Thai Cuisine Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

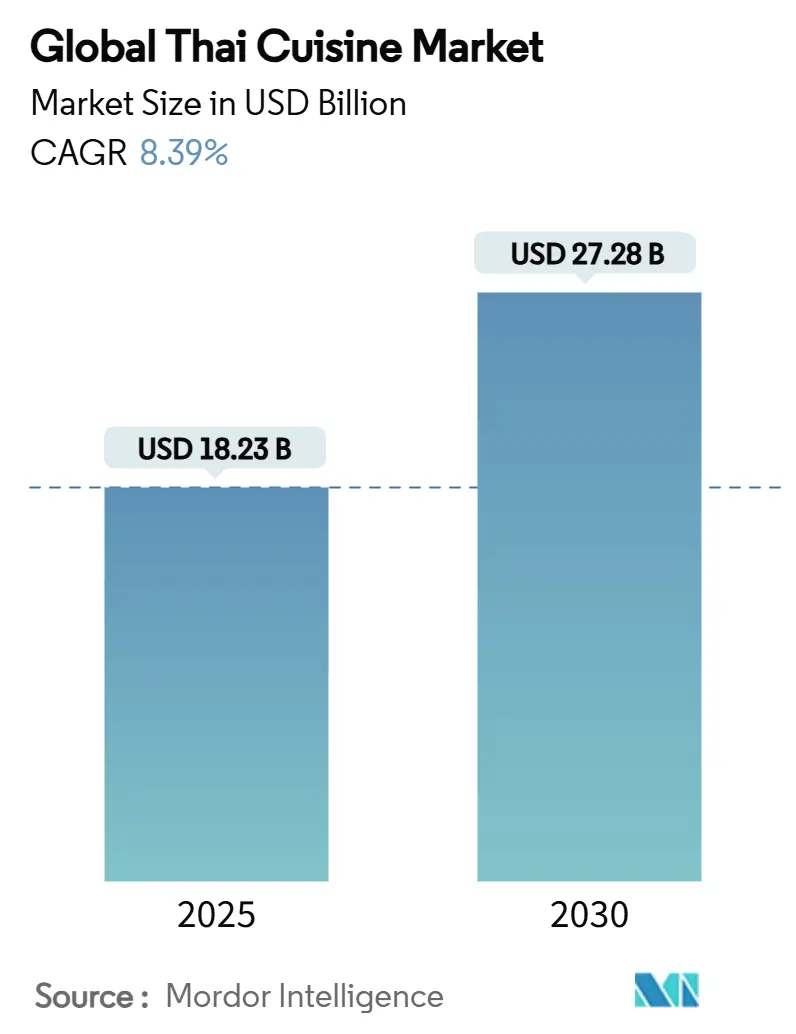

| Market Size (2025) | USD 18.23 Billion |

| Market Size (2030) | USD 27.28 Billion |

| Growth Rate (2025 - 2030) | 8.39% CAGR |

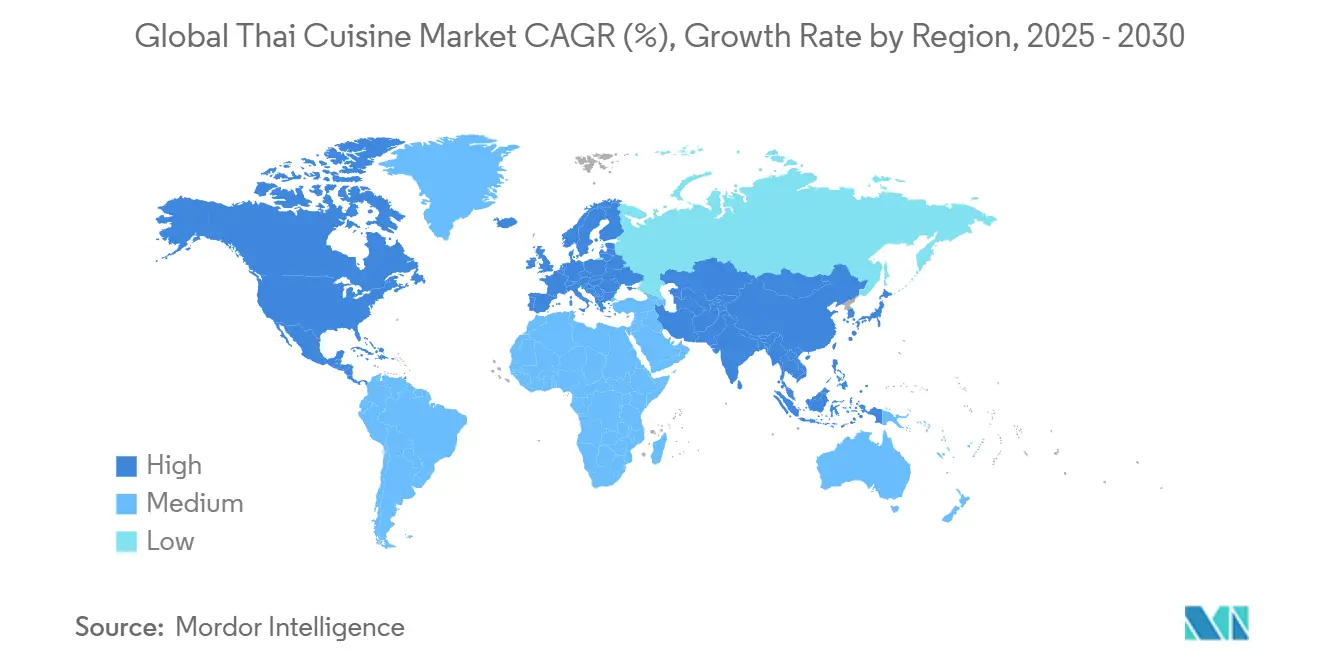

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thai Cuisine Market Analysis by Mordor Intelligence

The global Thai cuisine market size reached USD 18.23 billion in 2025 and is expected to grow to USD 27.28 billion by 2030, at a CAGR of 8.39% during the forecast period 2025-2030. The market growth is driven by increasing consumer demand for authentic Asian flavors, Thailand's gastrodiplomacy initiatives, and growing preferences for plant-based options across retail and food-service segments. While the Asia-Pacific region maintains market dominance due to established supply chains and cultural familiarity, North America shows the highest growth rate, primarily due to younger consumers' attraction to Thai flavor profiles. The market expansion is supported by improved cold-chain infrastructure using AI technology, which has reduced food waste in ready meals and frozen products. Market participants are implementing sustainability initiatives, including recyclable packaging and renewable energy in processing facilities, to comply with regulatory requirements in developed markets.

Key Report Takeaways

- By product type, Sauces, Pastes and Condiments led with 33.43% of Thai cuisine market share in 2024, whereas Ready Meals and Curries are projected to expand at a 9.64% CAGR through 2030.

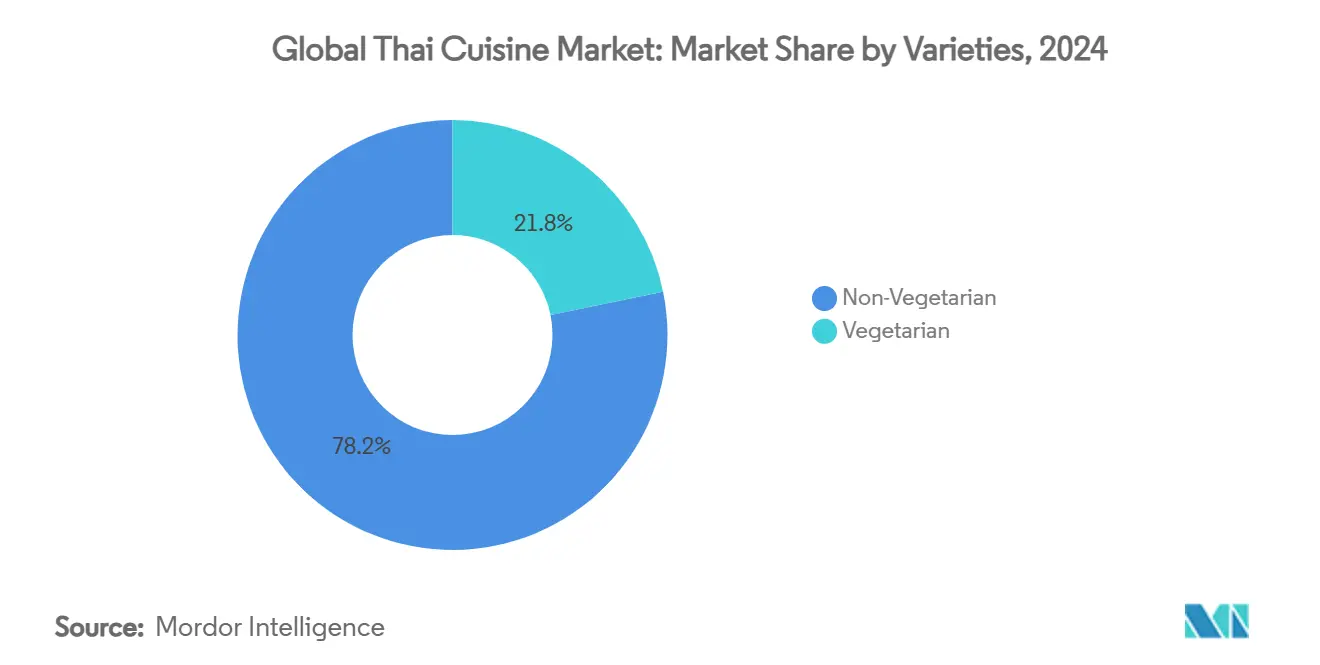

- By varieties, Non-Vegetarian offerings commanded 78.22% share of the Thai cuisine market size in 2024, while the Vegetarian segment is advancing at a 9.68% CAGR to 2030.

- By form, Shelf-Stable Ambient items captured 42.12% share in 2024, yet the Frozen segment is set to grow at 9.47% CAGR between 2025-2030.

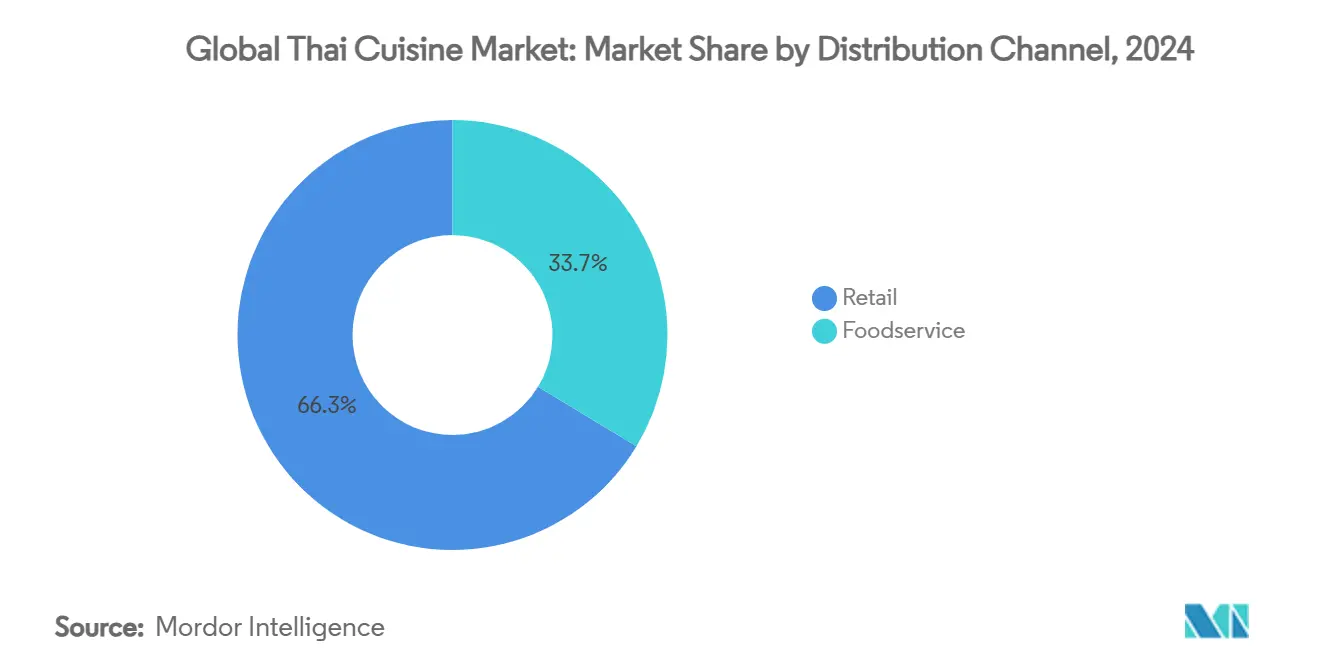

- By distribution channel, Retail held 66.34% Thai cuisine market share in 2024 and is expected to post a 9.77% CAGR through 2030, underpinned by E-commerce accounting for 31% of Thailand’s digital transactions.

- By geography, Asia-Pacific secured 42.88% share in 2024, whereas North America will rise at a 9.64% CAGR over 2025-2030 as Thai restaurant counts and Asian demographic growth accelerate.

Global Thai Cuisine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global interest in exotic cuisines | +1.8% | North America & Europe | Medium term (2-4 years) |

| Demand for authentic culinary experiences | +1.5% | Urban centers worldwide | Long term (≥ 4 years) |

| Popularity of plant-based diets | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Thai culture through media | +0.9% | Global with strength in APAC | Short term (≤ 2 years) |

| Access to authentic Thai ingredients | +0.8% | Developed markets | Long term (≥ 4 years) |

| Advances in packaging & preservation | +0.7% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Interest in International and Exotic Cuisines

The global demand for diverse culinary experiences continues to influence restaurant menus and retail product offerings, with Thai cuisine playing an important role in this transformation. McCormick's expansion of its crushed pepper portfolio in May 2025 through the introduction of Thai Style Chili reflects how major spice manufacturers are responding to consumer demand for authentic global flavors. This trend extends beyond traditional Thai food markets, as US consumers show increasing interest in Thai dishes, particularly those featuring spicy and sweet flavor combinations. The European market shows similar growth, with preserved chili imports increasing 4-5% annually in volume and 7-8% in value, driven by consumer demand for spicy and exotic flavors. The Netherlands serves as a key trade hub, recording significant growth in imports from Thailand as European consumers seek the distinct heat profiles characteristic of Thai cuisine.[1]Source: Confederation of British Industry, “European market potential for preserved chillies,” cbi.eu.

Rising Demand for Authentic Culinary Experiences

The global Thai food market is experiencing a significant transformation as consumers increasingly seek authentic, restaurant-quality experiences beyond basic Thai offerings in both retail and foodservice channels. The Thai SELECT certification program has established a strong presence with 1,377 certified locations spanning 70 countries, while Thai World Group has invested PHP 1 billion in a Philippines-based coconut processing facility with a 78,000-ton annual capacity for ultra-high temperature coconut milk, serving markets in Thailand, Europe, and the United States [2]Source: US-ASEAN Business Council, Inc., “Thailand’s Soft Power for the Creative Economy,” usasean.org. Minor Food has successfully expanded its authentic Thai cuisine footprint to over 2,400 outlets across 23 countries through its Thai Express and Patara Fine Thai Cuisine brands. This market evolution has prompted companies to strengthen their quality assurance mechanisms, develop international production capabilities, and implement vertical integration strategies to maintain flavor integrity. Minor Food's establishment of a dedicated culinary institute for promoting Thai cuisine globally represents a strategic shift in approaching authenticity as a systematic, scalable business asset rather than solely relying on inherent cultural advantages.

Growing Popularity of Plant-Based and Vegetarian Diets

The convergence of health-conscious consumer behavior and heightened environmental awareness is creating significant opportunities for innovations in plant-based Thai cuisine. European markets are experiencing similar momentum, with consumers actively seeking natural food additives driven by their preferences for clean-label products and increasing consumption of ethnic foods, particularly Thai cuisine. While the industry shows promising growth, manufacturers face the ongoing challenge of price competitiveness, as plant-based alternatives generally command higher price points compared to conventional meat products. This necessitates continuous improvements in production efficiency and compelling value propositions for consumers. The market dynamics are especially notable in developed regions where strong environmental consciousness aligns with sufficient disposable income levels, enabling consumers to embrace and sustain the purchase of premium plant-based options.

Influence of Thai Culture Through Media

Thailand's strategic implementation of cultural diplomacy through its culinary heritage has successfully expanded market opportunities beyond traditional tourism-driven consumption patterns. The country's Global Thai program has effectively leveraged Thai cuisine as a soft power instrument, with its influence permeating digital channels and contributing to the growth of Thailand's e-commerce marketplace. The government's ambitious 'One Community, One Thai Delicacy Chef' initiative, which targets the training of 70,000 chefs nationwide in 2024, exemplifies a methodical approach to cultural transmission for commercial benefits. The increasing popularity of hyperlocal dining experiences, combined with the seamless integration of Asian flavors into Western culinary traditions, has created pathways for Thai culinary elements to penetrate mainstream food culture beyond the confines of traditional Thai restaurants. This comprehensive influence manifests across various market segments, ranging from premium culinary tourism experiences to accessible convenience store offerings, thereby generating sustained consumer demand across diverse price points and consumption scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict food safety and import regulations | -1.4% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Dependence on fresh herbs and perishables | -1.1% | Global, with greater impact in markets distant from Thailand | Medium term (2-4 years) |

| Dietary restrictions and allergens | -0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Fluctuations in global tourism | -0.6% | Asia-Pacific and tourist-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Food Safety and Import Regulations

Thailand's intricate regulatory framework poses substantial challenges for new market entrants while providing a competitive advantage to established companies that have already invested in comprehensive compliance systems. The implementation of revised food additive regulations under Notification No. 444 B.E. 2566 requires manufacturers and importers to adapt their operations within a two-year timeframe, necessitating the removal of certain additives and adjustments to permitted usage across various food categories. In a significant expansion of its regulatory authority, the Thai FDA now mandates Good Manufacturing Practice (GMP) certification across all food products, departing from its previous category-specific approach. Additionally, the Thai Industrial Standards Institute oversees 129 mandatory product certifications spanning multiple sectors, with food safety certifications aligned with international standards. These extensive regulatory requirements generate considerable compliance costs, placing a disproportionate burden on smaller producers, particularly affecting traditional Thai food manufacturers whose authentic ingredients and time-honored production methods often struggle to align with modern industrial standards.

Dependence on Fresh Herbs and Perishables

The Thai food industry's dependence on fresh ingredients creates supply chain vulnerabilities that limit global market expansion and increase operational complexity. Thailand's rice production faces a decline through 2024 due to El Niño conditions, with recovery anticipated in 2025-2026, demonstrating the climate-related risks to essential ingredients. High production costs in the rice supply chain affect small and medium enterprises (SMEs), creating pricing pressures throughout Thai cuisine manufacturing. The projected decline in palm oil production by 2027, attributed to El Niño, indicates recurring supply constraints for coconut milk and curry paste production. Essential herbs such as Thai basil, lemongrass, and galangal present significant challenges due to their rapid flavor degradation and limited shelf life, even with optimal storage. Alternative meat products in Thailand face both perishability issues and price competitiveness challenges, as plant-based options generally exceed the cost of traditional ingredients, restricting their adoption in price-sensitive markets. These fresh ingredient requirements limit the geographic distribution of authentic Thai cuisine products while increasing operational expenses through specialized storage and transportation needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Varieties: Vegetarian Segment Accelerates

The vegetarian segment demonstrates robust growth potential with a projected CAGR of 9.68% during 2025-2030, reflecting evolving consumer preferences toward plant-based alternatives. This growth trajectory is particularly notable when compared to the non-vegetarian segment, which currently maintains a substantial market share of 78.22% in 2024. Thai Union's strategic entry into the plant-based market through its OMG Meat brand has garnered positive consumer response, particularly in the plant-based seafood alternatives category, indicating increasing market acceptance of vegetarian Thai cuisine options.

European markets have emerged as key drivers of vegetarian demand, with consumers increasingly gravitating toward ethnic food offerings and products with clean-label credentials. Natural food additives have become instrumental in plant-based formulations, serving multiple functional purposes while meeting consumer expectations for clean ingredients. Despite the non-vegetarian segment's continued market leadership through traditional Thai protein dishes, manufacturers face mounting operational challenges, including escalating ingredient costs and increasingly complex supply chain management requirements.

By Form: Frozen Innovation Drives Growth

The frozen segment demonstrates robust growth potential, with projections indicating a 9.47% CAGR during 2025-2030. This growth trajectory runs parallel to the shelf-stable ambient products segment, which commands a substantial 42.12% market share in 2024. The market evolution reflects significant advancements in food preservation technologies and responds to the increasing consumer demand for convenient meal solutions. The integration of sophisticated cold chain technologies, powered by artificial intelligence and machine learning algorithms for capacity planning, has delivered remarkable results. These technological implementations have successfully reduced food wastage by 76% while generating a tenfold increase in supplier profitability, making it commercially viable to distribute frozen Thai cuisine across geographically distant markets.

The fresh/chilled segment exhibits positive momentum through enhanced supply chain efficiencies, although natural product perishability continues to present operational challenges. The anticipated recovery of Thailand's rice industry in 2025-2026 promises to establish a dependable supply foundation for fresh rice-based Thai products, despite ongoing exposure to seasonal variations and climate-related supply risks. The industry has responded to these challenges by adopting innovative packaging technologies that focus on ethylene management and shelf life enhancement. These technological solutions incorporate 1-Methylcyclopropene (1-MCP) for ethylene suppression and potassium permanganate for ethylene removal, effectively addressing preservation challenges in the fresh food segment.

By Distribution Channel: Retail Dominance Strengthens

The retail channel maintains its strong position in Thailand's market with a substantial 66.34% market share in 2024. This channel is expected to experience robust growth at a 9.77% CAGR from 2025 to 2030, primarily due to the rapid expansion of e-commerce platforms and the increasing presence of convenience stores across the country. The evolution of Thailand's e-commerce landscape has been particularly noteworthy, with the food sector emerging as a key contributor, accounting for ~30% of all digital transactions. The widespread adoption of mobile technology has transformed shopping behaviors, with mobile devices now facilitating over 80% of online purchases [3]Source: International Trade Association, “Thailand Country Commercial Guide, ” trade.gov.

The competitive dynamics within Thailand's convenience store segment further illustrate the retail channel's expansion trajectory. 7-Eleven has established itself as the market leader with an extensive network of 12,740 stores throughout the country. The company's ambitious growth strategy includes plans to introduce 700 additional locations, demonstrating the continued potential for physical retail expansion. This combination of digital advancement and physical store growth positions the retail channel to effectively serve evolving consumer preferences and shopping patterns.

By Product Type: Ready Meals Drive Innovation

The Thai cuisine market analysis reveals that sauces, pastes, and condiments emerged as the dominant revenue-generating segment, commanding a substantial 33.43% share of total market revenue in 2024. This segment's market leadership underscores the increasing consumer appreciation for authentic Thai flavoring components, particularly as home cooking enthusiasts and food service establishments seek to recreate genuine Thai culinary experiences. The strong performance of this segment also reflects the growing integration of Thai flavors into fusion cuisines and contemporary cooking practices.

Looking ahead, the ready meals and curries segment presents compelling growth opportunities, with market projections indicating a substantial 9.64% CAGR through 2030. This remarkable growth trajectory is primarily driven by fundamental shifts in consumer behavior, as urban professionals and busy households increasingly gravitate toward convenient, restaurant-quality microwaveable options instead of traditional cooking methods. The market's evolution is further illustrated by the strategic diversification of established seafood companies into alternative protein segments, exemplified by the introduction of innovative plant-based dim sum products under the OMG Meat brand. This adaptation reflects the industry's responsiveness to changing consumer preferences and dietary requirements.

Geography Analysis

Asia-Pacific holds a 42.88% market share in 2024, benefiting from cultural similarities and established supply chains, though market maturation is moderating growth. Thailand's position within ASEAN trade networks and free trade agreements enhances export opportunities for Thai food products. Regional competition is increasing as local production capabilities grow, particularly with Chinese fried rice market expansion potentially affecting imported Thai ready meals in price-sensitive segments.

North America shows the highest growth rate at 9.64% CAGR from 2025-2030, supported by changing demographics and increasing interest in authentic Asian cuisines. The region's market infrastructure is well-developed, with the US containing 6,850 Thai restaurants, representing 39% of global Thai restaurant presence. Thai SELECT certification covers 1,377 locations across 70 countries.

Europe offers distinct opportunities through its sophisticated consumer base, though stringent regulations necessitate premium positioning strategies. The growing demand for natural food additives, driven by clean-label preferences and ethnic food consumption, creates opportunities for Thai cuisine products emphasizing authentic ingredients and transparent sourcing. However, the complex regulatory environment requires substantial compliance investments, including adherence to recognized standards such as BRC Global Standards.

Competitive Landscape

The Thai cuisine market maintains a fragmented competitive landscape, presenting significant opportunities for companies to pursue both market consolidation and specialized niche strategies. This market structure allows businesses to carve out distinct market positions while accommodating various business models and operational approaches.

Established companies in the market have successfully implemented vertical integration and sustainability initiatives to create unique value propositions. The implementation of QR code systems enables consumers to gain complete visibility into value chains, from raw material sourcing to production processes. This transparency directly addresses growing consumer concerns about food safety and influences their purchasing decisions in the market.

The market continues to evolve with emerging opportunities in convenience-focused segments and sustainable packaging solutions. Companies are increasingly adopting digital platforms and direct-to-consumer strategies to reach customers effectively. Digital transformation has become a crucial competitive factor, as demonstrated by initiatives like Ajinomoto's ADAMS data management platform. These technological investments enhance operational efficiency and customer engagement, transforming from optional advantages to essential business requirements in the current market environment.

Thai Cuisine Industry Leaders

Thai Union Group PCL

Charoen Pokphand Foods PCL

McCormick & Co.

Ajinomoto Co., Inc.

Thai President Foods Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: McCormick introduced Crushed Hatch Chile Pepper and Thai Style Chili Pepper products through its website, Amazon, and national grocery stores. The launch of these new products demonstrates the company's commitment to expanding its spice portfolio and meeting consumer demand for diverse flavor options.

- April 2025: PhilCo Food Processing, Inc., a subsidiary of Thai World Group, registered a PHP 1 billion investment with the Philippine Economic Zone Authority (PEZA) for a coconut processing facility in Misamis Oriental, Philippines. The facility plans to produce 78,000 tons of ultra-high temperature coconut milk and frozen coconut meat annually, with exports targeted to Thailand, Europe, and the United States.

- November 2024: Thai Wah launched its instant noodles in the retail market, expanding its product portfolio with four distinct Asian flavors - Thai tom yum kung, Thai boat noodles, Vietnamese pho, and Chinese mala.

Global Thai Cuisine Market Report Scope

| Ready Meals and Curries |

| Sauces, Pastes and Condiments |

| Noodles and Rice Dishes |

| Snacks and Confectionery |

| Soups and Broths |

| Others |

| Vegetarian |

| Non-Vegetarian |

| Frozen |

| Shelf-Stable Ambient |

| Fresh/Chilled |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Store | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Ready Meals and Curries | |

| Sauces, Pastes and Condiments | ||

| Noodles and Rice Dishes | ||

| Snacks and Confectionery | ||

| Soups and Broths | ||

| Others | ||

| By Varieties | Vegetarian | |

| Non-Vegetarian | ||

| By Form | Frozen | |

| Shelf-Stable Ambient | ||

| Fresh/Chilled | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Store | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Thai cuisine market and its expected growth?

The Thai cuisine market size is USD 18.23 billion in 2025 and it is forecast to reach USD 27.28 billion by 2030 at an 8.39% CAGR.

Which region is growing fastest for Thai cuisine products?

North America registers the quickest expansion, posting a 9.64% CAGR on the back of rising Thai restaurant density and omnichannel retail uptake.

Which product segment will contribute most to future growth?

Ready Meals and Curries are projected to expand at 9.64% CAGR, outpacing traditional sauce and paste lines as consumers seek convenient heat-and-eat options.

How are sustainability trends influencing competition?

Leading firms install solar power, adopt recyclable packaging, and deploy blockchain traceability, using ESG initiatives to win shelf space and build consumer trust.

Is plant-based Thai food a significant growth area?

Yes. The Vegetarian segment is growing at 9.68% CAGR, fueled by flexitarian diets and innovations such as algae-based seafood alternatives backed by major Thai processors.

Page last updated on: