Thailand CRM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

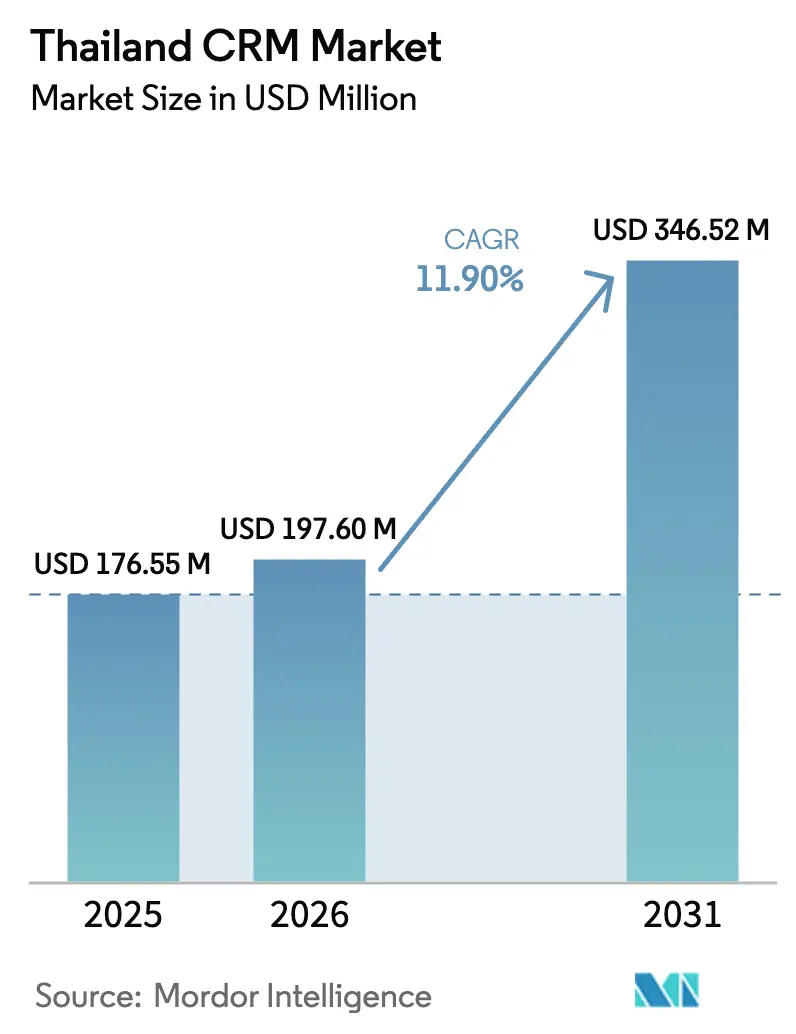

| Base Year Market Size (2025) | USD 176.55 Million |

| Market Size (2026) | USD 197.6 Million |

| Market Size (2031) | USD 346.52 Million |

| Growth Rate (2026 - 2031) | 11.90% CAGR |

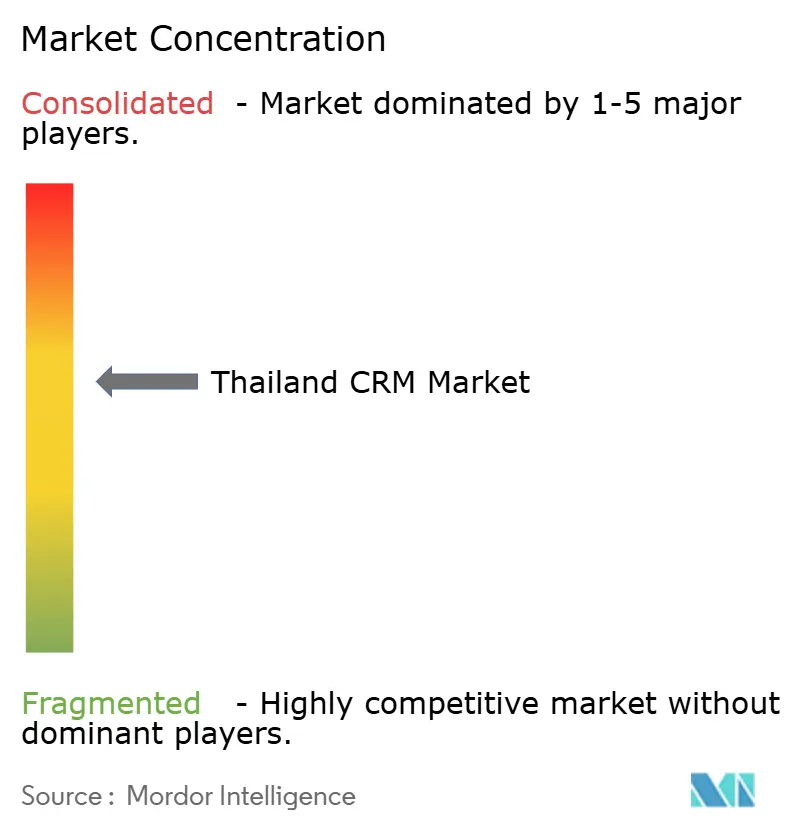

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand CRM Market Analysis by Mordor Intelligence

The Thailand CRM market size is expected to grow from USD 176.55 million in 2025 to USD 197.6 million in 2026 and is forecast to reach USD 346.52 million by 2031 at 11.90% CAGR over 2026-2031. Strong government backing through Thailand 4.0, mandatory PDPA compliance, and soaring Line Official Account (OA) usage are accelerating enterprise spending on cloud-native customer-relationship platforms. Rapid SME cloud migration, large-scale investments by BFSI incumbents, and social-commerce integration needs continue to anchor demand. Competition is intensifying as global vendors launch local data centers while domestic specialists leverage Thai-language functionality and deep cultural insight. Structural headwinds, talent shortages, legacy ERP constraints, and patchy regional broadband temper growth yet simultaneously create service opportunities for managed-integration providers. Overall, the Thailand CRM market shows a clear trajectory toward data-driven, AI-powered engagement as enterprises seek scalable platforms that balance compliance with omnichannel agility.

Key Report Takeaways

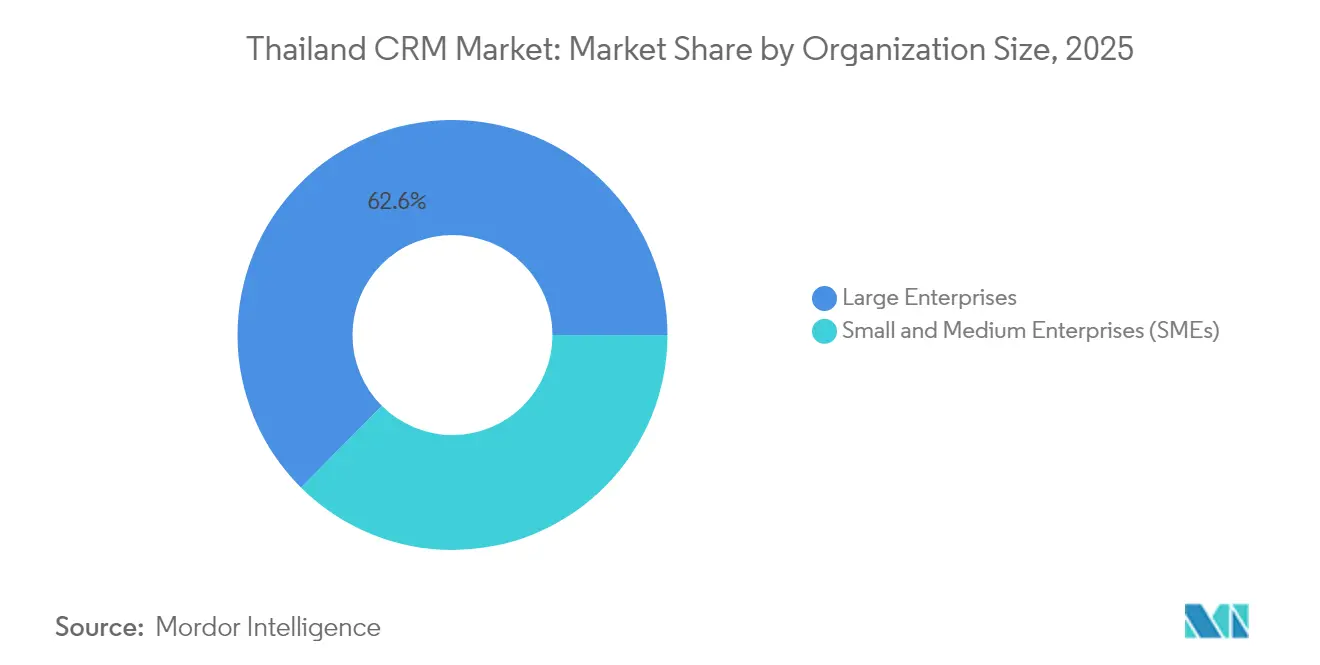

- By organization size, large enterprises held 62.55% of the Thailand CRM market share in 2025, while SMEs are expanding at a 12.68% CAGR through 2031.

- By deployment mode, cloud accounted for 62.20% of the Thailand CRM market size in 2025, and hybrid solutions are set to grow fastest at a 13.05% CAGR to 2031.

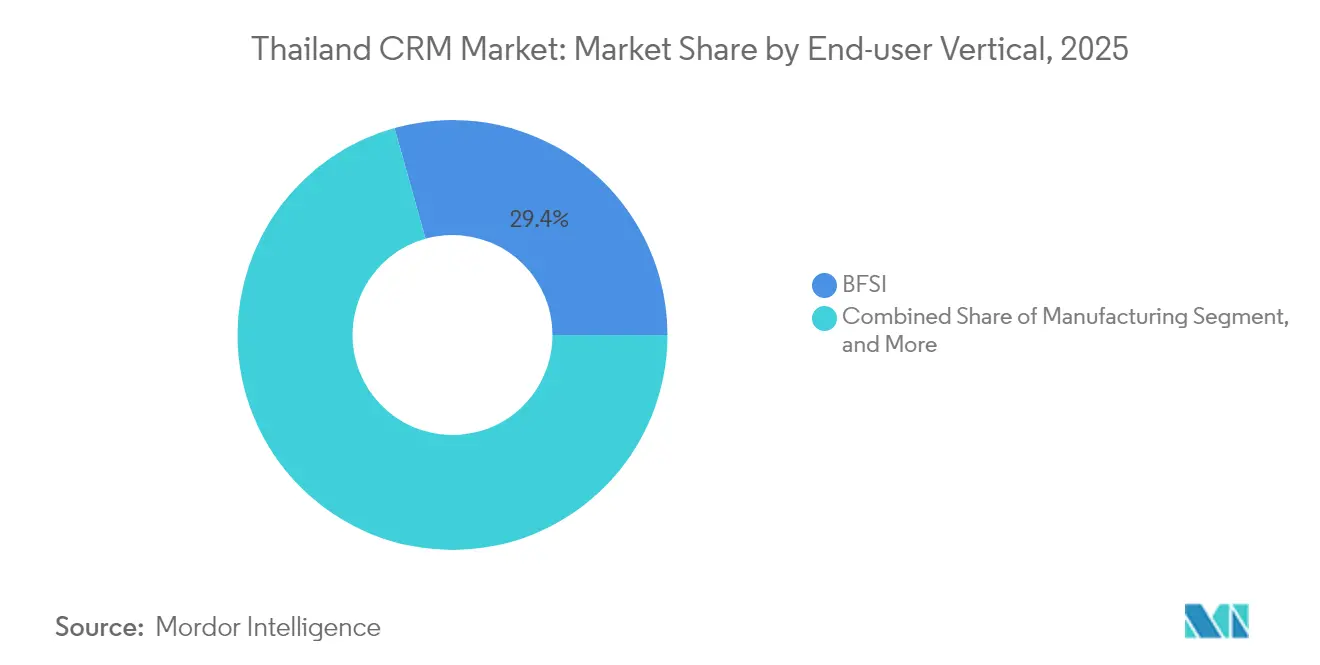

- By end-user vertical, BFSI led with 29.35% revenue share of the Thailand CRM market in 2025; retail and e-logistics are projected to climb at a 13.46% CAGR through 2031.

- By CRM function, Salesforce automation captured 36.05% of the Thailand CRM market size in 2025, whereas analytics and reporting are advancing at a 13.28% CAGR to 2031.

- By region, Bangkok and the Central regions commanded 48.10% of the Thailand CRM market share in 2025; the Eastern Economic Corridor is registering the highest 13.39% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand CRM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud-based CRM among Thai SMEs | +2.1% | National, concentrated in Bangkok and EEC | Medium term (2-4 years) |

| Government's Thailand 4.0 digital-transformation push | +1.8% | National, with priority zones in EEC and innovation districts | Long term (≥ 4 years) |

| Mobile-first consumer behaviour driving omnichannel CRM | +1.6% | National, strongest in urban centers | Short term (≤ 2 years) |

| Surge in Line OA social-commerce integrations | +1.4% | National, particularly strong in retail hubs | Short term (≤ 2 years) |

| Thai-language NLP chatbots unlocking analytics value | +1.2% | National, with early adoption in BFSI and retail | Medium term (2-4 years) |

| Loyalty-as-a-Service uptake with tourism rebound | +0.9% | Tourism-concentrated regions, Bangkok, Southern Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of cloud-based CRM among Thai SMEs

Soft-loan programs offering 1% interest and locally hosted hyperscale infrastructure have combined to remove historic cost and data-sovereignty barriers for small firms.[1]Bangkok Post, “SMEs Lag Behind in Using AI, Robotics,” bangkokpost.com Thai vendors such as Zanroo and Choco CRM provide native language interfaces and templated workflows that slash implementation time. The result is a decisive shift away from on-premise installations toward subscription-based platforms that deliver predictable cash-flow benefits and automatic feature updates. As cloud penetration rises, vendors offering bundled managed services gain traction among SMEs with minimal in-house IT resources.

Government’s Thailand 4.0 digital-transformation push

Policies under Thailand 4.0 embed digital-first standards across public procurement, e-government, and new virtual-bank licensing, compelling private firms to match service-delivery benchmarks. Enterprises integrating CRM platforms now view compliance with government digital expectations as table stakes for bidding on contracts and maintaining competitive relevance. Long-term stimulus funding and regulatory clarity ensure durable market momentum even during broader economic cycles.

Mobile-first consumer behavior driving omnichannel CRM

Line’s near-universal reach continues to reshape customer-journey expectations that require real-time integration across chat, mobile payments, and location-based offers.[2]klink.cloud, “Line App in Thailand: Key to Successful Omnichannel Customer Support,” klink.cloud Businesses now demand CRM suites that consolidate social and physical-store touchpoints to deliver consistent service and mitigate churn. Failure to unify interactions across Line, voice, email, and QR-code payments risks immediate customer attrition, elevating omnichannel orchestration from an optional feature to a core requirement.

Surge in Line OA social-commerce integrations

Line OA has emerged as Thailand’s pre-eminent social-commerce channel, enabling integrated messaging, payments, and inventory visibility inside one app. Retailers like Central Group restructured workflows around real-time Line data, driving adoption of CRM platforms capable of ingesting transaction streams and supporting individualized promotions. Enterprises lacking Line OA connectivity are increasingly excluded from Thailand’s digital commerce landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of skilled CRM implementation consultants | -1.8% | National, most acute outside Bangkok | Long term (≥ 4 years) |

| Data-privacy compliance burden after PDPA enforcement | -1.2% | National, with varying enforcement intensity | Medium term (2-4 years) |

| Legacy Thai-script ERP systems with limited API support | -0.9% | National, concentrated in traditional industries | Long term (≥ 4 years) |

| Patchy broadband outside Bangkok hurting SaaS uptime | -0.7% | Regional, primarily Northern and Northeastern Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of skilled CRM implementation consultants

The talent pool remains shallow: local consultancies average fewer than 10 certified specialists, extending deployment cycles and inflating project costs.[3]Salesforce AppExchange, “CRM-C: Thai and International CRM Consultant,” salesforce.com Offshore firms bridge gaps yet face cultural and language barriers, compelling many enterprises to adopt vendor-managed services that raise long-run operating expenses.

Data-privacy compliance burden after PDPA enforcement

PDPA’s stringent consent, audit, and data-residency rules mandate extensive re-engineering of CRM workflows and add certification costs, especially for SMEs. Implementation schedules often slip while legal teams interpret sector-specific guidance, delaying revenue realization and feature roll-outs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SME cloud migration accelerates

The Thailand CRM market size for large enterprises remained dominant at USD 110.42 million in 2025, yet SMEs are forecast to contribute the bulk of incremental revenue through 2031. Government soft-loan schemes and low-cost cloud subscriptions are shrinking adoption barriers. Vendors targeting SMEs emphasize template-driven setups, Thai-language UIs, and bundled compliance modules, positioning themselves for double-digit expansion. As SMEs graduate from basic contact management to analytics modules, upselling opportunities expand throughout the forecast.

Local suppliers like Choco CRM bundle pre-built Line OA connectors and PDPA consent tools, allowing SMEs to deploy functional systems within weeks. International vendors respond by establishing tier-two pricing tiers and self-service app stores. This democratization fuels geographic diffusion beyond Bangkok, reinforcing the Thailand CRM market’s long-run diversification.

By Deployment Mode: Hybrid models gain momentum

Cloud installations lead, but concerns over latency-sensitive operations, legacy data synchronization, and regulatory mandates are driving hybrid architectures. Banking, aviation, and logistics players increasingly combine on-premise analytics engines with cloud-based engagement layers to balance control with scalability. Hybrid’s 13.05% CAGR underscores its role as the bridge strategy for firms undertaking phased modernization.

Case in point, Bangkok Airways moved ERP workloads to AWS while retaining certain customer-service databases on-premise for real-time operational continuity. Such dual-stack environments catalyze demand for integration middleware and API-first CRM suites.

By End-user Vertical: Retail digitization drives growth

While BFSI commands the largest spend, retail and e-logistics clock the fastest CAGR due to omnichannel imperatives and social-commerce growth. Inventory-aware engagement, in-chat checkout, and AI-driven recommendation engines are critical differentiators in this sector. Logistics providers adopt CRM to manage shippers, riders, and end consumers in one platform, boosting last-mile transparency.

Manufacturing modernizes through direct-to-consumer channels, necessitating warranty and service modules. Government agencies embrace citizen-service CRMs, replicating private-sector best practices and reinforcing platform credibility across the Thailand CRM market.

By CRM Function: Analytics capabilities expand

Sales-force automation remains foundational, but analytics and reporting are now the prime budget priority. Enterprises seek behavioral segmentation, churn prediction, and marketing ROI dashboards that transform raw interaction data into actionable insight. SAS’s USD 1 billion global AI outlay is mirrored locally as vendors embed predictive models pre-trained on Thai datasets.

Marketing-automation modules capitalize on Line OA APIs to trigger personalized offers, while service-desk functions converge with chatbots for first-contact resolution. Together, they reinforce platform stickiness and expand average subscription revenue per user across the Thailand CRM market.

Geography Analysis

Bangkok and Central Thailand anchor nearly half of current spending due to cluster effects among banks, multinationals, and state agencies. Flagship deployments such as Siam Commercial Bank’s omnichannel revamp serve as proof points that spur cross-industry imitation. Depth of local integrators and high-availability broadband sustain shorter implementation cycles and richer partner ecosystems.

The Eastern Economic Corridor is evolving into a digital-manufacturing hotspot. Dedicated incentive packages, trade-zone status, and new hyperscale cloud availability underpin CRM uptake across auto, electronics, and logistics clusters. Real-time supply-chain visibility tied to customer portals becomes essential for export compliance and after-sales differentiation.

Tourism-heavy Southern Thailand and agriculture-driven Northern provinces advance through loyalty platforms and rural-commerce initiatives, respectively. Government e-service roll-outs, such as provincial one-stop citizen apps, expand CRM adoption beyond commercial entities, reinforcing market resiliency across diverse economic bases.

Competitive Landscape

The Thailand CRM market is moderately fragmented. Global suites such as Salesforce, Microsoft Dynamics, and Oracle secure enterprise accounts via breadth of functionality and compliance certifications. Oracle’s Thai data center partnership grants an edge on data-residency questions.[4]Oracle, “AIS Selects Oracle Alloy,” oracle.com

Domestic innovators Zanroo, Choco CRM, and Buzzebees win SME deals through Thai-language UX, Line OA plug-ins, and rapid-deployment templates. Mid-tier foreign providers (HubSpot, Zoho, Freshworks) target cost-sensitive mid-market users with freemium entry tiers.

AI feature depth, hybrid-deployment flexibility, and vertical accelerators are now decisive differentiators. A shortage of certified consultants elevates managed-service offerings and drives vendor investment in low-code configuration tools. As PDPA enforcement intensifies, platforms boasting built-in consent orchestration gain preference.

Thailand CRM Industry Leaders

Salesforce Inc.

Microsoft Corporation

Oracle Corporation

SAP SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OutSystems partnered with Siam Kubota to roll out AI-enabled low-code apps, including the Dealer’s Award System, within six months.

- January 2025: Krungsri Research forecasts 9.0–9.5% annual software-services growth through 2027, citing cloud and SME digitization.

- December 2024: SCB X sold the Robinhood app and announced the Home Credit Vietnam acquisition to broaden regional fintech reach.

Thailand CRM Market Report Scope

Customer relationship management technology helps manage a company's interactions with its customers and potential customers.

The Thai CRM market is segmented by organization size (small and medium, large scale), deployment mode (cloud, on-premise, hybrid), and end-user vertical (services, manufacturing, BFSI, retail and logistics, government, and other end-user verticals). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Cloud |

| On-premise |

| Hybrid |

| BFSI |

| Retail and E-logistics |

| Manufacturing |

| Services (IT, BPO, etc.) |

| Government and Public-Sector |

| Other End-user Verticals |

| Sales Force Automation |

| Marketing Automation |

| Customer Service and Support |

| Analytics and Reporting |

| By Organization Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Mode | Cloud |

| On-premise | |

| Hybrid | |

| By End-user Vertical | BFSI |

| Retail and E-logistics | |

| Manufacturing | |

| Services (IT, BPO, etc.) | |

| Government and Public-Sector | |

| Other End-user Verticals | |

| By CRM Function | Sales Force Automation |

| Marketing Automation | |

| Customer Service and Support | |

| Analytics and Reporting |

Key Questions Answered in the Report

What is the 2026 value of the Thailand CRM market?

The market is valued at USD 197.6 million in 2026.

How fast is the Thailand CRM market expected to grow?

It is projected to expand at a 11.90% CAGR from 2026 to 2031.

Which deployment mode is growing fastest?

Hybrid deployments are rising at a 13.05% CAGR through 2031.

Which region shows the highest growth rate?

The Eastern Economic Corridor is advancing at a 13.39% CAGR.

Why are SMEs rapidly adopting CRM platforms?

Government soft-loan incentives, low-cost cloud subscriptions, and Thai-language solutions have reduced entry barriers.

Page last updated on: