South Korea Tire Manufacturing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

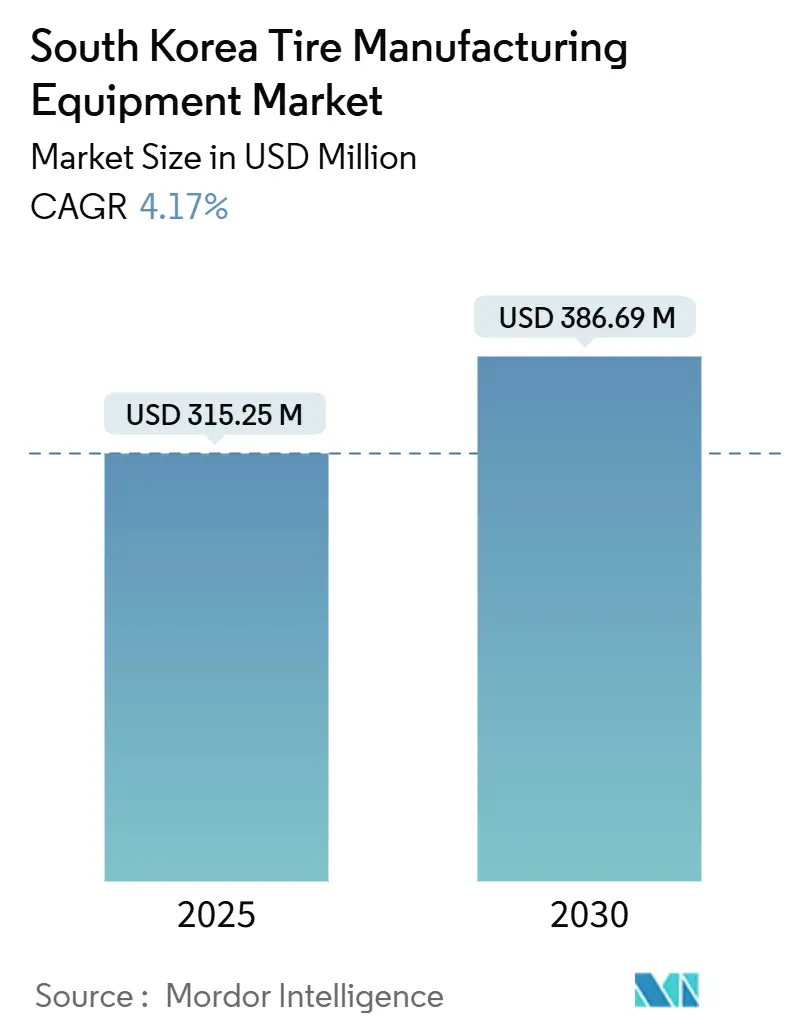

| Market Size (2025) | USD 315.25 Million |

| Market Size (2030) | USD 386.69 Million |

| Growth Rate (2025 - 2030) | 4.17% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Tire Manufacturing Equipment Market Analysis by Mordor Intelligence

The South Korea tire manufacturing machinery market size reached USD 315.25 million in 2025 and is projected to advance to USD 386.69 million by 2030, registering a 4.17% CAGR. The market’s momentum is underpinned by South Korea’s role as a global tire production hub. Rapid electrification of the vehicle parc, the industry’s pivot toward rim sizes above 18 inches, and government-backed smart-factory incentives are compelling tire makers to upgrade to advanced mixing, curing, and inspection systems. Upstream mixing machines already command the largest value pool, but the fastest growth flows to curing and inspection systems equipped with smart-vision analytics capable of 99.96% defect-detection accuracy[1]Max Wallis, “Tire Technology Expo 2025: A showcase of innovation, sustainability, digitalization and regulatory challenges,” Tire Technology International, tiretechnologyinternational.com. Localization of equipment supply has accelerated as manufacturers mitigate China-related risk, driving incremental orders to domestic suppliers. Simultaneously, rising labor shortages and the country’s top-ranked robot density create a fertile environment for automation, predictive-maintenance software, and energy-efficient presses.

Key Report Takeaways

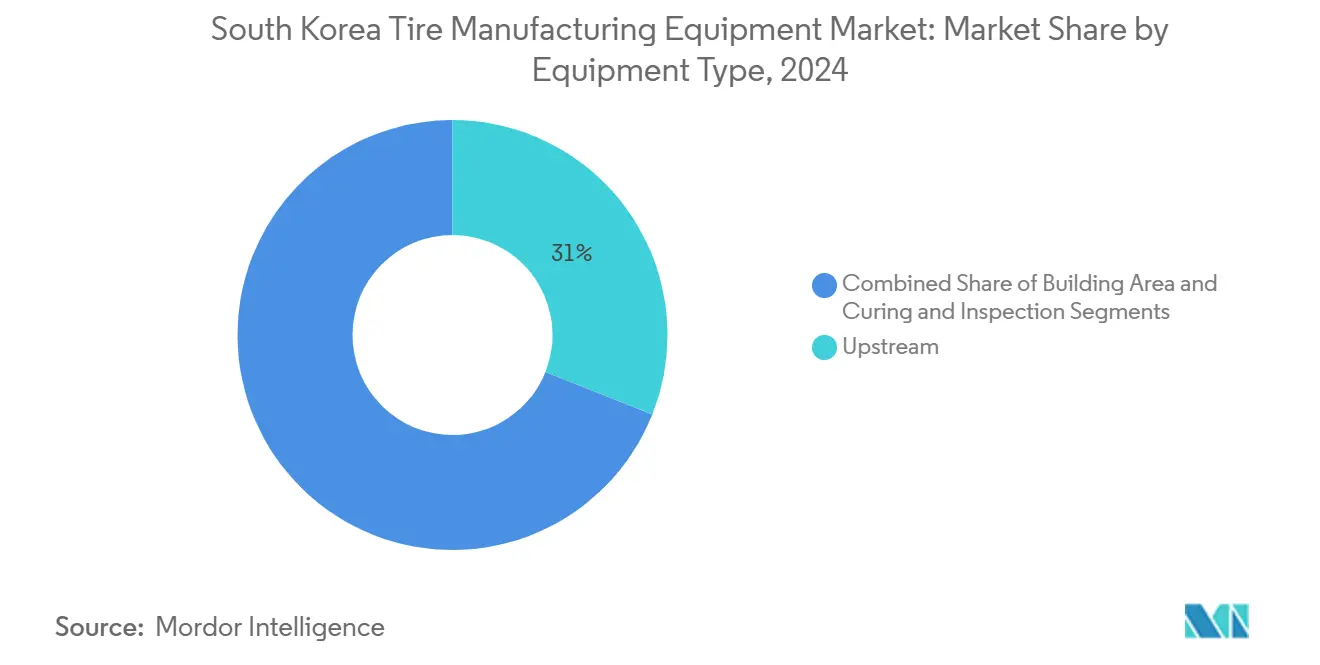

- By equipment type, upstream mixing machines led with 31.04% of the South Korea tire manufacturing machinery market share in 2024, while curing and inspection systems are projected to post the highest 8.39% CAGR to 2030.

- By tire design, radial technology captured 97.24% of the South Korea tire manufacturing machinery market size in 2024 and is expanding at a 4.67% CAGR.

- By vehicle type, passenger-car applications accounted for 46.55% of spending on South Korea tire manufacturing machinery in 2024 and are forecasted to grow at a 9.62% CAGR through 2030.

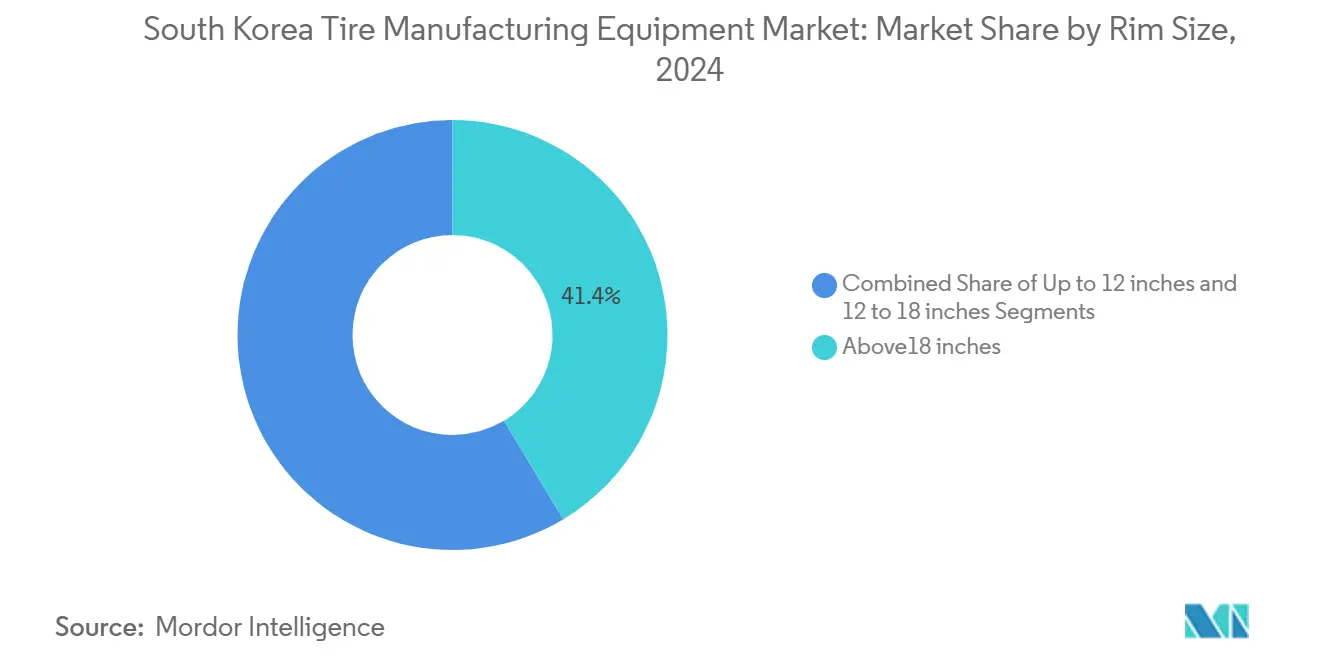

- By rim size, tires above 18 inches held 41.38% of the South Korea tire manufacturing machinery market size in 2024 and will rise at a 7.68% CAGR.

- By end-user, the aftermarket segment dominated with 81.73% of demand in 2024, yet OEM procurement is accelerating at a 6.14% CAGR to 2030.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of South korea. The tire manufacturing equipment market share in our global report expresses these relative weights.

South Korea Tire Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Led Capacity Expansion | +1.8% | Ulsan, Gyeonggi, Busan | Medium term (2-4 years) |

| Shift To Above 18-Inch Rims | +1.2% | Seoul, Ulsan, Gyeonggi | Short term (≤ 2 years) |

| Smart and Automated Factory Incentives | +0.9% | Nationwide, concentrated in Ulsan, Gyeonggi | Long term (≥ 4 years) |

| Localization Push | +0.7% | Ulsan, Busan, Gyeonggi | Medium term (2-4 years) |

| IIOT-Enabled Predictive Maintenance | +0.6% | Seoul, Ulsan, Daegu | Medium term (2-4 years) |

| Energy-Efficient Mixers/Curing Presses | +0.4% | Ulsan, Gyeonggi, Busan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Led Capacity Expansion for Advanced Tires

Electric-vehicle uptake is reshaping equipment requirements as manufacturers adopt silica-rich compounds and low-rolling-resistance designs that demand upgraded mixing and curing lines. Producers have earmarked new plants and retrofits around Hyundai’s dedicated EV facility in Ulsan, slated for launchv by 2026. Suppliers offering energy-efficient mixers and synchronized curing presses are therefore logging multi-year order books.

Shift to Above 18-Inch Rims Driving Precision Machinery Demand

As the automotive industry shifts towards larger rim sizes, there's a surging demand for advanced tire building and curing equipment. These machines must adeptly manage intricate geometries and stringent tolerances. To meet the challenge of tighter dimensional tolerances in bead winding and strip application, manufacturers are turning to AI-driven building drums and machine-vision inspections. These technologies significantly cut defect rates and minimize scrap.

Government Incentives for Smart and Automated Factories

The South Korean government is poised to bring the number of smart factories in the country up to 30,000 by 2025, with plans to train 40,000 skilled workers in preparation for the ever-expanding fourth industrial revolution. The government is also pumping 215.4 billion won into research and development projects for smart factories, as part of an initiative to implement ‘smart’ technology in the local manufacturing industry. Tire makers leverage these grants to deploy IIoT sensors, MES software, and autonomous guided vehicles that trim downtime and energy use.[2]Korea Bizwire in AI & Big Data, "South Korean Government Plans to Establish 30,000 Smart Factories by 2025", koreabizwire.com

Localization Push Amid China-Related Supply-Chain Risk

Supply chain diversification has emerged as a strategic imperative for Korean tire manufacturers, driving substantial investments in domestic equipment suppliers and alternative sourcing strategies. Trade uncertainty is steering procurement toward domestic equipment vendors that can guarantee delivery and parts availability. Leading Korean suppliers have boosted capacity for mixers and curing presses, capitalizing on reshoring incentives and buyers’ preference for proximate support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature Domestic Replacement-Tire | -1.1% | Nationwide, particularly Seoul, Busan | Long term (≥ 4 years) |

| Rubber Price Volatility | -0.8% | Ulsan, Gyeonggi, Busan | Short term (≤ 2 years) |

| Mechatronics Talent Shortage | -0.6% | Seoul, Daegu, Ulsan | Medium term (2-4 years) |

| Stricter VOC Limits | -0.4% | Ulsan, Gyeonggi, Busan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mature Domestic Replacement-Tire Demand Caps New Lines

South Korea's domestic replacement tire market has matured, limiting demand for new production lines as manufacturers focus on optimizing existing capacity. The saturation stems from a stable vehicle base and predictable replacement cycles, curbing growth opportunities. Korean tire makers are shifting focus to exports and premium segments, reducing the need for large-scale equipment investments. Aftermarket demand dominates at 81.73%, highlighting a preference for efficiency over expansion. Competition from imported tires in the passenger car segment further discourages premium equipment upgrades.

Rubber Price Volatility Tightening Capex Budgets

Natural rubber price volatility is tightening capital expenditure budgets for Korean tire manufacturers, as fluctuating input costs impact profitability and cash flow. Projected growth in Thailand’s rubber industry, driven by demand from China and the US, suggests continued price pressures. Manufacturers are deferring non-essential equipment investments to manage raw material costs. Supply-side risks like labor shortages and disease outbreaks add further uncertainty. Smaller equipment suppliers are especially affected, lacking financial flexibility to support manufacturers during volatile periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Smart Vision Systems Drive Innovation

The South Korea tire manufacturing machinery market size for upstream machines captured a 31.04% slice of the 2024 revenue. Predictive-maintenance modules and closed-loop temperature control have become default specifications as producers seek batch repeatability. Conversely, curing and inspection lines integrated with machine-vision sensors represent the fastest-growing niche, predicted to post an 8.39% CAGR. Capital budgets favor these systems because they lift first-pass yield and minimize warranty claims, especially critical for export-bound EV tires.

Suppliers bundling AI analytics with hardware capture disproportionate value as customers demand single-source integration. Second-tier segments such as building-area machines register steady, mid-single-digit expansion centered on upgrades for larger tire diameters. Extrusion and calendaring units gain incremental orders from compound innovations that require tighter gauge control. Auxiliary equipment, coolers, handling robots, and bead winders benefit from the holistic automation trend but command a smaller share of the South Korea tire manufacturing machinery market.

By Tire Design: Radial Dominance Reinforces Equipment Specialization

Radial construction accounted for 97.24% of the South Korea tire manufacturing machinery market share in 2024. Equipment is therefore optimized for steel-belt placement precision, uniform sidewall geometry, and high-speed bead seating. Growth at a 4.67% CAGR is fueled by premium radial designs for EVs and SUVs, necessitating finer cord tension control in building drums.

Bias-ply machines serve a sliding 2.76% niche focused on off-road and agricultural applications; investments here remain limited to maintenance rather than new capacity. Radial standardization lets vendors scale component manufacturing, lowering unit costs and freeing R&D budgets for smart-factory modules. Export regulations demanding enhanced wet-grip and low-noise characteristics intensify demand for next-generation radial machinery.

By Vehicle Type: Passenger Car Focus Drives Premium Equipment Demand

Passenger-car lines commanded 46.55% of equipment spending in 2024, and are projected to surge at a 9.62% CAGR. Growth is anchored in high-margin, large-rim EV and SUV tires that require sophisticated compound mixing and precise carcass profiling. Light commercial and delivery vehicle demand rises in tandem with e-commerce growth, albeit off a smaller base. Two- and three-wheeler equipment remains stable, driven by Southeast Asian export orders but constrained by cost-sensitive buyers.

Medium and heavy commercial vehicle lines face cyclical fleet replacement, limiting spending to incremental productivity upgrades. OEM-aligned passenger-car projects receive priority funding when automakers specify low-rolling-resistance tires for vehicle efficiency credits, amplifying machinery opportunities tied to advanced compounding and inspection.

By Rim Size: Large Diameter Trend Reshapes Manufacturing Requirements

Tires above 18 inches generated 41.38% of revenue in 2024, translating to USD 130.3 million of the South Korea tire manufacturing machinery market size. Their 7.68% CAGR compels manufacturers to recalibrate mold presses for higher cavity pressures and redesign building machines for greater drum diameter. The 12 to 18-inch bracket, at roughly 35% share, still represents the industry’s workhorse volume; investment here focuses on lifecycle upgrades.

Rims up to 12 inches continue to decline as entry-level vehicle sales stagnate. For large-diameter tires, bead winding stations with laser alignment and high-torque servomotors ensure concentricity, while smart vision inspects sidewall logos. Large-diameter tires, priced 30-50% above standard sizes, drive significant investments in equipment. This, in turn, fuels technological advancements and market growth, favoring specialized equipment suppliers.

By End-User: Aftermarket Dominance Shifts Toward OEM Growth

Aftermarket customers generated 81.73% of 2024 equipment sales, leveraging predictable replacement cycles to fund modernization that raises throughput without expanding footprint. Nonetheless, OEM demand is now the faster mover, rising at 6.14% CAGR through 2030 as automakers push EV localization. OEM projects often bundle customized MES software and traceability protocols to satisfy vehicle-platform specifications, placing higher requirements on machine-data integration.

The aftermarket segment's stability provides equipment suppliers with predictable revenue streams, though growth opportunities are limited by market maturity. As environmental regulations and quality standards tighten, compliance factors are increasingly shaping equipment selection and upgrade cycles, especially in facilities catering to export markets with stringent certification mandates.

Geography Analysis

Ulsan anchors the South Korea tire manufacturing machinery market, benefiting from the nation’s largest automotive cluster and a forthcoming dedicated EV plant slated to launch mass production in late 2025. Home to more than 300 automotive-related firms, the city generates over USD 38 billion in output. It hosts an eco-industrial park where waste-heat reuse and material-exchange schemes push factories toward energy-efficient mixers and smart-curing chambers. Machine suppliers have established service hubs nearby to satisfy rapid-response maintenance contracts demanded by 24-hour tire operations[3]Invest Korea, “Korea’s Future Car Industry, Continual Growth by Actively Responding to Domestic and Global Changes,” investkorea.org.

Gyeonggi Province ranks second, leveraging proximity to Seoul and the Banwol-Sihwa Smart Green Industrial Complex, which offers integrated logistics, cloud-based ERP, and pilot lines for autonomous guided vehicles. Companies here capitalize on government grants to retrofit legacy lines with IIoT sensors while maintaining export links via Incheon port. Equipment vendors often stage factory-acceptance tests in Gyeonggi, shortening commissioning cycles for regional buyers.

Busan and its hinterland form the third pole of activity. The port facilitates the import of specialty steel cords and the export of finished equipment, encouraging precision-machinery workshops to cluster nearby. Local authorities market Busan’s mechatronics skill base to support high-precision mold machining and servo-drive assembly. Although smaller, Daegu-Gyeongbuk Free Economic Zone aspires to become a knowledge-industry hub, courting supply-chain partners for smart-factory projects. Tighter VOC limits enforce press upgrades nationwide, driving uniform demand across regions for closed-loop exhaust systems.

Mordor Intelligence examines the tire manufacturing equipment market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for China, Japan, and United States and more.

Competitive Landscape

The South Korea tire manufacturing machinery market exhibits moderate consolidation: three leading suppliers account for roughly 46% of revenue, with the remainder diffused among specialized robotics integrators, mold makers, and IoT software firms. Incumbents differentiate through AI-powered automation; for example, one firm’s vision-inspection package boosts defect detection to 99.96%, reducing scrap and warranty costs.

Strategic investments spotlight energy-efficient hydraulic presses and electric-servo mixers that lower power draw by approximately 10–15%, aligning with eco-industrial-park KPIs. Partnerships between machinery builders and control-system providers embed predictive-maintenance algorithms, improving uptime guarantees that buyers increasingly demand within service-level agreements.

White-space opportunities lie in mid-tier smart-factory modules, especially edge-computing gateways that link legacy PLCs to cloud analytics. Suppliers agile enough to marry mechanical expertise with data science skills win contracts from tire manufacturers racing to harness South Korea’s highest robot density. Patent filings covering AI defect classification, real-time compound rheology monitoring, and automated palletizing have climbed sharply since 2024, underscoring intensifying innovation rivalry.

South Korea Tire Manufacturing Equipment Industry Leaders

-

Saehwa IMC

-

HF TireTech Group

-

VMI Group

-

Mesnac Co.

-

Kobelco (Kobe Steel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kumho Tire finalized its plant relocation deal from Gwangju to Hampyeong, paving the way for a 5.3 million-unit annual capacity by 2028.

- May 2025: Nexen Tire inked a long-term supply agreement with LD Carbon to deploy recovered carbon black across its global factories.

- January 2025: Hyosung Advanced Materials initiated the sale process for its tire-cord unit, targeting USD 1 billion to fund diversification.

- August 2024: Nexen Tire adopted 3-D printing to accelerate tire-mold production, trimming lead times and tooling costs.

South Korea Tire Manufacturing Equipment Market Report Scope

| Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | |

| Extrusion Machines | |

| Cutting Machines | |

| Others (Cooling Units, etc.) | |

| Building Area | Bead Winding Machine |

| Tire Building Machine | |

| Others (Strip Winding Machine, etc.) | |

| Curing and Inspection (Testing Area) | Curing Press Machines |

| Tire Painting Machines | |

| Others (Inspection Machines, etc.) |

| Bias |

| Radial |

| Two-wheelers |

| Three-wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Road Vehicles |

| Up to 12 inches |

| 12 to 18 inches |

| Above 18 inches |

| Original Equipment Manufacturers (OEMs) |

| Replacement / Aftermarket |

| By Equipment Type | Upstream (Mixer and Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | ||

| Extrusion Machines | ||

| Cutting Machines | ||

| Others (Cooling Units, etc.) | ||

| Building Area | Bead Winding Machine | |

| Tire Building Machine | ||

| Others (Strip Winding Machine, etc.) | ||

| Curing and Inspection (Testing Area) | Curing Press Machines | |

| Tire Painting Machines | ||

| Others (Inspection Machines, etc.) | ||

| By Tire Design | Bias | |

| Radial | ||

| By Vehicle Type | Two-wheelers | |

| Three-wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Road Vehicles | ||

| By Rim Size | Up to 12 inches | |

| 12 to 18 inches | ||

| Above 18 inches | ||

| By End-User | Original Equipment Manufacturers (OEMs) | |

| Replacement / Aftermarket | ||

Key Questions Answered in the Report

How big is the South Korea tire manufacturing machinery market in 2025?

The market stands at USD 315.25 million in 2025 and is forecast to grow to USD 386.69 million by 2030.

What is the projected CAGR for tire-machinery spending through 2030?

Spending is expected to rise at a 4.17% CAGR over the 2025–2030 period.

Which equipment segment is growing the fastest?

Curing and inspection systems equipped with smart-vision analytics are projected to post the highest 8.39% CAGR.

Why are rim sizes above 18 inches important for machinery suppliers?

These tires require high-precision building and curing equipment, driving a 7.68% CAGR for machinery targeting this rim class.

How does government policy influence machinery investment?

Subsidies covering up to 80% of smart-factory capex and favorable tax incentives accelerate adoption of automated, energy-efficient lines.

Who dominates demand—OEMs or the aftermarket?

The aftermarket still leads with 81.73% of 2024 demand, but OEM procurement is growing faster at a 6.14% CAGR as EV production ramps up.

Page last updated on: