Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

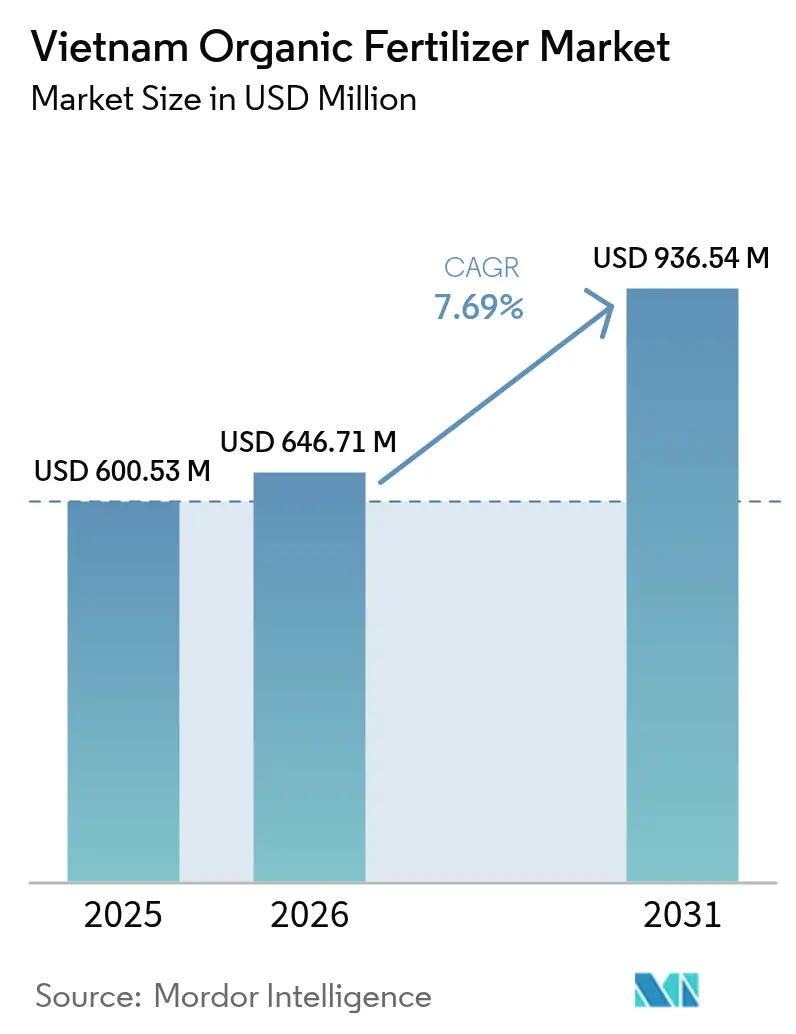

| Base Year Market Size (2025) | USD 600.53 Million |

| Market Size (2026) | USD 646.71 Million |

| Market Size (2031) | USD 936.54 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

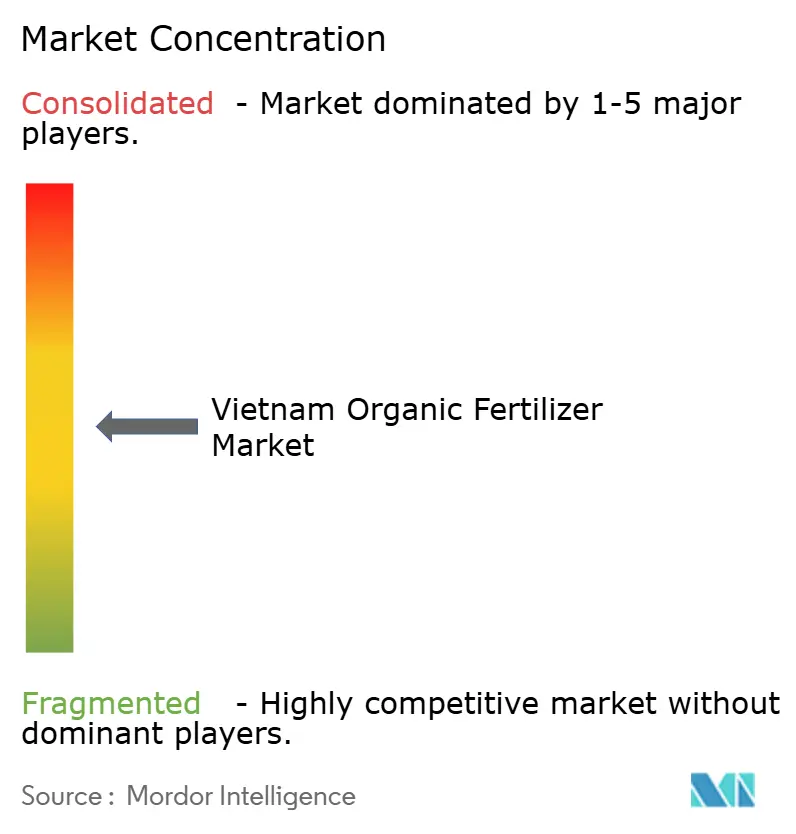

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Organic Fertilizer Market Analysis by Mordor Intelligence

The Vietnam organic fertilizer market size is expected to grow from USD 600.53 million in 2025 to USD 646.71 million in 2026 and is forecast to reach USD 936.54 million by 2031 at 7.69% CAGR over 2026-2031. This robust growth trajectory reflects Vietnam's strategic shift towards sustainable agricultural practices. The market's expansion is primarily driven by government initiatives targeting 50% organic fertilizer adoption by 2050, escalating chemical fertilizer prices, and increasing premium opportunities for certified organic produce across Vietnam's diverse agro-climatic regions. The country's well-developed composting infrastructure, coupled with readily available agricultural waste resources and advancing biotechnology capabilities, enables domestic manufacturers to expand production capacity with minimal dependence on imported materials. The market faces ongoing challenges, including quality control issues and higher labor intensiveness compared to conventional chemical fertilizers. These challenges emphasize the importance of established brands, automation-compatible product formulations, and comprehensive farmer training initiatives. The industry is witnessing increased consolidation as integrated market players strategically position themselves to secure raw material supplies, enhance technological capabilities, and strengthen certification credentials to effectively serve both domestic and export markets.

Key Report Takeaways

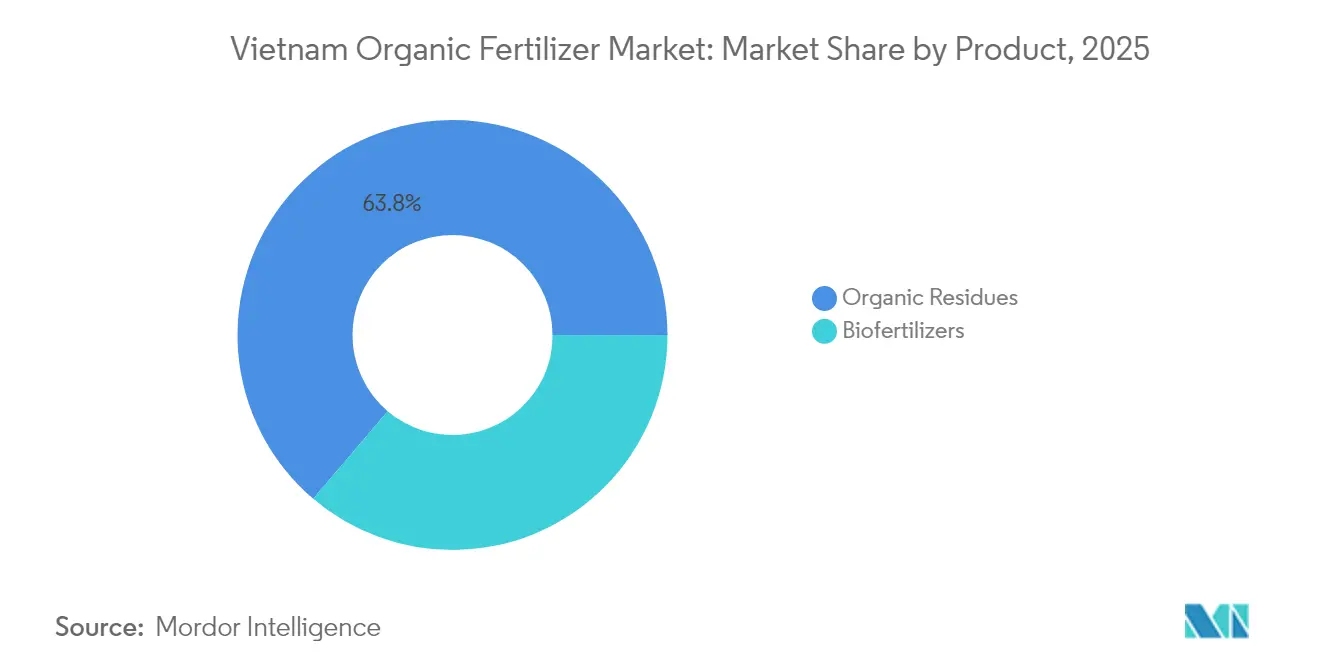

- By product category, organic residues held 63.78% of the Vietnam organic fertilizer market share in 2025, while biofertilizers are projected to grow at a 10.05% CAGR through 2031.

- By form, dry granules accounted for 70.88% of the Vietnam organic fertilizer market size in 2025, whereas liquid and suspension concentrates are forecast to expand at a 10.58% CAGR through 2031.

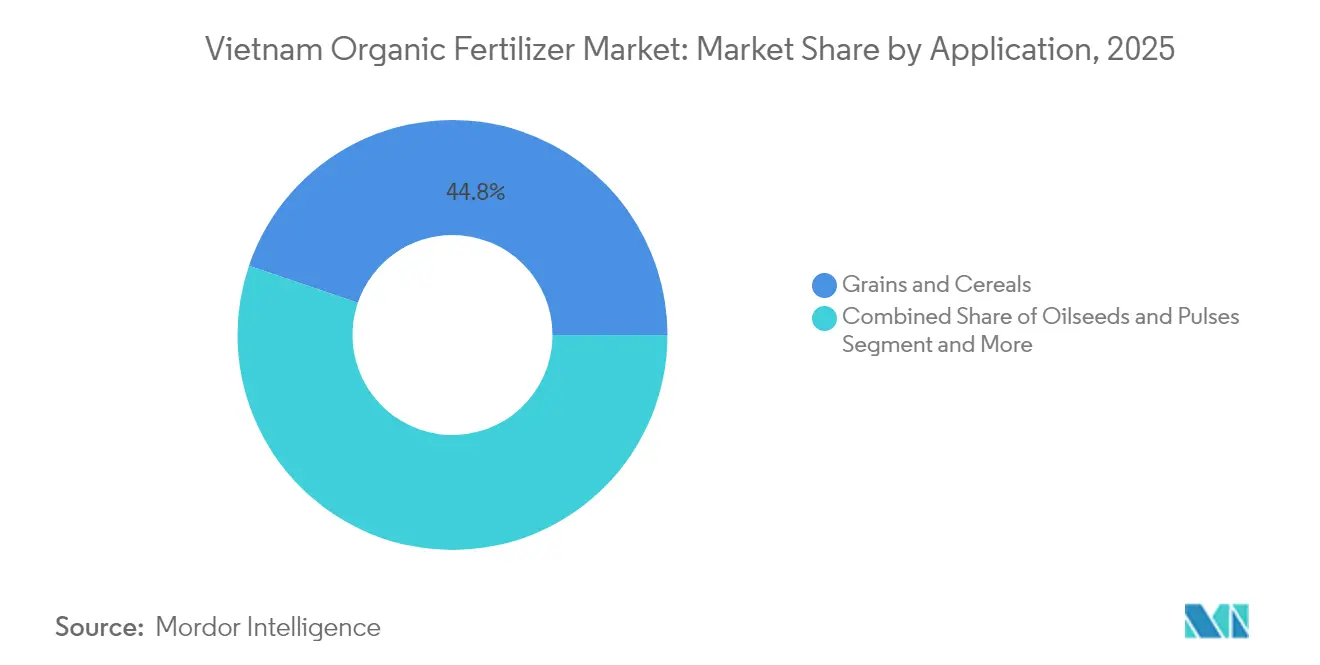

- By application, grains and cereals captured a 44.78% share of the market revenue in 2025, while fruits and vegetables recorded the highest projected CAGR at 8.95% through 2031.

- The market is moderately fragmented, with the top five companies, Binh Dien Fertilizer Joint Stock Company, PetroVietnam Fertilizer and Chemicals Corporation, Que Lam Group Joint Stock Company, Song Gianh Joint Stock Corporation, and Baconco Company Limited (PM Thoresen Asia Holdings PCL) collectively holding a significant portion of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Organic Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government target to raise organic fertilizer utilization | +1.6% | National, strongest in Southern Vietnam | Medium term (2–4 years) |

| Surging demand for certified organic exports | +1.3% | Southern and Central Vietnam export corridors | Short term (≤ 2 years) |

| High chemical-fertilizer prices widen the cost-competitiveness of organic inputs | +1.1% | National, acute for Northern smallholders | Short term (≤ 2 years) |

| Degraded soils require long-term organic-matter replenishment | +1.0% | Central Vietnam and Mekong Delta | Long term (≥ 4 years) |

| Technological advancement and product innovation | +0.9% | National industrial zones | Medium term (2–4 years) |

| Availability of raw materials and waste streams | +0.8% | Processing hubs nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Target to Raise Organic Fertilizer Utilization

Vietnam's target of 50% organic fertilizer usage by 2050 significantly impacts input procurement strategies across the agricultural sector. In 2025, the government's Decision 5190/QĐ-BNN-BVTV outlines specific targets for organic fertilizer development through 2030, including production capacity requirements and quality certification standards. While implementation varies by province, initiatives such as Bac Giang's target to recycle 80% of livestock waste by 2025 demonstrate how regional authorities implement national directives[1]Source: Bao Bac Giang, “Circular Agricultural Production in Bac Giang Increases Economic Value, Protects Environment,” baobacgiang.com.vn. The 2025 consolidation of agricultural and environmental oversight reduced regulatory approval times, allowing producers to launch new products more efficiently. These policy measures support consistent demand across crop varieties, providing stability to Vietnam's organic fertilizer market.

Surging Demand for Certified Organic Exports

The price premiums for certified organic produce in export markets drive the adoption of organic fertilizers in Vietnam's fruit and vegetable sectors. Vietnam's organic export revenues reached USD 335 million in 2025, with continued growth driven by increased supplier audits from European, North American, and developed Asian markets[2]Source: WTO Center, “Import and Export of Processed Food Expands Opportunities for Sustainable Production,” wtocenter.vn. The 20-30% premium over conventional produce encourages fruit and vegetable growers to transition to organic inputs, particularly near Ho Chi Minh City, where cold-chain facilities provide efficient port access. Producers in Southern Vietnam benefit from their proximity to Ho Chi Minh City's export infrastructure and distribution networks. These price premiums enable producers to absorb higher organic fertilizer costs while maintaining competitiveness in international markets.

High Chemical-Fertilizer Prices Widen the Cost-Competitiveness of Organic Inputs

The narrowing cost difference between chemical and organic fertilizers, driven by global price volatility, supply chain disruptions, and geopolitical tensions, has increased the economic viability of organic alternatives. Smallholder farmers in the Red River Delta achieved significant cost savings by replacing half of their urea applications with compost and microbial fertilizers. The increased cost of chemical fertilizer imports has encouraged organic fertilizer adoption nationwide, with usage continuing even after chemical fertilizer prices decrease. The economic benefits become more apparent when considering the long-term advantages of improved soil health and reduced reliance on imported chemical inputs, making organic alternatives attractive to farmers prioritizing sustainable profitability over maximum short-term yields.

Degraded Soils Require Long-Term Organic-Matter Replenishment

Vietnam's agricultural regions face soil organic matter depletion due to long-term chemical fertilizer use, necessitating organic matter restoration. The Soils and Fertilizers Research Institute has developed microbial-based fertilizers to address soil degradation caused by chemical fertilizers, drought, and intensive cropping. Field trials show these fertilizers increase productivity by 15-20% while reducing chemical fertilizer requirements by 15-20%. The restoration of organic matter provides long-term benefits across multiple growing seasons, as improved soil health leads to sustained productivity gains and lower fertilizer dependency, justifying the initial higher investment costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality variability and counterfeit “organic” products erode farmer trust | -1.1% | Nationwide, severe among Northern smallholders | Short term (≤ 2 years) |

| Smallholder cash-flow limits hinder upfront switch to premium biofertilizers | -0.9% | Central and Southern large farms | Medium term (2–4 years) |

| Limited cold-chain for organic produce tempers demand pull | -0.7% | Rural distribution networks | Medium term (2–4 years) |

| Slow nutrient release and risk perception | -0.5% | Intensive cropping systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Quality Variability and Counterfeit “Organic” Products Erode Farmer Trust

The widespread presence of low-quality and incorrectly labeled organic fertilizers reduces farmer trust and limits market growth, especially affecting small-scale farmers who cannot risk purchasing ineffective products. In Vietnam, only about 50 out of 1,000 bio-preparations in circulation have received national certification, creating significant quality control issues that allow counterfeit products to enter the market. This quality inconsistency is particularly problematic in Northern Vietnam's small-scale farming sector, where limited agricultural extension services make it difficult for farmers to identify genuine products from counterfeits, resulting in reluctance to adopt organic fertilizers.

Limited Cold-chain for Organic Produce Tempers Demand Pull

Limited cold-chain infrastructure in Vietnam restricts market access for organic produce, reducing economic incentives for farmers to adopt organic fertilizers. The lack of comprehensive cold-chain networks affects rural producers who cannot maintain product quality during transport to urban markets, making it difficult to obtain price premiums that offset higher organic fertilizer costs. This infrastructure deficit creates geographic differences in organic fertilizer adoption, where producers near urban centers and export facilities have better market access, while rural producers face weak demand for organic certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Organic Residues Hold Structural Advantage

Organic residues account for 63.78% of the Vietnam organic fertilizer market share in 2025, driven by the availability of livestock manure, rice husks, and coffee pulp as cost-effective feedstock compatible with existing composting systems. Farmyard manure dominates the sub-segments, while the 420 metric tons per day municipal waste composting facility of Binh Duong Water - Environment Joint Stock Company supplies the peri-urban vegetable farming regions. These sources support an established distribution network that maintains consistent pricing throughout the year, securing the dominant position of residues in the market.

Biofertilizers are projected to grow at a 10.05% CAGR through 2031, as domestic laboratories develop Azotobacter, Rhizobium, and Mycorrhiza strains specific to Vietnam's soil conditions. These products see the highest adoption in fruit orchards, where farmers can invest in premium inputs to enhance micronutrient absorption and product longevity. The ongoing support through Resolution 36-NQ/TW for biotechnology development is anticipated to expand field testing and accelerate commercial production, establishing biofertilizers as a significant growth segment in the Vietnam organic fertilizer market.

By Form: Liquid Concentrates Gain on Precision Farming

Dry granules accounted for 70.88% of the Vietnam organic fertilizer market size in 2025. This dominance stems from their compatibility with existing storage, transport, and broadcasting equipment, particularly in rice paddies and rubber plantations. Their resistance to tropical humidity and extended shelf life reduces dealer inventory risks, maintaining their position in conventional supply chains. The format aligns with outputs from traditional composting operations and municipal waste processing facilities, enabling distribution through established fertilizer dealer networks across Vietnam's rural agricultural regions.

Liquid and suspension concentrates are projected to grow at a 10.58% CAGR, driven by increased adoption in fertigation systems for greenhouse vegetables and drip-irrigated coffee estates. Advancements in production methods, including enzyme-assisted processing and microbial fermentation, improve product effectiveness and stability. Companies, including Vedan Vietnam, produce advanced formulations, such as amino-acid-based products and foliar fertilizers, which command higher prices in specialized agricultural applications. The high solubility enables precise micro-dosing, resulting in measurable yield improvements that justify premium pricing. Increased investment in irrigation automation indicates sustained demand for liquid fertilizers, supporting market diversification.

By Application: Fruits and Vegetables Capture Premiums

Grains and Cereals dominated the Vietnam organic fertilizer market with a 44.78% share in 2025, primarily due to rice's importance in national food security. The government's sustainable rice initiatives promote compost blends that enable exporters to meet the strict residue requirements in Japanese and Korean markets. The adoption of organic fertilizers in rice cultivation complements traditional Vietnamese farming methods while supporting the government's goals to reduce chemical fertilizer dependence and maintain food security.

The Fruits and Vegetables segment is projected to grow at a 8.95% CAGR, driven by 20-30% export premiums and increasing urban consumer demand. Dragon fruit farmers who convert 12-15 metric tons of pruned branches per hectare into compost report reduced costs. Organic fertilizer formulations for fruit trees, including mycorrhizal inoculants and slow-release compounds, yield improved results in perennial crops where soil health significantly impacts fruit quality and yields. The Turf and Ornamentals segment maintains steady growth through urban landscaping and golf course projects that emphasize environmental sustainability.

Geography Analysis

Southern Vietnam controlled a significant portion of the Vietnam organic fertilizer market, driven by its dense fruit orchards, aquaculture waste availability, and proximity to Ho Chi Minh City export terminals. Facilities such as Baconco's multi-line complex in Phu My Industrial Park optimize last-mile logistics for bulk compost and specialty liquids. The region's intensive fruit and vegetable production systems generate substantial organic waste streams for fertilizer production while supporting established composting operations and waste-to-fertilizer conversion facilities.

Central Vietnam is advancing agricultural development through Agribank's VND 50,000 billion (USD 2.08 billion) low-interest credit program in 2024. The program supports high-tech greenhouses, processing facilities, and waste-to-fertilizer operations. Provincial governments are implementing circular agricultural practices, with Bac Giang province setting targets of 80% livestock waste recycling and 60% agricultural by-product reuse by 2025. The region's biotechnology sector is developing microbial fertilizers and biochar production technologies through international research collaborations to improve organic fertilizer efficiency.

Northern Vietnam represents the smallest market segment, where smallholder farming and cooler climates create demand for low-odor microbial blends over raw manure. Government initiatives for sustainable agriculture and circular economy implementation drive market expansion through cooperative-based procurement and application programs. The region benefits from its proximity to China for cross-border trade opportunities, while local agricultural research institutions provide technical support for product development and farmer education programs.

Competitive Landscape

The market is moderately fragmented, with the top five companies, Binh Dien Fertilizer Joint Stock Company, PetroVietnam Fertilizer and Chemicals Corporation, Que Lam Group Joint Stock Company, Song Gianh Joint Stock Corporation, and Baconco Company Limited (PM Thoresen Asia Holdings PCL) collectively holding a significant portion of the Vietnam organic fertilizer market share in 2024. These companies leverage their scale advantages in raw-material contracts and dealer networks to cross-sell organic products alongside traditional NPK fertilizers.

Second-tier companies are establishing their market presence through specialized approaches. BIWASE processes 900 metric tons of household waste daily into branded compost through municipal-waste concessions. BioFix Fresh combines microbial inoculants with wastewater-treatment solutions for export-oriented fruit packers. The market success increasingly depends on collaborations between technology developers, raw material suppliers, and distribution networks, as shown in biochar production and EU-funded projects that transform agricultural residues into fertilizer products. Companies with quality control capabilities benefit from regulatory requirements set by the Vietnamese Ministry of Agriculture and Rural Development.

Key opportunities in the market include the integration of waste management with fertilizer sales, the development of proprietary microbial consortia, and digital platforms that support smallholders in organic farming practices. International collaboration continues to expand, as demonstrated by EU-funded biochar initiatives that convert coffee husks into high-carbon soil amendments.

Vietnam Organic Fertilizer Industry Leaders

Binh Dien Fertilizer Joint Stock Company

PetroVietnam Fertilizer and Chemicals Corporation

Que Lam Group Joint Stock Company

Song Gianh Joint Stock Corporation

Baconco Company Limited (PM Thoresen Asia Holdings Public Company Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Petrovietnam Fertilizer and Chemicals Corporation (PVFCCo or Phu My) launched phase 1 of the "Phu My" mobile application, a loyalty platform for users of organic Phu My fertilizer products. This development advances the company's digital transformation strategy while improving customer service for farmers and reinforcing PVFCCo's focus on customer needs.

- April 2025: Behn Meyer AgriCare Vietnam introduced a premium line of organic fertilizer products, including Growel M+, Minotec Super, Minotec Pro, and Gowin, formulated for various crops. These products resulted from research and development efforts, incorporating biotechnology that is environmentally friendly and compatible with soil-water-plant ecosystems.

- March 2024: The Vietnam Circular Agriculture Association and Que Lam Group collaborated to establish economic linkages supporting organic and circular agriculture within the Que Lam value chain. The Vietnam Circular Agriculture Association, in coordination with Que Lam Group, selected farmers for the linkage program. The program supplies organic microbial fertilizers and biological products while guaranteeing product purchases at prices above market rates.

Vietnam Organic Fertilizer Market Report Scope

Organic fertilizers are fertilizers produced from raw materials, including animal matter, animal excreta, human excreta, and other natural sources. The Vietnam Organic Fertilizers Market is Segmented by Product (Organic Residues and Biofertilizer), and Application (Grains and Cereals, Oilseeds, Fruits and Vegetables, Turf and Ornamentals, and Other Applications). The report offers the market size and forecasts in terms of value in USD thousand for all the above segments.

By Product

| Organic Residues | Farm Yard Manure |

| Crop Residues | |

| Green Manure | |

| Other Residues (Poultry Droppings, Fish Waste, Municipal Solid Waste, etc.) | |

| Biofertilizers | Azotobacter |

| Rhizobium | |

| Azospirillum | |

| Blue-Green Algae | |

| Azolla | |

| Mycorrhiza | |

| Other Biofertilizers (Bacillus, Frankia, etc.) |

By Form

| Dry Granules |

| Liquid and Suspension Concentrates |

By Application

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turf and Ornamentals |

| Other Crops (Fodder and Forage Crops, Commercial Crops, etc.) |

| By Product | Organic Residues | Farm Yard Manure |

| Crop Residues | ||

| Green Manure | ||

| Other Residues (Poultry Droppings, Fish Waste, Municipal Solid Waste, etc.) | ||

| Biofertilizers | Azotobacter | |

| Rhizobium | ||

| Azospirillum | ||

| Blue-Green Algae | ||

| Azolla | ||

| Mycorrhiza | ||

| Other Biofertilizers (Bacillus, Frankia, etc.) | ||

| By Form | Dry Granules | |

| Liquid and Suspension Concentrates | ||

| By Application | Grains and Cereals | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| Other Crops (Fodder and Forage Crops, Commercial Crops, etc.) | ||

Key Questions Answered in the Report

How large is the Vietnam organic fertilizer market in 2026?

The market is valued at USD 646.71 million in 2026 and is forecast to climb to USD 936.54 million by 2031.

Which segment leads by product type?

Organic residues hold 63.78% share, benefitting from plentiful livestock manure and crop residues.

What growth rate is anticipated for biofertilizers?

Biofertilizers are projected to register a 10.05% CAGR through 2031, the fastest among product categories.

Why are liquid organic fertilizers gaining traction?

They enable precision dosing via drip and fertigation systems, helping commercial farms raise nutrient-use efficiency despite higher unit prices.

Page last updated on: