Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

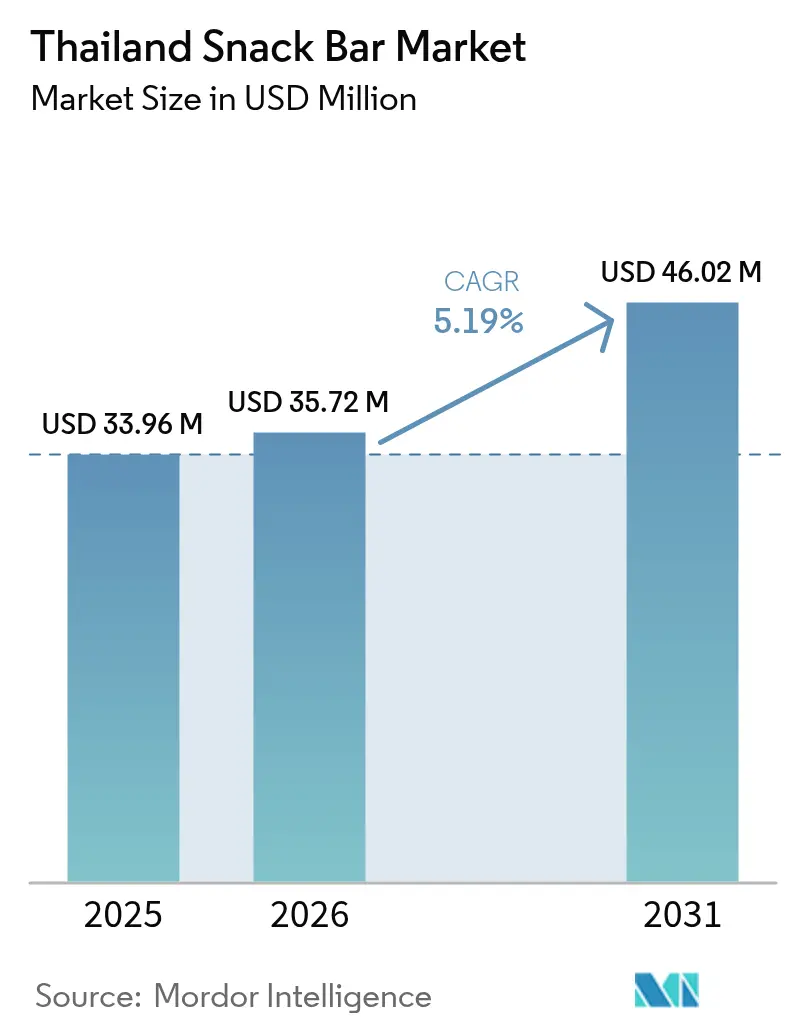

| Base Year Market Size (2025) | USD 33.96 Million |

| Market Size (2026) | USD 35.72 Million |

| Market Size (2031) | USD 46.02 Million |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

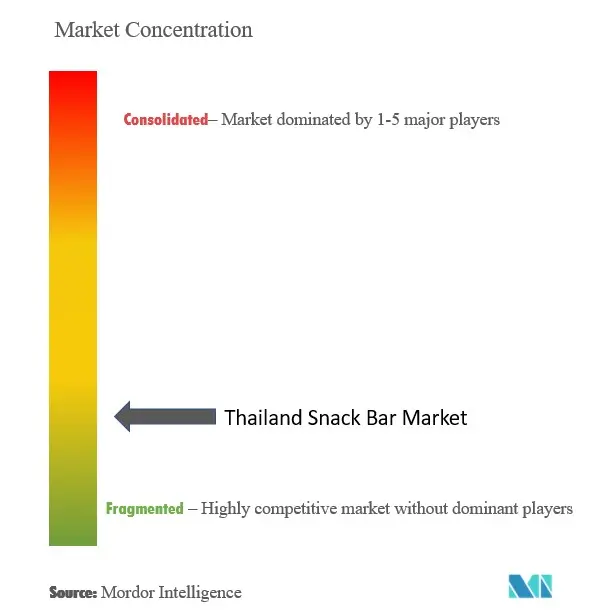

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Snack Bar Market Analysis by Mordor Intelligence

The Thailand snack bar market size was valued at USD 33.96 million in 2025 and estimated to grow from USD 35.72 million in 2026 to reach USD 46.02 million by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). This growth is driven by changing consumer lifestyles, increasing health awareness, and a rising preference for convenient, functional, and nutritious snack options. Factors such as urbanization, busier schedules, and the growing popularity of fitness and sports culture are encouraging consumers to opt for portable, on-the-go nutrition solutions, sustaining demand for products like protein bars, energy bars, cereal bars, and hybrid formulations. Additionally, consumer preferences are shifting toward healthier and functional ingredients, including oats, granola, nuts, dates, and protein isolates, as awareness of diet-related health concerns such as obesity, diabetes, and cardiovascular diseases continues to rise. Wellness trends have prompted manufacturers to develop clean-label, low-sugar, high-protein, and nutrient-fortified bars, catering to both mass-market and premium segments.

Key Report Takeaways

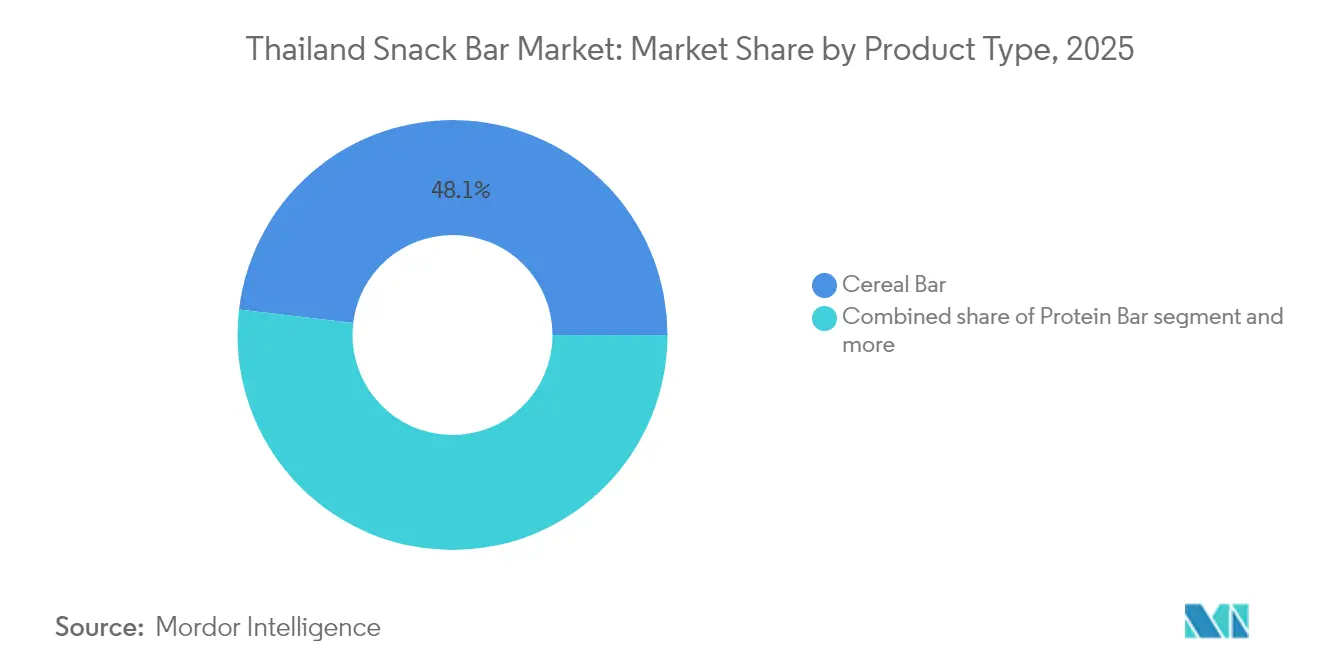

- By product type, cereal bars led with 48.10% of Thailand snack bar market share in 2025, while protein bars are forecast to expand at a 5.28% CAGR through 2031.

- By ingredient base, nut-based bars captured 36.15% of the Thailand snack bar market size in 2025, whereas granola and oat formulations are set to rise at a 6.05% CAGR to 2031.

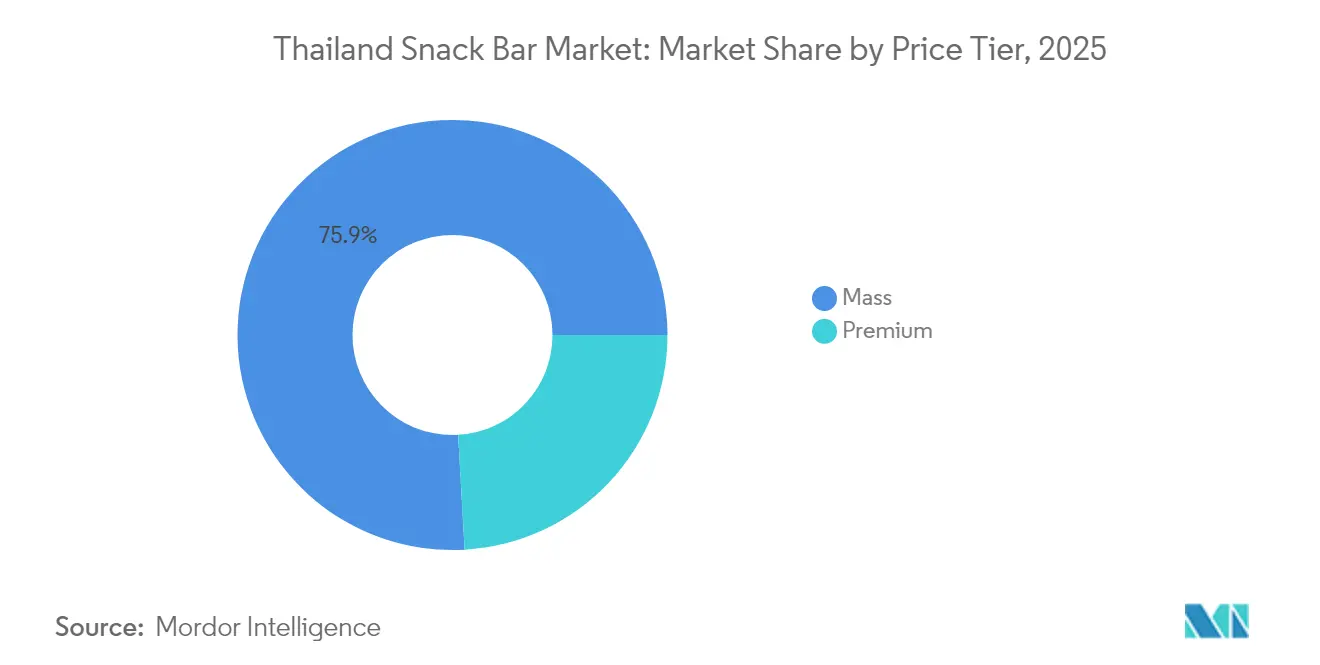

- By price tier, mass-tier SKUs commanded 75.90% revenue share in 2025, yet premium offerings are projected to post a 5.46% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 46.00% of value in 2025; online retail is poised for the fastest 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fitness and sports culture expansion | +0.9% | National, concentrated in Bangkok, Chiang Mai, Phuket | Medium term (2-4 years) |

| Increasing busy and on-the-go lifestyles | +0.7% | National, urban centers with highest intensity | Short term (≤ 2 years) |

| Tourism industry influence | +0.6% | National, peak impact in Phuket, Bangkok, Pattaya, Chiang Mai | Medium term (2-4 years) |

| Rising health and wellness awareness | +1.0% | National, early adoption in metropolitan areas | Long term (≥ 4 years) |

| Social media and influencer promotion | +0.8% | National, strongest in Gen Z and millennial demographics | Short term (≤ 2 years) |

| Innovation in packaging and portion control | +0.5% | National, premium segments lead adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fitness and sports culture expansion

The expansion of fitness and sports culture is a key factor driving the growth of Thailand's snack bar market. Increased participation in physical activities has led to higher demand for convenient, nutritious, and performance-focused snacks. According to the Ministry of Tourism and Sports, Thailand's sports industry generated a total output value of approximately 437 billion Thai Baht (USD 12.66 billion) in 2023, underscoring the economic and cultural significance of fitness and sports in the country [1]Source: The Ministry of Tourism and Sports, "Sports Economy", mots.go.th. The proliferation of gyms, yoga studios, running clubs, cycling communities, and organized sports events has further fueled consumer interest in snack bars that provide energy, protein, and essential nutrients to support workouts, recovery, and active lifestyles. This trend is particularly prominent among urban millennials and Gen Z consumers, who are driving demand for functional snack bars, such as protein bars, energy bars, and nutrient-rich hybrid formulations. In response, brands are introducing products tailored to pre- and post-workout nutrition, featuring low-sugar, high-protein options and clean-label ingredients.

Increasing busy and on-the-go lifestyles

Increasingly busy and fast-paced lifestyles are a significant driver of Thailand's snack bar market. Urbanization, extended working hours, and demanding daily routines have led to a rising demand for convenient, ready-to-eat nutritional options. Consumers in metropolitan areas such as Bangkok, Chiang Mai, and Phuket are managing work, education, commuting, and leisure activities, leaving limited time for traditional meals or snacks. Snack bars offer a portable, mess-free, and quick source of energy and nutrients, making them a practical choice for mid-morning breaks, office snacks, school lunches, and travel. This trend is evident across various demographic groups, including working professionals seeking healthier alternatives to vending machine snacks, students looking for affordable and satisfying options, and busy parents seeking convenient yet nutritious choices for their children. The preference for on-the-go snacks is further supported by the growing use of e-commerce and convenience-store retail channels, which ensure easy accessibility for quick purchases.

Tourism industry influence

The growth of the tourism industry significantly drives Thailand's snack bar market, as the rising number of domestic and international travelers boosts demand for convenient, portable, and ready-to-eat snacks. According to the Ministry of Tourism and Sports, Thailand welcomed approximately 25.82 million foreign tourists from Asia and the Pacific in 2024, along with over 7.3 million visitors from Europe, resulting in a total of about 35.5 million international visitors that year. Tourists often prefer grab-and-go snack options for activities such as sightseeing, airport travel, beach excursions, and day trips. This preference increases the consumption of snack bars in hotels, convenience stores, supermarkets, airports, and tourist hotspots. The diverse tourist population also drives product variety and innovation, as brands cater to varying taste preferences, dietary requirements, and nutritional expectations. For instance, snack bars are popular among health-conscious travelers, while chocolate- or cereal-based bars attract casual tourists seeking indulgent yet portable snacks. Retailers and snack bar brands capitalize on this demand by offering multipacks, travel-sized bars, and premium imported options tailored to tourist purchasing behavior.

Rising health and wellness awareness

Increasing health and wellness awareness is a significant driver of the Thailand snack bar market, as consumers focus more on nutritious, functional, and minimally processed food options in their diets. Awareness of diet-related health concerns, such as obesity, diabetes, and cardiovascular diseases, has led to a preference for snacks that are high in protein, fiber, vitamins, and minerals, while being low in sugar, artificial additives, and unhealthy fats. This trend is particularly evident among urban populations, younger consumers, and fitness-focused individuals who prioritize products that support weight management, muscle building, and overall wellness. Government initiatives and public health campaigns have further supported this shift by promoting healthier eating habits and educating consumers on balanced nutrition. Consequently, the demand for functional snack bars, including protein bars, nut-based bars, granola/oat-based bars, and low-sugar energy bars, has increased significantly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong preference for traditional Thai snacks | -0.8% | National, rural areas exhibit higher intensity | Long term (≥ 4 years) |

| High sugar and additive concerns | -0.6% | National, metropolitan areas show heightened sensitivity | Medium term (2-4 years) |

| Limited consumer education on functional nutrition | -0.4% | National, rural and lower-income segments most affected | Long term (≥ 4 years) |

| Shelf-life and texture challenges | -0.3% | National, exacerbated in southern coastal regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong preference for traditional thai snacks

The strong preference for traditional Thai snacks serves as a significant restraint on the growth of the snack bar market in Thailand. While health awareness and convenience trends are on the rise, a considerable portion of Thai consumers, particularly in non-urban areas and among older age groups, continue to favor traditional snacks such as khanom, sticky rice treats, dried fruits, savory crackers, and deep-fried snacks. These options are deeply rooted in Thai culture, readily available in markets, street stalls, and convenience stores, and are often perceived as more flavorful, authentic, and cost-effective compared to packaged snack bars. This cultural inclination restricts the penetration of modern snack bars in specific regions and consumer segments. Many consumers perceive packaged snack bars, especially imported or premium varieties, as less satisfying in terms of taste, portion size, or value for money when compared to traditional snacks. Furthermore, the emotional and cultural connection to traditional snacks poses challenges for brands in driving repeat purchases and fostering loyalty, particularly among households accustomed to local flavors and preparation methods.

High sugar and additive concerns

Concerns over high sugar content and additives significantly restrain the growth of Thailand's snack bar market. As health awareness increases, consumers are becoming more cautious about the dietary impact of processed snack bars, particularly those containing excessive sugar, artificial sweeteners, preservatives, or other chemical additives. These concerns are especially notable among parents selecting snacks for children, fitness enthusiasts, and urban consumers who prioritize clean-label and natural ingredients. The perception that snack bars are less healthy compared to traditional options like fruits, nuts, or homemade snacks can hinder both initial trials and repeat purchases. Even when snack bars provide functional benefits, such as protein or fiber enrichment, the inclusion of added sugars or artificial flavors may deter health-conscious consumers, particularly in premium or functional product segments. Additionally, regulatory scrutiny and public health campaigns emphasizing the risks associated with high sugar consumption further heighten consumer caution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Bars Gain Ground as Fitness Culture Matures

Cereal bars have become the leading product type in Thailand's snack bar market, accounting for 48.10% of the market share in 2025. This growth is attributed to evolving lifestyle trends, consumer preferences, and the versatility of these products. The increasing pace of urban life and the popularity of on-the-go snacking have made cereal bars a convenient and portable option for busy Thai consumers. They cater to a broad demographic, including schoolchildren seeking quick energy during breaks and office workers opting for mid-day snacks that are healthier alternatives to traditional fried or sugary options. Additionally, cereal bars are perceived as healthier and more natural due to their ingredients, such as oats, whole grains, nuts, and dried fruits.

Protein bars are projected to be one of the fastest-growing segments in Thailand's snack bar market, with an anticipated CAGR of 5.28% through 2031. This growth is driven by increasing fitness awareness, demand for functional nutrition, and significant government-backed health initiatives. Thailand has witnessed a cultural shift toward active lifestyles, marked by a rise in gym memberships, marathon participation, cycling clubs, and youth involvement in sports. This trend is strongly supported by national policies, including the National Plan to Promote Physical Activity (2018–2030) and its Action Plan (2018–2020), developed by the Ministry of Public Health in collaboration with the Ministry of Interior, Ministry of Education, Ministry of Labour, and the Thai Health Promotion Foundation. These initiatives promote regular physical activity, healthier dietary choices, and the integration of wellness programs into schools, workplaces, and communities.

By Ingredient Base: Granola and Oat Formulations Ride Clean-Label Wave

Nut-based bars hold a dominant 36.15% market share in Thailand's snack bar segment in 2025. This is supported by the country's well-established cashew-processing infrastructure, which benefits from Thailand's position as the 17th largest global importer of fresh and dried cashew nuts, valued at USD 73.6 million in 2023, according to the Observatory of Economic Complexity (OEC) . This advantage provides a consistent and cost-effective supply of high-quality nuts, including cashews, almonds, and peanuts. These nuts enable manufacturers to produce protein-rich, crunchy bars containing natural fats and antioxidants, appealing to health-conscious urban consumers seeking satisfying, cholesterol-friendly snacks amid growing wellness trends. Additionally, the increasing popularity of plant-based diets and the rising preference for nutrient-dense snacks further bolster the demand for nut-based bars in the market.

Granola and oat-based bars represent one of the fastest-growing ingredient segments in Thailand’s snack bar market, with a projected compound annual growth rate (CAGR) of 6.05% through 2031. This growth is driven by increasing health awareness, rising demand for high-fiber foods, and the adoption of Western-style wellness diets among Thai consumers. Oats and granola are increasingly associated with benefits such as heart health, digestive wellness, weight management, and sustained energy release. As a result, Thai consumers are gradually shifting toward products incorporating these ingredients, reflecting a broader trend toward healthier eating habits. Furthermore, the versatility of granola and oats in various snack formats, coupled with their alignment with clean-label and natural ingredient preferences, is expected to drive their continued expansion in the market

By Price Tier: Premium Segment Expands Despite Affordability Barriers

In 2025, mass-tier snack bar products dominated Thailand's snack bar market, accounting for 75.90% of the market share. This dominance was attributed to their affordability, widespread availability, and alignment with everyday consumer snacking habits. Thailand's packaged foods market is highly price-sensitive, with consumers balancing health aspirations against budget constraints. Mass-tier snack bars, often positioned as simple, familiar, and moderately nutritious, effectively meet this balance. Their competitive pricing makes them suitable for regular consumption, and they are commonly chosen as quick energy sources by students, office workers, commuters, and families seeking convenient, low-cost snack options. Additionally, the strong presence of local and regional brands in this segment has further enhanced accessibility and consumer trust, reinforcing their widespread appeal in the market.

Premium-tier snack bar products, while holding a smaller share of the market compared to mass-tier offerings, are expected to experience notable growth, with a projected CAGR of 5.46% through 2031. This growth is fueled by increasing health awareness, a growing fitness-oriented consumer segment, and a rising willingness among urban consumers to invest in higher-quality, cleaner, and more functional nutritional products. Premium snack bars often feature high-quality ingredients such as imported nuts, mixed seeds, whey or plant proteins, low-sugar formulations, superfoods, and organic or non-GMO components. These attributes appeal to consumers seeking nutritional benefits that go beyond basic snacking. Furthermore, the growing influence of social media and health-focused marketing campaigns has amplified consumer interest in premium-tier snack bars, positioning them as a desirable choice for health-conscious individuals.

By Distribution Channel: E-Commerce Disrupts Traditional Retail Hierarchies

In 2025, supermarkets and hypermarkets dominated Thailand's snack bar distribution landscape, capturing a 46.00% market share. This dominance is attributed to their extensive product variety, strong merchandising capabilities, and the trust they inspire among consumers seeking quality-assured packaged foods. Major chains such as Tesco, Tops, and Central Food Hall serve as key shopping destinations for urban and suburban households, where snack purchases are often part of weekly or monthly grocery trips. These retailers offer a broad assortment of snack bar brands, including mass-tier, premium, imported specialty bars, and functional nutrition formats. This extensive selection provides consumers with greater variety compared to convenience stores or smaller retailers, encouraging brand exploration, cross-shopping, and bulk purchases. As a result, supermarkets and hypermarkets remain the primary channel for accessing the most diverse snack bar offerings.

Online retail is emerging as the fastest-growing distribution channel for snack bars in Thailand, with a projected CAGR of 6.88% through 2031. This growth is driven by the country's rapidly advancing digital economy, seamless mobile payment systems, and a shift in consumer behavior toward convenience-focused, app-based purchasing. According to the Bank of Thailand, mobile banking now accounts for 30% of all online payments, while buy-now-pay-later (BNPL) services represent 41%, significantly reducing barriers to both planned and impulse purchases . These frictionless payment options, combined with targeted advertisements, influencer promotions, and platform-specific discounts, make it particularly easy for younger, tech-savvy consumers to purchase snack bars with minimal effort.

Geography Analysis

Thailand’s snack bar market exhibits a significant geographic concentration, with Bangkok and its surrounding metropolitan areas—including Nonthaburi, Samut Prakan, and Pathum Thani- accounting for the majority of national sales. These urban centers benefit from greater exposure to modern retail formats, higher purchasing power, and increased health-consciousness influenced by lifestyle trends, fitness participation, and digital media. The dense network of supermarkets, hypermarkets, convenience stores, gyms, and specialty health shops ensures wide availability of both mass-tier and premium snack bar products. Furthermore, Bangkok’s advanced e-commerce penetration and efficient delivery infrastructure drive consumption, as consumers in this region are early adopters of online shopping and functional foods.

Southern provinces such as Phuket, Krabi, Surat Thani, and Songkhla experience distinct market dynamics influenced by climate and tourism. Tourist-heavy areas in these regions generate higher demand for convenient, portable snack bars. However, persistent coastal humidity and warmer temperatures pose shelf-life challenges, particularly for chocolate-coated, nut-based, and oat-based bars, which are prone to texture degradation. To address these issues, manufacturers and retailers invest in robust packaging and temperature-controlled storage solutions. Despite these challenges, the southern provinces maintain a steady market presence, supported by hotel retail, airport shops, beachside convenience stores, and the strong influx of domestic and international tourists seeking on-the-go, healthier snack options.

Border provinces such as Mae Sot, Chiang Rai, Chiang Khong, Mukdahan, and Nong Khai present unique opportunities and challenges due to cross-border trade dynamics with Myanmar, Laos, and southern China. These regions often act as gateways for both formal and informal trade flows, with snack bars distributed through border markets, wholesale hubs, and small retailers catering to migrant workers and cross-border travelers. Product availability in these areas may vary depending on import patterns, local tariffs, and the enforcement of food safety regulations. While lower-cost mass-tier snack bars often enter these markets via parallel imports, premium products are less common due to limited purchasing power and the scarcity of modern retail outlets.

Competitive Landscape

The competitive landscape of Thailand’s nutrition bar market is highly fragmented, characterized by the presence of both multinational corporations and agile domestic brands. Global companies such as Nestlé S.A., Mars Incorporated, General Mills Inc., and Mondelez International, Inc. leverage their extensive product portfolios, advanced research and development capabilities, and strong distribution networks to maintain visibility and consumer trust across Thai retail channels. These companies offer internationally recognized brands, consistent product quality, and a diverse range of products, including cereal bars, protein bars, and indulgent snack bars, securing prominent shelf space in supermarkets, hypermarkets, and convenience stores.

In addition to global leaders, local players such as Tao Kae Noi, Malee Group, and Doi Kham significantly contribute to the market's fragmentation. These domestic companies benefit from a deep understanding of Thai cultural preferences, enabling them to cater to local tastes with products featuring tropical fruit flavors, nut-based formulations, and plant-forward snacks. Their agility in decision-making allows them to quickly adapt to emerging trends. Furthermore, by utilizing locally sourced ingredients and simplifying recipes, these brands achieve competitive production costs, making them particularly appealing in the mass-tier segment.

Technology adoption has emerged as a critical factor in strengthening market positions for both global and local firms. Companies are investing in supply chain optimization and digital operational efficiency to address logistical challenges and ensure product freshness, which is especially important in Thailand’s humid climate, where shelf-life issues are prevalent. Advanced demand forecasting, automated warehousing, and digitally integrated procurement systems are being implemented to minimize disruptions. Additionally, e-commerce integration, online inventory synchronization, and last-mile delivery partnerships are becoming essential for capturing the rapidly growing online retail channel.

Thailand Snack Bar Industry Leaders

-

Nestle S.A.

-

Mars, Incorporated (Be-Kind)

-

General Mills Inc.

-

Mondelez International, Inc.

-

PepsiCo, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Plantae has introduced a Banoffee Caramel flavor to its protein bar range. Each bar provides 10 g of protein, 170 kilocalories, 3,000 mg of fiber, contains 0% cholesterol, and includes no added sugar.

- June 2025: Nature Valley has launched its latest Crunchy Oats and Choco Chips Bar in Thailand, made with premium ingredients and devoid of artificial flavours, colours, and high fructose corn syrup.

Thailand Snack Bar Market Report Scope

Snack bars are made up of cereals such as wheat, barley, etc. Snack bars are produced by pressing the grains with nuts, berries, and other ingredients. They bind with glucose syrups and contain low caloric content. These are meal alternatives as they provide essential nutrients such as iron, starch, fiber, proteins, antioxidants, phosphorus, and potassium. The Thai snack bar market is segmented by product type and distribution channel. On the basis of product type, the market is segmented into cereal bars, energy bars, and other snack bars. Furthermore, the cereal bar segment has been sub-segmented into granola/muesli bars and other cereal bars. On the basis of distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist retailers, online retail, and other distribution channels. The report offers the market size and forecasts in value (USD) for all the above segments.

By Product type

| Cereal Bar |

| Protein Bar |

| Fruit and Nut Bar |

By Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product type | Cereal Bar |

| Protein Bar | |

| Fruit and Nut Bar | |

| By Ingredient Base | Nut-based bars |

| Granola/Oat-based | |

| Date-based | |

| Dairy/Protein-based | |

| Hybrid blends | |

| Other | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Thailand nutrition bar market in 2026?

It is valued at USD 35.72 million and is projected to reach USD 46.02 million by 2031.

What growth rate is forecast for nutrition bars in Thailand?

The category is expected to register a 5.19% CAGR between 2026 and 2031.

Which product segment is expanding fastest?

Protein bars are projected to grow at a 5.28% CAGR due to rising fitness adoption.

Why are online channels important for bar sales?

E-commerce is forecast to post a 6.88% CAGR as live commerce and mobile payments simplify nationwide access.

Page last updated on: