Healthcare Fabrics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

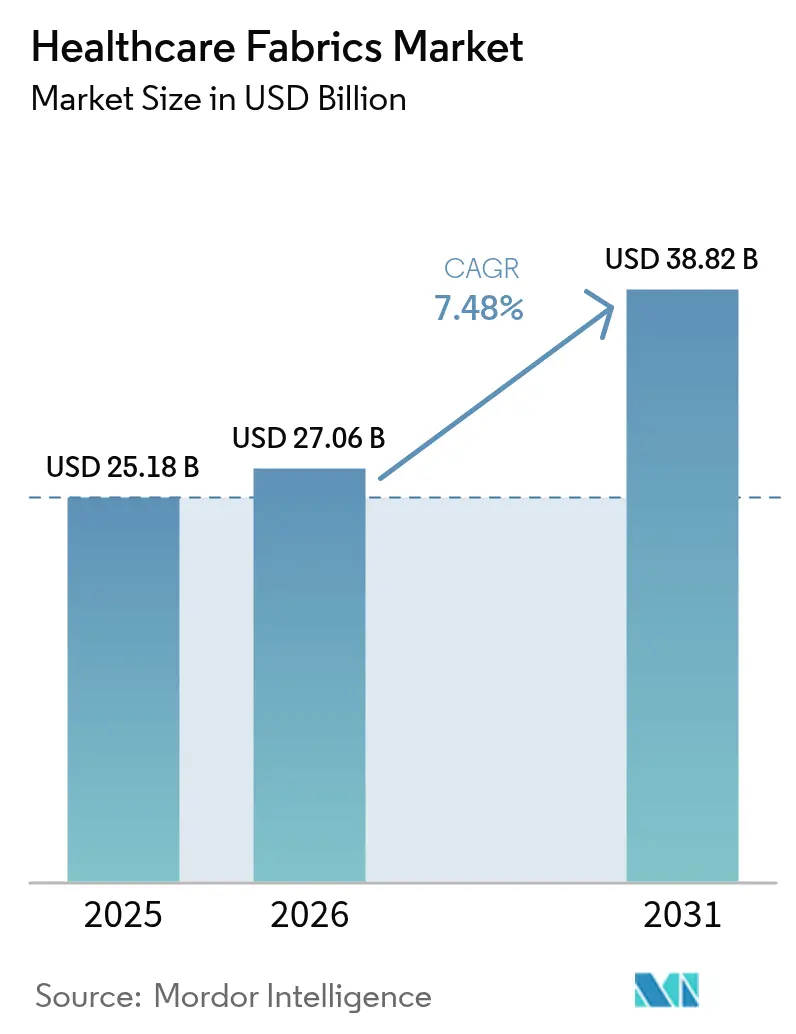

| Market Size (2026) | USD 27.06 Billion |

| Market Size (2031) | USD 38.82 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

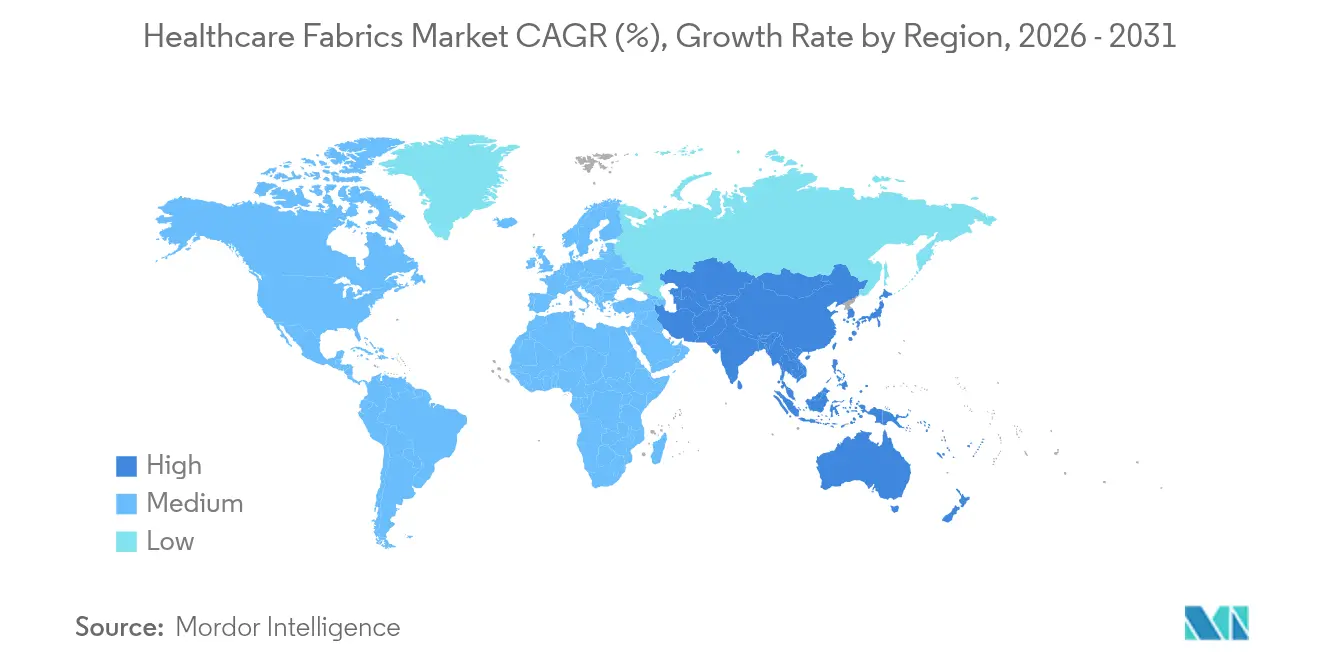

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Fabrics Market Analysis by Mordor Intelligence

The Healthcare Fabrics Market size was valued at USD 25.18 billion in 2025 and estimated to grow from USD 27.06 billion in 2026 to reach USD 38.82 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031). Rising hospital-acquired-infection (HAI) mitigation mandates, the pivot toward cellulose-based fibers, and the steady integration of sensor-enabled fabrics together widen the addressable base for the healthcare textiles market while helping providers meet infection-control and sustainability goals. Continuous material innovation, ranging from lyocell gauzes with more than 99% solvent recovery to zinc-nanocomposite barrier fabrics, allows manufacturers to offer premium products that combine durability with antimicrobial efficacy. Regulatory trends such as ISO 10993-1 biocompatibility testing in North America and upcoming PFAS restrictions in Europe amplify the need for compliant, high-performance textiles, reinforcing long-term demand. Meanwhile, Asia-Pacific’s capacity expansions and national health-insurance rollouts are tilting volume growth toward emerging economies, even as North American buyers remain early adopters of smart monitoring fabrics. Consolidation plays, illustrated by Berry Global’s merger that formed Magnera Corporation, underscore the strategic value of scale and vertical integration in a market where certification costs and R&D spending continue to rise.

Key Report Takeaways

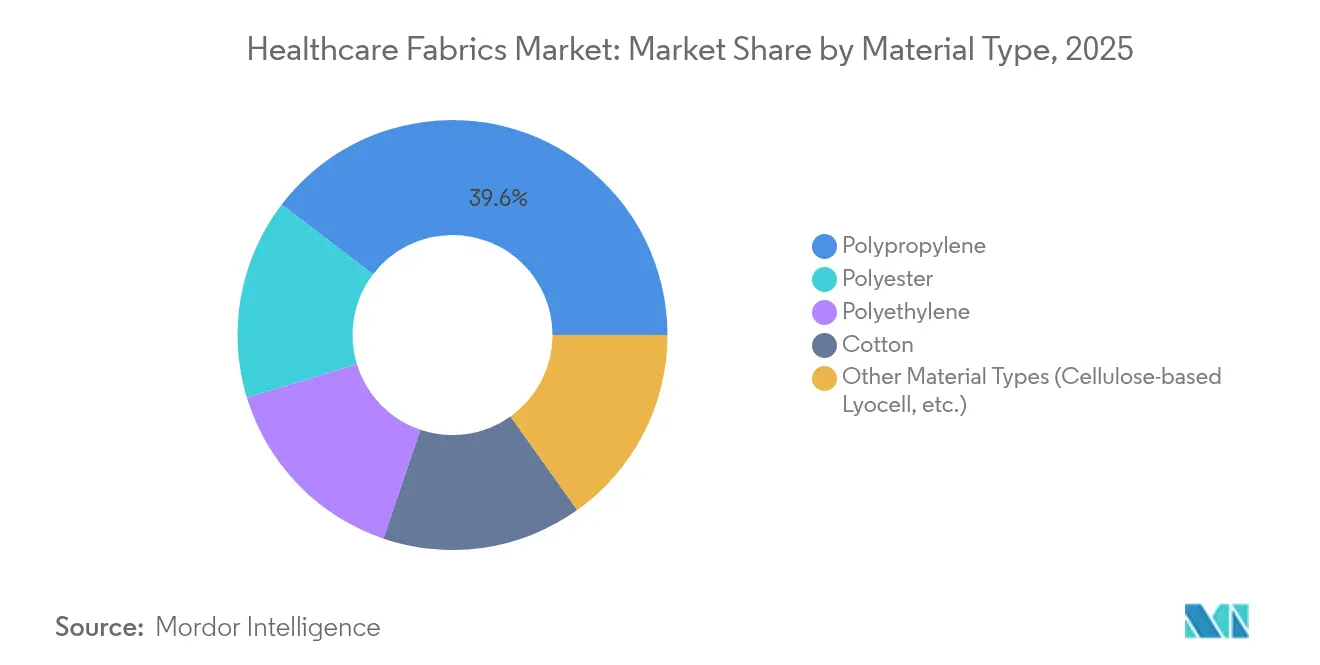

- By material, polypropylene captured 39.62% of the healthcare fabrics market share in 2025, whereas other material types are projected to expand at a 9.26% CAGR through 2031.

- By fabric type, non-wovens held 62.15% revenue share in 2025; knitted fabrics represent the fastest-growing category with a 9.06% CAGR to 2031.

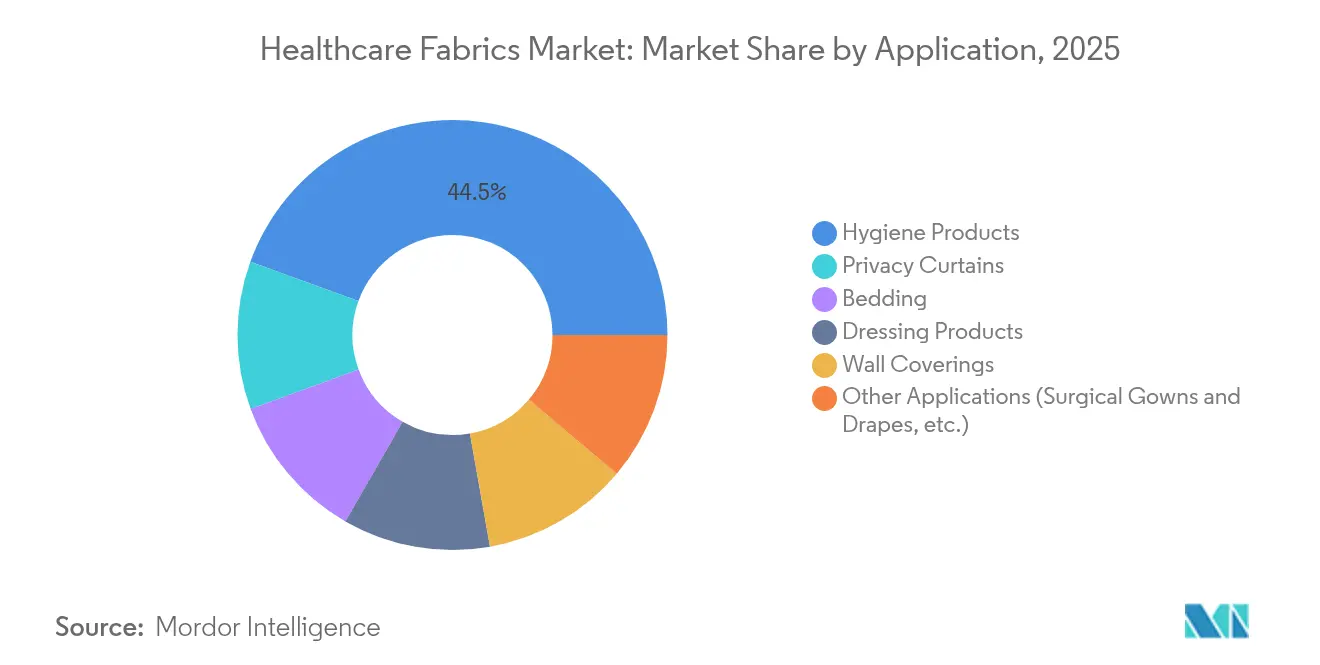

- By application, hygiene products accounted for 44.47% of the healthcare fabrics market size in 2025, while other applications, such as surgical gowns and drapes are forecast to grow at 8.92% CAGR to 2031.

- By geography, North America led with 37.68% revenue share in 2025; Asia-Pacific is advancing at a 9.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Fabrics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand in Developing Nations | +2.1% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Increasing Use of Cellulose Fibres in Healthcare | +1.8% | Global, with EU leadership | Long term (≥ 4 years) |

| Hospital-acquired-infection (HAI) Reduction Mandates | +2.3% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Growing Adoption of Antimicrobial & Antiviral Finishes | +1.9% | Global | Medium term (2-4 years) |

| Surge in Smart-textile Integration for Patient Monitoring | +1.7% | North America, EU, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand in Developing Nations

Fast-growing health-insurance programs are stimulating hospital construction from Jakarta to Johannesburg, lifting annual procurement budgets for antimicrobial drapes, breathable uniforms, and disposable Personal Protective Equipment (PPE). India’s technical-textiles sector, valued at USD 19 billion, has used 100% Foreign Direct Investment (FDI) allowances and the National Technical Textiles Mission to boost domestic capacity, slashing import dependence for specialized fibers [1]Invest India, “Technical Textiles: Next Growth Avenue for Indian Manufacturing,” investindia.gov.in. Personal Protective Equipment (PPE) scaling during the pandemic proved local suppliers can meet surge requirements, a lesson now informing strategic stockpiling policies. Manufacturers that localize production gain duty benefits and shorter lead times, positioning them to capture the incremental volumes generated by middle-class healthcare utilization. While price sensitivity remains high, tender documents increasingly reference International Organization for Standardization (ISO), American Society for Testing and Materials (ASTM), and European Union Medical Device Regulation (EU MDR) standards, signalling an upgrade path toward higher-margin, certified products.

Increasing Use of Cellulose Fibres in Healthcare

Lyocell and similar regenerated-cellulose fibers are displacing synthetics in wound dressings, patient clothing, and sustainable drapes because they provide hypoallergenic performance, superior moisture management, and a benign end-of-life profile. Solvent recovery rates above 99% in the N-Methylmorpholine N-oxide (NMMO) process lower environmental footprints, satisfying forthcoming European Union (EU)-wide textile eco-design rules. Antimicrobial post-treatments using chitosan derivatives, quaternary ammonium salts, or silver nanoparticles now bond effectively to cellulose matrices without degrading tensile strength. The Lenzing Group’s International Sustainability & Carbon Certification (ISCC) PLUS-certified sites in Luxembourg and Richmond generate Lyocell under 100% renewable electricity, offering hospitals Scope 3 emission reductions for procurement scorecards. As Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) bans tighten, cellulose fibers stand out for safe-chemistry compliance and traceable sourcing, reinforcing their long-run growth momentum.

Hospital-Acquired-Infection Reduction Mandates

The Centers for Disease Control and Prevention estimates that compliant textile-hygiene protocols can cut pathogen transmission by more than 70%, a figure driving adoption of durable antimicrobial linens and launderable privacy curtains. Updated FDA QMSR rules effective February 2026 align with ISO 13485:2016 and increase documentation requirements for medical-textile functional testing. Research shows polyhexamethylene biguanide (PHMB)-treated uniforms retain more than 99% efficacy against Staphylococcus aureus even after 50 industrial wash cycles, giving facilities confidence in long-term protection. Hospitals facing reimbursement penalties for HAIs are embedding antimicrobial performance clauses in linen contracts, accelerating replacement of untreated cotton with specialty blends that deliver both infection control and patient comfort.

Surge in Smart-Textile Integration for Patient Monitoring

Sensor-laden fabrics are migrating from pilot projects into mainstream procurement lists as care models shift toward chronic-disease monitoring. Massachusetts Institute of Technology (MIT)’s 3DKnITS platform embeds pressure sensors capable of detecting gait anomalies, enabling remote physiotherapy assessments. Energy-harvesting yarns engineered at the University of Waterloo convert body heat into power, eliminating battery-replacement cycles and lowering maintenance costs. Hospitals and home-health providers see value in textiles that capture vital signs passively, feeding analytics platforms that triage alerts and optimize staffing. Although certification pathways remain nascent, early adopters in rehabilitation and eldercare settings are validating clinical utility and Return on Investment (ROI), paving the way for scaled orders by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Consumer Awareness | -1.2% | Global, more pronounced in developing markets | Medium term (2-4 years) |

| Volatile Petro-polymer Raw-material Prices | -1.8% | Global | Short term (≤ 2 years) |

| Inadequate Disposal Infrastructure for Single-use Fabrics | -0.9% | Global, acute in developing nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Consumer Awareness

Procurement managers in lower-income regions often equate textile quality with thread-count rather than antimicrobial durability or sensor accuracy, slowing upgrade cycles. The absence of harmonized smart-textile standards complicates value assessments, while limited case-study dissemination keeps total-cost-of-ownership benefits under-recognized. Industry associations are expanding training modules, but uptake varies widely. Until consistent labelling and performance-tier frameworks emerge, bulk buyers may default to lowest-capex options, curbing near-term penetration of premium fabrics.

Volatile Petro-Polymer Raw-Material Prices

Polypropylene and polyester spot prices rose 18% in 2024 amid geopolitical disruptions, pressuring thin operating margins for non-woven converters. Medical device makers now allocate 3–5% of revenue to supply-chain risk mitigation, including multi-sourcing and hedging instruments [2]Medical Technology, “Supply Chain Challenges Intensify for Device Makers,” medical-technology.nridigital.com. Although cellulose-based inputs offer price stability, retrofitting melt-spinning lines to handle them demands multi-million-dollar capex, slowing material-mix shifts. Frequent raw-material cost spikes temper short-run growth, especially in price-sensitive hygiene-product segments where contracts are renewed annually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polypropylene Faces Sustainability-Driven Challenges

Polypropylene sustained a 39.62% revenue lead in 2025 thanks to low resin cost, melt-blown versatility, and hydrophobicity suited for disposable barrier products. Yet the healthcare textiles market is witnessing a pivot as other material types, such as cellulose-based competitors, grow 9.26% annually on the back of bio-compatibility and PFAS-free credentials. Europe’s forthcoming PFAS ban effective January 2025 raises compliance hurdles for legacy fluorochemical finishes, nudging buyers toward lyocell and chitosan-treated fabrics. Several United States hospital groups have published sourcing roadmaps that target a 30% procurement mix shift toward bio-based inputs by 2030, creating sizeable headroom for cellulose adoption. Polyester continues to service reusable privacy curtains and high-wash-count scrubs, but energy-recovery upgrades in dyeing plants are helping mitigate its carbon intensity. Niche volumes of polyethylene are preserved for micro-porous laminates offering high moisture-vapour transmission rates in critical-care drapes. Cotton’s presence recedes because moisture retention increases pathogen load, prompting its substitution with blends that embed antimicrobial chemistries. Start-up innovations such as enzymatic bleaching and low-temperature reactive dye formulas point to an incremental greening of legacy fibers, but their scalability against cellulose’s closed-loop process remains uncertain.

By Fabric Type: Non-Woven Leadership Spurs Continuous Innovation

Non-wovens controlled 62.15% of 2025 revenue, with melt-blown and spunbond processes scaling to billions of masks, gowns, and absorbent pads during recent public-health emergencies. The segment still grows 9.06% a year as filtration-efficiency upgrades and electrostatic-charge retention additives extend the functional life of single-use garments, improving value perception. Magnera Corporation's 46-plant footprint supports agile fulfillment, allowing hospital groups to build strategic reserves without inflating inventory-holding costs. Hybrid composites that fuse spunbond strength with melt-blown filtration layers continue to advance, yielding fabrics that balance breathability with ASTM-F2100 Level-3 fluid resistance. Woven textiles cling to niches demanding durability and launderability, such as privacy curtains replaced on 9- to 12-month cycles. Their refurbishment viability aligns with carbon-reduction targets, although laundering costs and energy intensity trim their advantage. Knitted fabrics are carving a share in patient-comfort apparel; integrating elastomeric filaments boosts stretch while maintaining pressure-redistribution in anti-decubitus bedding. Advances in circular knits with embedded silver yarns have demonstrated at least a 4-log bacterial kill even after 100 laundry cycles, creating opportunities in rehabilitation centers that require both infection control and long-term wearability.

By Application: Hygiene Products Maintain Lead Amid Smart Integration

Hygiene products, such as adult incontinence briefs, feminine pads, and disposable under-pads, retained 44.47% of 2025 revenue, a dominance explained by demographic aging and heightened infection-prevention adherence. Tender documents now specify super-absorbent cores with at least 600% saline uptake, pushing suppliers toward high-purity SAP and pulp composites. Brand owners differentiate through odor-control chemistries and dermatologically tested topsheets, lifting unit value even in competitive bid environments. Privacy curtains and wall-covering textiles migrate to antimicrobial fabrics treated with quaternary ammonium or silver-zeolite finishes that deliver 5-log reductions against Methicillin-Resistant Staphylococcus Aureus (MRSA) after 12 months in situ. Bedding solutions integrate phase-change microcapsules to stabilize patient skin temperature, improving sleep quality in geriatric wards and burn units.

Geography Analysis

North America took 37.68% revenue in 2025, underpinned by rigorous Food and Drug Administration (FDA) oversight that mandates ISO-10993-1 testing for skin-contact devices, including antimicrobial drapes and smart textiles. Providers in the United States prioritize infection-control efficacy and therefore adopt premium cellulosic or fluorine-free barrier fabrics despite higher unit prices. Supply-chain resiliency remains a board-level concern; Premier's 2023 survey showed 75% of executives expect disruptions to persist for at least two more years, prompting multi-sourcing strategies and near-shoring initiatives. Cardinal Health's AI-enabled 340,000 sq ft Fort Worth distribution hub exemplifies investment in logistics automation that shortens lead times and increases fill-rate guarantees.

Asia-Pacific is advancing at a 9.13% CAGR through 2031 as governments pour capital into hospital infrastructure and incentivize domestic technical-textile production. India's USD 19 billion technical-textiles base enjoys duty credits and 100% FDI allowances, capturing export orders and substituting imports. China is expanding its share of bandage and gauze exports and directing R&D grants toward antimicrobial and smart fabrics under the 14th Five-Year Plan, thereby reinforcing its position as a global manufacturing hub for healthcare textiles. Indonesia's Jaminan Kesehatan Nasional (JKN) national insurance scheme is accelerating hospital bed additions, driving higher procurement of privacy curtains and reusable bedding. Medical-tourism hotspots such as Thailand and Malaysia are specifying advanced gowns and smart compression garments to attract international patients, fostering demand for higher-margin technologically advanced textiles. Europe posts steady mid-single-digit growth, propelled by the European Environment Agency's 2024 PFAS risk assessment that places textiles on a path toward stricter chemical controls. Healthcare systems are actively replacing fluorinated barriers with bio-based coatings, a switch that benefits cellulose and polyethylene terephthalate-based fabrics treated with eco-certified chemistries. The European Green Deal's eco-design requirements are spurring investment in recyclable mono-material non-wovens and take-back logistics. South America and Middle East & Africa trail in market penetration but display pockets of rapid adoption: Brazil's private hospitals now pilot antimicrobial privacy curtains to curb nosocomial infections, while Saudi Arabia's Vision 2030 hospital projects include specifications for smart bedding that monitors patient vitals.

Value Chain Analysis

The healthcare fabrics value chain starts upstream with petrochemical and bio-based feedstocks (PP, PE, PET, and regenerated cellulose), along with medical-grade additives and finishes used for barrier performance, absorbency, and antimicrobial or antiviral properties. These inputs are then converted into fibers and fabrics (spunbond, meltblown, spunlace, needle-punch, knitting, and weaving), and finally assembled into end products such as hygiene components, dressings, gowns and drapes, and privacy curtains. Downstream activities include sterilization and packaging, distributor and group-purchasing logistics, and procurement by hospitals, clinics, and home-health providers, followed by post-use disposal or, for reusable textiles, take-back, laundering, and sterilization loops.

March 2026 reporting also points to the chain’s sensitivity to energy and feedstock logistics. Disruptions around the Strait of Hormuz have been linked to higher naphtha-linked costs, which is translating into rising PP, PE, and PET prices globally, and India-based manufacturers have faced a reported PP shortage and sharp price increases alongside elevated power and fuel constraints. These shocks tend to strengthen the case for multi-sourcing resin and nonwoven inputs, validating alternate materials including cellulose-based options, and tightening collaboration between fabric producers, converters, and healthcare buyers on performance specifications such as wash durability, biocompatibility, and sterility assurance, to limit revalidation when materials shift.

Competitive Landscape

The Healthcare Fabrics Market is fragmented owing to the presence of many players, yet niche innovators continue to secure specialized contracts. Berry Global’s spin-off and merger with Glatfelter that formed Magnera Corporation generated a USD 3.6 Billion non-woven giant with 46 manufacturing sites across four continents, leveraging cross-plant scheduling to slash lead times for high-demand gowns. DuPont sustains differentiation via material science, earning ISCC PLUS certification for Tyvek plants and guaranteeing 100% renewable electricity usage across United States operations. Freudenberg’s EUR 100 million acquisition of Heytex expands coated-textile capability, reinforcing its barrier-fabric portfolio and providing entry into technical-film laminates.

Healthcare Fabrics Industry Leaders

Amcor plc

Kimberly-Clark Worldwide, Inc.

Freudenberg SE

DuPont

Ahlstrom

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity and capability additions are clustering around higher-value niches and sustainability-led substrates, which creates room for suppliers that can combine certified performance with more resilient regional supply. In Europe, URGO Group’s January 2026 announcement to invest EUR 60 million in a new factory in Andrezieux-Boutheon, France, focused on medical compression textiles, points to continued pull-through for specialty knitted or elastic structures and skin-contact materials validated for medical use. In North America, Arvind Advanced Materials’ May 2026 acquisition of a majority stake in Dalco-GFT supports additional needle-punched nonwoven specialty fabric capacity in the Carolinas, improving faster local response for technical nonwovens used across healthcare and related industrial specifications.

Technology shifts in high-volume consumables are also creating opportunities, particularly for formats positioned as plastic-free or with reduced chemical use in wipes and dressing-related substrates. Kruger Nonwovens’ May 2026 order of an ANDRITZ Wetlace hybrid line for a new facility in Trois-Rivieres, Quebec, is aimed at plastic-free and chemical-free sustainable wipes, with production scheduled for 2028. On the innovation front, 2026 publications on advanced electrospun and nanofiber structures, including multi-stimuli responsive PLA-based nonwovens and PVDF nanofiber wound-dressing concepts, expand the development pipeline for next-generation wound care and patient-contact textiles, but adoption depends on scalable manufacturing, skin-contact safety validation, and procurement acceptance tied to measurable clinical and operational outcomes.

Recent Industry Developments

- July 2026: Arbex, created by Kimberly-Clark and Suzano, commenced operations as an independent global tissue and hygiene company, incorporating assets previously under Kimberly-Clark’s International Family Care and Professional business. The shift reshapes sourcing and manufacturing footprints for large-volume hygiene substrates and finished goods, influencing demand patterns for nonwovens and related healthcare fabric inputs across multiple regions.

- October 2025: Amcor launched AmSecure thermoformed trays and rollstock as a recycle-ready alternative to PETG for medical and pharmaceutical packaging applications. The platform supports healthcare customers pursuing mono-material and recyclability goals, and it tightens requirements for compatible barrier layers and sterilization-ready materials across the packaging-to-device supply chain.

- November 2024: Berry Global Group, Inc. finalized its merger with Glatfelter Corporation, combining Berry’s Health, Hygiene, and Specialties Global Nonwovens and Films business to form Magnera Corporation. The enlarged nonwovens footprint increases scale in meltblown and spunbond supply, improving responsiveness for PPE, hygiene components, and other healthcare fabric-intensive categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers fabrics made for and used in healthcare and medical environments, where performance needs such as hygiene, barrier protection, comfort, and durability shape purchase decisions at both facilities and product makers.

Scope exclusions: We exclude non-medical home textiles and general apparel fabrics that are not intended, tested, or marketed for healthcare use cases.

Segmentation Overview

- By Material

- Polypropylene

- Polyester

- Polyethylene

- Cotton

- Other Material Types (Cellulose-based Lyocell, etc.)

- By Fabric Type

- Woven

- Non-Woven

- Knitted

- By Application

- Privacy Curtains

- Wall Coverings

- Hygiene Products

- Dressing Products

- Bedding

- Other Applications (Surgical Gowns & Drapes, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting basic boundaries and terminology for healthcare fabrics, then aligns those boundaries with how production and use show up in public statistics. We review sources such as US Census Bureau manufacturing data, UN Comtrade trade statistics, Eurostat industry tables, the US FDA database and guidance notes for medical products, and US Centers for Disease Control and Prevention publications on infection prevention.

To keep assumptions practical, we also look at company annual reports, investor presentations, product catalogs, and reputable press coverage to understand where demand is rising, and where product mix is shifting toward nonwoven and barrier-heavy materials. Select paid subscriptions are used only for company financials and intelligence, patent lookups, and shipment level import and export checks, which helps us cross-check directional trends before speaking with experts. These sources are illustrative, and many other public references were also used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work is used to test what the desk data cannot fully explain, especially price movement, mix shifts across nonwoven versus woven, and what buyers treat as a healthcare fabric versus an adjacent textile. We speak with executives, product managers, sourcing leads, and operations teams across major regions so our assumptions on volumes, average pricing, and application mix stay consistent with how contracts are executed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 40% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 18% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

For sizing, we use a top-down approach that combines production and trade data with healthcare use intensity to reconstruct the demand pool for medical and healthcare fabric applications, then converts it to value using application-level pricing ranges. We corroborate totals with selective bottom-up approximations, such as sampled supplier and converter revenue patterns, channel checks, and volume multiplied by average selling price for a few high-visibility applications.

Key model inputs include hospital and clinic activity growth, procedure and admission trends that influence consumption of hygiene and dressing products, the share shift toward nonwoven formats, and price movements linked to polypropylene, polyester, and cotton feedstocks. Regulatory and product-performance signals are also tracked because they can change mix, such as infection control requirements and material restrictions that push substitution. Forecasts are built using scenario analysis, where short-term drivers like capacity additions and raw material cycles are separated from longer-term adoption of higher-performance and smart monitoring fabrics. When direct volume visibility is limited for niche applications, we apply conservative penetration rates and then re-check them through interviews before finalizing the series.

Data Validation & Update Cycle

Before sign-off, model outputs are checked against independent indicators such as trade flows, raw material price direction, and reported utilization or capacity commentary from public filings, and then any large variances are investigated. Outliers are reviewed in more than one internal step, and we re-contact sources when a key assumption like application mix or pricing changes beyond a reasonable range. Reports are refreshed annually, and interim updates are triggered when material events occur, such as new compliance rules, major capacity changes, or sharp feedstock price swings. Right before delivery, a fresh analyst pass is completed so clients receive the most up to date view that matches current market conditions.

Mordor Intelligence's Healthcare Fabrics Market Size Compared With Other Published Estimates

Published market values for healthcare fabrics can differ even when the topic name looks the same, because firms draw the line differently on what counts as healthcare use and how they treat applications that sit close to general textiles. Differences also show up when inflation, currency conversion timing, and product mix changes are applied in different ways.

Trade-flow checks for nonwoven inputs, combined with hospital activity signals and application-level pricing ranges, are the evidence used to keep the Mordor Intelligence 2025 estimate tied to the real consumption pool for hygiene products, bedding, and facility-focused textile needs. A few studies appear to apply a wider definition that blends in more general technical textile demand, or they project faster price escalation without re-checking it against raw material trends and procurement behavior. Update cadence matters too, because a model that does not refresh mix assumptions after regulatory and infection control changes can drift from what buyers are actually ordering.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.18 B (2025) | |

| Industry Publisher A | USD 22.01 B (2025) | This estimate appears more conservative on pricing and near-term demand, and it may lean more on broad macro growth without clearly reconciling application mix shifts across nonwoven formats and facility textiles. |

| Global Publisher B | USD 20.91 B (2024) | The year basis differs, and the scope seems to blend additional application buckets like implantable and device-related categories, which can change how fabric value is counted and how average prices are applied across the market. |

The spread in values is mostly explained by definition boundaries, the year used for the starting point, and how pricing and mix are carried forward into the forecast. By keeping scope tied to healthcare fabric use cases and re-checking the main drivers with observable signals, our number stays traceable to inputs that can be reviewed and repeated.

Key Questions Answered in the Report

What is the current value of the healthcare textiles market?

The healthcare textiles market size is USD 27.06 billion in 2026 and is projected to reach USD 38.82 billion by 2031 at a 7.48% CAGR.

Which material dominates healthcare textile production today?

Polypropylene leads with 39.62% market share in 2025, primarily for disposable gowns and masks, though cellulose-based fibers are the fastest-growing alternative.

Why are antimicrobial finishes so important in hospital linens?

Health Care-Associated Infections (HAI) reduction mandates show that treated fabrics can cut pathogen transmission by more than 70%, lowering liability and improving patient outcomes

Which region is growing fastest for healthcare textiles demand?

Asia-Pacific is expanding at a 9.13% CAGR through 2031, driven by large-scale hospital builds, medical tourism, and supportive manufacturing policies.

Are smart textiles commercially viable yet?

Pilot deployments of sensor-embedded gowns and wound dressings demonstrate clinical utility and are moving toward scaled procurement as certification pathways mature.

Page last updated on: