Automotive Garage Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 8.73 Billion |

| Market Size (2031) | USD 11.25 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

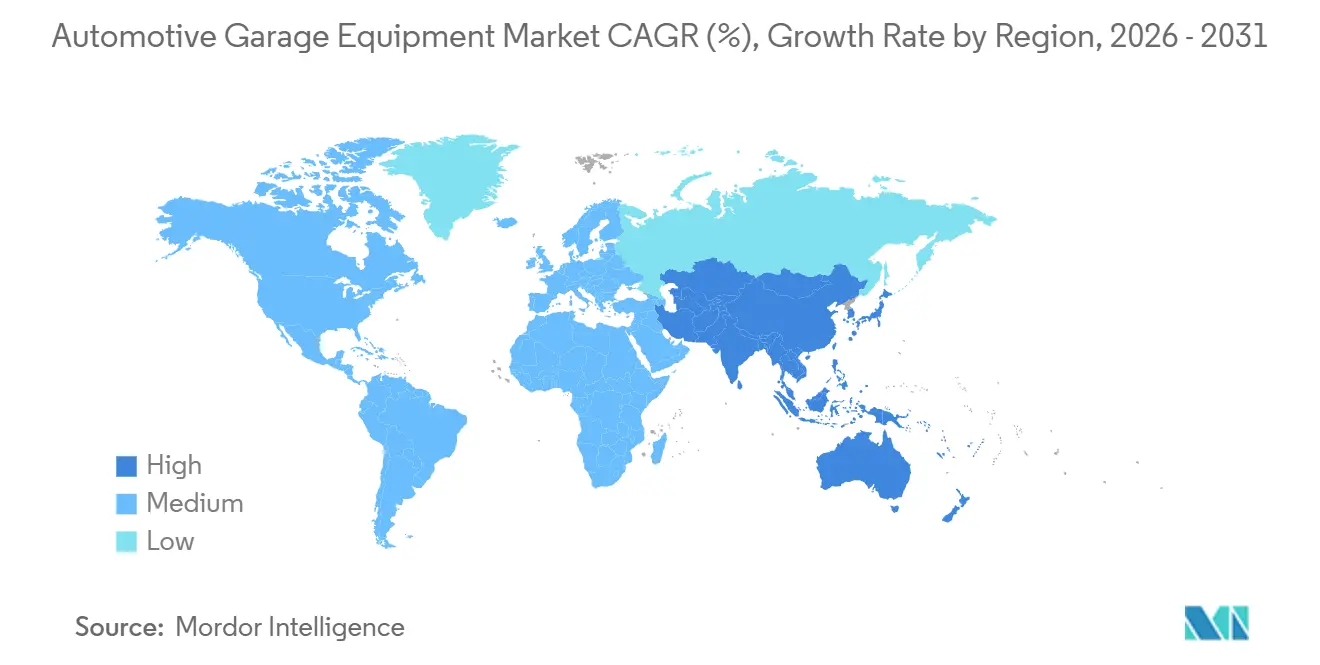

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

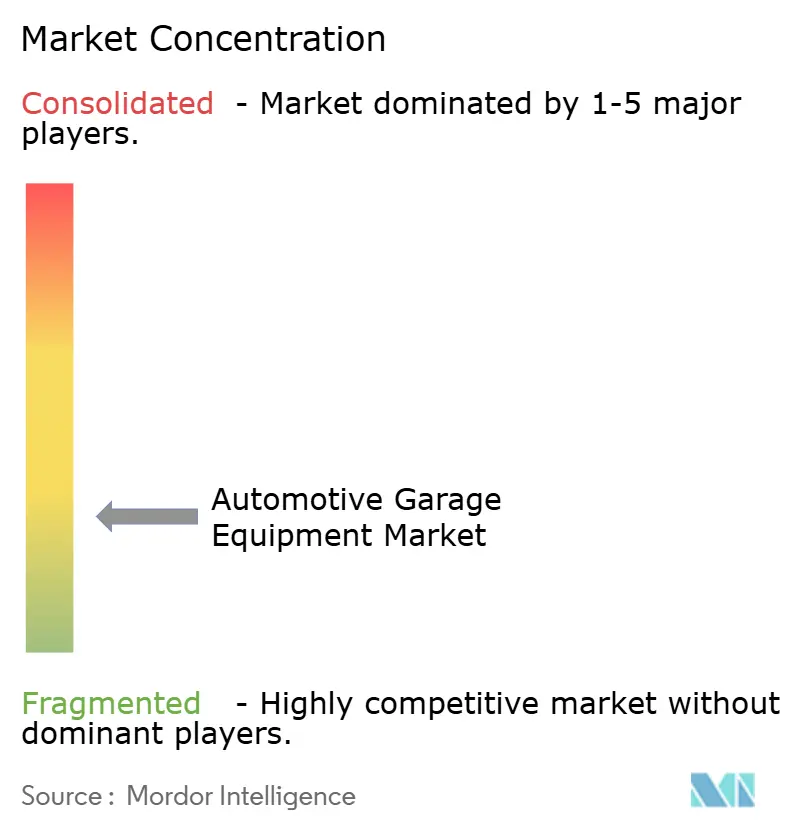

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Garage Equipment Market Analysis by Mordor Intelligence

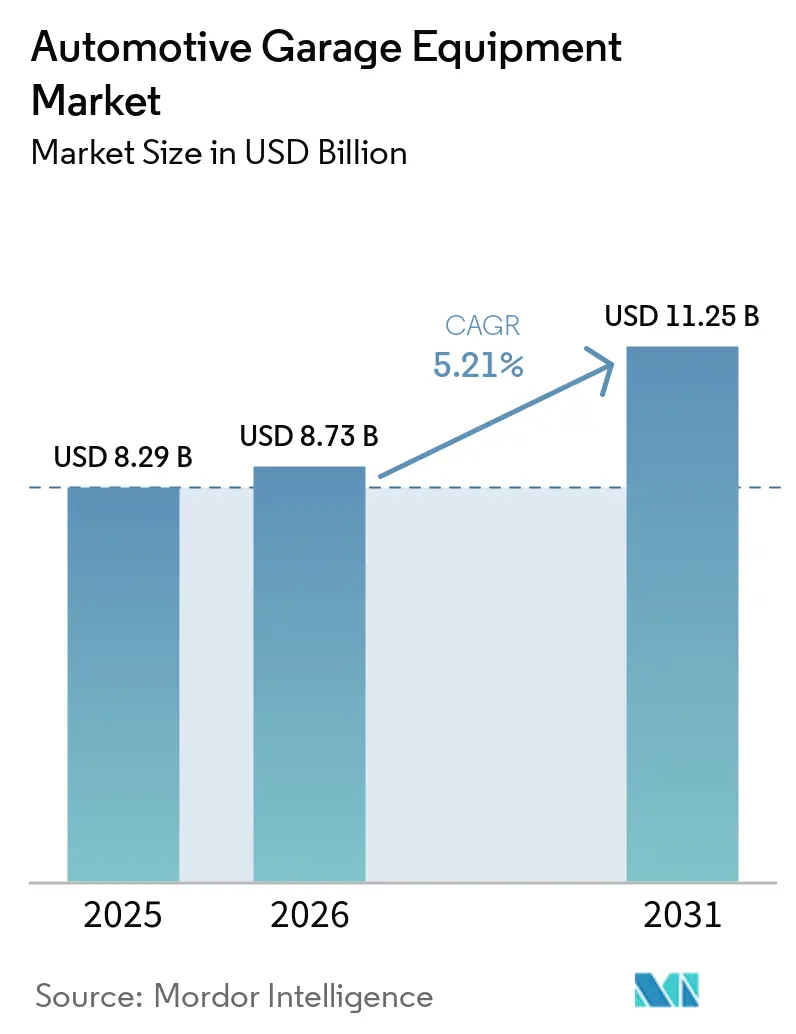

The Automotive Garage Equipment Market size is projected to be USD 8.29 billion in 2025, USD 8.73 billion in 2026, and reach USD 11.25 billion by 2031, growing at a CAGR of 5.21% from 2026 to 2031. Growing vehicle complexity, tightening emission rules, and a swing toward subscription-based ownership are reshaping workshop spending patterns. Lifting systems still absorb the largest share of capital outlays, yet cloud-connected emission analyzers and ADAS calibration rigs are expanding fastest as regulation drives mandatory upgrades. Independent garages are consolidating under franchise banners and private-equity platforms, unlocking scale benefits and heightening demand for standardized tool packages that lower training hurdles. Meanwhile, subscription procurement models are eroding the dominance of outright purchase, as operators seek shorter refresh cycles to keep pace with evolving vehicle technology. Vendors that couple equipment, software, and technician training into turnkey bundles are gaining negotiating leverage with chains that view reliable uptime as the prime differentiator in a tightening labor market.

Key Report Takeaways

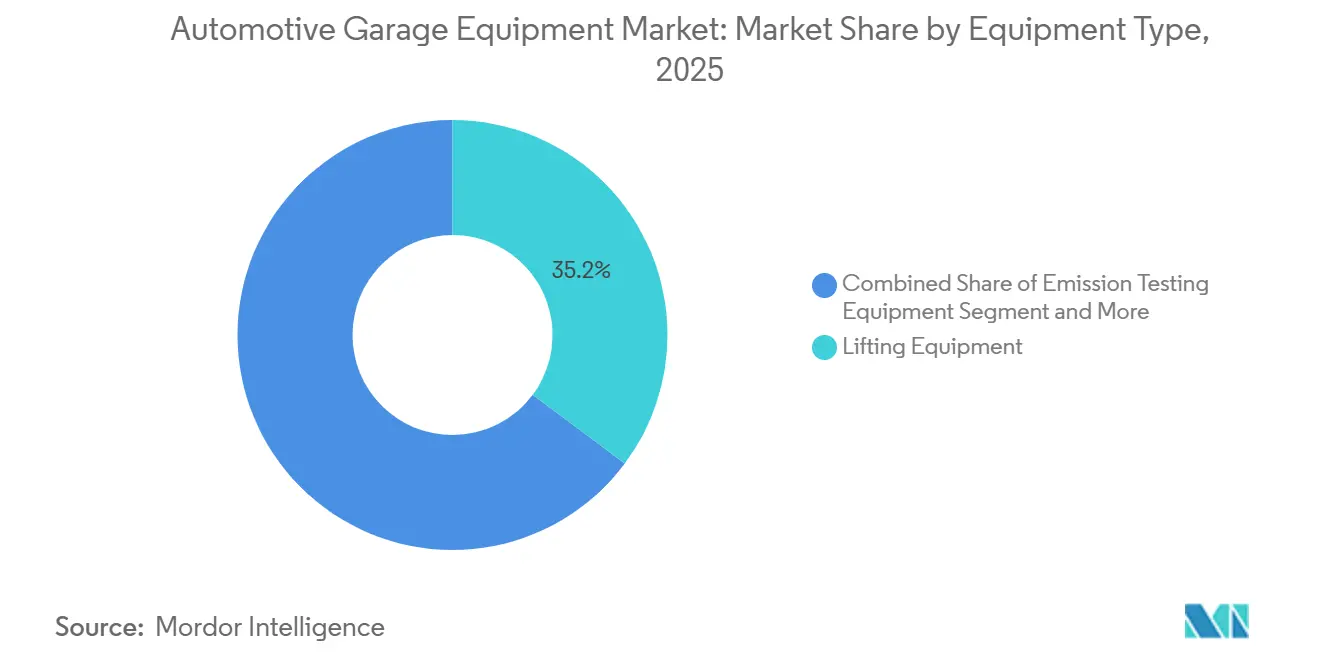

- By equipment type, lifting systems led with 35.17% of the automotive garage equipment market share in 2025; emission testing platforms are projected to post the fastest 5.23% CAGR through 2031, highlighting strong growth scope in the automotive garage equipment market.

- By vehicle type, passenger-car workshops accounted for 63.37% of 2025 revenue and are also advancing at a 5.31% CAGR through 2031.

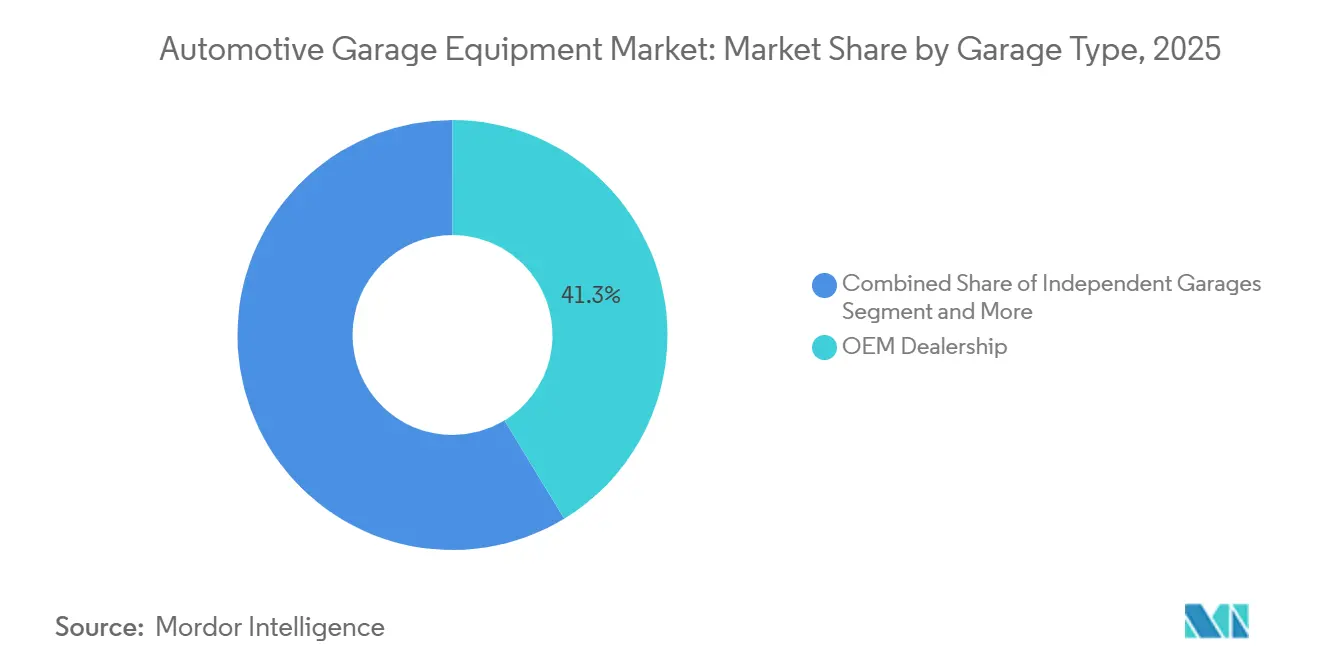

- By garage type, OEM dealerships retained 41.32% of 2025 turnover, yet independent facilities recorded the highest 5.37% CAGR forecast to 2031.

- By ownership model, outright purchases still represented 73.26% of 2025 orders, but subscription contracts are rising at a 5.27% clip across 2026-2031, indicating emerging growth potential in the automotive garage equipment market.

- By geography, Europe accounted for 34.46% of 2025 revenue, while Asia-Pacific is projected to post the fastest CAGR of 5.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Garage Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Emission Regulations | +1.2% | Europe and North America core, spillover to China and India | Medium term (2-4 years) |

| Expansion of Independent Aftermarket Service Centres | +1.0% | Asia-Pacific core, secondary gains in Latin America and Middle East | Medium term (2-4 years) |

| Rising Passenger-Car Parc | +0.9% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Ageing Vehicle Fleet in OECD Economies | +0.8% | North America and Europe, with selective impact in Japan and South Korea | Long term (≥ 4 years) |

| EV-Specific High-Voltage Workshop Tools Demand | +0.7% | Global, led by Europe and China, accelerating in North America | Medium term (2-4 years) |

| Equipment-As-A-Service Subscription Models | +0.6% | North America and Europe early adopters, gradual diffusion to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Emission Regulations

Euro 7 rules coming in 2027 obligate workshops to measure real-world emissions, which is expected to drive new sales of portable analyzers and OBD-II scanners across 27 EU states [1]“Proposal for Euro 7 Regulation,” European Commission, eur-lex.europa.eu . The U.S. EPA’s Tier 4 heavy-duty mandate, finalized in 2024, requires commercial-vehicle bays to install NOx and PM sensors at a higher cost [2]“Heavy-Duty Vehicle Emission Standards Final Rule,” Environmental Protection Agency, epa.gov . China’s National VI(b) curb on evaporative losses has already lifted orders for vapor-leak detectors, while India’s forthcoming Bharat Stage VII scheme could grow the national testing park by 30%. Each tightening cycle turns equipment into consumables, creating repeat-purchase revenue tied to recalibration and firmware rights, strengthening long-term demand in the automotive garage equipment market.

Expansion of Independent Aftermarket Service Centres

In 2025, independents captured a significant share of the global service income, driven by a consumer shift towards price clarity and proximity. Rollups, supported by substantial private-equity inflows, successfully negotiated fleet-pricing deals with tool vendors. In a strategic move, franchise groups like Midas transitioned a considerable portion of their outlets to a subscription-based procurement model, leveraging Bosch contract data to significantly reduce upfront capital needs. Meanwhile, in India, GoMechanic and other players notably expanded their operations, standardizing lifts and scan tools across networks to enhance technician training. As consolidation progresses, demand increasingly favors suppliers offering bundled services like remote diagnostics and utilization analytics, reinforcing growth in the automotive garage equipment market.

Rising Passenger-Car Parc

In the mid-term, the Asia-Pacific region accounted for the majority of global vehicle additions, pushing the total installed base to a significant milestone. While sales momentum is strong in India and Indonesia, service penetration hasn't kept pace. As a result, organized chains in these countries are enhancing their diagnostic capabilities to tap into this untapped potential. In the U.S., vehicles have aged considerably, leading to extended maintenance cycles that necessitate specialized testing equipment [3]“Average Age of Automobiles in the United States,” Bureau of Transportation Statistics, bts.dot.gov . China's vehicle population grew significantly during this period, driving up demand for modular diagnostic scanners, especially among cash-conscious independent operators. With longer vehicle ownership cycles, there's an increased emphasis on periodic emission checks to maintain resale value, ensuring a consistent demand for compliant analyzers. Suppliers that provide multi-brand compatibility and over-the-air software updates are poised to dominate procurement decisions, as these features significantly reduce hardware redundancy and strengthen long-term growth in the automotive garage equipment market.

EV-Specific High-Voltage Workshop Tools Demand

In the near future, battery-electric deliveries are expected to reach significant volumes. However, a small proportion of independent operators currently possess the insulated tools and heavy pack lifts required to meet Tesla's certification standards. Recently introduced safety guidelines, EN 50110-1, emphasize the need for insulated flooring and arc-flash breakers, which add substantial costs per lane in Europe. Autel has achieved notable success by rapidly selling a considerable number of MaxiSYS Ultra units, driven by the integration of battery-diagnostic and thermal-imaging functions. Workshops now face a critical decision: either invest in upskilling for electric vehicles (EVs) or risk losing that revenue to original equipment manufacturer (OEM) channels. This shift is creating a clear division in the aftermarket, separating EV-ready services from those focused solely on internal combustion engine (ICE) vehicles, further shaping demand in the automotive garage equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex of Advanced Equipment | -0.7% | Global, with acute impact in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Shortage of Trained Diagnostic Technicians | -0.5% | North America and Europe core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Proliferation of Counterfeit Garage Tools | -0.4% | Global, with primary source in Asia-Pacific, distribution via online channels | Medium term (2-4 years) |

| Downtime Due to Equipment Failure | -0.3% | Global, with higher incidence in Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex of Advanced Equipment

Many emerging-market garages find themselves overshooting their annual equipment budgets, as ADAS calibration bays are significantly expensive. A recent survey conducted by a European federation found that a substantial proportion of respondents identified pricing as the primary obstacle to adopting EV tools. Multi-brand garages often inflate their inventory by purchasing separate scanners to access proprietary OEM codes. While Equipment-as-a-Service offers a way to spread cash flows, it can consume a notable share of gross revenue, introducing fixed charges that become burdensome during periods of reduced demand. The Asia-Pacific region grapples with a pronounced challenge: as vehicle numbers surge, the pace of workshop capital formation lags, resulting in stretched bay utilization and longer customer wait times, highlighting structural constraints in the automotive garage equipment market.

Shortage of Trained Diagnostic Technicians

Over the next several years, the U.S. will face significant annual demand for mechanics, but it is already experiencing a substantial shortfall. German workshops have been struggling for extended periods to fill diagnostic positions, which has negatively impacted their operational efficiency. As vehicles increasingly rely on software, the skill gap among technicians continues to grow, requiring them to develop expertise in advanced data streams and cybersecurity updates. Although scan-tool vendors are integrating AI-driven guides, the high subscription costs are limiting their adoption across the industry. Consequently, operators are prioritizing tools that streamline fault detection and reduce training time, giving an advantage to brands that combine hardware with flexible e-learning solutions, further supporting innovation in the automotive garage equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Emission Testing Leads Regulatory Upgrade Cycle

Emission analyzers and smoke meters are the fastest-growing line, rising at a 5.23% clip through 2031, outpacing the broader automotive garage equipment market, even though lifting systems accounted for a 35.17% revenue share in 2025. Real-time compliance reporting pilots in California and the EU force garages to install cloud-enabled testers that upload data directly to regulators, turning a periodic obligation into a continuous service call. Vendors see pull-through sales of calibration gases and software licenses that are renewed every 12 months. Lifting gear remains the essential workshop backbone because each repair still starts with vehicle elevation, yet its growth now trails test equipment as safety standards plateau. Suppliers that integrate lift platforms with wheel-alignment cameras are eking out differentiation by saving bay floor space.

Wheel and tire machines account for nearly a fifth of current turnover and benefit from mandatory TPMS checks at every tire change in the United States. The automotive garage equipment market share for diagnostic handhelds is set to climb as ECUs in modern cars top 150 units, making fault isolation impossible without multi-protocol coverage. Body-shop gear lags behind ADAS, which has reduced collision frequency; however, paint booths with energy-efficient airflow are gaining ground in regions where utility costs soar. Smaller categories such as fluid dispensers and compressors still move steady volumes through bundle sales that ride on larger lift or analyzer contracts.

By Vehicle Type: Passenger Cars Sustain Dominance Amid ADAS Complexity

Passenger-car bays absorbed 63.37% of industry revenue in 2025, and that slice inches higher as camera and radar recalibrations become routine after windshield or bumper service. OEM work instructions now mandate post-repair alignment on every sensor, pushing specialized target boards and laser tools into even small independents. Consequently, the passenger-car slice within the automotive garage equipment market size grows alongside a 5.31% segment CAGR. Software content already crosses 150 million lines in luxury cars, swelling demand for firmware-flash stations and secure gateway access kits.

Commercial-vehicle operators invest in heavier lifts and battery-pack cradles as California and EU zero-emission mandates accelerate fleet electrification. Automated lanes that process a dozen trucks each shift illustrate the labor-saving theme as technician scarcity bites. Two-wheeler workshops remain the least tool segment; sub-USD 500 devices that decode domestic OEM protocols, presenting a volume opportunity that could lift two-wheeler contributions to the automotive garage equipment market share over the next decade.

By Garage Type: Independent Facilities Gain Share Through Consolidation

OEM dealerships captured 41.32% of 2025 turnover due to factory subsidies, but independents logged the fastest 5.37% growth. European legislative proposals that guarantee equal data access threaten to erode the dealership service moat, directing more complex jobs to multi-brand workshops. Chain franchisors now specify identical tool suites to harmonize SOPs and training across hundreds of sites, giving bulk-order leverage that trims unit costs and expands the addressable market for automotive garage equipment by mid-tier vendors.

Franchise networks pivot to subscription procurement where suppliers keep title to lifts and scanners while billing per-use fees, strengthening adoption across the automotive garage equipment market. This option resonates in markets with volatile demand cycles because it shifts cost from the balance sheet to the income statement. Independents also harvest telematics data from insurers to pre-schedule maintenance, raising bay utilization. OEM dealerships respond by adding valet and mobile service vans, a tactic that increases demand for portable lifts and battery jump packs.

By Ownership Model: Subscription Models Disrupt Traditional Capex

Outright equipment purchase still governs 73.26% of 2025 orders because established garages favor depreciation. Yet subscription contracts grow 5.27% annually, reflecting operators’ desire to align tool refresh with tech obsolescence. Bosch’s Automotive Service Solutions platform recruited multiple garages by end-2025. The automotive garage equipment market share captured by subscriptions, therefore, climbs steadily, even though early-exit penalties temper some enthusiasm.

Leasing remains prevalent among commercial-vehicle fleets that need additional capacity during seasonal peaks, supporting flexible adoption across the automotive garage equipment market.Vendors sweeten subscriptions with uptime SLAs and predictive maintenance powered by IoT sensors in lifts and analyzers, cutting unplanned downtime to an average of below 2 hours per month. However, locked-in three-year terms can hinder operators in downturns, nudging some to hybrid models that mix owned core assets with rented specialty rigs.

Geography Analysis

Europe accounted for 34.46% of 2025 revenue, as dense vehicle fleets and annual testing schemes drive steady equipment turnover. German workshops made substantial investments in new analyzers and scanners, ensuring compliance with the latest emission standards and preparing for upcoming regulations. The UK's MOT regime's demand for new brake testers last year led the Driver and Vehicle Standards Agency to accredit more suppliers. Meanwhile, independent workshops in France and Italy benefited from state subsidies, which reimbursed them for EV-tool purchases, helping them navigate broader economic challenges. However, with high bay density in Western Europe, the region faces limitations in expanding capacity, capping the long-term growth potential of its automotive garage equipment market.

Asia-Pacific is the fastest climber at 5.33% through 2031, anchored by China’s equipment take in 2025. Provincial inspection mandates for older vehicles drove significant sales of analyzers and diagnostic units last year. In India, multi-brand chains inaugurated new locations, making notable investments in lifts, balancers, and scanners, marking a significant shift away from the informal sector. To counter dwindling owner demographics, Japan and South Korea are channeling investments into EV service lanes, ensuring their dealerships remain relevant. Southeast Asia, notably under-equipped, sees countries like Indonesia and Vietnam with a limited number of organized bays, despite a combined vehicle parc exceeding tens of millions, highlighting a significant opportunity for the automotive garage equipment market.

North America contributed a substantial portion to 2025 sales, driven by an aging vehicle fleet and a trend of consolidation among franchise chains. In the U.S., chains are standardizing tool sets across their stores, leading to bulk purchases of alignment systems and cloud-licensed diagnostics. Provincial inspection mandates in Canada bolster the demand for analyzers, while new workshops in British Columbia are opting for premium earthquake-rated lifts. Together, South America and the Middle East & Africa account for a smaller but notable share of the global revenue. Brazil's biennial emission checks ensure consistent demand, while Argentina's recent tariff relief on scanners might trigger a surge in purchases once currency fluctuations stabilize. In the Gulf states, legislation mandates annual inspections for older vehicles, driving brisk imports of brake and suspension testers, reinforcing steady demand in the automotive garage equipment market.

Competitive Landscape

In recent years, five multinational leaders—Bosch, Continental, Snap-on, Hunter Engineering, and Vehicle Service Group—have commanded a significant share of the global revenue. These industry giants bundle software subscriptions, training, and calibration services, embedding themselves deeper into customer workflows. Meanwhile, mid-tier specialists like MAHA, Istobal, and Launch Tech clinch regional tenders by offering competitive pricing and local service crews, maintaining a moderate concentration in the automotive garage equipment market.

Key innovation themes spotlight remote diagnostics and robotic tire changers. Over the past few years, Bosch has secured multiple patents for cloud fault prediction and OTA calibration, while Snap-on has focused on augmented-reality repair guidance. Autel has disrupted the North American market by pricing its ADAS rigs significantly below competitors' and capturing a notable market share within a short period. Despite the advancements, counterfeit adapters pose a significant threat, with the EUIPO estimating substantial losses in recent years. Vendors that achieve ISO 9001 certification and collaborate with entities like the Automotive Service Association bolster their pricing power and gain access to regulated inspection tenders.

Robotic tire systems emerge as a solution to labor shortages. Recently, RoboTire's installations at several Discount Tire stores have significantly reduced wheel-change time, allowing technicians to focus on diagnostics. Industry players that streamline routine tasks without added complexity resonate with garages facing technician shortages. Furthermore, suppliers are embedding IoT sensors into lifts and analyzers, enabling them to preemptively schedule service calls before breakdowns. This capability is deemed mission-critical by chains aiming to maintain high bay uptime.

Automotive Garage Equipment Industry Leaders

Robert Bosch GmbH

Continental AG

Snap-on Incorporated

Hunter Engineering Company

Vehicle Service Group (Dover)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: QuickJack, a division of BendPak Inc., unveiled a range of upgrades to its portable car lift lineup, introducing brand-new models. The newly launched QuickJack 6000TL and 6000TLX models boast a capacity of 6,000 lbs, whereas the 8000TL and 8000TLX models can support weights of up to 8,000 lbs.

- April 2025: Robert Bosch GmbH, a player in technology and services, inked a master license deal for Bosch Car Service in Indonesia. The signing was with X-Motors, a service provider known for accelerating globalization for top automakers. This agreement signifies a deeper collaboration between X-Motors and Bosch Car Service in the automotive aftermarket services.

- April 2025: In a move to bolster its presence, Bosch Auto Service has rolled out franchise operations across the United States, committing to provide partners with branded equipment, comprehensive training, and robust marketing support, as highlighted on bosch.com.

Global Automotive Garage Equipment Market Report Scope

The scope of the report includes Equipment Type (Lifting and More), Vehicle Type (Passenger Cars and More), Garage Type (OEM and More), Ownership Model (Purchase and More), and Geography.

| Lifting Equipment |

| Emission Testing Equipment |

| Body-Shop Equipment |

| Wheel & Tire Service Equipment |

| Vehicle Diagnostic & Testing Equipment |

| Washing & Cleaning Equipment |

| Other Niche Garage Tools |

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| OEM Dealership Garages |

| Independent Garages |

| Franchise / Chain Workshops |

| Outright Purchase |

| Lease / Rental |

| Subscription (Equipment-as-a-Service) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Equipment Type | Lifting Equipment | |

| Emission Testing Equipment | ||

| Body-Shop Equipment | ||

| Wheel & Tire Service Equipment | ||

| Vehicle Diagnostic & Testing Equipment | ||

| Washing & Cleaning Equipment | ||

| Other Niche Garage Tools | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| By Garage Type | OEM Dealership Garages | |

| Independent Garages | ||

| Franchise / Chain Workshops | ||

| By Ownership Model | Outright Purchase | |

| Lease / Rental | ||

| Subscription (Equipment-as-a-Service) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global spending on automotive garage equipment be by 2031?

Automotive garage equipment are forecast to reach USD 11.25 billion in 2031, rising at a 5.21% CAGR from 2026.

Which region is expanding fastest in garage-equipment demand?

Asia-Pacific leads growth with a projected 5.33% CAGR to 2031, buoyed by China’s inspection mandates and India’s formalizing service chains.

Why does Europe still generate the highest revenues despite slower growth?

Dense vehicle fleets, strict annual emission-testing laws, and high bay saturation keep Europe’s equipment replacement cycle steady even as overall expansion moderates.

What drives equipment purchases in North America?

An aging 12.6-year vehicle fleet and franchised chain roll-outs of standardized tool suites sustain steady orders for lifts, alignment systems, and diagnostic tablets.

How are Middle East and African workshops upgrading capabilities?

New inspection rules in the UAE and Saudi Arabia spur demand for emission analyzers and brake testers, while tariff relief accelerates tool imports into emerging sub-regional markets.

Are subscription procurement models affecting regional buying patterns?

Yes, chains in North America and Europe increasingly favor subscription contracts that bundle hardware, software, and maintenance, shifting capital outlays to operating budgets and shortening refresh cycles.

Page last updated on: