Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

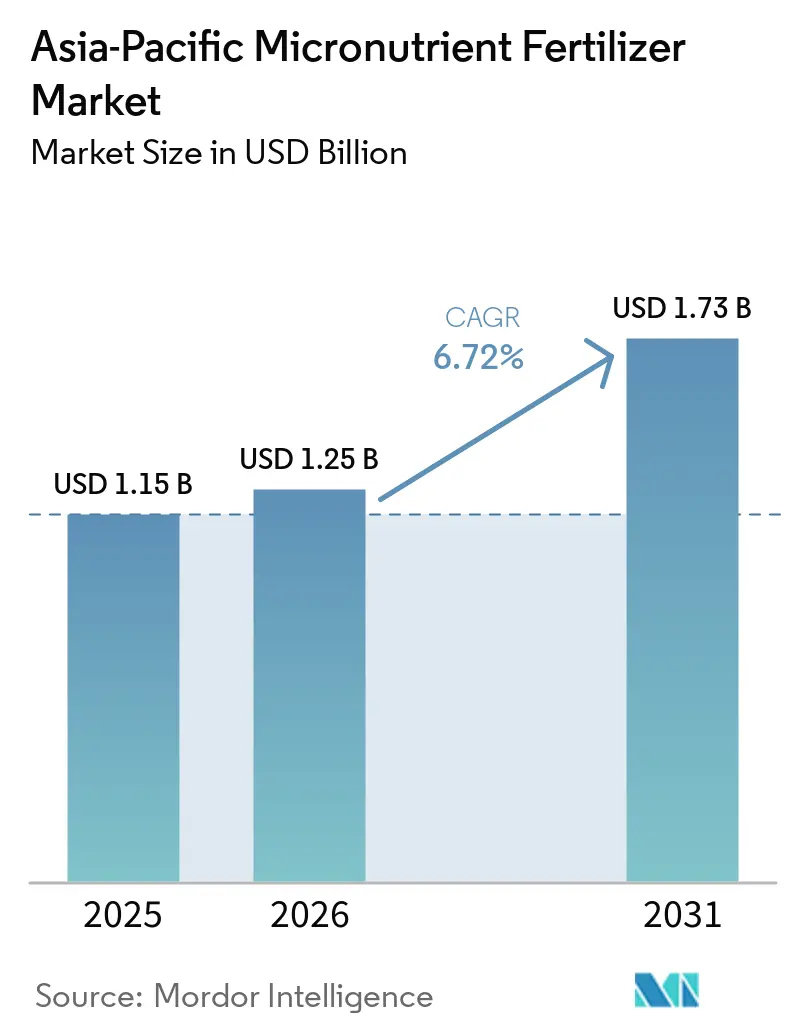

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Micronutrient Fertilizer Market Analysis by Mordor Intelligence

The Asia-Pacific micronutrient fertilizer market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.25 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). The upward trajectory reflects expanding precision-farming practices, widespread micronutrient deficiencies, and supportive fiscal incentives that lower input costs for smallholders. Province-level zinc subsidies in China also buoy the Asia-Pacific micronutrient fertilizer market, GST reductions in India, and fertigation uptake in Australia, all of which widen product access, spur demand for specialized formulations, and create white-space opportunities for regional innovators. Heightened digital-platform penetration, led by BASF’s xarvio and India’s Geoagro-iKrishi, accelerates advisory reach, while supply-side advances in nano and chelated technologies improve nutrient-use efficiency. However, raw-material price volatility for zinc sulfate ores, limited rural credit in parts of South Asia, and an influx of counterfeit inputs in Indonesia and the Philippines introduce short-term headwinds that temper but do not derail overall expansion of the Asia-Pacific micronutrient fertilizer market.

Key Report Takeaways

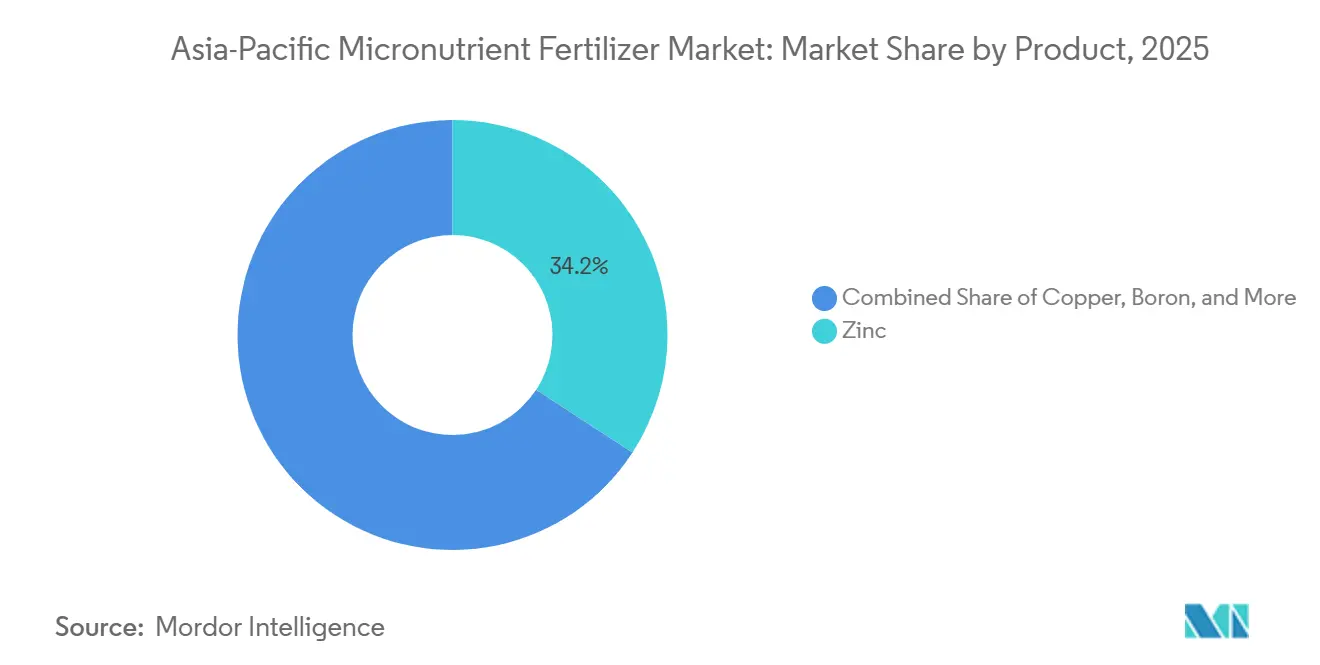

- By product category, zinc accounted for the largest Asia-Pacific micronutrient fertilizer market share, 34.2%, in 2025, while boron emerged as the fastest-growing product segment, projected to expand at a CAGR of 9.2% during 2026 to 2031.

- By application mode, soil application represented the largest Asia-Pacific micronutrient fertilizer market size in 2025 with a 49.9% share, whereas fertigation is projected to record the strongest growth, advancing at a CAGR of 10.6% during 2026 to 2031.

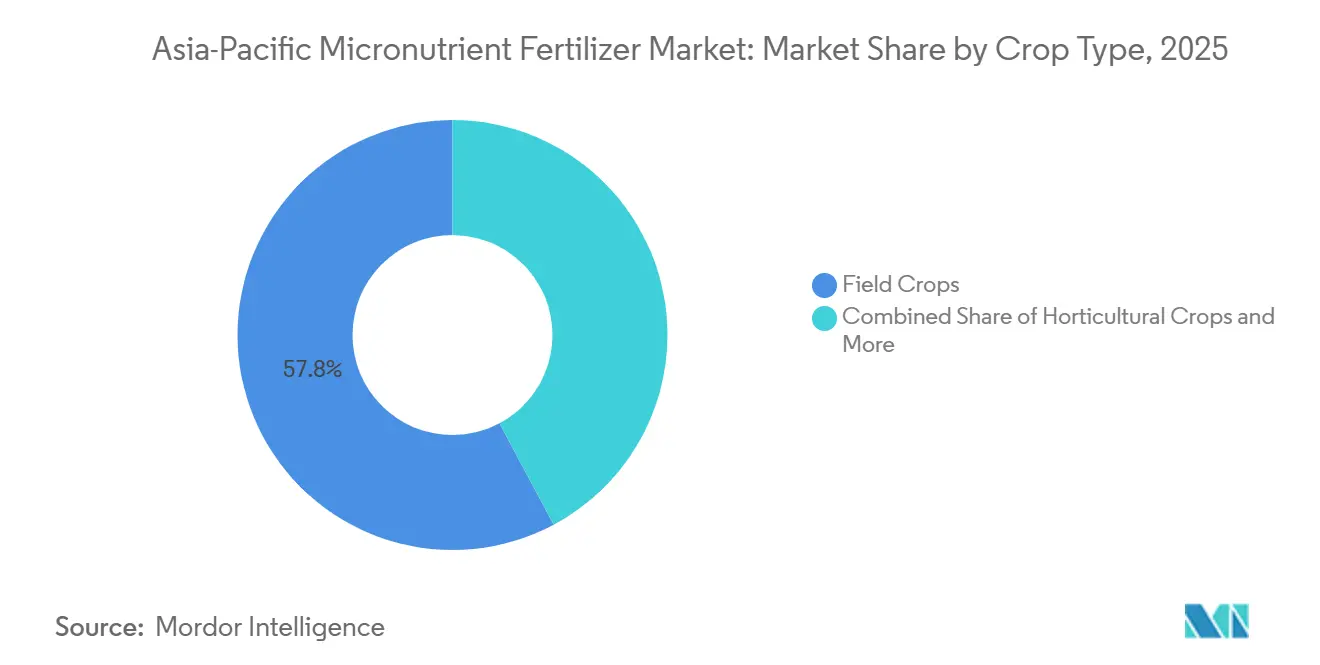

- By crop type, field crops remained the largest contributor to the Asia-Pacific micronutrient fertilizer market, accounting for 57.8% in 2025, while horticultural crops are forecast to register the highest growth rate, with a CAGR of 9.8% during 2026–2031.

- By geography, China accounted for the largest share of the Asia-Pacific micronutrient fertilizer market, representing 35.2% in 2025, whereas India is projected to be the fastest-growing country market, expanding at a CAGR of 9.1% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Micronutrient Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China's Zinc Subsidies Target Hidden Hunger Crisis | +1.2% | China core, spillover to wider Asia-Pacific | Medium term (2-4 years) |

| Australia's Fertigation Revolution in Protected Horticulture | +0.8% | Australia, New Zealand, spreading to Southeast Asia | Short term (≤ 2 years) |

| India's Soil Health Cards Drive Systematic Micronutrient Testing | +1.5% | India core, replication in Bangladesh and Pakistan | Long term (≥ 4 years) |

| Digital Platforms Accelerate Precision Micronutrient Applications | +0.7% | Vietnam, Thailand, widening to the Philippines | Medium term (2-4 years) |

| Specialty-Crop Expansion Drives Customized Demand | +0.9% | Region-wide, strongest in India and China | Short term (≤ 2 years) |

| Consumer Demand for Fortified Foods Spurs Farm-Level Biofortification | +0.6% | Major rice-growing areas of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China's Zinc Subsidies Target Hidden Hunger Crisis

China’s nutrition-centric subsidy scheme reallocates provincial funds toward zinc-enriched fertilizers that lift grain micronutrient density instead of merely boosting yields. The initiative reframes product success metrics around grain zinc content and aligns public health goals with farm-level practices, pushing the Asia-Pacific micronutrient fertilizer market toward value-added formulations. Field evidence shows foliar zinc delivers 55.2% higher biofortification efficacy than soil application, spurring R&D into next-generation foliar sprays. Multiplier effects arise as neighboring countries monitor China’s program to replicate its public health gains, unlocking additional addressable demand for specialized suppliers.

Australia's Fertigation Revolution in Protected Horticulture

Water-scarce Australia prioritizes fertigation to minimize waste and fine-tune nutrient timing for high-density blueberries and other greenhouse fruit crops[1]Source: Australian Government Department of Agriculture, “Protected Horticulture Industry Analysis,” agriculture.gov.au. This shift favors fully water-soluble chelated micronutrients that command premium pricing yet deliver measurable yield-and-quality gains. Early adopters report reductions in iron chlorosis episodes and improved firmness in export berries, catalyzing copy-cat investments in New Zealand and Southeast Asian greenhouses. Rising fertigation acreage, therefore, underwrites the fastest-growing application segment of the Asia-Pacific micronutrient fertilizer market.

Digital Platforms Accelerate Precision Micronutrient Applications

Platforms such as BASF’s xarvio and IRRI’s Rice Crop Manager blend satellite imagery, local weather, and soil analytics to dispense field-specific dosage alerts. These channels bypass legacy distribution layers, curbing counterfeit infiltration and enabling vendors to bundle premium chelated or nano products with agronomic support. Larger datasets continuously refine algorithms, improving recommendation accuracy and farmer trust, which in turn elevates adoption rates in the Asia-Pacific micronutrient fertilizer market.

Specialty-Crop Expansion Drives Customized Demand

Vietnam’s avocado plantings and Thailand’s blueberry acreage draw attention to boron-mediated fruit set and copper-dependent disease management, respectively. Because export buyers enforce strict nutrient specifications, growers willingly pay for crop-specific blends, encouraging manufacturers to differentiate SKUs by phenological stage and soil pH. Such diversification grows the value pool even if total micronutrient metric tons remain modest, reinforcing boron’s status as the fastest-growing product.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility Constrains Market Accessibility | -1.1% | China, Australia, wider Asia-Pacific | Short term (≤ 2 years) |

| Credit Constraints Limit Premium Product Adoption | -0.8% | Bangladesh, Pakistan, rural India | Medium term (2-4 years) |

| Counterfeit Products Erode Farmer Confidence | -0.6% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Port Bottlenecks Delay Chelated Micronutrient Exports | -0.4% | China export-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Constrains Market Accessibility

China’s mine closures under stringent environmental mandates curtail the supply of high-grade zinc sulfate ores, lifting feedstock costs and cascading into micronutrient price swings. Distributors struggle to hedge inventories, forcing periodic price hikes that strain smallholders’ cash flow and hinder uptake. Chelated and nano formulations, which rely on purer inputs, bear disproportionate cost pressure, narrowing the adoption of these high-efficacy options within the Asia-Pacific micronutrient fertilizer market.

Credit Constraints Limit Premium Product Adoption

In Bangladesh, where 80% of fertilizers are imported, currency volatility inflates landed costs and stretches subsidy budgets. Commercial banks in Pakistan apply conservative lending norms, preferring to finance low-risk NPK purchases. Without affordable seasonal credit, smallholders postpone or skip micronutrient applications despite proven yield benefits, muting the Asia-Pacific micronutrient fertilizer market’s value potential in lower-income segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Zinc Leads Demand While Boron Accelerates Growth

Zinc accounted for the largest Asia-Pacific micronutrient fertilizer market share, 34.2% in 2025, supported by widespread zinc deficiencies across agricultural soils and its critical role in crop growth, nutrient uptake, and yield improvement. The segment benefits from strong adoption across cereals, oilseeds, and horticultural crops, while continued product innovation in chelated, coated, and water-soluble formulations is enhancing nutrient-use efficiency. Growing government-led soil testing initiatives and balanced fertilization programs across major agricultural economies are further supporting zinc demand and reinforcing its leadership position in the Asia-Pacific micronutrient fertilizer market.

Boron is anticipated to be the fastest-growing product segment, with a projected CAGR of 9.2% during 2026 to 2031. This growth is fueled by the increasing cultivation of fruits, vegetables, oilseeds, and plantation crops, which require boron for flowering, pollination, fruit set, and quality improvement. The rising adoption of fertigation and foliar nutrient management practices is boosting demand for soluble and specialty boron formulations across various cropping systems. Meanwhile, micronutrients such as iron, copper, and manganese continue to address crop-specific nutrient deficiencies, ensuring a balanced portfolio of high-volume and value-added products in the Asia-Pacific micronutrient fertilizer market.

By Application Mode: Soil Dominance but Fertigation Momentum

Soil application held a 49.9% of the Asia-Pacific micronutrient fertilizer market size in 2025, supported by the widespread use of granular micronutrient products across rice, wheat, and corn cultivation. However, fertigation is projected to be the fastest-growing application mode, advancing at a CAGR of 10.6% during 2026 to 2031, as water-efficient irrigation systems and protected cultivation expand across the region. The growing adoption of drip irrigation is increasing demand for fully soluble micronutrient formulations that improve nutrient uptake and application precision.

Foliar spraying remains an important complementary application method, particularly for the rapid correction of micronutrient deficiencies during critical crop growth stages. The method is widely used in high-value crops and biofortification programs where nutrient absorption efficiency and crop quality are key priorities. Continued integration of precision agriculture technologies, including sensors and automated spraying systems, is further supporting advanced micronutrient application practices across the Asia-Pacific market.

By Crop Type: Field Crops Sustain Demand While Horticulture Drives Growth

Field crops remained the largest contributor to the Asia-Pacific micronutrient fertilizer market size, which accounted for 57.8% in 2025, supported by the extensive cultivation of staple crops such as rice, wheat, and maize across China, India, and Southeast Asia. Government-backed food security initiatives, increasing crop productivity demands, and heightened awareness of soil micronutrient deficiencies continue to drive the adoption of micronutrient fertilizers in large-scale field crop production systems. Additionally, the segment benefits from the growing application of zinc, iron, and manganese fertilizers, which enhance yields and nutrient-use efficiency in intensive farming practices.

Horticultural crops are anticipated to record the highest growth rate, with a CAGR of 9.8% during 2026–2031. This growth is attributed to the expanding production of fruits, vegetables, plantation crops, and other high-value crops that require precise micronutrient management to improve quality, appearance, shelf life, and yield. The increasing adoption of fertigation, protected cultivation, and export-oriented farming practices is further boosting demand for specialty micronutrient products. Meanwhile, turf and ornamental crops maintain steady demand, driven by urban landscaping, golf courses, sports facilities, and municipal greening projects across developing Asia-Pacific economies. These trends support market diversification and the adoption of premium micronutrient products.

Geography Analysis

China accounted for the largest share of the Asia-Pacific micronutrient fertilizer market, representing 35.2% in 2025, supported by its extensive agricultural base, widespread adoption of balanced nutrient management practices, and increasing use of specialty micronutrient formulations across field and horticultural crops. Government initiatives focused on improving soil health, promoting precision agriculture, and enhancing fertilizer efficiency continue to drive demand for micronutrients such as zinc, boron, and iron. In addition, China’s advanced fertilizer manufacturing capabilities and the expansion of its protected cultivation sector further reinforce its leading position in the regional market.

India is anticipated to be the fastest-growing market in the region, registering a CAGR of 9.1% during 2026–2031. Growth is driven by rising awareness of micronutrient deficiencies, expansion of soil testing programs, increased adoption of fertigation systems, and government initiatives aimed at improving agricultural productivity. Demand for micronutrient fertilizers is particularly strong in the cultivation of fruits, vegetables, oilseeds, and cereals, where balanced nutrient application is critical for enhancing yield and quality.

Other countries, including Australia, Indonesia, Thailand, Vietnam, Bangladesh, Pakistan, and the Philippines, along with the rest of Asia-Pacific, are also contributing to regional market growth. The adoption of precision farming practices and specialty crop cultivation is increasing across these markets. Furthermore, investments in irrigation infrastructure, protected agriculture, and nutrient-use efficiency programs are supporting broader adoption of micronutrient fertilizers, thereby sustaining long-term growth across the Asia-Pacific region.

Competitive Landscape

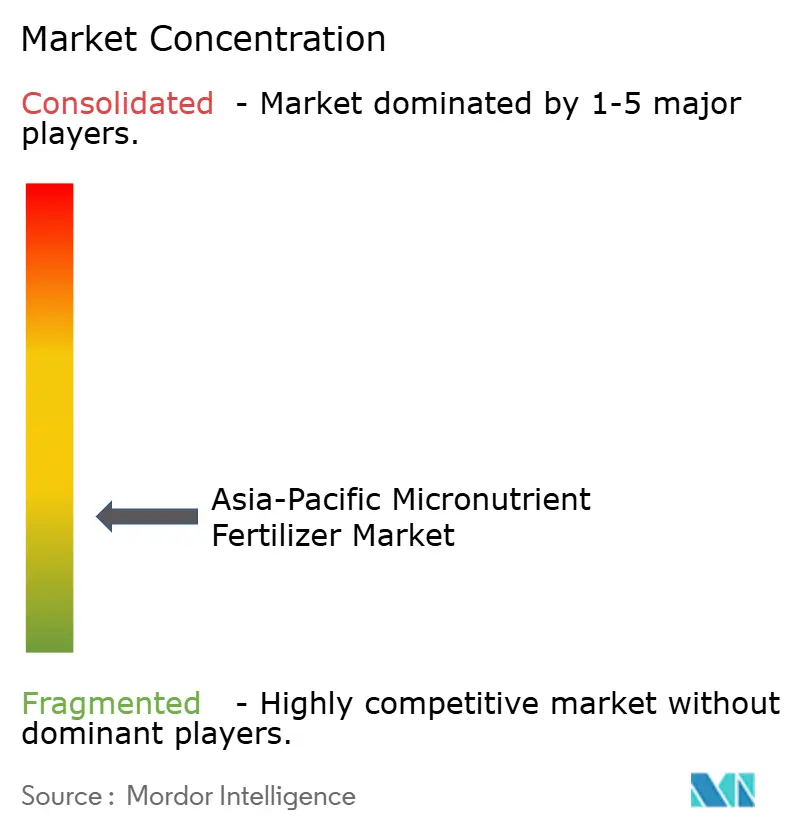

The Asia-Pacific micronutrient fertilizer market exhibits fragmented competition, with the top 5 players controlling a significant market share, creating substantial opportunities for regional specialists and technology innovators to capture market segments through differentiated product offerings and localized distribution strategies. This fragmentation reflects diverse agricultural systems, varying regulatory frameworks, and distinct crop requirements across the region that prevent any single player from achieving dominant market control.

Competition intensity centers on product innovation, particularly in nano-formulations and chelated micronutrients that offer superior bioavailability and application convenience compared to traditional sulfate-based products. Strategic patterns emphasize vertical integration and technology partnerships, with companies like IFFCO developing nano urea plus production capacity of 17 crore bottles annually, while maintaining extensive cooperative distribution networks that reach smallholder farmers directly.

Digital agriculture integration represents a key competitive differentiator, as companies partner with platform providers to deliver precision recommendations that optimize micronutrient applications based on soil testing data and crop monitoring insights. White-space opportunities exist in specialty crop segments, biofortification applications, and emerging markets where agricultural modernization creates demand for advanced micronutrient solutions. The competitive landscape benefits from regulatory frameworks established by bodies like Japan's FAMIC (Food and Agricultural Materials Inspection Center), which ensures product quality standards that support market development and farmer confidence in micronutrient investments.

Asia-Pacific Micronutrient Fertilizer Industry Leaders

Chambal Fertilizers & Chemicals Ltd

Coromandel International Ltd.

Indian Farmers Fertiliser Cooperative Limited

Yara International ASA

Zuari Agro Chemicals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Nutrien Ag Solutions has initiated construction on a new USD 70 million distribution center. This larger facility will boost the company's storage capacity for bulk granular fertilizers, including micronutrient fertilizers, by 20%, bringing the total to 130,000 Metric tons.

- May 2024: iffco revealed that the central government greenlit the launch of its two new offerings including nano liquid zinc and nano liquid copper. These innovations aim to address zinc and copper deficiencies in agricultural crops, thereby enhancing productivity.

- May 2023: Yara International announced plans for a new production facility in Yorkshire, UK, focused on specialty crop nutrition products and biostimulants to boost yields and quality. Projected to be operational by late 2025, the plant will double YaraVita production capacity, with potential for further expansion. Nearly all output will be exported to markets around the world, strengthening Yara's micronutrient fertilizer production.

Asia-Pacific Micronutrient Fertilizer Market Report Scope

Boron, Copper, Iron, Manganese, Molybdenum, Zinc, Others are covered as segments by Product. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type. Australia, Bangladesh, China, India, Indonesia, Japan, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Product

| Boron |

| Copper |

| Iron |

| Manganese |

| Molybdenum |

| Zinc |

| Others |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

Geography

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Product | Boron |

| Copper | |

| Iron | |

| Manganese | |

| Molybdenum | |

| Zinc | |

| Others | |

| Application Mode | Fertigation |

| Foliar | |

| Soil | |

| Crop Type | Field Crops |

| Horticultural Crops | |

| Turf & Ornamental | |

| Geography | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms