 2030.

- By vehicle type, passenger-car applications captured 41.27% revenue share in 2024; off-road vehicles are advancing at a 4.53% CAGR to 2030.

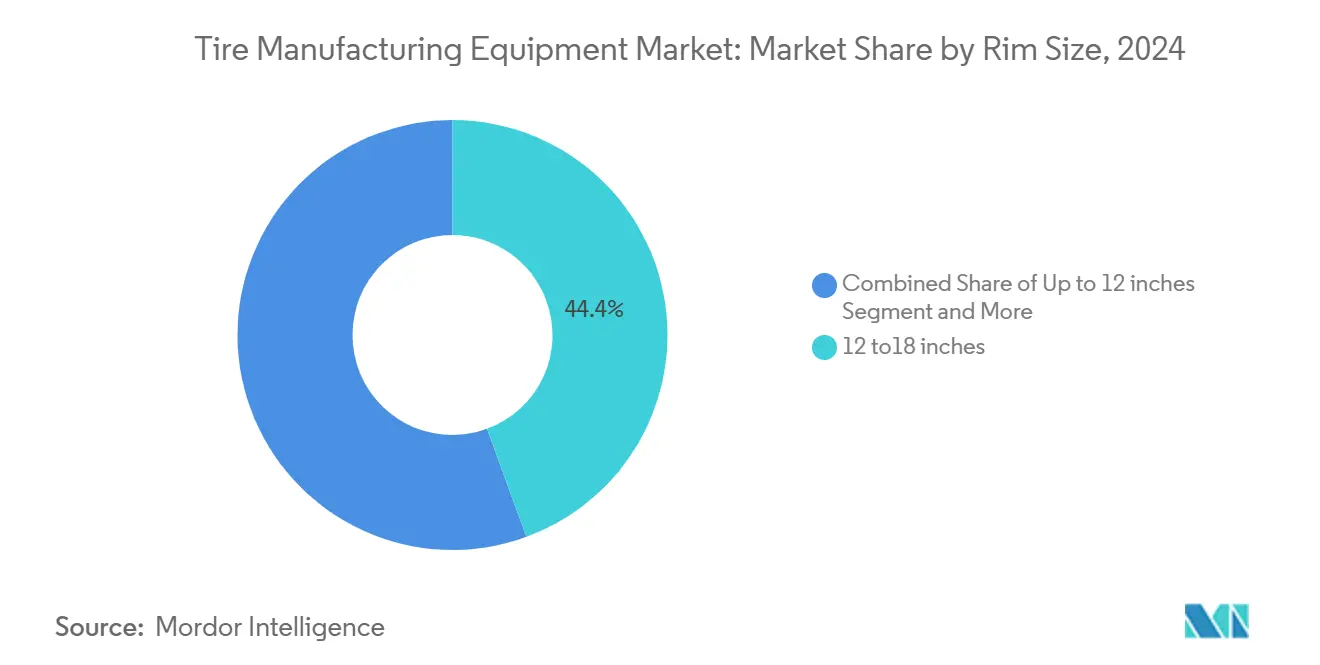

- By rim size, 12–18 inch lines accounted for 44.37% of the tire manufacturing equipment market size in 2024, whereas systems handling above-18-inch tires are slated for a 4.57% CAGR during the forecast window.

- By end-user, OEM demand commanded 63.27% of the tire manufacturing equipment market share in 2024, yet aftermarket service equipment is set to grow at a 4.61% CAGR to 2030.

- By geography, Asia-Pacific supplied 45.13% of global revenue by geography in 2024; the Middle East and Africa region is on track for a 4.66% CAGR up to 2030.

Global Tire Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation And Industry 4.0 Adoption | +1.2% | North America and EU, expanding to Asia Pacific | Short term (≤ 2 years) |

| Surge In Small-Batch and Customized Tire Skus | +0.9% | Global, premium markets first | Medium term (2-4 years) |

| Rising Global Vehicle Production Volumes | +0.8% | Global, with Asia Pacific leading | Medium term (2-4 years) |

| Environmental Legislation Pushing Solvent-Free Tire Manufacturing Processes | +0.7% | North America and EU primarily | Long term (≥ 4 years) |

| Increasing Demand For Radial Tires | +0.6% | Global, strongest in emerging markets | Long term (≥ 4 years) |

| Localization Strategies Of EV Start-Ups Creating Greenfield Tire Plants | +0.5% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Production Volumes

Light-vehicle output recovers steadily, with the U.S. Tire Manufacturers Association projecting 340.4 million domestic tire shipments in 2025, up from 337.3 million in 2024[1] “2025 U.S. Tire Shipment Forecast,” U.S. Tire Manufacturers Association, ustires.org. The rebound is weighted toward replacement demand, causing original-equipment volumes to stagnate and pushing manufacturers to adopt flexible building lines capable of low-volume, high-variety runs. Investment favors adaptive tire building machines that quickly change rim sizes instead of single-purpose assets. Bridgestone’s upgrade at its Kitakyushu off-the-road (OTR) facility typifies the pivot to specialized capacity that can chase profitable niches[2]“Bridgestone to Enhance Kitakyushu Plant,” Bridgestone Corporation, bridgestone.com. Equipment suppliers offering rapid changeover features and digital recipe management are gaining an edge, especially in Asia, where OEMs chase export and domestic replacement contracts.

Environmental Legislation Pushing Solvent-Free Tire Manufacturing Processes

EPA amendments to hazardous air-pollutant rules in early 2025 raise compliance hurdles for plants still relying on solvent-based cements. European Union directives add parallel pressure with strict volatile organic compound limits. Curing presses and innerliner extruders are redesigned to accommodate alternative, water-borne materials without compromising cycle times. Suppliers offering turnkey solvent-free lines see early adoption in Germany and the United States, with APAC multinationals accelerating pilots to meet export-market standards.

Increasing Demand For Radial Tires In Commercial Vehicles

Electrification, stricter emissions rules, and fuel-economy targets push fleets toward radial casings that deliver lower rolling resistance. The shift mandates precision calendaring and steel-belt handling systems, accelerating replacement cycles for legacy bias-tire lines. L&T, whose equipment portfolio dominates OTR curing machinery, reported strong order inflows in Q3 FY 2025 on the back of this radial transition[3]“Q3 FY25 Financial Results,” Larsen & Toubro Limited, larsentoubro.com . The need to modernize aging bias plants in emerging markets aligns with government incentives for cleaner transport, setting off long-tail demand for new radial-specific upstream equipment.

Localization Strategies Of EV Start-Ups Creating Greenfield Tire Plants In Emerging Markets

Several electric-vehicle newcomers commit to domestic tire plants instead of imports to secure supply chains, often encouraged by tariff shields and job-creation mandates. Pirelli’s USD 550 million joint venture with Saudi Arabia’s Public Investment Fund, slated for 3.5 million passenger-tire capacity, illustrates the greenfield momentum in the Middle East. Start-ups prefer highly automated, right-sized lines that match their limited but growing volumes, giving mid-scale equipment suppliers fresh ground to capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Volatile Raw-Material Prices | -0.8% | Global, commodity-dependent regions | Medium term (2-4 years) |

| Skilled-Labor Shortages | -0.4% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Supply-Chain Disruptions | -0.3% | Global, acute in Asia Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure For Advanced Equipment

Cutting-edge mixing rooms, automated building cells, and end-of-line X-ray machines require multimillion-dollar outlays that stress balance sheets, especially where borrowing costs are elevated. Apollo Tyres plans Rs 1,500 Crore Capex for FY26. Of this, Rs 700 crore will be dedicated to maintenance, ensuring operational efficiency, a strategy mirrored by many mid-tier manufacturers. For smaller Asian and African players, the hurdle is steeper, prompting vendors to roll out leasing models, outcome-based service contracts, or modular upgrade paths that break investments into digestible stages.

Volatile Raw-Material Prices Impacting Equipment ROI Calculations

Natural-rubber prices rose more than one-tenth quarter-on-quarter in Q4 2024, and the all-steel tire raw-material index climbed exponentially year-on-year, unsettling profit forecasts that underpin equipment payback analyses. Commodity swings extend decision cycles for big-ticket machinery and complicate service-contract pricing. Added friction comes from semiconductor shortages that inflate lead times for programmable logic controllers and vision sensors embedded in modern equipment. Suppliers now hedge cost risk by indexing maintenance fees to commodity baskets or by offering shorter warranty terms that can be renewed annually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Upstream Dominance Drives Integration

Upstream processing machines represented 36.71% of the tire manufacturing equipment market in 2024, confirming the premium manufacturers place on compound consistency. Mixing, milling, and calendaring systems now ship with inline viscosity sensors and recipe-tracking software that connect directly to plant MES layers. Curing and inspection equipment, projected to grow at a 4.45% CAGR, benefits from stricter quality mandates and the necessity for 100% in-process traceability. This evolution helps the tire manufacturing equipment market size for downstream quality control swell in lockstep with regulatory oversight.

Convergence among traditionally discrete stations accelerates: Comerio Ercole’s ultrathin-calender technology consolidates steps that previously required multiple passes. At the same time, adaptive curing presses adjust bladder pressure in real time to eliminate trapped air pockets. Vendors that bundle upstream and downstream assets with single dashboards find traction among Tier-1 tire makers, who prioritize streamlined procurement and unified data lakes. As plants seek smaller footprints, integrated cells replace linear layouts, supporting automation density without wholesale infrastructure overhauls.

By Tire Design: Radial Technology Reinforces Leadership

Radial-capable machinery controlled 78.15% revenue share in 2024 and is on course for a 4.48% CAGR, a duality that anchors the long-term dominance of steel-belted construction. Extensive fleet trials confirm up to 5% fuel-efficiency gains, sharpening the financial rationale for ongoing radial adoption across buses, heavy trucks, and specialty transport segments. That momentum enlarges the tire manufacturing equipment market size for high-precision belt-cutting and spot-cooling solutions essential to radial quality assurance.

Bias-tire machinery lingers in niches such as forestry and agriculture, where puncture repairability and low-speed durability trump highway performance. Equipment providers that continue to service bias plants do so through retrofit kits that add incremental PLC upgrades rather than wholesale replacements. Parallel advances in sulfur-radical coupling chemistries may soon modify cure profiles, compelling equipment designers to re-examine mold venting geometries and temperature-control algorithms.

By Vehicle Type: Off-Road Vehicles Accelerate Growth

Passenger-car applications accounted for 41.27% of 2024 revenue, but off-road vehicle lines are forecast to outpace the broader tire manufacturing equipment market at a 4.53% CAGR through 2030. Mining expansion and massive infrastructure spending in India, Indonesia, and Brazil fuel demand for OTR tires above 3 meters in diameter, swelling order books for specialist curing presses. These large-format presses typically command premium pricing, increasing their weight in the overall tire manufacturing equipment market size despite lower unit counts.

Equipment must now accommodate diverse bead constructions and extraordinary carcass stiffness that tax conventional bladder systems. L&T’s dominance in giant-tire curing machinery thus remains secure, particularly because competitive barriers include sophisticated finite-element modeling and forged-steel platen sourcing. Suppliers targeting growth in this segment invest heavily in virtual-commissioning tools that simulate press behavior before on-site installation, slashing ramp-up times for remote mining locations.

By Rim Size: Large Diameter Drives Premium Growth

Lines producing 12–18 inch tires owned a 44.37% share in 2024, reflecting their alignment with mainstream sedan and crossover production. However, machinery of above-18-inch sizes registers a 4.57% CAGR, propelled by the global appetite for sport-utility vehicles and premium EV platforms that favor 20-inch or larger rims. The upsizing wave also permeates agriculture: Michelin’s 2.32-meter CEREXBIB 2 ranges push rim diameters to unprecedented territory, demanding reinforced building drums and extended-stroke curing presses.

To serve wide-rim variability without downtime, next-generation building machines sport servo-driven turn-up modules that automatically adjust carcass positioning. Inline laser profilometers verify tread symmetry on each rotation, trimming scrap rates, and reinforcing the growth of the tire manufacturing equipment market share for high-diameter applications. Plants that embrace this flexibility report smoother changeovers across rim classes, a critical benefit as OEMs diversify wheel options within single vehicle platforms.

By End-User: Aftermarket Services Gain Momentum

OEM-focused installations still dominate at 63.27% of 2024 spending. Yet, aftermarket and refurbishment demand is rising faster at 4.61% CAGR because fleets keep vehicles longer and place a higher value on premium replacement tires. The effect enlarges the serviceable tire manufacturing equipment market size for upgrade kits, remote diagnostics, and performance-enhancement retrofits tied to existing assets.

Suppliers increasingly lead with bundled service contracts that guarantee throughput or defect-rate metrics instead of selling machines outright. Predictive-maintenance modules flag wear signatures before catastrophic line stoppages, proving especially attractive in high-utilization Asian plants. Vendors lock in recurring revenue streams by selling uptime and energy-efficiency improvements and strengthening customer intimacy that resists price-only competition.

Geography Analysis

Asia-Pacific contributed 45.13% of global revenue in 2024, reflecting China’s dense clustering of full-line tire plants and India’s ascent as an export hub that blends cost advantage with deep rubber-industry know-how. Equipment orders in the region continue to lean on domestically produced electronics and castings, buffering currency risks while sustaining short delivery cycles. Japan and South Korea sustain leadership in high-precision spindle drives and inspection optics, with several suppliers exporting modular sub-assemblies that boost the tire manufacturing equipment market size for premium lines. Indonesia and Vietnam attract mid-tier plants seeking tariff savings under regional trade pacts and robust local demand, further cementing Asia’s production gravity.

The Middle East and Africa are the fastest-growing areas, advancing at a 4.66% CAGR through 2030. Saudi Arabia’s Pirelli joint venture underscores a strategic pivot toward domestic tire production that slashes import reliance and anchors manufacturing ecosystems. Emerging clusters in Egypt and South Africa draw on skilled labor pools and port proximity, providing springboards into continental demand that exceeds 200 million units annually. Governments roll out special-economic-zone incentives and infrastructure bonds that ease logistics bottlenecks, coaxing global equipment vendors to establish regional service centers.

North America and Europe remain mature but technologically progressive. Goodyear’s CAD 575 million modernization of its Napanee, Ontario, facility adds advanced curing and final-finish automation to support EV-rated all-terrain tires[4]. European plants confront even stricter environmental legislation, seen in adopting solvent-free adhesives and energy-recapture systems that feed surplus heat into curing lines. Demand therefore concentrates on retrofitting rather than greenfield volume, with procurement teams valuing lifecycle analytics and carbon-footprint dashboards as much as mechanical uptime. Consolidation of smaller plants into regional super-sites accelerates in Germany and France, channeling capital into fewer but more sophisticated establishments.

Mordor Intelligence provides coverage of the tire manufacturing equipment market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, China, South Korea, and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

Competition in the tire manufacturing equipment market is moderate and technology-centric. Incumbents such as L&T leverage turnkey portfolios that stretch from mixing to curing, along with support for offshore installation, allowing them to serve global tenders from APAC to Latin America. European stalwarts like VMI Group embed AI modules into tire-building machines that adapt bead-apex angles and optimize splice positioning in real time, winning them the 2025 Tire Manufacturing Innovation Award. Japanese machinery providers emphasize servo precision and energy recovery, often partnering with sensor firms to package holistic Industry 4.0 offerings.

Strategic alliances dominate. Sumitomo Rubber Industries collaborates with Rockwell Automation to harmonize MES and PLC layers, shortening commissioning times and ensuring interoperable data streams across continents. Some specialist firms integrate digital twins that simulate compound flow and curing kinetics, enabling remote optimization that squeezes extra capacity out of existing lines without new hardware. Service differentiation rises as a key battleground: vendors deploy global parts depots and 24/7 virtual support to cut mean-time-to-repair metrics, reinforcing customer lock-in despite price pressure from lower-cost entrants in China.

White-space opportunities lie in modular upgrade kits that retrofit legacy presses with smart-sensor arrays and cloud dashboards. Some start-ups build software overlays that analyze equipment telemetry and prescribe energy-saving parameter tweaks. As integration depth widens, competitive advantage shifts from mechanical design elegance toward data analytics and predictive algorithms. In this climate, mid-sized vendors with agile engineering cultures and robust SaaS layers may capture a disproportionate share in the tire manufacturing equipment market over the next five years.

Tire Manufacturing Equipment Industry Leaders

HF Mixing Group

Kobe Steel (Kobelco)

VMI Group

MESNAC

Larsen & Toubro Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Mesnac confirmed a USD 20 million commitment to a Mexican manufacturing site that will localize mixing rooms and curing presses for North American customers.

- December 2024: Sumitomo Rubber Industries chose Rockwell Automation’s FactoryTalk Production Centre as its global MES backbone, starting at the Shirakawa plant in Japan.

- December 2024: Goodyear earmarked CAD 575 million to upgrade its Napanee, Ontario, facility, adding 200 manufacturing jobs and enhancing energy efficiency to serve EV and all-terrain segments.

Global Tire Manufacturing Equipment Market Report Scope

| Upstream | Mixing Machines / Rubber Mixers |

| Calendaring Machines | |

| Extrusion Machines | |

| Cutting Machines | |

| Others (Cooling Units, etc.) | |

| Building Area | Bead Winding Machine |

| Tire Building Machine | |

| Others (Strip Winding Machine, etc.) | |

| Curing & Inspection | Curing Press Machines |

| Tire Painting Machines | |

| Others (Inspection Machines, etc.) |

| Bias |

| Radial |

| Two-wheelers |

| Three-wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Off-Road Vehicles |

| Up to 12 inches |

| 12 to 18 inches |

| Above 18 inches |

| Original Equipment Manufacturers (OEMs) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Upstream | Mixing Machines / Rubber Mixers |

| Calendaring Machines | ||

| Extrusion Machines | ||

| Cutting Machines | ||

| Others (Cooling Units, etc.) | ||

| Building Area | Bead Winding Machine | |

| Tire Building Machine | ||

| Others (Strip Winding Machine, etc.) | ||

| Curing & Inspection | Curing Press Machines | |

| Tire Painting Machines | ||

| Others (Inspection Machines, etc.) | ||

| By Tire Design | Bias | |

| Radial | ||

| By Vehicle Type | Two-wheelers | |

| Three-wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| Off-Road Vehicles | ||

| By Rim Size | Up to 12 inches | |

| 12 to 18 inches | ||

| Above 18 inches | ||

| By End-User | Original Equipment Manufacturers (OEMs) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which region currently accounts for the largest tire manufacturing equipment market share?

Asia-Pacific leads with 45.13% of global revenue in 2024, driven by concentrated production centers in China and India.

What CAGR is forecast for tire manufacturing equipment used in off-road vehicle applications?

Off-road vehicle equipment will grow at a 4.53% CAGR between 2025 and 2030.

How big is the tire manufacturing equipment market expected to be by 2030?

The tire manufacturing equipment market will reach USD 2.68 billion in 2030.

Which equipment segment is growing the fastest?

Curing and inspection systems are forecast to expand at a 4.45% CAGR through 2030.

What is the primary restraint affecting near-term equipment purchases?

High upfront capital costs, particularly acute for smaller manufacturers in emerging markets, are the primary near-term constraint.

Page last updated on: