Thailand Fertilizers Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

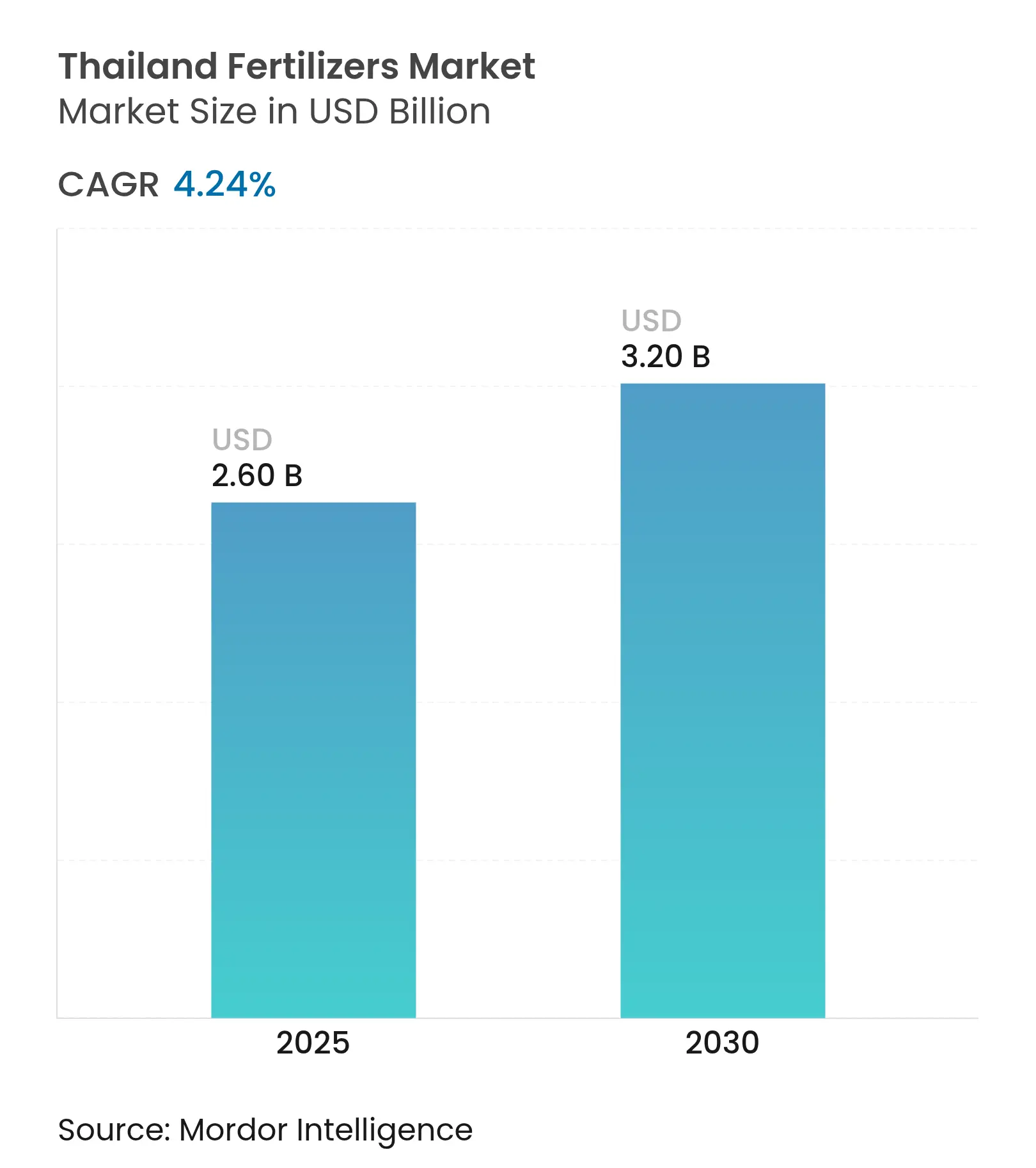

| Market Size (2025) | USD 2.60 Billion |

| Market Size (2030) | USD 3.20 Billion |

| Growth Rate (2025 - 2030) | 4.24 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Thailand Fertilizers Market Analysis by Mordor Intelligence

The Thailand fertilizers market size reached USD 2.60 billion in 2025 and is projected to grow at a CAGR of 4.24% to USD 3.20 billion by 2030. Thailand's rice exports reached 9.9 million metric tons, a 13% increase and the highest level since 2018. In 2024, the export value rose by 27% to USD 6.4 billion (225.6 billion baht), contributing to Thailand's export growth. Fertilizers remained essential for maintaining this high rice production.[1]Thai Rice Exporters Association, “Thai rice exports in 2025 struggling, Downward target revision ahead,” thairiceexporters.org.th. The market growth is driven by increasing domestic food demand, government food-security initiatives, and the development of a USD 1.8 billion potash mine that aims to reduce dependency on imported raw materials. The market faces challenges from fluctuations in fertilizer prices, which range from USD 400 to USD 1,200 per metric ton during supply disruptions. These price variations have encouraged investments in domestic production facilities and precision agriculture technologies. Carbon-credit incentives aligned with Thailand's commitment to reduce emissions by 20-25% are encouraging farmers to adopt low-emission fertilizer variants[2]World Bank Group, “Supporting Thailand's Climate Goals through the World Bank Partnership for Market Readiness,” worldbank.org.

Key Report Takeaways

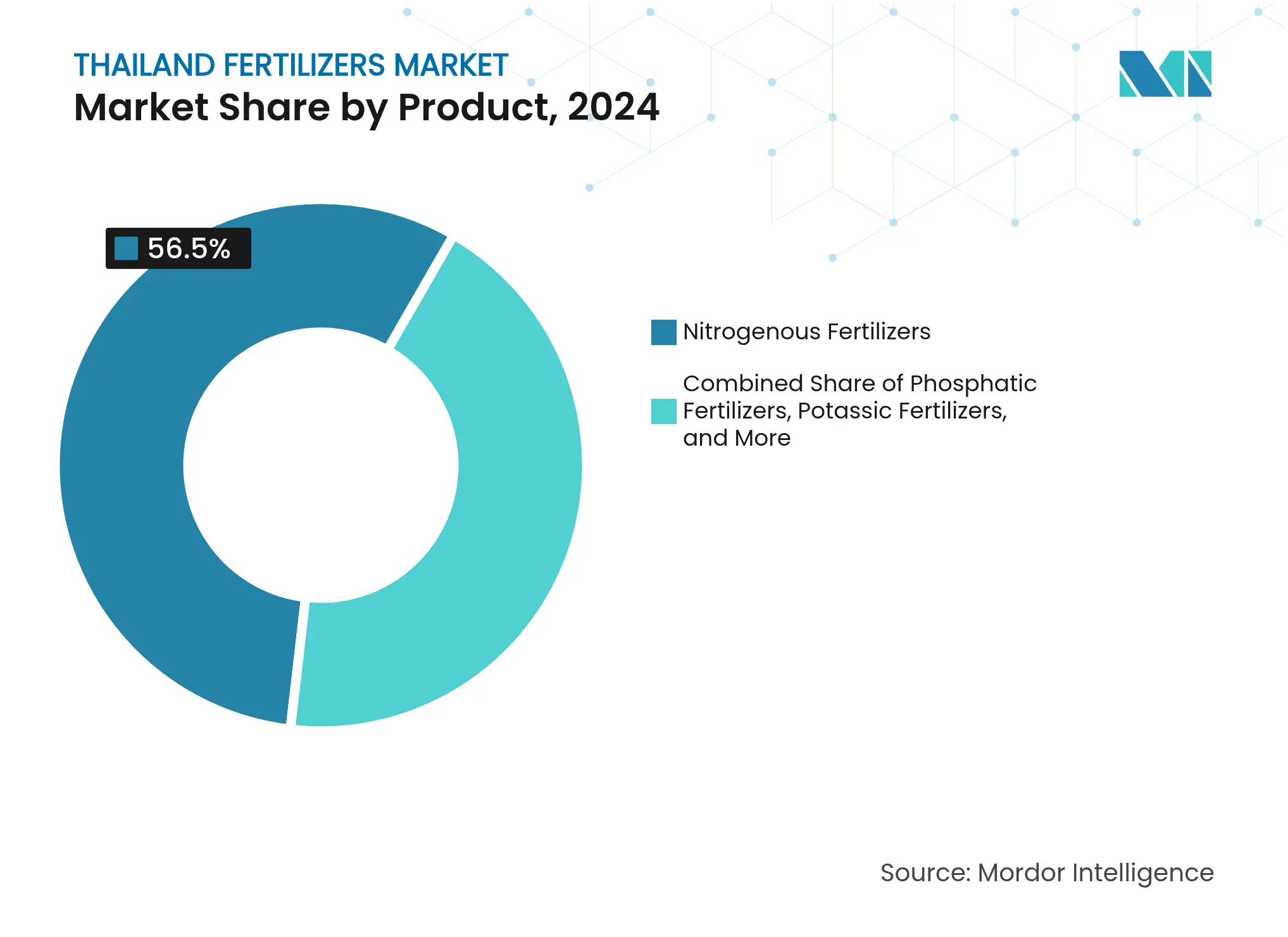

- By product, nitrogenous fertilizers led with 56.5% of the Thailand fertilizers market share in 2024, while micronutrient fertilizers are forecast to advance at a 5.3% CAGR through 2030.

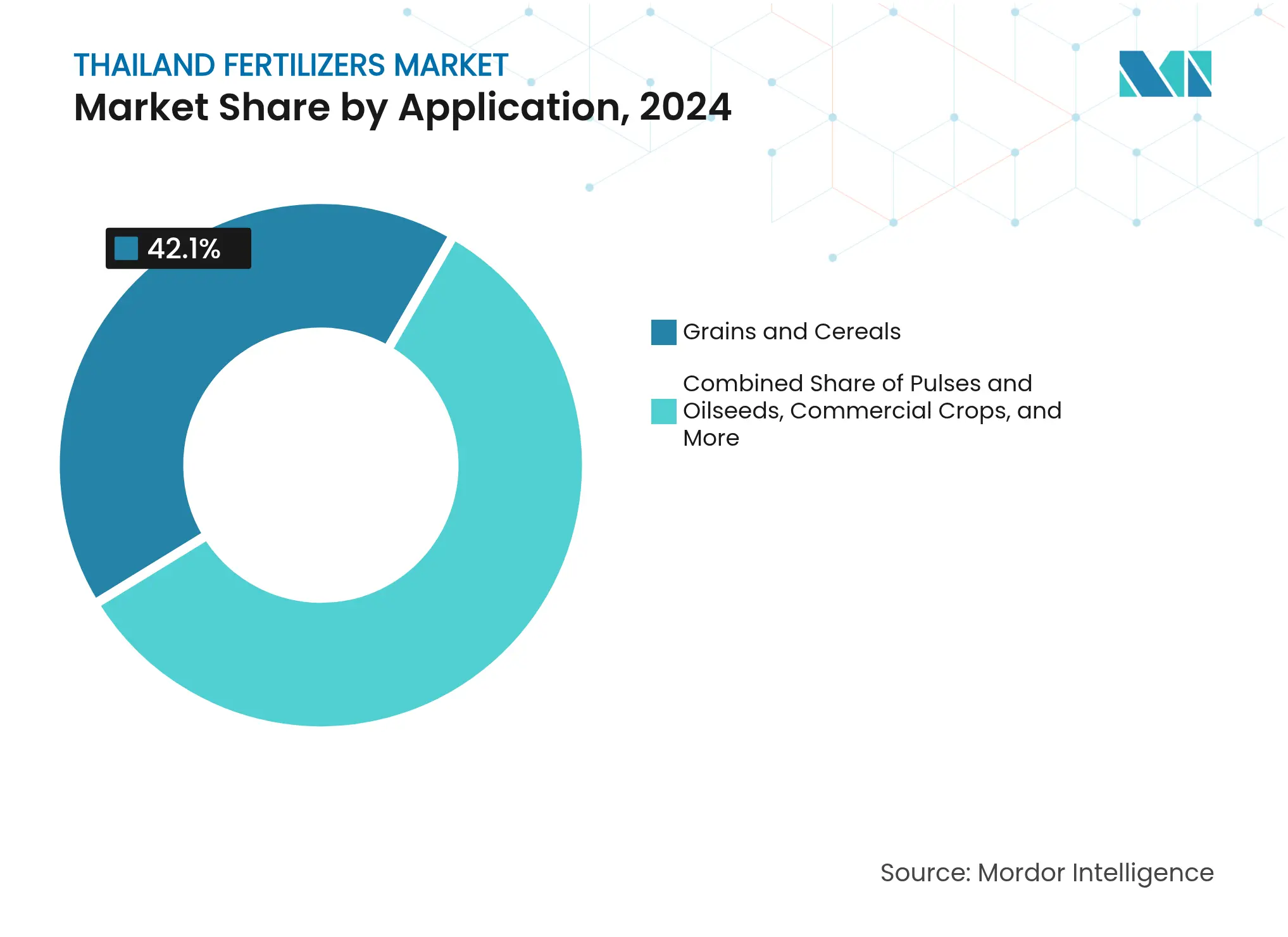

- By application, grains and cereals accounted for 42.1% of the Thailand fertilizers market size in 2024, whereas fruits and vegetables are poised to expand at a 6.7% CAGR between 2025 and 2030.

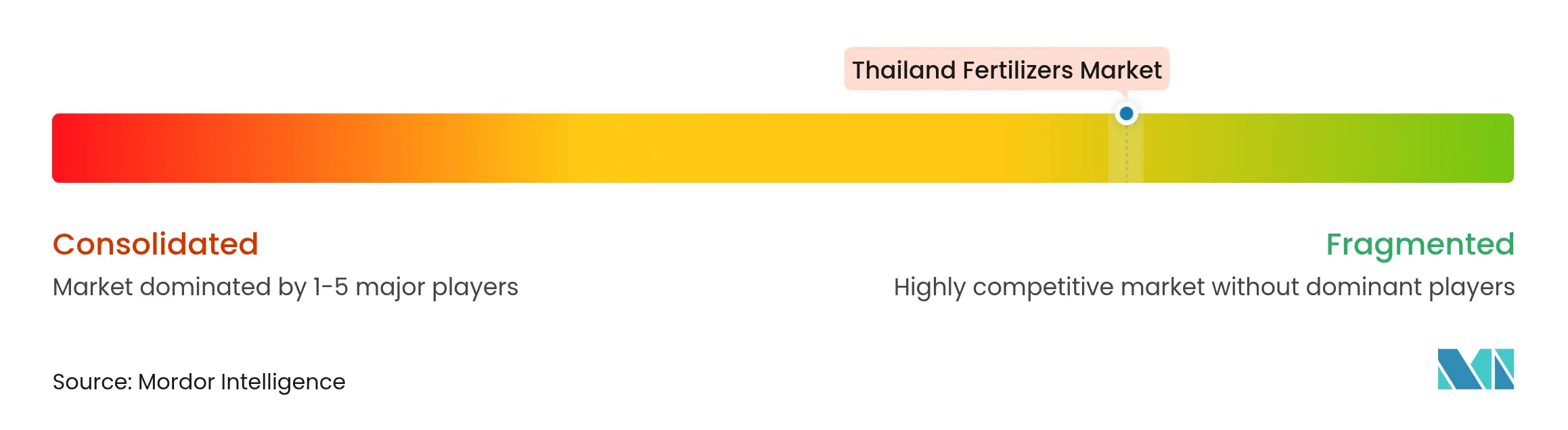

- The top five companies - Thai Central Chemical Public Co., Ltd., Yara International ASA, Charoen Pokphand Group (Chia Tai Co., Ltd.), ICP Fertilizer Co., Ltd., and TCC Group (Terragro Fertilizer Co., Ltd.) collectively hold 29.9% of the market share in 2024.

Thailand Fertilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government subsidies for fertilizer purchases Government subsidies for fertilizer purchases | +0.8% | National with greater effect in rural provinces | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:National with greater effect in rural provinces | Impact Timeline:Medium term (2-4 years) |

Rising domestic food demand and population Rising domestic food demand and population | +0.6% | National concentrated in urban centers | Long term (≥ 4 years) | |||

Declining soil fertility and nutrient depletion Declining soil fertility and nutrient depletion | +0.7% | Northeast and Central regions | Long term (≥ 4 years) | |||

Expansion of high-value horticulture and export crops Expansion of high-value horticulture and export crops | +0.9% | Export-oriented provinces | Medium term (2-4 years) | |||

Digital fertilizer-advisory platforms and e-commerce Digital fertilizer-advisory platforms and e-commerce | +0.4% | Developed regions nationwide | Short term (≤ 2 years) | |||

Carbon-credit incentives for low-emission fertilizers Carbon-credit incentives for low-emission fertilizers | +0.3% | National aligned with climate targets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Government Subsidies for Fertilizer Purchases

Thailand protects farmers from international fertilizer price volatility through direct subsidies and price controls, which mitigated the price increase from USD 400 to USD 1,200 per metric ton in 2024. While this policy ensures farmers can access fertilizers, it reduces profit margins for producers. The country plans to launch a USD 1.8 billion domestic potash project in 2026 to enhance supply security and reduce future subsidy requirements, following similar results achieved in neighboring markets with domestic production capabilities. The policy's success is demonstrated by Thailand maintaining consistent rice export volumes despite significant cost increases.

Rising Domestic Food Demand and Population

According to the OAE agricultural statistics of Thailand 2024, Thailand's agricultural product imports reached 740 billion Thai baht (USD 22.8 billion) in 2024, compared to 725.5 billion Thai baht (USD 22.4 billion) in 2023. The tourism sector's recovery contributed to increased premium food consumption. Government initiatives, including the "Young Smart Farmers" program, enhanced awareness about precision fertilization on crop quality. The 2023-2027 Food Management Action Plan focuses on increasing agricultural output through optimized fertilizer usage.

Declining Soil Fertility and Nutrient Depletion

Soil degradation from overuse is prevalent in the Northeast region, where many farmers rely on rain-fed agriculture. Nitrate pollution affects irrigation water at 95% of surveyed sites. Magnesium and other micronutrient deficiencies reduce durian and oil palm yields, increasing the need for targeted fertilizer supplements. The government's climate-smart agriculture policies focus on balanced fertilization to improve soil health. The National Science and Technology Development Agency (NSTDA) of Thailand developed a chelated fertilizer in 2021, which uses amino acids bonded with mineral micronutrients as organic complexing agents to enhance nutrient delivery.

Carbon-Credit Incentives for Low-Emission Fertilizers

The Joint Crediting Mechanism with Japan supports 48 pilot projects that monetize emission reductions through carbon markets. Rice cultivation accounts for the majority of farm-sector greenhouse gases and receives incentives for reduced-nitrogen practices. Premium T-VER credits generate additional revenue for farmers who adopt low-emission fertilizers. Thailand's voluntary carbon market, overseen by the Thailand Greenhouse Gas Management Organization (TGO), issues Thailand Voluntary Emission Reduction (TVER) credits. Organizations purchase these credits to offset their carbon footprints, creating financial incentives for emission reduction projects and encouraging lower-emission agricultural practices in fertilizer use and rice straw management.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile natural gas and raw material prices Volatile natural gas and raw material prices | –1.2% | Nationwide production cost exposure | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:–1.2% | Geographic Relevance:Nationwide production cost exposure | Impact Timeline:Short term (≤ 2 years) |

Farmer shift toward organic and biofertilizers Farmer shift toward organic and biofertilizers | –0.8% | Higher uptake in developed regions | Medium term (2-4 years) | |||

Climate-induced production disruptions Climate-induced production disruptions | –0.6% | Vulnerable agricultural regions | Long term (≥ 4 years) | |||

Stricter Thai nitrate-runoff regulations Stricter Thai nitrate-runoff regulations | –0.4% | Water-sensitive basins | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Natural Gas and Raw Material Prices

Thailand's domestic gas production averaged 2.1 million metric tons per month in 2024, while LNG imports increased to 11.3 million metric tons, increasing vulnerability to global price fluctuations. Pipeline supply uncertainties from Myanmar and elevated feedstock costs have limited new capacity investments. PTT Global Chemical secured a 400,000 metric tons ethane import agreement beginning in 2029 to diversify supply sources, though this requires significant capital investment. Export restrictions implemented by major fertilizer-producing countries in 2022 and 2023 led to supply constraints in Thailand, causing fertilizer prices to reach USD 1,200 per metric ton in 2023, according to the Thai Fertilizer and Agricultural Suppliers Association. The increased import costs have created financial strain for Thai farmers, especially smallholders, who make up over 60% of the agricultural workforce, as reported by the National Statistical Office.

Stricter Thai Nitrate-Runoff Regulations

Agriculture contributes substantial nitrogen levels to major river basins, leading to stricter runoff control measures. The implementation of odor concentration limits for fertilizer manufacturing facilities and potential mandatory application reporting requirements increases operational costs. Farmers are required to adopt balanced fertilization practices and enhanced-efficiency products to comply with new standards. The Thailand fertilizers market faces constraints from environmental regulations that impact compliance requirements and market growth. The Ministry of Natural Resources and Environment has implemented strict guidelines through the Environmental Quality Management Plan (2022-2026) to reduce soil and water pollution from nitrate fertilizers.

Segment Analysis

By Product: Nitrogen Dominance Faces Micronutrient Challenge

Nitrogenous fertilizers account for 56.5% of the Thailand fertilizers market share in 2024, supported by rice exports of 7.5 million metric tons. [3]U.S. Department of Agriculture, “Thailand: Grain and Feed Annual,” fas.usda.gov The growth in Thailand's agricultural exports increased the demand for nitrogen fertilizer, as farmers needed to enhance crop yields and improve soil quality to meet export requirements for products such as fruits and rice. Urea remains the primary choice among farmers due to its cost-effectiveness and multiple applications. The micronutrient segment is the fastest-growing segment, anticipated to grow at a rate of 5.3% annually through 2030, driven by increasing magnesium and zinc deficiencies in the soil. The market for micronutrients is expanding in tandem with investments in precision agriculture, which enable customized fertilizer blends based on soil analysis.

Potash imports of 700,000 metric tons, valued at THB 10 billion (approximately USD 285.7 million) in 2024, underscore its strategic importance. The planned domestic mine, with an investment of USD 1.8 billion scheduled for 2026, is anticipated to transform the market by providing locally sourced muriate of potash and supporting regional exports. The market is showing increased adoption of secondary macronutrients, as well as nitrogen, phosphorus, and potassium blends. Export-focused durian and rubber farmers are selecting specialized formulations to enhance fruit set, oil content, and stress tolerance. Environmental sustainability requirements are driving the adoption of nitrogen use efficiency enhancers and coated granules, creating new opportunities for technology providers.

Note: Segment shares of all individual segments available upon report purchase

By Application: Fruits and Vegetables Drive Premium Fertilizer Demand

Grains and cereals hold 42.1% of the Thailand fertilizers market size in 2024, supported by mechanized paddy fields using site-specific nutrient management. While stable export contracts sustain the grains segment, water scarcity poses risks to yields. The fruits and vegetables segment is projected to grow at a 6.7% annual rate, driven by premium varieties exported to China, Asia-Pacific countries, and high-end domestic retail markets. Farmers are increasingly implementing drip fertilization and fertigation systems to enhance nutrient uptake and improve product quality.

The commercial crops segment remains significant, driven by sugarcane and cassava production, which is supported by growing bioethanol and starch exports. Climate-smart programs promote pulses and oilseeds as crop diversification options to reduce monoculture risks. The ornamental and turf segment, although smaller, generates higher margins in resort areas that focus on landscape maintenance. The expansion of livestock operations increases demand for fertilizers in forage crop production to improve feed quality and digestibility.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Northeast, Thailand's largest agricultural zone, faces challenges with saline soils and rain-fed water systems. Farmers in this region need sulfur-coated and potassium-fortified fertilizer blends to counter nutrient leaching. Central Thailand's extensive irrigation system, connected to Chao Phraya River dams, enables increased adoption of micronutrient and specialty products, improving yield per hectare. The Southern provinces focus on rubber, oil palm, and tropical fruit production, requiring magnesium-rich formulas and balanced NPK to maintain latex flow and fruit sugar content.

The establishment of potash mining operations in the Northeast aims to reduce logistics costs, potentially equalizing regional fertilizer prices. The Northern highlands support the cultivation of cool-climate vegetables and specialty fruits at different elevations. Farmers implement precision agriculture methods, including drone-assisted soil mapping for micronutrient application adjustment, establishing demonstration sites for technology providers. Coastal regions affected by saltwater intrusion rely on chloride-tolerant crops and chloride-free potassium sources.

The Eastern Economic Corridor infrastructure projects enhance deep-sea port capacity and freight rail connections, reducing inbound fertilizer costs and improving distribution to remote areas. Regional climate adaptation initiatives support crop diversification, with drought-affected areas transitioning from water-intensive rice to sorghum, changing nutrient requirements. The 2023-2027 Food Management Action Plan's regional production targets guide provincial extension services in adapting fertilizer recommendations to specific crop advantages.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The market is moderately fragmented, with the top five suppliers, Thai Central Chemical Public Co., Ltd., Yara International ASA, Charoen Pokphand Group (Chia Tai Co., Ltd.), ICP Fertilizer Co., Ltd., and TCC Group (Terragro Fertilizer Co., Ltd.), holding 29.9% of the Thailand fertilizers market share in 2024. Thai Central Chemical maintains its position through domestic production capabilities and an extensive dealer network serving smallholder farmers. Yara International ASA focuses on advanced formulations and advisory platforms, including biological supplements like YaraAmplix to enhance nutrient uptake. Domestic firms are pursuing vertical integration strategies, as demonstrated by PTT Global Chemical's ethane import arrangement to secure feedstock for nitrogen production.

Companies are gaining competitive advantages through sustainability initiatives, with firms producing low-emission fertilizers benefiting from carbon credits. Digital agricultural services strengthen customer relationships by providing prescription-based solutions that improve yields while meeting environmental regulations on nitrate runoff. The market has seen growth in micronutrient-specific products, while fertilizer manufacturers, supported by incentives, are establishing a presence despite their currently limited market share.

International companies focus on premium horticulture products, while domestic firms leverage relationships with provincial cooperatives for bulk fertilizer distribution. Rising feedstock costs are driving operational improvements, exemplified by SCG Chemicals' implementation of energy-efficient processes for blended NPK production with reduced emissions. The industry is likely to see consolidation through mergers between regional distributors and specialty producers as companies seek economies of scale to manage regulatory compliance costs.

Thailand Fertilizers Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sumitomo Corporation established a joint venture with NFC Public Company Limited, a Thai tank terminal operator, to manage sulfuric acid tank terminal operations for phosphatic fertilizer production. The partnership focuses on enhancing operational safety and logistics reliability while developing a regional hub for agricultural operations across Asia.

- April 2025: Compo Expert introduced Basfoliar Premium SL fertilizers with LeafCare Technology for foliar application. The formulation meets the potassium requirements of fruits, vegetables, potatoes, and cereals during their critical growth stages.

- February 2025: Thailand's potash producer Asean Potash (Apot) obtained all necessary government permits to proceed with the construction of the country's first 1.2 million metric tons per year MOP plant in Chaiyaphum province at the end of this year, with plans to initiate commercial production in 2028.

Table of Contents for Thailand Fertilizers Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government Subsidies for Fertilizer Purchases

- 4.2.2Rising Domestic Food Demand and Population

- 4.2.3Declining Soil Fertility and Nutrient Depletion

- 4.2.4Expansion of High-Value Horticulture and Export Crops

- 4.2.5Digital Fertilizer-Advisory Platforms and E-Commerce

- 4.2.6Carbon-Credit Incentives for Low-Emission Fertilizers

- 4.3Market Restraints

- 4.3.1Volatile Natural Gas and Raw Material Prices

- 4.3.2Farmer Shift Toward Organic and Biofertilizers

- 4.3.3Climate-Induced Production Disruptions

- 4.3.4Stricter Thai Nitrate-Runoff Regulations

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Bargaining Power of Buyers

- 4.6.2Bargaining Power of Suppliers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Nitrogenous Fertilizers

- 5.1.1.1Urea

- 5.1.1.2Calcium Ammonium Nitrate (CAN)

- 5.1.1.3Ammonium Nitrate

- 5.1.1.4Ammonium Sulfate

- 5.1.1.5Anhydrous Ammonia

- 5.1.1.6Other Nitrogenous Fertilizers (Urea Ammonium Nitrate, and Others)

- 5.1.2Phosphatic Fertilizers

- 5.1.2.1Mono-Ammonium Phosphate (MAP)

- 5.1.2.2Di-Ammonium Phosphate (DAP)

- 5.1.2.3Triple Superphosphate (TSP)

- 5.1.2.4Other Phosphatic Fertilizers (Diammonium Phosphate (DAP), Single Superphosphate (SSP), Phosphate Rock, etc.)

- 5.1.3Potassic Fertilizers

- 5.1.3.1Muriate of Potash (MOP)

- 5.1.3.2Sulphate of Potash (SOP)

- 5.1.3.3Other Potassic Fertilizers (Potassium Nitrate, and Potash Salts)

- 5.1.4Micronutrient Fertilizers

- 5.1.5Other Products (NPK Compounds, Secondary Macronutrient Fertilizers)

- 5.2By Application

- 5.2.1Grains and Cereals

- 5.2.2Pulses and Oilseeds

- 5.2.3Commercial Crops

- 5.2.4Fruits and Vegetables

- 5.2.5Other Applications (Turfs and Ornamentals, and Forage and Fodder Crops)

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1Yara International ASA

- 6.4.2Thai Central Chemical Public Company Limited

- 6.4.3NFC Public Company Limited

- 6.4.4ICL Group Ltd.

- 6.4.5Haifa Chemicals Ltd.

- 6.4.6Saksiam International Co., Ltd.

- 6.4.7Rayong Fertilizer Trading Company Limited (UBE Corporation)

- 6.4.8ICP Fertilizer Co., Ltd.

- 6.4.9TCC Group (Terragro Fertilizer Co., Ltd.)

- 6.4.10Grupa Azoty S.A. (Compo Expert GmbH)

- 6.4.11Charoen Pokphand Group (Chia Tai Co., Ltd.)

- 6.4.12Wesco Chemical Thailand Co. Ltd.

- 6.4.13OCP S.A.

- 6.4.14TKK Fertilizer (Thailand) Company Limited

- 6.4.15Kaesad Marketing Co., Ltd.

7. Market Opportunities and Future Outlook

Thailand Fertilizers Market Report Scope

According to OECD, chemical fertilizers are commercially produced, usually synthetic, chemical compounds, such as nitrogen, phosphorus, and potassium, as well as a variety of micronutrients and additives used in farming. The Thailand fertilizers market is segmented by product (nitrogenous fertilizers, phosphatic fertilizers, potassic fertilizers, micronutrients fertilizers, and other products), and application (grains and cereals, pulses and oilseeds, commercial crops, fruits and vegetables, and other applications). The report offers the market size and forecasts in terms of volume in metric tons and value in USD for all the above segments.