Thailand Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

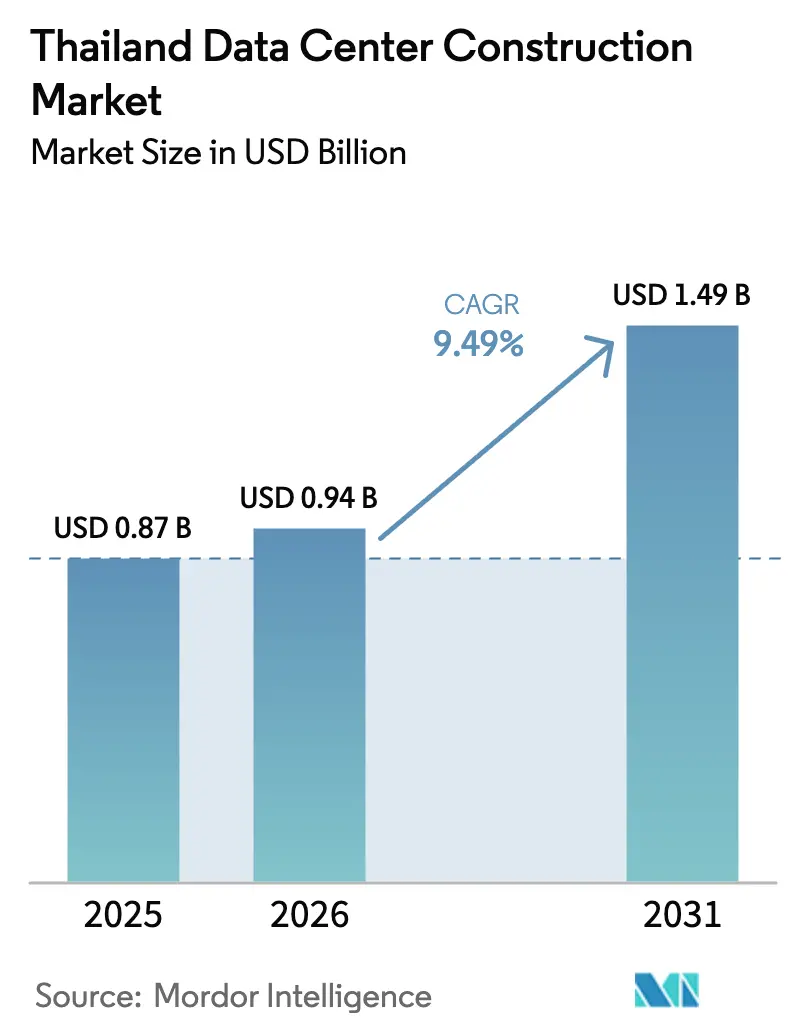

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Data Center Construction Market Analysis by Mordor Intelligence

The Thailand data center construction market size is expected to increase from USD 0.87 billion in 2025 to USD 0.94 billion in 2026 and reach USD 1.49 billion by 2031, growing at a CAGR of 9.49% over 2026-2031. The current expansion reflects cloud‐provider moves to diversify away from saturated Singapore and high-cost Tokyo, the Eastern Economic Corridor’s (EEC) fifteen-year tax holidays, and a dense subsea-cable network that positions the country within one hop of ASEAN’s 680 million consumers. Ongoing enforcement of the Personal Data Protection Act, fast-tracked permitting under the Thailand FastPass program, and a government-approved pipeline of eighty data-center and cloud projects valued at THB 480 billion are further accelerating construction. Electrical systems still command the largest slice of capital budgets, yet liquid-cooling retrofits, modular mechanical systems, and GPU-dense rack designs are rapidly pulling spend toward cooling. Competitive rivalry is intensifying as established colocation operators defend share against hyperscaler captive builds and REIT-backed newcomers, while headline risks around premium electricity tariffs and lengthy 115 kV grid approvals threaten schedules and margins.

Key Report Takeaways

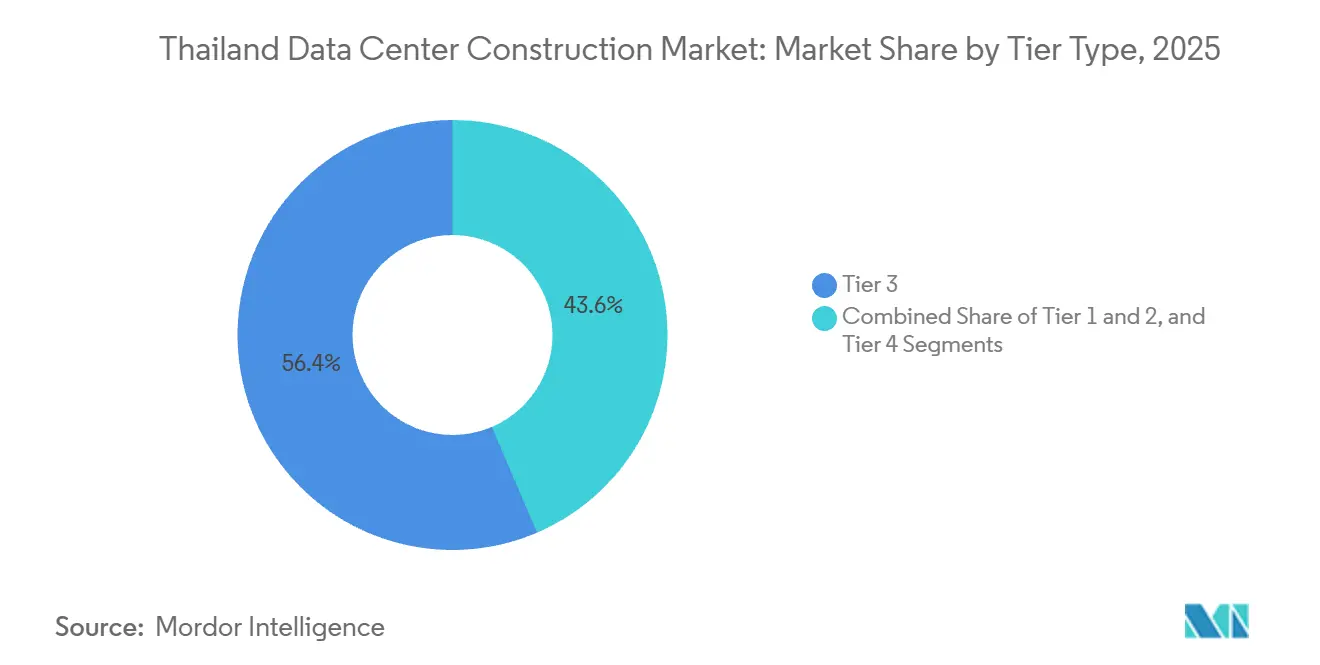

- By tier type, Tier 3 facilities led with 56.43% of Thailand data center construction market share in 2025, while Tier 4 builds are on track for a 10.32% CAGR through 2031.

- By data-center size, large-format facilities held 54.54% of Thailand data center construction market share in 2025, whereas hyperscale campuses are forecast to rise at a 10.64% CAGR through 2031.

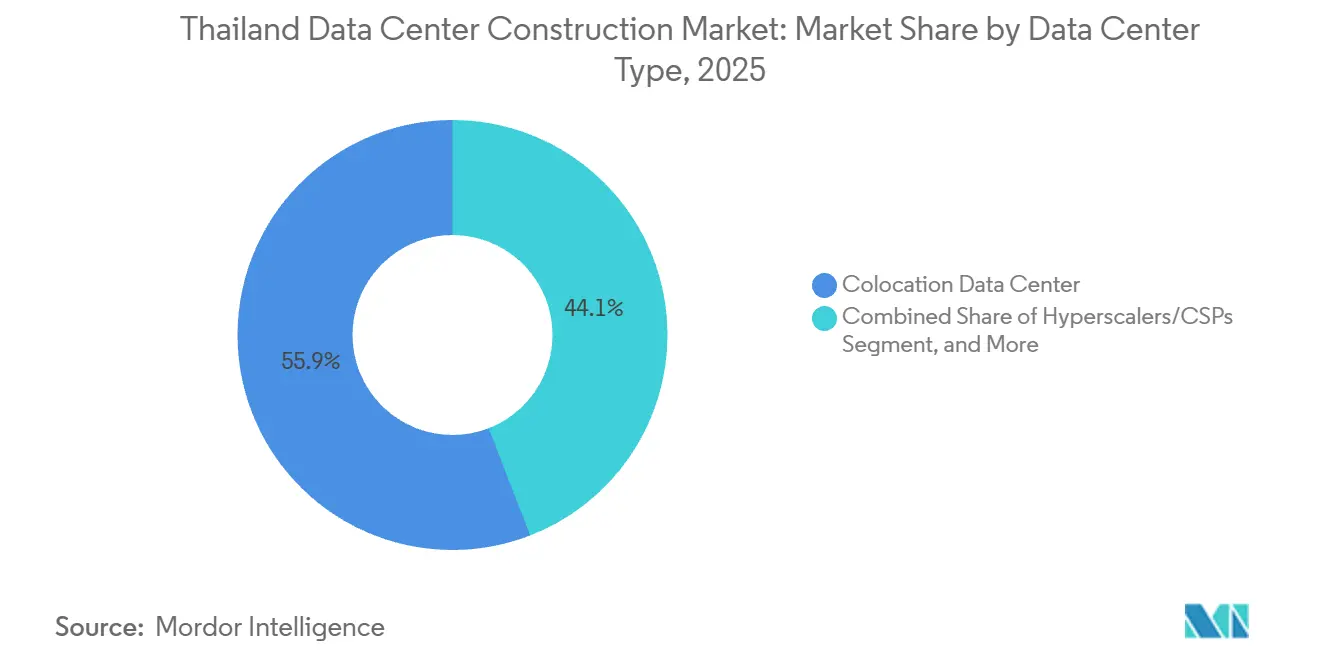

- By data-center type, colocation environments accounted for 55.88% share in 2025, and hyperscaler or cloud-service-provider projects are advancing at a 10.87% CAGR to 2031.

- By infrastructure component, electrical systems captured 39.12% share in 2025, yet mechanical infrastructure is expected to expand at a 10.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensified Cloud-Service Build-Outs by Hyperscalers | +2.8% | National, concentrated in Chonburi, Rayong, and Samut Prakan industrial estates | Medium term (2-4 years) |

| Government Incentives for Eastern Economic Corridor Digital Corridors | +2.1% | Eastern Economic Corridor provinces (Chonburi, Rayong, Chachoengsao), spillover to Bangkok periphery | Long term (≥4 years) |

| Growth in OTT Video Traffic and Edge-Node Demand | +1.5% | National, with urban concentration in Bangkok Metropolitan Region | Short term (≤2 years) |

| Accelerating Liquidity in REIT-Backed Data-Center Real-Estate | +1.2% | National, favoring EEC industrial zones with utility access | Medium term (2-4 years) |

| Mandatory Data-Sovereignty Compliance (PDPA) | +1.0% | National, cross-border data transfer constraints affecting multinational enterprises | Short term (≤2 years) |

| Emerging Quantum-Ready Power and Cooling Standards | +0.9% | National, early adoption in hyperscale and Tier 4 facilities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Intensified Cloud-Service Build-Outs by Hyperscalers

A multibillion-dollar wave of captive infrastructure is reshaping the Thailand data center construction market as Amazon Web Services, Google Cloud, and Microsoft Azure commit to local regions that must meet sovereign-cloud and renewable-energy mandates. The Board of Investment approved USD 2.7 billion in new data center projects in March 2025, including a 300 MW campus in Rayong by Beijing Haoyang, confirming the pull-through effect of hyperscaler anchor tenants. Chonburi and Rayong have emerged as core nodes thanks to land availability, proximity to submarine-cable landing sites, and direct power-purchase pilots that shave 10-15% off grid tariffs.[1]Thailand Board of Investment, “Thailand’s Data Center Investment Boom Continues with USD 2.7 Billion in New Approvals,” boi.go.th Liquid-cooling adoption is quickening in tandem because hyperscalers favor 100 kW-per-rack densities for AI training.[2]STT GDC, “Direct-to-Chip Liquid Cooling Technology at Bangkok 1 Facility,” sttgdc.com Competition for megawatt-scale sites is now spilling into secondary EEC plots as prime parcels sell out.

Government Incentives for Eastern Economic Corridor Digital Corridors

Fifteen-year tax holidays, duty-free imports of IT equipment, and streamlined land-ownership rights underpin the EEC policy package, removing much of the fiscal drag that historically pushed developers into neighboring Malaysia or Vietnam. Digital Park Thailand supplies dark fiber to submarine cable systems and enables qualifying data centers to procure up to 50 MW of renewable power at rates below commercial tariffs. The FastPass framework compresses permitting from eighteen to six months, a critical advantage for hyperscale builds that stage civil, electrical, and mechanical work concurrently. WHA Corporation disclosed land sales of 180 acres to a single data-center customer in 1Q 2025, underscoring sustained appetite for EEC plots. Collectively, these incentives add more than two percentage points to forecast CAGR.

Growth in OTT Video Traffic and Edge-Node Demand

Nationwide internet penetration topped 85% in 2024, and 96% of users stream video, prompting content-delivery networks to cache media closer to subscribers.[3]DataReportal, “Digital 2024: Thailand,” datareportal.com Colocation providers are therefore deploying micro-data centers in Chiang Mai, Phuket, and Hat Yai to cut backhaul latency. Concurrent 5G roll-outs, exceeding 30,000 base stations by mid-2025, intensify the need for distributed compute fabric that can handle real-time analytics. GPU-ready modular enclosures from Schneider Electric and Delta Electronics are gaining traction because they ship with integrated cooling and can be craned into urban rooftops or mall basements. This edge surge keeps Thailand data center construction market activity buoyant even outside the EEC core.

Mandatory Data-Sovereignty Compliance (PDPA)

Full enforcement of the Personal Data Protection Act in March 2024 compels enterprises to host sensitive Thai citizen data onshore or face fines up to THB 5 million, pushing multinational banks and hospitals into domestic colocation suites. Bangkok Bank and Siam Commercial Bank migrated core systems to PDPA-compliant facilities in 2025, locking in multi-year leases that underpin utilization. The Act’s extraterritorial reach forces regional SaaS vendors to place edge nodes locally, advancing the Thailand data center construction market as firms race to secure space that meets ISO 27001 and PCI DSS requirements. Many mid-tier providers seek Tier III certification to monetize this compliance premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Electricity Tariffs versus Regional Peers | -1.8% | National, acute for facilities outside Direct PPA eligibility | Medium term (2-4 years) |

| Lengthy 115 kV Grid-Connection Approval Cycles | -1.3% | National, concentrated in metro Bangkok and EEC industrial zones | Short term (≤2 years) |

| Rising Land Prices in Metro Bangkok | -0.7% | Bangkok Metropolitan Region, Samut Prakan, Pathum Thani | Medium term (2-4 years) |

| Shortage of Uptime-Tier-Accredited Engineers | -0.5% | National, with acute gaps in Tier III and IV facilities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Premium Electricity Tariffs versus Regional Peers

Commercial tariffs averaged THB 4.20 per kWh in 2025, roughly 15-20% higher than Malaysia or Vietnam, driving up total cost of ownership for GPU clusters that draw continuous high loads. EGAT’s direct power-purchase pilot lets qualifying facilities lock in renewable energy at discounts, but the 2 GW program supports fewer than forty large sites, advantaging hyperscalers and leaving mid-tier colocation firms on standard rates. Developers are now exploring on-site solar–plus-battery systems to shave peak demand, though capex adds payback risk. Unless the 2024 Power Development Plan’s 10 GW renewable expansion is accelerated, high tariffs may curb small-format builds.

Lengthy 115 kV Grid-Connection Approval Cycles

A multi-agency sign-off process involving EGAT, the Metropolitan Electricity Authority, and the Provincial Electricity Authority means that energizing lines larger than 20 MW can take 12-18 months. STT GDC’s 24 MW Bangkok 2 project waited 14 months for substation allocation, pushing mechanical handover close to target commissioning. Developers stockpile diesel generators and batteries to guarantee Tier III uptime during the lag but incur 8-12% higher electrical capex. The FastPass scheme promises utility coordination, yet effective relief hinges on synchronizing BOI incentives with regulator capacity planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Gains as AI Workloads Demand Redundancy

Tier 3 installations controlled 56.43% of Thailand data center construction market in 2025, offering enterprises 99.982% service-level agreements without Tier 4’s costlier fault tolerance. Hyperscalers, however, are driving a 10.32% CAGR in Tier 4 builds by insisting on N + N power and cooling to host AI training models at densities that breach 30 kW per rack. SUPERNAP Thailand’s Tier IV Chonburi campus became one of Southeast Asia’s only fault-tolerant sites in 2024, giving operators a blueprint for GPU-ready design. Liquid-cooling retrofits such as the 100 kW-per-rack system deployed by STT GDC in April 2025 further bolster Tier 4 economics by boosting power-usage effectiveness from 1.6 to 1.2.

Tier 1 and Tier 2 footprints, once popular with small enterprises, are declining as workloads consolidate into higher-tier colocation suites. Operators that cannot finance Tier 3 upgrades face acquisition or exit. The investment tilt toward Tier 4 elevates mechanical complexity, encouraging partnership with specialist engineering firms that can certify fault tolerance under Uptime Institute protocols. Over the forecast window, Tier 3 will still anchor the Thailand data center construction market size, but Tier 4 is set to outgrow every other tier as AI adoption accelerates.

By Data Center Size: Hyperscale Builds Reshape Capacity Mix

Large-format facilities (10-50 MW) represented 54.54% of 2025 spending, yet the hyperscale segment, defined as campuses topping 50 MW, is moving at a 10.64% CAGR. Amazon Web Services and Google Cloud have each earmarked multiyear investments exceeding USD 1 billion for hyperscale regions, while Beijing Haoyang’s 300 MW Rayong plan will dwarf existing Thai footprints once completed. The Thailand data center construction market size for hyperscale projects is set to overtake large-format colocation by 2029 if all announced capacity materializes. Modular construction and prefabricated power rooms from Schneider Electric let developers shave deployment cycles by 6 months, a competitive edge when anchor tenants require first-rack delivery within 24 months.

Medium-format (5-10 MW) facilities lag because enterprises either leapfrog directly into public cloud or consolidate workloads into shared 20 MW colocation halls. Small (sub-5 MW) sites now skew toward edge computing and disaster recovery, particularly in Chiang Mai and Phuket, where regional consumer bases justify local caching. Nonetheless, the Thailand data center construction market retains a place for micro-facilities tied to 5G towers and retail hubs, keeping supply chains diverse.

By Data Center Type: Colocation Retains Lead as Hyperscalers Build Captive Capacity

Colocation held 55.88% share in 2025, serving enterprises that prefer operating-expenditure models over ground-up builds. True IDC alone operates more than 49 MW across Bangkok sites and secured a USD 560 million loan in November 2025 to add a 102.6 MW Rayong campus, signaling lender confidence in continued enterprise demand. However, the Thailand data center construction market faces structural bifurcation as hyperscalers erect captive campuses for sovereign-cloud use-cases, bypassing colocation providers for mission-critical AI workloads.

Edge and enterprise facilities, although fragmented, remain crucial for latency-sensitive logistics and retail applications. Containerized builds from Delta Electronics compress civil works to a few weeks, letting retailers place 500 kW pods near distribution hubs. Going forward, colocation operators are layering liquid-cooling and AI-as-a-service offerings to avoid disintermediation and retain wallet share among banks, insurers, and healthcare networks.

By Infrastructure: Mechanical Spend Surges on Liquid-Cooling Adoption

Electrical systems commanded 39.12% of 2025 budgets because 115 kV substations, N + N UPS chains, and diesel gensets remain prerequisites for Tier III compliance. Nevertheless, mechanical outlays are climbing at 10.98% CAGR as direct-to-chip and rear-door liquid coolers enable 100 kW racks that keep pace with GPU roadmaps. STT GDC’s Bangkok 1 retrofit reduced operating PUE from 1.6 to 1.2, cutting annual energy spend 25% and paying back incremental capex inside four years.

Modular mechanical skids slash onsite installation time, a vital benefit because Thailand data center construction market timelines are squeezing under hyperscaler pressure. General construction is shifting to tilt-up concrete and steel frame modules, while service-line design, commissioning, and maintenance command higher margins as engineering complexity mounts. The mechanical emphasis will continue as GPU roadmaps double thermal design power by 2028.

Geography Analysis

The EEC provinces of Chonburi, Rayong, and Chachoengsao are absorbing the bulk of Thailand data center construction market activity, buoyed by fifteen-year tax holidays, duty-free imports, and direct-power-purchase pilots that together cut total project cost by up to 20%. Proximity to the AAG, AAE-1, and MCT cable landing stations lets hyperscalers deliver sub-30 millisecond round-trip latency to Singapore and Ho Chi Minh City, a compelling operational advantage for multinational tenants. Land parcels remain comparatively abundant, though recent transactions show rapid price appreciation as developers race to secure sites before 2027.

Metro Bangkok still hosts over half of the installed IT load because financial services and telecom cores demand sub-5 millisecond response times to the city’s central business district. Yet rising land prices, congested substations, and a twelve-month average wait for building permits are nudging new entrants outward. Grid scarcity compels developers to over-provision diesel backup in Bangkok and Samut Prakan, adding 10% to electrical capex. Many operators, therefore, pre-lease in Rayong while keeping edge pods downtown for latency-critical workloads.

Secondary cities such as Chiang Mai, Phuket, and Hat Yai now attract edge and enterprise-class builds under 5 MW. Retailers, OTT platforms, and logistics providers are placing containerized data centers near regional distribution hubs to trim backhaul costs. These micro-nodes anchor future demand for high-capacity fiber loops and set the stage for a distributed compute layer that complements hyperscale hubs along the EEC. Collectively, geography diversification helps sustain the Thailand data center construction market across varied economic zones.

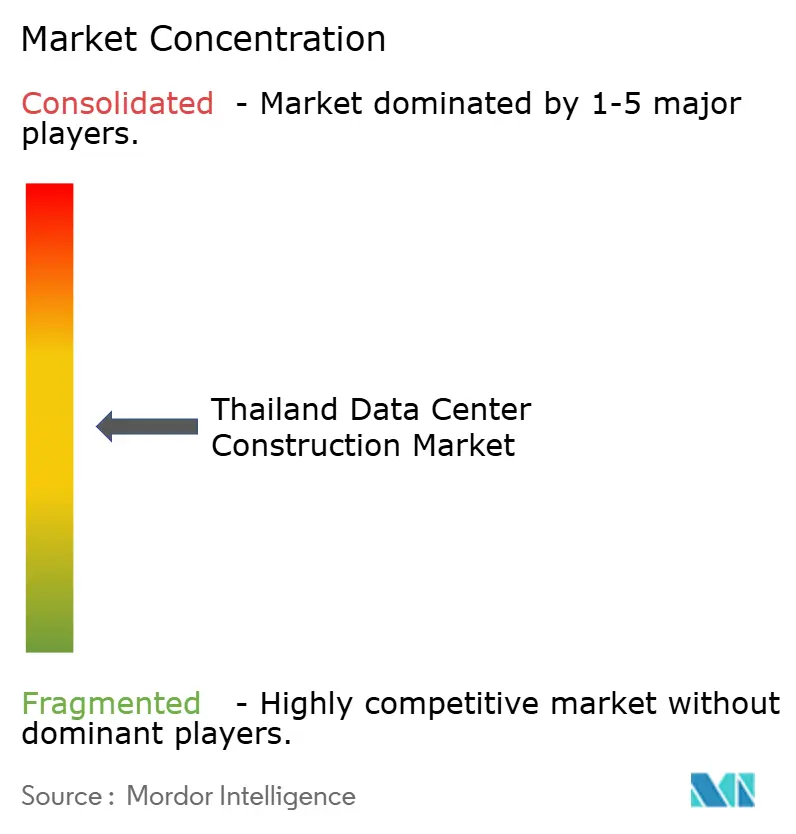

Competitive Landscape

The Thailand data center construction market is moderately fragmented. STT GDC Thailand, True IDC, and SUPERNAP Thailand maintain leadership through Tier III and Tier IV certifications, early adoption of liquid cooling, and anchor-tenant contracts with banks and global SaaS vendors. Technology differentiation is emerging as the decisive wedge; STT GDC’s direct-to-chip system and True IDC’s AI Hyperscale Data Center cater to GPU workloads that legacy air-cooled halls cannot safely host.

Construction contractors such as Thai Kajima, Thai Obayashi, and Syntec pivoted into data-center specialization to offset slowing commercial real-estate demand. Syntec’s THB 455 million Osprey facility employed tilt-up panels, reducing build time to 10 months. Supplier ecosystems expanded in parallel, with Schneider Electric and Delta Electronics delivering prefab power rooms and integrated cooling racks that shrink site work.

REIT-backed entrants like INETREIT inject long-dated capital, enabling bulk land purchases and multi-phase campus rollouts that smaller private players cannot match. Regulatory compliance further segments the field: facilities carrying ISO 27001, PCI DSS, and Uptime Institute stamps command 10-15% rental premiums and enjoy lower churn because PDPA rules lock tenants into certified sites. As a result, mid-tier operators lacking the balance sheet to upgrade toward Tier III standards face acquisition or gradual market exit.

Thailand Data Center Construction Industry Leaders

Syntec Construction PCL

Frasers Property (Thailand) PCL

WHA Corporation PCL

STT GDC Thailand Co., Ltd

NTT Global Data Centers (Thailand) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: True Internet Data Center secured a USD 560 million syndicated loan to fund a 102.6 MW Rayong campus targeting 2027 commissioning.

- November 2025: The Thai government launched the Thailand FastPass program, shortening data-center permit timelines from eighteen to six months and covering eighty projects worth THB 480 billion (USD 13.4 billion).

- May 2025: True Internet Data Center opened its 20-plus MW AI Hyperscale Data Center with Tier III certification and direct 5G connectivity.

- May 2025: WHA Corporation sold 180 acres of EEC industrial land to a data-center developer, earmarking proceeds for utility expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Thailand data center construction market as all capital spending directed toward building new greenfield or major brownfield data center facilities, covering core and shell works, electrical and mechanical fit-outs, and project services, whose primary purpose is to host IT workloads within Thailand's borders.

Scope exclusion: minor equipment refreshes inside already commissioned halls are kept out to avoid double counting.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Size

- Small

- Medium

- Large

- Hyperscale

- By Data Center Type

- Colocation Data Center

- Hyperscalers/Cloud Service Provider (CSPs)

- Enterprise and Edge Data Center

- By Infrastructure

- Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Services - Design and Consulting, Integration, Support and Maintenance

- Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with design-build firms, colocation planners in Bangkok, hyperscaler procurement leads, and regional electrical consultants, spanning interviews across Bangkok, Chonburi, and Chiang Mai. Discussions clarified live ASP spreads per MW, typical contingency buffers, and realistic power-on timelines that literature seldom quantifies.

Desk Research

We began by mapping facility counts, announced pipelines, and average megawatt build costs from open government sources such as the Board of Investment filings, Customs import dashboards, and Egat grid connection data, which are then cross-checked with statistics released by the Digital Economy Promotion Agency. Price trends for steel, switchgear, and CRAC units were gathered from the Ministry of Commerce trade indices and the Thai Contractors Association. To enrich corporate disclosures, our team pulled construction contract values and leaseback details from SET filings, D&B Hoovers, and Dow Jones Factiva. These references illustrate but do not exhaust the secondary pool consulted.

Market-Sizing and Forecasting

A top-down model converts historical MW additions and average cost per MW into 2024 value, which is then validated through sampled supplier roll-ups on generator sets and switchgear. Key variables monitored include Board-approved investment pledges, grid upgrade spending, rack density migration, regulator-mandated PUE targets, and median land prices around the Eastern Economic Corridor. Forecasts employ multivariate regression on these drivers, with scenario pivots for tariff shocks. Bottom-up gaps are filled using sampled EPC order books.

Data Validation and Update Cycle

Outputs pass a two-step peer review, variance checks against fresh BOI approvals, and anomaly flags from our cost tracker dashboard. Reports refresh annually, and we inject mid-cycle revisions whenever investments above USD 200 million close.

Why Our Thailand Data Center Construction Baseline Earns Investor Trust

Published figures often diverge because firms mix total facility investment with fit-out spending or use different cost per MW curves. Our scope fixes on new-build CAPEX only, uses live BOI filings for base year 2025, and updates FX monthly; others may rely on older press mentions or unverified operator quotes. Divergence also stems from how future rack densities and liquid cooling premiums are treated.

In short, our disciplined variable selection, bottom-up reality checks, and faster refresh cadence give decision-makers a balanced, transparent baseline that can be readily traced back to public filings and on-ground cost evidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.87 B (2025) | Mordor Intelligence | - |

| USD 1.56 B (2024) | Global Consultancy A | Bundles retrofit projects and average ASEAN cost curve instead of Thai-specific inputs |

| USD 1.50 B (2024) | Regional Consultancy B | Assumes hyperscalers self-build every announced MW within three years, overstating near-term spend |

In short, our disciplined variable selection, bottom-up reality checks, and faster refresh cadence give decision-makers a balanced, transparent baseline that can be readily traced back to public filings and on-ground cost evidence.

Key Questions Answered in the Report

What is the forecast value of the Thailand data center construction market by 2031?

The Thailand data center construction market is projected to reach USD 1.49 billion by 2031, supported by a 9.49% CAGR.

Which tier category is growing the fastest within Thai data-center builds?

Tier 4 facilities are advancing at a 10.32% CAGR because hyperscalers require full fault tolerance for AI workloads.

How do government incentives influence site selection?

Fifteen-year tax holidays and direct renewable power access in the EEC reduce total project cost by up to 20%, making Chonburi and Rayong preferred locations.

Why are electricity tariffs a restraint for developers?

Commercial tariffs average THB 4.20 per kWh, roughly 15-20% higher than Malaysia or Vietnam, eroding cost competitiveness unless projects qualify for discounted direct PPAs.

What technology shift is shaping mechanical spending?

Direct-to-chip liquid cooling supports 100 kW-per-rack densities, lowering PUE to 1.2 and driving mechanical infrastructure growth at nearly 11% CAGR.

Page last updated on: