Pakistan Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

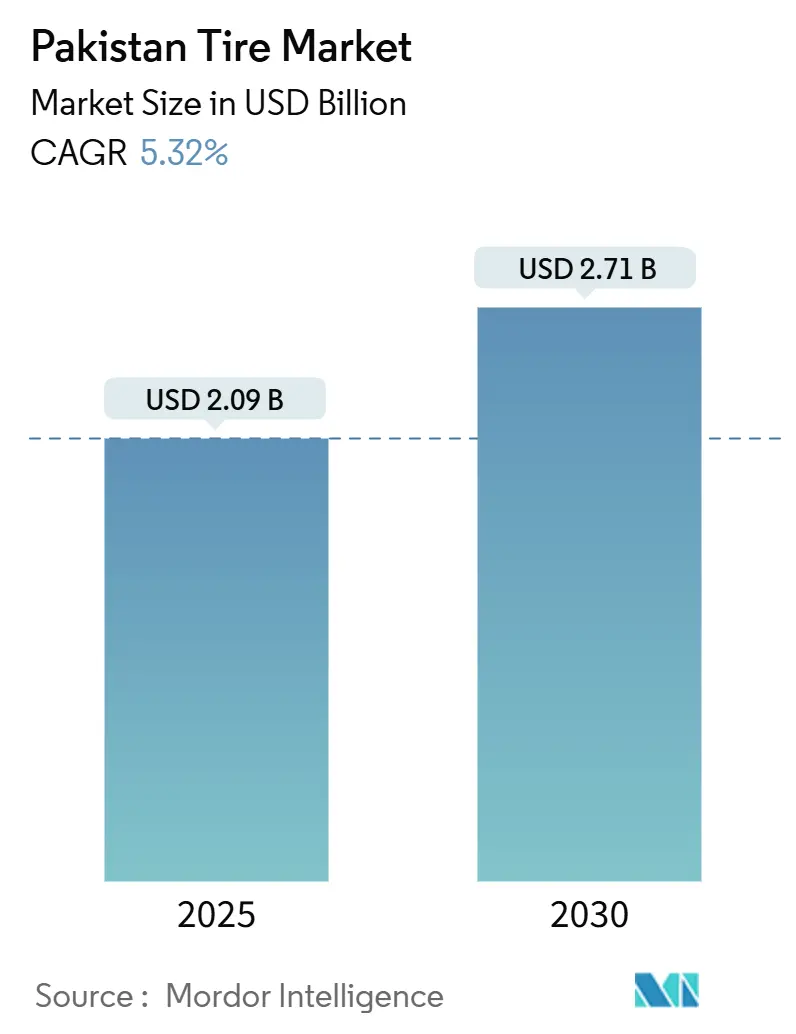

| Market Size (2025) | USD 2.09 Billion |

| Market Size (2030) | USD 2.71 Billion |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Tire Market Analysis by Mordor Intelligence

The Pakistan tire market size stood at USD 2.09 billion in 2025 and is forecasted to climb to USD 2.71 billion by 2030, advancing at a 5.32% CAGR. Persistent demand from replacement channels, the build-out of freight corridors under the China-Pakistan Economic Corridor (CPEC), and gradual normalization of light-vehicle production underpin this expansion. Commercial and two-wheeler fleets absorb the bulk of volumes, while radial-technology adoption, stricter provincial inspection rules, and localization incentives steer manufacturers toward efficiency-oriented product lines. Input-cost headwinds remain pronounced because natural rubber and electricity prices swing widely, yet price-sensitive buyers continue to opt for organized aftermarket outlets that balance quality and affordability. Punjab’s outsized road network, Sindh’s import gateway role, and Khyber Pakhtunkhwa’s logistics corridors collectively shape provincial demand, ensuring that the Pakistan tire market retains its long-term growth profile even when domestic vehicle output fluctuates.[1]Zafar Haque & Saba Anwar, “Transports and Logistics,” Pakistan Institute of Development Economics, pide.org.pk

Key Report Takeaways

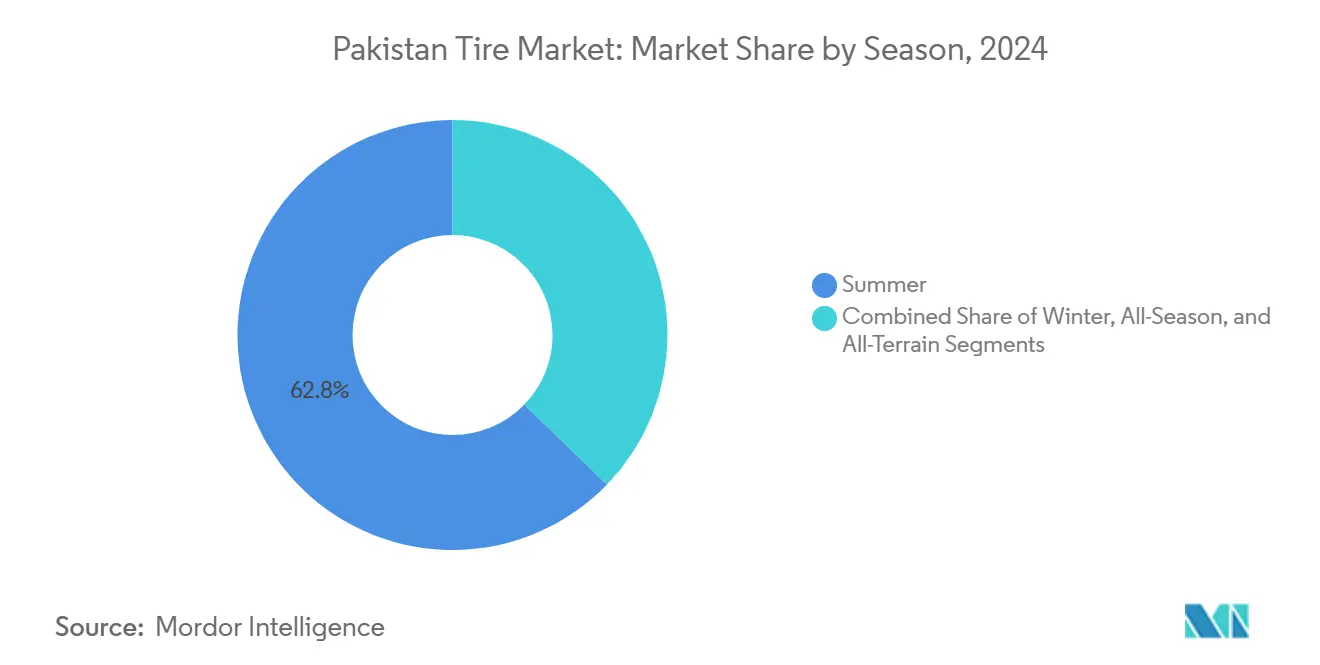

- By season, summer tires led with 62.76% of the Pakistan tire market share in 2024; winter tires are projected to register a 6.50% CAGR to 2030.

- By tire design, radial products held 75.95% of the Pakistan tire market share in 2024, while non-pneumatic designs are poised for a 6.56% CAGR through 2030.

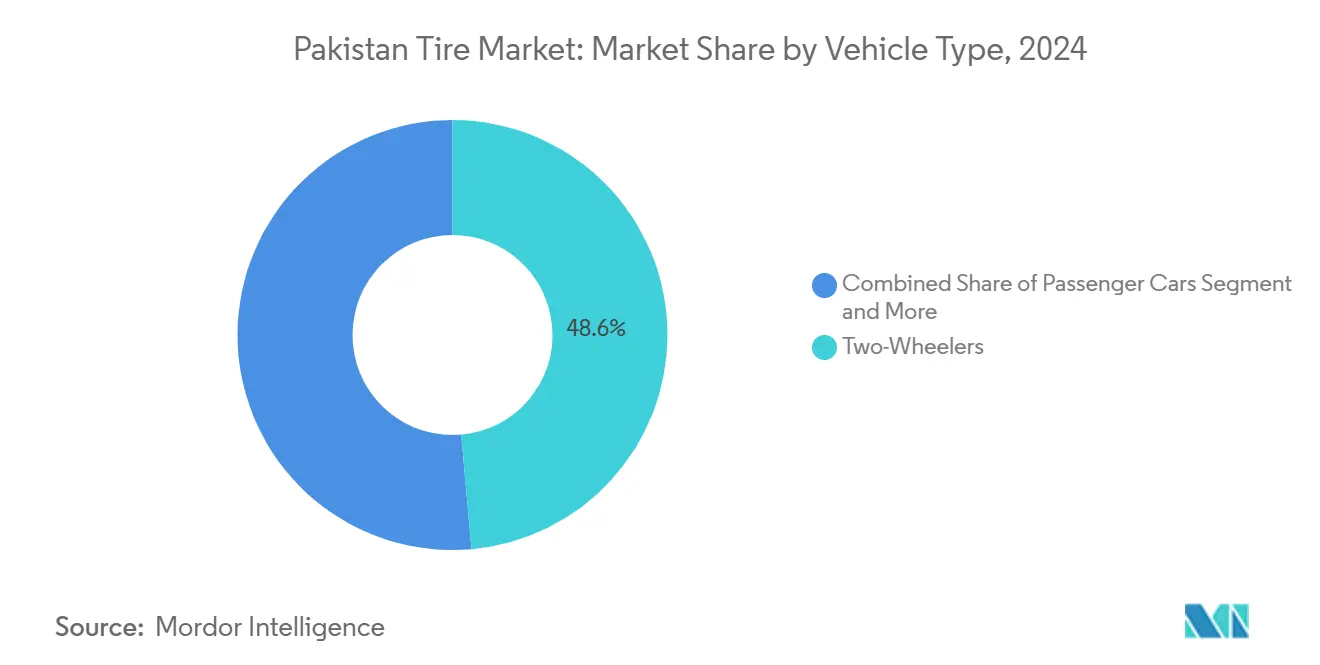

- By vehicle type, two-wheelers accounted for 48.59% of the Pakistan tire market share in 2024; passenger cars are forecasted to expand at a 7.38% CAGR over 2025-2030.

- By application, on-road categories captured 80.02% of the Pakistan tire market share in 2024, whereas off-road tires are estimated to post a 5.89% CAGR during the outlook period.

- By end user, the aftermarket commanded 74.91% of the Pakistan tire market share in 2024; OEM demand is expected to rise at a 6.97% CAGR through 2030.

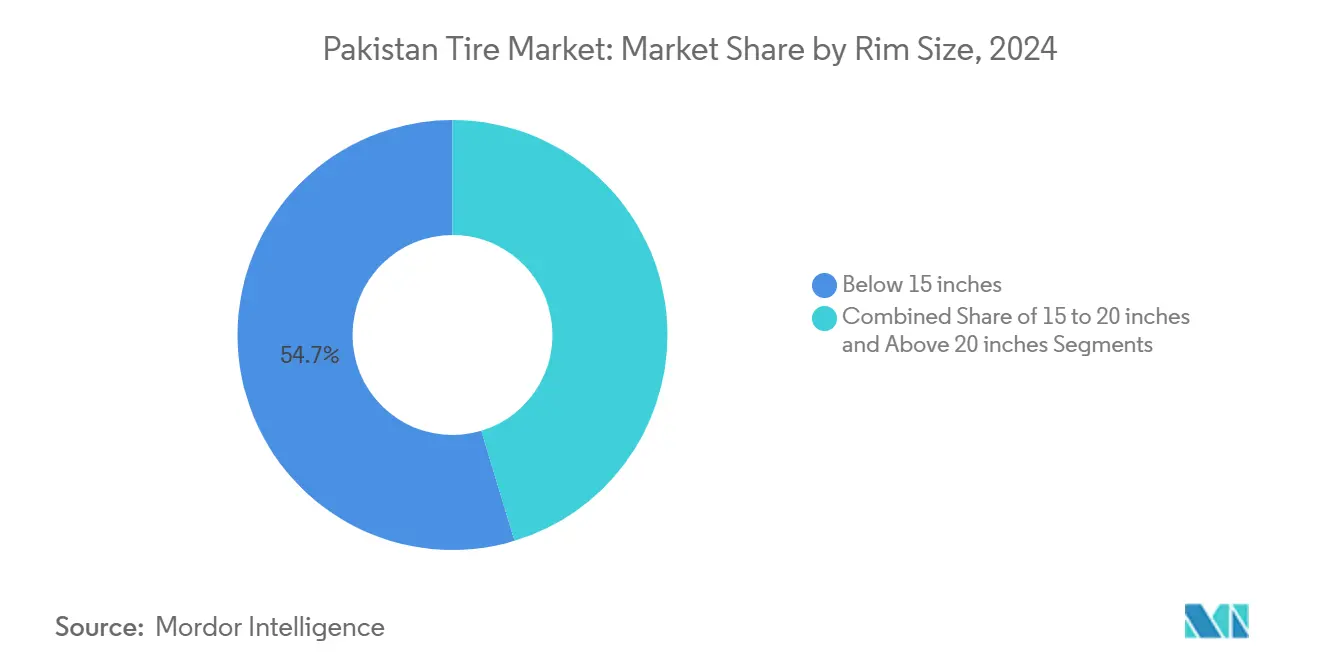

- By rim size, below 15-inch tires represented 54.66% of the Pakistan tire market share in 2024; above 20-inch fitments are projected to advance at a 7.77% CAGR.

- By propulsion, internal-combustion vehicles kept 91.12% of the Pakistan tire market share in 2024; battery-electric models are projected to grow at a 14.33% CAGR to 2030.

- By province, Punjab captured 43.92% of the Pakistan tire market share in 2024, while Khyber Pakhtunkhwa is estimated to post the fastest CAGR of 5.69% to 2030.

Pakistan Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Parc Expansion | +1.8% | Punjab, Sindh, Khyber Pakhtunkhwa | Medium term (2-4 years) |

| Infrastructure Mega-Projects | +1.5% | Punjab, Khyber Pakhtunkhwa, Balochistan | Long term (≥ 4 years) |

| Higher Import Tariffs | +1.2% | Punjab, Sindh | Medium term (2-4 years) |

| E-Commerce Delivery Fleets | +0.9% | Punjab, Sindh | Short term (≤ 2 years) |

| OEM Localization Mandates | +0.7% | Punjab, Sindh | Long term (≥ 4 years) |

| Tire Retail and Service Chains | +0.4% | Punjab, Sindh, Khyber Pakhtunkhwa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Motor-Vehicle Parc Expansio

Pakistan’s registered vehicle base rose in 2024, ensuring that replacement demand remains decoupled from cyclical factory output swings. Aging cars, motorcycles, and trucks translate into shorter tire-change intervals, while dense city traffic accelerates tread wear. Punjab’s large fleet amplifies aftermarket volumes, and service networks proliferate to capture recurring business. Even when 2023 production sank to a 20-year low, wholesalers reported steady sell-through, validating the resilience of the Pakistan tire market. Over the medium term, fleet expansion drives ancillary services such as retreading and alignment to strengthen ecosystem revenues.

Infrastructure Mega-Projects (CPEC, Motorways)

CPEC’s USD 65 billion as of 2022, spans 2,700 km of freight corridors and is projected to add 100,000 heavy trucks to the road by 2030. Construction phases lift immediate demand for off-the-road tires, while completed highways boost commercial-fleet mileage, raising replacement cycles. Special Economic Zones embedded along the route encourage depot and service-center clusters, anchoring long-term sales. Harsh climate differentials from desert heat to alpine cold favor premium specifications with reinforced casings, nudging the Pakistan tire market toward higher value units. Logistics firms increasingly link tire procurement to uptime guarantees, deepening partnerships with organized distributors.[2]“Cross-Border Logistics Between Pakistan and China,” IEEE-SEM, ieeesem.com

Higher Import Tariffs Encouraging Local Manufacturing

Successive duty revisions on completely built-up vehicles and tire consignments push assemblers to localize component sourcing. Tariff protection shields domestic producers from low-priced imports, improves capacity-utilization rates, and attracts foreign direct investment into greenfield plants. Provincial authorities complement fiscal measures with anti-smuggling checkpoints, restricting grey-channel flows that once dominated border trade. As compliant manufacturers regain volume, scale efficiencies translate into competitive pricing, reinforcing the tariff-localization cycle. Sustained capacity additions broaden product portfolios, supporting the Pakistan tire market’s transition from bias to radial and specialty designs.

Growing Two-Wheeler E-Commerce Delivery Fleets

Rapid urban delivery growth stimulates specialized motorcycle-tire demand tuned for high-frequency stop-start usage. Funding inflows to electric scooter platforms accelerate this shift because electric drivetrains require low-rolling-resistance compounds to preserve battery range. Provincial EV incentives, from purchase subsidies to battery-swap infrastructure, reinforce the trajectory. Branded dealerships offer subscription-based tire-and-service bundles to fleet operators, locking in predictable volumes. Over time, performance benchmarks set by delivery companies spill into consumer two-wheeler segments, raising expectations for durability and safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility | -1.4% | Punjab, Sindh | Short term (≤ 2 years) |

| Grey-Channel/Used-Tyre Imports | -1.1% | Punjab, Sindh, Khyber Pakhtunkhwa, Balochistan | Medium term (2-4 years) |

| Working-Capital Crunch | -0.8% | Punjab, Sindh | Short term (≤ 2 years) |

| Limited Domestic Testing | -0.3% | Punjab, Sindh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Natural-Rubber and Energy-Price Volatility

Raw-material costs account for roughly 60% of a tire’s ex-factory value, so a surge in global rubber quotations erodes producers’ margins quickly. Local electricity tariffs, frequently revised to close fiscal gaps, add another layer of unpredictability. Smaller manufacturers struggle to hedge input costs or pass them on to buyers accustomed to discount channels. Resulting cash-flow stress slows capacity upgrades, delays product launches, and narrows the price spread between compliant and non-compliant imports. Energy-efficiency retrofits and procurement consortia emerge as coping mechanisms, yet volatility remains a periodic drag on the Pakistan tire market.

Grey-Channel / Used-Tire Imports Undercutting Prices

Smuggled and second-hand tires reportedly satisfy nearly half of the national demand, depressing price realization for compliant producers. Border topology, document falsification, and under-invoicing schemes feed the parallel supply chain, exposing consumers to safety risks and depriving authorities of tax revenue. Provincial spot inspections dismantle select shipments, but enforcement gaps persist across rugged frontiers. Persistent undercutting discourages multinationals from introducing premium ranges, limiting technology transfer. Industry associations lobby for harsher penalties and digital tracking, yet sustained reductions in illicit trade will depend on coordinated customs and law-enforcement action.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Summer Dominance Mirrors Climate Reality

Summer products captured a commanding 62.76% of the Pakistan tire market share in 2024, underscoring how Pakistan’s predominant hot-weather profile marginalizes winter-specific compounds. Extended high-temperature exposure, monsoon moisture, and abrasive asphalt surfaces steer consumers toward tread patterns optimized for heat dissipation and wet grip. Winter lines, while nascent, notch a 6.50% CAGR as tourism and trade in high-altitude zones expand travel during colder months.

All-season ranges gain traction among logistics fleets that shuttle across climatic zones, balancing inventory simplicity with adequate performance. Meanwhile, all-terrain and mud-terrain SKUs tap into construction and agricultural demand suppressed in traditional passenger-vehicle segments. Incremental growth in northern hill stations and off-road recreation may narrow the share gap but will not overturn summer leadership throughout the forecast horizon.

By Tire Design: Radial Technology Sets the Benchmark

Radials controlled 75.95% of the Pakistan tire market share in 2024, establishing their role as the efficiency standard in the Pakistan tire market. Longer tread life, lower rolling resistance, and fuel-economy benefits resonate with fleet operators eager to tame operating costs amid fuel-price volatility. Bias construction remains attractive for vintage tractors and selected industrial equipment where sidewall stiffness outweighs mileage.

Non-pneumatic concepts, though starting from a low base, log a 6.56% CAGR as mining, military, and material-handling buyers value puncture immunity. Regulatory scrutiny by the Pakistan Standards and Quality Control Authority is gradually phasing out sub-standard biased imports, further tilting demand toward radials. Over time, higher-silica tread compounds and advanced belt designs percolate from passenger to commercial catalogs, expanding the performance envelope.

By Vehicle Type: Two-Wheelers Anchor Volume Momentum

Motorcycles and scooters delivered 48.59% of the Pakistan tire market share in 2024, mirroring their status as Pakistan’s principal mobility mode. Dense urban traffic, ride-hail services, and expanding two-wheeler delivery fleets require frequent tire replacement due to high mileage and load cycles. The Pakistan tire market size for passenger-car fitments, however, is forecast to accelerate at a 7.38% CAGR as macro-stability and localized assembly improve new-car affordability.

Light and heavy commercial segments absorb CPEC-induced mileage gains, especially along Lahore–Islamabad and Karachi–Sukkur motorways. Specialty niches agricultural, mining, and motorsport post small but profitable volumes given limited competition. OEM localization policies gradually diversify product mix toward higher-diameter radials compatible with modern suspension geometries.

By Application: On-Road Usage Dominates but Off-Road Picks Up Pace

On-road categories held an 80.02% of the Pakistan tire market share in 2024, a direct corollary of Pakistan’s freight-skewed road infrastructure, where trucks carry 96% of cargo. Expressway expansion trims transit times yet amplifies tire wear because fleets clock higher daily mileage. Despite dominance, the off-road segment grows at a 5.89% CAGR, fueled by quarrying, power-plant construction, and large-scale irrigation works.

Demand for extra-deep treads, cut-resistant compounds, and reinforced sidewalls lifts the value mix in off-road catalogs. Hybrid usage vehicles, such as tipper trucks that shuttle between construction sites and paved arteries, spur crossover tread patterns balancing traction with fuel economy. As renewable-energy installations spread to wind-rich corridors, specialized crane tires join the off-road roster.

By End User: Aftermarket Outweighs OEM but the Gap Narrows

The Aftermarket segment accounted for 74.91% of the Pakistan tire market share in 2024, reflecting Pakistan's aging vehicle fleet, limited new vehicle production capacity, and consumer preference for independent tire service providers over dealer networks. Organized chains leverage procurement scale to offer warranty-backed fitments and ancillary services such as nitrogen inflation and computerized balancing, capturing urban footfall.

The OEM channel, however, charts a 6.97% CAGR on the back of production recovery and localization mandates that embed tire contracts within domestic value chains. Manufacturers diversify by introducing dual-channel SKUs, factory-grade compounds sold under distinct aftermarket labels, blurring traditional boundaries. As assembly plants secure just-in-time supply, domestic makers invest in compound-mixing automation to comply with evolving OEM durability benchmarks.

By Rim Size: Smaller Diameters Still Reign

Below 15-inch dimensions comprised 54.66% of the Pakistan tire market share in 2024, reflecting Pakistan's vehicle mix, dominated by motorcycles, small cars, and commercial vehicles that utilize smaller wheel diameters for cost efficiency and durability in challenging road conditions. Smaller wheels with higher-profile tires provide better protection against pothole damage and rough road surfaces that characterize much of Pakistan's road network. High-profile sidewalls cushion pothole impacts common on feeder roads, prolonging wheel integrity.

Yet, above 20-inch sizes notch a 7.77% CAGR as premium SUVs and crossovers filter into urban garages, and high-deck buses adopt larger wheels to accommodate disc brakes. Mid-range 15-to-20 inch sizes align with emerging mid-market sedans and pickup trucks aimed at fleet buyers, gradually diluting the small-diameter stranglehold. Styling preferences among younger consumers also nudge the market toward alloy wheels that pair with wider, lower-aspect-ratio tires.

By Propulsion: Combustion Keeps Lead while Electrics Sprint

Internal-combustion drivetrains retained 91.12% of the Pakistan tire market share in 2024 as gasoline and diesel infrastructure remain ubiquitous. Battery-electric units, though niche, sprint at 14.33% CAGR thanks to fiscal incentives, lower running costs, and the government’s 30% adoption target. Electric-specific tread patterns focus on low rolling resistance and load distribution to offset battery mass.

Electric vehicle adoption creates distinct tire requirements, including optimized rolling resistance to maximize battery range, enhanced load-carrying capacity to accommodate battery weight, and specialized compounds to handle electric motors' instant torque delivery characteristics. Hybrid and fuel-cell categories stay experimental but offer upside once charging networks mature. Local producers explore silica-rich compounds and aero-optimized sidewalls for EV models, signaling technology transfer beyond combustion-centric catalogs.

Geography Analysis

Punjab captured 43.92% of the Pakistan tire market share in 2024, owing to its share of the national road grid, cluster of three leading assembly plants, and dense freight corridors that funnel agricultural and consumer goods toward Karachi port. Even during currency-driven production stoppages in 2023, replacement sales in Lahore and Faisalabad remained resilient because motorcycles and light trucks kept urban commerce moving. A broad dealer footprint and periodic-inspection mandates spur short replacement cycles, cementing Punjab’s leadership in the Pakistan tire market.

Sindh ranks second, anchored by Karachi’s status as the country’s commercial and maritime hub. Port throughput channels imported carcasses and raw materials to inland factories, while Karachi’s sprawling ride-hail and delivery fleets demand high-frequency tire changes. Industrial estates surrounding Hyderabad and Nooriabad bolster commercial-tire consumption. Authorities have tightened port-scanner protocols to curb under-invoiced imports, yet price competition from grey-channel tires persists, tempering margins for compliant distributors.

Khyber Pakhtunkhwa, positioned along the CPEC’s northern section, is the fastest-growing province at 5.69% CAGR. Road-widening projects and border-trade facilities near the Khunjerab Pass swell heavy-truck traffic, increasing demand for robust steer and drive-axle radials. Mining concessions in Swat and Dir lift off-the-road consumption, while orchard mechanization in the Malakand division supports agricultural-tractor tires. Balochistan remains the smallest market but gains niche traction from Gwadar port expansion and mineral extraction in Chagai, albeit offset by security restrictions that constrain retail-network growth.

Competitive Landscape

The Pakistan tire market exhibits high concentration that reflects decades of local manufacturing experience and established distribution networks. The entrenched distribution networks, OEM linkages, and familiarity with local homologation norms erect entry barriers for latecomers. Nevertheless, a robust demand still leaks to grey-channel imports that dodge duties and undercut prices, forcing incumbents to emphasize product provenance and after-sales warranties.

Strategic investment tilts toward capacity debottlenecking and radial-line modernization rather than cutting-edge smart-tire technologies. General Tyre completed a rubber-mixing upgrade in 2024 to lift radial output, while Panther Tyres added a new curing press line aimed at 2-wheeler radials. Servis Tyres unveiled the Starlux brand in July 2025, signaling a push into mid-premium segments with higher silica content tread compounds.

International brands pursue fleet-service contracts instead of volume-centric retail strategies. A leading Southeast Asian manufacturer secured a multi-year agreement with a Karachi-based logistics operator that requires on-time delivery guarantees and periodic performance audits. Meanwhile, electric-mobility startups source bespoke low-rolling-resistance tires under private-label agreements, introducing small yet potentially disruptive volumes as EV adoption rises. As regulatory audits tighten, compliance-certified sellers leverage their status to win municipal bus and utility-fleet tenders, gradually shifting price competition toward quality differentiation.

Pakistan Tire Industry Leaders

General Tyre & Rubber Co. of Pakistan Ltd.

Panther Tyres Ltd.

Service Industries Ltd.

Diamond Tyres Ltd.

Ghauri Tyre & Tube (Pvt.) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Servis Long March introduced the Starlux brand, pledging advanced materials and safety features aimed at midsize passenger-car and SUV owners.

- December 2024: The International Finance Corporation and Pakistani banks agreed to lend USD 50.2 million to Armstrong ZE and its UAE parent for a greenfield tire plant in Sindh.

- December 2024: Huasheng Rubber and Ghandhara Tyre & Rubber signed a joint-venture accord to build a manufacturing facility in Pakistan.

Pakistan Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| Punjab |

| Sindh |

| Khyber Pakhtunkhwa |

| Balochistan |

| Rest of the Pakistan |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles | |

| By Province | Punjab |

| Sindh | |

| Khyber Pakhtunkhwa | |

| Balochistan | |

| Rest of the Pakistan |

Key Questions Answered in the Report

How large is the Pakistan tire market in 2025?

The Pakistan tire market size is USD 2.09 billion in 2025.

What CAGR is forecasted through 2030?

Sales are expected to rise at a 5.32% CAGR between 2025 and 2030.

Which province leads demand?

Punjab holds the largest share at 43.92% because it concentrates assembly plants and freight corridors.

Which vehicle segment consumes the most tires?

Two-wheelers account for 48.59% of total volume owing to their dominance in personal and delivery transport.

How fast are battery-electric vehicle tires growing?

The segment is projected to advance at a 14.33% CAGR under the national 30% EV target.

Page last updated on: