Conductive Textiles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

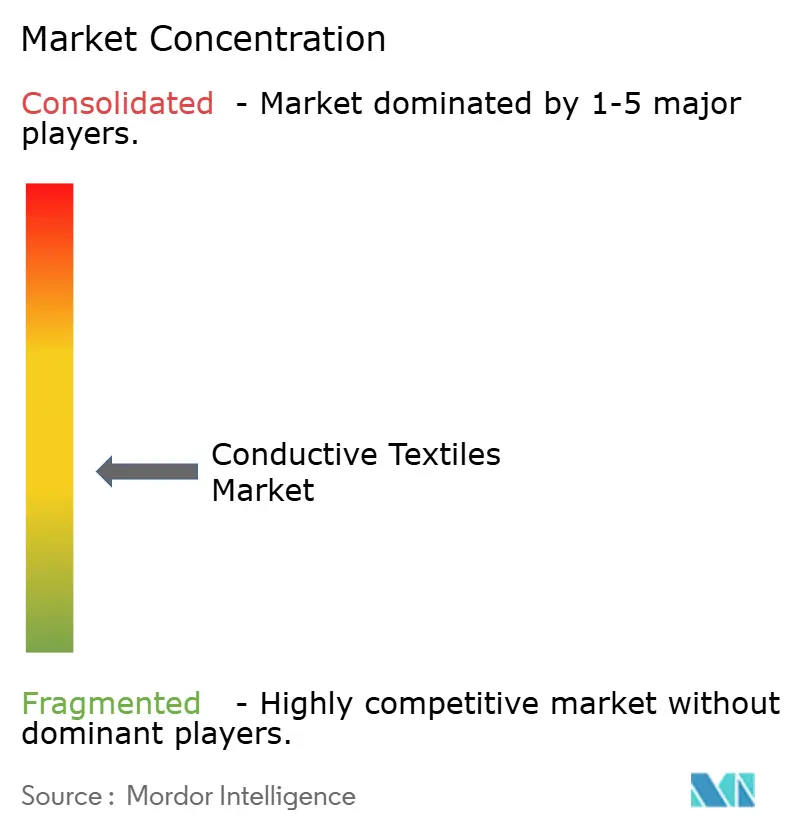

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conductive Textiles Market Analysis by Mordor Intelligence

The Conductive Textiles Market size was valued at USD 3.82 billion in 2025 and estimated to grow from USD 3.98 billion in 2026 to reach USD 4.86 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031). Sustained demand for lightweight electromagnetic-interference (EMI) shielding in autonomous vehicles, growing military modernization programs, and the rapid spread of healthcare wearables are the principal forces enlarging the conductive textiles market. Rising integration of artificial‐intelligence algorithms with textile-based sensors is turning garments into real-time health-monitoring platforms, while carbon-based yarns answer sustainability mandates without sacrificing conductivity. Automotive OEMs embed woven shielding fabrics behind dashboards and seat covers to protect advanced driver-assistance systems, and gaming brands use tactile haptic panels to enrich e-sports apparel. As these trends converge, the conductive textiles market is moving from niche prototypes toward large-volume consumer and industrial supply chains.

Key Report Takeaways

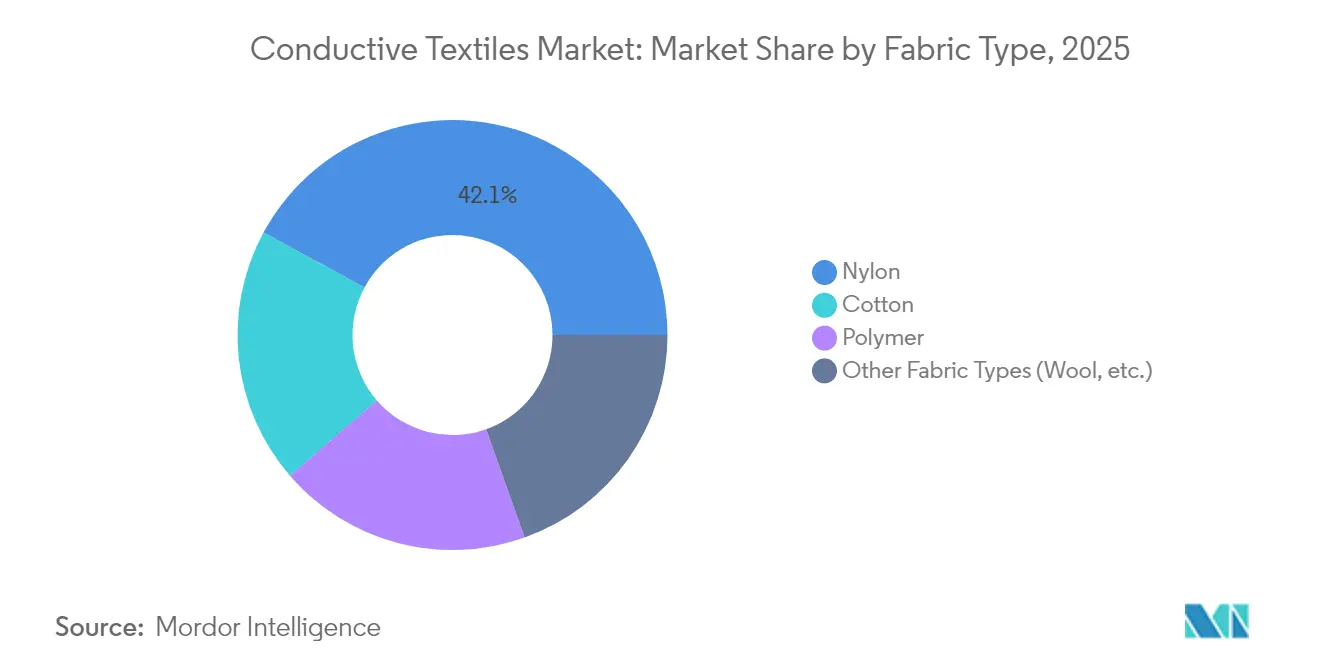

- By fabric type, nylon led with 42.10% revenue share in 2025, while its 4.88% CAGR keeps it the fastest-advancing fabric through 2031.

- By conductive material, metal-coated fibers held the top 34.72% share in 2025; carbon-based textiles record the highest 5.07% CAGR over the outlook period.

- By technology, woven constructions commanded 46.85% of 2025 value and are projected to climb at a 4.76% CAGR to 2031.

- By end-user industry, defense and military applications accounted for 30.10% of 2025 revenue, whereas other emerging industries expand at 5.01% CAGR to 2031.

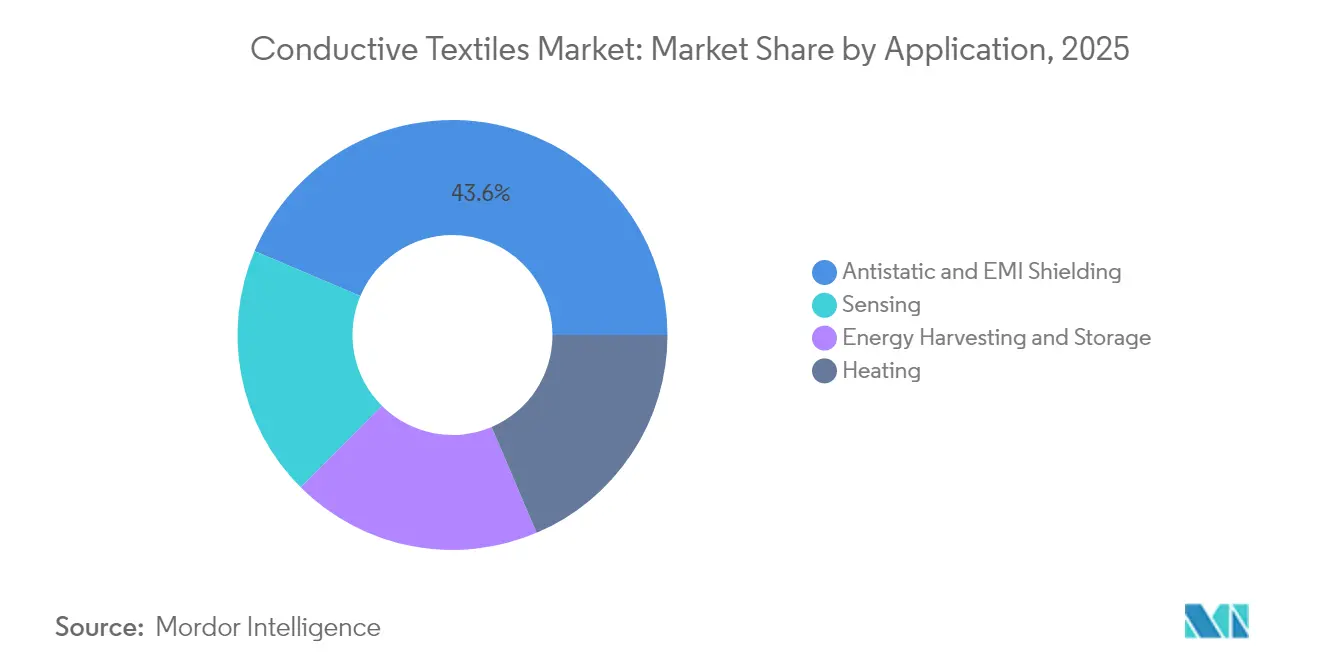

- By application, antistatic and EMI shielding captured 43.62% share in 2025; sensing solutions lead growth at a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conductive Textiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption in Smart Fabrics and Wearable Electronics | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Demand from Defense and Military Intelligent Gear | +0.8% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Expansion of Physiological-Monitoring Healthcare Wearables | +1.0% | Global, led by developed markets | Short term (≤ 2 years) |

| Rising Need for EMI Shielding in Autonomous-Vehicle Interiors | +0.7% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Growth of Haptic-Feedback E-Sports Apparel | +0.4% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption in Smart Fabrics and Wearable Electronics

Miniaturized chips now slip inside yarns, turning shirts, socks, and hospital gowns into connected devices that read motion, temperature, and heart rates without rigid modules. Hospital groups are procuring washable monitoring garments to cut skin-adhesive discomfort and to free nurses from wired sensors, accelerating commercial orders. Integrated energy-harvesting layers remove bulky batteries, extending wear time and widening consumer acceptance. Athletic brands market performance outfits that stream biometric data to mobile dashboards, and insurers explore policy discounts tied to verified activity logs. The spread of these real-time insights cements conductive fabrics as a core building block of next-generation digital health ecosystems.

Growing Demand from Defense and Military Intelligent Gear

Armed forces seek lighter uniforms that combine power distribution, radio links, and adaptive camouflage in one fabric panel[1]European Defence Agency, “Textile Integration for Soldier Systems,” eda.europa.eu. Woven conductive grids replace cables, cutting soldier carry weight and reducing snag hazards in confined vehicles. U.S. naval research funds low-cost signature-management cloth that can heat, cool, and sense chemical threats in the field. Field trials indicate 20% faster mission setup times because electronics arrive pre-wired in garments, lowering the fumbling of connectors under stress. With long procurement cycles, approved suppliers secure multi-year contracts that anchor demand even when commercial markets fluctuate.

Expansion of Physiological-Monitoring Healthcare Wearables

Textile electrodes match the accuracy of gel pads yet avoid skin irritation, enabling multi-week cardiology studies outside hospitals. Clinics remotely track chronic conditions, cutting readmissions and freeing beds for acute cases. For seniors, smart vests signal fall risk or respiratory decline, allowing earlier interventions that reduce emergency costs. Algorithmic analysis of continuous data feeds also supports precision dosing in cardiac and diabetes care. Payers studying pilot programs report improved adherence and lower long-term expenditure, bolstering reimbursement arguments that drive wider roll-outs.

Rising Need for EMI Shielding in Autonomous-Vehicle Interiors

Electric powertrains and radar arrays pump out electromagnetic noise that can scramble safety sensors unless cabins are lined with shielding cloth. Silver-plated woven fabrics block more than 77 dB while adding negligible weight versus metal foils. Tier-1 suppliers stitch these panels behind headliners and under carpets to satisfy evolving compatibility mandates. With production of autonomous shuttles ramping in Asia-Pacific, fabric makers secure multi-year volume contracts. Regulators tightening millimeter-wave limits ensure shielding demand remains structural rather than cyclical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost and Price Premium | -0.9% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Durability and Wash-Wash Cycle Degradation | -0.6% | Global, with higher impact in consumer applications | Short term (≤ 2 years) |

| Absence of Global Testing and Quality Standards | -0.4% | Global, with regional variations in regulatory approaches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Price Premium

Conductive yarns demand vacuum sputtering or polymer metallization steps that add process minutes and material waste, lifting unit prices by up to 40% versus conventional fabrics. Low volumes hinder scale economies, especially for niche medical patches. Buyers in price-sensitive mass fashion stall adoption until cost curves bend. Equipment amortization further squeezes smaller mills, limiting geographic spread and reinforcing supply concentration in capital-rich regions. Although learning rates are improving, the premium remains a brake on rapid commoditization.

Durability and Wash-Wash Cycle Degradation

Laundering scours coatings and bends microfilaments, raising resistance and dulling sensor accuracy after 40 wash cycles. Protective over-coats improve life but add stiffness and cost. Without universal durability labels, consumers hesitate to pay more for garments that may fail mid-season. Industrial buyers, such as hospitals, also require predictable sterilization outcomes, making repeatability a gating factor in procurement tenders. Progress in plasma treatments and encapsulated yarns is promising yet not fully proven at industrial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fabric Type: Nylon Leads Performance Applications

Nylon represented 42.10% of 2025 sales and is projected to grow at a 4.88% CAGR through 2031, underscoring its versatility across rugged defense gear and form-fitting sportswear. Its tensile strength withstands battlefield abrasion, while its chemical resilience accepts silver, copper, or carbon coatings without significant fiber degradation. The conductive textiles market benefits as automakers specify nylon mesh for headliner shielding, pushing mill demand upward.

Elastic recovery keeps sensors seated against skin during motion, sustaining signal quality for medical garments. Cotton retains share in comfort-first hospital linens, but nylon captures new contracts where durability and stretch matter most. On the research front, silver-coated nylon achieved conductivity of 96 S/cm in washability trials and still met breathability targets, expanding its runway in premium functional apparel.

By Conductive Material: Metal-Coated Fibers Dominate Despite Carbon Growth

Metal-coated fibers owned 34.72% of 2025 revenue thanks to proven EMI shielding in aerospace and automotive assemblies. Their low sheet resistance meets stringent aircraft avionics protocols. However, carbon-based textiles post the briskest 5.07% CAGR to 2031 as regulators steer away from heavy metals. Graphene weaves provide robust elasticity and maintain conductivity despite repeated bending, suiting consumer electronics sleeves. Cost curves for carbon nanotube inks are falling, narrowing the historical price gap. Hybrid yarns that combine carbon cores with thin metallic skins are emerging to balance conductivity with sustainability goals.

By Technology: Woven Fabrics Excel in Structural Applications

Woven constructions captured 46.85% of 2025 demand and are headed for a 4.76% CAGR through 2031, reflecting their structural integrity and uniform electrical pathways. Three-dimensional weave patterns embed complex circuits, allowing localized heating or sensing without extra layers. Knitted fabrics target stretchable sports gear, though higher resistance limits their role in rigorous EMI shielding. Non-wovens stay relevant in disposable sterile covers where low cost trumps performance. Automation in jacquard looms now places conductive yarn only where needed, trimming waste and reducing finished-goods cost.

By End-User Industry: Defense Leads While Consumer Applications Accelerate

Defense accounted for 30.10% of 2025 revenue, reflecting long-term modernization projects and the preference for battlefield-proven materials. Yet consumer electronics and automotive sectors propel the fastest 5.01% CAGR as wearable controllers and in-cabin sensors scale production. Hospital networks broaden use of smart bedding to detect patient movement, moving healthcare past pilot stages. Sportswear brands adopt conductive panels for muscle-activation feedback, elevating training apparel beyond mere moisture management. Diversified demand reduces revenue cyclicality tied to military budgets.

By Application: EMI Shielding Dominates Current Demand

Antistatic and EMI shielding represented 43.62% of 2025 turnover, driven by dense electronics in cars, aircraft, and 5G base stations. Conductive cloth shields cockpit avionics without adding metal weight. Sensing applications, forecast to advance at 4.93% CAGR, capture investment as Internet-of-Things roll-outs require flexible form factors. Heating panels maintain relevance in outdoor gear and battery-temperature management. Energy harvesting remains nascent but benefits from research that raises triboelectric power densities to device-ready levels.

Geography Analysis

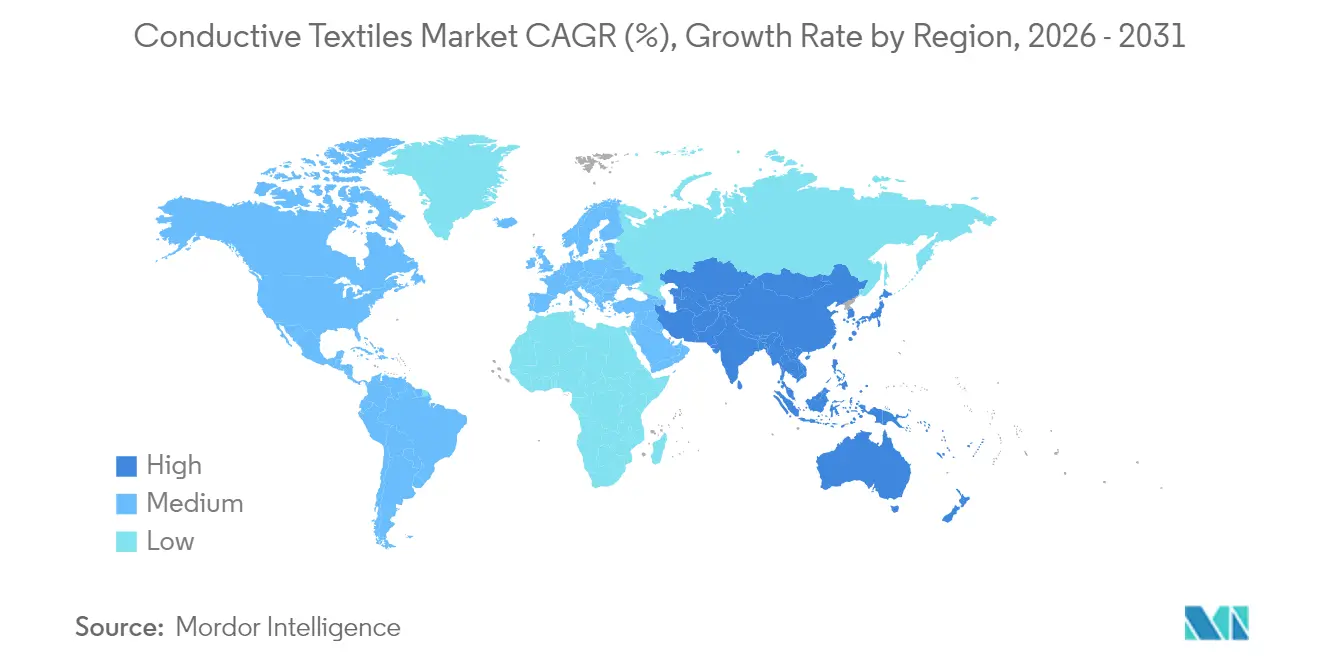

North America held 40.55% of 2025 revenue, powered by defense procurement contracts and early adoption of connected healthcare garments. Advanced supply links between textile mills and chip designers shorten prototype cycles, allowing rapid market entry. Research institutes secure federal grants to refine wash-resilient coatings, keeping regional know-how ahead of global peers. State incentives for semiconductor reshoring further tighten local value chains, insulating lead times from geopolitical freight disruptions.

Asia-Pacific delivers the highest 4.69% CAGR to 2031 as China leverages its textile scale to undercut global prices while climbing the technology ladder. Japanese automakers embed shielding cloth in electric sedans slated for global export, locking in baseline demand. South Korean display makers invest in fabric-integrated touch sensors, broadening market avenues beyond clothing. Government subsidies for Industry 4.0 equipment help local mills retrofit lines for conductive yarns, accelerating volume and squeezing unit costs.

Europe balances solid market share with a sustainability lens that favors recyclable and metal-free alternatives. German tier-1 suppliers qualify carbon-based cloth for next-generation vehicle interiors to meet end-of-life recycling rules. Nordic brands trial bio-based conductive threads in performance outerwear, aligning with circular-economy targets. The EU’s medical-device regulation offers a clear pathway for textile electrodes, easing cross-border hospital adoption.

Regulatory Landscape

Regulation and standardization for conductive textiles is split between electrical performance verification for e-textiles and chemical stewardship for textile inputs, with requirements varying by end use (defense, healthcare, automotive, and consumer). In February 2025, SIST EN IEC 63203-201-4:2025 formalized test methods to measure sheet resistance of conductive fabrics after abrasion, aligning qualification language for suppliers selling into wearable and smart textile programs. In October 2025, ASTM F3732-25 was published as a performance specification for conductive clothing in industrial applications, raising expectations in RFQs for protective and workwear products.

Chemical compliance requirements also act as a gate for commercialization, particularly for metal-coated fibers and coated fabrics. In China, GB/T 46755-2025 sets general technical requirements for smart textile products and includes restricted substance limits, such as cadmium content at or below 0.01% and nickel release limits at or below 0.5 ug/(cm squared week), shaping material selection and supplier qualification. In Europe, the REACH framework (EC 1907/2006) and the POP Regulation (EU 2019/1021) influence allowable chemistries and disclosure for textile components, while the EU Ecodesign for Sustainable Products Regulation (ESPR) introduces Digital Product Passport obligations that increase traceability expectations across conductive yarns, coatings, and finished garments.

Value Chain Analysis

The conductive textiles value chain starts with upstream feedstocks and functional materials (silver, copper, stainless steel, nickel and metallization chemistries, conductive polymers, and carbon-based materials such as graphene and carbon nanotubes), then moves into yarn formation and functionalization (spinning, blending, twisting, and metal-coating or coating processes). Midstream converters produce fabrics through weaving, knitting, or nonwoven routes, followed by finishing steps aimed at durability and electrical repeatability (encapsulation, lamination, plasma treatments, and protective topcoats) to manage wash-cycle and abrasion-driven resistance drift. Downstream, fabrics are integrated into applications through sewing, printing/embroidery of circuits, connectorization, and module integration, before distribution to OEMs and brands in defense, healthcare, automotive interiors (EMI shielding), sportswear, and consumer electronics.

Standardization is increasingly embedded in commercial transactions and supplier qualification workflows, shaping how materials are specified and tested across the chain. The Global Electronics Association (IPC) released IPC-8911 in July 2025 as the first global standard for requirements, classification, designation, and qualification of conductive yarns for e-textiles, helping suppliers and buyers align on terminology and minimum validation. In parallel, the IPC-8900 family (including IPC-8921A for fabrics and IPC-8953 for embroidered circuits) and the IEC 63203 measurement series are used as reference points for electrical property measurement and component-level testing, supporting cross-border sourcing while also increasing documentation and test-data expectations for mills, coaters, and garment integrators.

Competitive Landscape

The conductive textiles market features moderate fragmentation. Specialist firms leveraging proprietary coating chemistries compete with legacy mills now integrating electronics. Early movers secure supply agreements in defense and healthcare, locking in volumes that finance process refinements. Partnerships between yarn producers and printed-circuit makers blend textile and electronics know-how, shortening design iterations.

Competitive advantage hinges on maintaining conductivity after 50 wash cycles while keeping costs within consumer thresholds. Companies refining plasma-bonded silver coatings report resistance losses below 5% after standard home laundering, outperforming rivals by a clear margin[2]A. Singh, “Plasma-Bonded Silver Coatings for Wearable Electronics,” MDPI Coatings, mdpi.com. Standard IPC-8921 benchmarks gain traction in RFQ documents, rewarding suppliers with certified test data.

Strategic acquisitions intensify. Traditional apparel conglomerates purchase sensor startups to capture margin from smart-garment lines, while automotive suppliers buy weaving specialists to internalize EMI shielding capability. These moves tighten control over patented processes and help spread R&D expense across larger order books.

Conductive Textiles Industry Leaders

TORAY INDUSTRIES

Bekaert

Shieldex

Laird Performance Materials

HS HYOSUNG ADVANCED MATERIALS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One near-term whitespace is reducing commercial friction through harmonized qualification and reliability language for conductive yarns and fabrics across industries that use different acceptance criteria. The July 2025 release of IPC-8911 by the Global Electronics Association provides a common framework for classifying and qualifying conductive yarns and complements the IEC 63203 measurement series used for basic electrical property assessment. Together, this standard stack supports scalable procurement for brands and OEMs by tightening specifications for conductivity retention, abrasion effects, and repeatable measurement, addressing a key restraint tied to the absence of global testing and quality standards.

Materials innovation creates a second opportunity area, particularly where metal load, wash durability, and sustainability constraints intersect. In April 2026, Covestro, FILK Freiberg, and OUT e.V. disclosed a flexible conductive polymer smart textile system based on Impranil polyurethane dispersions with carbon nanotubes, positioning conductive polymers and carbon-based pathways as alternatives to heavier metal coatings in medical and therapeutic garment concepts. Adjacent expansion in electronic-grade cloth capacity also reinforces the broader electronics ecosystem that shares process know-how and supply infrastructure with conductive textile finishing and converting. China Jushi commissioned a new Huai'an line in March 2026 for electronic fiberglass and electronic cloth and, in May 2026, announced a USD 653 million planned investment for additional capacity in the same location.

Recent Industry Developments

- April 2026: Covestro, FILK Freiberg, and OUT e.V. disclosed a flexible conductive polymer smart textile system based on Impranil polyurethane dispersions with carbon nanotubes. The collaboration highlights a polymer-based path toward durable, lightweight conductive textiles for medical and therapeutic garments, signaling a strategic shift in material selection and production thinking.

- July 2025: The Global Electronics Association (IPC) released IPC-8911, a global standard defining requirements, classification, designation, and qualification for conductive yarns used in e-textiles. A formal yarn standard improves comparability across suppliers and streamlines technical communication from yarn makers through fabric converters to OEMs and brands, reducing rework in sampling and validation.

- December 2024: Bally Ribbon Mills developed E-WEBBINGS e-textile products for aerospace applications that integrate embedded electronics to transmit data, sensations, and power within smart textile systems. Embedding functionality into webbing architectures supports lightweighting and packaging efficiency for aerospace and other high-reliability markets, expanding the addressable scope beyond apparel into engineered textile assemblies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers textiles that are engineered to carry electrical current or signals through conductive fibers, yarns, coatings, or fabric structures, and which are sold into end uses like wearable sensing, EMI shielding, and related functional applications.

Scope exclusions: We exclude conventional apparel textiles without a defined conductivity function and exclude non-textile electronic components sold separately from the textile.

Segmentation Overview

- By Fabric Type

- Cotton

- Nylon

- Polymer

- Other Fabric Types (Wool, etc.)

- By Conductive Material

- Metal-coated Fibers

- Conductive Polymers

- Carbon-based Textiles

- Hybrid Composites

- By Technology

- Woven

- Non-woven

- Knitted

- By End-user Industry

- Defense and Military

- Healthcare

- Sports and Fitness

- Other End-user Industries (Consumer Electronics, etc.)

- By Application

- Sensing

- Heating

- Antistatic and EMI Shielding

- Energy Harvesting and Storage

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for demand signals and supply readiness before any modeling was finalized. We referred to public sources such as the US International Trade Commission trade data, UN Comtrade, the US Bureau of Labor Statistics for producer and material cost direction, and the European Commission regulatory pages covering chemicals and product compliance that can affect textile coating choices.

To keep the inputs grounded, we also reviewed patent databases for activity around conductive fibers and textile integration methods, along with peer reviewed journals that report performance benchmarks for silver, carbon, and polymer based conductive layers. Company filings, investor presentations, and credible press releases were then used to confirm capacity additions, application focus, and regional manufacturing footprints. We also used paid subscriptions for company financials and for patent analytics, mainly to speed up cross checks. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of technical textile demand is specified as conductive, and how pricing shifts with material choice and application complexity. We spoke with stakeholders across fiber and yarn suppliers, fabric manufacturers, coating and finishing specialists, and downstream buyers in wearables, medical textiles, defense applications, and automotive interiors. Regional coverage was balanced across APAC, EMEA, and the Americas to reflect manufacturing and demand centers.

The respondent input was used to tighten the conductive share rules (for example, when a textile is sold for sensing or shielding versus when conductivity is only a lab capability) and to confirm how quickly adoption changes after product qualification cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 21% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 22% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where technical textile and end use demand pools are reconstructed using production and trade direction, and then filtered by the share that requires conductivity as a specification rather than as a lab feature. That total is corroborated with selective bottom-up checks, such as sampled volume and average selling price ranges for conductive yarns and coated fabrics, plus channel checks on adoption across key applications.

The model uses a small set of practical inputs that can be tracked and refreshed, including the adoption rate of wearable and medical sensing textiles, defense and industrial EMI shielding textile demand, conductive material mix (silver versus carbon based layers), average coating add-on cost, and the split between woven, knitted, and non-woven formats where performance needs differ. For forecasting, we apply scenario analysis supported by expert views, and then smooth the trajectory using recent demand indicators so the curve does not overreact to one-time projects. Where volume indicators are incomplete for smaller producing countries, gaps are handled through proxy shares based on trade participation, known manufacturing hubs, and interview-backed utilization assumptions.

Data Validation & Update Cycle

Outputs are validated by triangulating the modeled totals against independent signals like conductive material consumption direction, trade flows for relevant textile categories, and the pace of new product launches tied to wearable and shielding uses. Any large variance is reviewed by re-checking unit assumptions, currency conversions, and the implied price-volume mix, and then by re-contacting sources when the shift looks event-driven.

Before sign-off, the work goes through multiple analyst reviews that test logic, math integrity, and whether the narrative matches the numbers. Reports are refreshed annually, and interim updates are made when material events occur such as sudden raw material price moves or meaningful capacity changes. Right before delivery, a final freshness check is done so clients receive the latest updated view.

Mordor Intelligence's Conductive Textiles Market Size Measured Against Other Published Estimates

Published market numbers for conductive textiles can look far apart, even when the same words are used, because each study sets its own scope and then applies different pricing and adoption assumptions. Differences usually come from what is counted as a textile sale, which end uses are included, and how quickly the model updates pricing and penetration inputs.

Some published estimates expand the scope to include broader smart textile revenue pools or add adjacent electronic components bundled with garments, which pushes the total up quickly. Mordor Intelligence sizing counts revenue only when a textile product is sold with a defined conductive function, and prices are refreshed using material mix checks and application specific adoption feedback so non-conductive smart fabric value is not blended in.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.98 B (2026) | |

| Global Consultancy A | USD 4.30 B (2025) | Uses an earlier base year and can capture a wider smart textile value pool, and the uplift is sensitive to how conductive share is assumed across sports, medical, and defense applications. |

| Industry Research Group B | USD 3.54 B (2024) | Base year is set earlier and the forecast step-up implies aggressive penetration and pricing, with less visibility on how material mix and coating add-on costs are reconciled to trade and production signals. |

Taken together, the spread is mainly explained by scope cutoffs, base-year selection, and how fast adoption and pricing are allowed to move in the forecast. Our approach stays traceable because each step ties back to observable demand indicators, a clear conductive function rule, and repeatable price-volume checks that can be revisited during updates.

Key Questions Answered in the Report

What is the current size of the conductive textiles market?

The conductive textiles market is valued at USD 3.98 billion in 2026 and is projected to reach USD 4.86 billion by 2031.

How fast is the conductive textiles market growing?

The market is expected to expand at a 4.09% CAGR between 2026 and 2031.

Which region holds the largest share of the conductive textiles market?

North America leads with 40.55% of 2025 revenue due to robust defense spending and early healthcare adoption.

What are the main growth drivers for conductive textiles?

Rising demand for EMI shielding in electric and autonomous vehicles, expansion of healthcare wearables, and military modernization programs are the primary growth drivers.

Which material type is gaining the most traction?

Carbon-based textiles record the fastest 5.07% CAGR through 2031, favored for durability and sustainability advantages.

Page last updated on: