Europe Tire Manufacturing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

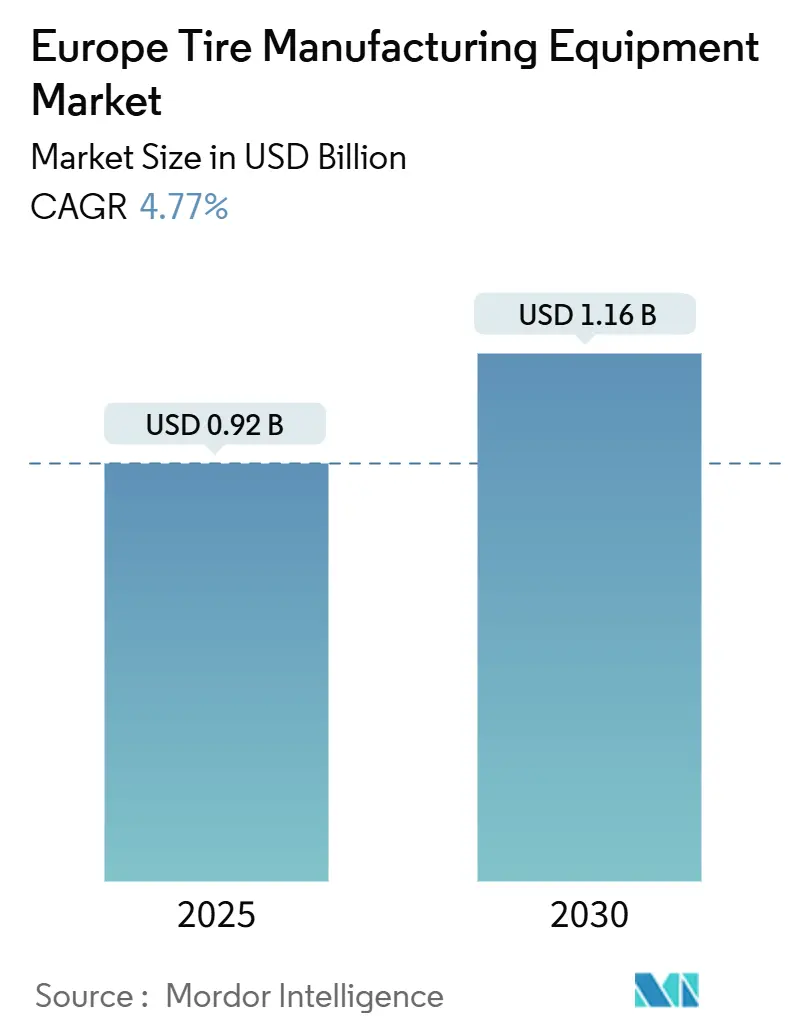

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.16 Billion |

| Growth Rate (2025 - 2030) | 4.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Tire Manufacturing Equipment Market Analysis by Mordor Intelligence

The Europe tire manufacturing equipment market size reached USD 0.92 billion in 2025 and is forecast to attain USD 1.16 billion by 2030, advancing at a 4.77% CAGR. Growth stems from the rapid electrification of Europe’s vehicle fleet, new Euro 7 particle limits, and the need for precision mixing, building, and curing systems that accommodate high-silica compounds. Suppliers report steady orders for digital-ready machinery as tire makers integrate smart-factory analytics for predictive maintenance and traceability. Energy-efficient all-electric presses are gaining traction because rising power costs and carbon goals make legacy hydraulics less attractive. Investment momentum is further boosted by OEM requirements for tight tire–vehicle performance matching, which pushes manufacturers toward equipment with higher uniformity and real-time quality monitoring.

Key Report Takeaways

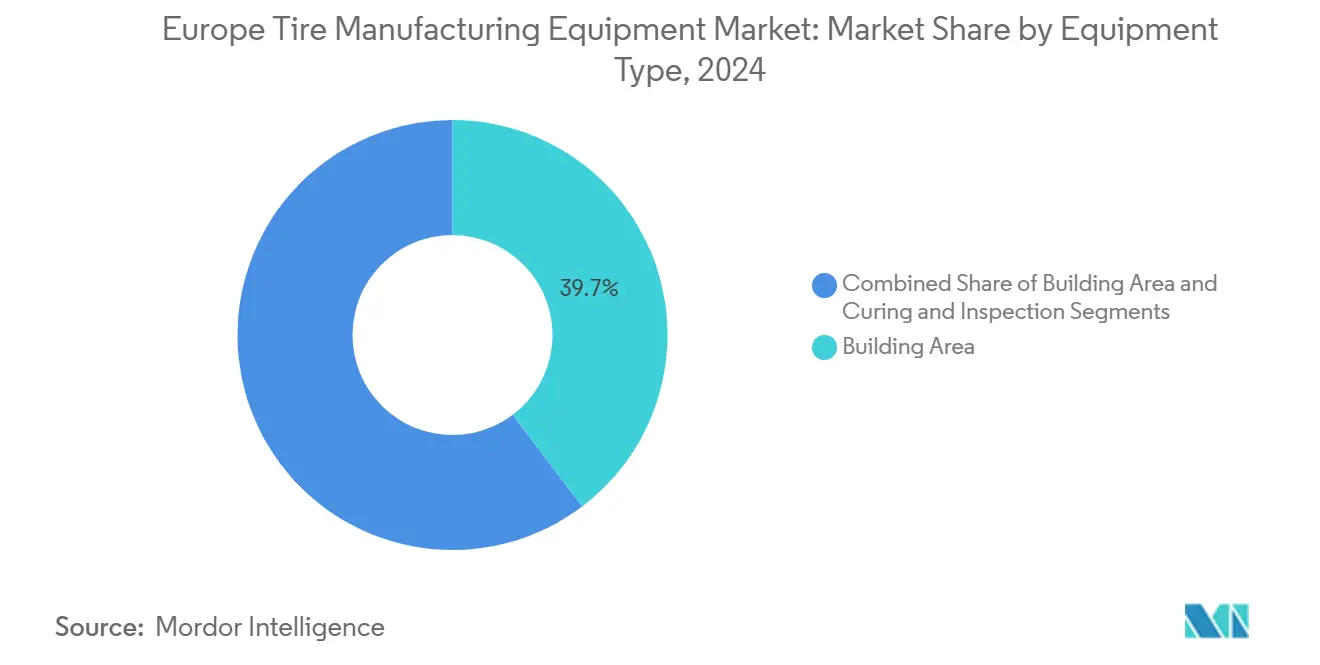

- By equipment type, Building Area led with 39.69% revenue share in 2024; Curing and Inspection is forecasted to expand at 10.41% CAGR through 2030.

- By tire design, Radial captured 88.79% of the Europe tire manufacturing equipment market share in 2024, and is projected to grow at 5.97% CAGR to 2030.

- By vehicle type, Passenger Car held 48.57% share of the Europe tire manufacturing equipment market size in 2024, and is projected to grow at 9.15% CAGR through 2030.

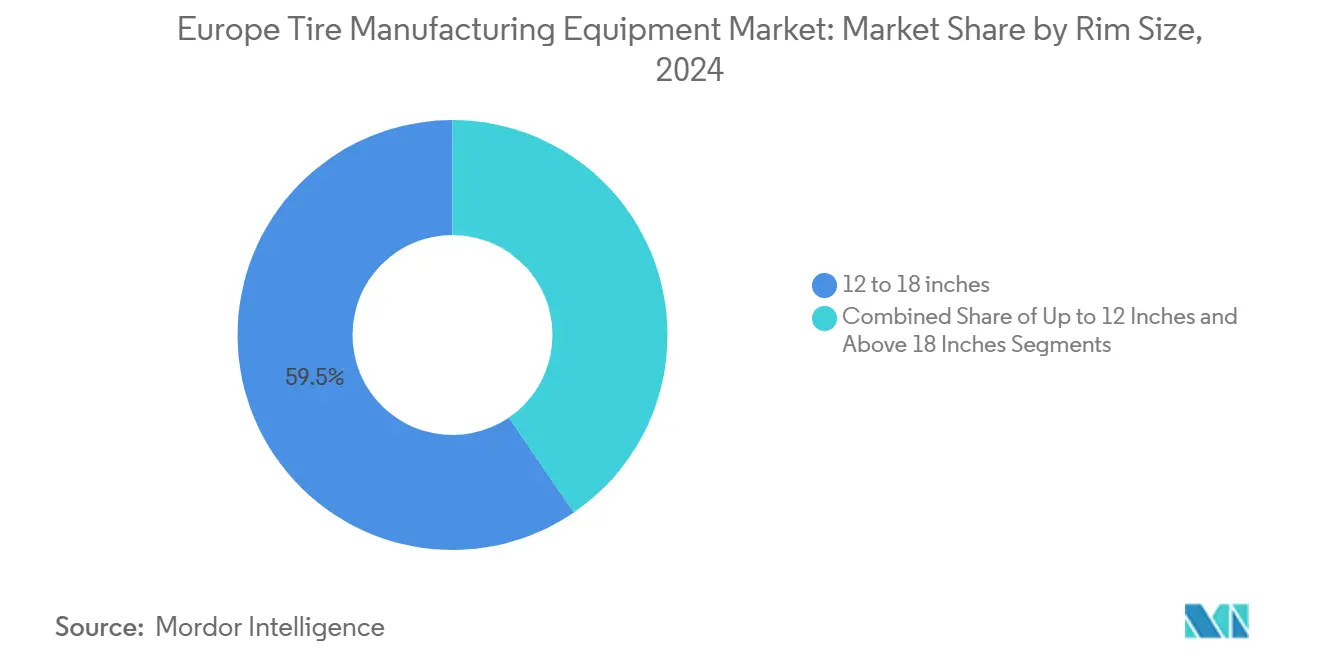

- By rim size, 12-18 inches commanded 59.54% share in 2024; Above 18 inches is forecasted to grow at 7.59% CAGR to 2030.

- By end-user, OEMs dominated with 63.72% share in 2024; OEM-driven orders are forecasted to rise at 6.38% CAGR through 2030.

- By country, Germany led with 21.94% share in 2024, whereas Rest of Europe is forecasted to be the fastest at 6.26% CAGR.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global tire manufacturing equipment market data by Mordor Intelligence represents that combined structure.

Europe Tire Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Silica Radial Compounds | +1.8% | Germany, France, Netherlands, Spain | Medium term (2-4 years) |

| Euro 7 Tire-Particle Limits | +1.2% | EU-wide, particularly Germany, France, Italy | Short term (≤ 2 years) |

| Industry 4.0 Retrofits | +0.9% | Germany, Netherlands, France, UK | Medium term (2-4 years) |

| Tire-Maker Capacity Expansions | +0.7% | Romania, Spain, Germany, Italy | Short term (≤ 2 years) |

| Energy-Cost Spikes | +0.5% | Germany, Netherlands, UK, France | Medium term (2-4 years) |

| EU Circular-Economy Rules | +0.4% | EU-wide, led by Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Led Surge in High-Silica Radial Compounds Needs Advanced Mixing and Extrusion Lines

Electric vehicle tires require high-silica formulations that legacy mixers cannot handle. European manufacturers are accelerating similar upgrades because compound complexity rises with every EV model launch. High-precision temperature management and automated feeding systems deliver the consistency needed for low rolling resistance and wet-grip targets. As the learning curve flattens, suppliers bundle mixing and downstream extrusion into turnkey packages, lifting order values. The sustained shift toward bio-sourced fillers further cements demand for next-generation mixers that can process varied material viscosities at scale.

Euro 7 Tire-Particle Limits Accelerate Uptake of Precision Curing and Inspection Machines

Euro 7 introduces the first legal cap on tire wear particles, prompting immediate replacement of aging presses. Equipment with advanced bladder-pressure control and automated mold cleaning is now mandatory to cut surface roughness that generates micro-debris. VMI’s integrated press-plus-inspection cell, which measures tread uniformity in-line, has become a benchmark. German and Italian plants expedite adoption schedules to avoid production bottlenecks during the 2027–2028 enforcement window. Suppliers report rising quotes for laser-based shearography and X-ray systems that validate internal structure. This regulatory driver is set to lock in multi-year demand for high-accuracy curing solutions across the Europe tire manufacturing equipment market.

Smart-Factory and Industry 4.0 Retrofits for Productivity and Traceability

Large tire makers embed sensors and edge-computing modules into mixers, builders, and presses to capture cycle-time and energy data. Bridgestone uses a unified digital stack to orchestrate thousands of machines across its European plants, evidencing the scale of connectivity deployments. The retrofit wave favors machinery with open protocols and plug-and-play analytics. Predictive maintenance cuts unplanned stoppages, lifting overall equipment effectiveness by high single-digits. Vendors that bundle software licenses and cloud dashboards with hardware secure sticky revenue streams. Even mid-tier manufacturers pursue selective upgrades, creating a broad addressable market for retrofit modules within the Europe tire manufacturing equipment market.

Tire-Maker Capacity Expansions Drive Fresh Capex for Building Area Machines

Europe has seen a resurgence in greenfield plants and major line extensions. Nokian Tyres’ zero-emission facility in Romania underscores the scale of current projects and their focus on sustainable production. Each expansion demands dozens of fully automated tire building machines with quicker bead-set and change-over features. Spain, Germany, and Italy also record sizeable capex announcements, tightening delivery schedules for Building Area suppliers. Automation intensity rises because labor scarcity and ergonomic regulations limit manual processes. Consequently, Building Area equipment remains the single largest revenue contributor to the Europe tire manufacturing equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility | -0.6% | EU-wide, particularly Germany, Italy, Spain | Short term (≤ 2 years) |

| High Capex and Long Paybacks | -0.4% | Eastern Europe, smaller facilities across EU | Medium term (2-4 years) |

| PFAS Ban | -0.3% | EU-wide regulatory impact | Medium term (2-4 years) |

| Skilled-Maintenance Shortage | -0.2% | Germany, Netherlands, France, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Rubber and Petrochemical Prices Delay Equipment Purchases

Swinging rubber and carbon black prices compress margins and force tire makers to conserve cash. Procurement teams postpone non-critical machinery orders when raw materials spike, leading to lumpy booking patterns for equipment vendors. Hedging strategies only partially protect budgets because feedstock and freight remain unpredictable. Suppliers respond with financing plans and rental models, yet uptake among cautious buyers is modest. The result is a short-term dampener on growth, particularly for optional upgrades within the Europe tire manufacturing equipment market.

High Capex and Long Payback Horizons Deter Smaller Manufacturers

State-of-the-art tire lines can exceed USD 40 million, a hurdle for regional players with limited balance-sheet strength. Grant schemes help, but interest-rate hikes in 2024–2025 raise borrowing costs and prolong break-even timelines. Smaller firms also struggle to recruit technicians capable of running complex robotics, which adds hidden lifetime costs. Some opt for modular retrofits instead of full line replacements, slowing overall equipment turnover. This capex barrier caps market penetration in Eastern Europe, mildly trimming the long-term growth slope.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Building Area Maintains Commanding Lead as Curing Innovation Accelerates

Building Area machinery accounted for 39.69% of the Europe tire manufacturing equipment market in 2024, reflecting its central role in automating bead winding and carcass assembly. Rising plant expansions and labor cost pressures keep demand high, while integrated servo-drives improve cycle time. Curing and Inspection, although a smaller base, is projected as the fastest-growing category at 10.41% CAGR through 2030. The shift is tied to Euro 7 compliance and the search for lower energy consumption presses.

Energy-optimized direct-pressure curing systems can cut consumption by up to 86%, pushing operators to accelerate replacements. Vendors integrate machine-vision and laser shearography, creating a bundled sales proposition that raises average deal values. Upstream equipment such as mixers and calenders records steady but less spectacular growth. However, mixers capable of recycled and bio-filler handling are in focus as sustainability targets tighten, ensuring that upstream lines continue to modernize within the Europe tire manufacturing equipment market.

By Tire Design: Radial Supremacy Dictates Specialized Machinery Demand

Radial tires held 88.79% share in 2024 and remain the dominant design across passenger and commercial segments. The segment is projected to post a 5.97% CAGR, driven by electric vehicle adoption and performance tire demand that requires advanced radial construction techniques. Bias construction lingers only in niche off-road and agricultural use, resulting in minimal new equipment orders.

Radial production needs advanced steel belt application, splice control, and uniformity measurement. Suppliers refine tension-controlled let-off systems and automated belt placers to enhance consistency. Emerging very-high-flexion radial formats for large agricultural tires introduce even more layers, spurring incremental machinery upgrades. Collectively, radial dominance secures a long runway for equipment tailored to its complex build architecture.

By Vehicle Type: Passenger Car Leads yet Commercial Segments Accelerate Investment

Passenger Car applications represented 48.57% of the Europe tire manufacturing equipment market in 2024, benefiting from scale and standardized specifications. This segment is forecast to grow 9.15% CAGR through 2030 as EV volumes rise and premium tire variants proliferate. Light and heavy commercial vehicle lines invest in larger carcass drum formats and robust bead assemblies to meet higher load demands.

Commercial fleets shift toward fuel-efficient tires, which require specialized tread patterns and high-tensile steel reinforcement, driving separate equipment streams. Off-road vehicle producers employ giant building drums and curing presses for diameters above 50 inches, a high-margin niche. Two-wheeler demand in Southern Europe remains steady, supplying a baseline market for compact builders and vulcanizers.

By Rim Size: Mid-Range Dominates while Large Diameters Gain Momentum

The 12-18 inch category commanded 59.54% share in 2024, anchoring capacity utilization across legacy European plants. Standardization in this mid-range yields economies of scale and streamlined tooling. Above 18 inches is the fastest riser with a 7.59% CAGR, reflecting SUV, premium sedan, and EV trends that favor bigger wheels.

Large-diameter tires necessitate extended-stroke presses and heavier bead setters, inducing fresh capex among established plants. Suppliers develop adaptive clamping systems to handle the wider dimension spread without productivity loss. Up to 12 inch sizes, dominated by industrial and trailer applications, deliver consistent but modest volumes, forming a reliable though limited revenue base.

By End-User: OEM Partnerships Shape Technology Roadmaps

OEMs accounted for 63.72% share in 2024, leveraging their scale to demand precision and traceability from tire manufacturers. As vehicle platforms evolve, tire suppliers must prove compound performance and NVH characteristics through tighter production tolerances. The result is continuous equipment upgrades synchronized with new car launches. OEM-related demand is expected to rise at 6.38% CAGR, slightly ahead of the replacement market.

Aftermarket-oriented production, while smaller at 36.28%, offers flexibility advantages and cushions downturns in OEM schedules. The replacement market segment supports equipment demand through volume requirements and diverse tire specification needs that require flexible production capabilities. However, higher SKU diversity forces investment in rapid-change tooling and advanced scheduling software, keeping equipment modernization relevant across both end-user groups within the Europe tire manufacturing equipment market.

Geography Analysis

Germany led with 21.94% share in 2024 due to its integrated automotive ecosystem and the presence of global tire brands. The country’s push for EV leadership compels manufacturers to install high-precision mixers and smart-factory modules that comply with stringent quality benchmarks. Domestic machinery builders also benefit as local customers favor nearby service and customization support.

Southern and Western Europe, notably Spain, Italy, France, the United Kingdom, and the Netherlands, comprise a significant collective share. Spain’s recent plant modernizations attracted USD 207 million in new technology and elevated demand for next-generation builders and presses[1]“Bridgestone Announces up to €207 m Investment in Burgos Plant,” Bridgestone EMEA, press.bridgestone-emea.com. Italy’s premium tire focus keeps calendering and bead apex lines active, while France consolidates activity around sustainable materials and bio-chem integration. Each sub-region applies its own specialty, creating a mosaic of equipment needs that suppliers must meet with configurable offerings.

Rest of Europe is the fastest-growing sub-region at 6.26% CAGR. Romania’s zero-emission plant and EIB-backed financing showcase the scale of eastern capacity expansion. Lower labor costs, tax incentives, and proximity to both EU and export markets underpin the surge. Regional logistics corridors improve, enabling efficient shipment of large machinery. Eastern Europe’s rise diversifies the geographic footprint of the Europe tire manufacturing equipment market and provides new opportunities for service contracts and spare-parts supply chains.[2]“Romania Gets EIB Support for World’s First Zero-Emissions Tyre Factory,” European Investment Bank, eib.org

The tire manufacturing equipment market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for United States, China, South Korea, and Japan, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

VMI Group, HF TireTech Group, and MESNAC are spearheading consolidation in the European tire manufacturing equipment market, which is characterized by moderate fragmentation, through strategic acquisitions and technology partnerships. Their edge lies in full-line integration, proprietary software, and global service centers. VMI’s quality-monitoring press cell has won multiple customer awards, reinforcing its premium positioning. HF invests in extrusion and calendering expertise to bundle upstream and downstream capabilities, while MESNAC leverages scale advantages and R&D hubs in Asia and Europe.

Technology leadership centers on Industry 4.0. Vendors incorporate edge-analytics boxes, digital twins, and IoT architecture from the design stage. Predictive-maintenance subscriptions generate recurring revenue and foster customer lock-in. Smaller specialists often target niche modules, such as bead apexers or laser inspection heads, and become acquisition targets once their technology matures.

Sustainability themes drive product roadmaps. Developers showcase presses with energy-recovery hydraulics and mixers with optimized rotor designs that cut power draw. Recycling-ready mixers accept higher crumb-rubber ratios, and curing presses adopt low-temperature compounds. M&A activity reflects this trend: larger groups buy innovators with carbon-footprint credentials, accelerating consolidation yet maintaining a multi-player field within the Europe tire manufacturing equipment market.

Europe Tire Manufacturing Equipment Industry Leaders

VMI Group

HF TireTech Group

MESNAC Co., Ltd.

Kobelco Stewart Bolling

Bartell Machinery Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nokian Tyres began deliveries from its zero-emission Romania factory, the first of its kind worldwide.

- June 2025: Black Donuts Inc. launched InTire Labs, an independent material research center in Tampere, Finland.

- September 2024: Marangoni formed a strategic partnership with Prinx Chengshan Europe / Austone Tires to commercialize a new ring tread design.

Europe Tire Manufacturing Equipment Market Report Scope

| Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | |

| Extrusion Machines | |

| Cutting Machines | |

| Others (Cooling Units, etc.) | |

| Building Area | Bead Winding Machines |

| Tire Building Machines | |

| Others (Strip Winding Machines, etc.) | |

| Curing and Inspection (Testing Area) | Curing Press Machines |

| Tire Painting Machines | |

| Others (Inspection Machines, etc.) |

| Bias |

| Radial |

| Two-Wheelers |

| Three-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Road Vehicles |

| Up to 12 inches |

| 12 – 18 inches |

| Above 18 inches |

| Original Equipment Manufacturers (OEMs) |

| Replacement / Aftermarket |

| Germany |

| United Kingdom |

| Spain |

| Italy |

| France |

| Netherlands |

| Rest of Europe |

| By Equipment Type | Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | ||

| Extrusion Machines | ||

| Cutting Machines | ||

| Others (Cooling Units, etc.) | ||

| Building Area | Bead Winding Machines | |

| Tire Building Machines | ||

| Others (Strip Winding Machines, etc.) | ||

| Curing and Inspection (Testing Area) | Curing Press Machines | |

| Tire Painting Machines | ||

| Others (Inspection Machines, etc.) | ||

| By Tire Design | Bias | |

| Radial | ||

| By Vehicle Type | Two-Wheelers | |

| Three-Wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Road Vehicles | ||

| By Rim Size | Up to 12 inches | |

| 12 – 18 inches | ||

| Above 18 inches | ||

| By End-User | Original Equipment Manufacturers (OEMs) | |

| Replacement / Aftermarket | ||

| By Country | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe tire manufacturing equipment market?

The market stands at USD 0.92 billion in 2025.

How fast is the market expected to grow through 2030?

It is projected to expand at a 4.77% CAGR, reaching USD 1.16 billion by 2030.

Which equipment segment shows the highest revenue share?

Building Area machinery leads with 39.69% share in 2024.

Which geographic area is growing the fastest?

Rest of Europe, led by Romania and other Eastern countries, is forecast to grow at 6.26% CAGR.

What regulatory factor most influences new equipment purchases?

Euro 7 tire-particle limits necessitate precision curing and inspection systems to ensure compliance.

Page last updated on: