Thailand Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

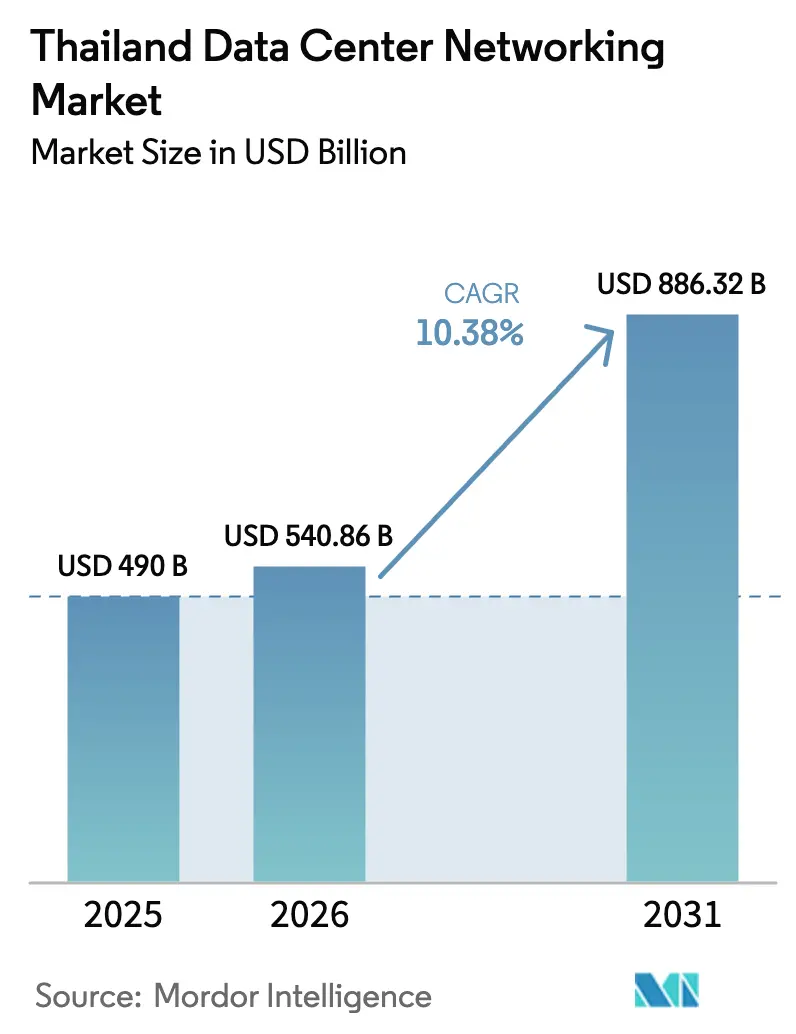

| Base Year Market Size (2025) | USD 490 Billion |

| Market Size (2026) | USD 540.86 Billion |

| Market Size (2031) | USD 886.32 Billion |

| Growth Rate (2026 - 2031) | 10.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Data Center Networking Market Analysis by Mordor Intelligence

Thailand data center networking market size in 2026 is estimated at USD 540.86 million, growing from 2025 value of USD 490 million with 2031 projections showing USD 886.32 million, growing at 10.38% CAGR over 2026-2031. Growth is fueled by the government-backed Thailand 4.0 program, hyperscale capital inflows, and accelerating cloud adoption. Deepening fiber backbones, falling latency targets for AI workloads, and a widening edge footprint in provincial cities are also shaping the Thailand data center networking market. Foreign investors continue to be attracted by tax holidays, green-energy credits, and proximity to subsea cable landing stations, while domestic enterprises ramp up network automation to offset labor shortages. Rising electricity tariffs, however, intensify the focus on power-efficient routing and switching platforms.

Key Report Takeaways

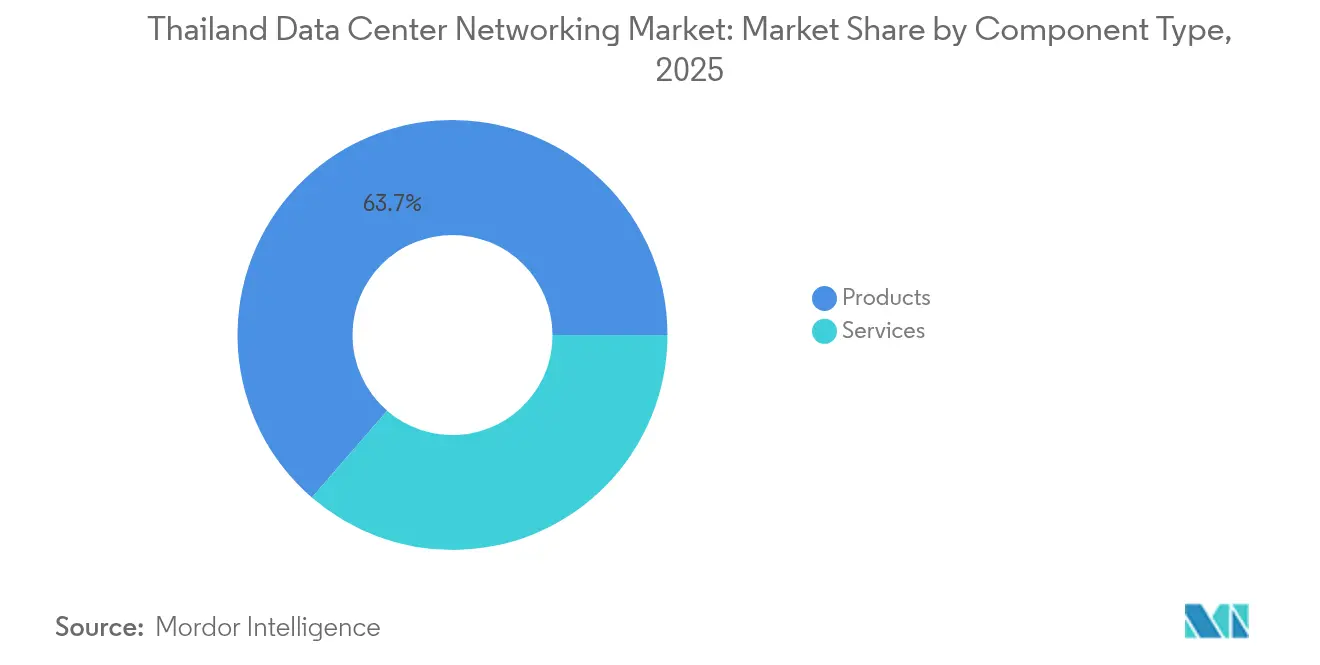

- By component, products led with 63.65% revenue share in 2025, while services are forecast to post the fastest 11.78% CAGR through 2031.

- By end-user, IT & telecommunications held 34.74% of Thailand data center networking market share in 2025; healthcare & life sciences is set to grow at 12.96% CAGR through 2031.

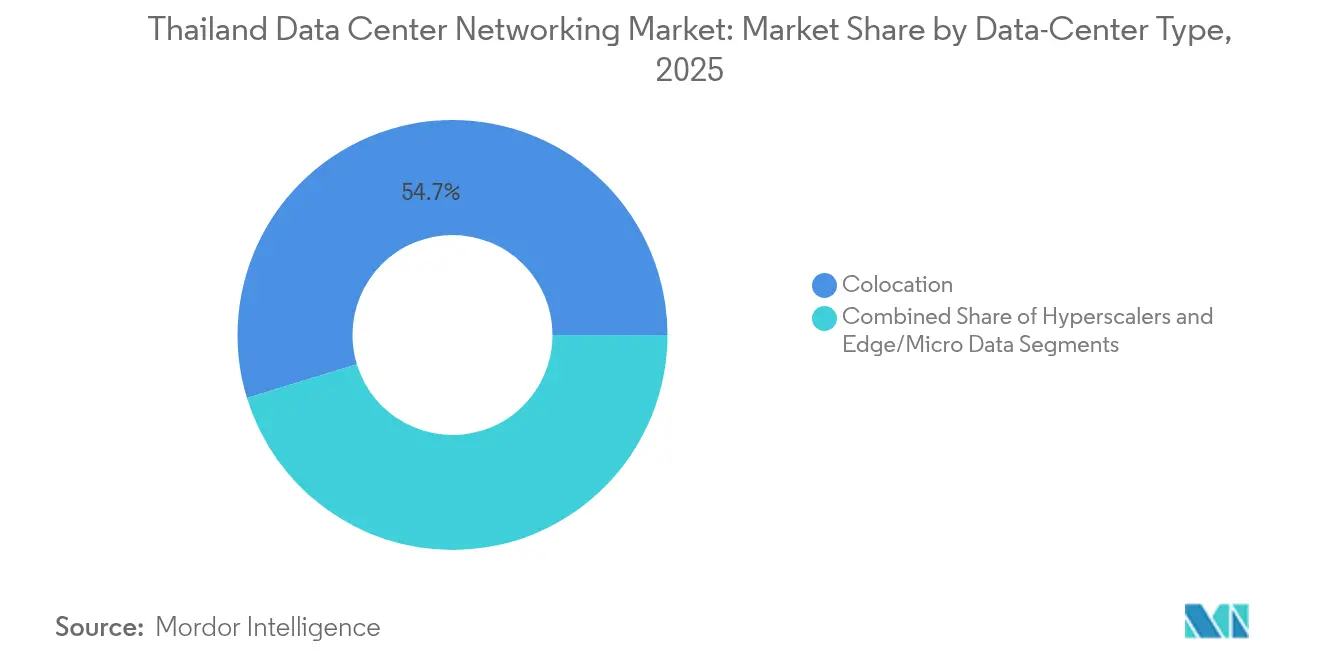

- By data-center type, colocation captured 54.73% of the Thailand data center networking market size in 2025, yet hyperscalers and cloud service providers are advancing at a 13.92% CAGR to 2031.

- By bandwidth, 50-100 GbE commanded 35.88% revenue share in 2025, whereas >100 GbE will expand at 14.12% CAGR by 2031.

- Cisco, Huawei, and Juniper together supplied just under 40% of switching and routing ports shipped in 2024, indicating a moderately concentrated vendor environment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The conditions observed in Thailand are shaped as much by international forces as by domestic ones. Mordor Intelligence’s data center networking market research places those conditions within the broader global frame.

Thailand Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first and hyperscale build-outs | +2.8% | National (Bangkok, EEC) | Medium term (2-4 years) |

| Thailand 4.0 digital-economy initiatives | +2.1% | National | Long term (≥ 4 years) |

| OPEX-reduction pressure spurring network automation | +1.7% | National, enterprise | Short term (≤ 2 years) |

| ASEAN Digital Gateway and cross-border traffic corridors | +1.4% | Regional | Medium term (2-4 years) |

| OTT video / e-sports edge traffic | +0.9% | Provincial cities | Short term (≤ 2 years) |

| ERC green-energy credit incentives | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first and hyperscale build-outs

Hyperscale cloud providers are scaling 400 GbE and 800 GbE fabrics to support AI and real-time analytics requirements concentrated in the Eastern Economic Corridor. Microsoft, AWS, and Google collectively announced more than USD 6 billion of incremental capacity in 2025 alone, triggering a steady upgrade cycle among regional carriers that peer with these facilities.[1]Government Public Relations Department, “BOI Approves THB 241 Billion Data Center Investments,” thailand.go.th The resulting demand for high-port-density spine switches and coherent optics is cascading into enterprise roadmaps. Vendors such as Ciena introduced 8192-slot coherent routers that deliver 800 Gbit/s per channel while consuming 30% less power.[2]François Locoh-Donou, “Introducing the 8192 Coherent Router,” Ciena Insights Blog, ciena.com Large local banks are mirroring these architectures inside private cloud zones to keep latency below 1 ms for real-time payment rails.

Thailand 4.0 digital-economy initiatives

Public-sector digitalization mandates stable, low-latency networking from provincial hospitals to revenue-collection offices. Universal broadband targets by 2027 require hundreds of micro data centers at the sub-district level, each linked by software-defined WAN overlays. The Personal Data Protection Act is accelerating demand for encrypted east-west traffic visibility and zero-trust segmentation, pushing firewall throughput requirements above 1 Tb/s.

OPEX-reduction pressure spurring network automation

Electricity costs climbed to USD 0.11/kWh in 2025, and utilities signaled an additional 4% hike tied to upcoming carbon levies. Operators are turning to intent-based networking and closed-loop automation to trim 20-30% of routine configuration hours. Cisco’s Network Services Orchestrator and Red Hat Ansible are now bundled with pre-built playbooks for optical wavelength provisioning.

ASEAN Digital Gateway and cross-border traffic corridors

Thailand’s role in regional data corridors is being strengthened by new submarine cable landings that cut round-trip latency to Singapore below 25 ms. The government signed memoranda with Laos and Cambodia to harmonize IX taxation, spurring demand for terabit-scale border routers with deep packet inspection. Export-oriented manufacturers are adopting on-premises encryption appliances capable of handling 400 GbE links to meet data-residency requirements of clients anchored in Vietnam and Indonesia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for advanced networking gear | -1.9% | National, mid-market | Short term (≤ 2 years) |

| Shortage of SDN / DevNet skill sets | -1.2% | National | Medium term (2-4 years) |

| Delays in subsea-cable landing permits | -0.8% | Coastal regions | Medium term (2-4 years) |

| Rising electricity tariffs and looming carbon tax | -0.7% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex for advanced networking gear

A typical 800 GbE leaf-spine deployment for a 5 MW facility can exceed USD 4 million in capital outlay, placing it beyond the reach of Thailand’s mid-sized service providers. Leasing options are limited because local banks remain cautious about residual-value risk on rapidly obsoleting optical modules.

Shortage of SDN / DevNet skill sets

Industry surveys indicate that certified DevNet professionals number fewer than 2,000 nationwide, leading to salary premiums upward of 70% over traditional CCNP roles. The talent bottleneck delays migration projects and forces operators to rely on vendor professional services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Products Dominance

Products dominated 63.65% of 2025 revenue thanks to brisk orders for fixed-configuration spine switches and coherent optics. The Thailand data center networking market size for products is projected to reach USD 514.27 million by 2031 at an 8.12% CAGR, sustained by switch-to-server refresh cycles. In parallel, professional services, managed network operations, and training recorded a 11.78% CAGR, benefiting from scarce in-house DevSecOps talent. Enterprises choose managed services to obtain 24/7 monitoring and intent-based change control, cutting mean-time-to-repair below 30 minutes. Vendors bundle lifecycle support to guarantee firmware compliance under the Personal Data Protection Act. Demand for SLA-bound services stems from regulatory penalties that can exceed 3% of annual revenue for downtime-induced data breaches.

The Thailand data center networking market is also witnessing expanded consumption of proactive maintenance services that harness AI-driven telemetry. Operators ingest streaming sensor data into predictive models that pre-empt line-card failures up to 20 days in advance. Consulting and design services are in demand during edge-site build-outs, where space and cooling constraints call for custom topologies. Remote hands services gain traction among overseas cloud providers co-locating hardware in Bangkok but lacking resident engineers.

By End-User: Healthcare Emerges as Growth Leader

IT & telecommunications held 34.74% of Thailand data center networking market share in 2025, driven by 5G backhaul densification and OTT content caching nodes. Yet healthcare & life sciences will post a 12.96% CAGR through 2031 as hospitals digitalize imaging archives and deploy tele-ICU platforms. The Thailand data center networking market size for healthcare could top USD 112.34 million by 2031, assuming continued e-health reimbursement incentives. High-resolution CT scans generate 1–2 TB per session, pushing edge storage and 100 GbE interconnect mandates inside hospital campuses.

Pharmaceutical labs in Rayong are building air-gapped data centers for genome analytics using 400 GbE clusters. BFSI remains a high-value vertical with sustained appetite for deterministic low-latency networks supporting real-time settlement and fraud analytics. Government agencies expand secure WAN overlays that meet Cyber Security Act stipulations. Media & entertainment companies leverage adaptive bitrate encoding nodes placed in tourist hotspots, while manufacturing outfits operate private 5G MEC hubs enabling digital twins.

By Data-Center Type: Hyperscalers Drive Transformation

Colocation operators commanded 54.73% of revenue in 2025, but hyperscalers are adding capacity at twice the pace of carrier-neutral builds. The Thailand data center networking market is seeing hyperscalers deploy larger 18-50 MW campuses needing 1024-port spine meshes. Saturation of Bangkok’s power grid pushes new builds toward the EEC, where tax holidays and LNG terminal access lower PUE. Colocation players respond by integrating software-defined interconnection fabrics, allowing enterprises to spin up 10 GbE cross-connects within minutes.

Edge and micro data centers register an 11.46% CAGR through 2031, reflecting IoT and smart-city rollouts. Low-height racks and outside-plant enclosures dominate these sites, often powered via rooftop solar. Operators adopt open-compute switches flashed with SONiC to meet budget constraints. Workload orchestration platforms facilitate live VM migrations between edge clusters and core regions, ensuring compliance with data-sovereignty rules.

By Bandwidth: Ultra-High-Speed Migration Accelerates

The 50-100 GbE tier retained 35.88% market share in 2025, offering an optimal balance of cost and throughput for most enterprises. Thailand data center networking market size for this tier will still climb because enterprises stagger upgrades, but its share will slip as AI training and inference require 400 GbE fabrics. Deployments above 100 GbE rise at 14.12% CAGR, propelled by hyperscale AI clusters using NVLink and RoCE.

Less than or equals to 10 GbE ports persist in out-of-band networks and KVM management links. Meanwhile, 25-40 GbE acts as a stepping-stone for SMEs migrating from 1 GbE. Vendors now ship optics supporting both PAM4 and coherent modulation, simplifying field upgrades. Dynamic bandwidth licensing enables pay-as-you-grow, curbing initial capex anxieties.

Geography Analysis

Bangkok concentrates nearly 70% of installed rack capacity and remains the primary junction for subsea cables linking India and Singapore. The capital’s dense fiber rings and proximity to IXs lower transit costs, making it the preferred landing zone for multicloud edge nodes. The Thailand data center networking market benefits from municipal incentives that discount grid power by 3% for data centers achieving PUE below 1.3.

The Eastern Economic Corridor—covering Chonburi, Rayong, and Chachoengsao—anchors the second-largest cluster of hyperscale campuses. Land grants, LNG import terminals, and high-voltage substations accelerate approvals. The Thailand data center networking market share of the EEC will approach 27.62% by 2031 as AWS, Google, and local conglomerates commission multi-availability-zone regions.

Provincial cities such as Chiang Mai and Phuket experience double-digit growth in micro-edge nodes. Smart-tourism projects stream 8K VR content that demands under-10 ms latency, prompting deployment of MEC cabinets beside 5G base stations. National broadband projects extend fiber backhaul to 40,000 villages, enabling edge-aggregation routers that hand off traffic to regional IXs. The trend diversifies capacity away from the Bangkok metro and underpins a resilient, distributed topology.

The data center networking market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, Africa, and North America, along with detailed country-level analysis for India, New Zealand, Netherlands, Nigeria, United States, and Japan.

Competitive Landscape

Global incumbents—Cisco, Huawei, and Juniper—supplied just under 40% of switch and router ports in 2024, signaling moderate concentration. Each vendor now bundles AI-driven assurance engines, seeking stickier software annuities. Cisco promotes Routed Optical Networking that collapses IP and optical layers, lowering total cost by up to 45%.[3]Kip Compton, “Routed Optical Networking Explained,” Cisco Blogs, cisco.com Huawei offers CloudFabric 3.0 with lossless Ethernet for AI clusters, while Juniper’s Apstra automates multi-vendor fabrics through intent-based design.

Local system integrators—G-Able, MFEC, and Jasmine—address customization gaps by offering site preparation, power-train integration, and bilingual NOC services. Hyperscalers fast-track campus builds via joint ventures with property developers that provide land, power, and renewable PPAs. Partnerships between CP Group and BlackRock aim to erect a 200-MW “Giga Data Hub” near Rayong, pressuring incumbents to pre-position inventory and swap lines to meet condensed procurement windows.

Optical component vendors—Ciena and Lumentum—push coherent pluggables that fit QSFP-DD form factors, enabling easy upgrades from 100 GbE to 400 GbE without chassis replacement. The open-optics trend erodes traditional vendor lock-ins and intensifies price competition. Meanwhile, security appliance specialists such as Palo Alto Networks collaborate with NTT DATA to bake 5G-aware firewalls into edge data centers. The evolving mix of traditional hardware, disaggregated white-box platforms, and managed services keeps bargaining power distributed among buyers.

Thailand Data Center Networking Industry Leaders

Cisco Systems Inc.

Huawei Technologies Co. Ltd.

Juniper Networks Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise (HPE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Global Infrastructure Partners pledged more than USD 1 billion for hyperscale builds in Thailand, focusing on ultra-high-density optical fabrics

- June 2025: Equinix acquired three Manila data centers, expanding its regional interconnection footprint for Thai enterprises.

- May 2025: FPT Corporation partnered with Sunline to modernize Thai digital banking stacks and underpin low-latency APIs

- March 2025: MUFG Bank and NTT DATA validated sub-1s live migration across a 50 km IOWN all-photonics link, meeting stringent RTO needs

- March 2025: Ciena released its 8192 coherent router delivering 800 G channels with 30% power savings.

- February 2025: NTT DATA and Palo Alto launched a managed service pairing private 5G with zero-trust edge firewalls

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Thailand data-center networking market as all value earned from the sale of switches, routers, storage-area network gear, application-delivery controllers, optical interconnects, software-defined networking controllers, and associated integration or support services that are deployed inside purpose-built data-center facilities across Thailand.

Scope Exclusions: Equipment that primarily serves campus LANs, metro or long-haul telecom backbones, and managed telecom services is kept outside our market boundary.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- Less Than equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater Than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

We interviewed network architects at hyperscale builders, procurement heads at leading colocation firms, regional distributors, and SDN software vendors across Bangkok and the Eastern Economic Corridor. Their insights on port mix shifts, ASP pressure, and lead-time constraints shaped key assumptions and confirmed model outputs.

Desk Research

Our analysts began by mapping Thailand's installed rack base and hyperscale pipeline using public sources such as the National Broadcasting and Telecommunications Commission, the Digital Economy Promotion Agency, Customs import records, and statistics from trade bodies like the Thai Data Center Council. Industry filings, audited financials, and operator presentations then helped us benchmark port shipments and average selling prices.

Paid databases, D&B Hoovers for company financials and Dow Jones Factiva for deal flows, were tapped to validate revenue splits, while patent analytics from Questel illustrated the pace of SDN innovation. These sources, together with reputable press and regulatory releases, formed the backbone of our secondary evidence set; many additional references supported validation yet remain unlisted here for brevity.

Market-Sizing & Forecasting

A top-down build starts with 2024 rack counts, power draw, and typical ports-per-rack values; these are multiplied by confirmed ASPs to reach a preliminary revenue pool, which is then balanced against sampled supplier roll-ups (our selective bottom-up check). Critical variables include new rack additions, hyperscale campus announcements, average port density, switch ASP trends, 5G subscriber growth, and public-cloud capex. Multivariate regression on these drivers underpins our 2025-2030 forecast, with scenario analysis testing conservative and aggressive rollout timelines. Gaps in bottom-up estimates, for example, when import data lags, are bridged through channel checks with distributors before figures are finalized.

Data Validation & Update Cycle

Every draft model passes anomaly screening, peer review, and senior analyst sign-off. We refresh datasets annually and trigger interim updates after material events such as major campus landings or tariff shifts, ensuring clients always receive the latest calibrated view.

Why Our Thailand Data Center Networking Baseline Commands Trust

Published estimates can diverge because firms pick different product scopes, conversion rates, and refresh cycles.

Key gap drivers include some publishers folding campus backbone gear into market value, others applying uniform global ASPs without Thai discounting, and a few locking forecasts for multiple years while Mordor reassesses inputs each quarter.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.49 B (2025) | Mordor Intelligence | - |

| USD 0.44 B (2025) | Global Consultancy A | excludes services revenue, relies on generic APAC ASPs |

| USD 0.39 B (2024) | Regional Consultancy B | narrower scope (omits >100 GbE ports), last update mid-2024 |

In sum, our disciplined scope setting, live variable tracking, and dual-layer validation give decision-makers a balanced baseline that is transparent, reproducible, and aligned with Thailand's fast-moving digital-infrastructure reality.

Key Questions Answered in the Report

What is the current size of the Thailand data center networking market?

The market stands at USD 540.86 million in 2026 and is forecast to reach USD 886.32 million by 2031, implying a 10.38% CAGR.

Which segment is growing fastest?

Services, particularly managed operations and integration, are expanding at 11.78% CAGR due to talent shortages and rising network complexity.

Why are hyperscalers investing heavily in Thailand?

Factors include tax incentives in the Eastern Economic Corridor, strategic proximity to ASEAN traffic corridors, and government support under Thailand 4.0.

What bandwidth tier is advancing most quickly?

Links above 100 GbE, including 400 GbE and 800 GbE, are growing at 14.12% CAGR as AI and real-time analytics workloads surge.

How are rising power costs influencing network design?

Operators adopt power-efficient silicon, routed optical architectures, and AI-driven automation to curb OPEX as electricity tariffs climb.

What are the major restraints facing the market?

High upfront cost for cutting-edge gear and a shortage of SDN/DevNet talent can delay deployments and limit broader technology uptake.

Page last updated on: