Thailand Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

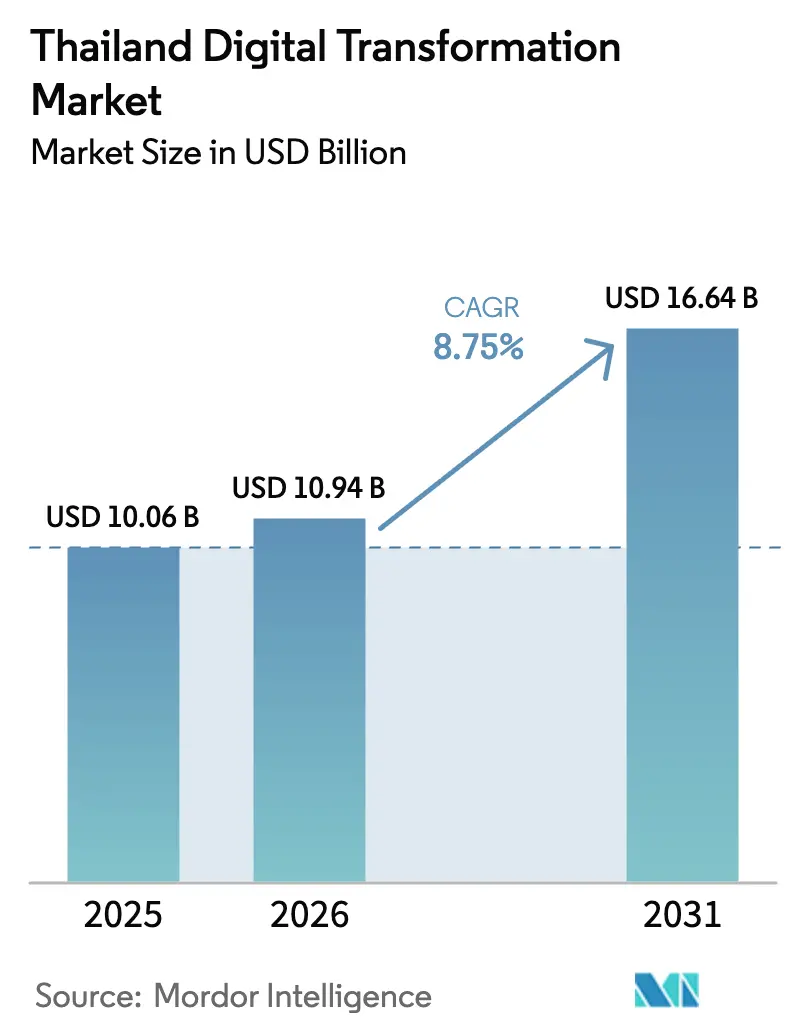

| Base Year Market Size (2025) | USD 10.06 Billion |

| Market Size (2026) | USD 10.94 Billion |

| Market Size (2031) | USD 16.64 Billion |

| Growth Rate (2026 - 2031) | 8.75% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Digital Transformation Market Analysis by Mordor Intelligence

The Thailand Digital Transformation Market size was valued at USD 10.06 billion in 2025 and estimated to grow from USD 10.94 billion in 2026 to reach USD 16.64 billion by 2031, at a CAGR of 8.75% during the forecast period (2026-2031). Government policy, hyperscale cloud investments, and rapid 5G deployment combine to move the national economy from light manufacturing toward data-driven growth. Large capital inflows from AWS, Google, and Huawei are establishing multiple local availability zones that shorten latency and encourage edge-native applications. Expanded fiber networks and nearly nationwide 5G coverage are driving cloud adoption among retailers, banks, and hospitals. A tightening privacy regime under the Personal Data Protection Act (PDPA) is forcing enterprises to budget more for cybersecurity, creating parallel demand for compliance-grade security tools. Talent shortages remain a structural risk, yet special visas, reskilling funds, and vendor training pledges are building a deeper workforce pipeline that supports sustained expansion of the Thailand digital transformation market.

Key Report Takeaways

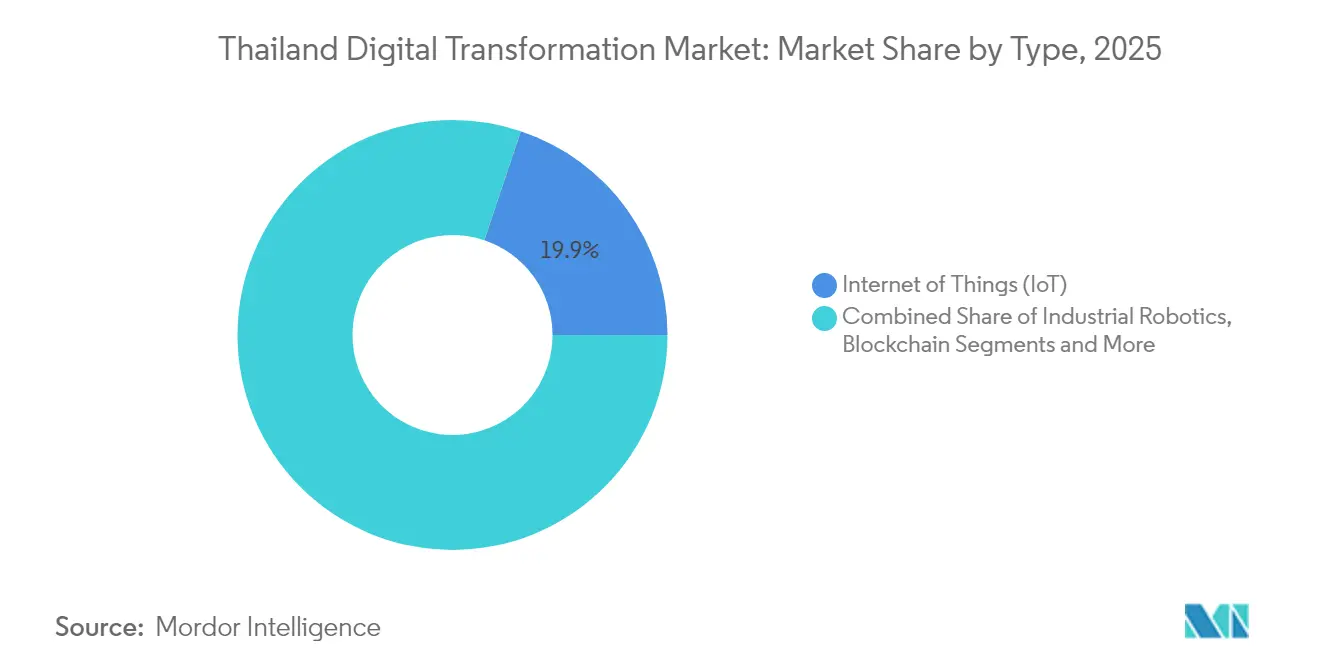

- By technology type, Internet of Things led with 19.85% revenue share in 2025; Cloud & Edge Computing is forecast to advance at a 20.55% CAGR through 2031.

- By region, the Southern region held 13.78% of Thailand digital transformation market share in 2025, while the Eastern Economic Corridor is set to grow at a 12.95% CAGR to 2031.

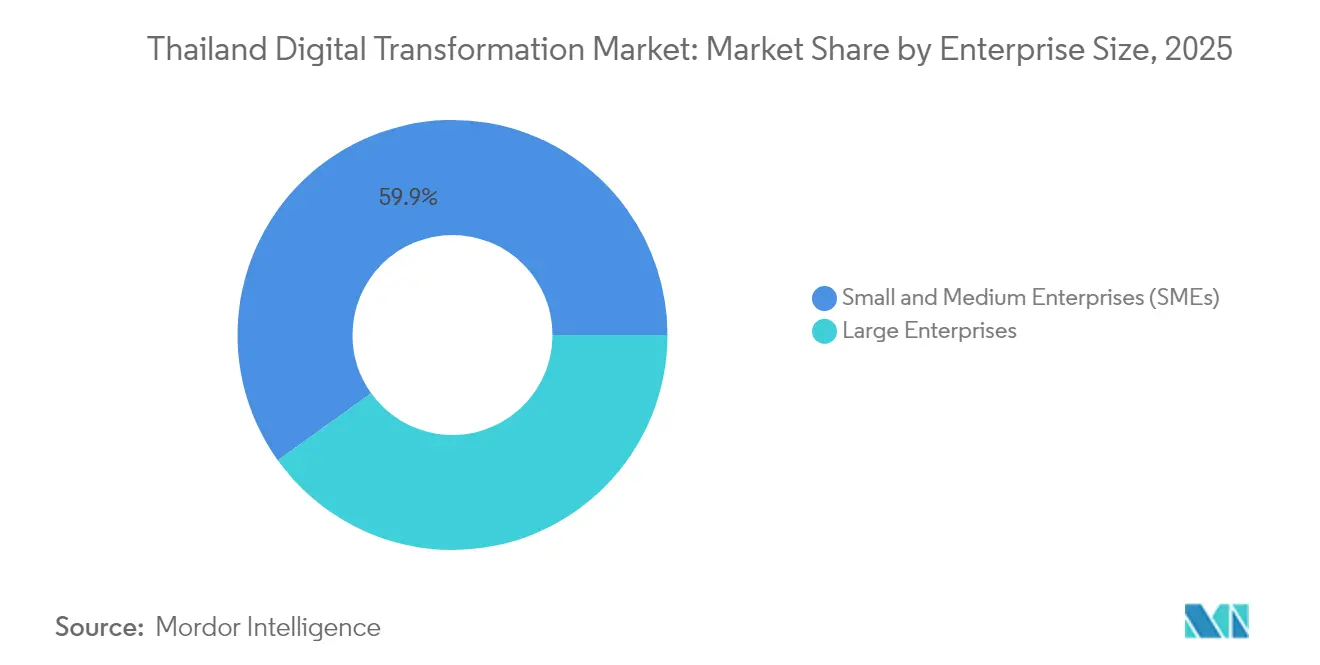

- By enterprise size, large enterprises controlled 40.10% share of the Thailand digital transformation market size in 2025, whereas SMEs are projected to expand at 14.95% CAGR through 2031.

- By end-user industry, retail and e-commerce commanded 13.85% share of the Thailand digital transformation market size in 2025; healthcare is progressing at a 18.65% CAGR to 2031.

- By deployment model, cloud deployment accounted for 55.05% share of the Thailand digital transformation market size in 2025 and is growing at a 19.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand operates as part of an interconnected international environment rather than as a self-contained country level unit. The digital transformation (dx) market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Thailand Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of big-data analytics, AI & ML | +2.1% | National; Bangkok & EEC | Medium term (2–4 years) |

| Government’s Thailand 4.0 and cloud-first policies | +1.8% | National; focus on EEC | Long term (≥4 years) |

| Rapid 5G/fiber roll-out boosting connectivity | +1.5% | National; urban first | Short term (≤2 years) |

| Hyper-scale cloud investments | +1.7% | Bangkok, Central, EEC | Medium term (2–4 years) |

| EEC edge-data-center clusters | +1.2% | Eastern Economic Corridor | Medium term (2–4 years) |

| AI-enabled public-safety pilots | +0.9% | Bangkok & nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surging adoption of big-data analytics, AI & ML

New AI spending, led by a THB 1.5 billion government program, is on track to create 30,000 AI-skilled workers by 2027.[1]Bangkok Post, “National AI strategy outlines 6 projects,” bangkokpost.com Hospitals such as Vimut already use AI triage systems to ease physician shortages, while manufacturers including Thai Summit have lifted revenue by 50% after integrating predictive-maintenance AI into shop-floor execution. The banking sandbox run by the Bank of Thailand allows risk-based pricing that uses machine-learning models for real-time rate setting. AWS research shows workers with AI skills could command salary premiums exceeding 41%, which is accelerating enrollment in reskilling courses. Together these factors underpin steady demand for analytics platforms, cloud GPUs, and data-governance software inside the Thailand digital transformation market.

Government’s Thailand 4.0 & cloud-first policies

The Digital Government Development Agency is automating 149 public services under its “Smart Nation Smart Life” roadmap.[2]Digital Government Development Agency, “Smart Nation Smart Life,” dga.or.th A USD 12.5 billion digital-wallet scheme distributes targeted payments via the Tang Rat super-app, illustrating how citizen-facing platforms stimulate back-office modernization. Tax holidays, fast-track permits, and a USD 2.7 billion data-center incentive package have drawn a 300 MW hyperscale build from Haoyang Cloud&Data, broadening infrastructure for local software houses. These initiatives encourage every ministry to migrate workloads to accredited cloud regions, giving sustained structural lift to the Thailand digital transformation market.

Rapid 5G/fiber roll-out boosting connectivity

The National Broadcasting and Telecommunications Commission expects 5G to cover nearly 90% of the population by end-2025, enabling latency-sensitive use cases such as automated port cranes and remote radiology. True Corporation’s merger with dtac is increasing spectrum density, while AIS has demonstrated mmWave manufacturing lines with Alliance Laundry Systems. Big-ticket transport projects, including an electric-bus fleet and 554 km metro expansion, further depend on high-capacity mobile backhaul. These roll-outs are pivotal to edge-native architectures, sustaining momentum inside the Thailand digital transformation market.

Hyper-scale cloud investments (AWS, Google, Huawei)

AWS committed more than USD 5 billion through 2037 for its Asia Pacific (Thailand) Region, supporting 11,000 jobs annually and injecting USD 10 billion into GDP AWS. Google’s USD 1 billion Chonburi region is forecast to add USD 4 billion in economic output and create 14,000 jobs yearly Google Cloud. Local firms such as Bank of Ayudhya and CP Group are already migrating core platforms, accelerating SaaS demand. Cloud security spending is rising 25% per year to meet PDPA controls, adding another high-growth pocket within the Thailand digital transformation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PDPA-driven privacy & cybersecurity compliance burden | -1.4% | National, hitting multinationals hardest | Medium term (2-4 years) |

| Acute digital-talent shortage & wage inflation | -1.6% | Nationwide, most acute in Bangkok and the EEC | Long term (≥4 years) |

| Limited capital budgets at legacy SME manufacturers | -0.8% | Northern and Central factory belts | Medium term (2-4 years) |

| Higher power prices squeezing data-center margins | -0.7% | Bangkok, Central region, and EEC server clusters | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

PDPA-driven privacy & cybersecurity compliance burden

Since full PDPA enforcement in 2024, fines have reached THB 7 million and now extend to overseas processors that handle Thai resident data.[3]Chambers and Partners, “Data Protection & Privacy 2025—Thailand,” chambers.com Cross-border transfer rules released in 2024 require data-mapping exercises and frequent audits, raising cost structures for cloud migrations. Attack volumes averaging 3,180 per week, 70% higher than the global mean, compel companies to harden defenses and divert OPEX from innovation budgets. The extra layers of encryption, tokenization, and consent management moderate, but do not halt, growth in the Thailand digital transformation market.

Acute digital-talent shortage & wage inflation

Thailand needs 100,000 AI professionals yet has only 21,000 qualified workers, pushing annual salaries for AI engineers to THB 1.5 million.[4]nationthailand, “Thailand eyes special visas for digital nomads,” nationthailand.com A THB 5 billion state program will train 17,500 specialists across semiconductors, EVs, and AI, while AWS pledges to upskill 100,000 citizens by 2026 Bangkok Post. Global Digital Talent visas aim to lure remote experts, but persistent gaps still lengthen project timelines and inflate payrolls. This shortage constrains deployment capacity in the Thailand digital transformation market, especially for SMEs that cannot match multinational pay scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IoT dominance drives edge computing evolution

Internet of Things held 19.85% share of the Thailand digital transformation market in 2025 as manufacturers connected sensors to track machine status and retailers instrumented supply chains. Cloud & Edge Computing is rising fastest at a 20.55% CAGR, supported by new hyperscale regions and corridor-level micro-data centers that supply low-latency compute. The Thailand digital transformation market size for cloud-centric solutions is projected to widen sharply as factories retrofit robotics lines and as hospitals integrate diagnostic devices into patient record systems. Analytics, AI, and ML add depth by converting raw data into decisions; government funding for 30,000 new specialists accelerates this pipeline. Extended reality pilots in tourism and rehabilitation clinics showcase fresh experiential layers that rest on the same edge backbone. Industrial robots, fuelled by THB 45 billion earmarked for Industry 4.0, are expected to lift shop-floor automation from today’s 30% to 50% within five years . Blockchain remains niche yet influential, with the Bank of Thailand’s CBDC sandbox proving cross-border payment viability and Phuket’s crypto-tourism pilot enabling point-of-sale settlement. Cybersecurity has become a foundational purchase, expanding 9.27% annually to USD 572.6 million by 2029 as attackers target expanded attack surfaces. Digital twins and mobility platforms round out the stack, ensuring the Thailand digital transformation market delivers value beyond mere connectivity.

By End-User Industry: Healthcare transformation outpaces retail leadership

Retail and e-commerce retained leadership with 13.85% share in 2025, helped by a USD 26.5 billion e-commerce sector where mobile devices generate more than 80% of checkouts. Yet healthcare is now the high-velocity customer, advancing at a 18.65% CAGR through 2031 as hospitals adopt AI triage, telemedicine, and electronic medical records. The Thailand digital transformation market share for healthcare will rise as teleconsultation apps such as Mordee scale alongside public insurance reforms. Manufacturers remain pivotal, illustrated by Thai Summit’s downtime cut from 90 minutes to 20 minutes per shift after installing MES automation. Energy companies like PTTEP embed digital twins and AI in exploration to support THB 261 billion annual outlays, while transport agencies allocate more digital budget to traffic analytics and fleet electrification. Finance continues to digitize aggressively, with KASIKORNBANK chasing double-digit ROE through 22.2 million active app users. Each vertical’s trajectory underscores the breadth of opportunity inside the Thailand digital transformation market.

By Enterprise Size: SME acceleration challenges large-enterprise dominance

Large enterprises controlled 40.10% of spending in 2025 thanks to deeper capital pools and central IT teams. Despite that lead, SMEs are growing at 14.95% CAGR through 2031, signaling a pivotal shift in the Thailand digital transformation market. Cloud pay-as-you-go billing and state loan guarantees reduce upfront costs, while dedicated programs under the Innovation-Driven Enterprise scheme steer grants toward firms with THB 100-1,000 million in sales. ASEAN’s SME Policy Index 2024 finds Thai micro-enterprises that implement digital tools improve logistics efficiency and revenue per employee. Persistent gaps in cybersecurity awareness and digital literacy still hamper the smallest firms, making managed-service bundles a rising sales channel.

By Deployment Model: Cloud infrastructure accelerates hybrid adoption

Cloud deployment captured 55.05% share in 2025 and will remain the growth engine, expanding at 19.95% CAGR through 2031 as more workloads migrate to local regions operated by AWS, Google, and Huawei. PDPA data-sovereignty clauses keep certain banks and state utilities on-premise, yet hybrid architectures are flourishing because they balance compliance with scalability. The Thailand digital transformation market size for hybrid models is rising quickly where factories need on-premise control-loops but still analyze data in the cloud for maintenance and supply-chain orchestration. A separate USD 17.4 million cloud-security segment is growing at 25% yearly, pulling in vendors that harden container pipelines and zero-trust frameworks.

Geography Analysis

Thailand digital transformation market momentum varies sharply by region yet exhibits an unmistakable eastward pull. The Eastern Economic Corridor is adding 12.95% CAGR to 2031 on the back of THB 1.34 trillion smart-city funding, a USD 1 billion Google data center, and an AWS availability zone that collectively anchor a deep technology talent reservoir. Industrial land take-up jumped 53% in 1H 2024, showing manufacturer preference for edge-ready parcels that shortcut deployment timelines. Upgrades at Laem Chabang Port and U-Tapao Airport require integrated digital twins, further enlarging addressable spending on sensors, 5G private networks, and SaaS logistics platforms.Bangkok and adjacent central provinces remain the strategic command center. Government ministries are migrating services to the cloud under a “Smart Nation Smart Life” agenda, while local banks roll out super-apps that shape consumer expectations. A THB 2.68 trillion transport overhaul, including 3,100 electric buses and 554 km of rail, creates strong demand for fleet-management analytics and payment gateways. Nationwide PDPA enforcement, however, forces Bangkok-based multinationals to update data-protection controls, stimulating a secondary market for privacy-enhancing technologies.Northern and Northeastern provinces illustrate how tailored programs support inclusive digital progress. Government-backed factory-logistics pilots cut transport cost by 25% and inventory days by 55% in Chiang Mai and Lampang, while Betagro’s THB 297 million smart-processing plant demonstrates rural high-tech job creation. In the South, AIS Business deploys 5G smart-city platforms that improve tourist services and port congestion management. A rolling THB 253.45 billion infrastructure budget spreads broadband and roadway improvements nationwide, setting the stage for more uniform growth inside the Thailand digital transformation market.

The digital transformation (dx) market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Asia, Europe, and North America, along with detailed country-level analysis for South Korea, Japan, Netherlands, Canada, Mexico, and Spain.

Competitive Landscape

Thailand digital transformation market shows moderate fragmentation as global hyperscalers, local carriers, and specialized software vendors carve out defensible positions. AWS, Google, and Microsoft lead infrastructure services, using billion-dollar data-center projects to lock in enterprise accounts and earn cross-sell rights for analytics and AI stacks. True Corporation and AIS Business exploit 5G footprints to bundle connectivity with edge services, giving them a localized advantage in sectors where low latency is critical. International software publishers—SAP, Oracle, Salesforce—focus on large conglomerates, while Thai ISVs customize lightweight platforms for SMEs priced out of global suites.

Cybersecurity emerges as a stand-alone battleground. Attack rates 70% above global norms push CISOs to prioritize threat-intelligence services and zero-trust network access, which has allowed regional specialists to gain share against broader platform vendors. True IDC’s joint venture with SIAM.AI CLOUD showcases vertical integration: hosting generative AI workloads atop domestic GPUs adds sovereign-cloud assurances attractive to banks and state bodies. In healthcare, start-ups such as Eidy exemplify point-solution disruptors that use AI to augment scarce medical staff, indicating white-space opportunities for niche providers unattached to legacy stacks.

Strategic differentiation increasingly hinges on multi-technology convergence. Vendors that combine cloud, AI, IoT, and cybersecurity in unified service catalogs neutralize single-product commoditization. Government procurement rules that reward local data residence and enterprise data-sovereignty further shape partner ecosystems and influence market-entry playbooks. Collectively, these dynamics sustain competitive churn yet reinforce the growth trajectory of the Thailand digital transformation market.

Thailand Digital Transformation Industry Leaders

Accenture PLC

Google LLC (Alphabet Inc.)

Siemens AG

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thailand confirmed THB 1.34 trillion allocation to build a Huai Yai smart city under the EEC program, targeting 350,000 residents served by pervasive IoT grids.

- May 2025: The National AI Committee officially launched, coordinating AI policy across ministries and the private sector.

- March 2025: The cabinet approved USD 2.7 billion in data-center investments, including a 300 MW build by Haoyang Cloud&Data.

- March 2025: Betagro opened a THB 297 million smart processing plant in Lampang that uses real-time monitoring to meet global food-safety standards.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Thailand's digital transformation market as all business-to-business spending on enabling technologies, including analytics and AI, extended reality, IoT, industrial robotics, blockchain, additive manufacturing, cybersecurity, plus cloud and edge computing that organizations deploy to digitize operations, customer interfaces, and new-service creation. Values are expressed in constant 2024 USD and include software, hardware, and associated services purchased within Thailand.

Scope Exclusions: Pure consumer devices, standalone telecom voice revenues, and unlicensed off-the-shelf apps are omitted.

Segmentation Overview

- By Type

- Analytics, AI and ML

- Extended Reality (XR)

- Internet of Things (IoT)

- Industrial Robotics

- Blockchain

- Additive Manufacturing / 3-D Printing

- Cyber-security

- Cloud and Edge Computing

- Others

- By End-User Industry

- Manufacturing

- Oil, Gas and Utilities

- Retail and E-commerce

- Transportation and Logistics

- Healthcare

- BFSI

- Telecom and IT

- Government and Public Sector

- Others

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Deployment Model

- On-premise

- Cloud

- Hybrid

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with Thai CIOs, hyperscale-cloud executives, systems integrators, and policy officials across Bangkok, the Eastern Economic Corridor, and Chiang Mai. Discussions validated adoption timelines, typical deal sizes, and sector-specific pain points, filling data gaps from desk work.

Desk Research

We began with industry statistics from the Digital Economy Promotion Agency, the National Broadcasting and Telecommunications Commission, and trade bodies such as the Thai IoT Association. Supplementary insights came from UN Comtrade shipment data, World Bank digital-economy trackers, company 10-Ks, and press releases. Subscription databases, such as D&B Hoovers for enterprise financials and Dow Jones Factiva for news flow, helped us size supplier revenue streams. These sources, while illustrative, do not represent the full range consulted.

Market-Sizing & Forecasting

A top-down demand-pool model starts with national ICT outlays and then apportions digital-transformation spend using penetration ratios for 5G enterprise connections, SaaS migration, and e-commerce GMV, which are in turn benchmarked against macro indicators like manufacturing PMI and FDI in data centers. Selected bottom-up checks, including sampled supplier billings and average selling price multiplied by volume estimates, fine-tune totals. Key variables include 5G population coverage, cloud hyperscaler capital expenditure, PDPA-driven cybersecurity budgets, SME digital loan disbursements, and smart-city investment pipelines. Five-year forecasts employ multivariate regression blended with scenario analysis to capture policy shocks, such as new virtual-bank licenses, and currency swings. Where granular bottom-up data was partial, we adjusted segment weights using primary-research consensus.

Data Validation & Update Cycle

Outputs pass variance tests against import data, listed-vendor revenues, and independent digital-economy indices. A senior analyst reviews anomalies before sign-off. We refresh models annually and issue interim updates when events, such as large hyperscale investments, trigger material shifts. Just before publication, an analyst reruns the checks so clients receive our freshest view.

Why Our Thailand Digital Transformation Baseline Commands Reliability

Published estimates vary widely because publishers choose different scope items, forecasting windows, and currency assumptions.

Key gap drivers include whether hardware services are counted, the depth of SME coverage, use of nominal versus constant exchange rates, and refresh cadence. Mordor reports focus on enterprise spending linked to measurable technology rollouts, use constant 2024 USD, and update every twelve months, which narrows volatility that arises when others rely on older input series or broad GDP ratios.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.06 B (2025) | Mordor Intelligence | - |

| USD 9.21 B (2024) | Regional Consultancy A | Excludes robotics services; uses 2023 FX rates |

| USD 8.35 B (2025) | Trade Journal B | Omits edge-computing spend and SME cloud uptake |

| USD 12.5 B (2022) | Global Consultancy A | Counts consumer devices and applies nominal growth multipliers |

In sum, the disciplined scope definition, variable alignment, and annual refresh cycle adopted by Mordor Intelligence give decision-makers a balanced, transparent baseline that traces directly to observable Thai technology-adoption signals.

Key Questions Answered in the Report

What is the current size of the Thailand digital transformation market?

It stood at USD 10.94 billion in 2026 and is projected to reach USD 16.64 billion by 2031.

Which technology segment is growing fastest?

Cloud & Edge Computing is expanding at a 20.55% CAGR through 2031, supported by hyperscale data-center investments.

Why is the Eastern Economic Corridor important for digital growth?

The EEC concentrates more than half of new tech investment pledges, offers edge-ready industrial parks, and is growing at a 12.95% CAGR.

How does the PDPA affect digital projects?

The PDPA imposes strict consent and data-transfer rules, adding compliance costs yet stimulating demand for cybersecurity and privacy solutions.

What talent initiatives address the digital-skills gap?

A THB 5 billion government program and vendor-led reskilling commitments aim to train 17,500 AI, semiconductor, and EV specialists, while special visas attract foreign experts.

Which end-user industry shows the highest growth?

Healthcare leads with a 18.65% CAGR to 2031 as hospitals adopt AI triage, telemedicine, and electronic medical records.

Page last updated on: