South East Asia CRM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.27 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 1.55% CAGR |

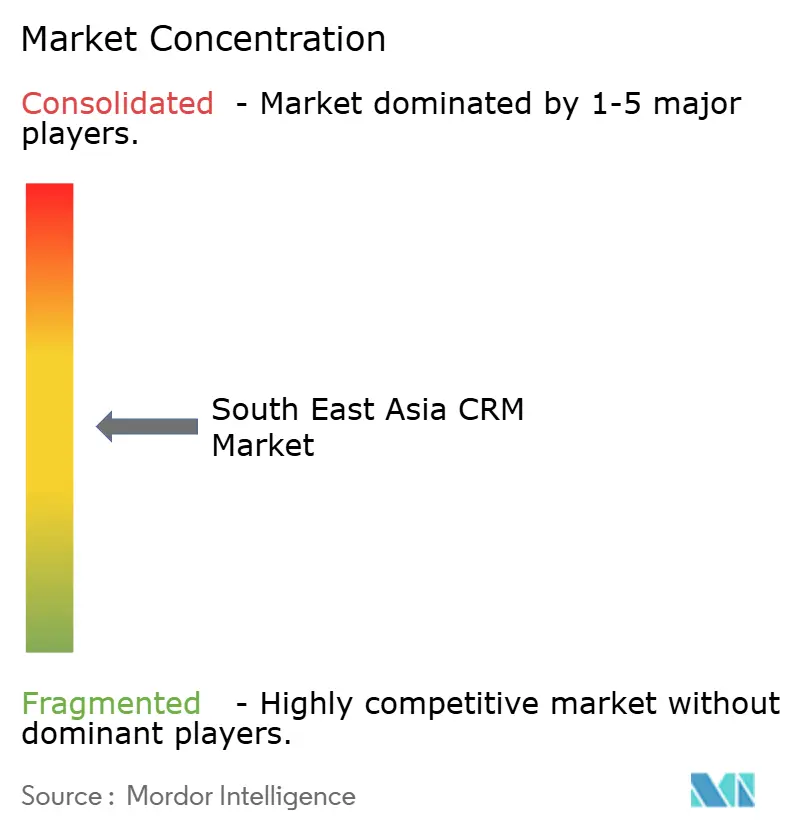

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South East Asia CRM Market Analysis by Mordor Intelligence

The Southeast Asia CRM market size was valued at USD 2.27 billion in 2025 and estimated to grow from USD 2.31 billion in 2026 to reach USD 2.49 billion by 2031, at a CAGR of 1.55% during the forecast period (2026-2031). Cloud-first grant schemes in Singapore, Thailand, and Malaysia are underwriting rapid adoption, while data-center investments by global hyperscalers reduce latency and satisfy sovereignty rules. Currency fluctuations have raised the cost of USD-denominated SaaS contracts, yet subsidized funding and open-API mandates offset some of the budget pressure. Social-commerce expansion is steering vendors toward LINE, WhatsApp, and TikTok integrations that deliver conversational selling at scale. At the same time, embedded artificial intelligence elevates upsell performance by predicting customer intent and generating tailored content in real time.

Key Report Takeaways

- By organization size, SMEs captured 42.60% of the Southeast Asia CRM market share in 2025 and are projected to expand at a 2.11% CAGR through 2031.

- By deployment model, cloud solutions accounted for 63.10% of the Southeast Asia CRM market size in 2025 and are forecast to grow at a 2.72% CAGR through 2031.

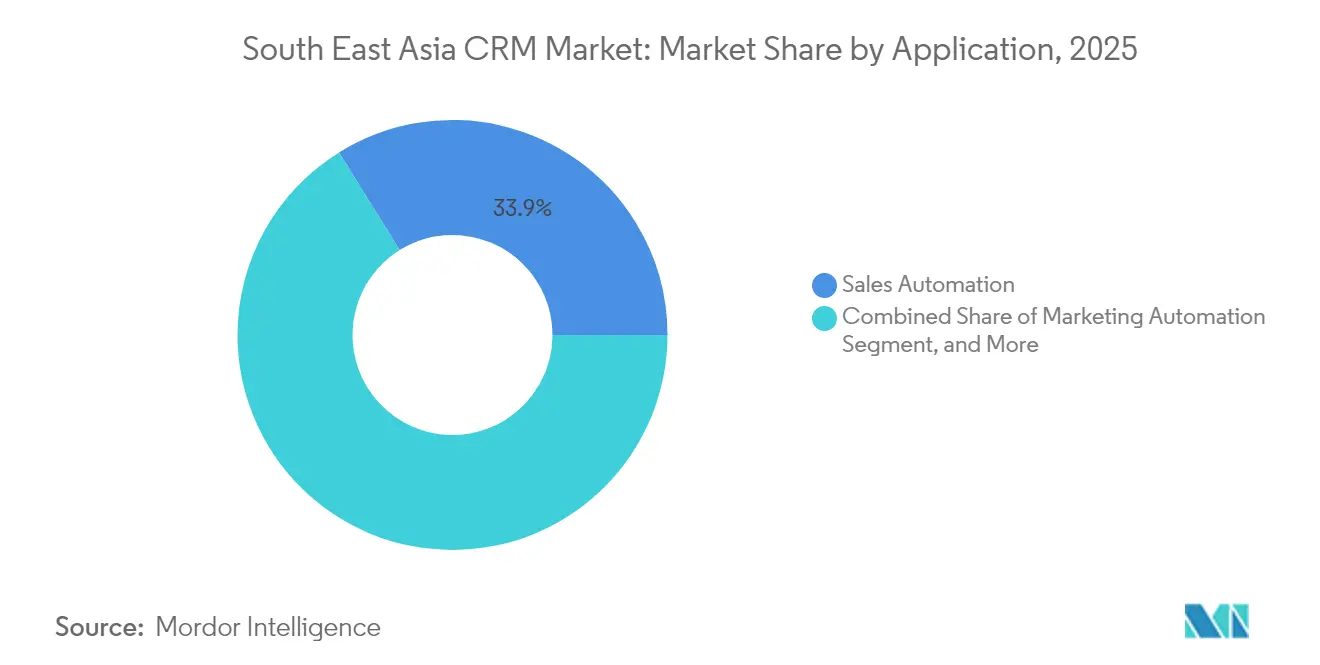

- By application, sales automation led with a 33.85% revenue share in 2025, while marketing automation is set to record the fastest 2.42% CAGR through 2031.

- By end-user vertical, retail and e-commerce contributed 27.20% of deployments in 2025; BFSI is expected to advance at a 3.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South East Asia CRM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digitalisation across SMEs | +0.80% | Indonesia, Thailand, Malaysia with spillover to Philippines | Medium term (2-4 years) |

| AI-enabled hyper-personalisation driving upsell | +0.60% | Singapore, Malaysia core, expanding to Indonesia and Thailand | Long term (≥ 4 years) |

| Social-commerce boom integrating CRM into chat-apps | +0.40% | Thailand, Indonesia, Philippines with LINE and WhatsApp dominance | Short term (≤ 2 years) |

| Government 'Go-Digital' incentives in ASEAN | +0.50% | Singapore, Thailand, Malaysia with national program rollouts | Medium term (2-4 years) |

| Open-API ecosystems lowering vendor lock-in | +0.30% | Indonesia, Singapore with SNAP and open banking initiatives | Long term (≥ 4 years) |

| CX outsourcing pivoting to value-add CRM services | +0.20% | Philippines, Malaysia with established BPO infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digitalization Across SMEs

Government-backed grant programs are shifting technology spending toward Software-as-a-Service, allowing SMEs to bypass expensive on-premises stacks entirely. Singapore’s enhanced SMEs Go Digital scheme now covers up to 50% of pre-approved CRM solutions for the city-state’s 219,000 small businesses, which collectively generate USD 142.3 billion of gross value added.[1]Infocomm Media Development Authority, “SMEs Go Digital,” imda.gov.sg Thailand’s Go Digital ASEAN initiative trained more than 44,000 micro and small firms, and 69% reported revenue growth after adopting customer-facing digital tools. In Indonesia, pre-pandemic digital adoption among MSMEs stood at 12.5%, yet the COVID-19 lockdowns made cloud CRM essential for sustaining buyer communication, pushing implementation rates materially higher. Malaysia’s latest SME survey shows 82% online adoption, but 77% remain at the entry stage, leaving major headroom for CRM modernization. Together, these shifts anchor long-run demand for the Southeast Asia CRM market.

AI-Enabled Hyper-Personalization Driving Upsell

The next growth curve for the Southeast Asia CRM market stems from machine-learning tools that turn static customer data into predictive revenue actions. Thai banks illustrate the model, combining real-time behaviour scoring with generative AI content to raise cross-sell conversion and improve client retention.[2]Krungsri Research, “Social Commerce: The New Wave of E-commerce,” krungsri.com Singapore firms show the highest readiness: 94.6% have adopted at least one digital capability, and 44% run production AI workloads.[3]AvePoint, “Combating IT Talent Shortage,” avepoint.com Regional vendors are democratizing the technology by embedding pretrained models into SME-friendly packages; an example is the AI-enabled CRM launched by Advocado in partnership with HUAWEI CLOUD and 4Paradigm. These features resonate with social-commerce merchants that need one-to-one messaging at scale rather than blanket promotions. As deployment costs fall, AI modules will become baseline expectations rather than premium options within the Southeast Asia CRM market.

Social-Commerce Boom Integrating CRM Into Chat-Apps

Southeast Asia’s mobile consumers treat messaging platforms as storefronts, a behaviour that forces CRM systems to support conversational workflows. In Thailand, 91% of shoppers made purchases through social channels in the last six months, with Facebook and LINE serving as primary gateways. Vendors respond by building native connectors: Antsomi’s CDP 365 on LINE enables rich-menu personalization, gamification, and data capture in a single canvas. Indonesian telecom operator Telkom has rolled out multi-chatbot CRM for WhatsApp, Facebook, Telegram, and LINE to cut service costs while lifting customer satisfaction. HubSpot’s TikTok integration in Singapore now drops leads directly into CRM, acknowledging that traditional landing-page funnels underperform where short-form video dominates. These rollouts blend commerce, marketing, and service into chat threads that customers already use daily, reinforcing the Southeast Asia CRM market’s channel-agnostic evolution.

Government “Go-Digital” Incentives in ASEAN

Policy makers across the bloc have built a multilayer set of fiscal incentives, regulatory clarity, and advisory services that remove classic barriers to CRM upgrades. Singapore’s Industry Digital Plans map software choices by sector, while CTO-as-a-Service portals offer step-by-step guidance on vendor selection. The latest ASEAN SME Policy Index confirms every member state now runs targeted e-commerce and digital-payment programs, funneling resources to the 99% of enterprises classified as SMEs.[4]ASEAN Secretariat, “SME Policy Index 2024,” asean.org Malaysia’s IR 4.0 Master Plan and multi-billion-dollar cloud region investments from Oracle create the infrastructure layer essential for sophisticated CRM deployments. Regional education grants further build digital literacy, as illustrated by The Asia Foundation’s Go Digital ASEAN cohort, where 77% of participants adopted at least one new tool. The coordinated policy architecture locks in long-term structural support for the Southeast Asia CRM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchy data-privacy enforcement across SEA | -0.30% | Indonesia, Thailand, Malaysia with varying PDPA implementations | Medium term (2-4 years) |

| Scarcity of CRM implementation talent | -0.40% | Singapore, Malaysia, Philippines with acute skills shortages | Short term (≤ 2 years) |

| Legacy on-premise ERP lock-ins slowing migration | -0.20% | Indonesia, Thailand with established SAP and Oracle installations | Long term (≥ 4 years) |

| Currency volatility squeezing SaaS budgets | -0.50% | Regional impact with particular pressure in Indonesia and Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of CRM Implementation Talent

Implementation timelines in the Southeast Asia CRM market lengthen because qualified administrators, developers, and change-management specialists remain in short supply. Singapore ranks among the world’s tightest labour markets, with 83% of employers citing hiring challenges, and will need 41,000 additional tech roles by 2028. Malaysia shows only 15% of citizens possessing advanced ICT skills, yet 65% of firms list digital talent as a priority. Startups likewise struggle to fill CRM-dependent roles—40% lack customer-success talent and 46% lack marketing expertise. Indonesia’s willingness-to-reskill ratio sits at 53%, a figure made more problematic by technology’s rapidly shrinking skill half-life. Higher wages and longer projects raise the total cost of ownership, prompting some companies to defer upgrades even when funding is available.

Currency Volatility Squeezing SaaS Budgets

Southeast Asian finance chiefs benchmark most CRM subscriptions in USD, so local currency depreciation magnifies recurring costs. The impact is felt acutely by mid-market enterprises that lack hedging tools; as a result, some companies choose local vendors or hybrid deployments to cap exposure. Analysts note that the 2024 deal value for technology investments in Indonesia fell 66% year over year, reflecting both macro headwinds and funding caution. Inflation worries add another layer of unpredictability, prompting CFOs in Thailand to delay discretionary software upgrades until clearer economic signals emerge. Although government grants soften the blow for SMEs, the broader pricing uncertainty tempers adoption speed and trims incremental growth potential for the Southeast Asia CRM market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SME Momentum Outpaces Enterprise Upgrades

Small and medium enterprises held 42.60% of the Southeast Asia CRM market share in 2025 and are expanding at a 2.11% CAGR to 2031. Subsidized grant schemes and pay-as-you-go cloud billing align tightly with SME cash-flow cycles. Singapore’s SMEs Go Digital grants bridge upfront investment gaps, while Malaysia’s collaboration between Zoho and Cradle Fund delivers USD 10 million in software credits to 4,400 start-ups. Indonesian SMEs report sales uplifts of up to 30% within one year of CRM usage.

Large enterprises still generate the bulk of absolute revenue for the Southeast Asia CRM market, but their upgrade cadence is slower due to complex legacy estates. Integration with entrenched SAP and Oracle ERPs frequently involves multi-phase projects that must align with global transformation roadmaps. Boards remain cautious about migrating mission-critical data off-premises until in-country data-center availability and legal clarity mature. As a result, SME demand is increasingly the headline growth story, while enterprise accounts drive premium professional-service revenue.

By Deployment Model: Cloud Leads Growth While Hybrid Cushions Compliance

Cloud deployments captured 63.10% of the Southeast Asia CRM market size in 2025 and are projected to grow at a 2.72% CAGR. Singapore tops regional cloud readiness indices with a 56/60 score for banking, providing explicit guidelines on cross-border data flows. Indonesia’s SNAP open-API mandate lowers integration costs, encouraging banks and fintechs to move client engagement workloads into the cloud.

On-premises solutions persist in heavily regulated verticals or where data localization laws remain stringent, particularly in Indonesia and Thailand. Hybrid architectures serve as a transitional setup, giving firms on-site control for sensitive fields while benefiting from cloud elasticity for customer-facing use cases. Oracle’s USD 6.5 billion plan for a Malaysian cloud region expands local residency options, making full SaaS deployments more palatable for compliance teams.

By Application: Marketing Automation Overtakes in Growth

Sales automation maintained a 33.85% revenue share in 2025, reflecting its historical primacy. Marketing automation, however, is the fastest-rising module at 2.42% CAGR as brands lean into multichannel orchestration. TikTok, LINE, and WhatsApp now feed real-time leads directly into CRM, creating a feedback loop that improves targeting accuracy.

Customer service and support modules continue to gain traction among BPO-heavy economies such as the Philippines, where vast contact-center operations require omnichannel ticketing. Contact-center CRM adoption dovetails with the country’s English-language labour advantage, cementing its role as a regional service hub.

By End-User Vertical: BFSI Accelerates Amid Open-Banking Rules

Retail and e-commerce represented 27.20% of the Southeast Asia CRM market in 2025, powered by mobile wallets and “shoppertainment.” Loyalty programs like Bata’s multinational rollout show ROI multipliers—57× Facebook campaign returns in Malaysia and 2.2× higher spend in Singapore. BFSI, though smaller in base, records the highest 3.02% CAGR as digital-banking licensees in Singapore and Malaysia require enterprise-grade CRM from day one.

Manufacturing sees steady uptake owing to supply-chain diversification into Vietnam, Thailand, and Indonesia, where ERP and CRM converge to manage distributor networks. Government adoption is nascent but rising, especially where national digital-citizen service portals embed CRM features for case management.

Geography Analysis

Indonesia commands 31.10% of the Southeast Asia CRM market in 2025 on the strength of its 53 million SMEs and growing fintech scene. The National Open API Payment Standard, effective June 2025, reduces integration friction, particularly for BFSI deployments. Salesforce opened a Jakarta office and appointed its first country leader to deepen local engagement. Yet technology deal value fell 66% in 2024, and data-localization clauses still lengthen procurement cycles.

The Philippines is set to record the highest 3.34% CAGR to 2031. Forthcoming Salesforce operations endorsed by the Department of Trade and Industry will add AI training facilities and SME enablement programs. The Bangko Sentral ng Pilipinas permits offshore cloud hosting under strict controls, unlocking CRM SaaS adoption for rural lenders. Established BPO infrastructure ensures ready demand for omnichannel customer-service modules, although 38% of startups cite insufficient data maturity as an implementation barrier.

Singapore remains the premium segment due to predictable regulations and high per-capita IT spend. The updated SMEs Go Digital grants cover AI-centric CRM, and Salesforce’s USD 1 billion commitment designates the city as a regional R&D hub. Talent shortages may hinder rollouts, but the country’s partner ecosystem partly compensates through upskilling incentives.

Thailand and Malaysia round out the core markets. Thailand leverages its social-commerce dominance LINE penetration exceeds 80% to pioneer chat-integrated CRM configurations. Malaysia positions itself as a cloud hub after Oracle’s sovereign AI investment, giving regulated industries more local options.

Competitive Landscape

Global platform leaders such as Salesforce, Microsoft, and Oracle compete for multinational accounts, each backing local data centers to satisfy residency laws. Salesforce’s USD 1 billion plan in Singapore funds Agentforce AI and regional partner enablement, while Oracle’s Malaysian build-out widens in-country compliance coverage. Microsoft leans on its Cloud Solution Provider channel, offering Dynamics 365 bundles via regional systems integrators.

Regional challengers differentiate through vertical expertise and government-aligned pricing. Creatio’s no-code playbook resonates with Indonesian banks, supported by partnerships with PT Mastersystem Infotama and PT Indocyber Global Teknologi. Barantum, Qontak, and Deskera focus on language localization and bundled accounting features favoured by SMEs.

Talent scarcity shapes competitive dynamics: vendors with strong service ecosystems and template-based deployments shorten time-to-value. Social-commerce tooling represents the next battleground; integrations with LINE, TikTok, and WhatsApp are decisive for retailers and DTC brands. Open-API mandates like Indonesia’s SNAP Favor providers that expose modular, integration-ready architectures.

South East Asia CRM Industry Leaders

Salesforce.com Inc.

Oracle Siebel

SAP SE

IBM Corporation

Microsoft Dynamics by Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Salesforce announced a USD 1 billion investment in Singapore to expand Agentforce AI and co-innovate with Singapore Airlines.

- March 2025: EY Digital Solutions acquired Indonesian Microsoft partner PT Kreatif Dinamika Integrasi, adding 114 Dynamics 365 specialists.

- March 2025: Catcha Digital agreed to buy 51% of Digital Symphony for RM 22.95 million (USD 5.1 million) to merge performance-marketing data with ad inventory.

- February 2025: Creatio opened an Indonesian data center to support AI-native no-code CRM for ASEAN customers.

South East Asia CRM Market Report Scope

The Customer Relationship Management (CRM) Software market is a subsegment of the Enterprise Software market geared toward managing external business contacts and communication in marketing, sales, and acquisition. It offers standalone software designed to help end-user companies manage a customer's entire life cycle, including marketing, sales, customer services, and contact center. The market estimations consider CRM software applications (license/subscription) in Sales, Marketing, Contact centers, and Customer Services. In contrast, CRM Analytics and other custom applications of CRM Software are excluded from the study scope as these are offered as an enhanced capability based on requirement and charged for customization that is not tracked owing to feasibility factors.

The Southeast Asian CRM market is segmented by organization size (small and medium and large scale), deployment size (cloud, on-premise, and hybrid), end-user vertical (services, manufacturing, BFSI, retail and logistics, government), and country (Indonesia, Singapore, Philippines, Thailand, Malaysia, Rest of South East Asia)

The market sizes and forecasts are provided in terms of value (in USD) for all the above segments.

| Small and Medium |

| Large Scale |

| Cloud |

| On-Premise |

| Hybrid |

| Sales Automation |

| Marketing Automation |

| Customer Service and Support |

| Contact Centre |

| Retail and E-commerce |

| BFSI |

| Manufacturing |

| Services (IT, BPO, Hospitality) |

| Government |

| Indonesia |

| Singapore |

| Philippines |

| Thailand |

| Malaysia |

| Rest of the South East Asia |

| By Organization size | Small and Medium |

| Large Scale | |

| By Deployment model | Cloud |

| On-Premise | |

| Hybrid | |

| By Application | Sales Automation |

| Marketing Automation | |

| Customer Service and Support | |

| Contact Centre | |

| By End-User Vertical | Retail and E-commerce |

| BFSI | |

| Manufacturing | |

| Services (IT, BPO, Hospitality) | |

| Government | |

| By Country | Indonesia |

| Singapore | |

| Philippines | |

| Thailand | |

| Malaysia | |

| Rest of the South East Asia |

Key Questions Answered in the Report

What is the current value of the Southeast Asia CRM market?

The market stands at USD 2.31 billion in 2026 with a 1.55% CAGR forecast to 2031.

Which deployment model is most popular in Southeast Asia?

Cloud deployments hold 63.10% share and are expanding at a 2.72% CAGR.

Which user segment is driving growth?

SMEs lead with 42.60% market share and benefit from grant-funded cloud adoption.

Which country offers the fastest growth opportunity?

The Philippines is projected to post the highest 3.34% CAGR through 2031.

Which application area is growing quickest?

Marketing automation is set to grow at a 2.42% CAGR thanks to social-commerce integrations.

How concentrated is vendor competition?

The market earns a concentration score of 5, indicating moderate dominance by top vendors but ample room for regional specialists.

Page last updated on: