Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

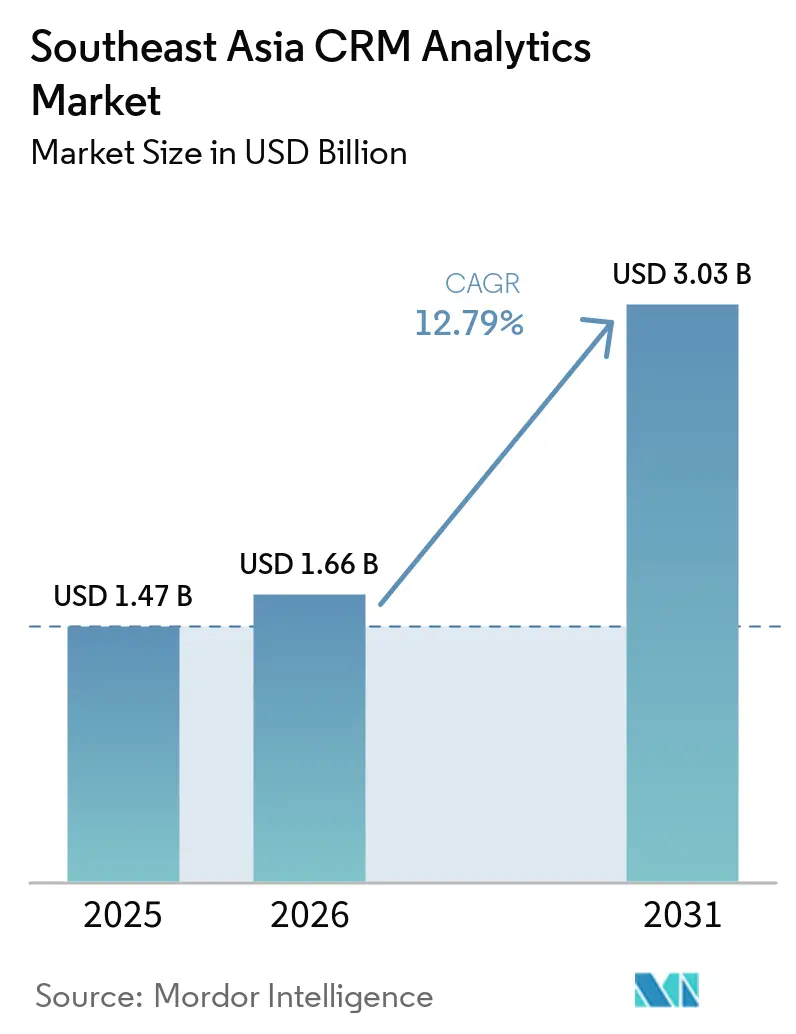

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

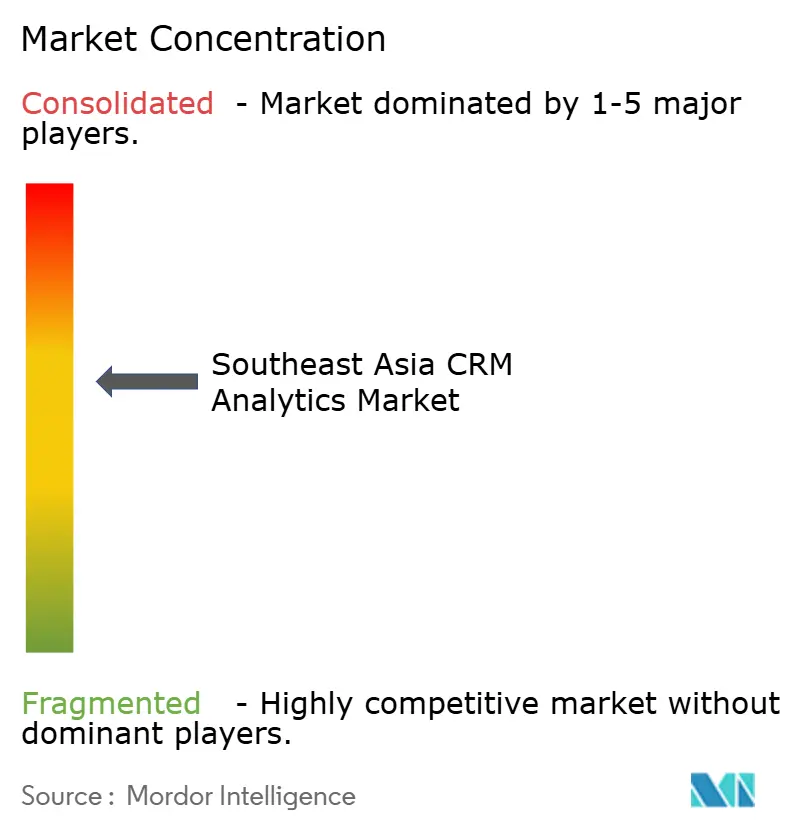

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia CRM Analytics Market Analysis by Mordor Intelligence

The Southeast Asia CRM analytics market size in 2026 is estimated at USD 1.66 billion, growing from 2025 value of USD 1.47 billion with 2031 projections showing USD 3.03 billion, growing at 12.79% CAGR over 2026-2031. Rising digital-first consumer habits, formal government digitalization programs, and the region’s cloud-first start-up culture underpin this momentum. Companies are prioritizing omnichannel data capture, real-time personalization, and AI-driven campaign optimization to protect margins amid fierce online competition. Public-sector platforms such as Indonesia’s INA Digital and Singapore’s SMEs Go Digital initiative normalize advanced data practices, accelerating private-sector demand. At the same time, local vendors are using multilingual NLP, localized data connectors, and subscription pricing to address the needs of 70 million regional SMEs, steadily eroding the historical dominance of global mega-suites.

Key Report Takeaways

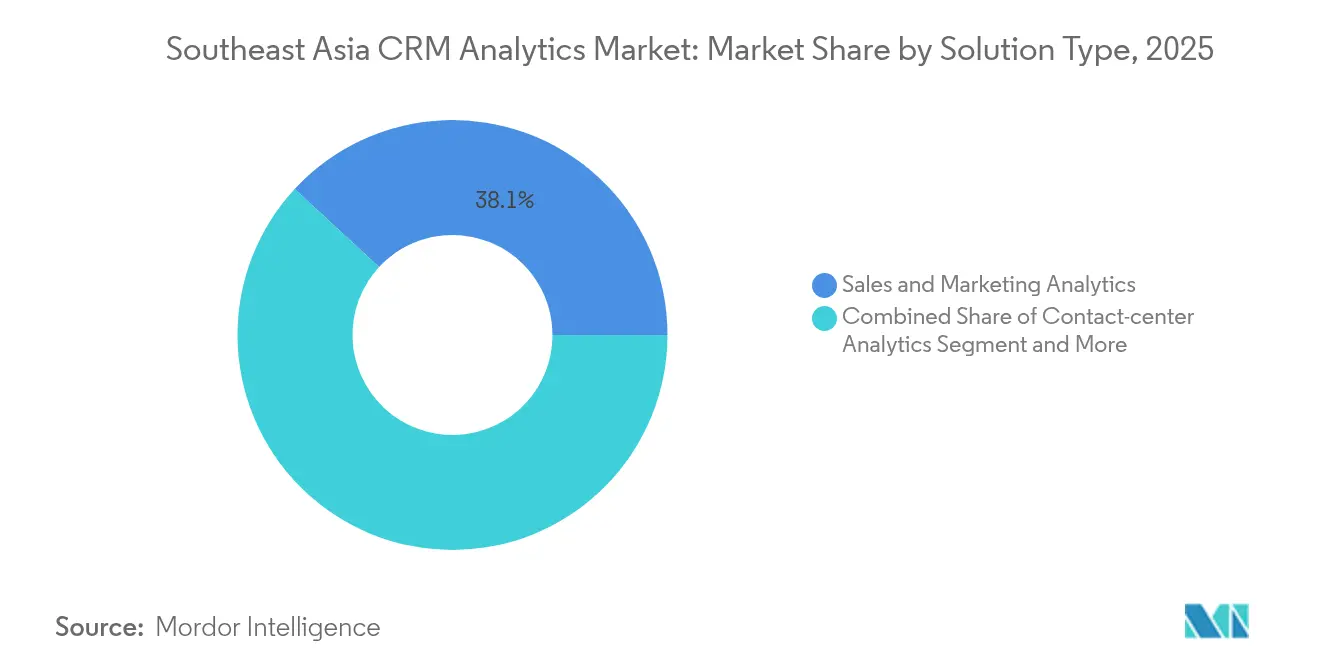

- By solution type, sales and marketing analytics led with 38.12% of the Southeast Asia CRM analytics market share in 2025, while Social-Media/Web and Sentiment Analytics is projected to expand at an 18.06% CAGR through 2031.

- By deployment model, cloud captured 70.93% revenue in 2025; moreover, the cloud segment is poised to grow at a CAGR of 17.12% over the forecast period.

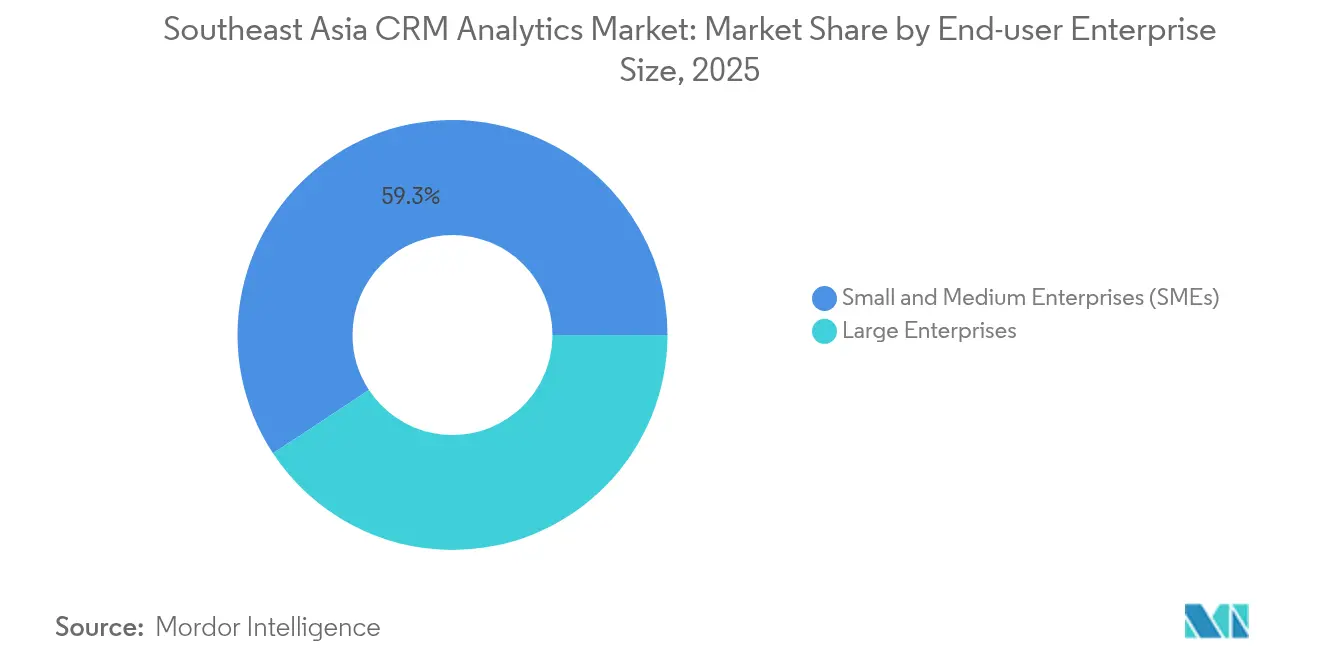

- By end-user enterprise size, SMEs accounted for 59.27% of 2025 spending, while it is also expected to grow at a 16.85% CAGR through 2031 over the forecast period.

- By end-user industry, retail and e-commerce commanded 25.94% revenue in 2025; healthcare is accelerating at a 16.12% CAGR to 2031 as telemedicine platforms integrate electronic medical record data with real-time engagement tools.

- By country, Indonesia held 23.55% of 2025 revenue, whereas Vietnam is poised for a 18.76% CAGR through 2031 due to aggressive national AI roadmaps and semiconductor investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia CRM Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitalisation and omnichannel retail expansion | +2.8% | Indonesia and Vietnam | Medium term (2-4 years) |

| Growing e-commerce and mobile commerce volume | +2.1% | Indonesia, Thailand, Singapore | Short term (≤ 2 years) |

| Rising adoption of cloud-based SaaS CRM among SMBs | +1.9% | Singapore, Malaysia, Vietnam | Medium term (2-4 years) |

| Government-backed SME digital-voucher programs | +1.6% | Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Integration of conversational commerce via super-apps | +1.6% | Indonesia, Singapore, Malaysia | Long term (≥ 4 years) |

| FinTech-driven alternative data enrichment for CRM | +1.2% | Philippines, Vietnam, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitalisation and Omnichannel Retail Expansion

National e-government projects standardize data pipelines that enterprises can extend for commercial use, fundamentally raising expectations for real-time customer insights. Thailand’s Central Pattana leverages its “The 1” loyalty program across more than 200 planned mixed-use developments, pushing transaction, footfall, and engagement data into a single analytics layer that marketing teams query in seconds.[1]Central Pattana. "20240308-cpn-one-report-2023-en-v06." July 5, 2024. Regional e-commerce leaders keep enhancing first-party data depth; Shopee maintains a 48% share while TikTok Shop surged to 14.2% in under twelve months, compelling retailers to refine sentiment tracking beyond conversion logs.[2]KrASIA. "TikTok Shop's GMV soared in 2023, putting Shopee and Lazada on edge." July 19, 2024 Retailers now fuse store traffic sensors, social-commerce feeds, and logistics events, which expands input variables for propensity scoring models. The result is a sustained preference for customer-journey visualizers, sales forecasting engines, and attribution dashboards delivered as SaaS accelerators. Vendors with pre-built connectors to point-of-sale, marketplace, and social-video APIs are securing multi-year contracts that bundle analytics with customer-data-platform functionality.

Growing E-commerce and Mobile Commerce Volume

Southeast Asia’s digital economy cleared USD 100 billion in 2023 and continues to climb on a mobile-first trajectory. In Indonesia, 7.4 million shoppers transact online daily, posting timestamped events that feed real-time recommendation engines. Travel marketplace Wego illustrates data monetization potential, lifting daily unique conversions to 27,000 by embedding predictive content blocks that drove a 20X jump in e-mail open rates and a 28% lift in purchase conversions during peak seasons.[3]Zawya. "27K unique conversions every day: Here's how travel brand Wego achieved a remarkable feat." October 4, 2022 Because third-party cookies are fading, marketers double down on CRM suites that stitch transaction, engagement, and social-graph attributes into unified identities. Payment-time insights such as basket abandonment, coupon usage, and delivery-slot selection flow into look-alike modeling pools, sharpening cross-sell algorithms. The regional surge in buy-now-pay-later adoption further enriches alternative credit scoring data that CRM engines use to personalize financing offers.

Rising Adoption of Cloud-based SaaS CRM Among SMBs

Singapore’s SMEs Go Digital program subsidizes more than 450 accredited solutions and reports 85% efficiency gains among participants, effectively lowering proof-of-concept barriers for predictive-analytics modules. Indonesian micro-business polls show 93% awareness of cloud benefits, yet actual penetration trails at below 30%, highlighting a vast untapped user base. Solution providers now bundle AI chatbots, lead-scoring algorithms, and omnichannel dashboards into starter tiers priced under USD 50 per seat. Advocado’s partnership with Huawei Cloud and 4Paradigm AI delivers sentiment detection, voucher orchestration, and churn early-warning features to café chains in hours instead of weeks. Barantum clients report 90% productivity gains and 85% faster service resolution, validating the ROI narrative for cloud CRM among resource-constrained firms. As public-cloud latency falls below 20 milliseconds in major metros, edge decision nodes process on-premise sensor data while synchronizing enriched profiles to regional data centers overnight.

Government-backed SME Digital-voucher Programs

Targeted grants and tax incentives neutralize upfront licensing costs, a major hurdle for the 70 million small businesses that anchor Southeast Asian economies. Singapore’s Productivity Solutions Grant reimburses up to 70% of approved CRM software expenses and includes a Chief Technology Officer-as-a-Service advisory layer that guides workflow redesign. Malaysia’s Digital Financing Initiative extends credit lines dedicated to digital tools, shrinking payback periods for analytics projects committed to revenue uplift or cost avoidance. Structured Industry Digital Plans provide sector-specific blueprints that align CRM analytics deployment sequences with manpower competency training, minimizing change-management friction. Early adopters cite reductions in manual order processing and paper-based account ledgers, freeing staff to focus on consultative selling and loyalty-program management. The virtuous cycle of more adopters generating richer benchmark datasets further sharpens predictive models available to new entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and localisation law fragmentation | -1.8% | Malaysia, Vietnam | Medium term (2-4 years) |

| Analytics and data-science talent shortage | -2.1% | Thailand, Vietnam | Long term (≥ 4 years) |

| High churn in SME customer contracts | -1.4% | Indonesia, Philippines | Short term (≤ 2 years) |

| Super-app ecosystem limits first-party data ownership | -1.6% | Indonesia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and Localisation Law Fragmentation

Indonesia’s Personal Data Protection Law mandates explicit consent rules and local storage commitments by October 2024, forcing CRM vendors to spin up Jakarta-based clusters and overhaul consent-management workflows. Vietnam and Malaysia add differing cross-border transfer thresholds, raising architecture complexity for multi-country rollouts. Financial-services and health-tech buyers impose extra encryption and audit-logging layers, elongating procurement cycles. Because regional harmonization is slow, product roadmaps now include country-selectable data-residency toggles and modular compliance widgets. Budget-strapped SMEs struggle to keep policies current, occasionally stalling renewal discussions until turnkey compliance packages appear.

Analytics and Data-science Talent Shortage

Thailand counts only 300–400 formally trained data scientists, while the wider Asia-Pacific shortfall tops 1 million positions. Vietnam’s AI Academy warns that enrollment rates in applied ML programs lag employer demand, despite national pledges to train 5,000 AI engineers. Scarce specialists drive salary inflation above 25% year over year, widening affordability gaps for SMEs. Outsourcing to India or Eastern Europe helps, yet time-zone misalignment slows agile iteration on localized models. Governments respond with bootcamps and scholarship incentives, but meaningful workforce expansion will require curriculum overhauls and stronger university-industry partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Sales Analytics Maintains Scale While Sentiment Tools Accelerate

Sales and Marketing Analytics accounted for 38.12% of the Southeast Asia CRM analytics market size in 2025, reflecting its direct tie to pipeline velocity and deal closure. Retailers and marketplace sellers deploy win-rate visualizers and discount-elasticity models that parse millions of SKU-level events each night. The sub-segment matures as marketers shift from open-rate vanity metrics to lifetime-value optimization, forcing vendors to expand attribution grids and AI-generated content recommendations.

Social-Media/Web and Sentiment Analytics is projected to clock an 18.06% CAGR, moving from niche listening dashboards to core revenue-influencing pipelines. TikTok Shop’s rapid GMV climb re-emphasizes the need for language-agnostic emotion classifiers that capture informal slang, emojis, and mixed scripts. Providers like Wisesight deliver Thai-script tokenization and regional meme mapping, differentiating on culturally nuanced taxonomies. As a result, procurement teams allocate bigger budgets to sentiment layers that feed risk-trigger alerts into enterprise customer-data platforms, setting the stage for suite-level upsells.

By Deployment Model: Cloud First Becomes Cloud Norm

Cloud models generated 70.93% of 2025 billings, translating into USD 1.04 billion of the Southeast Asia CRM analytics market size. Rapid Kubernetes adoption, liberal peering policies, and sub-50-millisecond round-trip times across major ASEAN internet exchanges dissolve latency objections. New Singapore data centers featuring NVIDIA GH200 Grace Hopper superchips promise local inference of billion-parameter LLMs without rerouting data to the United States. Global ISVs now default to SaaS delivery and offer on-premise connectors only for regulated workloads.

On-premise demand is likely to settle below 10% of the Southeast Asia CRM analytics market by 2031 as regulators gradually certify sovereign-cloud designs. Hybrid remains a bridge option for telcos and banks that host core ledger systems on proprietary hardware. Vendors respond with split-compute architectures where identity resolution happens in private-cloud nodes while model training runs in shared GPU pools overnight.

By Enterprise Size: SME Momentum Dominates Volume

SMEs formed 59.27% of total spending in 2025, roughly USD 0.87 billion of the Southeast Asia CRM analytics market size, as subsidized bundles and no-code interfaces eliminated technical hurdles. Merchants deploy template playbooks for cart-abandonment mails, WhatsApp loyalty campaigns, and AI chat deflection in under a week. Because subscription churn plagues this tier, vendors integrate usage-nudging widgets and payment-failure retries, slashing logo attrition by up to 15 points.

Large enterprises still dictate roadmap innovation. Telkomsel’s Veronika voice agent doubled self-service adoption and pushed daily message volumes beyond 3 million, stress-testing intent-classification pipelines. Lessons learned cascade into SME editions as simplified AI co-pilots that suggest reply snippets and next-best-offer cards, ensuring continuous feature parity.

By End-user Industry: Retail Leads, Healthcare Surges

Retail and e-commerce captured 25.94% revenue in 2025, equal to USD 0.38 billion of Southeast Asia CRM analytics market share thanks to deep SKU catalogs, high transaction cadence, and abundant coupon data. Dynamic bundle engines, price-elasticity simulations, and dark-store fulfillment insights sit atop clickstream and inventory ledgers, enabling 15–20% average basket uplift according to vendor benchmarks.

Healthcare is pacing at a 16.12% CAGR. Digital-health platforms ingest triage chat logs, remote-patient-monitor readings, and insurance claim codes into pattern-discovery models that flag abandonment risk or medication-adherence anomalies. Hospitals integrate CRM screens within electronic medical record viewers, exposing unified contexts to front-desk agents who can schedule follow-ups based on predictive no-show probabilities. Regulatory push for value-based care further anchors analytics budgets despite fiscal constraints.

Geography Analysis

Indonesia retains market leadership by pairing population scale with coordinated digital-service rollouts. INA Digital integrates nine public services, prompting private brands to comply with unified citizen-ID structures that simplify data matching. Telkomsel’s 50 TB daily feed funnels into Cloudera clusters that realize USD 665,000 cost savings per year and provide templates for cross-industry deployments. The Personal Data Protection Law catalyzes demand for data-governance toolkits embedded inside CRM suites, turning compliance into a purchasing trigger.

Singapore’s influence extends beyond domestic revenues. The city-state operates as a testbed where global providers refine regional language packs, AI-safety features, and sovereign-cloud routing before scaling into neighboring countries. Salesforce’s five-year USD 1 billion investment, coupled with an AI partnership with Singapore Airlines, underlines the virtuous cycle of enterprise innovation and public-sector collaboration. SMEs Go Digital shows that structured voucher systems can push adoption rates from concept to live use within three months, offering a replicable blueprint for ASEAN peers.

Vietnam’s acceleration stems from industrial policy that designates AI and semiconductor fabrication as dual growth engines. FPT’s AI Factory and planned hyperscale data centers address both local demand and export-service ambitions, positioning the country to leapfrog legacy CRM deployments with modern, GPU-accelerated designs. Healthcare providers pilot predictive triage and appointment clustering tools, while e-commerce newcomers harness sentiment classifiers tuned to dialectal Vietnamese. The Philippines, Malaysia, and Thailand show steady mid-teen growth, while Cambodia, Laos, and Myanmar form a long-tail opportunity once telecom backbone investments reach maturity.

Competitive Landscape

Global suites such as Salesforce, Microsoft Dynamics 365, and Oracle Fusion remain dominant in multinational accounts, yet local specialists increasingly win mid-market deals through localized UX and modular pricing. Salesforce’s USD 1 billion Singapore outlay secures data residency, AI model tuning, and workforce skilling commitments that reassure regulated buyers. Microsoft’s Azure OpenAI Service powers Telkomsel’s Veronika chatbot, demonstrating how hyperscalers embed generative AI inside telecom-grade environments.

Regional challengers follow a land-and-expand playbook. Barantum leverages Bahasa interfaces and WhatsApp Business APIs to deliver 90% productivity gains and 40% churn reduction for Indonesian SMEs. Qontak and Freshworks target omnichannel inbox unification, while Wisesight differentiates on Thai sentiment lexicons. Merger speculation around Grab and GoTo, with a rumored USD 7 billion valuation, signals an impending shift where super-apps internalize CRM stacks to monetize cross-business datasets.

Technology roadmaps tilt toward autonomous-workflow orchestration. ServiceNow’s AI-powered CRM platform reportedly amassed USD 1.4 billion annual contract value, growing 30% year on year through embedded agents that predict ticket deflection and SLA breaches. Vendors able to harmonize data-protection controls across Indonesia, Vietnam, and Malaysia enjoy a structural edge, because compliance costs deter smaller entrants. Over the medium term, consolidation will likely compress the field to a dozen full-suite providers supplemented by vertical specialists for healthcare, logistics, and media.

Southeast Asia CRM Analytics Industry Leaders

-

Salesforce.com Inc.

-

Oracle Corporation Malaysia Sdn Bhd

-

Microsoft Services Asia

-

AquaCRM (Thailand) Co. Ltd

-

Peppercan (Safecoms.com)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Salesforce announced a USD 1 billion investment in Singapore over five years to accelerate AI platform development and secure local data residency for Agentforce

- February 2025: Ernst & Young Digital Solutions acquired PT Kreatif Dinamika Integrasi to create a Southeast Asia Center of Excellence for ERP and CRM cloud migration

- February 2025: Grab began exploratory talks to acquire GoTo in a USD 7 billion deal aimed at building the region’s most comprehensive super-app data platform

- February 2025: Singtel partnered with NVIDIA to build AI-ready data centers in Singapore, Indonesia, and Thailand, with first availability in early 2026

- January 2025: FPT Corporation unveiled eight national digital-transformation priorities, including AI talent development and multi-petabyte data-center construction

Southeast Asia CRM Analytics Market Report Scope

CRM analytics is an application assessing an organization's customer data to facilitate and streamline business choices. CRM analytical solutions use various applications that help measure the usefulness of customer-related processes and eventually provide customer categorization, such as profitability analysis, event monitoring, what-if scenarios, and predictive modeling. The countries considered under the scope of the Southeast Asian region include Malaysia, Thailand, Indonesia, Singapore, and Vietnam.

The Southeast Asian CRM analytics market is segmented by Type (Sales and Marketing Analytics, Contact Center Analytics, Customer Analytics, and Other Types), Deployment (On-premises, Cloud), End-User (BFSI, Health Care, Retail, Telecom, and IT, Transportation and Logistics, Media, and Entertainment, and Other End-Users), and Country (Malaysia, Singapore, Thailand, Indonesia, Vietnam and Rest of Southeast Asia.

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Solution Type

| Sales and Marketing Analytics |

| Contact-Centre Analytics |

| Customer and Journey Analytics |

| Social-Media/Web and Sentiment Analytics |

| Other Solution Type (Loyalty, Location) |

By Deployment Model

| Cloud |

| On-premises |

| Hybrid |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

By End-user Industry

| BFSI |

| Retail and E-commerce |

| Telecom and IT Services |

| Healthcare |

| Logistics and Transportation |

| Travel and Hospitality |

| Media and Entertainment |

| Other End-user Industry (Education, Transportation) |

By Country

| Indonesia |

| Singapore |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Southeast Asia (Cambodia, Laos, Myanmar, Brunei) |

| By Solution Type | Sales and Marketing Analytics |

| Contact-Centre Analytics | |

| Customer and Journey Analytics | |

| Social-Media/Web and Sentiment Analytics | |

| Other Solution Type (Loyalty, Location) | |

| By Deployment Model | Cloud |

| On-premises | |

| Hybrid | |

| By End-user Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By End-user Industry | BFSI |

| Retail and E-commerce | |

| Telecom and IT Services | |

| Healthcare | |

| Logistics and Transportation | |

| Travel and Hospitality | |

| Media and Entertainment | |

| Other End-user Industry (Education, Transportation) | |

| By Country | Indonesia |

| Singapore | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Southeast Asia (Cambodia, Laos, Myanmar, Brunei) |

Key Questions Answered in the Report

How large is the Southeast Asia CRM analytics market in 2026?

The market stands at USD 1.66 billion in 2026 and is projected to grow to USD 3.03 billion by 2031 at a 12.79% CAGR.

Which solution type holds the biggest revenue share?

Sales and Marketing Analytics leads with 38.12% revenue share in 2025, reflecting its direct impact on pipeline and conversion performance.

Why are SMEs the dominant buyers of analytics platforms?

Subsidized voucher schemes and low-cost cloud subscriptions make advanced CRM functions affordable, so SMEs account for 59.27% of 2025 spending.

What drives Vietnam’s exceptional growth rate?

Aggressive national AI strategies and FPT’s semiconductor investments fuel a 18.76% CAGR, the fastest across the region.

How are data-privacy laws affecting deployments?

Divergent localization rules in Indonesia, Malaysia, and Vietnam force vendors to add country-specific data-residency and consent modules, increasing implementation complexity.

Which industry vertical is growing the fastest?

Healthcare registers a 16.12% CAGR as telehealth and electronic medical record initiatives generate new analytics demand.

Page last updated on: