Hybrid Fabric Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

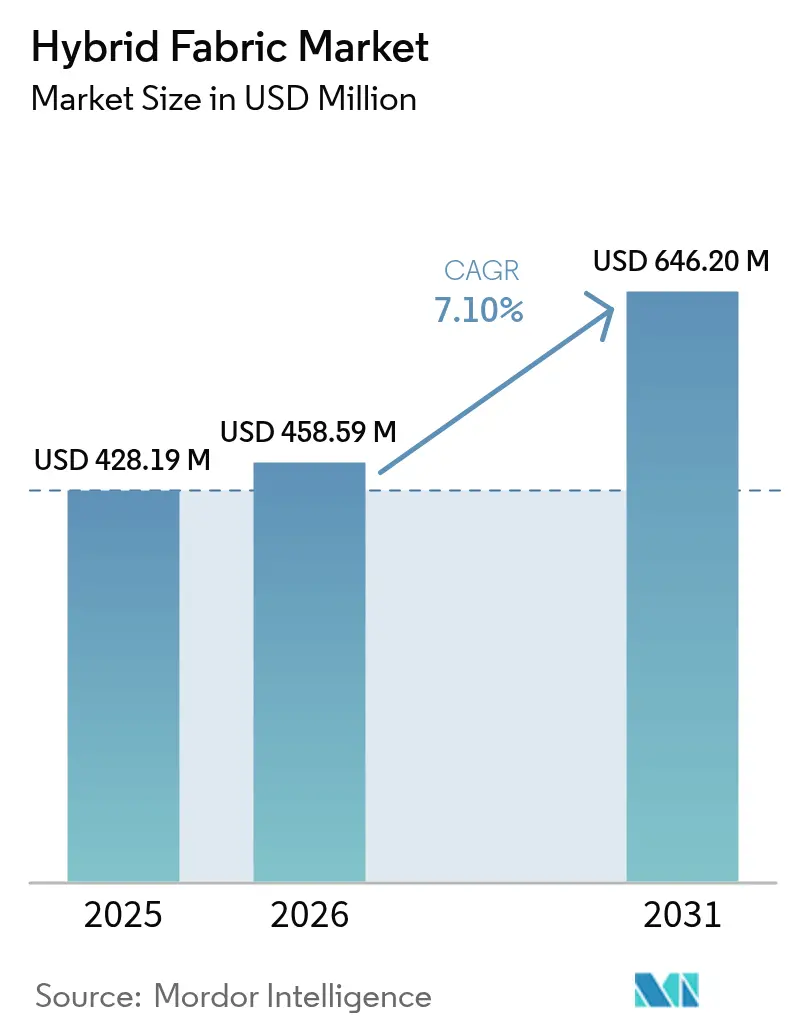

| Market Size (2026) | USD 458.59 Million |

| Market Size (2031) | USD 646.2 Million |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

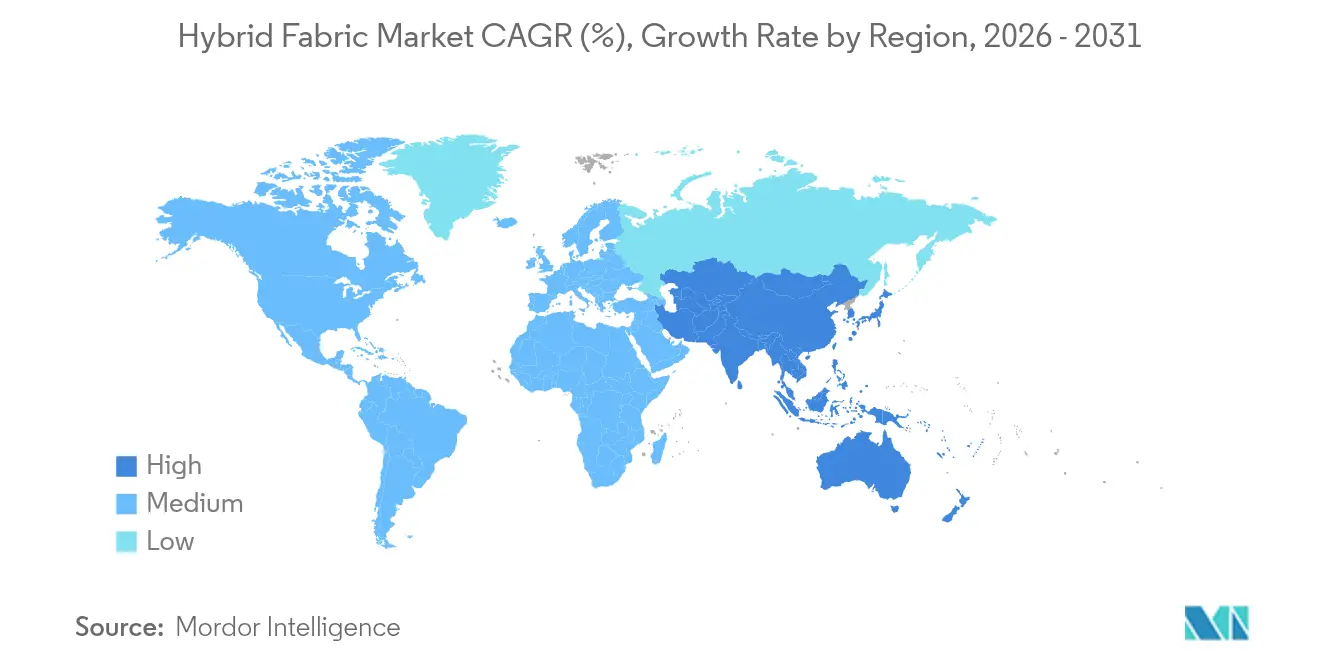

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

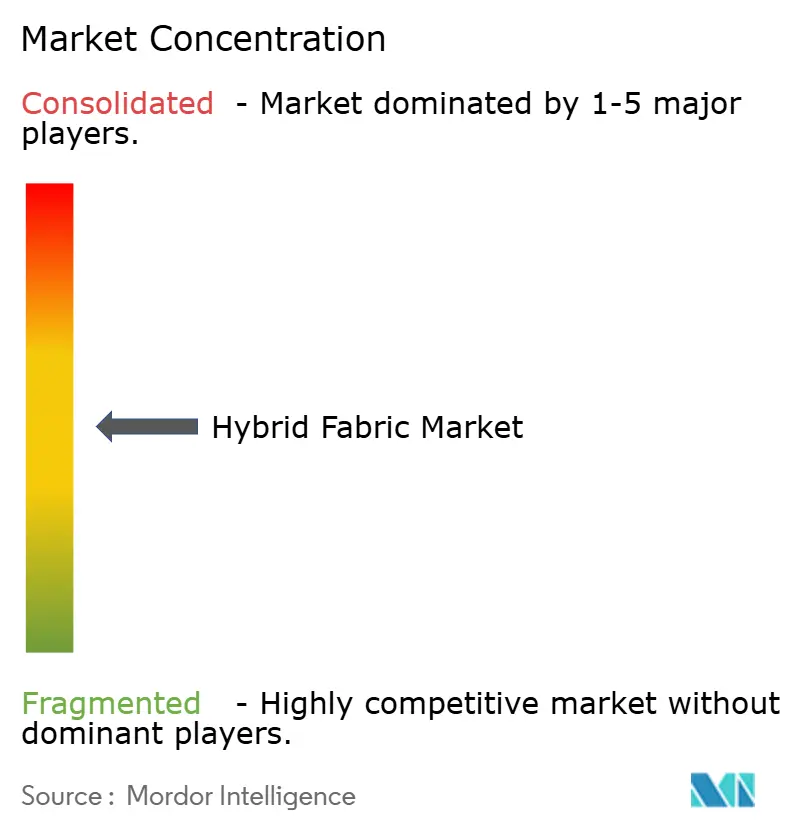

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Fabric Market Analysis by Mordor Intelligence

The Hybrid Fabric market size is expected to grow from USD 428.19 million in 2025 to USD 458.59 million in 2026 and is forecast to reach USD 646.2 million by 2031 at 7.10% CAGR over 2026-2031. This trajectory reflects how multi-material composites that merge distinct fiber chemistries are displacing single-fiber fabrics across mobility, energy, and aeronautics applications. Automakers are switching to hybrid reinforcements to hit weight‐reduction rules, turbine manufacturers need lighter blades to extend rotor length, and aircraft builders are specifying fabrics that offer higher fatigue resistance at lower thickness. Raw-material suppliers have responded with wider product portfolios, and process-equipment firms are automating lay-up, braiding, and winding steps to cut waste and cycle time. End-users are also valorizing recyclability, a factor that has pushed thermoplastic matrices into mainstream programs. Geographically, China, India, and South-East Asia have become the largest production hubs because of integrated supply chains and public incentives for clean energy components.

Key Report Takeaways

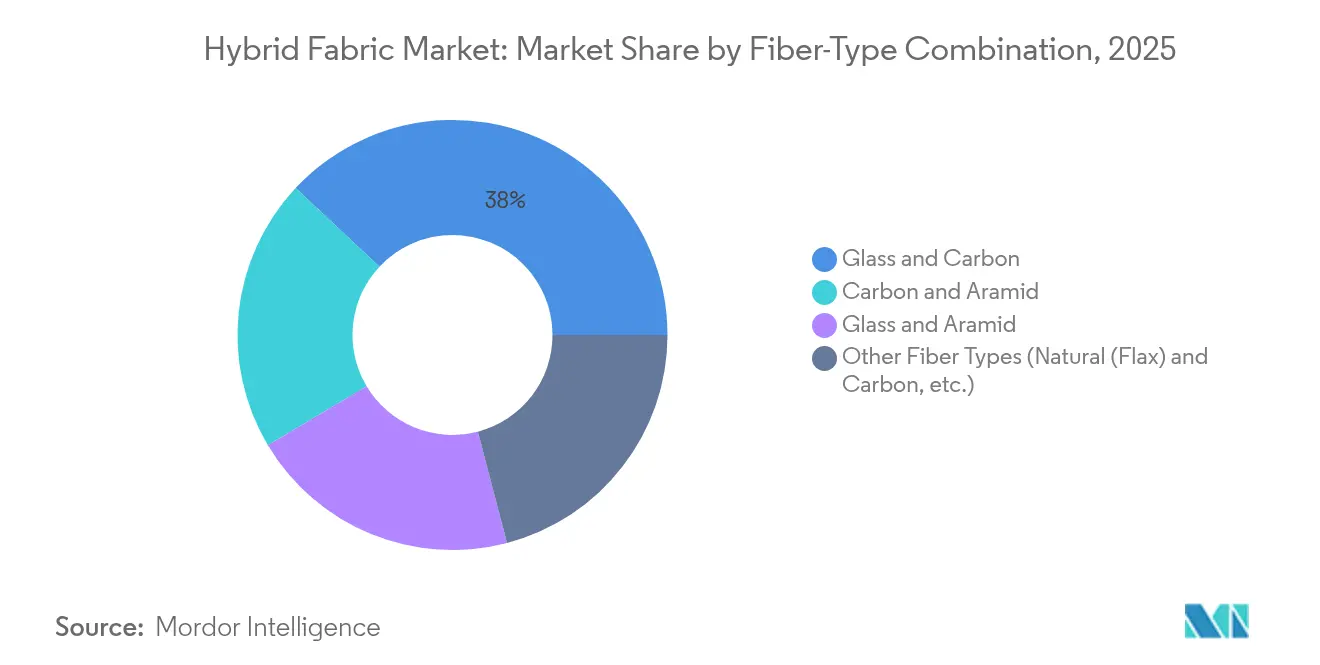

- By fiber-type combination, glass–carbon hybrids captured 38.02% of hybrid fabric market share in 2025, while other combinations that integrate natural fibers are projected to expand at a 9.05% CAGR to 2031.

- By resin matrix, thermoset systems held 61.88% of the hybrid fabric market size in 2025; thermoplastic systems are forecast to grow at an 8.71% CAGR through 2031.

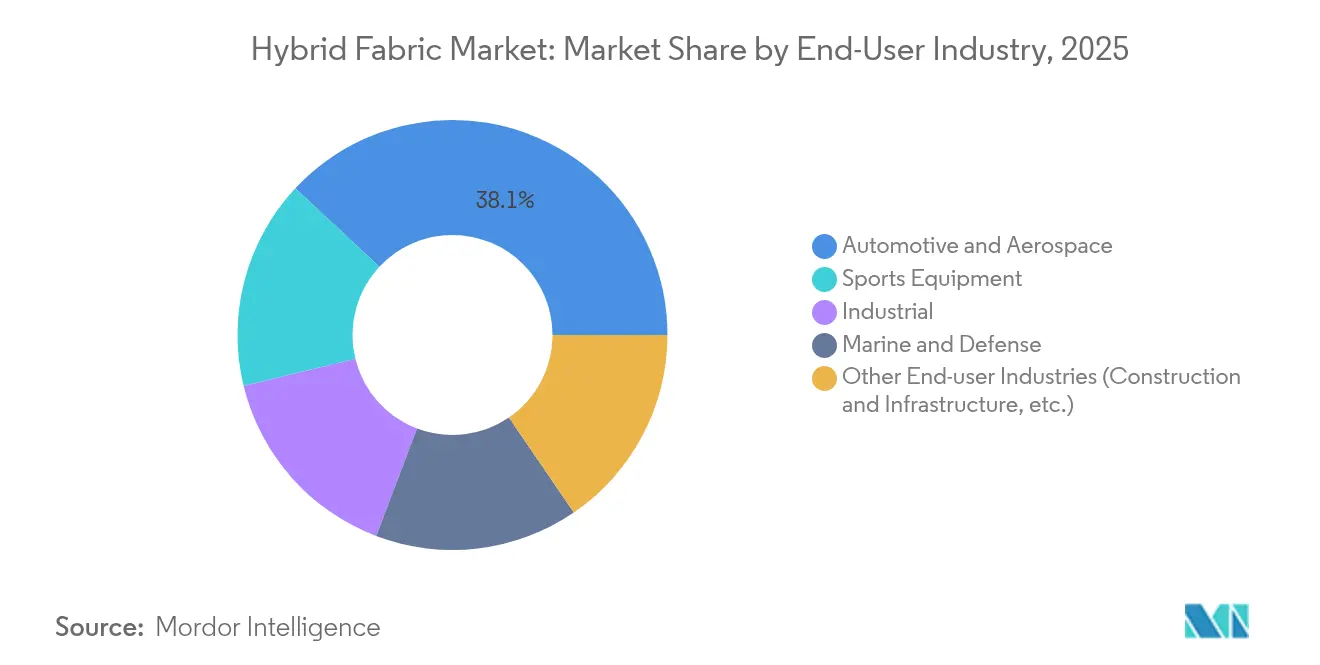

- By end-user industry, automotive and aerospace led with 38.05% revenue share of the hybrid fabric market in 2025; sports equipment is advancing at a 8.88% CAGR to 2031.

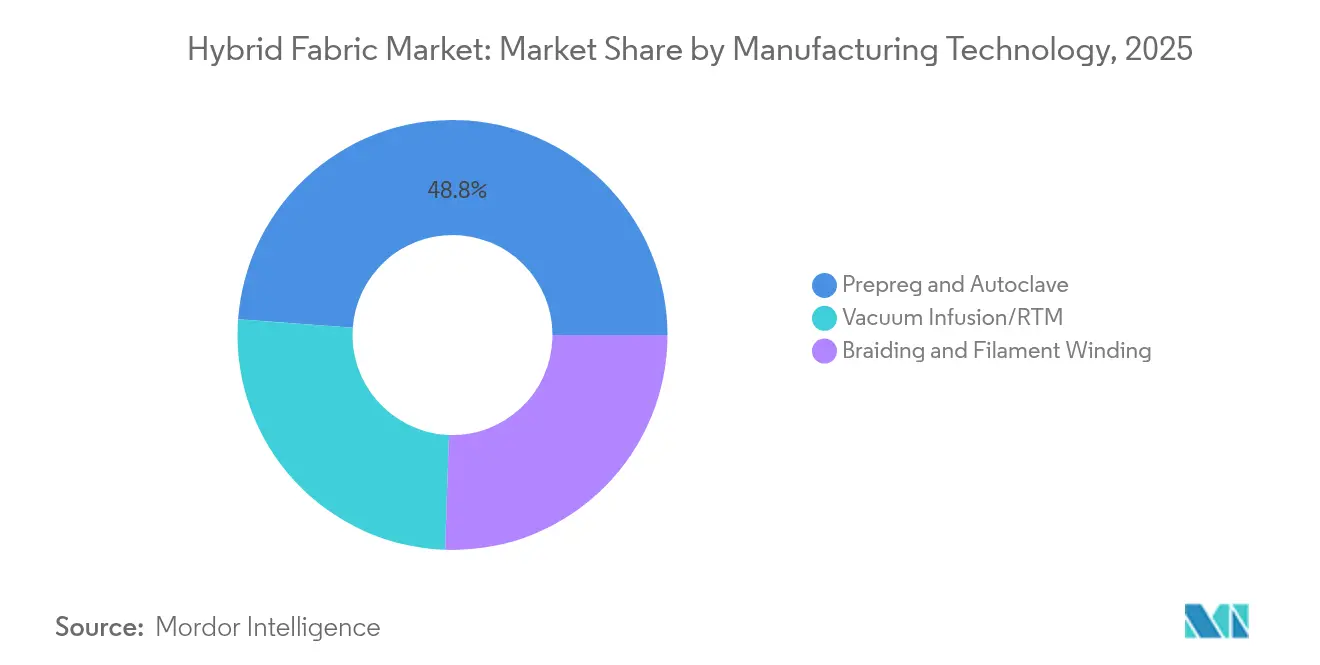

- By manufacturing technology, prepreg and autoclave processing accounted for 48.83% share of the hybrid fabric market size in 2025, whereas braiding and filament winding methods are expanding at an 8.73% CAGR.

- Regionally, Asia-Pacific dominated with 42.61% hybrid fabric market share in 2025, and the same region is projected to post the fastest 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hybrid Fabric Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive light-weighting demand for glass and carbon hybrids | +2.10% | Global, with concentration in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rise in demand from wind turbine blade manufacturing | +1.80% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Growing demand for high durability and thermal resistant fabrics | +1.30% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing applications for carbon fiber fabrics | +1.10% | Global, with aerospace concentration in North America | Short term (≤ 2 years) |

| Commercialisation of recycled-carbon and glass hybrid textiles | +0.90% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive Light-weighting Demand for Glass and Carbon Hybrids

Automotive OEMs are accelerating adoption of hybrid reinforcements to comply with the European Union rule that requires a 15% vehicle mass reduction by 2027. Ford’s composite C-brace for the Bronco Raptor shows how a glass–carbon fabric raises torsional rigidity while trimming weight. Battery-electric platforms use the same hybrid fabric market solutions inside structural battery enclosures that must insulate high-voltage packs and absorb crash energy. As OEMs migrate from steel to modular composite architectures, design studios gain freedom to mold complex ribs and nodes that were formerly welded, boosting demand for positional fiber placement technologies. The driver is most pronounced in China and Germany, where high electric-vehicle penetration coincides with public-sector fuel-economy targets.

Rise in Demand from Wind Turbine Blade Manufacturing

Blade makers need longer rotors to extract more energy per tower, yet aerodynamic loads soar with each additional meter. LM Wind Power solved this dilemma with an 88.4 meter blade that uses carbon–glass hybrid spar caps for stiffness without punitive mass. Offshore installations magnify the need for fatigue tolerance because salt spray and yaw cycles erode surface layers over a 25-year duty life. SAERTEX responded with an H-modulus glass fabric and self-adhesive non-crimp product family that cuts lay-up time by 30%[1]SAERTEX, “H-Modulus Glass Fabrics for Wind Blades,” saertex.com . Hybrid fabric market orders are therefore booked several quarters in advance, giving fiber suppliers visibility that supports capacity expansion in Jiangsu, Gujarat, and Schleswig-Holstein.

Growing Demand for High Durability and Thermal Resistant Fabrics

Hydrogen-powered aviation has realigned material specifications toward cryogenic toughness. Tanks that store liquid hydrogen at minus 253 °C rely on hybrid glass–carbon fabrics because the alpha-beta thermal expansion mismatch is lower than pure carbon solutions. Defense planners also look to the hybrid fabric industry for lightweight armor capable of defeating both fragments and overpressure; aramid–carbon stacks fill that niche on Future Long Range Assault Aircraft programs. Commercial shipbuilders see similar value in corrosion-immune hybrid laminates for hull inserts that cut life-cycle maintenance costs, broadening end-market diversity.

Increasing Applications for Carbon Fiber Fabrics

Carbon content inside hybrid constructions is spreading to high-volume consumer products. Running-shoe plates that pair carbon with glass reinforcements deliver spring rates that improve stride economy yet remain durable for 600 kilometers. Oak Ridge National Laboratory’s carbon nanofiber technology lifts tensile strength by 50% inside thermoplastic matrices and signals a route to aerospace-grade performance at automotive throughput. Infrastructure owners see parallel benefits in concrete reinforcement where recycled carbon fibers add flexural muscle and cut steel corrosion problems, expanding the hybrid fabric market beyond cyclical aerospace demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production & qualification costs | -1.40% | Global, particularly impacting North America and Europe | Short term (≤ 2 years) |

| Carbon-fiber supply-chain tightness | -0.90% | Global, with acute impact in Asia-Pacific | Medium term (2-4 years) |

| Absent recycling standards for multi-material fabrics | -0.70% | Europe leading regulatory development, global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production & Qualification Costs

Hybrid fabric production involves precise tension control, dual-fiber impregnation, and multi-stage cure cycles that raise capital needs. An aerospace qualification campaign can last five years and cost USD 15 million per fabric system according to NASA studies[2]NASA, “Composite Qualification Cost Study,” nasa.gov . Smaller mills therefore hesitate to enter the hybrid fabric market, restricting supplier diversity. Autoclave units add USD 10 million of fixed assets per line; out-of-autoclave methods exist yet still require complex tooling and data acquisition. These economics make price-sensitive segments, such as mid-class passenger cars, slower adopters despite evident weight savings.

Absent Recycling Standards for Multi-Material Fabrics

Disassembling co-cured fabrics that combine glass, carbon, and aramid fibers remains an unsolved challenge because burn-off temperatures differ and fiber lengths shorten during thermal reclamation. The European Commission is drafting end-of-life-vehicle rules that may classify unrecyclable composite content as landfill-restricted waste, creating compliance risk for the hybrid fabric industry. Until clear protocols appear, OEMs must rely on voluntary certification schemes, hindering mass adoption in time-critical consumer goods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber-Type Combination: Glass–Carbon Dominance Drives Cost–Performance Balance

Glass–carbon hybrids held 38.02% hybrid fabric market share in 2025, underscoring their sweet-spot blend of stiffness, fatigue endurance, and moderate raw-material cost. Turbine spar caps remain the flagship use case because carbon boosts bending rigidity while glass handles cyclic loading in the web region. Other combinations such as aramid-carbon address niche programs in ballistic armor and helicopter rotors where impact absorption is critical. Researchers at the University of Michigan increased flax-carbon modulus by 33% using a supercritical CO₂ treatment that cleans and roughens fiber surfaces, a result that has drawn interest from electric vehicle interiors. Market participants capitalize on this spectrum through modular product catalogs that offer the same weave in multiple fiber ratios. Pricing strategies reward volume commitments that stabilize loom scheduling and resin-mix forecasting. OEMs compare total-part costs rather than raw-fabric costs alone, validating the glass–carbon route whenever weight reduction brings downstream benefits like smaller propulsion units or simplified assembly hardware.

By Resin Matrix: Thermoplastic Systems Gain Traction Despite Thermoset Dominance

Thermoset chemistries accounted for 61.88% of hybrid fabric market size in 2025, with epoxy leading due to trusted flight-critical pedigrees and wide supplier availability. These resins cure at temperatures below 180 °C and accept accelerators that match production takt times. In contrast, thermoplastic matrices such as PEEK and PEKK need melt processing above 340 °C yet shorten press cycles to 3 minutes, a boon for high-volume structures. Thermoplastic scrap is also remeltable, giving fabricators a recycling pathway that reduces landfill fees. Adoption still faces tooling-price hurdles because matched-metal molds are required, and part-cool rates must be tuned to avoid crystallinity gradients. Nevertheless, battery enclosure projects at European gigafactories have locked in thermoplastic-hybrid laminates because heat resistance above 150 °C ensures integrity during thermal runaway events. Process lines increasingly feature induction heating and in-mold monitoring to secure repeatability, and these investments will cascade to marine deck panels and rail carbody shells during the forecast horizon.

By End-User Industry: Sports Equipment Emerges as Growth Leader

Automotive and aerospace commanded 38.05% of the hybrid fabric market in 2025. Automakers see a direct trade-off between every kilogram saved and battery pack capacity, an equation that pays off within premium vehicle segments. Aerospace OEMs lifted composite content on narrow-body programs to 55% by mass, and hybrid fabrics are integral to spars, ribs, and control surfaces that need localized stiffness variations. Sports and leisure products register the fastest 8.88% CAGR. Running-shoe companies incorporate carbon–glass plates in mid-soles, bicycle brands use hybrid lay-ups in crank arms for tuned flex, and archery manufacturers specify natural-carbon blends for limb performance. The hybrid fabric industry therefore benefits from influencer marketing that highlights performance gains, stimulating consumer willingness to pay premium prices. Marine, defense, and construction segments round out demand, each governed by tailored standards that increasingly factor in recyclability metrics.

By Manufacturing Technology: Automation Drives Braiding and Filament Winding Growth

Prepreg lay-up followed by autoclave consolidation captured 48.83% of hybrid fabric market size in 2025. Aerospace primes favor this route because porosity levels remain below 1% and fiber volume fractions reach 60%, two metrics essential for certification. Hexcel’s automated ply-forming cell now produces one preform per minute, cutting traditional hand-lay by 70%. Even so, braiding and filament winding are advancing at an 8.73% CAGR because their automated heads can place discrete bundles of different fibers in a single pass, perfect for pressure vessels and torque shafts. Robot-integrated winding equipment scales up to 10 meter parts and runs at 100 m/min fiber placement speed, reducing labor content to less than 5% of total transformation cost. Vacuum infusion and RTM processes mediate between cost and performance, operating at mold temperatures below 160 °C and using reusable silicone bags to slash consumables spending. Novel out-of-autoclave cures now achieve the same interlaminar shear strength as traditional autoclave parts when pressure is applied via smart bladders, aligning hybrid fabric market economics with mid-volume transport structures.

Geography Analysis

Asia-Pacific captured 42.61% hybrid fabric market share in 2025. China installed 75 GW of wind capacity in 2024 and ordered corresponding glass–carbon fabric volumes eighteen months ahead of blade production slots. Beijing’s Made-in-China 2025 plan earmarks advanced composite fabrication as a strategic pillar, which grants tax breaks to firms that localize value chains. India is following with a production-linked incentive scheme that reimburses 4% of free-on-board value for composite exports, prompting global tier-ones to twin plant footprints in Gujarat and Tamil Nadu. North America demonstrates strong revenue generation driven by its aerospace and defense hubs in Washington, Kansas, and Alabama. The HiCAM project at NASA Langley aims to quadruple composite airframe build rates, and Toray engineers supply customized prepreg systems that cure in under four hours. Canada cooperates through a national advanced materials supercluster that co-funds pilot lines, while Mexico strengthens the automotive base with duty-free composite parts under the USMCA, improving cost competitiveness even when raw fiber is imported. Europe maintains a robust position despite energy-price spikes. Offshore wind farms in the North Sea rely on hybrid spar caps shipped from German and Danish converters, and regional automakers have mandated an average 10% composite content for next-generation battery electric vehicles. Brussels also drives the regulatory frontier, with circular-economy directives forcing OEMs to confirm recycling pathways before product launch. This environment motivates R&D into natural fiber hybrids and low-temperature thermoplastic resins, ensuring Europe stays relevant on intellectual property even as production volumes drift toward Asia.

Competitive Landscape

The hybrid fabric market shows moderate fragmentation. Hexcel, Toray, and SAERTEX defend legacy aerospace and wind positions via proprietary fiber chemistries and pre-impregnation expertise. Newer entrants build niches in natural fiber and Z-axis reinforced fabrics. Owens Corning’s USD 755 million sale of its glass-fiber unit to Praana Group reshapes the upstream landscape and underscores the role of mergers in consolidating capacity. Solvay is divesting its process-materials division to Composites One to focus on high-margin specialty polymers, a move that frees capital for thermoplastic scale-up.

Competition increasingly rests on automation. Companies able to deliver closed-loop digital manufacturing win long-term agreements because defect traceability keeps warranty costs down. Another vector is supply-chain resilience; customers prefer vendors that run dual-continent plants to hedge political risk. Intellectual-property filings center on hybrid lay-up architectures and surface-treatment chemistries that improve interfacial bonding between dissimilar fibers. Venture investors have taken note, placing USD 13.5 million into Boston Materials to accelerate commercial roll-out of its Z-axis fiber technology.

White-space opportunities lie in recycled carbon blends and structural battery integration. Firms that combine vertical integration with specialized application engineering attract joint-development deals from OEMs looking to compress design cycles. Market leaders maintain share by locking customers into multi-year supply programs that include off-take guarantees for any scrap stream, aligning interests around sustainability metrics.

Hybrid Fabric Industry Leaders

Hexcel Corporation

SAERTEX GmbH & Co.KG

SGL Carbon

Solvay

Toray Hybrid Cord,Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Owens Corning has finalized an agreement to sell its glass fiber reinforcements business to Praana Group. The divested business is expected to contribute significantly to the hybrid fabric market by supporting advancements in lightweight and durable material solutions.

- April 2024: Teijin Limited divested its US subsidiary, Teijin Automotive Technologies North America, to Aurelius Private Equity. The deal highlights the rising importance of lightweight composite materials, including hybrid fabrics, in the automotive and transportation markets.

Global Hybrid Fabric Market Report Scope

The hybrid fabric market report includes:

| Glass and Carbon |

| Carbon and Aramid |

| Glass and Aramid |

| Other Fiber Types (Natural (Flax) and Carbon, etc.) |

| Thermoset (Epoxy, Polyester, Vinyl-Ester) |

| Thermoplastic (PP, PA, PEEK, PEKK) |

| Automotive and Aerospace |

| Industrial |

| Marine and Defense |

| Sports Equipment |

| Other End-user Industries (Construction and Infrastructure, etc.) |

| Prepreg and Autoclave |

| Vacuum Infusion/RTM |

| Braiding and Filament Winding |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Fiber-Type Combination | Glass and Carbon | |

| Carbon and Aramid | ||

| Glass and Aramid | ||

| Other Fiber Types (Natural (Flax) and Carbon, etc.) | ||

| By Resin Matrix | Thermoset (Epoxy, Polyester, Vinyl-Ester) | |

| Thermoplastic (PP, PA, PEEK, PEKK) | ||

| By End-User Industry | Automotive and Aerospace | |

| Industrial | ||

| Marine and Defense | ||

| Sports Equipment | ||

| Other End-user Industries (Construction and Infrastructure, etc.) | ||

| By Manufacturing Technology | Prepreg and Autoclave | |

| Vacuum Infusion/RTM | ||

| Braiding and Filament Winding | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hybrid fabric market?

The hybrid fabric market size reached USD 458.59 million in 2026 and is projected to grow to USD 646.2 million by 2031 at a 7.10% CAGR.

Which region leads the hybrid fabric market?

Asia-Pacific dominates with 42.61% hybrid fabric market share and is also the fastest-growing region with an 8.54% CAGR through 2031.

What end-user sector is expanding fastest?

Sports equipment is the fastest-growing end-user segment, advancing at a 8.88% CAGR due to premium consumer demand for performance materials.

Why are thermoplastic hybrid fabrics gaining popularity?

Thermoplastic systems offer shorter cycle times and recyclability advantages, driving their 8.71% CAGR despite thermoset dominance.

How is automation influencing hybrid fabric production?

Automated braiding and filament winding equipment cuts labor cost and improves repeatability, fueling an 8.73% CAGR for these technologies.

What is the key restraint facing the hybrid fabric industry?

High production and qualification costs remain the largest hurdle, reducing short-term adoption especially among small and mid-sized manufacturers.

Page last updated on: