Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Thailanddata Center Rack Market is Segmented by Rack Size (Quartely Rack, Half Rack, Full Rack), Rack Height (42U, 45U and More), Rack Type (Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Racks), Data Center Type (Colocation Facilities, Hyperscale and Cloud Service Provider DCs, Enterprise and Edge), Material (Steel, Aluminum, Other Alloys and Composites). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

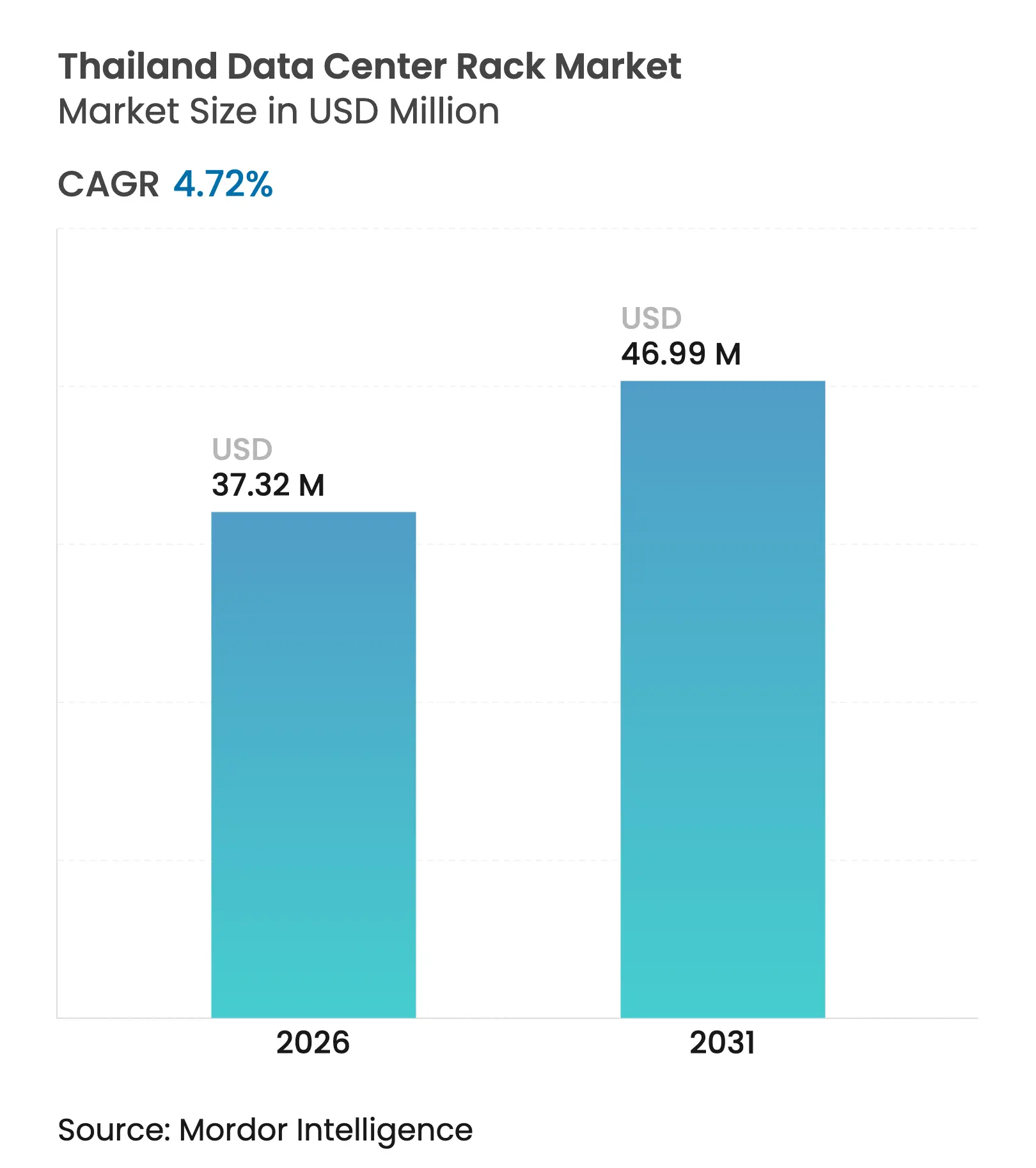

| Market Size (2026) | USD 37.32 Million |

| Market Size (2031) | USD 46.99 Million |

| Growth Rate (2026 - 2031) | 4.72 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Thailand data center rack market size was valued at USD 35.64 million in 2025 and estimated to grow from USD 37.32 million in 2026 to reach USD 46.99 million by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Rising hyperscale deployments, supportive government incentives, and AI-driven high-density computing workloads are accelerating rack demand. Foreign direct investments from Google, AWS, Microsoft, and TikTok are locking in multi-year capacity pipelines that emphasize 42U-to-48U full-cabinet configurations with liquid-cooling integration to address thermal loads exceeding 100 kW per rack. Operators are also tapping BOI incentives and Eastern Economic Corridor (EEC) fast-track approvals, shortening build schedules while lowering upfront land and tariff costs. However, elevated electricity tariffs at THB 4.18 per kWh (USD 0.13), fragmented grid reliability outside Bangkok, and Thailand’s rank as ASEAN’s most frequent ransomware target temper the growth outlook and compel operators to budget for higher security and power-redundancy spending.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in hyperscale and cloud capex (Google, AWS, MSFT) Surge in hyperscale and cloud capex (Google, AWS, MSFT) | +1.8% | National, concentrated in Bangkok-Chonburi corridor | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

National, concentrated in Bangkok-Chonburi corridor

|

Impact Timeline

:

Medium term (2-4 years)

|

Government incentives – BOI, EEC, power-tariff cuts

Government incentives – BOI, EEC, power-tariff cuts

| +1.2% | National, with enhanced benefits in EEC zones | Long term (≥ 4 years) | |||

5G-led data consumption and smartphone density 5G-led data consumption and smartphone density | +0.8% | National, with urban concentration | Short term (≤ 2 years) | |||

AI workloads driving high-density and liquid-cooling

racks AI workloads driving high-density and liquid-cooling

racks | +1.1% | National, premium facilities focus | Medium term (2-4 years) | |||

Edge DC build-out in secondary Thai cities

Edge DC build-out in secondary Thai cities

| +0.6% | Regional, Chiang Mai, Phuket, Pattaya expansion | Long term (≥ 4 years) | |||

Submarine / cross-border fiber positioning TH as ASEAN hub

Submarine / cross-border fiber positioning TH as ASEAN hub

| +0.7% | National, with international connectivity benefits | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in hyperscale and cloud capital expenditure

Massive multi-billion-dollar commitments from Google, AWS, and Microsoft are reshaping demand curves in the Thailand data center rack market through pre-commitments for 42U- and 48U-full-cabinet footprints at densities of 15-20 kW per rack.[1]Google Cloud Editorial Team, “Google to Build First Cloud Region and Data Centre in Thailand,” Google Cloud, cloud.google.comThese orders compress local supply chains, spur standardization of power-bus architectures, and magnify bargaining power for component suppliers. Financial institutions such as TMBThanachart Bank are mirroring the hyperscale blueprint, adopting Huawei all-flash systems that require higher rack power densities. Consequently, premium colocation providers are introducing SLA tiers tied to guaranteed thermal envelopes and liquid-cooling readiness, allowing price premiums versus legacy air-cooled spaces.

Government incentives via BOI and EEC programs

Thailand’s Board of Investment awards eight-year tax holidays, duty exemptions, and land-ownership rights, accelerating project schedules by up to 12 months and reducing capex by approximately 10% for qualifying digital infrastructure.[2]Board of Investment Thailand Press Release, “EEC Incentives for Digital Infrastructure,” boi.go.th The Eastern Economic Corridor extends these benefits through expedited environmental approvals and flexible foreign-ownership caps, attracting landmark pledges such as Equinix’s USD 500 million platform expansion. A nationwide tariff freeze at THB 4.18 per kWh (USD 0.13) offers near-term cost visibility, though operators remain vigilant about potential hikes to THB 6.01 (USD 0.18), which would erode Thailand’s edge over Malaysia and Indonesia in total cost of operations.

AI workloads requiring high-density liquid racks

GPU-intense AI training demands power densities set to breach 500 kW per rack, prompting early adoption of rear-door heat exchangers and immersion baths in flagship Thai facilities.[3]Vertiv White Paper, “Preparing for 500-1000 kW Racks,” vertiv.com CMKL University’s 1,024-GPU cluster underscores academia’s role in mainstreaming liquid cooling, which can cut energy use by up to 50% compared with forced-air systems. Rack manufacturers are collaborating with thermal-technologies firms, notably Delta Electronics’ air-assisted liquid modules, to ship prefabricated units rated for 1.7 MW power-trains. These innovations push the Thailand data center rack market toward new service models where suppliers deliver racks, coolant distribution, and DC-in-a-box prefabs under bundled contracts.

Restraint Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High electricity cost and grid reliability outside

Bangkok High electricity cost and grid reliability outside

Bangkok | -0.9% | Regional, affecting secondary city expansion | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

Regional, affecting secondary city expansion

|

Impact Timeline

:

Medium term (2-4 years)

|

Escalating cybersecurity and ransomware risks Escalating cybersecurity and ransomware risks | -0.6% | National, with enterprise segment focus | Short term (≤ 2 years) | |||

Shortage of certified DC infrastructure engineers

Shortage of certified DC infrastructure engineers

| -0.7% | National, acute in specialized roles | Long term (≥ 4 years) | |||

Cost-competition from Malaysia and Indonesia DC

corridors Cost-competition from Malaysia and Indonesia DC

corridors | -0.5% | Regional, affecting hyperscale decisions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High electricity cost and grid reliability gaps

With Thai tariffs fifth highest in ASEAN, data centers outside Bangkok shoulder heavier opex by budgeting 15-25% more for redundant gensets and battery strings. The Electricity Generating Authority of Thailand’s reliance on volatile gas feedstock heightens price risk, incentivizing hyperscale operators to locate megawatt footprints in Johor and Batam where renewables and stable grids prevail. These dynamics force Thai developers to adopt modular power islands and pursue private-wire PPAs, increasing project complexity and funding needs.

Escalating cybersecurity and ransomware incidents

Thailand logged 109,315 ransomware attacks in 2023, a volume 70% above the global mean, imposing higher insurance premiums and hardware allocations for inline security appliances that absorb valuable U-spaces in every rack. Banks and healthcare groups must over-specify rack-level firewalls and SIEM nodes to satisfy impending amendments to the Cybersecurity Act, inflating both capex and ongoing power draw. Until national standards match Singapore’s MAS TRM code, international enterprises will price in additional compliance overhead when evaluating Thai colocation options.

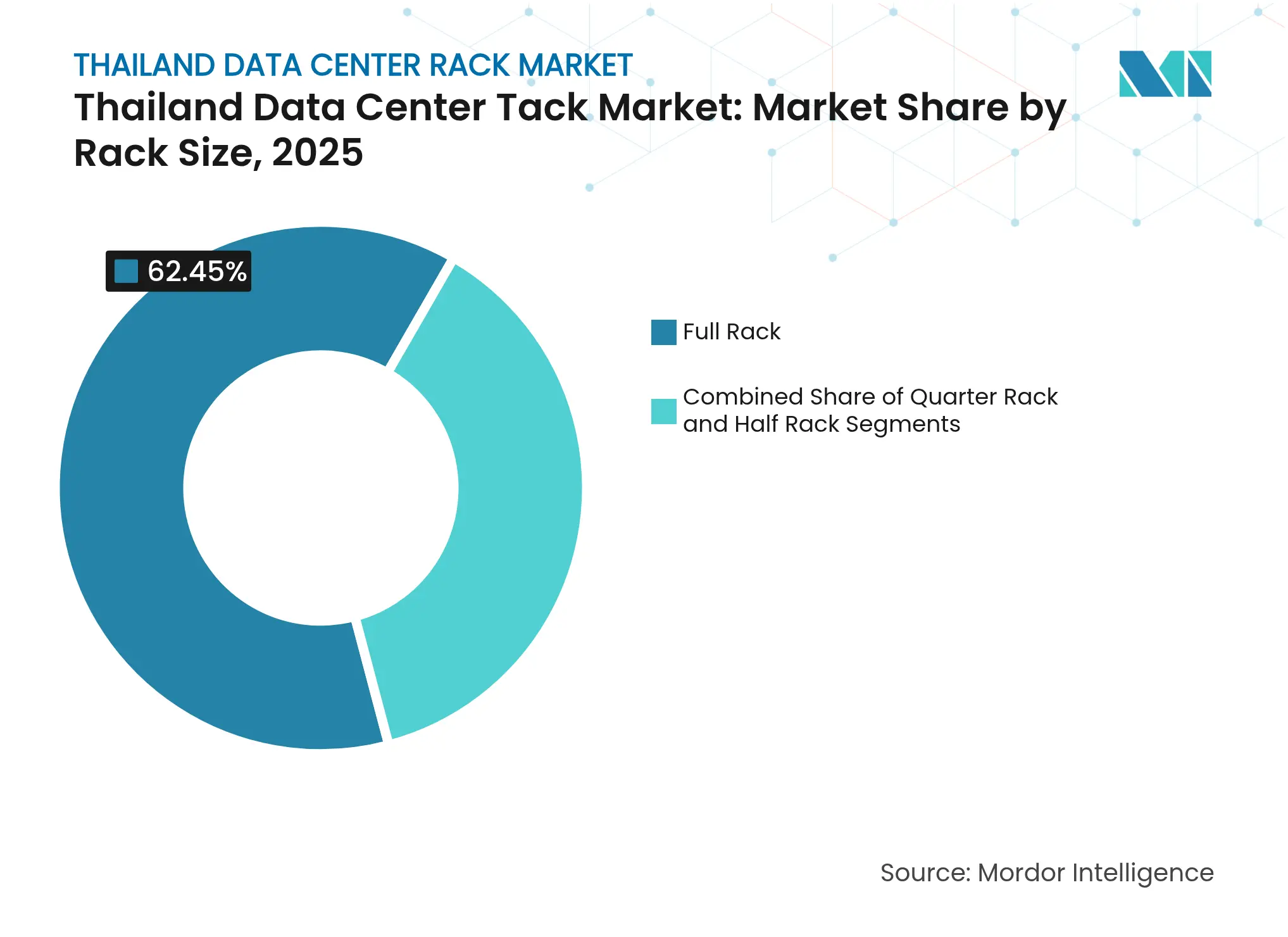

By Rack Size: full racks anchor standardized high-density deployments

Full racks led the Thailand data center rack market with 62.45% share in 2025 and are on track for a 5.05% CAGR through 2031 as hyperscale customers lock in 42U-to-48U templates that streamline automation and remote-hands workflows. The segment’s momentum is reinforced by liquid-cooling adoption because full cabinets offer the structural integrity and space needed for coolant distribution, redundant pumps, and CDU plumbing. Quarter and half racks address edge and SMB workloads yet lack volume power to influence ASP trajectories, while micro-racks remain a niche for telco street-level enclosures.

AI workloads intensify full-rack preference; operators condense GPU clusters into fewer cabinets to optimize floor-plate economics. Containerized AI data centers showcased by Delta Electronics demonstrate how integrated full-rack lines accelerate rollout schedules by shipping prefabricated cooling and power modules that hook directly to distribution skids. Consolidation also drives larger anchor orders, further skewing supply balances toward manufacturers with global logistics and compliance footprints.

Note: Segment shares of all individual segments available upon report purchase

By Rack Height: 42U standards hold while 48U accelerates AI scale-out

The Thailand data center rack market maintained 53.02% share for 42U cabinets in 2025 because this height balances cable-management ergonomics with floor-tile loading constraints. Yet 48U units deliver 14% more payload capacity without stretching raised-floor grids, supporting a robust 5.48% CAGR through 2031. The popularity of taller racks is evident in STT GDC Thailand’s AI-ready chambers that pre-install 48U frames to house NVIDIA HGX boards and liquid manifolds, minimizing field retrofits.

Legacy facilities confront height-clearance ceilings that cap growth; operators may either lower raised floors or phase in new halls with higher headroom. For telecom and scientific institutions, custom 45U or >52U racks fulfill proprietary gear demands. However, these bespoke units lack economies of scale, and most future orders will consolidate around 42U and 48U standards to simplify spares, accessories, and maintenance toolkits across multisite portfolios.

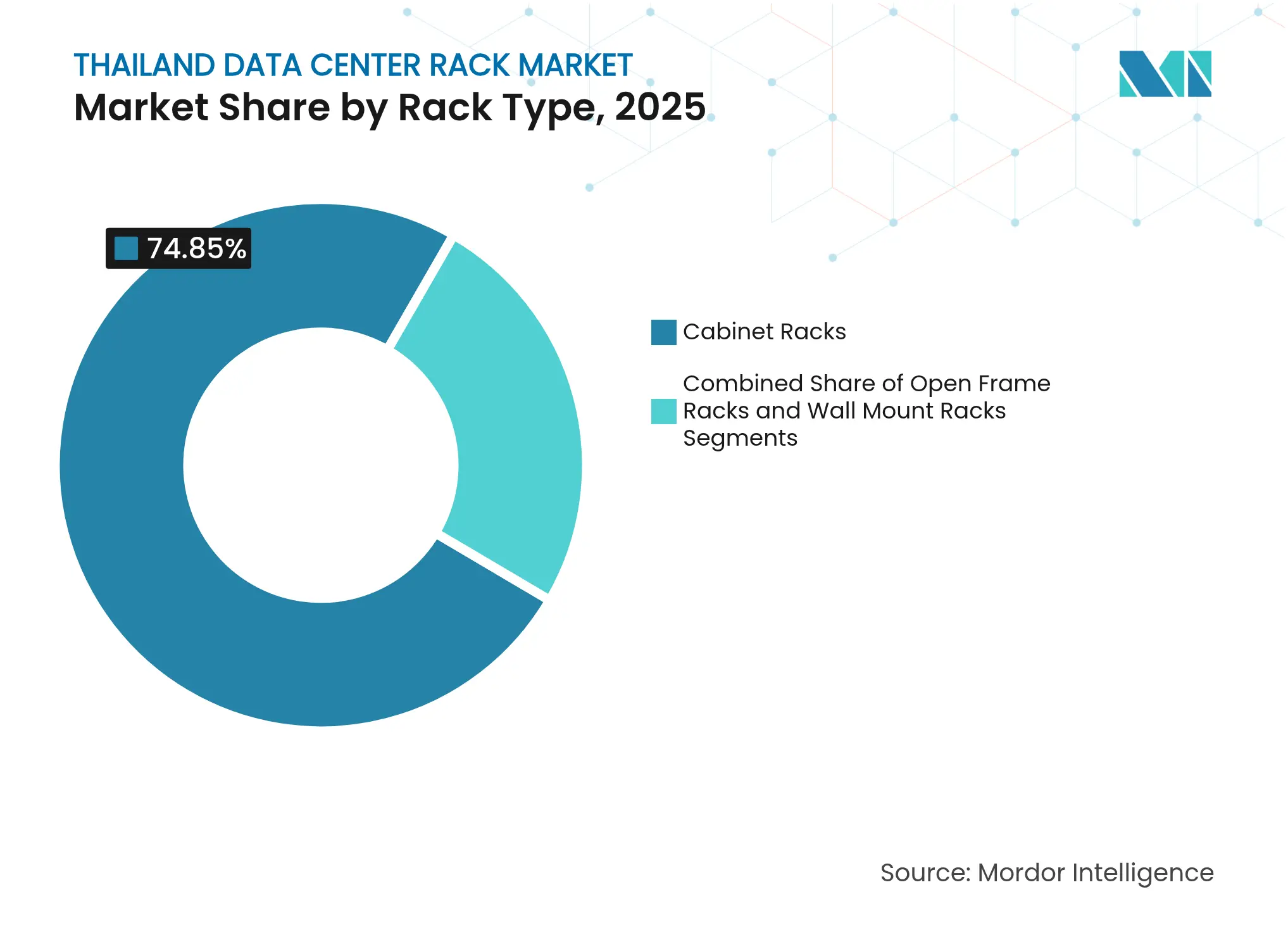

By Rack Type: cabinet dominance reflects humidity control and security

Cabinet racks held 74.85% share of the Thailand data center rack market size in 2025, as enclosed frames mitigate high humidity and enable aisle-containment best practices. Cabinets support physical-access locks and EMI shielding, critical for financial services and healthcare tenants under tightening data-sovereignty rules. Growth at 5.82% CAGR through 2031 aligns with nationwide cybersecurity concerns, encouraging enterprises to trade slightly higher unit cost for incremental protection.

Open-frame racks persist for lab environments and telecom headends where airflow and technician accessibility outweigh security factors. Wall-mount units gain modest traction in roadside edge POPs driven by 5G densification, but their aggregate volume stays small. Liquid immersion favors cabinet form factors because sealed chassis limit spill risk and simplify leak-detection sensor placement, further entrenching closed-rack predominance as AI density scales.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: colocation leadership meets hyperscale disruption

Colocation facilities captured 52.10% revenue in 2025 yet now face competitive headwinds as the hyperscale cohort accelerates at 6.08% CAGR through 2031. Hyperscalers negotiate multiyear land and power blocks directly with authorities, leveraging BOI incentives to lower taxes and secure tariff certainty, thereby compressing colocation addressable markets among top-tier Thai corporates. In response, colocation incumbents such as True IDC partner with SIAM.AI to retrofit halls with GPU-optimized racks, water-loop cooling, and AI-as-a-service offerings, blurring lines between wholesale and retail delivery models.

Edge and enterprise data centers carve space in latency-sensitive niches smart-factory sites, fintech compliance nodes, and content caching facilities. While they command smaller footprints, their rack configurations skew toward ruggedized, shallow-depth frames tailored to constrained real estate, providing incremental growth for specialized vendors.

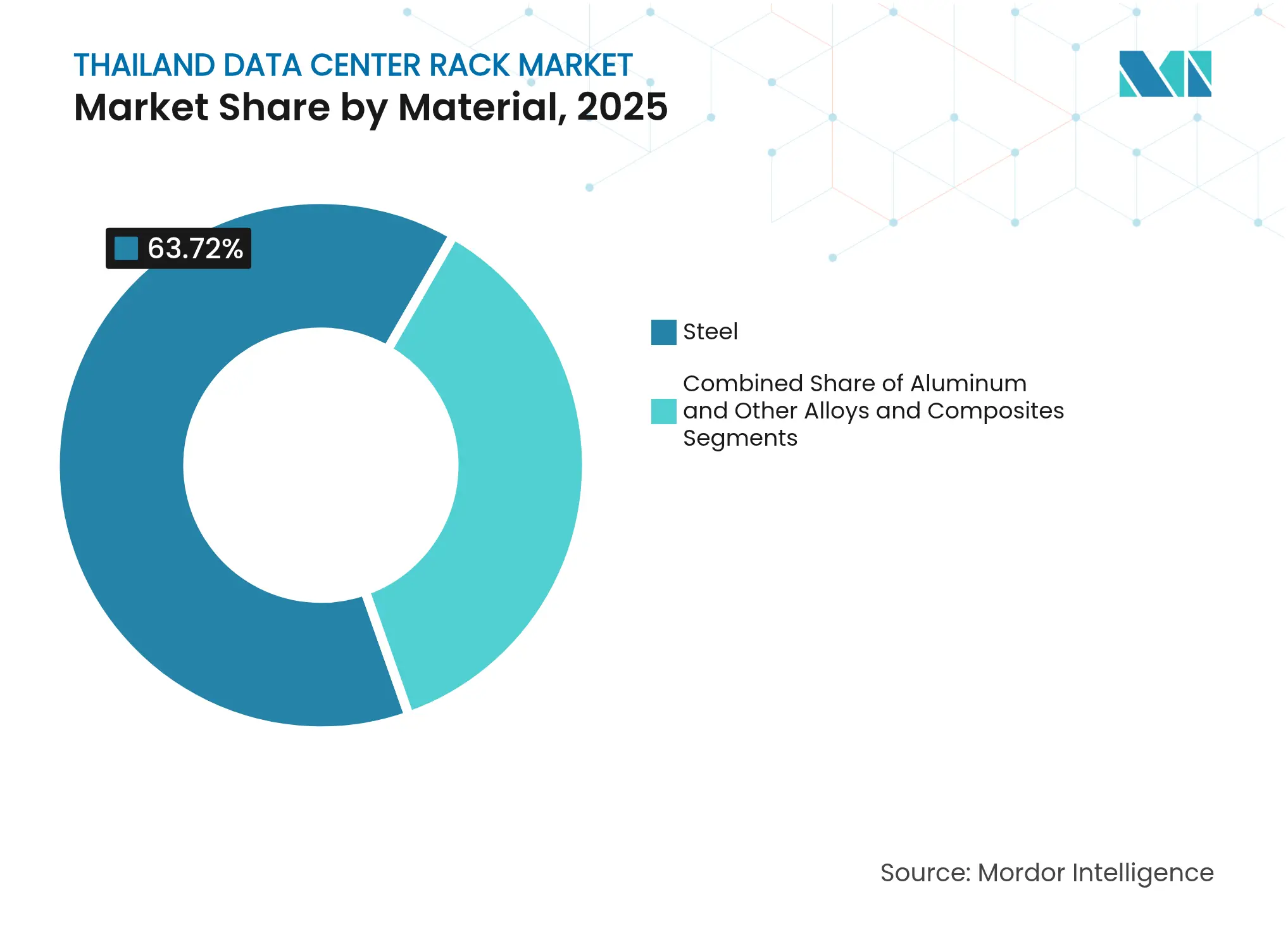

By Material: steel prevails on strength while aluminum scales on thermals

Steel retained 63.72% share in 2025 due to its load-bearing capacity and electromagnetic shielding, essential for densely packed GPU blades in the Thailand data center rack market. Aluminum, however, is notching a 5.01% CAGR as operators prioritize thermal conductivity and lighter frames to ease seismic anchoring compliance. Weight savings of up to 40% reduce freight costs for imported racks and facilitate two-person installs, trimming labor overhead.

Delta Electronics’ expansion into Amata City positions the firm to fabricate both steel and aluminum chassis near key customers, shortening lead times and offering tailored finishes for immersion-coolant compatibility. Hybrid materials such as carbon-steel skeletons with aluminum door panels emerge in niche builds where operators pursue the strength-cost midpoint while enhancing airflow with perforated lightweight surfaces.

Note: Segment shares of all individual segments available upon report purchase

Bangkok-Chonburi remains the epicenter of Thailand data center rack market deployments, concentrating is increasing due to submarine-cable landings, dual-feed power grids, and inter-metro dark-fiber rings. Google’s USD 1 billion Chonburi project and AWS’s Bangkok region anchor fresh rack orders that cascade through local OEMs, integrators, and logistics partners. The EEC’s high-speed rail links, U-tapao airport expansion, and BOI tax holidays further strengthen its gravitational pull for hyperscale siting.

Northern and southern corridors are emerging edge clusters. Chiang Mai leverages its electronics manufacturing base and university R&D zones to justify compact data halls serving AI-enabled industrial IoT. Phuket and Pattaya, reliant on tourism and real-time hotel analytics, introduce localized racks that mesh with content-delivery POPs to lower latency beneath 20 ms. These secondary nodes underpin the Thailand data center rack industry’s strategy of distributing compute for regulatory compliance and service-quality uplift without replicating full hyperscale footprints.

Market Concentration

The Thailand data center rack market features moderate fragmentation, with Schneider Electric, Vertiv, and Rittal contending against fast-growing regional specialists such as Delta Electronics, SITEM, and Interlink Communication. Multinationals differentiate through integrated DCIM software, prefabricated power modules, and global logistics, winning hyperscale bids that mandate standardized, high-quality supply. Regional firms leverage lower cost bases, proximity, and BOI relationships to secure telco, public-sector, and mid-enterprise contracts.

Product roadmaps converge on liquid-cooling compatibility, tool-less rail systems, and AI-ready cable-management kits. Schneider’s USD 140 million Rayong plant expansion targets shorter lead times for cabinet and busway assemblies while bundling Green Premium carbon disclosures that align with multinational ESG mandates. Vertiv promotes 500-1000 kW rack density blueprints with rear-door exchangers to future-proof client footprints. Local champions respond with competitively priced immersion tanks and regional service networks that assure rapid spare-parts turnaround.

M&A and joint ventures escalate. Delta Electronics partners Cal-Comp Electronics on industrial automation, embedding rack solutions within smart-factory packages. SITEM scouts alliances for modular DC builds, and Interlink scales fiber-optic assemblies to complement its rack sales. Competitive intensity compresses gross margins on commoditized SKUs, shifting value capture toward bundled services—remote monitoring, preventative maintenance, and compliance auditing tied to each installed rack.

________________________________________

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the Thailand data center rack market as revenue earned from the sale of new, factory-assembled quarter, half, and full server racks, both open-frame and enclosed cabinets, installed inside colocation, hyperscale/cloud, enterprise, and edge facilities across Thailand.

Scope exclusion: aftermarket refurbishment, rental cabinets, and integrated server-in-chassis systems are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed local colocation operators, global cloud infrastructure managers active in Bangkok and the EEC corridor, and channel distributors serving system integrators. These conversations validated prevailing rack heights, average selling prices, and near-term procurement pipelines, while also stress-testing energy-density assumptions passed down from the secondary scan.

Desk Research

We compiled publicly available supply, demand, and regulatory clues from tier-1 sources such as Thailand's Board of Investment statistics, National Broadcasting & Telecommunications Commission filings, and DEPA digital-economy trackers. We then overlaid import-export codes for HS 84733090 racks from the Customs Department. Trade association insights from the Open Compute Project, patent counts accessed via Questel, and earnings disclosures by leading global rack vendors added production and pricing context. Company 10-Ks, IDC hyperscale capex trackers cited in Dow Jones Factiva, and regional press articles rounded out historical baselines. This list is illustrative; many additional secondary datapoints fed our desk analysis.

Market-Sizing & Forecasting

We anchored the 2025 baseline with a top-down reconstruction that multiplies Thailand's installed IT power (MW) by surveyed rack density (kW per rack) and average cabinet prices, which are then corroborated with selective bottom-up vendor shipment checks. Key model variables include: hyperscale capex commitments announced under BOI incentives, 5G subscriber growth, average rack densities shifting toward 10-15 kW, steel price trajectories, and floor-space additions in Bangna-Trad campuses. Forecasts through 2030 run a multivariate regression where rack demand is explained by real GDP, cloud workloads, and power-cost index; residuals are adjusted after expert consensus. Gap-filled bottom-up estimates are scaled to ensure convergence within +/-5 % of reconciled secondary totals.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer-analyst cross-checks, and lead-analyst sign-off. We re-contact primary sources when quarterly hyperscale announcements or tariff shifts move model drivers materially. Every published figure is refreshed annually, with mid-cycle tweaks for major investments, ensuring clients receive the latest calibrated view before each release.

Why Mordor's Thailand Data Center Rack Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because firms apply different rack definitions, bundle wider hardware, or model hyperscale rollouts on uneven refresh cadences.

Key gap drivers arise when others bundle servers and PDUs into 'rack' revenue, inflate ASPs by using retail colocation pricing, or convert THB to USD at dated exchange rates rather than the mid-year Bank of Thailand average we adopt. Mordor's disciplined segmentation, annual refresh, and dual-path validation minimize such skews.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 35.64 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 460 million (2024) | Global Consultancy A | Combines racks with server chassis and power strips; ASP based on list prices | ||

USD 400 million (2023) | Industry Association B | Reports server-system revenue that subsumes rack sales; excludes discounting patterns |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.