Antimicrobial Textile Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.29 Billion |

| Market Size (2031) | USD 17.25 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

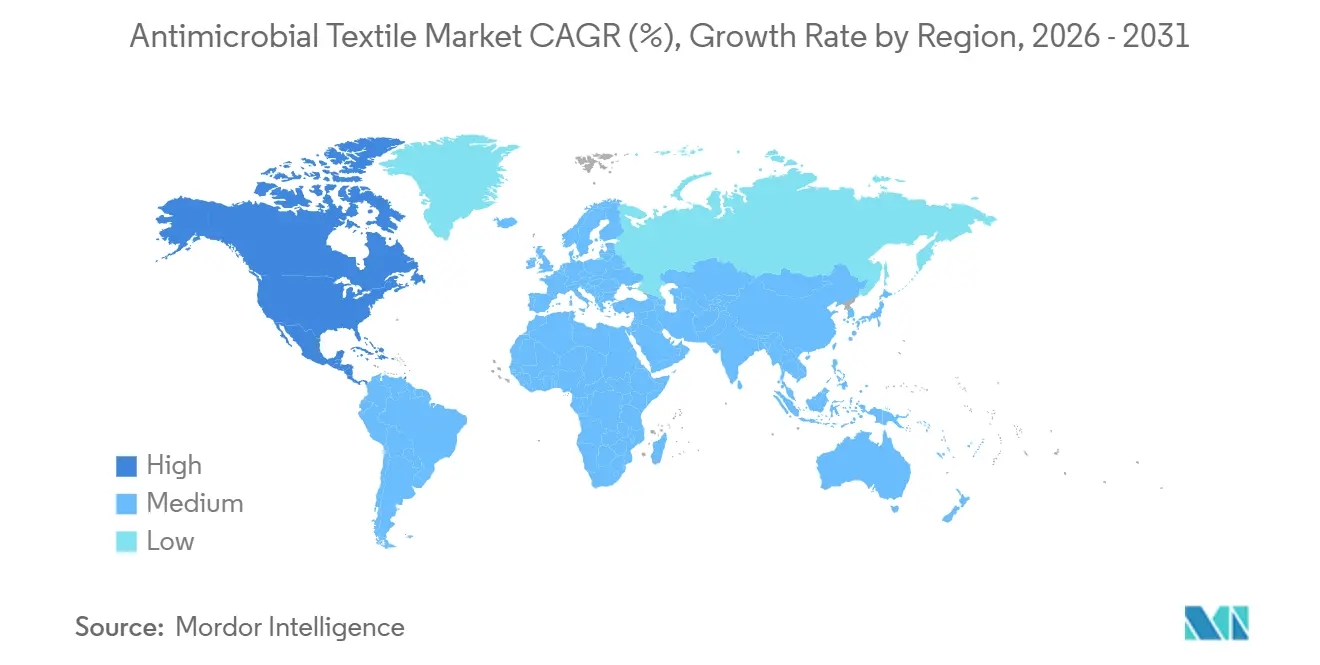

| Fastest Growing Market | North America |

| Largest Market | Europe |

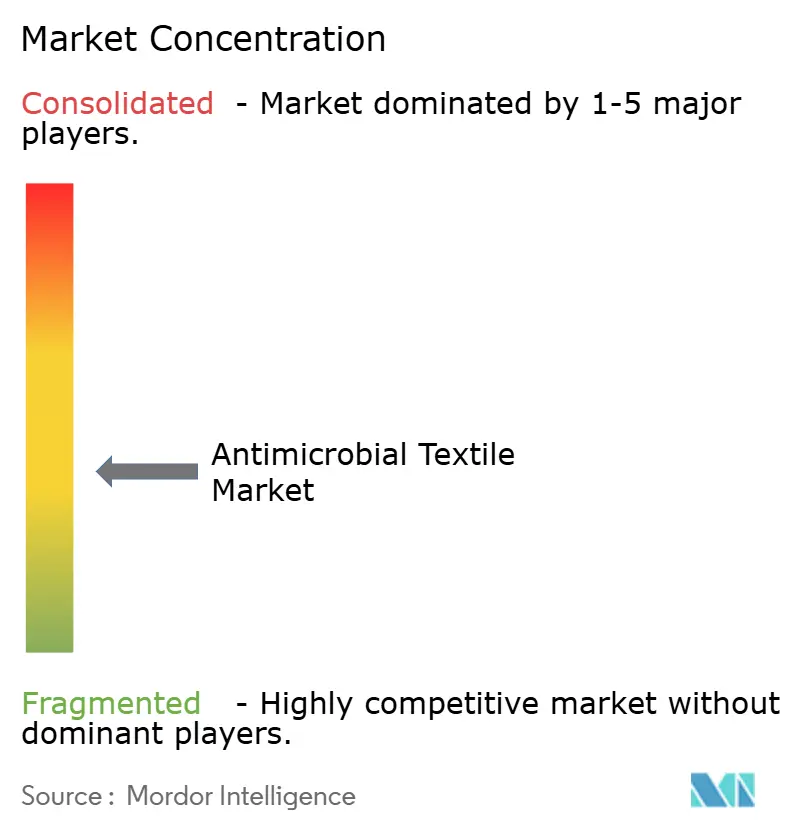

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antimicrobial Textile Market Analysis by Mordor Intelligence

The Antimicrobial Textile Market size is estimated at USD 14.29 billion in 2026, and is expected to reach USD 17.25 billion by 2031, at a CAGR of 3.84% during the forecast period (2026-2031). Demand is shifting from opportunistic hygiene add-ons toward mandated infection-control solutions in healthcare, public transit, and shared-mobility interiors, where regulators now require verified microbial-reduction data rather than generic “antimicrobial” claims. Continued enforcement of REACH Annex XVII in Europe boosts adoption of durably bonded chemistries that remain effective after industrial laundering, while North American transit authorities retrofit upholstery in line with CDC soft-surface guidelines, lifting regional growth prospects. Medical textiles retain a clear volume lead, yet premium sportswear brands are expanding silver-ion polyamide deployments in moisture-wicking layers to control odor without hindering recyclability. Heightened regulatory scrutiny of nanoparticle discharge and silver-price swings continues to redirect R&D toward recyclable masterbatch systems and biopolymer actives.

Key Report Takeaways

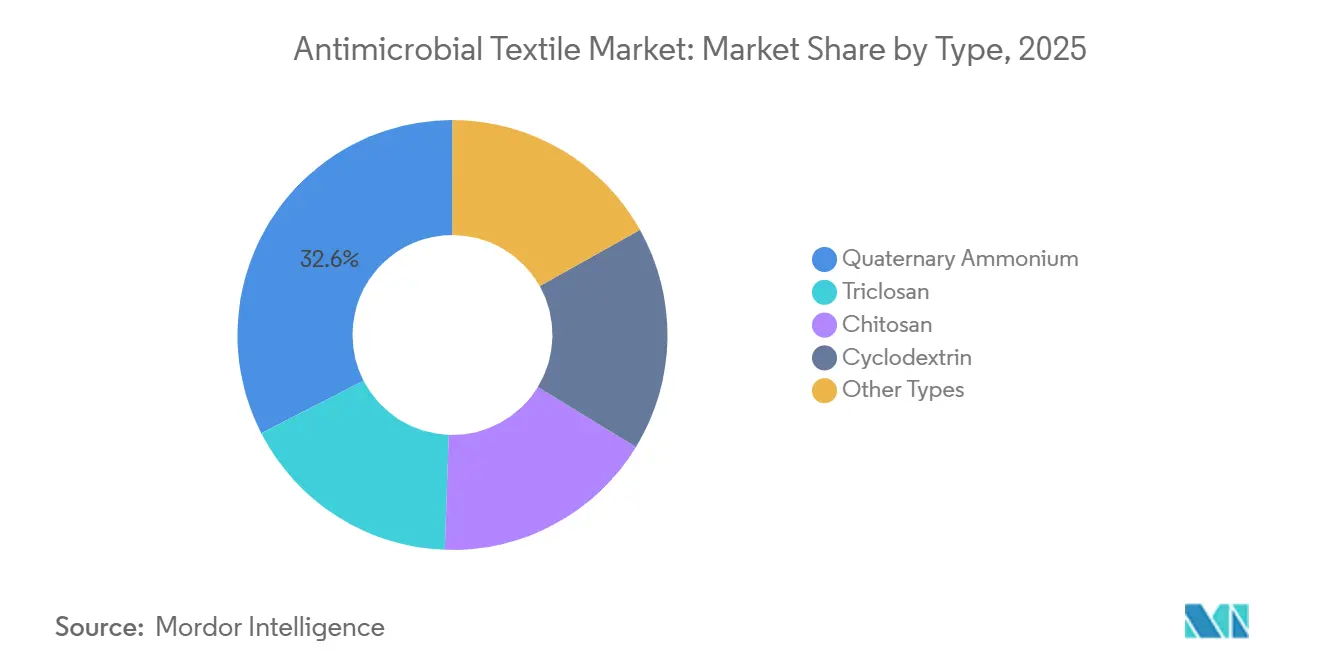

- By type, quaternary ammonium captured 32.56% of antimicrobial textile market share in 2025, while chitosan is forecast to record a 5.81% CAGR through 2031.

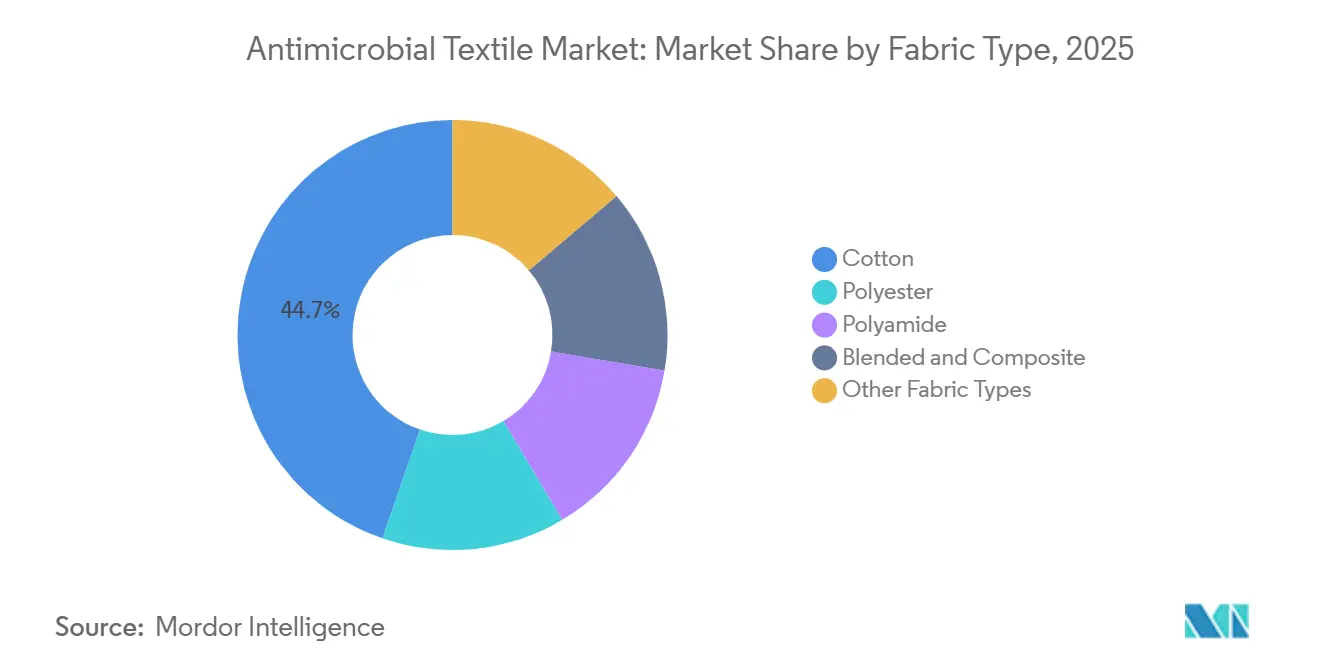

- By fabric type, cotton accounted for 44.71% of antimicrobial textile market share in 2025, whereas polyamide is projected to expand at a 5.94% CAGR to 2031.

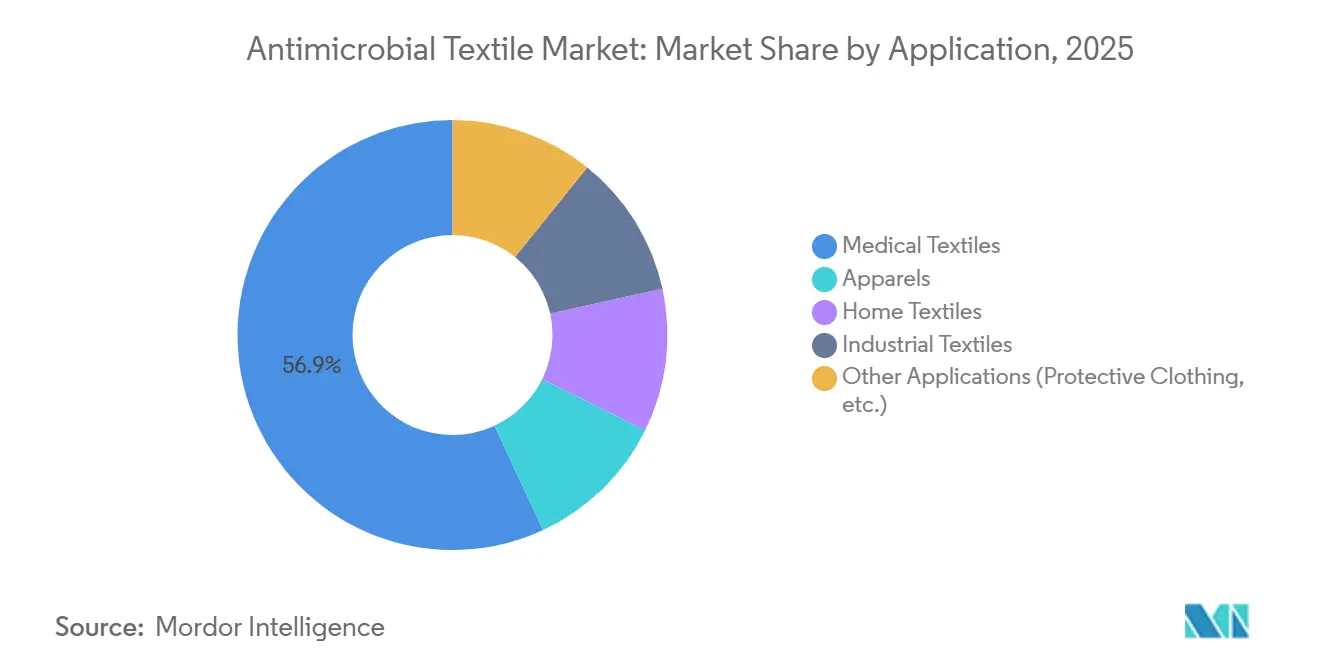

- By application, medical textiles held 56.92% of antimicrobial textile market share in 2025, while other applications are expected to grow at a 5.06% CAGR to 2031.

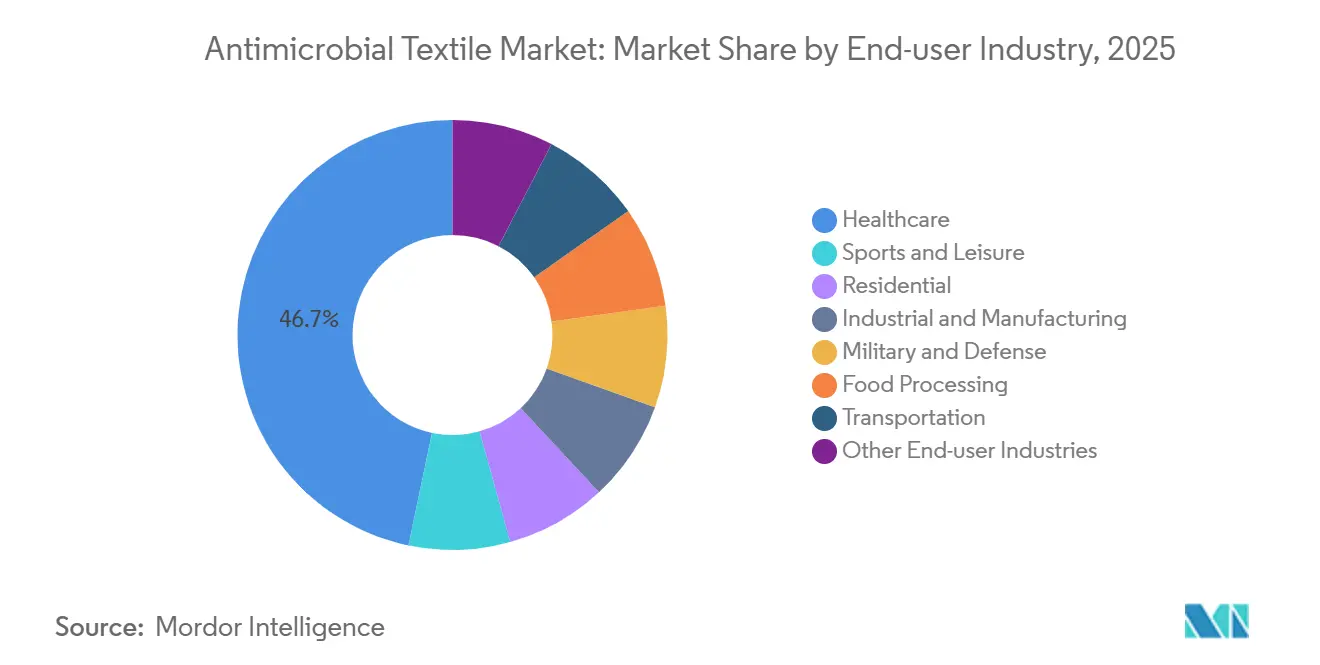

- By end-user industry, healthcare represented 46.71% of antimicrobial textile market share in 2025, while sports and leisure is poised for a 5.98% CAGR on the back of athleisure upgrades.

- By geography, Europe generated 35.01% of antimicrobial textile market share in 2025, while North America is predicted to advance at a 4.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antimicrobial Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Healthcare-Associated Infection (HAI) Prevention Mandates | +1.2% | Global, with early enforcement in EU and North America | Medium term (2-4 years) |

| Athletic-Odor Management Demand in Premium Sportswear | +0.9% | North America, Europe, APAC urban centers | Short term (≤2 years) |

| Smart-Wearables Using Antimicrobial Sensor Fabrics | +0.6% | North America, Japan, South Korea | Long term (≥4 years) |

| Public Transport and Shared-Mobility Upholstery Hygiene Upgrades | +0.7% | North America, Europe, APAC megacities | Medium term (2-4 years) |

| Recycling-Ready Silver-Ion Masterbatch Adoption | +0.5% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Healthcare-Associated Infection Prevention Mandates

ISO 20743 now underpins hospital tenders, obliging suppliers to verify log-3 bacterial‐reduction performance against Staphylococcus aureus and Klebsiella pneumoniae, the pathogens driving 42% of 2024 bloodstream infections in the CDC network[1]Centers for Disease Control and Prevention, “NHSN CLABSI Surveillance Report 2024,” cdc.gov . Procurement teams favor mills that maintain in-house AATCC 100 and ASTM E2149 capability, shrinking opportunities for job‐dyers dependent on external certification. The U.K. NHS mandated 71 °C, 3-minute thermal disinfection in 2025, a practice that degrades topical quats yet leaves silver-bonded polyamide intact, prompting a pivot to inherently antimicrobial synthetics in drapes and gowns. Comparable durability requirements entered Japan’s JIS L 1902, driving consolidation around masterbatch solutions. Similar stringency now applies to ISO 13629-2 cleanroom garments and FDA 510(k) wound dressings, reinforcing demand for proven, wash-resilient fabrics.

Athletic-Odor Management Demand in Premium Sportswear

Nike’s February 2025 Aero-FIT base layers introduced silver-polymer masterbatch in recycled polyester, addressing the USD 12 billion performance-apparel segment where malodor accounts for 23% of returns. A Textile Research Journal study found untreated polyester emitted 4.7 times more methanethiol than wool, yet matched wool once dosed with 0.8 wt% silver ion. Adidas, Under Armour, and Lululemon have since specified antimicrobial polyamide in compression zones, extending garment life and reducing wash frequency. Fulgar’s Q-SKIN polyamide retains 94% efficacy after 100 household washes, meeting OEKO-TEX Class I safety limits. Brands also lean on REACH Annex XVII entry 72, which caps silver release at 0.1 mg/kg per wash, guiding chemistry selection.

Smart-Wearables Using Antimicrobial Sensor Fabrics

Conductive yarns in glucose-monitoring patches and ECG tees need antimicrobial coatings to prevent biofilm that can raise electrode impedance by up to 40% within 72 hours. MIT and ETH Zurich trials showed graphene oxide layers on silver-plated polyamide kept impedance below 50 ohms after simulated 14-day wear. Medtronic invested USD 15 million in a European consortium to commercialize such fabrics for remote patient monitoring in 2024. Japan’s NEDO is funding JPY 2.3 billion to develop washable antimicrobial e-textiles aiming for ISO 13485 certification by 2027. Regulatory ambiguity persists: EU MDR classifies antimicrobial sensor fabrics as Class IIa when infection-prevention claims are made, while U.S. FDA routes them through 510(k) predicates.

Public Transport and Shared-Mobility Upholstery Hygiene Upgrades

EPA’s 2023 guidance on soft-surface disinfection in high-traffic environments pushed U.S. transit agencies to require fabrics that log-3-reduce bacteria within 24 hours. New York’s MTA awarded a USD 47 million contract in August 2024 for quaternary-treated polyurethane-coated polyester seat covers meeting AATCC 100 performance. Transport for London retrofitted 1,200 buses in Q1 2025 using BioCote silver-additive covers compatible with U.K. flame-retardant rules. Singapore’s LTA now mandates ISO 22196 reports for rail upholstery procured after January 2025. Airbus likewise selected antimicrobial seat fabrics for A350 retrofits delivering from 2026 to Gulf carriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Nanoparticle Discharge Restrictions (EU REACH, US EPA) | -0.8% | Europe, North America | Short term (≤2 years) |

| Premium Cost Delta vs. Untreated Textiles | -0.5% | Global, acute in price-sensitive ASEAN and South America | Medium term (2-4 years) |

| Silver Price Volatility and Supply-Chain Concentration | -0.3% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightening Nanoparticle Discharge Restrictions (EU REACH, US EPA)

ECHA placed nano-silver on its SVHC Candidate List in March 2024, forcing importers of articles with more than 0.1 wt% nano-silver to submit Article 7 notices and pay dossier fees ranging from EUR 50,000 to EUR 150,000[2]European Chemicals Agency, “SVHC Candidate List March 2024,” echa.europa.eu . The move has already reduced European antimicrobial-finish formulators from 47 to 29 between 2022 and 2025. In parallel, the U.S. TSCA Section 8(a) nanomaterial rule, active January 2025, mandates production-volume and exposure reports for sub-100 nm silver particles with penalties up to USD 50,000 per day. Because polymer-bound silver is exempt, mills are racing to install twin-screw lines for masterbatch integration, extending development cycles by a year or more.

Premium Cost Delta Vs. Untreated Textiles

Silver-ion masterbatch can cost USD 8–12/kg against USD 1.80/kg for virgin PET, translating to a 22–35% price premium at the fabric level, a hurdle in price-sensitive home-textile markets. Large mills above 5,000 tpa capacity cut the premium to 15–18% through scaling, yet small converters in ASEAN and South America face 40–50% penalties. Indonesia’s Ministry of Industry found only 3.2% of domestic home textiles used antimicrobial treatments in 2024 owing to affordability gaps. Consumer habits also matter; regions that favor hot-water washing see slower payback from low-temperature optimized antimicrobial fabrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Quaternary Ammonium Dominates, Chitosan Accelerates

Quaternary ammonium held 32.56% of 2025 antimicrobial textile market share, reflecting its broad-spectrum activity and favorable economics in workwear and hospitality linen. Yet California’s Safer Consumer Products list now flags benzalkonium chlorides, adding compliance costs that erode its advantage. Triclosan persists only in niche surgical scrubs after FDA bans on OTC antiseptics. Chitosan is forecast to grow at a 5.81% CAGR, benefiting from GRAS status under FDA 21 CFR 184 and biocompatibility that eases ISO 10993 cytotoxicity hurdles. Studies in Carbohydrate Polymers confirm log-3 reductions at 1 wt% loading, competitive with silver at a fraction of the material cost.

Durability expectations amplify these shifts. EPA FIFRA registration requires public-health claims for quats, yet chitosan marketed for odor control can bypass pesticide status, allowing quicker commercialization. Hybrid formulations blending chitosan with low-dose silver aim to balance cost, safety, and wash resistance. Meanwhile, copper and zinc pyrithione fill specialist gaps in diabetic socks and mildew-resistant outdoor gear.

By Fabric Type: Cotton Leads, Polyamide Surges

Cotton kept 44.71% of 2025 volume, driven by home-textile and hospital-linen comfort requirements, but its topical finishes lose efficacy after 30–40 industrial washes, raising lifecycle costs. Polyamide, forecast to grow at 5.94%, integrates silver ions during melt-spinning, locking them within the polymer matrix and retaining 94% activity after 100 domestic washes, thus commanding a premium in compression hosiery and surgical garments.

Blends such as 65/35 polyester–cotton meet NFPA 1999 EMS garment codes and provide a midway option where comfort and durability must coexist. Aramid and modacrylic variants serve flame-retardant military uses, with Milliken enlarging capacity via its January 2025 Two Rivers acquisition to supply Artemis mission garments. Across all fabrics, ISO 6330 wash-test compliance and REACH Annex XVII silver-release caps govern chemistry choices.

By Application: Medical Textiles Anchor Demand, Protective Clothing Gains

Medical textiles secured 56.92% of 2025 revenue as hospital gowns, drapes, and wound dressings must meet ISO 13629-2 and AATCC 100 benchmarks. The NHS thermal-laundering update accelerates polyamide adoption by guaranteeing performance after 50 industrial cycles. Apparel follows but at modest growth because casualwear buyers rarely absorb full premiums outside high-end sportswear. Home-textile uptake remains selective yet grows in hospitality; Marriott’s 2024 pilot saw a 19% linen-replacement reduction after adopting antimicrobial duvet covers.

Protective clothing, grouped under “other applications,” are set for a 5.06% CAGR. The U.S. DoD funds 14-day no-launder base layers under ASTM F1980, and food processors need antimicrobial garments to curb Listeria under FDA 21 CFR 110. Cleanroom wipes rated to ISO 14644 add another growth pocket in semiconductor fabs.

By End-user Industry: Healthcare Leads, Sports and Leisure Outpace

Healthcare accounted for 46.71% of 2025 spending because hospitals target measurable infection reductions under ISO 20743 contracts. The CDC logged 16,730 CLABSI cases in 2024, reinforcing demand for antimicrobial patient wear and securement devices. Sports and leisure, however, will post a 5.98% CAGR: silver-ion polyamide in athleisure base layers lowers odor and extends garment life, aligning with consumer sustainability goals.

Residential penetration is concentrated in humid zones prone to mildew, while industrial clients in cleanrooms and conveyor systems seek longer service intervals. Military applications focus on extended-wear uniforms, and transit upholstery gains relevance as transport authorities adopt EPA soft-surface guidance.

Geography Analysis

Europe led the antimicrobial textile market with 35.01% of 2025 revenue, driven by stringent REACH Annex XVII controls that push mills toward masterbatch solutions, eliminating leachable nanoparticle finishes. Germany’s machinery suppliers, notably Oerlikon, enable in-line silver dosing, while the U.K. NHS laundry protocol favors polyamide surgical packs, lifting demand in Britain and Ireland. France’s ANSM requires MDR 2017/745 CE marking for antimicrobial dressings, consolidating the supplier base among vertically integrated firms. Italy’s Prato district is shifting into polyamide-cotton blends to mitigate finish degradation on traditional wool lines.

North America is set to grow at a 4.77% CAGR through 2031 as TSCA rules encourage polymer-bound silver, prompting domestic spinning investments and reducing reliance on Asian imports subject to nanoparticle reporting. Health Canada harmonized its PMRA guidance with EPA FIFRA in late 2024, cutting registration delays for cross-border suppliers. Mexico’s maquiladoras supply antimicrobial workwear under USMCA origin rules, benefiting from proximity to U.S. clients.

In Asia-Pacific, China’s GB/T 20944 revision aligns to ISO 20743, making exports smoother, while Japan’s 50-wash JIS L 1902 durability test favors Toray and Unitika masterbatches. South Korea’s MFDS fast-tracked chitosan wound dressings in 2025, and ASEAN’s regulatory patchwork slows uptake outside Thailand and Malaysia. South America and the Middle East and Africa remain nascent, though Brazil’s ANVISA instituted hospital antimicrobial-textile registration in 2024.

Competitive Landscape

The antimicrobial textile market is moderately concentrated. HeiQ Materials, Microban International, Polygiene, Sanitized, and Milliken together supplied an estimated 44% of additives in 2025, leaving space for regional specialists. To protect margins, leading firms pivot to licensing masterbatch technologies to fiber producers rather than selling finished fabric. HeiQ’s restructuring and 2024-2025 delisting underscore this shift, trimming direct consumer exposure to focus on B2B royalties. Indorama Ventures’ joint venture with Jiaren exemplifies vertical integration that captures recycling revenue and secures silver supply.

Regulatory acumen is a differentiator. Noble Biomaterials’ EPA-registered Ionic+ Botanical line sidesteps heavy-metal limits, offering formulators an alternative to silver subject to REACH and TSCA reporting. Smaller players lacking hedged silver contracts suffered when spot prices climbed 40% in 2024, triggering exits and reinforcing the position of vertically integrated giants like Toray and Indorama. ISO 13485 and OEKO-TEX certification have become de facto gatekeepers, directing buyers toward suppliers that can prove consistent quality and skin safety.

Technology roadmaps converge on circularity and safety. Masterbatch integration eliminates wastewater silver discharge, aligns with forthcoming ECHA wastewater norms, and facilitates end-of-life silver recovery. Chitosan suppliers exploit GRAS status to avoid pesticide registration and capture wound-care niches. Meanwhile, copper and zinc formulations address diabetic-care socks and mildew-prone outdoor gear but must navigate aquatic-toxicity scrutiny under EPA Copper Action Plan.

Antimicrobial Textile Industry Leaders

Polygiene Group AB

Sanitized AG

Microban International

HeiQ Materials AG

Milliken

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Researchers from Telangana, India and South Korea developed an eco-friendly method for producing antimicrobial textiles using silver nanoparticles (AgNPs) synthesized from Bryophyllum pinnatum (Air plant) leaf extract. This process involved coating cellulose cotton fabric (CCF) with silver nanoparticles through an environmentally friendly deposition technique.

- October 2024: 1888 Mills, LLC partnered with FUZE Technologies (FUZE), a company specializing in antimicrobial textile treatments. FUZE's textile treatment, F1, is a chemical-free, water-based solution that permanently adhered to materials without requiring binders or surfactants.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the antimicrobial textile market as finished fabrics and ready-made items that permanently embed active agents such as silver salts, quaternary ammonium compounds, or chitosan that suppress bacterial, fungal, and viral growth through repeated wash cycles in medical, apparel, home-furnishing, and light-industrial uses.

Scope exclusion: one-time after-market spray or fogging services applied once products leave the mill are outside this study.

Segmentation Overview

- By Type

- Quaternary Ammonium

- Triclosan

- Chitosan

- Cyclodextrin

- Other Types

- By Fabric Type

- Cotton

- Polyester

- Polyamide

- Blended and Composite

- Other Fabric Types

- By Application

- Medical Textiles

- Apparels

- Home Textiles

- Industrial Textiles

- Other Applications (Protective Clothing, etc.)

- By End-user Industry

- Healthcare

- Sports and Leisure

- Residential

- Industrial and Manufacturing

- Military and Defense

- Food Processing

- Transportation

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We held dialogs with finish formulators, hospital buyers in the United States and Germany, and sportswear sourcing heads in India and China. Their insights on average selling prices, wash-life thresholds, and bio-agent substitution rates helped us tighten volume assumptions.

Desk Research

We began with UN Comtrade HS-5603 and 300590 flows, Eurostat PRODCOM 1392, and USITC trade files, then mapped biocidal-finish patent families on Questel. Mordor analysts layered CDC infection-control advisories, AATCC journals, company 10-Ks, and paid repositories such as D&B Hoovers and Dow Jones Factiva to benchmark treated-fabric revenue. These examples show our reach, while many additional sources supported corroboration.

Market-Sizing & Forecasting

We start with a top-down rebuild of woven, knitted, and non-woven substrate output drawn from production and trade data, then layer penetration shares captured in interviews. Targeted bottom-up checks, supplier roll-ups, and sampled ASP × volume temper the totals. Key variables include treated-fabric share, treatment ASP, wash-life driven replacement, hospital bed additions, and sports-apparel floor-space growth. A multivariate regression fed by these drivers and CPI-linked fiber costs projects demand to 2030, while scenario analysis covers stricter biocide rules.

Data Validation & Update Cycle

Outputs clear two analyst reviews, and any unexplained variance triggers fresh calls. We refresh models each year and push interim updates whenever a material event alters a driver.

Why Mordor's Antimicrobial Textile Baseline Commands Confidence

Published figures often diverge because other publishers pick different scopes, agent baskets, base years, and update cadences.

Some count post-treat spray services, others freeze ASPs, and a few model medical demand from bed stock, whereas Mordor tracks textile turnover.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.77 B (2025) | Mordor Intelligence | - |

| USD 10.98 B (2024) | Global Consultancy A | Excludes industrial and transit textiles, constant 2020 ASP |

| USD 10.70 B (2021) | Industry Association B | Older base year, linear growth, narrow geography |

| USD 16.00 B (2023) | Trade Journal C | Counts spray services and HVAC fabric coatings |

These contrasts show how our disciplined scope selection, dual-path modeling, and yearly refresh deliver a transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the antimicrobial textile market size in 2026?

The antimicrobial textile market size reached USD 14.29 billion in 2026 and is projected to hit USD 17.25 billion by 2031.

Which segment commands the highest antimicrobial textile market share?

Medical textiles led with 56.92% of 2025 revenue, reflecting stringent infection-control protocols in hospitals worldwide.

Which type is growing fastest?

Chitosan is forecast to expand at a 5.81% CAGR through 2031 thanks to favorable biocompatibility and regulatory status.

Why is polyamide gaining traction?

Polyamide fibers anchor silver ions within their matrix, retaining 94% antimicrobial activity after 100 washes, outperforming cotton finishes.

Page last updated on: