Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Thailand Data Center Processor Market is Segmented by Processor Type (GPU, CPU and More), Application( Advanced Data Analytics, AI/ML Training and Inference, High-Performance Computing and More), Architecture (X86, ARM-Based, RISC-V and Power), Data Center Type (Enterprise, Colocation, Cloud Service Providers / Hyperscalers). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

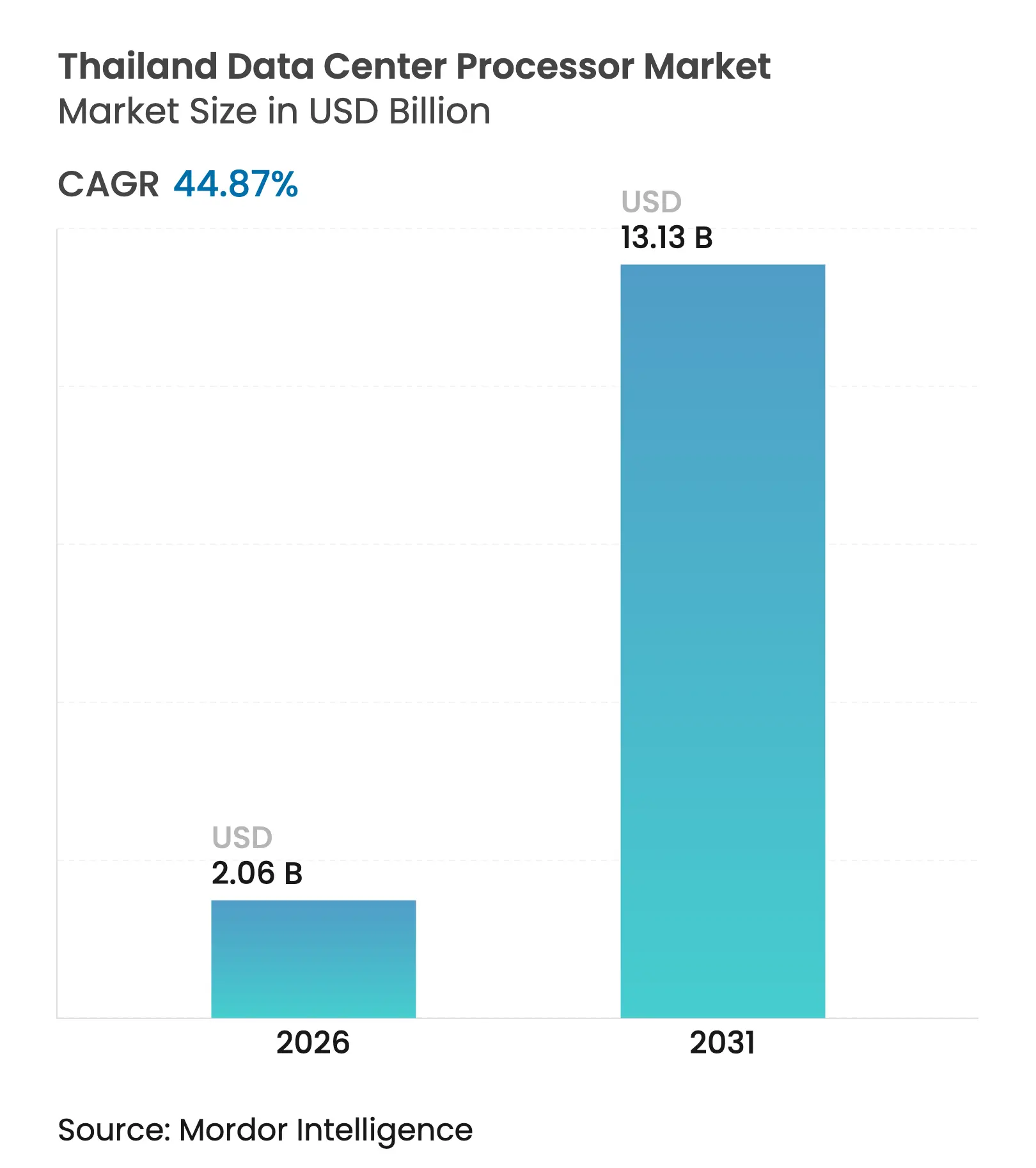

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 13.13 Billion |

| Growth Rate (2026 - 2031) | 44.87 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Thailand data center processor market size in 2026 is estimated at USD 2.06 billion, growing from 2025 value of USD 1.42 billion with 2031 projections showing USD 13.13 billion, growing at 44.87% CAGR over 2026-2031. Momentum comes from hyperscale cloud cap-ex, rapid 5G rollout, and the National AI Action Plan. Edge deployments are shifting processor selection toward energy-efficient architectures, while tax incentives in the Eastern Economic Corridor (EEC) shorten upgrade cycles. Competitive pressure among Intel, AMD, NVIDIA, and emerging RISC-V suppliers is stimulating continuous innovation, keeping prices in check despite supply constraints. Demand resilience mirrors global expectations that data-center AI chips will exceed USD 400 billion by 2030

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G roll-out accelerating edge & cloud workload

demand

5G roll-out accelerating edge & cloud workload

demand

| 8.2% | National, concentrated in Bangkok and EEC zones | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

8.2%

|

Geographic Relevance

:

National, concentrated in Bangkok and EEC zones

|

Impact Timeline

:

Medium term (2-4 years)

|

Government digital-economy incentives & EEC tax

breaks

Government digital-economy incentives & EEC tax

breaks

| 7.1% | Eastern Economic Corridor, spillover to Bangkok | Short term (≤ 2 years) | |||

Hyperscale cloud entrants' cap-ex (AWS, Google,

Alibaba)

Hyperscale cloud entrants' cap-ex (AWS, Google,

Alibaba)

| 9.3% | National, with primary hubs in Bangkok and Chonburi | Medium term (2-4 years) | |||

Crypto-mining compliance push for efficient processors

Crypto-mining compliance push for efficient processors

| 4.8% | National, with concentration in industrial zones | Short term (≤ 2 years) | |||

Corporate net-zero goals boosting ARM/low-power chips

Corporate net-zero goals boosting ARM/low-power chips

| 6.2% | Bangkok metropolitan area, expanding to regional centers | Long term (≥ 4 years) | |||

National AI Action Plan (2022-27) driving AI

accelerator uptake

National AI Action Plan (2022-27) driving AI

accelerator uptake

| 8.9% | National, with government sector leading adoption | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

5G Roll-out Accelerating Edge & Cloud Workload Demand

Thailand’s nationwide 5G build-out is redefining processor requirements. Ultra-low-latency use cases need inference engines close to subscribers, encouraging telecom operators to specify ARM-based chips for edge nodes because of their superior performance-per-watt. [1]Digitimes Staff, “Thailand 5G Rollout Spurs Edge Demand,” digitimes.comTrue Corporation’s multi-city expansion highlights how decentralized topologies split demand between energy-efficient edge silicon and high-core-count x86 devices at regional hubs. Vendor roadmaps now prioritize thermal envelopes and real-time AI processing over peak clock speed, reshaping procurement criteria across the Thailand data center processor market.

Government Digital-Economy Incentives & EEC Tax Breaks

The EEC’s incentive framework trims total cost of ownership for high-density compute installations by up to 15%, giving Thailand cost parity with Singapore. These rebates accelerate AI-accelerator adoption, allowing firms to retain sensitive data onshore instead of relying exclusively on foreign clouds. Early adopters across automotive and electronics clusters in Chonburi have moved pilot ML workloads onto local silicon, reinforcing sovereign-cloud objectives within the Thailand data center processor market.[2]BOI Thailand, “EEC Investment Promotion Measures,” boi.go.th

Hyperscale Cloud Entrants’ Capital Expenditure

AWS, Google, and Alibaba each deploy distinct processor mixes in Thai facilities. AWS combines Intel Xeon for general workloads with in-house Graviton chips for cost-sensitive tiers. Google supplements x86 nodes with TPU racks, and Alibaba optimizes power budgets through ARM cores. Their disparate strategies create a heterogeneous ecosystem that spreads opportunity among multiple chipmakers and cements Thailand’s role as a multi-cloud hub.

National AI Action Plan Driving Accelerator Uptake

Public-sector projects under the 2022-27 plan mandate on-prem inference for health, education, and smart-city pilots. Procurement guidelines specify dedicated AI accelerators, lifting the penetration of ASICs and GPUs in provincial data centers. This policy channel secures baseline volumes and de-risks local supply chains, underpinning the rapid expansion of the Thailand data center processor market.

Restraint Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of skilled chip & DC engineering talent

Shortage of skilled chip & DC engineering talent

| -4.7% | National, most acute in Bangkok and industrial zones | Long term (≥ 4 years) | (~)% Impact on CAGR Forecast:

-4.7%

|

Geographic Relevance

:

National, most acute in Bangkok and industrial zones

|

Impact Timeline

:

Long term (≥ 4 years)

|

Import tariffs & customs delays on high-end processors

Import tariffs & customs delays on high-end processors

| -3.2% | National, affecting all import-dependent segments | Short term (≤ 2 years) | |||

Power-quality issues outside Bangkok for high-TDP chips

Power-quality issues outside Bangkok for high-TDP chips

| -2.8% | Regional centers excluding Bangkok metropolitan area | Medium term (2-4 years) | |||

US export controls on advanced AI GPUs creating supply

risk

US export controls on advanced AI GPUs creating supply

risk

| -5.1% | National, particularly affecting AI-focused enterprises | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Skilled Chip & DC Engineering Talent

Insufficient local expertise in ASIC design and advanced cooling limits deployment velocity. Rising salary premiums prompt Thai operators to outsource critical roles, lengthening commissioning cycles across the Thailand data center processor market. Universities are revamping curricula, yet a multi-year gap persists before supply meets demand.

US Export Controls on Advanced AI GPUs Creating Supply Risk

Tighter licencing on leading-edge GPUs complicates procurement for high-end Thai AI projects. Enterprises must commit capital without certainty of delivery dates or resort to alternative accelerators with lower throughput. This unpredictability inflates total project costs and moderates the otherwise steep growth curve of the Thailand data center processor market.[3]AMD Inc., “EPYC 9004 Series Performance Brief,” amd.com

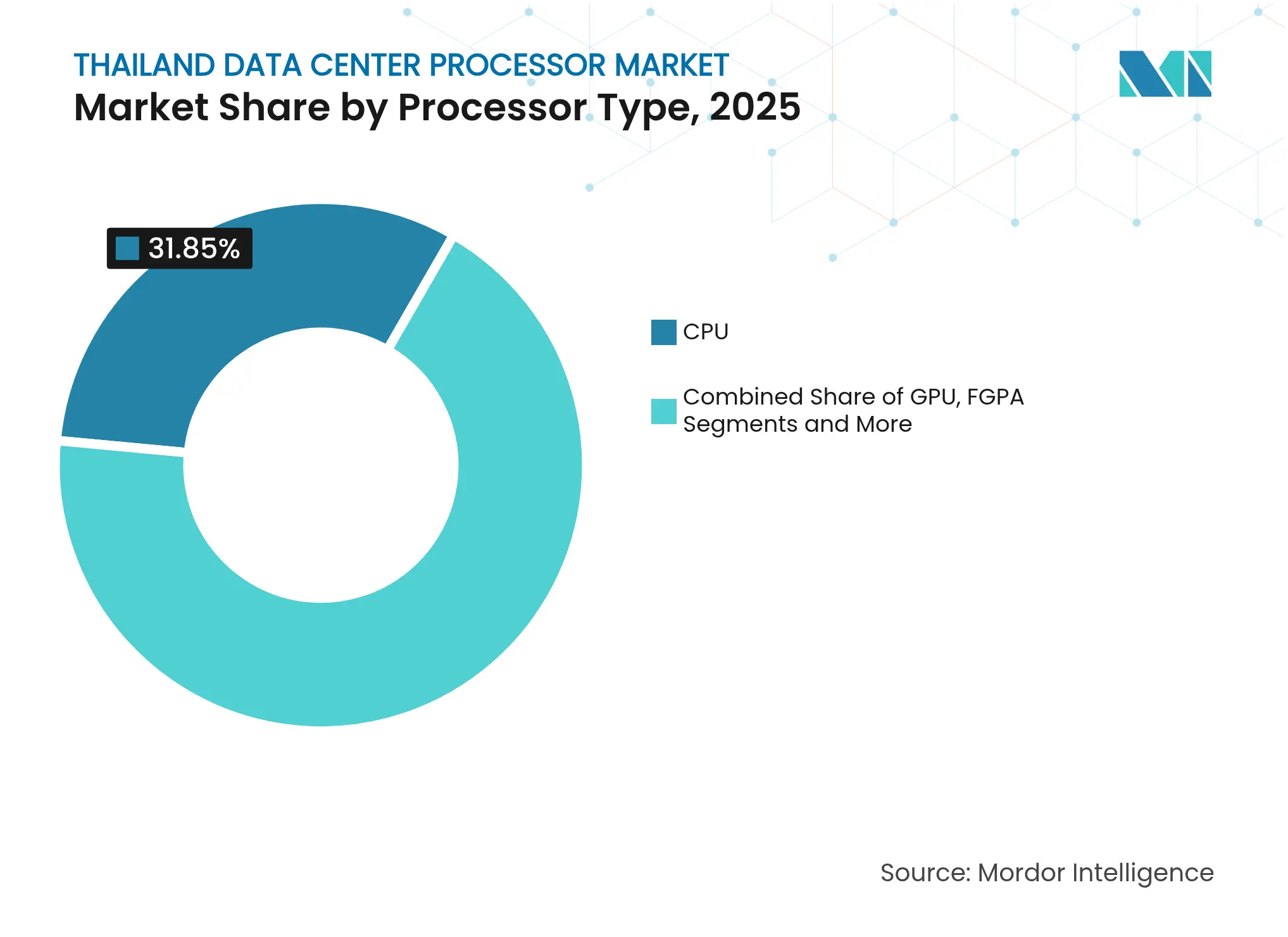

By Processor Type: AI Accelerators Drive Next-Generation Workloads

CPU devices retained 31.85% of the Thailand data center processor market share in 2025, underscoring their role in payroll, ERP, and web hosting. The Thailand data center processor market size for AI accelerators is on track to enlarge at 45.3% CAGR, reflecting widespread machine-learning adoption under government stimulus. GPU cards remain pivotal for deep-learning training, especially in research clusters, whereas FPGA deployments concentrate on workloads demanding ultra-low latency.

Elevated electricity tariffs push buyers toward purpose-built ASICs that deliver higher operations-per-watt. Tier-2 colocation providers bundle liquid-cooled racks to host dense accelerator nodes, monetizing rising demand without overstressing grid connections. This heterogeneity signals a longer-term shift from monolithic CPU estates to specialized silicon within the Thailand data center processor market.

Note: Segment shares of all individual segments available upon report purchase

By Application: AI/ML Training Dominates Current Demand

AI/ML workloads commanded a 33.62% slice of the Thailand data center processor market in 2025, cementing machine intelligence as today’s principal consumption driver. The Thailand data center processor market size tied to advanced data analytics is expanding at a 45.8% CAGR as finance, telecom, and retail sectors embed predictive modeling into daily operations. High-performance computing clusters in universities prioritize weather forecasting and genomic research, while security analytics nodes gain traction due to stricter cyber-threat reporting.

Software-defined networks create fresh demand for packet-processing engines that can be re-flashed on-the-fly. As use cases diversify, operators allocate distinct processor pools—CPUs for transaction integrity, accelerators for AI inference, and FPGAs for network functions—strengthening overall spend within the Thailand data center processor market.

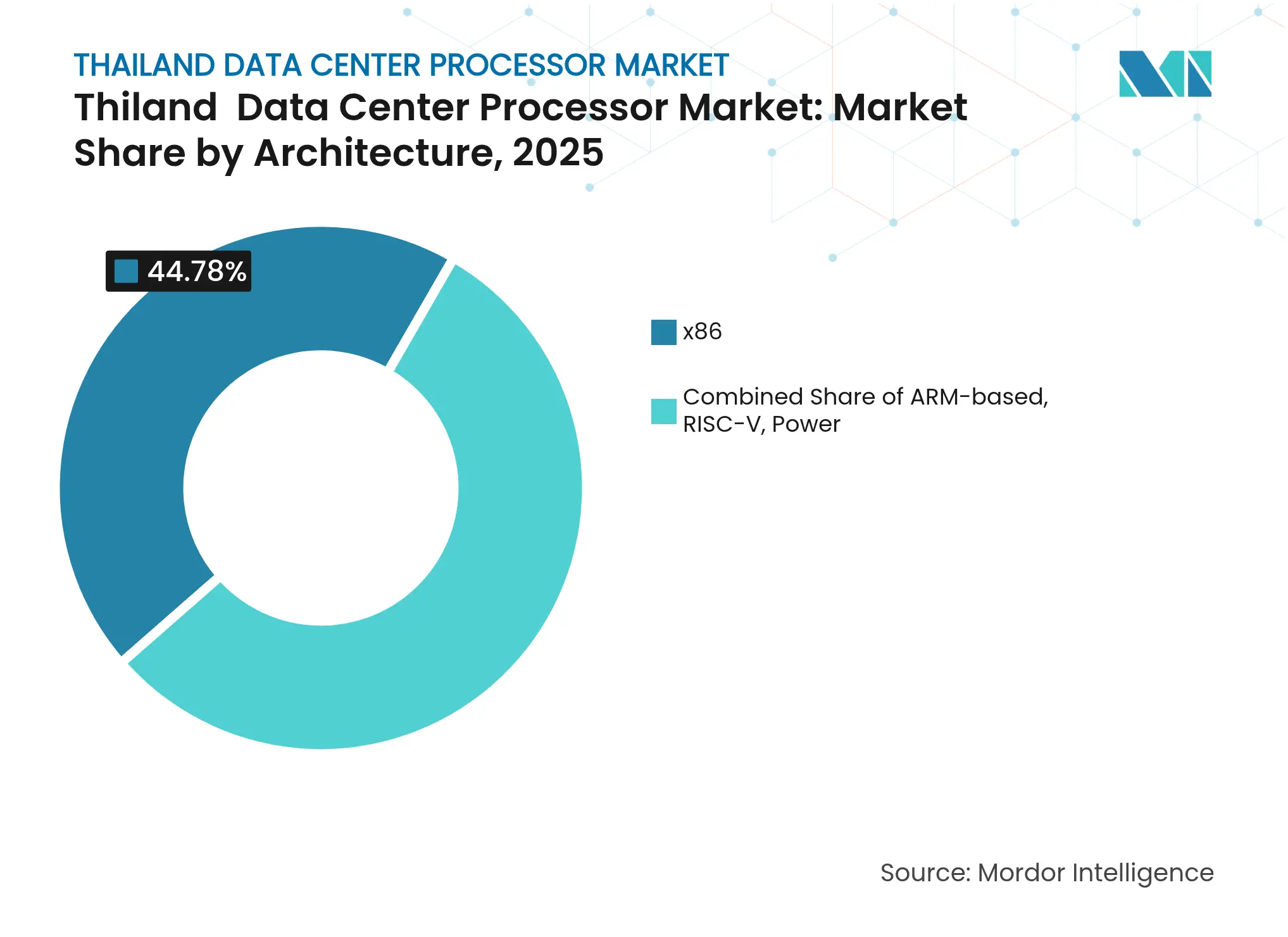

By Architecture: x86 Dominance Faces ARM Challenge

x86 retained 44.78% of the architecture mix in 2025, supported by a mature software stack and deep systems-integrator skills. Nevertheless, RISC-V is accelerating at 45.1% CAGR on the promise of open-source customization, while ARM wins in edge form factors where a 40% lower power draw matters. The Thailand data center processor market now features hybrid racks blending instruction sets to fine-tune cost-per-operation.

Government interest in RISC-V aligns with long-term digital sovereignty agendas, spurring local start-ups to design domain-specific cores. Meanwhile, hyperscalers pilot chiplet-based x86 variants that reduce die size and boost manufacturing yields. Multi-architecture adoption is set to grow as workload diversity intensifies across the Thailand data center processor market.

Note: Segment shares of all individual segments available upon report purchase

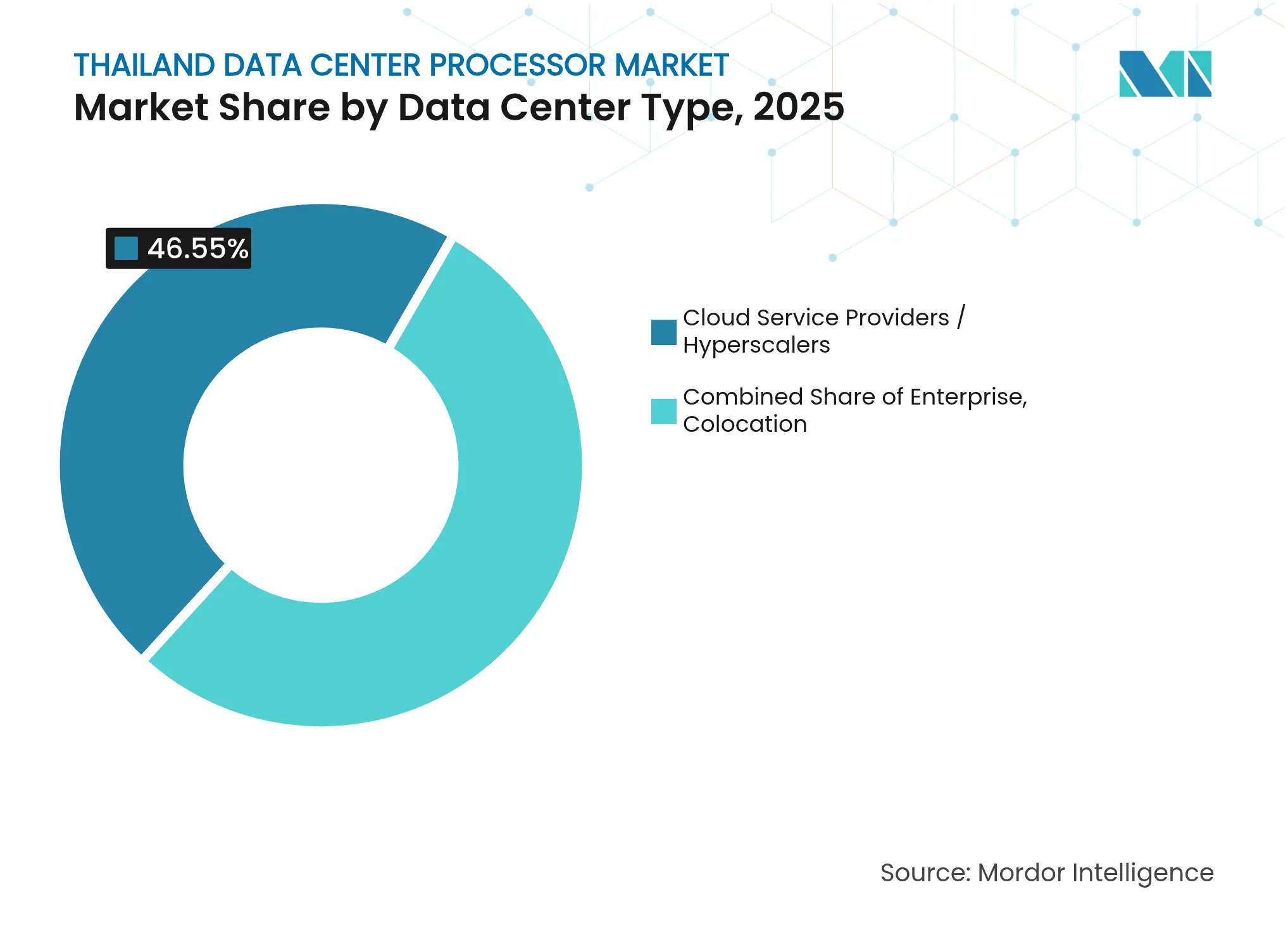

By Data Center Type: Hyperscalers Lead, Colocation Accelerates

Cloud service providers held 46.55% of deployments in 2025, driven by AWS, Google, and Alibaba region launches. Colocation space, rising at 46.0% CAGR, appeals to enterprises seeking hybrid strategies that balance sovereignty with hyperscale connectivity. The Thailand data center processor market size inside colocation halls will expand rapidly as mid-market firms lift their AI compute budgets without building in-house facilities.

Enterprise on-premise sites remain essential for regulated workloads, yet capital budgets are shifting toward procuring edge nodes connected to regional pods. Power quality outside Bangkok prompts operators to invest in modular DC designs and front-end power conditioning, shaping processor mix decisions throughout the Thailand data center processor market.

Note: Segment shares of all individual segments available upon report purchase

Bangkok and its periphery currently absorb over two-thirds of processor shipments as digital businesses cluster near submarine-cable gateways and the national internet exchange. The Thailand data center processor market size in the capital benefits from robust fiber density and reliable power, making it the launchpad for new architectures. Suburban expansion into Chonburi reflects tax relief under the EEC, where land availability supports hyperscale campuses.

Second-tier cities such as Chiang Mai and Khon Kaen are leveraging 5G backhaul upgrades to deploy compact edge facilities. Here, ARM and RISC-V boards tackle local inference tasks for smart-logistics and telemedicine pilots, diversifying revenue streams within the Thailand data center processor market. Power grids in these regions still face voltage variability, steering operators toward lower-TDP silicon.

Thailand’s role as an ASEAN logistics hub enables efficient cross-border parts flow. Supply-chain resilience improves as regional neighbours, notably Vietnam, add advanced test and assembly capacity that can funnel processors into Thai projects with reduced transit times. This proximity lessens tariff exposure and hedges against ocean-freight disruptions.

Market Concentration

Market leadership remains in the hands of Intel, AMD, and NVIDIA, whose combined portfolios address general compute, HPC, and AI acceleration. Their deep channel networks and long software support cycles resonate with Thai CIOs who prioritize continuity. The Thailand data center processor market still offers headroom for challengers; Ampere Computing courts cloud natives with high-core ARM parts, while Huawei’s HiSilicon line targets AI inference under tighter power budgets.

Strategy is shifting from sheer core counts to workload-specific optimization. NVIDIA’s latest GPU modules integrate network adapters and shared memory stacks, simplifying AI cluster scale-out. AMD counters with 4th Gen EPYC processors that double energy efficiency over prior x86 iteration. Intel has fast-tracked 18A node production, promising competitive per-watt gains once volume ramps.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the Thailand data center processor market as the annual value of central processing units, graphics processing units, field-programmable gate arrays, and AI accelerators that are installed inside Thai-based data centers run by cloud service providers, colocation operators, or large enterprises.

Scope exclusions: chips embedded in consumer PCs, smartphones, or edge IoT gateways are left outside this boundary.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with cloud operators, colocation facility managers, semiconductor distributors, and DC design engineers across Bangkok and the EEC validated shipment volumes, average selling prices, and refresh cycles. Follow-up surveys with procurement heads clarified lead-time shifts and price premiums on AI accelerators, closing gaps left by secondary data.

Desk Research

We began with trade statistics and customs codes that disclose inbound shipments of server-class CPUs and GPUs, pulling monthly data from Thailand's Customs Department and UN Comtrade. Macroeconomic drivers, such as national AI spending, 5G subscriber additions, and IT cap-ex trends, were retrieved from the Bank of Thailand, the Digital Economy Promotion Agency, and IMF datasets. Industry associations, including the Thailand Data Center Council and the Semiconductor Equipment & Materials International chapter, provided install-base and utilization ratios. Company filings and investor presentations from listed hyperscalers complemented the public data. Finally, paid databases like D&B Hoovers (financials) and Dow Jones Factiva (deal flow) helped us size local footprints of global chip vendors. This list is illustrative; many additional open and subscription sources fed our desk analysis.

In parallel, we reviewed relevant patents on Questel to track upcoming processor architectures and scanned regulatory circulars on export controls that could curtail high-end GPU imports. News alerts from Factiva flagged mid-year cap-ex revisions by cloud majors, prompting model tweaks.

Market-Sizing & Forecasting

We applied a top-down build. Processor import values were reconstructed from customs lines, adjusted for warranty spares and local assemblies, and then mapped to data-center use via sectoral penetration rates. Select bottom-up checks, rack population surveys, vendor roll-ups, and sampled ASP × unit counts served to benchmark and refine totals. Key variables modeled include hyperscale cap-ex pipelines, rack power density migration, average core counts, GPU attach rates per server, and currency swings. A multivariate regression linked these inputs to historical spend before an ARIMA overlay projected 2025-2030 demand. Expert panels reviewed elasticity assumptions and scenario spreads.

Data Validation & Update Cycle

Outputs undergo variance checks against independent shipment trackers, while senior analysts review anomalies before sign-off. Mordor updates every report annually and triggers interim revisions after material events such as new export curbs or billion-dollar DC announcements.

Why Mordor's Thailand Data Center Processor Baseline Commands Reliability

Benchmark comparison

Published values differ because firms choose distinct scopes, assumptions, and refresh cadences.

Key gap drivers include whether AI accelerators are counted, the year used as a base, and the depth of shipment cross-checks versus simple revenue surveys. Our disciplined definition, dual-sourced variables, and yearly refresh make Mordor's figures a balanced decision-making anchor.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.42 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 0.40 B (2023) | Regional Consultancy A | Counts only server hardware revenue and omits GPUs; older base year limits relevance | ||

USD 28.70 B (2025) | Industry Journal B | Aggregates all AI server spend, mixes software and services, and lacks bottom-up shipment validation |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.