Taiwan Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 9.79% CAGR |

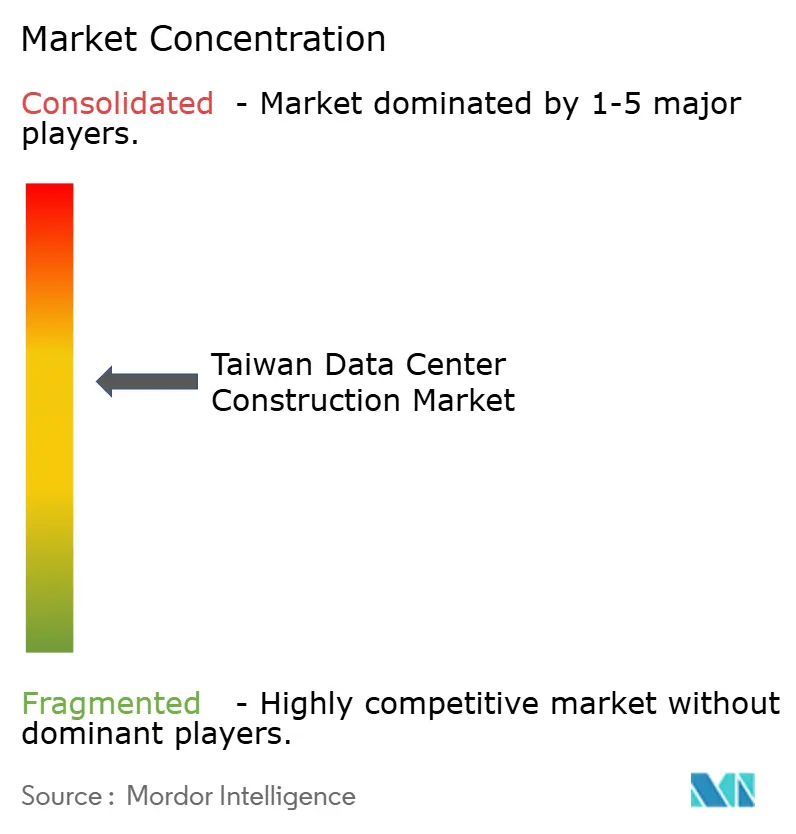

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Data Center Construction Market Analysis by Mordor Intelligence

The Taiwan data center construction market size was valued at USD 0.94 billion in 2025 and estimated to grow from USD 1.03 billion in 2026 to reach USD 1.64 billion by 2031, at a CAGR of 9.79% during the forecast period (2026-2031). This momentum is fueled by Taiwan’s role as a linchpin in the global AI and semiconductor supply chain, its maturing sovereign-AI strategy, and a nationwide shift toward edge computing that is reshaping infrastructure demand. Accelerating cloud-service adoption, dense 5G coverage, and 14 international submarine cables are enabling low-latency connectivity that supports cross-border workloads. Cooling innovation, renewable-energy procurement, and battery energy-storage pilots are addressing power density and sustainability challenges. Meanwhile, geopolitical risk is prompting hyperscalers to prioritize sovereign capacity that can operate independently from external jurisdictions, driving continued private and government capital inflows into the Taiwan data center construction market.

Key Report Takeaways

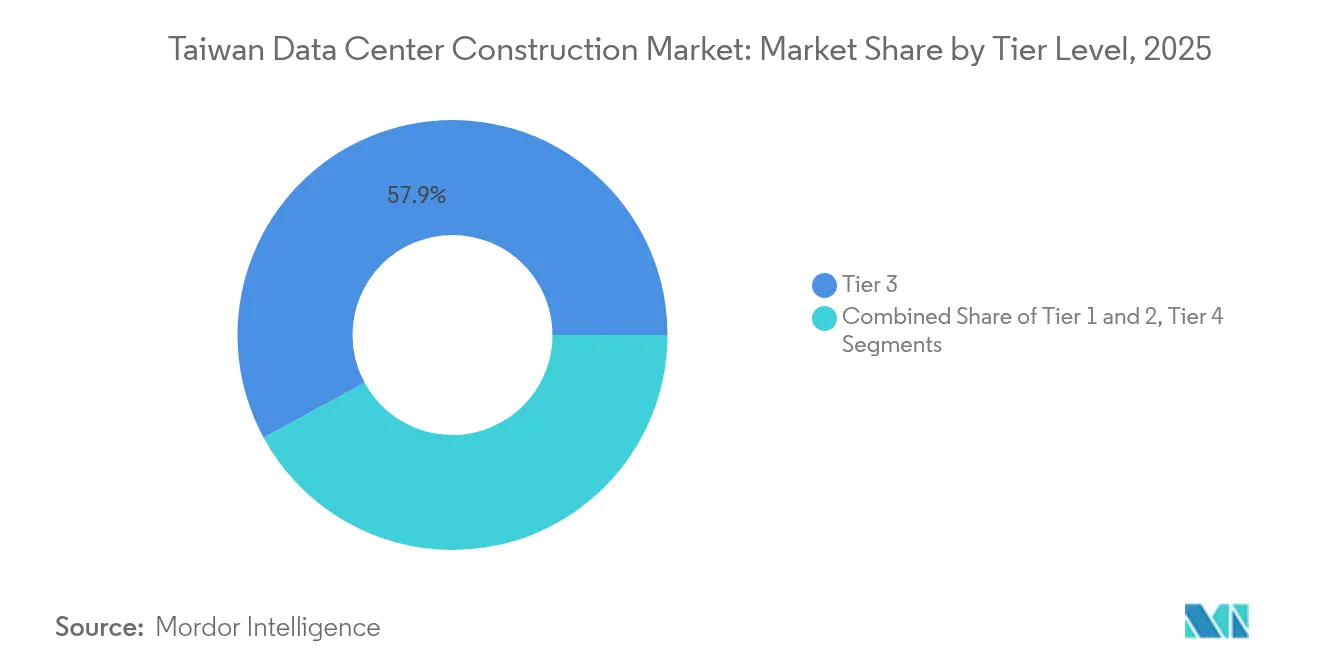

- By tier type, Tier 3 facilities led with 57.92% revenue share in 2025; Tier 4 installations are projected to advance at a 9.86% CAGR through 2031.

- By data center type, colocation held a 53.95% share of the Taiwan data center construction market size in 2025, while self-built hyperscalers are expected to grow at a 10.04% CAGR.

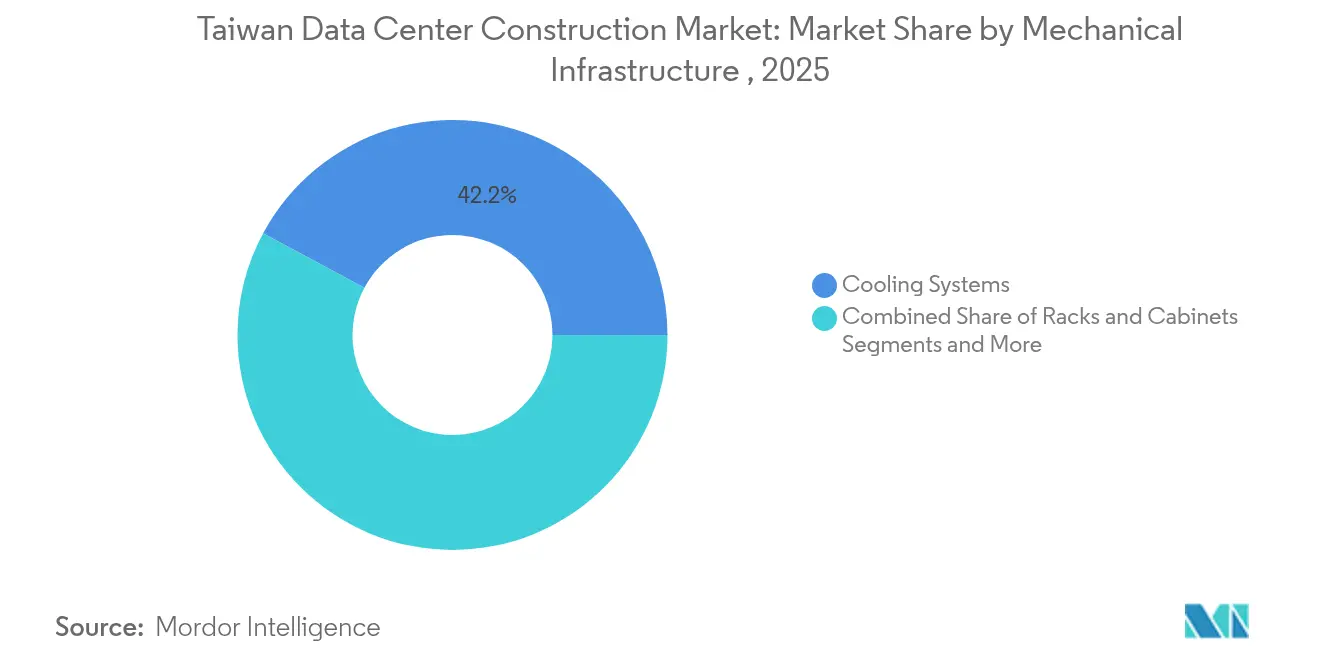

- By mechanical infrastructure, cooling systems accounted for 42.15% share of the Taiwan data center construction market size in 2025; servers and storage components are developing at a 10.34% CAGR.

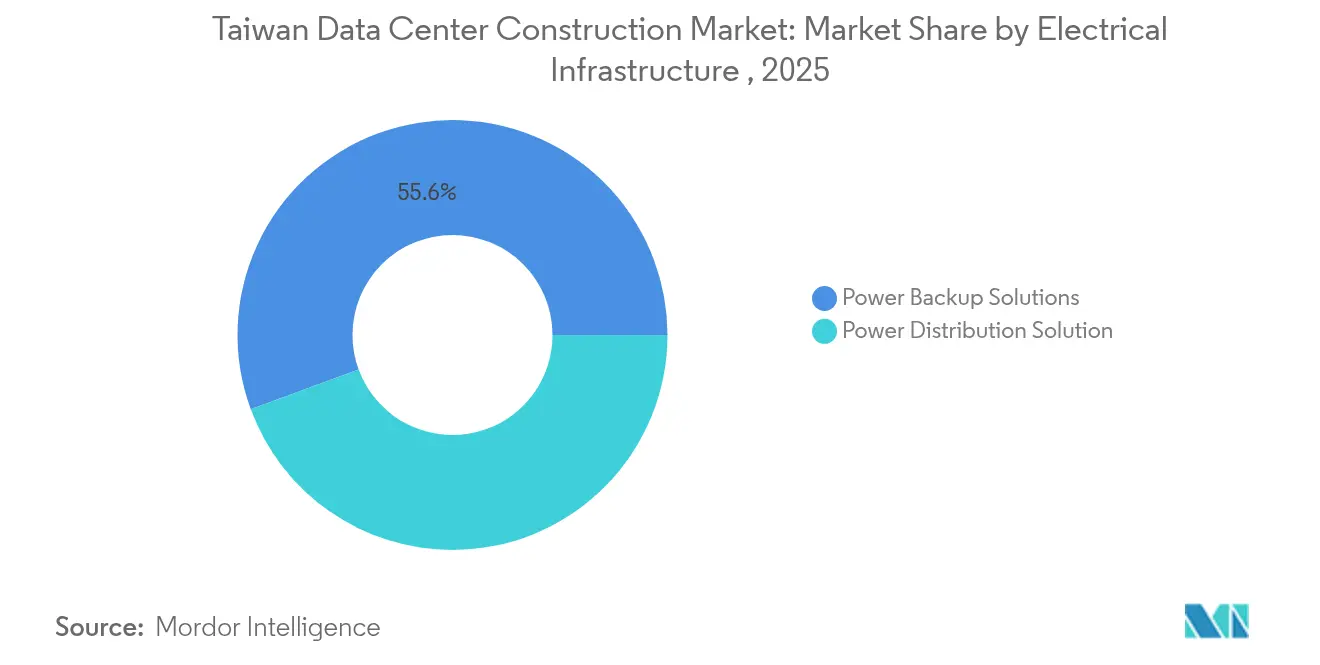

- By electrical infrastructure, power backup solutions captured 55.62% of the Taiwan data center construction market share in 2025, whereas power-distribution solutions are expanding at an 10.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cloud-service adoption | +2.8% | Taipei metro, Hsinchu Science Park | Medium term (2-4 years) |

| 5G rollout and national digitisation initiatives | +2.1% | Taipei, Taichung, Kaohsiung | Short term (≤ 2 years) |

| Government tax-rebate programme for green DC builds | +1.5% | Science parks and industrial zones | Long term (≥ 4 years) |

| Semiconductor-driven edge/AI workload localisation | +3.2% | Hsinchu, Taichung, expanding to Tainan | Medium term (2-4 years) |

| New submarine-cable landings lowering latency | +1.8% | Northern and central coastal regions | Long term (≥ 4 years) |

| Grid-level BESS pilots enabling >50% renewable integration | +1.4% | Yilan, Hsinchu, Taoyuan, Tainan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-Service Adoption

Cloud-service penetration is extending beyond conventional enterprise migrations as data-sovereignty policies mandate local processing of sensitive IP and citizen data. Amazon Web Services committed USD 5 billion for its first Taiwanese region with three availability zones, confirming long-term confidence in the Taiwan data center construction market.[1]Tim Culpan, “AWS to invest USD 5 billion in Taiwan region,” aws.amazon.comHybrid and multi-cloud strategies dominate in semiconductor design, where air-gapped networks and low-latency connections to nearby fabs remain essential. Colocation operators are adding direct cloud on-ramp nodes that satisfy both compliance and performance needs. Government programs aiming for 80% uptake of digital lifestyle services further guarantee demand for scalable facilities.

5G Rollout and National Digitization Initiatives

Taiwan achieved 94% 5G coverage in 2024, and more than 16,000 base stations now blanket the island, creating a foundation for edge-computing workloads that must be processed locally within milliseconds. Telecoms such as Chunghwa Telecom have coupled 5G with all-photonics backbone networks and low-earth-orbit satellite backup, reducing latency for critical applications. Smart-manufacturing pilots that rely on 5G edge nodes have already cut traffic-signal wait times by 35%, proving the practical value of micro data centers in urban corridors.

Government Tax-Rebate Programme for Green DC Builds

A tiered incentive grants 5%–20% tax credits on capital and operational expenditure for data centers that achieve stringent PUE and renewable-energy goals.[2]Ministry of Finance R.O.C., “Green data center tax incentives,” mof.gov.tw Google’s 500 MW offshore-wind PPA with Copenhagen Infrastructure Partners underscores how foreign operators leverage the scheme to green their footprints. Facilities meeting Taiwan’s EEWH Gold or Diamond standards can tap accelerated depreciation, which lowers build-out payback periods and propels the Taiwan data center construction market toward more sustainable designs.

Semiconductor-Driven Edge/AI Workload Localization

Taiwan Semiconductor Manufacturing Company is adding 11 wafer-fabrication plants and four advanced-packaging lines that must interface with design verification and AI training clusters on-site. AI inferencing adjacent to fabs reduces design turnaround and IP-leak risk, prompting demand for high-tier facilities equipped with precision cooling and seismic damping. Government-backed sovereign-AI projects plan 1,200 petaflops of public compute by 2029, cementing a long runway for the Taiwan data center construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power scarcity and volatile electricity pricing | -2.4% | Island-wide, acute in science parks | Short term (≤ 2 years) |

| Scarce land and escalating Taipei metro real-estate costs | -1.8% | Taipei, New Taipei, Taoyuan | Medium term (2-4 years) |

| High seismic-design CAPEX for Tier III/IV facilities | -1.2% | Seismic zones nation-wide | Long term (≥ 4 years) |

| Slow EIA permitting for hyperscale campuses | -0.9% | Projects above 50 MW | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Power Scarcity and Volatile Electricity Pricing

Electricity demand is expected to climb 12%–13% by 2030, largely from AI compute clusters.[3]Energy Administration, “Electricity demand forecast 2025-2030,” energy.gov.tw Imported fossil fuels still make up 83% of the energy mix, exposing operators to commodity-price swings and supply risks. Battery-energy storage rollouts totaling 160 MW offer limited relief. Repeated summer reserve-margin shortfalls are forcing projects to integrate on-site solar, wind, and liquid-cooling systems that cut facility power envelopes. Those mitigation costs temporarily weigh on the Taiwan data center construction market, yet they also accelerate the adoption of more efficient designs.

Scarce Land and Escalating Taipei Metro Real-Estate Costs

Downtown parcel scarcity is pushing new builds toward Taoyuan, Taichung, and Kaohsiung. Amazon Web Services chose a suburban Taoyuan industrial park for its region, reflecting the pivot to locations that balance cost and fiber proximity. Science parks provide pre-approved zoning, though competition with semiconductor expansions intensifies bidding. Developers respond with multi-story layouts and higher rack densities to maximize limited footprints, a trend that is now standard across the Taiwan data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Growth Accelerates Despite Tier 3 Dominance

Tier 3 facilities maintained a 57.92% stake of the Taiwan data center construction market in 2025, signaling client preference for balanced uptime and cost. This translates to the largest contribution to the overall Taiwan data center construction market size. Financial institutions, hyperscalers, and government bodies, however, are driving Tier 4 demand with an anticipated 9.86% CAGR. Seismic-resistant engineering that surpasses nuclear-plant standards is mandatory, and builders employ viscous-fluid dampers and dual active-active grids to meet Tier 4 certification.

Seismic retrofits for older Tier 3 shells allow modular upgrades to near-Tier 4 capability, illustrating a shift toward resilient brownfield expansion. Contract-win criteria now emphasize verifiable seismic isolation and in-rack liquid cooling. Builders adding these features position themselves for higher-margin Tier 4 contracts, reinforcing a premium tier that the Taiwan data center construction market will continue to reward as AI workloads intensify.

By Data Center Type: Hyperscaler Self-Build Momentum Challenges Colocation Leadership

Colocation retained 53.95% of 2025 revenue as SMEs and semiconductor suppliers favor shared facilities for cost control. This portion underscores how colocation remains a linchpin in the Taiwan data center construction market. Nevertheless, self-built hyperscaler campuses are set to outpace all other formats at a 10.04% CAGR. Amazon, Google, and Microsoft increasingly favor outright ownership to secure compliance and optimize AI training clusters, bringing bespoke power and cooling.

Enterprise edge deployments are evolving fastest in design. Telecoms are installing micro data centers at 5G base stations to host latency-sensitive workloads. These edge nodes feature prefabricated, two-rack enclosures with integrated liquid cooling, reflecting how diversified architectures extend the physical scope of the Taiwan data center construction market.

By Electrical Infrastructure: Power Distribution Innovation Drives Grid Modernization

Backup generators, UPS strings, and static transfer switches formed 55.62% of the 2025 spend, illustrating the priority placed on availability. Battery-storage pilots are embedding lithium-iron-phosphate chemistries that allow rapid response to grid disturbances. Power-distribution units are on a trajectory to log 10.98% CAGR, lifted by smart-switchgear adoption that mitigates intermittent renewable feeds.

Projects now require busway systems rated above 6,000 A and intelligent power quality monitoring. These specifications are becoming the baseline for any facility seeking long-term power purchase agreements tied to renewables. The electrical segment, therefore, stands at the forefront of technological upgrades that buttress the Taiwan data center construction market.

By Mechanical Infrastructure: Cooling Innovation Responds to AI Density Demands

Cooling represented 42.15% of mechanical spend in 2025, and immersion plus direct-to-chip solutions are gaining ground. Liquid cooling removes thermal limits that once capped rack power at 15 kW; Foxconn’s upcoming 100 MW supercomputing center will run at over 70 kW per rack. Servers and storage sub-systems will exhibit 10.34% CAGR because advanced GPUs and high-bandwidth memory demand bespoke configurations.

Vendors are shipping compact brushless pumps and integrated CDU-plus-rack assemblies that can be field-retrofit, letting legacy sites raise densities without floor-plan increases. Such innovations demonstrate why thermal management continues to define competitive differentiation in the Taiwan data center construction market.

Geography Analysis

Taipei and New Taipei host the highest facility count, leveraging dense fiber backbones and financial-sector proximity. However, land costs and grid constraints encourage a southward migration. Hsinchu Science Park links directly to semiconductor fabs, which fuels the fastest regional facility additions at mid-double-digit megawatt bookings. Taichung offers lower real-estate prices and grid headroom, functioning as a central corridor that bridges northern and southern workloads.

Southern Taiwan Science Park in Tainan benefits from government plans to install a 120-petaflop AI center by 2025 and a sovereign-cloud complex by 2029, both of which anchor forthcoming demand. Offshore-wind zones along the west coast supply up to 500 MW of contracted energy for hyperscale campuses, aligning geography with renewable goals. Coastal cable-landing stations at Toucheng, Fangshan, and Tamsui safeguard latency to North Asia and the United States, ensuring that distributed builds still maintain carrier-neutral reach.

Reclaimed-water programs and desalination plants add 628,100 tons per day of non-potable water, guaranteeing chiller make-up for high-density sites. This resource diversification further stabilizes operational risk across the Taiwan data center construction market. As a result, Taiwan is evolving from a single-hub model into a three-node topology of north, central, and south that balances power, land, and connectivity.

Competitive Landscape

The Taiwan data center construction market features a mid-level concentration where local EPC firms, international engineering specialists, and equipment vendors converge. United Integrated Services, TECO, and CTCI hold large backlogs linked to semiconductor clients, while global groups such as Exyte bring clean-room pedigrees required for on-fab data halls. Schneider Electric, ABB, and Delta Electronics embed power and cooling gear, bundling design-build packages that shorten project delivery.

Sustainability credentials increasingly decide bid outcomes. Firms demonstrating sub-1.3 PUE designs and renewable-PPA arrangements gain preferred-vendor status under Taiwan’s green-build incentives. Liquid-cooling consortia comprising Foxconn, Nvidia, and CoolIT Systems showcase the synergy between hardware providers and general contractors. Edge-facility specialists like Advantech are partnering with telecoms to deploy containerized units that align with 5G rollouts.

Taiwan Data Center Construction Industry Leaders

TECO Corporation

CTCI Group

M+W Group

Exyte

AECOM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Foxconn and Nvidia confirmed plans for a 100 MW AI supercomputing center using 10,000 Blackwell GPUs in Kaohsiung.

- June 2025: Amazon Web Services pledged USD 5 billion to build Taiwan’s first AWS region featuring three availability zones.

- May 2025: The government launched the ‘AI Next’ program, listing ten strategic AI infrastructure projects and targeting 1,200 petaflops by 2029.

- April 2025: Google executed a 500 MW offshore-wind PPA with Copenhagen Infrastructure Partners to power local data centers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Taiwan data-center construction market as the capital spending required to plan, design, erect, equip, and commission new green-field or major brown-field facilities whose primary function is to host IT workloads. The spending pool covers civil works, electrical distribution and backup, mechanical cooling, racks, and project services across colocation, hyperscale cloud, enterprise, and edge builds.

Scope exclusion: Ongoing operations, retrofit maintenance, and pure land-acquisition costs are not counted.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

We interviewed project engineers at local electrical contractors, facility design consultants, and procurement managers at colocation operators across Taipei, Taoyuan, and Kaohsiung. Follow-up surveys with global UPS, chiller, and rack vendors validated equipment share, lead-time shifts, and typical cost per square meter assumptions, ensuring region-specific inputs echoed on-ground realities.

Desk Research

Analysts began with public sources such as Taiwan's Ministry of Economic Affairs investment filings, National Communications Commission telecom statistics, international trade customs records, and energy-usage disclosures from the Bureau of Energy. Industry material from bodies such as the Asia Cloud & Data Center Association, academic papers indexed in IEEE Xplore, and company 10-K or prospectus filings enriched the demand picture. Paid databases, D&B Hoovers for contractor revenues and Dow Jones Factiva for project news, supplied additional granularity. This list is illustrative; many further references supported validation and clarification efforts.

Market-Sizing & Forecasting

A top-down build started with publicly disclosed annual project completions, power capacity adds, and average construction cost per MW to reconstruct total spend. These results were cross-checked with selective bottom-up rollups from sampled contractor revenues and average selling-price times volume data for key equipment lines. Key model variables include commissioned IT load (MW), average fit-out intensity (US$ per MW), Tier-standard mix, green-design adoption rate, and Taipei land-availability index. A multivariate regression relating spend to MW adds and Tier mix underpins forecasts, with scenario overlays reflecting currency movements and steel cost shifts. Gaps in bottom-up data were bridged by benchmarking against regional projects of similar scale and adjusting for Taiwan's higher seismic-proofing requirements.

Data Validation & Update Cycle

Outputs pass successive analyst reviews that test coherence with build-cost benchmarks, vendor backlog disclosures, and macro indicators. Variances beyond ±7 percent trigger re-contacts with primary respondents. Mordor Intelligence refreshes this dataset each year, releasing interim updates after material policy or mega-project announcements. A final pre-publication sweep assures clients receive the latest validated view.

Why Mordor's Taiwan Data Center Construction Baseline Stands Firm

Published values often diverge because firms embrace different cost scopes, geography filters, and refresh cadences.

Key gap drivers stem from including multi-year service contracts, combining renovation outlays with new builds, or applying global cost per MW benchmarks without Taiwan-specific seismic and power-quality premiums. Mordor analysts limit the scope to first-year capital outlay, apply local cost curves vetted through supplier interviews, and update annually, which narrows uncertainty.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.94 B (2025) | Mordor Intelligence | |

| USD 1.85 B (2024) | Regional Consultancy A | Combines land purchase and full life-cycle CapEx, inflating base |

| USD 2.50 B (2024) | Global Consultancy B | Adds multi-year facility-management contracts and global cost averages |

The comparison shows that once ancillary costs are stripped out and Taiwan-specific premiums are applied, Mordor's balanced, transparent baseline offers decision-makers a reliable yardstick grounded in verifiable variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Taiwan data center construction market?

The market stands at USD 1.03 billion in 2026 and is projected to reach USD 1.64 billion in 2031.

Which tier classification leads the market?

Tier 3 facilities hold 57.92% revenue share, reflecting balanced reliability and cost performance.

How fast is the Hyperscaler self-build segment growing?

Self-build campuses are forecast to expand at a 10.04% CAGR through 2031, outpacing all other data-center types.

Why are liquid-cooling systems gaining traction in Taiwan?

High GPU densities, warm climate, and power constraints make liquid cooling essential for efficient heat removal and lower PUE.

Page last updated on: