Wheel Alignment Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

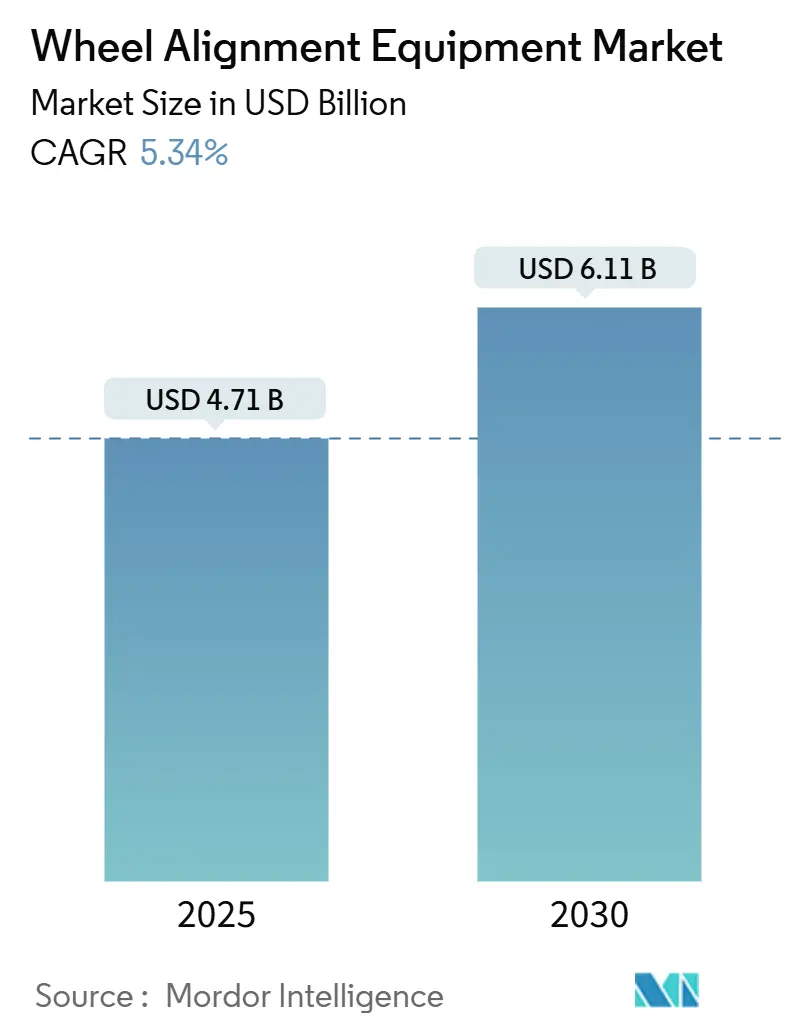

| Market Size (2025) | USD 4.71 Billion |

| Market Size (2030) | USD 6.11 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

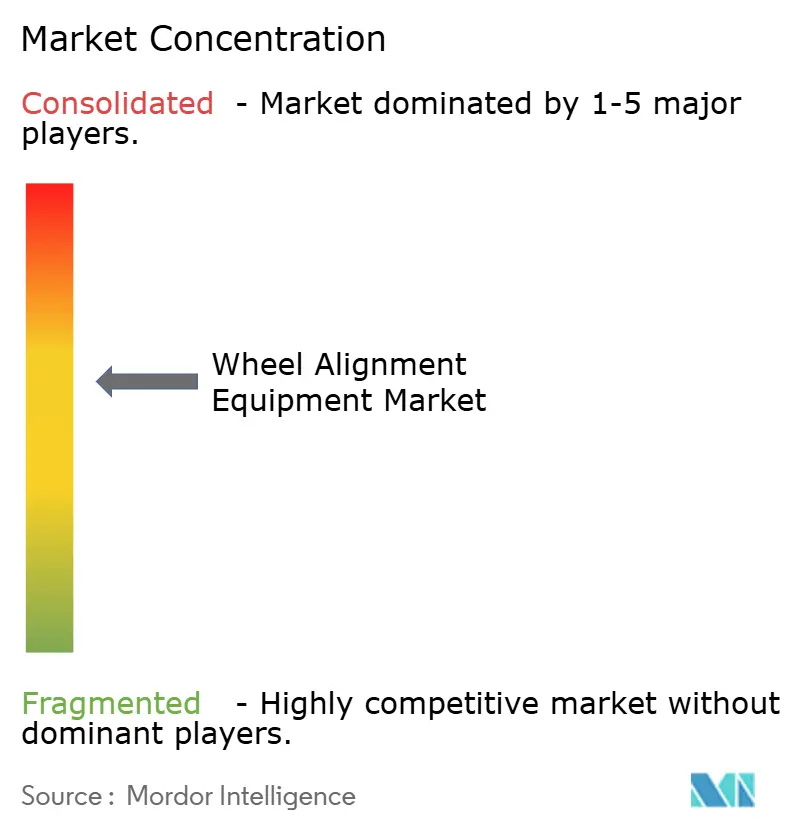

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wheel Alignment Equipment Market Analysis by Mordor Intelligence

The wheel alignment equipment market size stands at USD 4.71 billion in 2025 and is projected to reach USD 6.11 billion by 2030, registering a 5.34% CAGR over the period. Momentum stems from 3D vision adoption that cuts cycle times, IoT-ready wireless features that elevate workshop productivity, and resilient aftermarket demand tied to Asia-Pacific’s expanding vehicle parc. Regulatory tightening around periodic safety inspections, together with right-to-repair legislation, turns alignment from a discretionary add-on into a mandated service, reinforcing baseline demand across mature and emerging economies. Competitive strategies increasingly pivot toward subscription software, data analytics, and mobile service models, which lower acquisition barriers and widen addressable end-user segments. Meanwhile, capital-intensive workshops balance rising equipment capability with tight labor availability, nudging decision-makers toward automated systems that maximize return per technician hour.

Key Report Takeaways

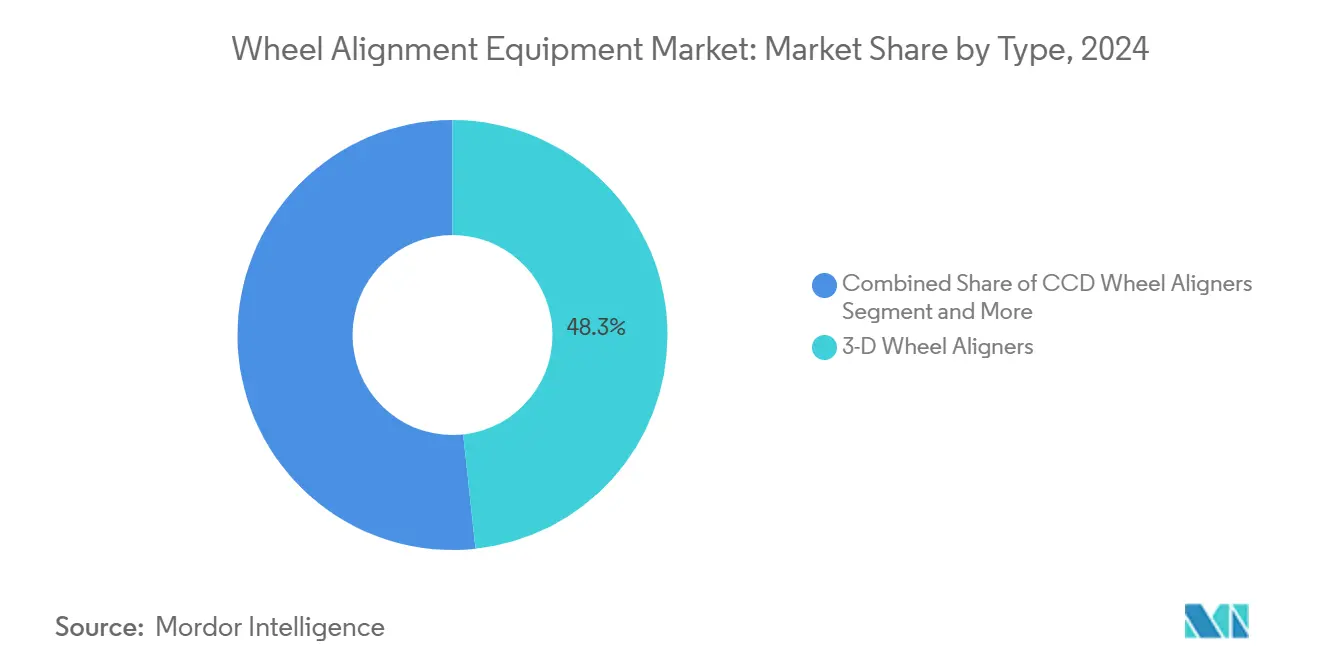

- By type, 3D wheel aligners led with 48.31% revenue share in 2024 and are forecast to expand at a 5.88% CAGR through 2030.

- By application, passenger cars accounted for a 60.14% share of the wheel alignment equipment market size in 2024, and light commercial vehicles are advancing at a 6.56% CAGR through 2030.

- By automation level, manual systems held 54.25% of the wheel alignment equipment market share in 2024, while automatic platforms are projected to grow at a 7.45% CAGR to 2030.

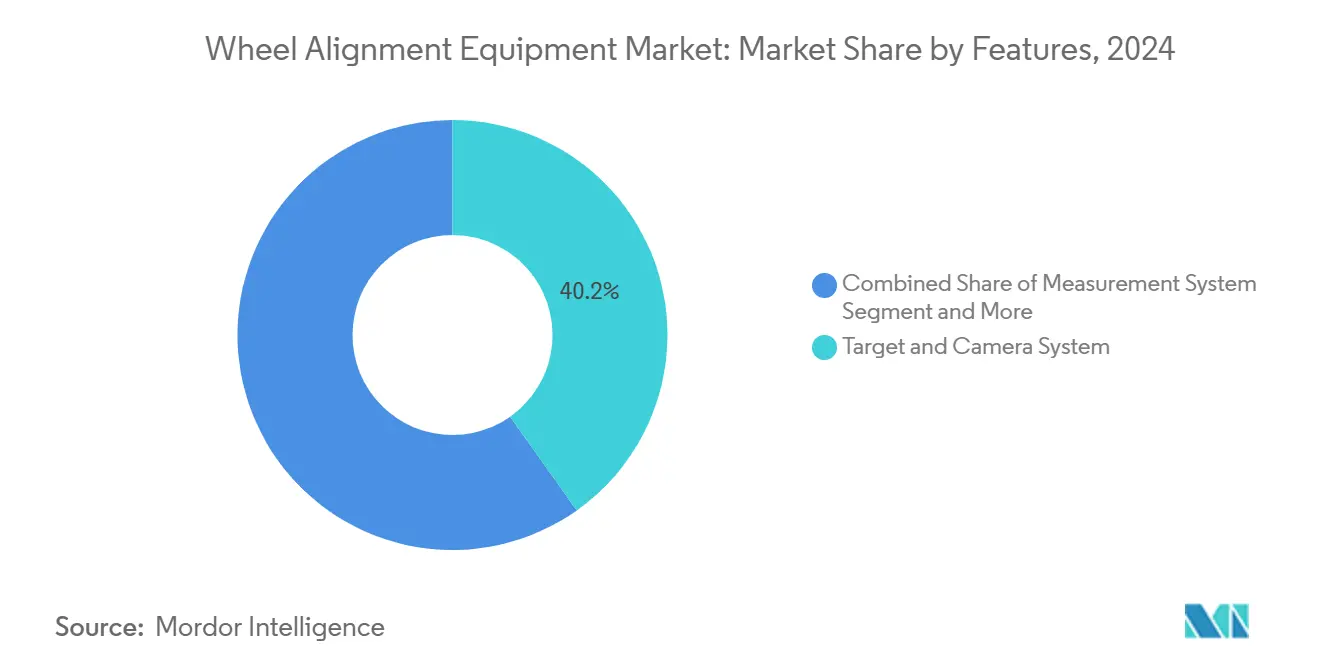

- By features, target and camera system led with 40.17% share of the wheel alignment equipment market size in 2024, while wireless connectivity is forecast to expand at a 7.82% CAGR through 2030.

- By end-user, automotive repair shops captured 45.66% revenue share in 2024; fleet management companies record the highest projected CAGR at 6.94% through 2030.

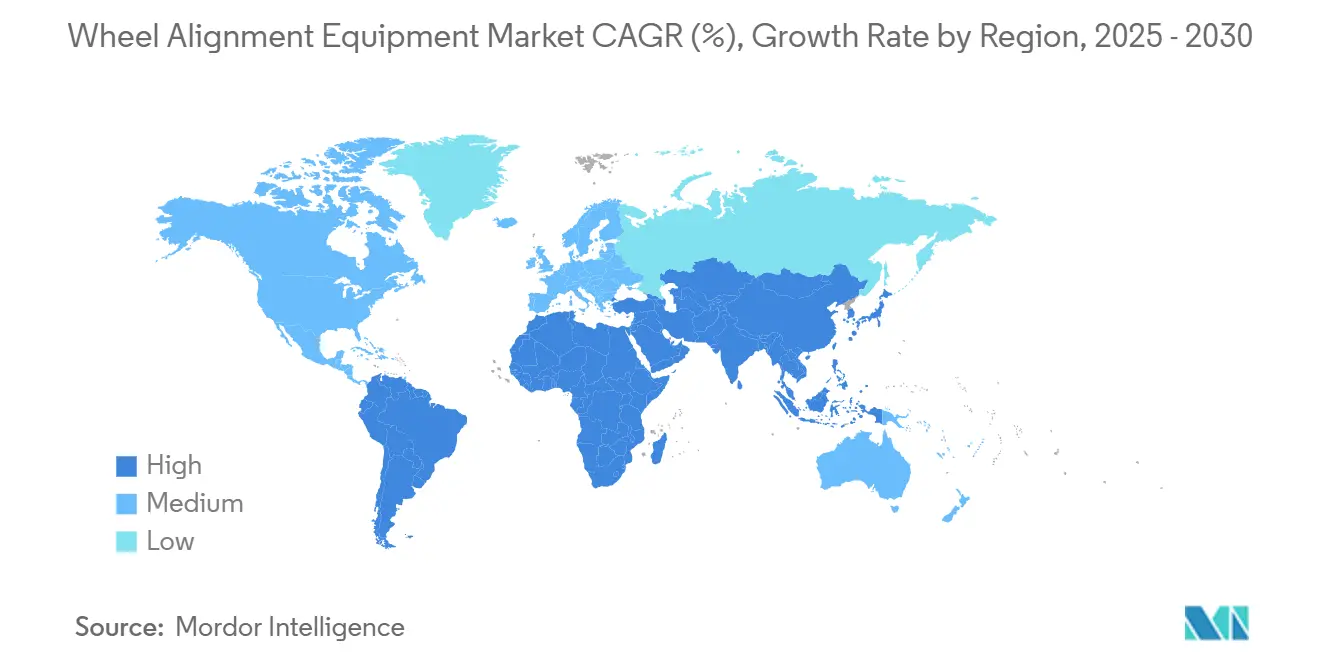

- By geography, Asia-Pacific commanded a 42.58% share in 2024 and is forecast to expand at a 7.12% CAGR to 2030.

Global Wheel Alignment Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising New-Vehicle Parc in APAC Sustaining Workshop Investments | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Stricter Periodic-Inspection Laws Mandating Wheel-Alignment Checks | +0.9% | Global, early gains in Europe, North America | Short term (≤ 2 years) |

| Shift from CCD to 3D Vision Systems Improves Throughput and ROI | +0.8% | Global | Medium term (2-4 years) |

| Surge of Mobile Tire-Service Vans Driving Demand for Portable Aligners | +0.6% | North America and the EU, expanding to APAC | Short term (≤ 2 years) |

| Automaker Right-to-Repair Data Sharing Boosts Independent Garages | +0.5% | North America and the EU | Medium term (2-4 years) |

| Subscription-Based SaaS Pricing Lowering Acquisition Barriers | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising New-Vehicle Parc in APAC Sustaining Workshop Investments

Asia-Pacific’s vehicle population continues to climb, prompting independent and chain workshops to add bays, modernize facilities, and schedule equipment replacement cycles earlier than planned. Growing urban incomes in China, India, and Southeast Asia spur higher vehicle utilization, driving consistent alignment demand tied to tire, steering, and suspension upkeep. Insurance penetration offers a parallel indicator of aftermarket depth, non-life premiums across the region, reflecting a broad service ecosystem that keeps demand insulated from short-term macro volatility. Multi-year capital planning by large workshop groups further steadies equipment orders, giving suppliers visibility into production volumes. Because imported EVs carry warranty clauses that specify certified alignment results, distributors report escalating inquiries for high-precision systems compatible with ADAS calibration.

Stricter Periodic-Inspection Laws Mandating Wheel-Alignment Checks

State-level and federal safety regulations tighten wheel-assembly scrutiny, making alignment verification a compulsory element of annual or biannual inspections. California’s Vehicle Safety Systems Inspection Program, launched in March 2024, explicitly adds alignment criteria to an expanded safety checklist. U.S. federal standard 49 CFR 570 likewise codifies alignment measurement tolerances to curb crash risk linked to steering failure[1]“49 CFR 570 Vehicle In-Use Inspection Standards,” National Highway Traffic Safety Administration, nhtsa.gov. European Union member states already require alignment evidence during road-worthiness tests, pushing garages to upgrade outdated CCD rigs in favor of faster, print-ready 3D platforms that satisfy auditors. Compliance-driven throughput raises average workshop utilization and cushions revenue when consumer discretionary repairs soften. ADAS-equipped models further upscale compliance complexity, as steering-angle reset and radar calibration must coincide with alignment, prompting integrated service workflows.

Shift from CCD to 3D Vision Systems Improves Throughput and ROI

Workshops tracking billable hours find that 3D systems slash setup time, curb comebacks, and increase ticket value by packaging alignment with other diagnostics. Hunter’s HawkEye Elite logs a full four-wheel measurement in 70 seconds, turning bays an extra two to three times daily in high-volume centers [2]“HawkEye Elite Productivity Metrics,” Hunter Engineering Co., hunter.com. The uptick in labor productivity offsets the 10%–20% price premium over CCD and appeals to chains struggling to recruit qualified technicians. Because 3D systems also satisfy OEM alignment specifications for ADAS recalibration, they protect dealership service departments from warranty claim disputes. An equipment ROI threshold of roughly 15 alignments per week has emerged, guiding purchase decisions and allowing suppliers to segment marketing by workshop size.

Surge of Mobile Tire-Service Vans Driving Demand for Portable Aligners

Consumer convenience trends and fleet uptime imperatives nurture a growing fleet of mobile tire vans that now offer on-site alignment. Launch Tech’s wireless X-613 aligner, designed around magnet-mounted targets, eliminates fixed-rack requirements and runs from a compact battery module [3]“X-613 Mobile Aligner Specifications,” Launch Tech USA, launchtechusa.com. Operators targeting large logistics depots cite the ability to align six-wheel light commercial trucks curbside, avoiding lost revenue from out-of-service vehicles. Real-estate constraints in dense metro areas reinforce the model, as mobile operations bypass the need for costly workshop leases. Premium pricing for portable aligners reflects robust housings, quick-release clamps, and ruggedized tablets, allowing manufacturers to preserve margins despite lower volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front Capex Remains Prohibitive for Small Workshops | -0.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Skilled-Technician Shortage Limits Equipment Utilization | -0.6% | North America and the EU | Medium term (2-4 years) |

| ADAS-Calibration Complexity Delaying Alignment Cycle-Times | -0.4% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Proliferation of Refurbished Equipment Suppresses New-Unit Demand | -0.3% | Global, prominent in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front Capex Remains Prohibitive for Small Workshops

Independent garages operating on thin margins often defer equipment replacement until outright failure because a new 3D system surpasses USD 25,000. Financing hurdles are acute in emerging economies where credit histories are limited and interest rates remain high. The divide widens competitive disparity; well-capitalized chains accumulate alignment volume and cross-sell services while neighborhood shops lose high-ticket repairs. Subscription models alleviate pressure yet remain unfamiliar to owners accustomed to outright purchase, slowing conversion.

Skilled-Technician Shortage Limits Equipment Utilization

Even when equipment is installed, many shops struggle to assign certified staff, leading to idle racks during peak demand. Advanced systems require calibration, know-how, ADAS alignment skills, and familiarity with evolving software interfaces. Wage inflation outpaces shop labor rates in tight markets, compressing margins and undermining ROI assumptions for high-end aligners. Consolidation accelerates as multi-location groups lure technicians with structured training and career paths, widening the capability gap versus single-site operators. Without human capital, hardware upgrades cannot translate into throughput gains or customer satisfaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: 3D Vision Systems Anchor the Technology Shift

3D aligners controlled 48.31% of 2024 revenue, underscoring their maturity as the workshop standard for accuracy and rapid measurement. This segment is slated to grow at a 5.88% CAGR, keeping the wheel alignment equipment market ahead of baseline automotive service expansion. CCD systems hold ground in cost-sensitive shops but face declining orders as OEM warranty protocols increasingly favor 3D documentation. Laser aligners stay relevant in motorsport and specialty applications where sub-millimeter precision matters. Infrared variants cater to niches such as off-road vehicle fleets operating in dusty environments where camera lenses may foul.

Growth drivers for 3D systems include bundled ADAS calibration modules, cloud reporting, and integrated ride-height sensing that eliminate the need for mechanical turnplates. Vendors offer trade-in credits for aging CCD racks, shortening payback and swelling upgrade pipelines. Laser and infrared systems command premium price points, so unit sales remain limited; however, their performance reputation protects margins. CCD installations are prominent in emerging markets, providing an initial foothold that vendors later convert to 3D through phased financing plans.

By Application: Commercial Vehicles Accelerate Despite Car Dominance

Passenger cars remain the revenue cornerstone at 60.14% in 2024, yet light commercial vehicles chart the fastest 6.56% CAGR thanks to rising last-mile delivery mileage and tire cost sensitivity. Fleet managers calculate clear ROI from alignment, given tire wear’s contribution to operating cost per mile, leading to dedicated service bays or in-house portable aligners. Medium and heavy trucks add complexity and require extended runways, spurring demand for heavy-duty racks and camera towers. Two-wheeler alignment emerges slowly, mainly in Southeast Asia, but specialized jigs and compact laser kits keep costs modest.

The wheel alignment equipment market size tied to commercial vehicles expands as electrified vans join fleets; optimal toe and camber become critical to range and cargo efficiency. Data analytics from connected aligners provide fleet dashboards that benchmark wear, steering angles, and energy consumption. In the passenger segment, C-segment SUVs and crossovers with larger wheel diameters lift alignment ticket values, helping shops raise blended revenue. Heavy truck alignment demands consolidate at highway service hubs where multi-axle calibration is bundled with mandatory safety inspections, smoothing seasonal volume swings.

By Level of Automation: Manual Systems Persist, Automation Gains Traction

Manual rigs dominated with a 54.25% share in 2024, illustrating the enduring appeal of low entry cost and direct technician control. Yet automatic systems’ 7.45% CAGR reflects a strategic pivot by large chains that face chronic labor shortages and require standardization across sites. Semi-automatic options blend camera automation with manual target placement, appealing to operators seeking incremental upgrades.

Automated platforms integrate robotic camera booms, self-centering clamps, and guided workflow prompts, reducing skill thresholds and quickening bay turnover. Cloud-linked automatic aligners underpin fleet maintenance contracts that demand standardized reports and KPI dashboards. Manual rigs retain relevance in rural markets, hobbyist garages, and specialty restoration shops where labor costs are low and mechanical involvement is preferred. Nonetheless, vendor roadmaps show declining R&D for purely manual products, signaling eventual migration toward at least semi-automatic capability.

By Features: Wireless Connectivity Leads Functional Innovation

Target-and-camera systems captured 40.17% revenue in 2024, but wireless connectivity features are projected to grow at a 7.82% CAGR, as workshops digitize workflows. Wi-Fi and Bluetooth modules channel alignment data to shop management systems, automating customer reports and parts ordering. Measurement software migrates to cloud back ends, enabling remote diagnostics, database updates, and AI-driven anomaly detection. Connected aligners support over-the-air calibrations, slashing downtime and technician travel.

Vehicle databases grow with each model year, stretching onboard storage limits and making cloud libraries indispensable. Suppliers now monetize subscription access to OEM specs, generating recurring income. Rapid target recognition, auto-VIN capture, and live specification updates push connected aligners to the top of procurement lists. As EV architectures proliferate, real-time database refreshes safeguard accuracy, ensuring service compliance with battery weight distributions and new suspension geometries.

By End-User: Fleet Management Companies Rapidly Expand Share

Automotive repair shops claimed 45.66% revenue in 2024, yet fleet management companies drive a 6.94% CAGR as they internalize maintenance to tame the total cost of ownership. National rental, leasing, and logistics operators standardize on brand-agnostic aligners capable of handling mixed vehicle classes. Tire dealerships diversify into alignment to defend margins against online tire retailers. At the same time, OEM service centers invest in keeping warranty customers in the network through bundled alignment and ADAS calibration offers.

Fleet operators leverage utilization data from connected aligners to optimize dispatch and schedule tire rotations. Subscription hardware suits fleet depots where cash-flow predictability is paramount. Independent garages ride right-to-repair momentum, equipping bays with multi-brand ADAS alignment options that rival dealer capabilities. Market penetration among municipal fleets and public transit authorities remains early-stage, though zero-emission mandates may accelerate adoption.

Geography Analysis

Asia-Pacific heads the wheel alignment equipment market with 42.58% share in 2024, and is anticipated to grow at 7.12% CAGR by 2030, driven by urbanization, infrastructure expansion, and an enlarging middle class. Workshop density in China’s eastern provinces and India’s tier-two cities rises each quarter, lengthening order books for mid-range 3D systems. Government incentives for domestic EV production reinforce demand for alignment racks compatible with lightweight suspension geometries. Because replacement cycles average five years, suppliers benefit from predictable refresh business as early 3D installs approach the end of life.

North America shows slower unit growth but steady value gains thanks to ADAS-ready upgrades and software subscriptions. U.S. right-to-repair debates center on technician access to OEM calibration files, and passage of supportive legislation in several states boosts independent service viability. Canadian buyers emphasize bilingual UI options and metric tolerance settings, nudging vendors to localize software. Mobile alignment fleets targeting last-mile delivery trucks proliferate across coastal metros where commercial real estate is scarce.

Europe balances stringent inspection laws and sustainability drives. Mandatory road-worthiness checks push garages to own calibrated alignment rigs certified under local standards, sustaining replacement demand even as vehicle sales plateau. Germany anchors technological innovation, with TÜV certification requirements steering workshops toward premium vendors. Scandinavian markets, keen on electrified vehicle performance, adopt connected aligners that integrate with national service data hubs. Middle East and Africa remain nascent; yet large Gulf logistics fleets and South African aftermarket franchisers demonstrate rising interest, provided financing solutions spread cost.

Competitive Landscape

Market concentration is moderate, with Hunter Engineering, Snap-on, and Bosch collectively controlling a significant revenue block through integrated diagnostic ecosystems, global distribution, and intensive R&D. Hunter’s HawkEye platforms pair with HunterNet analytics, giving workshops actionable KPIs that reinforce brand loyalty. Snap-on’s Tru-Point integrates ADAS calibration workflows, bundling vehicle-specific targets with alignment hardware. Bosch leverages its broader diagnostic suite, meshing alignment with its ESI[tronic] Evolution software for a full-vehicle approach.

Mid-tier European specialists—including HAWEKA and CEMB—focus on precision niches, boasting OEM homologations that appeal to premium dealerships. HAWEKA’s AXIS4000MB secured Mercedes-Benz endorsement, lending credibility that commands pricing power. Asian entrants, notably from China and South Korea, compete on cost, offering feature-rich packages at 10%–15% discounts, pressuring incumbents in price-sensitive tranches of the wheel alignment equipment market.

Strategic moves in 2024-2025 trend toward SaaS bundling, AI-based error detection, and remote service contracts. Partnerships with fleet telematics providers create recurring software revenue, while acquisitions target software firms capable of expanding data analytics capability. Vendors also invest in training academies to mitigate technician shortages, creating ecosystems that encompass hardware, software, and human capital solutions.

Wheel Alignment Equipment Industry Leaders

Hunter Engineering Co.

Snap-on Inc. (John Bean / Hofmann)

Bosch Automotive Service Solutions

Ravaglioli S.p.A. (VSG)

Manatec Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Madhus Garage Equipment introduced the Hunter HawkEye XL across India, broadening access to the manufacturer’s most advanced alignment platform.

- May 2025: Supertracker unveiled the STR420 T at the Commercial Vehicle Show, marketing a straightforward wheel aligner solution for heavy-duty fleets.

- December 2024: Launch Tech USA rolled out the X-613 Mobile Aligner, a wireless system covering 50,000+ vehicle models with minimal setup.

- September 2024: SmartSafe launched the WA613 Wireless 3D Wheel Aligner, marrying precision and ease in a cable-free configuration.

Global Wheel Alignment Equipment Market Report Scope

| 3-D Wheel Aligners |

| CCD Wheel Aligners |

| Laser Wheel Aligners |

| Infrared Wheel Aligners |

| In-Ground Wheel Aligners |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two-Wheelers |

| Manual |

| Semi-Automatic |

| Automatic |

| Target and Camera System |

| Measurement System |

| Software and Computer System |

| Vehicle Database |

| Wireless Connectivity |

| Automotive Repair Shops |

| Tire Dealers |

| OEM Service Centers |

| Fleet Management Companies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Type | 3-D Wheel Aligners | |

| CCD Wheel Aligners | ||

| Laser Wheel Aligners | ||

| Infrared Wheel Aligners | ||

| In-Ground Wheel Aligners | ||

| By Application | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| By Level of Automation | Manual | |

| Semi-Automatic | ||

| Automatic | ||

| By Features | Target and Camera System | |

| Measurement System | ||

| Software and Computer System | ||

| Vehicle Database | ||

| Wireless Connectivity | ||

| By End-User | Automotive Repair Shops | |

| Tire Dealers | ||

| OEM Service Centers | ||

| Fleet Management Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the wheel alignment equipment market in 2025?

The wheel alignment equipment market size is valued at USD 4.71 billion in 2025.

What CAGR is expected for wheel alignment systems through 2030?

The market is forecast to grow at a 5.34% CAGR between 2025 and 2030.

Which region leads global demand for wheel alignment equipment?

Asia-Pacific commands the largest share at 42.58% in 2024 and is also the fastest-growing region.

Why are 3D vision aligners gaining popularity over CCD systems?

3D platforms deliver 70-second measurements, integrate ADAS calibration, and improve technician productivity, driving faster ROI.

Page last updated on: