Market Overview

| Study Period | 2020 - 2031 |

|---|---|

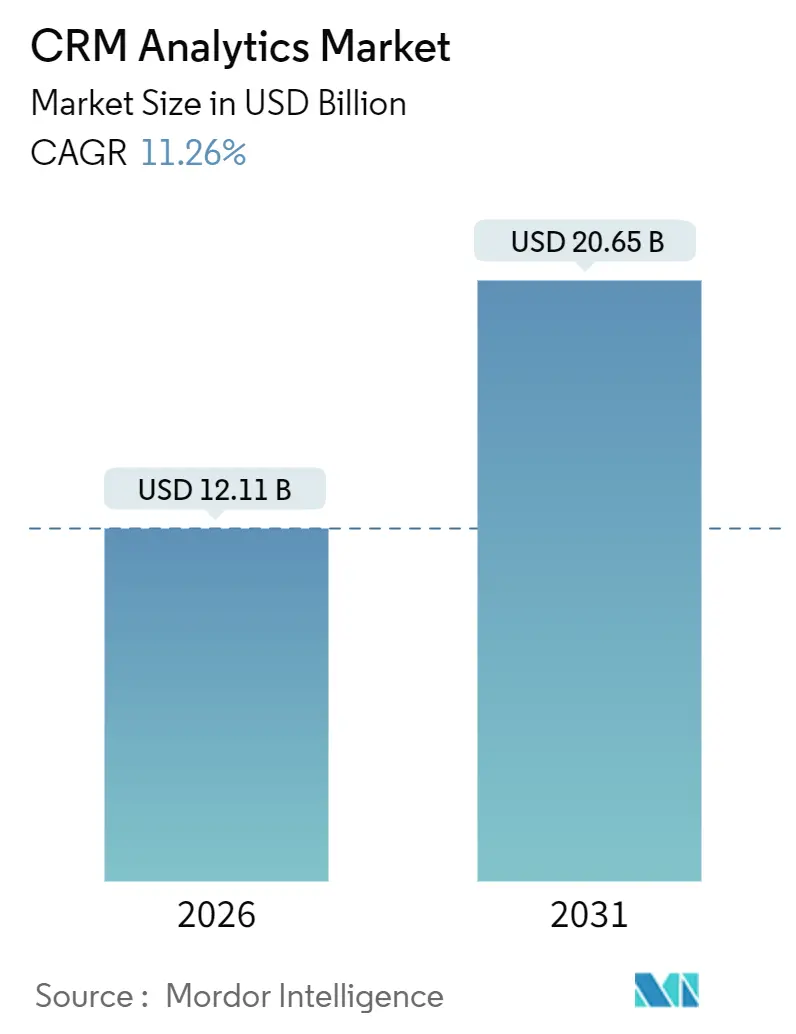

| Market Size (2026) | USD 12.11 Billion |

| Market Size (2031) | USD 20.65 Billion |

| Growth Rate (2026 - 2031) | 11.26% CAGR |

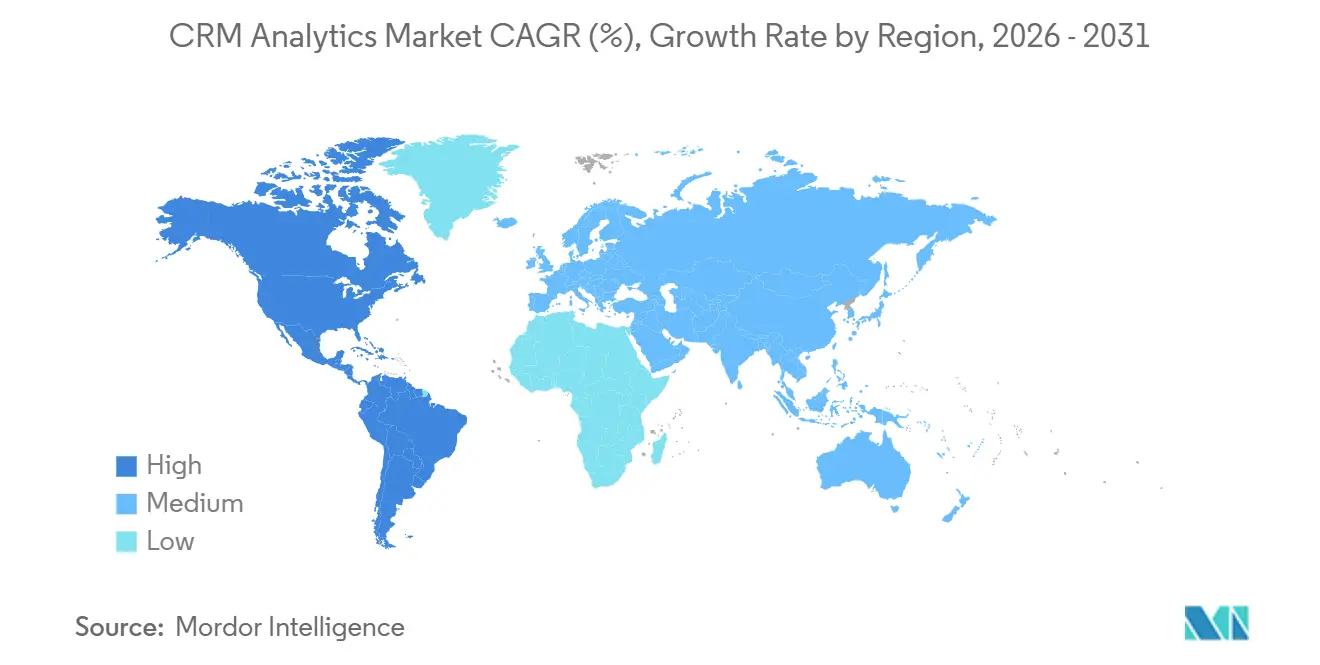

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

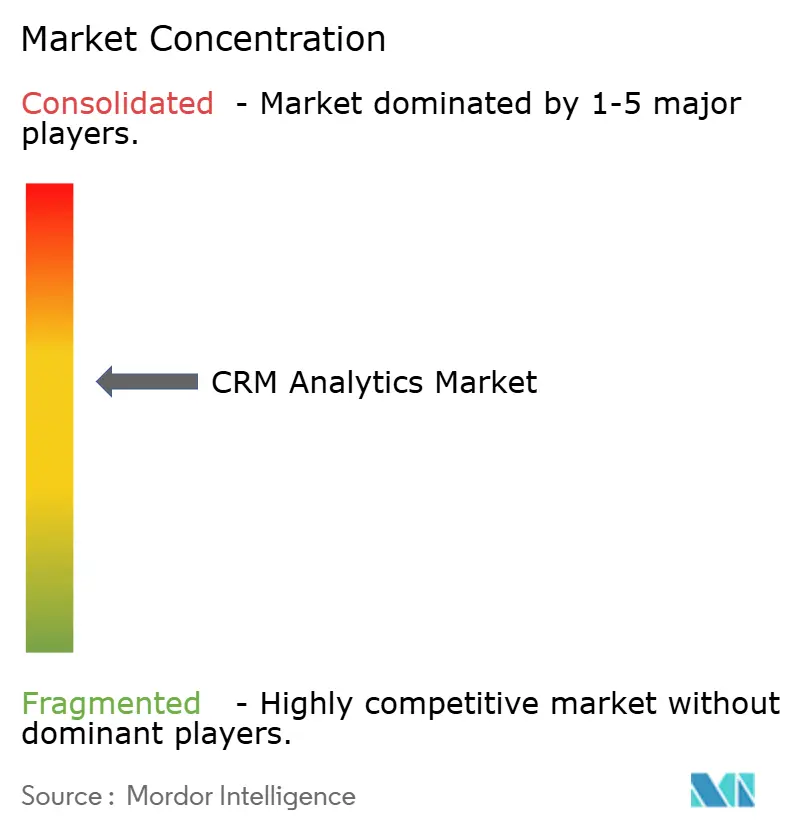

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CRM Analytics Market Analysis by Mordor Intelligence

The CRM Analytics market size is valued at USD 12.11 billion in 2026 and is projected to reach USD 20.65 billion by 2031, registering an 11.26% CAGR during the forecast period. Demand accelerates as enterprises shift from traditional dashboards to prescriptive, real-time decisioning engines embedded in every customer touchpoint. Cloud deployment, the dominant architecture, fulfills elastic compute requirements for large language models while shifting capital expenses to usage-based operational expenses. Social media and web analytics tools integrate unstructured sentiment with structured records, unlocking granular pipeline scoring that was previously not feasible due to the immaturity of transformer models in 2024. Retail and e-commerce firms remain the largest adopters, yet interoperability mandates and patient-engagement APIs push healthcare to become the fastest-growing vertical. SMEs are closing the capability gap by adopting serverless inference and pre-trained vertical models that were once reserved for Fortune 500 budgets.

Key Report Takeaways

- By deployment, the cloud segment led with 63.84% of the CRM Analytics market share in 2025 and is advancing at a 13.35% CAGR through 2031.

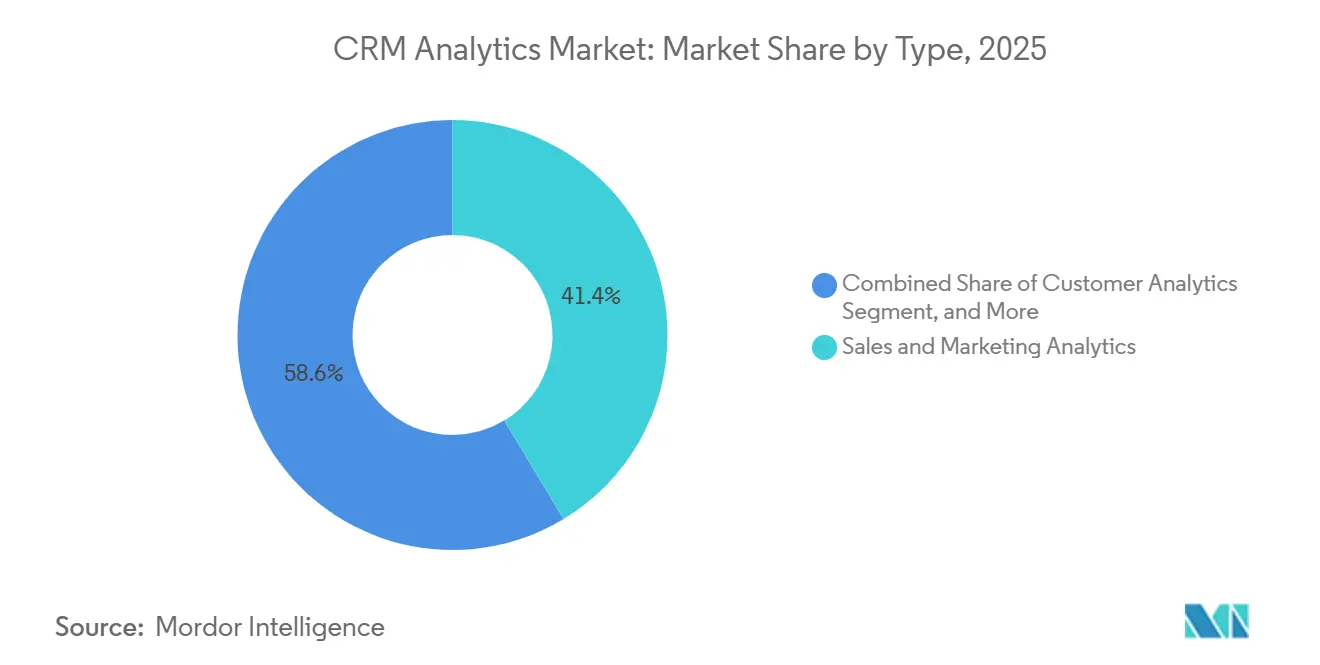

- By type, social media and web analytics are growing at a 12.66% CAGR to 2031, while sales and marketing analytics held 41.36% of the CRM Analytics market share in 2025.

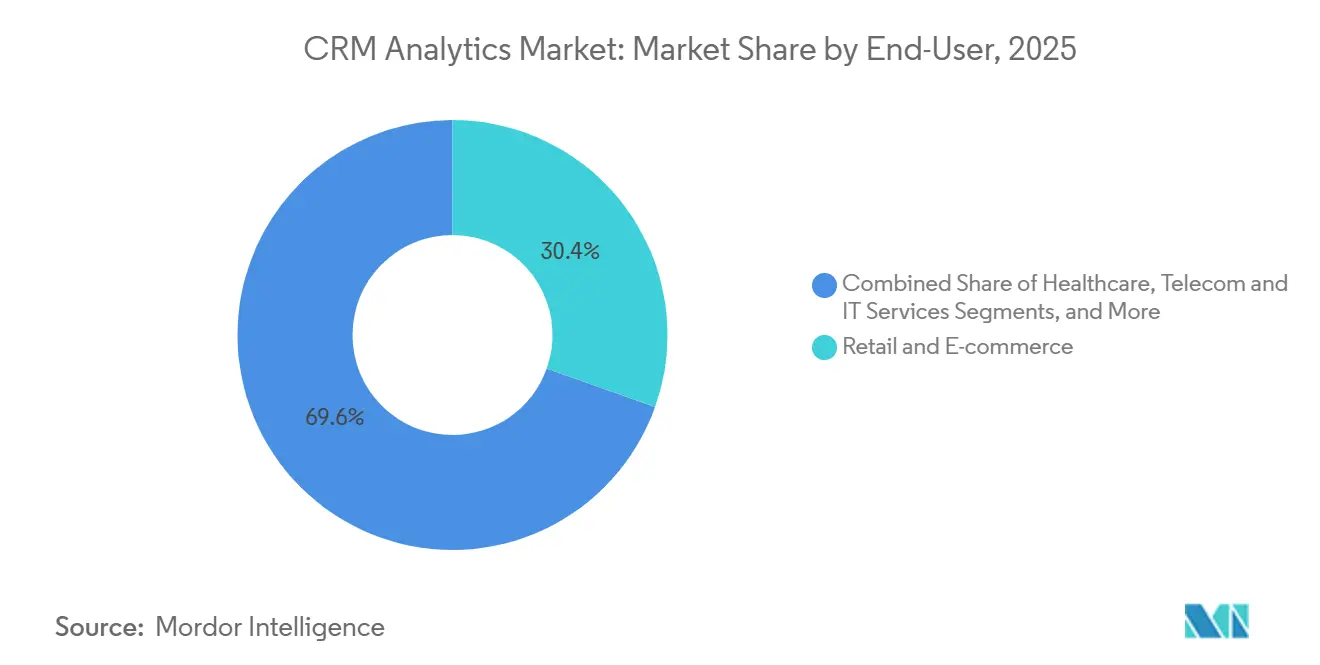

- By end-user, retail and e-commerce captured 30.44% revenue share in 2025; healthcare is forecast to expand at an 11.89% CAGR through 2031.

- By organization size, large enterprises accounted for 53.48% of the CRM Analytics market size in 2025, whereas SMEs are growing at a 12.12% CAGR to 2031.

- By geography, North America held 36.75% share in 2025, but Asia-Pacific is projected to grow at a 13.05% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CRM Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Cloud-based CRM Analytics | +2.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Demand for Hyper-personalised Customer Engagement | +2.3% | Global, particularly Retail and E-commerce verticals | Short term (≤ 2 years) |

| Rapid Integration of AI/ML for Predictive Insights | +2.6% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Real-time CDP-CRM Convergence | +1.9% | Global, with early adoption in BFSI and Telecom | Medium term (2-4 years) |

| Open Banking and Ecosystem APIs Unlocking New Ideas | +1.2% | Europe (PSD2), UK, Australia, emerging in APAC | Long term (≥ 4 years) |

| Privacy-preserving Analytics (Federated Learning) | +0.8% | Europe (GDPR), North America (CPRA), China (PIPL) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-based CRM Analytics

Cloud deployment removes capital expenditure, enables near-instant sandbox creation for A/B testing, and supports consumption pricing that aligns cost with usage, an approach 78% of Einstein Analytics seats adopted in 2025. Microsoft Dynamics integrates Azure Synapse and Azure Machine Learning to condense weeks of data-wrangling into days, while Oracle Fusion Cloud CX released per-prediction pricing that peaks only during holiday surges. Certified security frameworks such as ISO/IEC 27001 and SOC 2 Type II reduce audit burdens, further accelerating migration to cloud platforms.

Demand for Hyper-personalized Customer Engagement

Managed services such as Amazon Personalize have delivered 23% higher conversion rates in retail pilots by embedding collaborative filtering directly into checkout flows.[1]Amazon Web Services, “Amazon Personalize,” aws.amazon.com Shopify now adjusts product bundles in real time through event-driven propensity scoring, while Salesforce Interaction Studio triggers next-best-action recommendations within milliseconds of user clicks. The move from nightly batch segmentation to streaming micro-moments favors platforms that can ingest clickstreams, score intent, and deploy tailored content before a prospect abandons a session.

Rapid Integration of AI and ML for Predictive Insights

Salesforce Einstein GPT combines large language models with CRM data to predict deal closure dates at 87% accuracy and draft personalized outreach automatically. Microsoft Dynamics 365 Copilot uses GPT-4 to synthesize meeting notes and recommend cross-sells, while the NIST AI Risk Management Framework sets voluntary standards that vendors follow to expose feature importance, bias checks, and lineage metadata. In regulated banking and healthcare sectors, explainability is now a core procurement criterion.

Real-time CDP-CRM Convergence

Adobe Experience Platform streams 15 trillion events per month to fuel sub-second audience targeting, eliminating the 12- to 24-hour lag of batch exports. Salesforce Data Cloud merges identity resolution with analytics, enabling a single governance layer across marketing, sales, and service clouds. Convergence ensures consent preferences and retention rules apply uniformly, shrinking compliance burdens and closing the loop between prediction and intervention.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Integration Complexity Across Siloed Sources | -1.8% | Global, acute in enterprises with legacy on-premises systems | Short term (≤ 2 years) |

| Skill-set Shortages in Advanced Analytics | -1.3% | Global, most severe in APAC and emerging markets | Medium term (2-4 years) |

| Heightened Data-privacy Compliance Costs (GDPR/CPRA) | -1.5% | Europe, North America (California, Virginia, Colorado) | Medium term (2-4 years) |

| Algorithmic Bias and Model-governance Concerns | -0.9% | Global, particularly regulated sectors (BFSI, Healthcare) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Integration Complexity Across Siloed Sources

IBM reported that 42% of AI projects stalled in 2025 due to fragmented schemas and mismatched identifiers, forcing data engineers to spend 38% of their time troubleshooting connector failures.[2]IBM Institute for Business Value, “Data and AI Trends Report 2025,” ibm.com Legacy databases lack modern APIs, while SaaS tools impose proprietary rate limits. Change-data-capture streams must reconcile simultaneous updates across systems, extending project timelines by six weeks on average. Without unified identifiers, predictive accuracy degrades and total cost of ownership rises.

Heightened Data-privacy Compliance Costs (GDPR/CPRA)

PwC estimated that midsize firms incur USD 1.2 million to USD 2.8 million in annual compliance overhead to satisfy consent tracking and right-to-erasure workflows mandated by GDPR and CPRA. The UK ICO requires firms to prove models do not process special-category data without explicit permission, shrinking the feature sets available for churn prediction. California’s expanded sensitive-information categories further tighten requirements, compelling enterprises to integrate consent orchestration directly into analytics pipelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Social Listening Fuels Fastest Segment Expansion

Sales and marketing analytics held 41.36% of the CRM Analytics market share in 2025, underlining its role in pipeline forecasting and attribution reporting. However, social media and web analytics are advancing at a 12.66% CAGR, reflecting recognition that unstructured social sentiment predicts churn and product failures earlier than ticket volume. For example, social monitoring detected emerging issues 4.2 days sooner, reducing churn by 18%. Contact center analytics blends speech-to-text transcription and emotion detection to lower service costs, while customer analytics remains the backbone for lifetime-value modeling. Vendors now bundle these once-separate modules, as HubSpot’s Customer Platform unifies marketing, sales, and service analytics in a single interface.

The convergence simplifies user experience but demands platforms handle multimodal data at scale. Real-time text, voice, and video inputs require low-latency processing and elastic storage, capabilities delivered through cloud data lakes and stream engines. Regulatory frameworks such as the EU Digital Services Act drive adoption by mandating content-moderation transparency for platforms exceeding 45 million users. This spurs demand for advanced social listening metrics such as flagged-post tracking and appeal outcomes. The type segmentation gap will narrow as sales, service, and social insights merge into a unified analytical fabric.

By Deployment: Cloud Dominance Reflects Architectural Imperatives

Cloud deployments captured 63.84% of the CRM Analytics market in 2025 and are forecast to grow at a 13.35% CAGR through 2031. Elastic compute engines enable training of transformer-scale models and power real-time inference workloads. On-premises installations persist in finance and government but increasingly adopt hybrid designs. Oracle Fusion Cloud CX allows banks to store personal data on-premises Oracle Exadata while streaming anonymized telemetry to Oracle Cloud Infrastructure for modeling, resolving data-sovereignty mandates under China’s PIPL. Consumption-based pricing further tips economics in favor of cloud and reduces unused capacity endemic to on-premises data centers.

Hybrid clouds also streamline compliance. FedRAMP, ISO/IEC 27001, and SOC 2 Type II attestations shift audit responsibility from the customer to the vendor. Microsoft bills Dynamics 365 Customer Insights by the number of unified profiles, aligning cost with value. Salesforce Einstein Analytics Flex introduced per-query billing, enabling thousands of occasional users without per-seat fees. Security, elasticity, and economic viability jointly reinforce cloud supremacy in the deployment landscape.

By End-User: Healthcare’s Regulatory Tailwinds Drive Outperformance

Retail and e-commerce accounted for 30.44% share in 2025, leveraging analytics to minimize cart abandonment and optimize inventory. Healthcare, however, is projected to grow at 11.89% CAGR through 2031, buoyed by mandates like USCDI v4 that compel EHR vendors to expose patient engagement APIs. Epic Systems now feeds engagement data to Salesforce Health Cloud, enabling care coordinators to view adherence and outreach patterns in a single view. BFSI remains foundational, using analytics for credit scoring and fraud detection. Telecom predicts churn by correlating network quality with customer sentiment, as shown by Verizon’s 2025 integration with Nokia network analytics.

Transportation, logistics, and media apply analytics to freight matching and subscriber retention, respectively. SAP’s logistics data models track shipment milestones, while streaming services leverage recommendations to curb subscriber churn. Other verticals - manufacturing, energy, and professional services - adopt analytics for contract renewals and partner management, enabled by Microsoft Dynamics industry accelerators. Healthcare’s surge aligns with rising patient-experience benchmarks and reimbursement tied to engagement metrics.

By Organization Size: SMEs Close the Capability Gap

Large enterprises held 53.48% of the CRM Analytics market size in 2025. They deploy multi-tier architectures, integrate customer data platforms, and maintain in-house data science teams. SMEs are forecast to expand at 12.12% CAGR to 2031, supported by freemium tiers and automated model templates. HubSpot recorded 68% of new bookings from firms with fewer than 500 employees, a cohort that benefits from serverless inference and consumption billing. Zoho’s Zia assistant and Freshworks’ Freddy AI offer conversational interfaces and auto-generated insights without costly specialists.

Cloud vendors amortize training costs across thousands of tenants, lowering entry barriers. Salesforce Starter at USD 25 per user per month bundles predictive scoring once available only to enterprise customers. SMEs thus achieve pipeline forecasting and churn mitigation parity with enterprises, challenging incumbents that relied on scale-based advantages.

Geography Analysis

North America retained 36.75% of the CRM Analytics market in 2025, anchored by a dense ecosystem of platform vendors, hyperscale clouds, and early adopters in retail and financial services.[3]Salesforce Investor Relations, “Financials,” salesforce.com U.S. banks implement analytics to meet open-banking standards, while Canadian institutions align with the FCAC’s framework. Europe balances growth with GDPR compliance costs; vendors emphasize privacy-by-design to satisfy EDPB guidelines. Germany and France lead in manufacturing analytics, while the United Kingdom accelerates fintech experimentation supported by open-banking APIs.

Asia-Pacific is the fastest-growing region at 13.05% CAGR. India’s Digital Personal Data Protection Act triggers demand for consent orchestration, spurring hybrid cloud adoption. China enforces data-localization under PIPL, favoring domestic clouds such as Alibaba and Tencent. Japan migrates legacy on-premises deployments as Salesforce opens a third Tokyo data center, mitigating residency concerns. ASEAN markets embrace analytics to support digital banking and super-app ecosystems; Grab integrates ride-hailing, food delivery, and payments data into unified profiles.

South America faces macroeconomic volatility yet incrementally adopts cloud analytics through consumption pricing, led by Brazilian retailers digitizing loyalty programs. The Middle East aligns CRM analytics with Saudi Vision 2030 diversification mandates, deploying Salesforce and Dynamics to manage citizen services. Africa remains nascent but shows momentum in South Africa and Nigeria, where mobile-first architectures require real-time churn prediction and personalized top-ups. Zoho’s Johannesburg data center helps local enterprises comply with the Protection of Personal Information Act.

Competitive Landscape

The top four providers - Salesforce, Microsoft, Oracle, and SAP - hold roughly 55% of the CRM Analytics market, yet fragmentation persists because enterprises pursue best-of-breed stacks. Incumbents embed analytics into their native clouds, locking in customers via unified data models and consolidated billing. Salesforce’s integration of Tableau unlocked self-service visualization without data export. Microsoft bundles Power BI with Dynamics 365, enabling natural language queries within Teams workspaces.

Specialists thrive in white-space niches. Veeva Systems dominates life-sciences engagement by delivering HIPAA-compliant audit trails. Google Cloud leads commercialized federated-learning deployments, enabling cross-border modeling without centralizing raw data. Freshworks and HubSpot undercut incumbent pricing by 60–70%, attracting SMEs migrating from spreadsheets. NICE and Verint focus on contact-center analytics, offering speech emotion detection and workforce optimization unavailable in generalist suites. Strategic acquisitions continue to redraw the landscape, as Zendesk absorbs Tymeshift for workforce scheduling analytics.

Mergers and product launches intensify the arms race to embed large language models. Salesforce Einstein GPT for Service automates case summaries; Microsoft Copilot recalibrates pipeline forecasts based on external events. Oracle’s integration of Cerner analytics strengthens its healthcare position, while Adobe’s streaming CDP capability compresses activation latency to milliseconds. Competition centers on model governance, consumption pricing, and pre-built vertical templates that minimize time-to-value.

CRM Analytics Industry Leaders

Oracle Corporation

SAP SE

Microsoft Corporation

Salesforce Inc.

International Business Machines Corporation (IBM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Salesforce Einstein GPT for Service entered general availability, cutting response drafting time by 40% in pilot contact centers.

- September 2025: Microsoft expanded Dynamics 365 Copilot to deliver predictive pipeline forecasting using real-time external signals.

- August 2025: Oracle finalized its acquisition of Cerner analytics assets, integrating them into Oracle Health Cloud to target payer and provider workflows.

- July 2025: HubSpot launched Customer Platform, unifying analytics across marketing, sales, and service hubs in a single dashboard.

- June 2025: SAP introduced Industry Cloud for Retail, embedding pre-built analytics for inventory optimization and omnichannel attribution.

Global CRM Analytics Market Report Scope

The CRM Analytics Report is Segmented by Type (Sales and Marketing Analytics, Contact Center Analytics, Customer Analytics, and Social Media and Web Analytics), by Deployment (On-premise, and Cloud), End-User (BFSI, Healthcare, Retail and E-commerce, Telecom and IT Services, Transportation and Logistics, Media and Entertainment, and Other End-Users), by Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Sales and Marketing Analytics |

| Contact Center Analytics |

| Customer Analytics |

| Social Media and Web Analytics |

By Deployment

| On-premise |

| Cloud |

By End-User

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Retail and E-commerce |

| Telecom and IT Services |

| Transportation and Logistics |

| Media and Entertainment |

| Other End-Users |

By Organization Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Sales and Marketing Analytics | |

| Contact Center Analytics | ||

| Customer Analytics | ||

| Social Media and Web Analytics | ||

| By Deployment | On-premise | |

| Cloud | ||

| By End-User | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare | ||

| Retail and E-commerce | ||

| Telecom and IT Services | ||

| Transportation and Logistics | ||

| Media and Entertainment | ||

| Other End-Users | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the CRM Analytics market in 2031?

The market is projected to reach USD 20.65 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments are advancing at a 13.35% CAGR, driven by elastic compute and consumption pricing.

Why is healthcare the fastest-growing vertical?

Interoperability mandates such as USCDI v4 compel EHR vendors to expose engagement APIs, enabling advanced patient analytics and pushing healthcare growth to an 11.89% CAGR.

How are SMEs adopting advanced analytics?

Freemium tiers and no-code AutoML templates from vendors such as HubSpot and Zoho allow SMEs to deploy predictive lead scoring without in-house data scientists.

Which region is expected to grow most rapidly?

Asia-Pacific leads with a 13.05% CAGR, supported by data-privacy legislation in India and China that encourages hybrid cloud architectures.

What is the primary restraint on market expansion?

Data integration complexity across siloed systems reduces project velocity and inflates total cost of ownership.

Page last updated on: