Thailand Construction Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

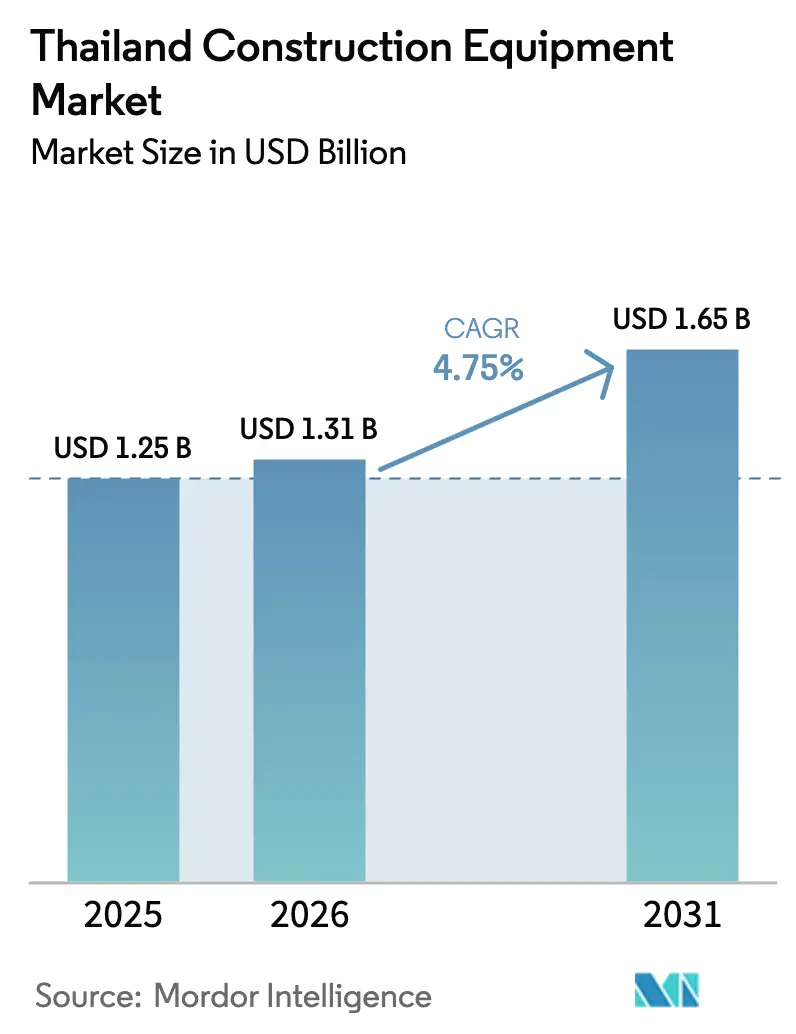

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Construction Equipment Market Analysis by Mordor Intelligence

The Thailand Construction Equipment Market size is projected to expand from USD 1.25 billion in 2025 and USD 1.31 billion in 2026 to USD 1.65 billion by 2031, registering a CAGR of 4.75% between 2026 to 2031. As Phase 2 of the Eastern Economic Corridor (EEC) allocates significant investments to transport, port, and airport projects through the coming years, contractors are shifting their capital expenditures. They're now favoring high-tonnage excavators, telescopic handlers, and GPS-enabled cranes. Additionally, public-private partnership (PPP) concessions, valued at substantial amounts, are steering preferences towards wheel loaders and motor graders. These choices not only expedite project timelines but also align with fuel-efficiency mandates. With SME borrowing costs remaining high and a significant operator shortfall widening, there's a noticeable uptick in rental penetration. This trend is further bolstered by the allure of pay-per-hour fleet models. Meanwhile, Bangkok's push for cleaner air is spurring initial trials of battery-electric excavators. Despite a scarcity of charging points, this move signals a shift for the segment, moving it past mere demonstrations.

Key Report Takeaways

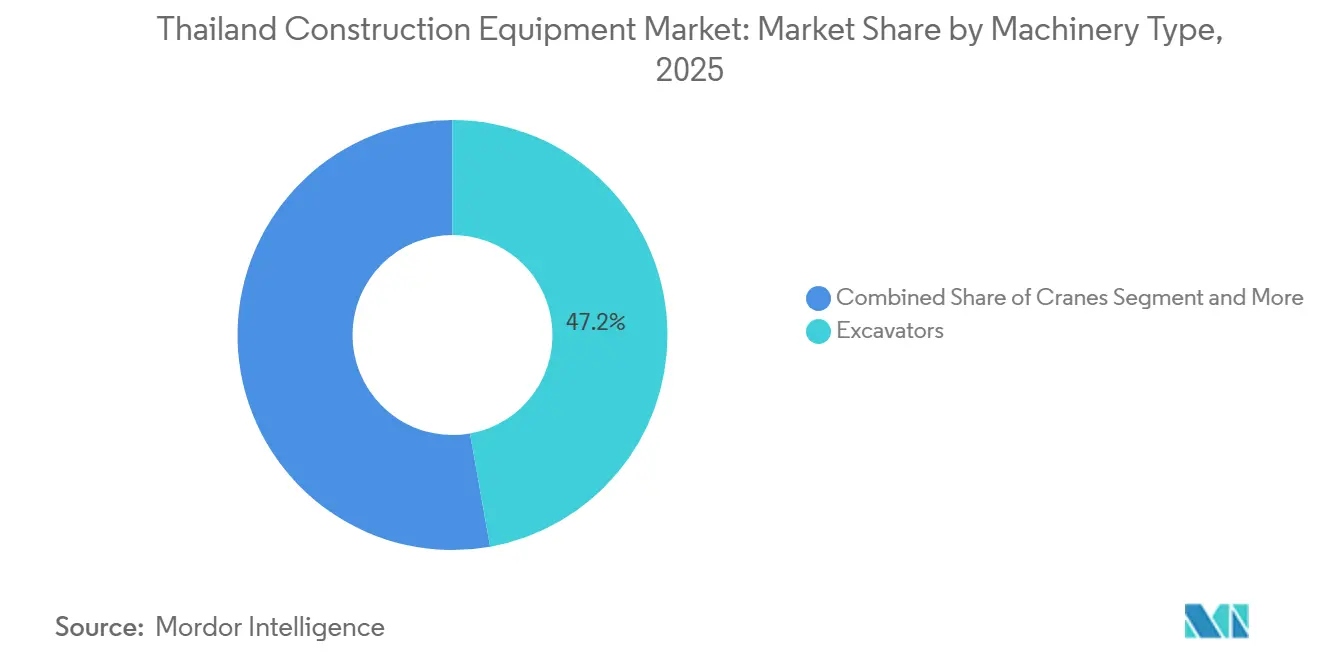

- By machinery type, excavators led with 47.16% of the Thailand construction equipment market share in 2025, whereas loaders and backhoes are projected to grow fastest at 4.77% CAGR through 2031.

- By propulsion, internal-combustion equipment accounted for 88.71% of 2025 revenue, but electric and hybrid models will grow at a 4.88% CAGR over 2026-2031.

- By power output, the 101-200 HP band accounted for 56.65% of the Thailand construction equipment market size in 2025, while sub-100 HP machines are poised to expand at a 4.91% CAGR.

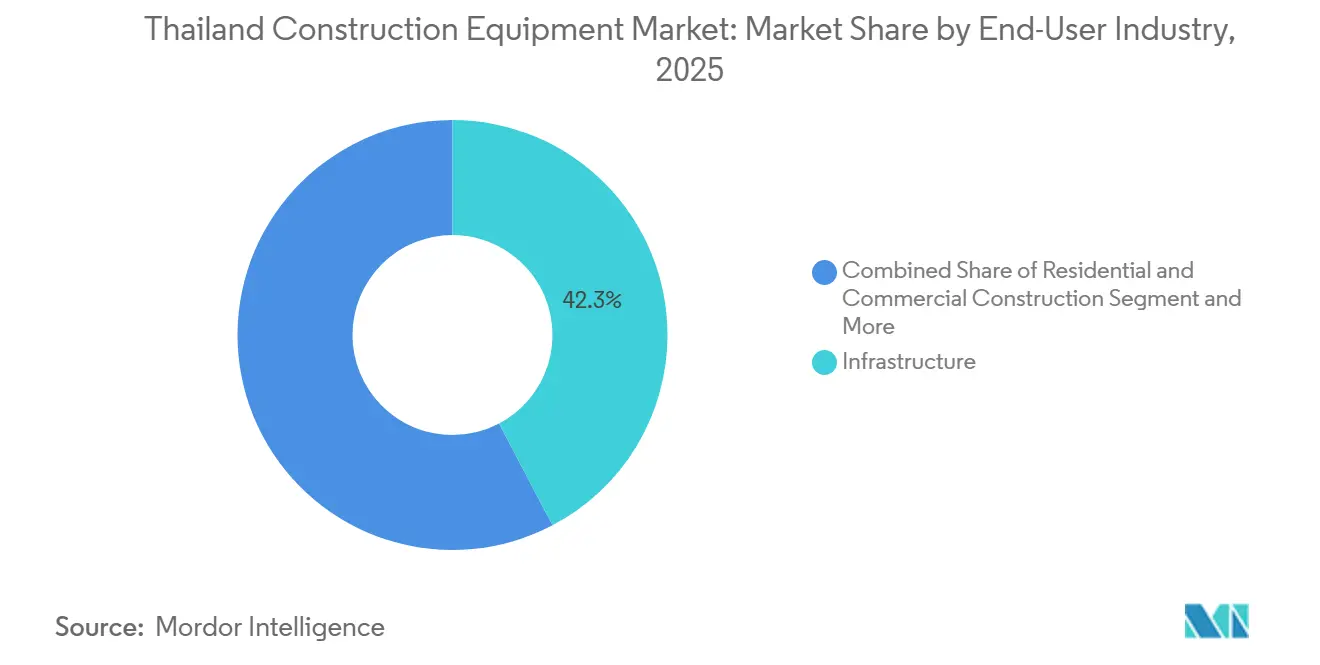

- By end-user, infrastructure accounted for 42.27% of spending in 2025; energy and utilities will grow fastest, with a 4.79% CAGR to 2031.

- By application, earth-moving accounted for 48.71% of activity in 2025, yet lifting and hoisting is expected to increase at a 4.85% CAGR during the forecast window.

- By region, the Bangkok Metropolitan Area accounted for 35.45% of the 2025 demand, while Northeastern Thailand is forecast to grow at a 4.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Megaprojects Under Eastern Economic Corridor | +1.3% | EEC provinces (Chonburi, Rayong, Chachoengsao), spillover to Bangkok Metropolitan Area | Medium term (2-4 years) |

| Public-Private Partnerships Accelerating Infrastructure Roll-Outs | +1.1% | National, with concentration in Bangkok, Central Thailand, and Southern Thailand | Medium term (2-4 years) |

| Tourism-Led Rebound in Commercial and Hospitality Construction | +0.8% | Bangkok Metropolitan Area, Southern Thailand (Phuket, Krabi, Surat Thani) | Short term (≤ 2 years) |

| Renewable-Energy Build-Out Lifting Demand for Cranes and Earth-Moving Gear | +0.7% | National, with early concentration in Central and Northeastern Thailand dam sites | Long term (≥ 4 years) |

| Localization of EV Supply-Chain Plants Requiring Green-Field Factory Construction | +0.6% | EEC core (Rayong, Chonburi), emerging in Northern Thailand (Chiang Mai industrial zones) | Medium term (2-4 years) |

| Rapid Adoption of Machine-Control & BIM-Integrated Equipment to Cut Project Over-Runs | +0.3% | Bangkok Metropolitan Area, EEC provinces, pilot adoption in Central Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Megaprojects Under Eastern Economic Corridor

Several EEC Phase 2 projects, valued at a significant amount, are driving demand for medium- to large-excavators, lattice-boom crawler cranes, and amphibious pile drivers. Important infrastructure developments, including an aviation hub expansion, a port upgrade, and a high-speed rail corridor connecting multiple airports, are operating at fleet capacities well above pre-pandemic levels. Contractors are increasingly favoring telematics-enabled machines that transmit utilization data to lenders and insurers, enabling notable reductions in financing costs. In certain regions, secondary leasing markets have emerged, allowing smaller contractors to sub-lease idle equipment and capitalize on additional project opportunities. Japanese OEMs are incorporating predictive-maintenance subscriptions into long-term service contracts, ensuring steady aftermarket revenue and extending equipment's operational lifespan.

Public-Private Partnerships Accelerating Infrastructure Roll-Outs

The Ministry of Transport has unveiled a significant public-private partnership (PPP) docket encompassing numerous projects. In addition, additional funding has been allocated for several new initiatives set to launch in the near future. Key motorways operating under a build-operate-transfer model impose emissions ceilings, promoting the use of fuel-efficient graders and compactors. The ambitious Southern Land Bridge, a significant infrastructure project, is set to deploy a substantial number of heavy machines, with operations expected to commence later in the decade. Embedded in PPP contracts are provisions for liquidated damages in the event of schedule delays. This has spurred the adoption of BIM-integrated machinery, which ensures real-time compliance tracking. In response to the capital demands of primary concession bids, smaller firms are strategically shifting towards subcontracting niche roles and pursuing short-term rentals.

Tourism-Led Rebound in Commercial and Hospitality Construction

By the mid-term, the target for international arrivals is set to increase significantly, driving a substantial revival of hotel pipelines nationwide. In the capital city, a notable number of keys are being commissioned, while a major tourist destination is planning to add a considerable number of rooms across multiple properties over the next few years. With a resurgence in hospitality capital expenditure projected for the near future, there is a growing demand for compact excavators, tower cranes, and rough-terrain forklifts, all designed to meet advanced emissions standards. Global hotel chains are increasingly adopting battery-electric mini-excavators for landscaping purposes. This shift enables rental fleets with compliant assets to charge a premium during high-demand periods. Additionally, green-certification scorecards are becoming critical in tender evaluations, favoring contractors whose fleets meet established sustainability thresholds such as LEED or EDGE.

Renewable-Energy Build-Out Lifting Demand for Cranes and Earth-Moving Gear

Gulf Energy, with its numerous solar farms generating significant capacity, is placing orders for amphibious cranes and GPS-guided rammers designed for floating platforms. This comes alongside a large-scale solar and battery energy storage system tranche, financed by the Asian Development Bank. Meanwhile, EGAT's ambitious floating-solar initiative, spanning multiple dams, is turning to modular pontoons and low-ground-pressure excavators to ensure shoreline stabilization. A hybrid array that began operations recently has set a new engineering benchmark. Original Equipment Manufacturers (OEMs) are now looking to replicate this success at other reservoirs. With the Ministry of Energy pushing for a substantial renewable share in the grid within the next decade, contractors are seeing a clear demand trajectory. This clarity is driving them to make bulk orders and establish framework agreements for specialized fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-Input Inflation Squeezing Contractor CAPEX | -0.8% | National, with acute impact in Northeastern and Southern Thailand | Short term (≤ 2 years) |

| Skilled-Operator Shortages | -0.7% | National, especially in Bangkok and EEC provinces | Medium term (2-4 years) |

| High Import Duties and Sparse Charging Infra | -0.5% | National, with higher barriers in Central and Northern Thailand | Long term (≥ 4 years) |

| Tight Credit Conditions for SMEs Slowing Fleet Renewal Cycles | -0.4% | National, with pronounced effects on provincial contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-Input Inflation Squeezing Contractor CAPEX

In 2024, Thailand's construction cost index rose moderately, driven by ongoing inflationary pressures on steel, cement, and diesel. Labor costs also rose significantly, further squeezing subcontractors' already tight margins. As a result, smaller builders are postponing fleet upgrades, turning instead to used equipment from EEC surplus inventories. While government price caps have been implemented, their impact is limited, leaving project budgets vulnerable to fluctuations in global commodity prices. Without a return to price stability or a rise in escalator clauses, sales of new equipment to micro-contractors are expected to remain subdued.

Skilled-Operator Shortages Pushing Renters Over Buyers

A workforce that's aging and a sluggish uptake in vocational training have resulted in a significant operator gap for heavy machinery. While the importation of foreign labor helps address this shortfall, challenges such as language barriers and certification issues diminish overall efficiency. To counteract potential downtime risks, rental houses are now pairing certified operators with their leases, catering to the needs of primary contractors. Original Equipment Manufacturers (OEMs) are investing in simulators and e-learning platforms, yet the country's capacity still lags behind demand, particularly for advanced telematics platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Hold Value, Loaders Set Pace

Excavators accounted for 47.16% of the Thailand construction equipment market share in 2025, reflecting their indispensable role in pile foundations and trenching across the EEC megaproject lattice. This segment alone accounted for nearly half of Thailand's construction equipment market, driven by a procurement surge for the three-airport high-speed rail and the U-Tapao aviation hub. Chinese brands gained volume with minimal price discounts, but Japanese incumbents defended margins through advanced telematics and five-year service pacts.

Loaders and backhoes are forecast to register a 4.77% CAGR through 2031 as provincial roadworks, irrigation canals, and agriprocessing complexes demand multi-function machines that toggle between earth-moving and material-handling roles. Rental yards diversify into skid-steer and articulated loaders to serve smallholder cooperatives, modernizing cassava logistics. Telescopic handlers and motor graders, although smaller in volume, are increasingly deployed on PPP motorway sites where cross-slope precision is prioritized.

By Propulsion: ICE Dominates, Electric Picks Momentum

Internal combustion engines retained 88.71% of revenue in 2025, underpinned by diesel’s national availability and the absence of universal charging. Nevertheless, electric and hybrid units are predicted to outpace, expanding at a 4.88% CAGR through 2031 and lifting the Thailand construction equipment market size in the low-carbon segment. Luxury hotel chains and corporate headquarters in Bangkok contractually require battery-electric mini-excavators for LEED credits, enabling OEMs to trial lithium-iron-phosphate packs rated for humid environments.

Hybrid drivetrains marry diesel generators to battery buffers on cranes, cutting idle emissions by nearly 30% on congested sites. ICE will stay entrenched in quarrying and mining until fast-swap battery skids reach 300 kWh capacities. Government waivers on excise for zero-emission machinery narrow the total cost of ownership, but uptake remains gated by range constraints and resale liquidity uncertainties.

By Power Output: Mid-Range Leads, Compact Equipment Surges

Machines in the 101-200 HP envelope dominated the Thailand construction equipment market with 56.65% of the market share in 2025, as this horsepower bracket spans commercial mid-rises, arterial road restorations, and port expansion bulkworks. OEMs spotlight fuel-mapping software that optimizes torque curves, claiming diesel savings in Bangkok stop-start cycles.

Sub-100 HP equipment will climb at a brisk 4.91% CAGR by 2031, propelled by Northeast agricultural mechanization grants that subsidize mini-backhoes and skid steers for cassava and sugarcane handling. Compact track loaders now feature quick-coupler hydraulics, allowing farmers to switch from pallet forks to trench buckets within minutes. Units over 200 HP serve mining and mass earthworks but face slower volume growth as telematics reveal excess idle time, steering contractors toward multi-shift scheduling instead of new purchases.

By End-User: Infrastructure Remains Core, Energy & Utilities Accelerate

Infrastructure schemes accounted for 42.27% of outlays in 2025, a share that anchors the Thailand construction equipment industry, as PPP motorways, double-track railways, and port deepening collectively span more than 3,000 km. Concessionaires prioritize burn-rate predictability and select machines with dealer-backed uptime-guarantee clauses.

Energy and utilities, led by solar and battery-energy-storage system clusters, will grow fastest at a 4.79% CAGR through 2031, incrementally expanding the Thailand construction equipment market. Floating-solar installations require amphibious cranes and low-ground-pressure dozers, niches that reward OEMs investing in purpose-built models. Residential and commercial real estate benefits from the tourism rebound, yet office take-up remains cautious amid hybrid work norms.

By Application: Earth-Moving Dominant, Lifting & Hoisting Rising

Earth-moving captured 48.71% of 2025 activity, mirroring the deep-cut profiles of runway, motorway, and rail embankments. Machine-control levelling systems now integrate with drone topography feeds, truncating survey-to-dig cycles to a minimum.

Lifting and hoisting will expand at a 4.85% CAGR as condominium towers in Chonburi and Rayong demand tower cranes with anti-collision sensors mandated by the Department of Industrial Works. Renewable arrays and EV part depots further boost orders for rough-terrain forklifts and telehandlers equipped with 14-meter booms. Material handling, demolition, and tunnelling applications each add incremental slices, supported by specialty attachments that convert standard excavators into versatile platforms.

Geography Analysis

Bangkok Metropolitan Area delivered 35.45% of 2025 demand, cementing its position as the single largest consumer within the Thailand construction equipment market [1]“Orange Line Extension Overview,” Bangkok Metropolitan Transportation Planning Division, bmtp.go.th . Projects such as the Orange Line extension and mixed-use skyscrapers in Ratchathewi are pushing contractors to lease battery-electric mini-loaders and Stage V-compliant cranes to meet urban emissions codes. Land scarcity spurs vertical builds, elongating crane deployment cycles, and favoring OEMs offering rapid mast-height reconfiguration kits.

Northeastern Thailand is the fastest climber, projected to grow at a 4.83% CAGR through 2031, as cassava processing, sugarcane logistics, and irrigation revamps unlock backhoe-loader and grader procurement in Khon Kaen, Udon Thani, and Nakhon Ratchasima. Provincial governments allocate matching grants for agricultural mechanization, helping cushion farmer cooperatives from up-front capital costs. Rental firms locate mobile depots along Highway 2 to slash equipment delivery lead times to under 24 hours, a critical differentiator during harvest peaks.

Central Thailand maintains steady momentum as a logistics and manufacturing hub, bolstered by warehouse clusters near Ayutthaya and Saraburi, where forklifts and automated storage solutions are gaining traction. Northern Thailand taps industrial estates in Chiang Mai and Lamphun, albeit from a smaller base, emphasizing compact excavators suitable for mountainous terrain. Southern Thailand benefits from dual-track railways and resort refurbishments in Phuket, channeling orders for compactors and truck-mounted concrete pumps. Regional disparities in permitting speeds, skilled-labor pools, and grid reliability shape contractors' fleet deployment calculus.

Competitive Landscape

The Thailand construction equipment market hosts a moderately concentrated field where Caterpillar, Komatsu, and Hitachi preserve entrenched dealer reach and command parts availability within 24-hour windows [2]“Dealer Network Expansion in Thailand,” Caterpillar Inc., caterpillar.com. Their combined dominance is challenged by SANY and XCMG, whose service centers doubled between 2024 and 2026, leveraging 48-hour parts guarantees and price undercuts to penetrate provincial highway tenders [3]“Thailand Service-Center Milestones,” XCMG, xcmg.com . Japanese and Korean brands, including Kobelco, Hyundai, and Doosan, are pivoting toward telematics-rich offerings that promise higher uptime through predictive analytics.

Strategic maneuvers center on digital ecosystem plays. In 2025, Komatsu inked a Bangkok pilot with a telecom provider to stream high-resolution machine data over private 5G, slicing latency to sub-50 milliseconds for autonomous-grade control. SANY counters by bundling one-year operator-training vouchers with each excavator sale, tackling the skills drought head-on. Volvo CE appointed CHAIRATCHAKARN as its new distributor in January 2025, expanding showroom clusters into the Eastern Seaboard corridor.

Rental penetration breached in metropolitan Bangkok during 2025, spawning software platforms that algorithmically match idle inventory with last-minute project spikes. These marketplaces monetize utilization gaps and pressure OEMs to design rental-ready iterations emphasizing quick coupling, vandal-proof telematics, and transportability within 12-ton slide-bed truck limits. Regulatory pulls such as mandatory BIM submission elevate digital compliance services, creating subscription revenue for tech-forward dealers.

Thailand Construction Equipment Industry Leaders

Caterpillar Inc.

SANY Group

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

Kobelco Construction Machinery Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Volvo CE, at a premier event in Bangkok, introduced its New Generation EC210 excavator, showcasing its state-of-the-art design and efficiency-focused featureswhich. This event also served as a pivotal moment for customers, commemorating the collaboration with CHAIRATCHAKARN (Bangkok) Co., Ltd (CHAB), who has recently been designated as Volvo CE's dealer in Thailand.

- January 2025: Thailand's 2025-2026 infrastructure program unveiled 223 projects aimed at enhancing the country's development and economic growth. This initiative is expected to bolster equipment demand in the medium term, providing significant opportunities for market players in the construction and infrastructure sectors.

Thailand Construction Equipment Market Report Scope

The scope of the report includes Machinery Type (Cranes and More), Propulsion (Internal Combustion Engine and Electric & Hybrid), Power Output (Below 100 HP and More), End-user (Infrastructure and More), Application (Earth-moving and More), and Geography.

| Cranes |

| Telescopic Handlers |

| Excavators |

| Loaders & Backhoe |

| Motor Graders |

| Other Machinery Types |

| Internal Combustion Engine |

| Electric & Hybrid |

| Below 100 HP |

| 101 - 200 HP |

| Above 200 HP |

| Infrastructure |

| Residential and Commercial Construction |

| Mining and Industrial |

| Agriculture |

| Energy and Utilities |

| Earth-moving |

| Material Handling |

| Road Construction |

| Lifting & Hoisting |

| Bangkok Metropolitan Area |

| Central Thailand |

| Northern Thailand |

| Northeastern Thailand |

| Southern Thailand |

| By Machinery Type | Cranes |

| Telescopic Handlers | |

| Excavators | |

| Loaders & Backhoe | |

| Motor Graders | |

| Other Machinery Types | |

| By Propulsion | Internal Combustion Engine |

| Electric & Hybrid | |

| By Power Output | Below 100 HP |

| 101 - 200 HP | |

| Above 200 HP | |

| By End-user | Infrastructure |

| Residential and Commercial Construction | |

| Mining and Industrial | |

| Agriculture | |

| Energy and Utilities | |

| By Application | Earth-moving |

| Material Handling | |

| Road Construction | |

| Lifting & Hoisting | |

| By Region | Bangkok Metropolitan Area |

| Central Thailand | |

| Northern Thailand | |

| Northeastern Thailand | |

| Southern Thailand |

Key Questions Answered in the Report

How large will Thailand’s construction equipment sector be by 2031?

The Thailand construction equipment market size is projected to reach USD 1.65 billion by 2031, expanding from USD 1.31 billion in 2026 at a 4.75% CAGR.

Which machinery type commands the most sales?

Excavators led with 47.16% of 2025 revenue, fueled by deep-foundation needs across EEC and PPP megaprojects.

What segment is growing fastest?

Loaders and backhoes are forecast to rise at a 4.77% CAGR through 2031, reflecting demand for multi-function machines on provincial road and agrilogistics sites.

Where is regional growth highest?

Northeastern provinces are expected to post a 4.83% CAGR, supported by irrigation modernization and cassava-processing investments.

How quickly are electric machines penetrating?

Electric and hybrid equipment is predicted to advance at a 4.88% CAGR as Bangkok clean-air rules and hotel sustainability mandates multiply pilot deployments.

What financing trends dominate equipment procurement?

Rising SME lending rates and operator shortages are accelerating rental and pay-per-use models, pushing rental penetration beyond 50% in Bangkok.

Page last updated on: