Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

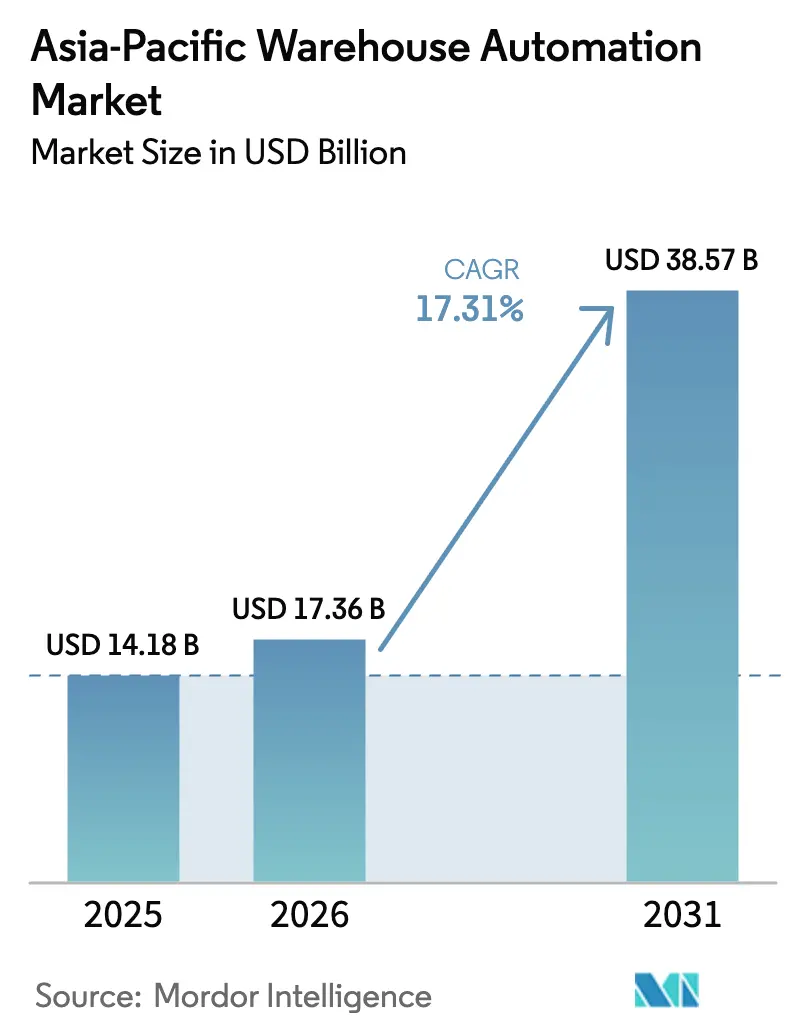

| Base Year Market Size (2025) | USD 14.18 Billion |

| Market Size (2026) | USD 17.36 Billion |

| Market Size (2031) | USD 38.57 Billion |

| Growth Rate (2026 - 2031) | 17.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Warehouse Automation Market Analysis by Mordor Intelligence

The Asia-Pacific warehouse automation market size is expected to increase from USD 14.18 billion in 2025 to USD 17.36 billion in 2026 and reach USD 38.57 billion by 2031, growing at a CAGR of 17.31% over 2026-2031. Elevated e-commerce volumes, urban delivery commitments under two hours, and widespread 5G pilots are accelerating automation investments, especially in micro-fulfillment nodes that shorten the last mile. Hardware keeps the largest revenue pool, yet services are expanding slightly faster as operators lean on integration and predictive maintenance expertise that lowers lifetime costs. Fast-growing grocery fulfillment, tightening cold-chain rules, and green mandates that link future tax incentives to energy-per-order metrics provide sizable opportunities for solution vendors. Competitive intensity is moderate, with Japanese and European incumbents emphasizing reliability while Chinese disruptors compete on price for autonomous mobile robots. Throughout 2026, investors are rewarding suppliers that package automation, software, and financing, an approach that appeals to small and mid-size 3PLs seeking rapid payback.

Key Report Takeaways

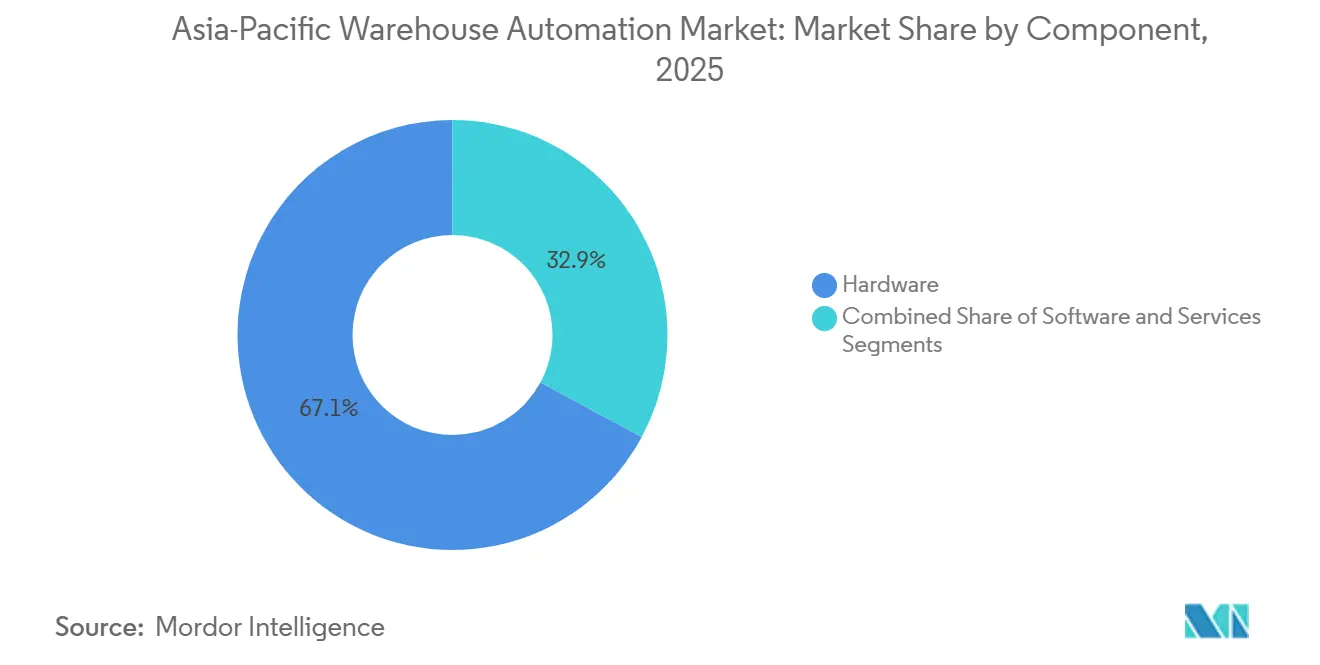

- By component, hardware led with 67.13% of the Asia-Pacific warehouse automation market share in 2025, while services are advancing at a 17.93% CAGR to 2031.

- By end user, food and beverage accounted for 23.44% of the Asia-Pacific warehouse automation market in 2025; groceries are growing at an 18.77% CAGR between 2026-2031.

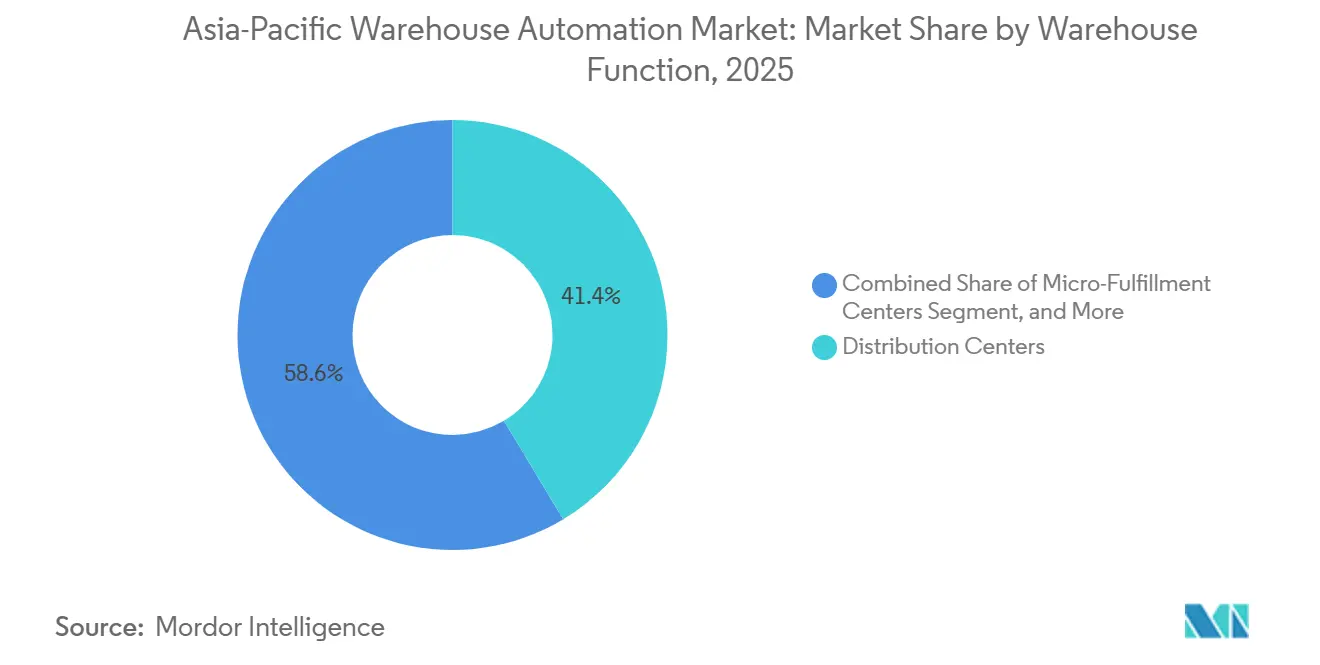

- By warehouse function, distribution centers accounted for 41.38% of revenue share in 2025, but micro-fulfillment centers posted the highest 18.51% CAGR through 2031.

- By warehouse size, large facilities above 250,000 ft² accounted for 46.78% share of the Asia-Pacific warehouse automation market size in 2025, whereas small facilities below 50,000 ft² expanded at 17.92% CAGR.

- By geography, China retained 56.83% of the revenue share in 2025, while India recorded the fastest 18.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Warehouse Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential Growth of the E-commerce Industry and Same-Day Delivery Expectations | +4.2% | China, India, Southeast Asia core, spill-over to Australia | Short term (≤ 2 years) |

| Government Incentives for Smart Manufacturing Under Industry 4.0 Programs | +3.1% | Japan, South Korea, China, India | Medium term (2-4 years) |

| Rising Labor Costs Amid Aging Workforce in Developed Asia-Pacific Economies | +2.8% | Japan, South Korea, Australia, Singapore | Medium term (2-4 years) |

| Surge in Dark Store and Micro-Fulfillment Adoption in Urban Centers | +2.5% | China tier-1 cities, Singapore, Tokyo, Seoul, Sydney | Short term (≤ 2 years) |

| Deployment of 5G Private Networks Enabling Ultra-Low-Latency Warehouse Control | +1.9% | South Korea, China, Japan, early pilots in India | Long term (≥ 4 years) |

| Decarbonization Mandates Driving Automation to Reduce Energy per Order | +1.7% | Japan, South Korea, Australia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Growth of the E-commerce Industry and Same-Day Delivery Expectations

Southeast Asia’s e-commerce gross merchandise value reached USD 139 billion in 2024, a 15% year-on-year jump that tightened delivery windows across Jakarta and Manila.[1]Temasek Holdings, “e-Conomy SEA 2024 Report,” temasek.com.sg During China’s Singles’ Day 2024, platforms processed 2.9 billion parcels in 72 hours, forcing logistics providers to adopt sortation robots capable of handling 30,000 packages per hour. In India, 58% of online shoppers expected same-day service for electronics and apparel orders in 2024, up from 41% two years earlier, putting pressure on warehouses to automate pick-and-pack flows. Amazon India reported that goods-to-person robotics trimmed order-to-dispatch time by 40%, enabling two-hour delivery in 15 metropolitan areas. The surge in urban demand is pushing capital toward micro-fulfillment hubs within 5 kilometers of customers, where automation offsets urban real estate premiums.

Government Incentives for Smart Manufacturing Under Industry 4.0 Programs

Japan earmarked JPY 200 billion (USD 1.8 billion) in fiscal 2024 to subsidize collaborative robots and warehouse execution systems, aiming for 50% logistics automation by 2027.[2]METI Japan, “Connected Industries Initiative,” meti.go.jp China’s 14th Five-Year Plan mandates 70% mechanization in cold-chain warehouses by 2025, accelerating the deployment of shuttles and AS/RS systems that reduce food waste and energy per order. South Korea launched a USD 500 million Smart Logistics Innovation Fund in 2024, covering up to 40% of capital outlays for mobile robots for small and medium operators. India’s Production-Linked Incentive scheme, announced in 2024, provides tax credits equal to 6% of incremental revenue for warehouses installing automation through 2028. These fiscal levers shorten typical payback periods from five years to under three, unlocking projects that mid-tier 3PLs once deemed unaffordable.

Rising Labor Costs Amid Aging Workforce in Developed Asia-Pacific Economies

Japan’s median worker age climbed to 49 years in 2024, and a 6.4 million labor shortfall is projected by 2030, which is expected to lift logistics wages 12% year-over-year.[3]Japan Institute for Labour Policy and Training, “Labor Force Projections 2024-2030,” jil.go.jp South Korea’s working-age population shrank 1.2% in 2024, prompting operators to boost base pay 9% to retain warehouse staff. Australia’s minimum wage rose 5.75% in July 2024, compressing margins for labor-intensive picking operations. Singapore capped foreign-worker ratios in logistics to 35% in 2024, accelerating the adoption of autonomous mobile robots to sustain throughput. Yamato Logistics cut its reliance on temporary staff by 60% after installing 1,000 Geek+ robots across 12 Japanese sites in 2024, lowering parcel labor costs by 18%.

Surge in Dark Stores and Micro-Fulfillment Adoption in Urban Centers

Coles operated 15 automated micro-fulfillment centers in Melbourne and Sydney by mid-2025, each processing 10,000 orders per day within two-hour windows using AutoStore grids. FairPrice Group and Ocado opened a 20,000 m² automated facility in 2024 that assembles 30,000 grocery orders weekly, serving 90% of Singapore within one hour. Alibaba’s Freshippo chain expanded to 350 dark stores by December 2024, where robotic arms reduced order assembly time from 12 minutes to four. JD.com launched 80 micro-fulfillment centers in second-tier Chinese cities during 2024, each under 5,000 ft² and stocked with 3,000 SKUs, trimming last-mile delivery cost by 25%. Vendors report that 62% of Asia-Pacific orders in 2024 came from facilities smaller than 50,000 ft², reversing the previous decade’s focus on mega-sheds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure and Long Payback Periods | -2.3% | India, Southeast Asia, smaller operators across Asia-Pacific | Medium term (2-4 years) |

| Availability of Low-Cost Labor in Emerging Economies | -1.8% | India, Vietnam, Indonesia, Philippines | Short term (≤ 2 years) |

| Complexity of Integrating Legacy IT and OT Systems | -1.4% | Japan, South Korea, established operators in China | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities in Connected Robotic Fleets | -0.9% | Global, with acute risk in Japan, Australia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Long Payback Periods

Installing an automated storage and retrieval system for a 100,000 ft² warehouse typically costs USD 8-15 million, with payback stretching three to five years depending on wage differentials. Autonomous mobile robots price between USD 20,000 and USD 100,000 each, and fleets of 50 units push upfront spend beyond USD 1 million, plus annual software fees near 20% of the hardware cost. Commercial loan rates in India averaged 9.5% in 2024, thereby inflating the weighted-average cost of capital and extending breakeven timelines for thin-margin operators. Robotics-as-a-service contracts at USD 2,000-4,000 per robot per month lower barriers but raise the total five-year cost 20-30%. These financing hurdles leave automation penetration below 12% in Vietnam and Indonesia, despite robust online retail growth.

Availability of Low-Cost Labor in Emerging Economies

Average monthly warehouse wages are USD 180 in India and USD 220 in Vietnam, which is one-fifth of the rates in Japan or Australia, reducing the urgency for automation. Vietnam’s logistics sector employed 1.2 million workers in 2024, and low wages stretch robotic ROI to six-plus years for basic picking tasks. Indonesia’s logistics unemployment rate was 4.8% in 2024, allowing firms to scale manual teams for peak seasons at minimal fixed costs. The Philippines supplies warehouse labor at USD 200-250 per month, undercutting annualized operating costs of a single mobile robot by roughly 40%. Flipkart automated only 18% of its Indian fulfillment footprint in 2024, limiting deployments to high-throughput electronics and grocery zones where volumes justify capex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integration-Heavy Services Gain Ground

Services revenue is growing at a 17.93% CAGR, slightly outpacing hardware’s 17.31% trajectory, as operators discover that successful projects hinge on the smooth integration of legacy ERP, WMS, and OT layers. In 2025, hardware still delivered 67.13% of the Asia-Pacific warehouse automation market, largely because mobile robots, shuttle systems, and conveyors remain the backbone of throughput gains. Mobile fleets alone accounted for 28% of component turnover, buoyed by deployments such as 1,000 Geek+ units at Yamato Logistics, which trimmed processing time by 35%. Software captured 18% market share and is accelerating as real-time control and predictive maintenance mature, evidenced by a 40% jump in Blue Yonder and Manhattan Associates WMS licenses.

System integrators stand to benefit most, as 68% of operators surveyed in 2024 cited IT-OT convergence as their top hurdle. Consulting lines now bundle process redesign, safety certification, and workforce upskilling into multi-year contracts, swelling service margins. Hardware vendors respond by offering end-to-end packages, yet many mid-sized 3PLs prefer neutral advisers who can orchestrate mixed fleets. As warehouse complexity rises and the Asia-Pacific warehouse automation market expands, demand for cyber-secure integration eclipses the allure of marginal mechanical upgrades.

By End-User: Grocery Cold-Chain Automation Accelerates

Grocery stores register the fastest 18.77% CAGR as strict temperature compliance and one-hour delivery windows intensify capital allocation toward mechanized cold storage. Food and beverage retained the largest 23.44% share of the Asia-Pacific warehouse automation market in 2025, underpinned by beverage distributors that streamline repetitive case handling with palletizing robots. State mandates in China require 70% mechanization of cold-chain sites by 2025, prompting carriers like SF Express to adopt multi-zone AS/RS systems with temperature ranges from -25 °C to +15 °C.

Post and parcel accounted for 19% of 2025 revenue, driven by high-speed sorters at hubs processing over 18,000 parcels per hour. Apparel and general merchandise accounted for 22%, but slower automation due to SKU variability complicates robotic grasping. Manufacturing accounted for 16%, with auto and electronics plants using AGVs to improve safety and increase space utilization. Pharmaceuticals, chemicals, and other niches expand on traceability standards that reward automated data capture. Overall, grocery momentum, especially for frozen and fresh produce, is driving the Asia-Pacific warehouse automation market beyond its historical reliance on parcel carriers.

By Warehouse Function: Micro-Fulfillment Outpaces Distribution Giants

Distribution centers still accounted for 41.38% of 2025 revenue, underscoring the need for master hubs that feed regional spokes. Yet micro-fulfillment centers log an 18.51% CAGR, the highest among functions, because urban consumers now value speed over assortment breadth. Goods-to-person workcells in spaces under 10,000 ft² store upward of 20,000 SKUs, delivering pick rates previously achievable only in full-scale facilities.

In Beijing, Singapore, and Sydney, dark stores play a pivotal role in the micro-fulfillment landscape. These stores, strategically located to optimize last-mile delivery, enhance operational efficiency and customer satisfaction. By diversifying revenue streams, this complex arrangement bolsters the stability and resilience of the Asia-Pacific warehouse automation market. It minimizes the risks associated with dependency on a single channel, ensuring the market remains adaptable to changing dynamics and external disruptions.

By Warehouse Size: Small Urban Sites Gain Traction

Large complexes above 250,000 ft² accounted for 46.78% of 2025 turnover, led by mega-distribution facilities processing over 2 million parcels daily. Small sites under 50,000 ft², however, grow fastest at a 17.92% CAGR because inner-city rents push operators to vertical storage, which multiplies cubic capacity. AutoStore grids in Singapore pack 30,000 SKUs into footprints under 10,000 ft², justifying high capex with four-fold density gains.

Japan and South Korea witness the sharpest shift to small formats as zoning limits curb greenfield builds, compelling retrofit solutions with lift heights exceeding 16 bins. In India and parts of Southeast Asia, land availability still favors sprawling sheds, yet rising labor costs and consumer demand for next-day delivery are nudging operators toward compact automated hubs. Vendors now offer plug-and-play packages for ceilings below 8 meters, enabling rapid fit-outs and accelerating the adoption of the Asia-Pacific warehouse automation market.

Geography Analysis

China’s leading 56.83% share in 2025 mirrors its unparalleled e-commerce scale. Cainiao and JD Logistics jointly processed 120 billion parcels in 2024 across 1,200 automated facilities loaded with 200,000 mobile robots, delivering 99.9% accuracy. Cold-chain objectives in the 14th Five-Year Plan compel food distributors to install shuttle systems that cut food waste by 15% while reducing energy per order by 22%. Domestic vendors Geek+ and HAI Robotics supply robots priced 30-40% below foreign rivals, accelerating adoption in second-tier cities and keeping the Asia-Pacific warehouse automation market leadership firmly in Chinese hands.

India follows with the region’s fastest CAGR of 18.56%. Government mega-corridor spending and a 6% production-linked tax credit for logistics automation shorten payback to near three years for mid-tier 3PLs. Amazon will add 15 new fulfillment centers by 2027, Flipkart pledged USD 700 million for automation, and Reliance Retail uses 500 GreyOrange robots to sustain same-day service across 12 metros. While wages remain low, high-throughput segments such as electronics and grocery justify capital outlays, helping India steadily chip away at China’s dominance in the Asia-Pacific warehouse automation market.

South Korea showcases the region’s first large-scale 5G private network at CJ Logistics’ Icheon hub, synchronizing 500 robots with sub-10 ms latency. Australia experiments with decentralized micro-fulfillment, with Coles operating 15 AutoStore cells that serve 90-minute windows across urban corridors. Southeast Asia, grouped as Rest of Asia-Pacific, accelerates sortation automation for Lazada and Shopee hubs, pushing the combined share to 14% and adding diversity to the Asia-Pacific warehouse automation market growth profile.

Competitive Landscape

The competitive field is moderately fragmented. The top five Daifuku, Murata Machinery, Geek+, GreyOrange, and SSI Schaefer commanded 38% revenue in 2025, leaving 62% to niche robotics firms, local integrators, and pure-play software vendors. Japanese and European suppliers highlight safety and ISO 3691-4 compliance, both of which are requirements for insurance coverage in mature markets. Chinese disruptors compete aggressively on price, offering autonomous mobile robots for USD 20,000-35,000, undercutting incumbents by up to 40%. The tug-of-war keeps margins in check but broadens customer choice, driving deeper penetration of the Asia-Pacific warehouse automation market.

Strategy bifurcates into asset-heavy turnkey providers and asset-light subscription models. Daifuku and Murata favor 10-15-year service wraps with guaranteed uptime, stabilizing revenue but requiring large capital budgets from clients. GreyOrange and Locus Robotics promote robotics-as-a-service at USD 2,000-4,000 per robot per month, opening doors for smaller 3PLs but inflating total costs in the longer term. Cybersecurity now influences buying decisions after Daifuku’s 2024 ransomware outage. Vendors rushing to certify under IEC 62443 gain preference among risk-averse operators, nudging the Asia-Pacific warehouse automation market toward more secure architectures.

Partnerships flourish as technology lines blur. AutoStore links with SoftBank Robotics to add mobile manipulators to its cube storage, enabling mixed-SKU pick automation previously limited by gripping constraints. Geek+ partnered with Uniqlo to deploy 800 robots across 10 sites, reinforcing confidence in Chinese tech to Japanese standards. Daifuku’s 60% stake in Godrej Consoveyo strengthens its Indian exposure and tropical-climate engineering capabilities. Funding rounds remain robust. GreyOrange secured USD 135 million in Series D funding during 2025, signaling investor confidence that the Asia-Pacific warehouse automation market retains a multi-year runway.

Asia-Pacific Warehouse Automation Industry Leaders

Daifuku Co., Ltd.

Murata Machinery, Ltd.

Swisslog Holding AG

ABB Ltd.

Toshiba Global Commerce Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Geek+ formed a USD 45 million alliance with Uniqlo to roll out 800 robots at 10 distribution centers in China and Japan, targeting 40% faster fulfillment.

- September 2025: JD Logistics opened a 600,000 m² automated facility in Guangzhou equipped with 250 robots and 12 high-speed sorters, handling 2.5 million parcels daily while cutting energy 22%.

- August 2025: GreyOrange raised USD 135 million in Series D funding to widen robotics-as-a-service offerings across India and Southeast Asia.

- July 2025: Daifuku acquired a 60% stake in India’s Godrej Consoveyo for USD 180 million, adding tropical-climate AS/RS to its portfolio.

Asia-Pacific Warehouse Automation Market Report Scope

The Asia-Pacific Warehouse Automation Market Report is Segmented by Component (Hardware, Software, Services), End-User (Food and Beverage, Post and Parcel, Groceries, General Merchandise, Apparel, Manufacturing, Other End-User), Warehouse Function (Distribution Centers, Fulfillment Centers, Return Centers, Cold Storage Facilities, Micro-Fulfillment Centers, Dark Stores), Warehouse Size (Small, Medium, Large), and Geography (China, India, Japan, South Korea, Australia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware | Mobile Robots (AGV, AMR) |

| Automated Storage and Retrieval Systems (AS/RS) | |

| Automated Conveyor and Sorting Systems | |

| De-palletizing/Palletizing Systems | |

| Automatic Identification and Data Collection (AIDC) | |

| Piece Picking Robots | |

| Software | Warehouse Management Systems (WMS) |

| Warehouse Execution Systems (WES) | |

| Services |

By End-User

| Food and Beverage |

| Post and Parcel |

| Groceries |

| General Merchandise |

| Apparel |

| Manufacturing (Durable and Non-Durable) |

| Other End-User |

By Warehouse Function

| Distribution Centers |

| Fulfillment Centers |

| Return Centers |

| Cold Storage Facilities |

| Micro-Fulfillment Centers |

| Dark Stores |

By Warehouse Size

| Small (Below 50 000 sq ft) |

| Medium (50 000 – 250 000 sq ft) |

| Large (Above 250 000 sq ft) |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Rest of Asia Pacific |

| By Component | Hardware | Mobile Robots (AGV, AMR) |

| Automated Storage and Retrieval Systems (AS/RS) | ||

| Automated Conveyor and Sorting Systems | ||

| De-palletizing/Palletizing Systems | ||

| Automatic Identification and Data Collection (AIDC) | ||

| Piece Picking Robots | ||

| Software | Warehouse Management Systems (WMS) | |

| Warehouse Execution Systems (WES) | ||

| Services | ||

| By End-User | Food and Beverage | |

| Post and Parcel | ||

| Groceries | ||

| General Merchandise | ||

| Apparel | ||

| Manufacturing (Durable and Non-Durable) | ||

| Other End-User | ||

| By Warehouse Function | Distribution Centers | |

| Fulfillment Centers | ||

| Return Centers | ||

| Cold Storage Facilities | ||

| Micro-Fulfillment Centers | ||

| Dark Stores | ||

| By Warehouse Size | Small (Below 50 000 sq ft) | |

| Medium (50 000 – 250 000 sq ft) | ||

| Large (Above 250 000 sq ft) | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific warehouse automation market in 2031?

The sector is expected to reach USD 38.57 billion by 2031, growing at a 17.31% CAGR from 2026 to 2031.

Which end-user category is growing fastest in warehouse automation adoption across Asia-Pacific?

Groceries lead with an 18.77% CAGR through 2031, propelled by stricter cold-chain rules and rapid-delivery models.

How significant is China’s role in regional warehouse automation spending?

China accounted for 56.83% of 2025 revenue, reflecting its vast e-commerce ecosystem and state-backed mechanization targets.

Why are services revenue expanding faster than hardware in the region?

Operators increasingly rely on integration, predictive maintenance, and workforce upskilling, driving services to a 17.93% CAGR.

Which warehouse function records the highest growth rate through 2031?

Micro-fulfillment centers post the fastest rise, logging an 18.51% CAGR as retailers move inventory closer to urban shoppers.

What financing option helps smaller 3PLs adopt automation without large upfront costs?

Robotics-as-a-service subscriptions, typically USD 2,000-4,000 per robot each month, cut capex though raise long-term spend.

Page last updated on: