China Tire Manufacturing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

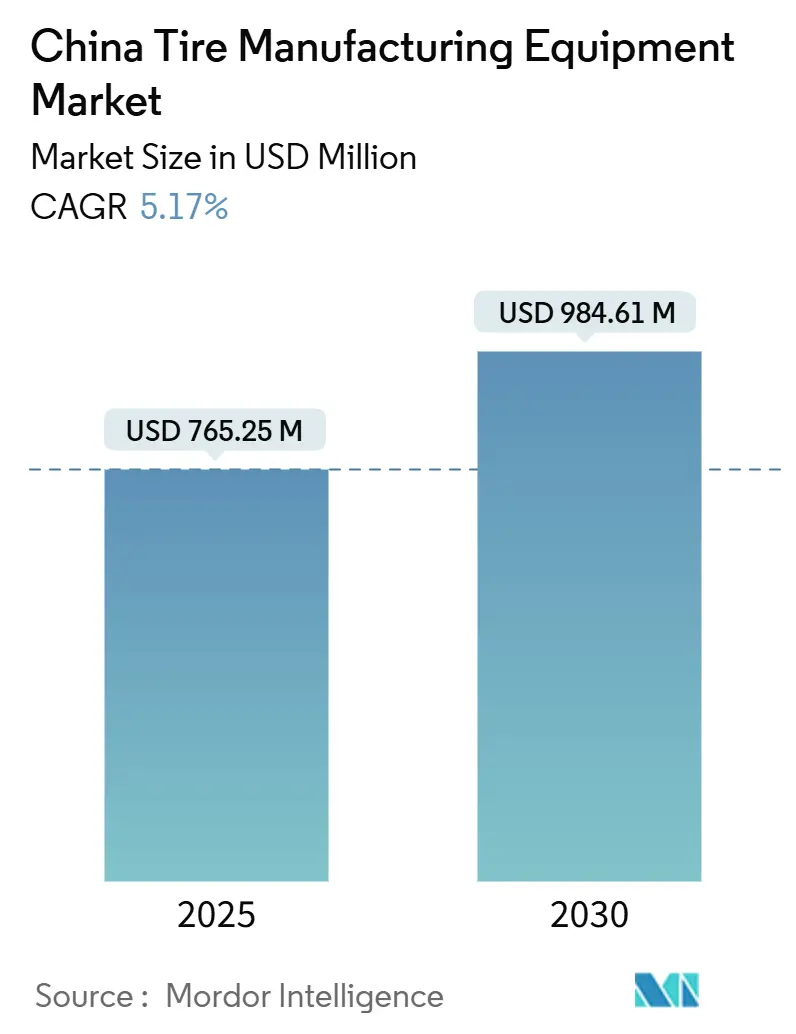

| Market Size (2025) | USD 765.25 Million |

| Market Size (2030) | USD 984.61 Million |

| Growth Rate (2025 - 2030) | 5.17% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Tire Manufacturing Equipment Market Analysis by Mordor Intelligence

The China tire manufacturing equipment market size stands at USD 765.25 million in 2025 and is forecast to reach USD 984.61 million by 2030, advancing at a 5.17% CAGR. Robust domestic passenger-car and radial-tire output, accelerated Industry 4.0 roll-outs, and aggressive procurement of cost-competitive turnkey lines underpin this expansion. Export-oriented capacity additions in truck, bus, and off-the-road (OTR) tires are sustaining demand for specialized curing presses, while electric-vehicle (EV) tire requirements are steering upgrades toward larger-rim, low-noise production capabilities. Digitalized quality-control systems, predictive-maintenance platforms, and energy-efficient vulcanization technologies are sharpening competitive differentiation as tire makers seek lower defect rates, shorter cycle times, and carbon-reduction gains. Volatility in rubber and petrochemical prices and persistent anti-dumping duties reshape global sourcing, but domestic capital expenditure on smart factories and recycling lines continues to propel the China tire manufacturing equipment market.

Key Report Takeaways

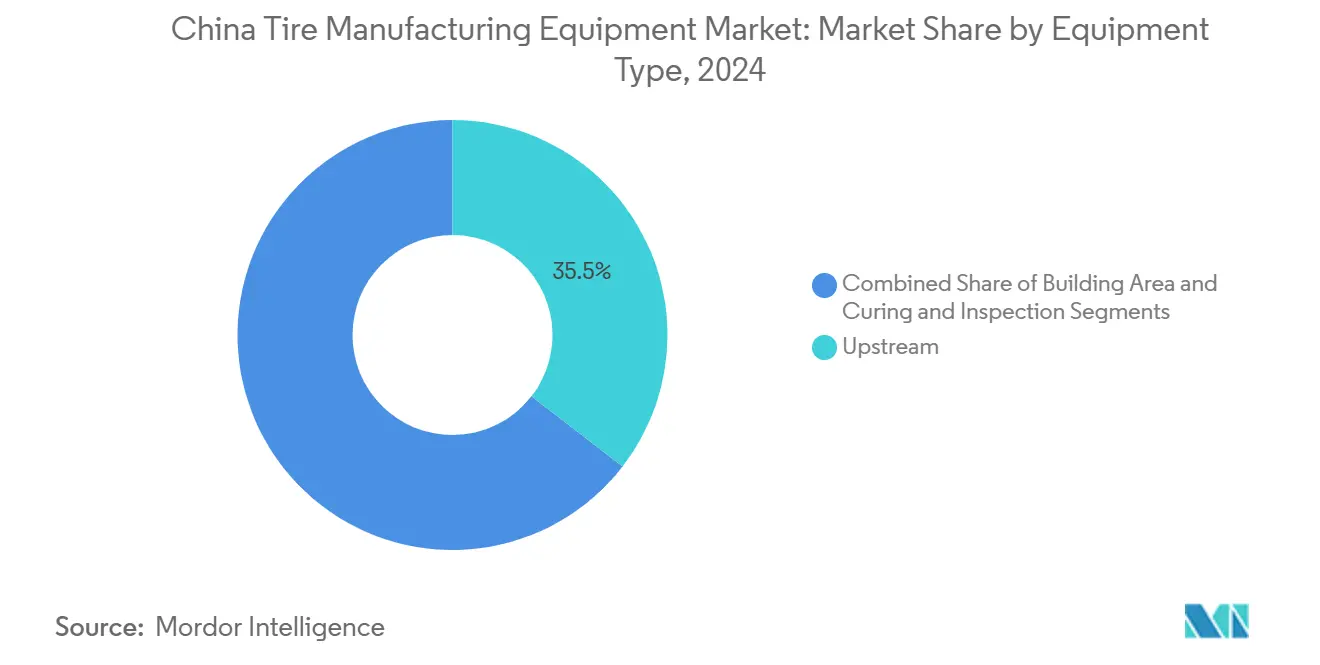

- By equipment type, mixing machines led with 35.48% of China tire manufacturing equipment market share in 2024; curing and inspection equipment is progressing at an 8.53% CAGR through 2030.

- By tire design, radial construction accounted for 86.61% of China tire manufacturing equipment market size in 2024 and is advancing at a 5.34% CAGR to 2030.

- By vehicle type, passenger-car applications held 56.35% of China tire manufacturing equipment market size in 2024, while EV-specific lines are expanding at a 10.63% CAGR.

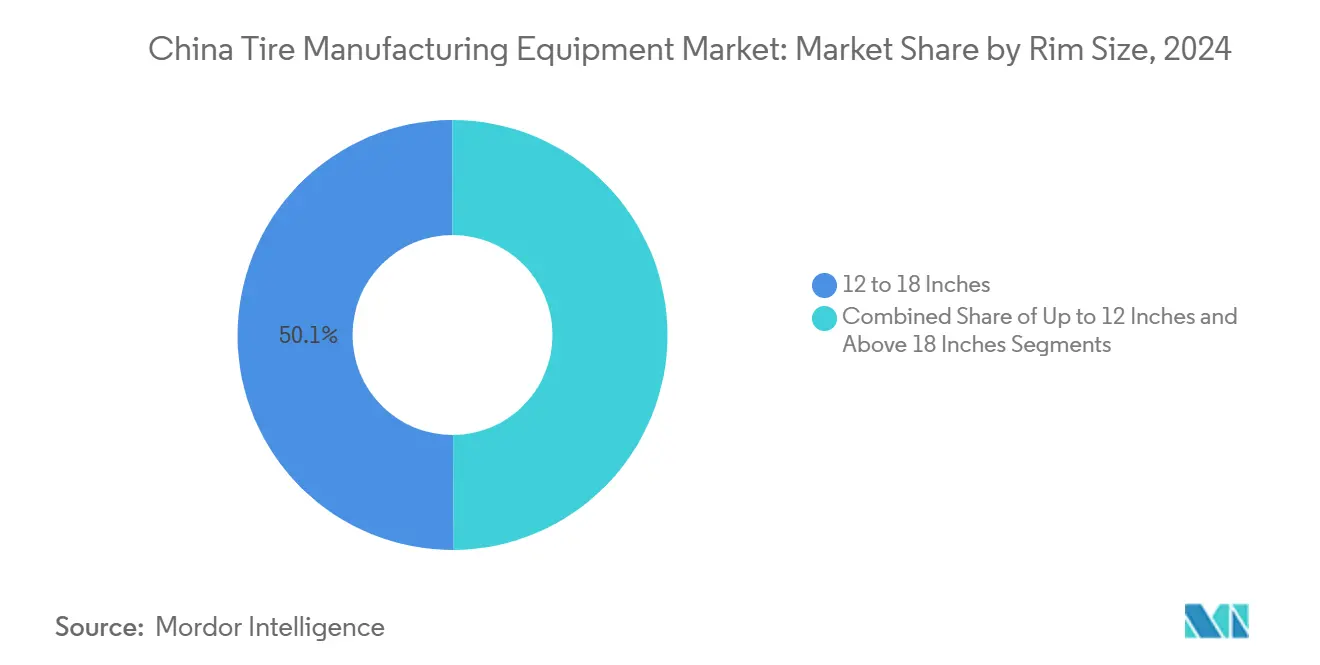

- By rim size, the 12–18 inches category captured 50.09% of China tire manufacturing equipment market share in 2024; sizes above 18 inches are registering the fastest growth at 9.97% CAGR.

- By end-user, the aftermarket dominated with 64.65% revenue share in 2024; original-equipment demand is projected to increase at a 6.97% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with China being one of the contributors. Our global tire manufacturing equipment market size represents that cumulative total.

China Tire Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-Led Capacity Expansion | +1.8% | Shandong, Jiangsu, Guangdong | Medium term (2-4 years) |

| Large-Rim Tire Demand | +1.5% | Shandong, Jiangsu, Zhejiang | Long term (≥ 4 years) |

| Industry 4.0 Adoption | +1.2% | Shandong, Jiangsu, Hubei | Medium term (2-4 years) |

| Growth in Passenger-Car Output | +1.0% | Shandong, Jiangsu, Guangdong, Zhejiang | Short term (≤ 2 years) |

| Cost-Competitive Turnkey Lines | +0.8% | Shandong, Jiangsu, Liaoning | Short term (≤ 2 years) |

| Carbon-Reduction Subsidies | +0.6% | Shandong, Jiangsu, Guangdong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Led Capacity Expansion for TBR and OTR Tires

Manufacturers are enlarging truck, bus, and OTR tire capacity despite overseas tariff barriers, channeling funds into high-cavity curing presses and automated building machines that optimize unit costs and throughput. The U.S. decision to uphold countervailing duties is prompting on-shore efficiency upgrades in Shandong and Jiangsu, where integrated supply ecosystems speed equipment commissioning. Premium OTR lines demand wider-throat presses and heavier molds, steering suppliers toward modular hydraulic platforms. Project pipelines in mining-tire segments illustrate the pivot toward higher-margin niches as producers hedge against tariff exposure, keeping the China tire manufacturing equipment market on a steady investment footing.

EV-Specific, Large-Rim Tire Demand

EVs accelerate tread wear by around 20% and command rims above 18 inches, forcing compound reformulation and side-wall redesign. Production lines therefore add precision bead-winding heads, adaptive cutter modules, and larger-plate mold sets. A Hefei facility’s 17 million-unit ramp-up dedicated to new-energy vehicles exemplifies how OEM tire makers retool for quiet-running, low-rolling-resistance products. Advanced servo-controlled presses maintain ±3 °C plate uniformity, ensuring consistent curing across wide profiles. As domestic EV sales surge, this driver enlarges addressable demand for AI-enabled inspection tunnels and automatic uniformity testers inside the China tire manufacturing equipment market.

Industry 4.0 Adoption in Domestic Tire Plants

Digitized factories blend IoT sensors, machine-learning defect detection, and cloud dashboards to shorten changeovers and cut scrap rates. Deployments of integrated execution software synchronize mixing, calendaring, and building islands, producing real-time key performance indicators for line supervisors. A 99.96% reproducibility rate achieved in automatic inspection showcases the gains from vision analytics and robotic palpation stations. Provincial grants for digital transformation lower payback periods, spurring mid-tier producers to upgrade legacy assets. This wave of smart-factory spending is broadening revenue streams for software-hardware turnkey vendors active in the China tire manufacturing equipment market.

Rapid Growth in Passenger-Car and Radial-Tire Output

Domestic car output and rising export orders sustain high utilization at radial-tire plants, anchoring demand for energy-efficient internal mixers, steel-cord calendars, and twin-screw extruders. Investments in Southeast Asian satellite plants still rely on homegrown Chinese machinery, reinforcing export order books for upstream equipment makers. The clustering of capacity in Shandong and Jiangsu enables dense service networks, easing preventive-maintenance delivery and spare-parts logistics, and further stimulating new-equipment cycles across the China tire manufacturing equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -1.4% | Shandong, Jiangsu, Guangdong, Zhejiang | Short term (≤ 2 years) |

| Anti-Dumping Duties on Tire Exports | -1.2% | Shandong, Jiangsu, Liaoning | Medium term (2-4 years) |

| Mechatronic Talent Shortage | -0.8% | Shandong, Jiangsu, Hubei | Long term (≥ 4 years) |

| Cap-Ex Diversion to Recycling | -0.5% | Shandong, Jiangsu, Guangdong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rubber and Petro-Chemical Price Volatility

Natural rubber costs increased more than 33% in early 2024, while styrene-butadiene rubber prices swung sharply amid tariff-induced supply dislocations. These spikes squeeze tire-maker margins, deferring discretionary machine purchases and shifting focus toward yield-enhancing mixers and compound-recovery systems. Elevated feedstock bills also accelerate interest in devulcanization and reclaimed-rubber processing modules, marginally redirecting capital from traditional production lines. The resulting budgeting caution exerts a moderating influence on the China tire manufacturing equipment market[1]Jayashree Bhosale, "Hardening rubber prices to put pressure on tyre makers’ margin", economictimes.indiatimes.com .

Anti-Dumping Duties on Chinese Tire Exports

Countervailing duties imposed on selected truck and bus tire exporters have prompted producers to build offshore plants, tempering domestic equipment demand while creating outbound sales prospects in Southeast Asia. Suppliers must now design modular, easily relocatable machinery suited to quick redeployment across borders. This regulatory friction compresses near-term growth and diversifies geographical order flow for participants in the China tire manufacturing equipment market[2]"Truck and Bus Tires from China", U.S. International Trade Commission, usitc.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Upstream Dominance Drives Automation

Upstream mixing machines generated the highest revenue, commanding 35.48% of the China tire manufacturing equipment market share in 2024 amid persistent raw-material cost pressures that elevate the value of precision compound blending. Automated internal mixers with real-time viscosity feedback and cloud diagnostics underpin efficiency drives in Shandong mega-plants. Curing and inspection equipment is the fastest-advancing category with an 8.53% CAGR thanks to AI-vision platforms that detect bead-area defects and radial run-out in milliseconds, safeguarding brand reputations and reducing warranty claims.

Cascading upgrades in building, cutting, and calendaring lines follow mixing-hall modernization, promoting adopting integrated supervisory-control systems that harmonize recipe delivery and batch traceability. Integrated upstream packages lower total project cycle times by approximately 15%, fortifying supplier stickiness and reinforcing recurrent-service revenues. These developments collectively expand addressable opportunities for vendors operating in the China tire manufacturing equipment market.

By Tire Design: Radial Technology Reinforces Market Position

Radial-tire technology held 86.61% of China tire manufacturing equipment market size in 2024 and continues to outpace bias constructions at a 5.34% CAGR as automakers demand superior fuel efficiency and ride comfort. Equipment specifications therefore favor steel-cord actuation calendars capable of ±0.05 mm thickness accuracy and belt-edge trimmers that minimize splice rejection.

Bias-tire lines remain relevant for certain agricultural and industrial uses, yet investments focus on compact, multi-stage presses configurable for both constructions, granting producers flexibility without redundant assets. This dual-capability approach supports rural equipment uptake while safeguarding returns on capital within the China tire manufacturing equipment market.

By Vehicle Type: Passenger Cars Lead Electric Transition

In 2024, passenger car applications command a dominant 56.35% share of the equipment market. Notably, within this segment, electric vehicles are leading the charge, boasting a robust growth rate of 10.63% CAGR projected through 2030. This surge underscores the automotive industry's pivot towards electrification and the consequent demand for specialized tires. Specialized mixing and curing technologies are seizing the opportunity as EV tire production requires equipment adept at handling unique compound formulations. These formulations aim to reduce rolling resistance, boost durability, and minimize noise.

Light commercial-vehicle equipment demand benefits from e-commerce parcel volumes, while two- and three-wheeler lines maintain resilience in cost-sensitive urban centers. Medium and heavy commercial-vehicle investments concentrate on retread-ready carcass designs to offset export tariff impacts. This vehicle-mix evolution sustains a diversified revenue base for the China tire manufacturing equipment market.

By Rim Size: Large Wheels Accelerate Growth Momentum

The 12–18 inches rim size segment dominates the market with a 50.09% share in 2024, while rims above 18 inches are growing rapidly at a 9.97% CAGR through 2030, driven by consumer demand for larger wheels and enhanced aesthetics. This shift has increased the need for specialized equipment like building machines and curing presses that can handle larger tire dimensions and complex sidewall designs. Although the up to 12 inches segment remains relevant in cost-sensitive markets, its growth is comparatively modest.

The trend toward larger rims is closely tied to electric vehicle adoption, as EVs benefit from larger wheels for regenerative braking and aerodynamic efficiency. This has created opportunities for equipment suppliers offering precision manufacturing and advanced inspection systems to meet higher performance and safety standards. Manufacturers in Shandong and Jiangsu provinces are actively upgrading their equipment to serve this premium segment, supported by proximity to automotive hubs and government incentives for advanced technologies.

By End-User: Aftermarket Dominance Faces OEM Challenge

In 2024, the aftermarket segment captured the largest market share at 64.65%, driven by the global reach of replacement tire demand and diverse vehicle applications. Its dominance stems from predictable replacement cycles and widespread distribution networks. Equipment demand in this segment emphasizes flexibility and efficiency to meet varied tire specifications across regions and vehicle types.

Meanwhile, the OEM segment is growing faster at a 6.97% CAGR through 2030, fueled by new vehicle production and specialized tire requirements, especially for electric vehicles. This growth has increased demand for precision manufacturing and advanced testing equipment to meet strict OEM standards. Equipment suppliers are responding with integrated production systems and quality certifications like ISO 9001 to align with automotive industry expectations.

Geography Analysis

China’s coastal manufacturing belt anchors equipment demand, with Shandong supplying a dense cluster of tire makers and machinery vendors that shorten lead times, trim logistics costs, and reinforce localized innovation linkages. Qingdao’s industrial parks host integrated foundries, CNC centers, and automation integrators that enable end-to-end turnkey delivery, sustaining the China tire manufacturing equipment market’s momentum. Guangdong’s subsidy program of up to RMB 1 million per foreign investor further broadens the customer base by drawing overseas brands into joint ventures, thereby importing leading automation standards into domestic facilities[3]"2025 Invest Guangdong", Department of Commerce of Guangdong Province, com.gd.gov.cn.

Interior provinces such as Hubei leverage central logistics corridors to service multiple automotive hubs, creating fertile ground for mid-scale equipment installations that balance cost and capability. Zhejiang, home to EV supply-chain nodes, prioritizes low-carbon production lines, stimulating procurement of electromagnetic-heating vulcanizers and regenerative-drive material-handling robots. Collective provincial policies nurture a virtuous circle of talent, component supply, and after-sales support, consolidating China’s leadership in tire machinery exports.

Beyond national borders, Southeast Asia has emerged a pivotal growth corridor as Chinese tire groups locate plants in Indonesia, Vietnam, and Cambodia to sidestep trade barriers. Turnkey orders for Jakarta or Phnom Penh facilities typically originate with Qingdao or Yancheng machine builders, reinforcing export receipts. Although Europe and North America remain selective, cost-quality parity gains win bids for certain presses and bead-appliers, illustrating the widening international footprint of the China tire manufacturing equipment market.

Coverage of the tire manufacturing equipment market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for South Korea, Japan, and United States, each shaped by local operating conditions.

Competitive Landscape

The China tire manufacturing equipment market exhibits moderate consolidation. This concentration reflects the capital-intensive nature of equipment development and the technical expertise required to serve sophisticated tire manufacturing requirements. Flagship player Qingdao Mesnac leverages proprietary automation software layered onto mechanical platforms, while peers specialize in curing, building, or upstream processes, creating complementary niches. Scale economies aid large groups in securing bulk steel, proprietary hydraulics, and R&D talent, but agile mid-tier firms compete through customization and rapid engineering cycles.

Technology differentiation remains the prime battleground. Vendors integrate machine-learning engines that predict mold contamination or cord misalignment before failures occur, lowering scrap ratios. Award-winning quality-monitoring suites combine shearography, infrared imaging, and real-time analytics within a single console, evidencing the shift toward data-centric value propositions. Energy-efficient electromagnetic heaters curtail steam demand by 30%, aligning with provincial carbon-credit programs, and conferring procurement advantages for compliant factories.

Strategic moves in 2025 include a multinational’s upgrade at a Kyushu OTR facility that sources specialty presses from Shandong suppliers. Joint development agreements with robotics firms accelerate the convergence of motion-control algorithms and tire-building kinematics, easing the industry’s skilled-labor bottleneck. Collectively, these initiatives underscore an ecosystem capable of exporting sophisticated, yet cost-competitive solutions, reinforcing the ascendancy of the China tire manufacturing equipment market.

China Tire Manufacturing Equipment Industry Leaders

-

Qingdao Mesnac Co., Ltd.

-

Jiangsu Safe-Run Machinery Co., Ltd.

-

HF TireTech Group

-

VMI Group

-

Tianjin Saixiang Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Yokohama Rubber expects to produce the world’s first self-repairing tires at its Suzhou plant by late 2025.

- April 2025: Goodyear showcased advanced tire technologies and launched the SightLine sub-brand dedicated to intelligent-tire solutions at Auto Shanghai 2025.

- February 2025: Gubersail Tire rolled off its first green, low-carbon tire at a fully automated Jiangsu plant featuring state-of-the-art mixing and curing lines.

China Tire Manufacturing Equipment Market Report Scope

| Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | |

| Extrusion Machines | |

| Cutting Machines | |

| Others (Cooling Units, etc.) | |

| Building Area | Bead Winding Machine |

| Tire Building Machine | |

| Others (Strip Winding Machine, etc.) | |

| Curing and Inspection (Testing Area) | Curing Press Machines |

| Tire Painting Machines | |

| Others (Inspection Machines, etc.) |

| Bias |

| Radial |

| Two-wheelers |

| Three-wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Road Vehicles |

| Up to 12 Inches |

| 12 to 18 Inches |

| Above 18 Inches |

| Original Equipment Manufacturers (OEMs) |

| Replacement / Aftermarket |

| By Equipment Type | Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | ||

| Extrusion Machines | ||

| Cutting Machines | ||

| Others (Cooling Units, etc.) | ||

| Building Area | Bead Winding Machine | |

| Tire Building Machine | ||

| Others (Strip Winding Machine, etc.) | ||

| Curing and Inspection (Testing Area) | Curing Press Machines | |

| Tire Painting Machines | ||

| Others (Inspection Machines, etc.) | ||

| By Tire Design | Bias | |

| Radial | ||

| By Vehicle Type | Two-wheelers | |

| Three-wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Road Vehicles | ||

| By Rim Size | Up to 12 Inches | |

| 12 to 18 Inches | ||

| Above 18 Inches | ||

| By End-User | Original Equipment Manufacturers (OEMs) | |

| Replacement / Aftermarket | ||

Key Questions Answered in the Report

What is the 2025 value of the China tire manufacturing equipment market?

The market is valued at USD 765.25 million in 2025.

How fast is demand for EV-specific tire equipment growing?

Production lines dedicated to EV tires are expanding at a 10.63% CAGR through 2030.

Which equipment segment shows the fastest growth?

Curing and inspection systems lead with an 8.53% CAGR owing to AI-enabled quality control.

Why are large-rim tires influencing machinery orders?

Rims above 18 inches grow at 9.97% CAGR, requiring taller building drums and higher-tonnage curing presses.

How do anti-dumping duties affect domestic equipment demand?

Tariffs encourage some tire makers to build overseas plants, tempering local orders but opening export sales for Chinese machinery.

Page last updated on: