Testing, Inspection, and Certification for the Natural Resources Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

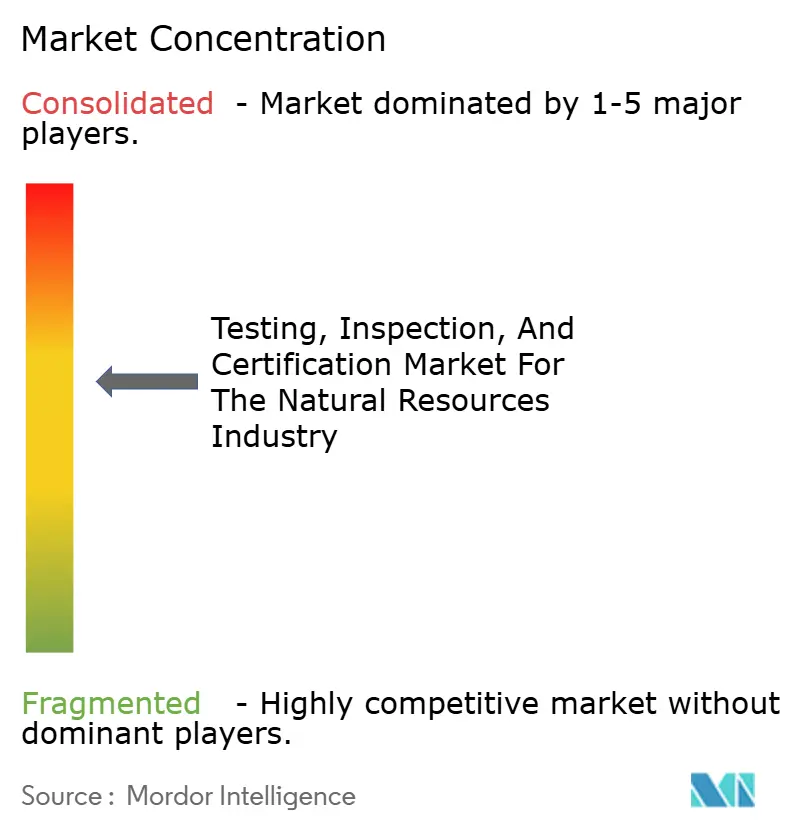

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Testing, Inspection, and Certification for the Natural Resources Industry Analysis by Mordor Intelligence

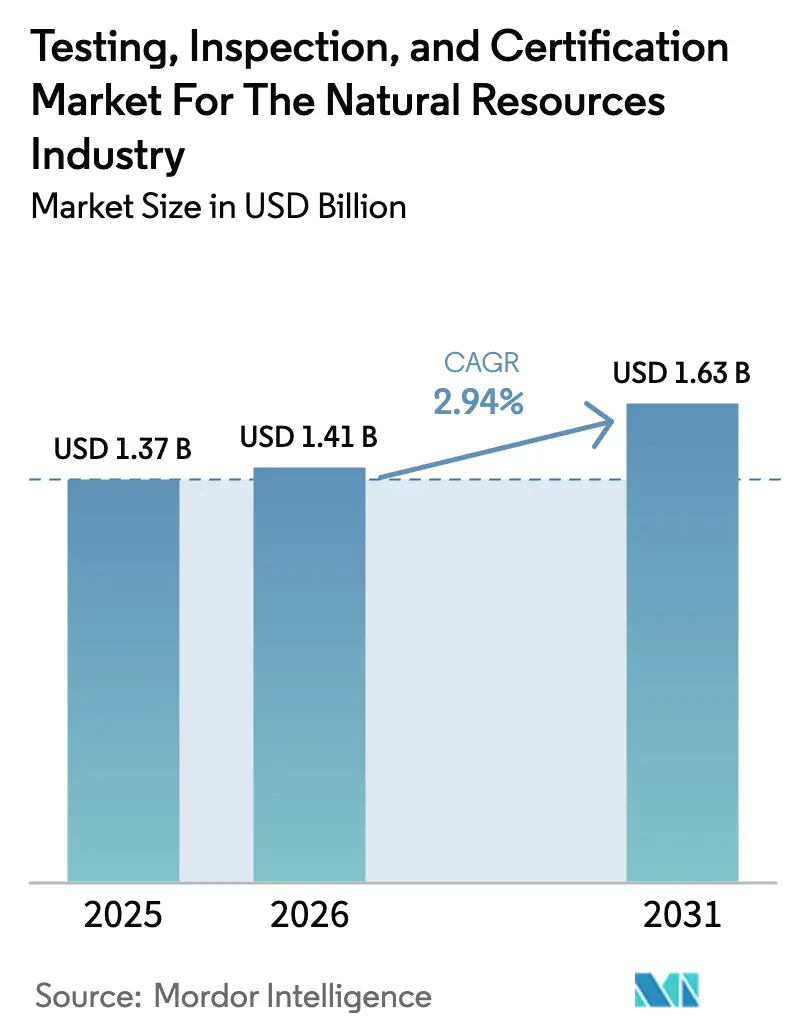

The testing, inspection, and certification market size for the natural resources industry is expected to grow from USD 1.37 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 1.63 billion by 2031 at 2.94% CAGR over 2026-2031. Asia-Pacific leads with 38.9% revenue share in 2024 and posts the fastest 3.9% CAGR, underscoring the region’s dual position as the largest consumer of energy and minerals and the most active infrastructure builder. Demand accelerates as stricter environmental regulations, expanding critical minerals supply chains, and digital transformation create fresh verification requirements across exploration, production, and downstream logistics. Operators are increasingly outsourcing technical compliance tasks to conserve capital for core extraction activities, while cybersecurity certification, IoT device validation, and data integrity testing emerge as high-value niches. Consolidation potential remains moderate as no player controls more than 15% of revenue, yet technology-driven differentiation is widening competitive gaps across the Testing, Inspection, and Certification for the Natural Resources Industry.

Key Report Takeaways

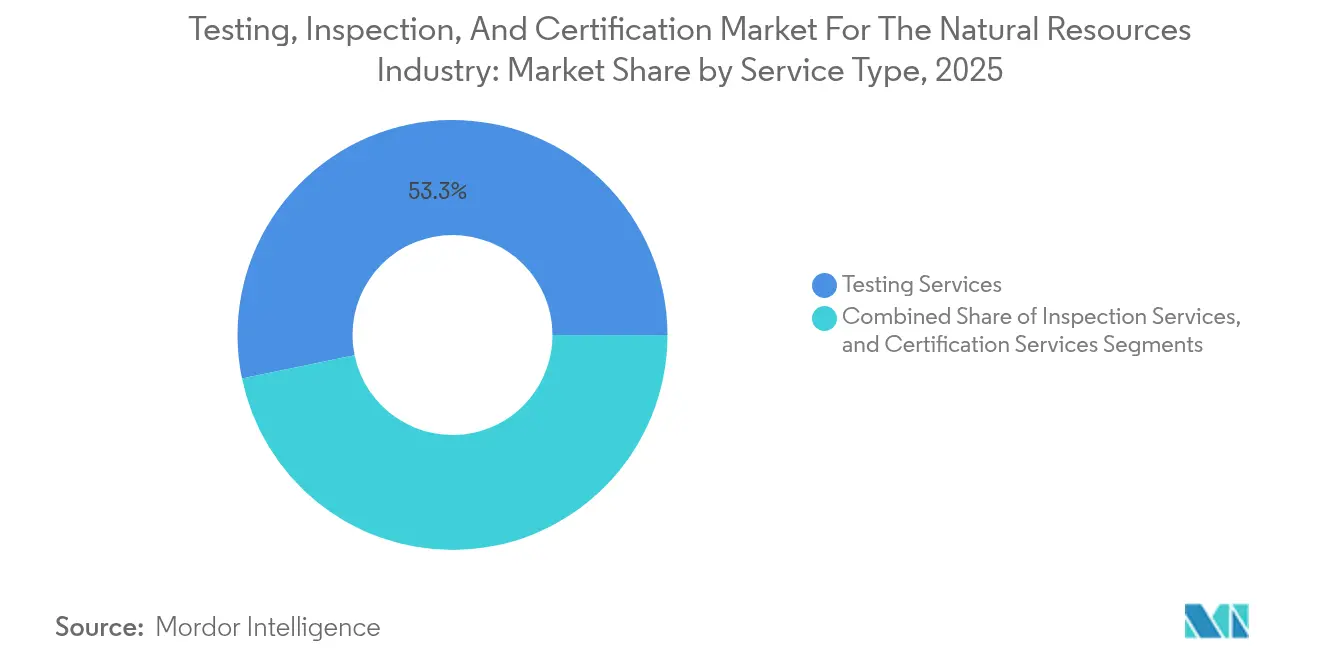

- By service type, testing services held 53.25% of the Testing, Inspection, and Certification for the Natural Resources Industry share in 2025; certification services are forecast to expand at a 3.55% CAGR through 2031.

- By sourcing type, the outsourced model accounted for a 66.15% share of the testing, inspection, and certification market size for the natural resources industry in 2025 and is projected to advance at a 3.28% CAGR through 2031.

- By geography, the Asia-Pacific region accounted for 38.55% of the testing, inspection, and certification market size for the natural resources industry in 2025, and is projected to grow at a 3.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Testing, Inspection, and Certification for the Natural Resources Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations mandating third-party compliance testing | +1.4% | Global, with the strongest impact in North America and Europe | Medium term (2-4 years) |

| Rising global demand for energy and minerals is driving exploration activities | +1.0% | Asia-Pacific core, spill-over to the Middle East, and Africa | Long term (≥ 4 years) |

| The increasing complexity of commodity supply chains necessitates traceability audits | +0.7% | Global, with early gains in North America, Europe, and developed Asia-Pacific markets | Medium term (2-4 years) |

| Growing adoption of digital oilfields and smart mining requires real-time inspection services | +0.6% | North America and Europe are leading, expanding into the Asia-Pacific region. | Short term (≤ 2 years) |

| Rapid expansion of the critical minerals value chain is spurring specialized assay testing | +0.4% | Asia-Pacific and North America, with emerging opportunities in South America | Long term (≥ 4 years) |

| ESG-driven investment pressure for independent sustainability certification | +0.3% | Global, with the strongest adoption in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations Mandating Third-Party Compliance Testing

Global oversight is pivoting from operator self-reporting to mandatory independent verification that covers emissions, groundwater quality, waste management, and soil impacts. The U.S. Environmental Protection Agency’s 2024 PFAS National Primary Drinking Water Regulation added extensive sampling obligations near oil and gas wells, creating new revenue streams for accredited laboratories.[1]Environmental Protection Agency, “PFAS National Primary Drinking Water Regulation,” EPA.gov Parallel changes to the European Union Industrial Emissions Directive require continuous emissions monitoring calibrated by third parties. U.S. states such as California and Texas demand quarterly methane-leak inspections using optical gas imaging, while nations adopting carbon-pricing regimes stipulate verified greenhouse-gas measurement. The Testing, Inspection, and Certification for the Natural Resources Industry, therefore, benefits from large volumes of laboratory work and on-site audits as regulatory fragmentation generates localized niches that favor seasoned providers.

Rising Global Demand for Energy and Minerals Driving Exploration Activities

A sustained annual 4% growth in energy consumption across Asia-Pacific is spurring fresh LNG, pipeline, and mining projects, each requiring exhaustive geological, environmental, and asset-integrity examinations. Renewable-energy installations themselves depend on lithium, cobalt, and nickel extraction, intensifying demand for environmental impact assessments and specialized assay testing. China’s Belt and Road financing funnels capital into Central Asian oil and mining ventures that must demonstrate compliance with multilateral lending standards, thereby importing international verification requirements. Emerging hydrogen economies in Japan, Australia, and India introduce brand-new certification needs for electrolyzers, storage tanks, and transport pipelines. As exploration budgets climb, the Testing, Inspection, and Certification for the Natural Resources Industry expands through the provision of sophisticated laboratory analytics, structural inspections, and certification audits tailored to ever more complex project-design specifications.

Increasing Complexity of Commodity Supply Chains Necessitating Traceability Audits

Global attention has moved from conflict-mineral screening to full ESG-based provenance verification. The OECD Due Diligence Guidance now compels chain-of-custody documentation underpinned by analytical fingerprinting.[2]OECD, “OECD Due Diligence Guidance for Responsible Supply Chains of Minerals,” OECD.orgAutomotive and electronics OEMs require blockchain-backed validation of battery-metal origins, generating continuous service demand for field sampling, isotope analysis, and data-integrity assurance. The forthcoming EU Critical Raw Materials Act introduces compulsory quality checks for strategic stockpiles, institutionalizing year-round laboratory and audit activity. These developments favor outsourced specialists that possess ISO 17025 accreditation for high-precision assays and the IT skills necessary to secure distributed-ledger platforms, enabling them to capture recurring revenue from the Testing, Inspection, and Certification for the Natural Resources Industry.

Growing Adoption of Digital Oilfields and Smart Mining Requiring Real-Time Inspection Services

Operational technology convergence with IT in extraction industries is reshaping service portfolios toward cybersecurity testing, sensor validation, and software-algorithm bias checks. Deployments such as SLB’s digital oilfield rely on uninterrupted data flows that require third-party verification of network security and measurement fidelity. Mining operators deploy IoT devices across haul trucks, drills, and conveyors; each device must meet electromagnetic-compatibility and functional-safety standards validated by accredited TIC labs. Artificial-intelligence engines used for predictive maintenance demand periodic third-party model validation to satisfy safety regulators. These needs elevate high-margin digital compliance work and help shift the testing, inspection, and certification services industry toward a platform-based, always-on monitoring model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-price volatility is causing cyclical TIC budget cuts | -0.8% | Global, with the strongest impact in commodity-dependent regions | Short term (≤ 2 years) |

| Shortage of certified inspectors for remote resource sites | -0.5% | Asia-Pacific, Middle East and Africa, and remote North American locations | Medium term (2-4 years) |

| In-house sensor and analytics adoption is reducing external testing demand | -0.4% | North America and Europe are leading, expanding into developed Asia-Pacific markets | Medium term (2-4 years) |

| Geopolitical sanctions restricting TIC access in resource-rich regions | -0.3% | Russia, Iran, and other sanctioned territories with spillover effects globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Causing Cyclical TIC Budget Cuts

Swings in crude oil and base-metal benchmarks lead operators to slash non-core expenditures when cash flows tighten, putting discretionary verification programs in the firing line. World Bank data show post-2020 price variance up 40%, mirrored by average 15-25% spending cuts during downturns.[3]World Bank, “Commodity Markets Outlook,” WorldBank.org Federal Reserve studies note TIC costs are often treated as overhead, letting them fall disproportionately when budgets shrink. Service providers consequently endure revenue lulls of up to 40%, hindering long-term investment in new laboratories and inspector training. The Testing, Inspection, and Certification for the Natural Resources Industry must therefore diversify across commodities and geographies to smooth revenue cycles, yet smaller regional firms may lack the capital resilience to ride out sharp contractions.

Shortage of Certified Inspectors for Remote Resource Sites

An aging technical workforce and tight certification pipelines constrain the supply of qualified inspectors able to travel to distant mines, Arctic pipelines, and offshore platforms. Research shows 35% of oil and gas professionals will reach retirement eligibility within 10 years, outpacing new-entrant rates. Harsh climates, rotational schedules, and multilingual communication requirements deter younger talent, while standards from ISO, ASTM, and ASNT impose stringent experience thresholds. Advanced inspection techniques such as drone-based photogrammetry and phased-array ultrasonics demand additional training, lengthening time-to-competence and elevating labor costs. The deficiency slows project approvals, raises service prices, and limits how fast the Testing, Inspection, and Certification for the Natural Resources Industry can grow in frontier regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Services Anchor Market Leadership

Testing services generated 53.25% of revenue in 2025, reflecting indispensable laboratory analysis of hydrocarbon streams, critical mineral ores, and emerging contaminants. That dominance persists because environmental regulators enforce quantitative verification, a task that only accredited laboratories can execute with traceable standards and documented uncertainty. Evolving protocols for PFAS, microplastics, and trace metals are widening the analytical menu and sustaining double-digit sub-segment growth inside the broader Testing, Inspection, and Certification for the Natural Resources Industry.

Certification services, though smaller, register the fastest 3.55% CAGR as institutional investors and lenders demand third-party attestation of ESG metrics. New ISO 14064 standards for greenhouse-gas inventory and carbon-credit quantification are elevating demand for independent certificates, while battery-material supply chains require continuous chain-of-custody validation. Inspection services remain the stalwart for structural integrity checks on pipelines, storage tanks, and heavy equipment, yet their growth lags as more visual routines migrate to drone and sensor platforms. Even so, inspection retains a critical role when catastrophic failure risks preclude relying solely on digital surrogates, ensuring stable demand within the Testing, Inspection, and Certification for the Natural Resources Industry.

By Sourcing Type: Outsourced Model Sustains Two-Thirds Share

Outsourced service provision controlled 66.15% of revenue in 2025, confirming operators’ preference to allocate capital toward drilling, extraction, and refining rather than running complex laboratories. Rising regulatory sophistication, from real-time methane monitoring to cybersecurity protocols, further discourages in-house buildouts because compliance requires specialized talent and costly equipment. Consequently, the outsourced approach grows at a 3.28% CAGR, reinforcing scale advantages for global chains and niche specialists alike.

In-house units still perform routine checks such as daily water-quality tests or equipment calibration, but specialized jobs—PFAS analysis, blockchain-traceability audits, industrial-control-system penetration tests—shift to external experts. Cost-plus contracts are giving way to outcome-based models in which providers guarantee turnaround times, data-integrity thresholds, or uptime percentages. This transition aligns incentives and secures multiyear revenue visibility for suppliers, fortifying the Testing, Inspection, and Certification for the Natural Resources Industry as a strategic extension of operators’ compliance architectures.

Geography Analysis

Asia-Pacific’s 38.55% share underscores vast energy and infrastructure spending, from LNG import terminals in China to nickel mines in Indonesia. The region’s 3.78% CAGR is powered by renewable-energy build-outs that increase demand for materials testing and by tightening local environmental laws that prescribe third-party audits. China’s roadmap to 70% renewable electricity by 2050 alone spawns thousands of verification projects annually. Australia, the Philippines, and Vietnam add further momentum with copper, lithium, and rare-earth developments that must prove sustainable sourcing to global buyers. Japan and South Korea’s hydrogen-economy ambitions drive certification requests for new electrolyzer and storage technologies, expanding the Testing, Inspection, and Certification for the Natural Resources Industry footprint into emerging clean-energy hubs.

North America contributes substantial volume through mature shale plays that require hydraulic-fracturing-fluid analysis, produced-water treatment validation, and methane-emissions monitoring under Environmental Protection Agency rules. Domestic-content requirements in the Inflation Reduction Act accelerate mining projects for battery metals, translating into assay testing and ESG audits. Canada’s oil-sands and Arctic offshore prospects demand cold-weather materials testing and remote inspection, while Mexico’s upstream liberalization opens offshore safety-verification opportunities aligned with American Petroleum Institute standards. Although commodity price volatility periodically dents exploration budgets, the region’s robust regulatory oversight maintains a baseline need for third-party services, securing stable revenue for the Testing, Inspection, and Certification for the Natural Resources Industry.

Europe’s stringent sustainability framework shapes a distinctive service mix centered on renewable-energy-component testing, carbon-capture project validation, and recycling-process certification. The Corporate Sustainability Reporting Directive compels granular third-party data assurance for thousands of companies, expanding certification revenue pools. Norway’s offshore wind fields and CO₂ storage sites foster demand for marine geotechnical testing and subsea pipeline inspection. Germany’s industrial decarbonization funds catalyze hydrogen infrastructure build-outs that require verifying electrolyzer efficiency, storage integrity, and pipeline material compatibility. Meanwhile, Eastern European states adopt EU-aligned regulations, boosting demand for accredited TIC laboratories to support cross-border energy and mineral flows. Collectively, these dynamics anchor Europe as a high-value but technically demanding arena within the Testing, Inspection, and Certification for the Natural Resources Industry.

Competitive Landscape

The market is moderately fragmented, with the top five firms collectively capturing a significant share, limiting pricing power but rewarding innovation. SGS, Bureau Veritas, and Intertek leverage global laboratory networks and digital platforms to streamline sample logistics, automate data processing, and deliver real-time dashboards. SGS and Microsoft’s AI collaboration cuts test-result turnaround times while enhancing anomaly detection accuracy.[4]SGS, “Cross-Industry Collaboration to Create Digital TIC Services,” SGS.com Bureau Veritas employs AI-driven document automation that trims 75% of processing time, freeing engineers for higher-value consulting assignments. Intertek’s expansion into operational-technology cybersecurity tests positions it to capture the rising demand for digital-asset assurance.

Mid-tier specialists adopt niche strategies. Nordic Inspekt Group acquires hydrogen-infrastructure labs to enter high-growth clean-energy verticals, while Sansidor scales phased-array ultrasonic capabilities after private-equity infusion. Smaller outfits win contracts by targeting PFAS analysis, critical minerals fingerprinting, or autonomous-vehicle sensor validation—areas where large generalists lag in expertise. Persistent Systems reports the sector is migrating toward subscription-style monitoring platforms that ingest IoT data, run AI analytics, and issue predictive maintenance alerts. Such models promise recurring revenue and deep integration into client workflows, gradually transforming the testing, inspection, and certification services industry from episodic testing to continuous compliance assurance.

Consolidation is expected to intensify as regulatory complexity raises barriers to entry and digital-technology capex scales upward. Global firms will likely acquire domain specialists to fill capability gaps in hydrogen, carbon capture, and blockchain-based traceability. Conversely, regional champions may merge to achieve the geographic coverage required by multinational mining and energy clients. Midsize providers that fail to secure capital for digital upgrades risk marginalization, ceding ground to data-driven competitors in the Testing, Inspection, and Certification for the Natural Resources Industry.

Testing, Inspection, and Certification for the Natural Resources Market Leaders

SGS SA

Intertek Group Plc

Bureau Veritas SA

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Intertek expanded cybersecurity testing for operational-technology systems in digitalized oil and gas facilities.

- November 2024: UL Solutions rolled out PFAS groundwater and soil testing protocols aligned with new EPA requirements.

- August 2024: Nordic Inspekt Group acquired a German materials-testing laboratory to expand hydrogen-infrastructure and renewable-energy certification capabilities.

- July 2024: IK Partners invested EUR 50 million (USD 54 million) in Sansidor Group to accelerate phased-array ultrasonic and computed-radiography inspection services across Europe.

Global Testing, Inspection, and Certification for the Natural Resources Industry Report Scope

The report on the Testing, Inspection, and Certification for the Natural Resources Industry segments the market by Service Type, including Testing, Inspection, and Certification Services. It also categorizes the market by Sourcing Type, distinguishing between In-House and Outsourced services. Geographically, the report covers North America (United States, Canada, Mexico), South America (Brazil, Argentina, and the Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, South-East Asia, and the Rest of Asia-Pacific), and the Middle East and Africa (Saudi Arabia, United Arab Emirates, Turkey, the Rest of the Middle East, South Africa, Nigeria, and the Rest of Africa). Market forecasts are presented in terms of value (USD).

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the testing inspection and certification market for the natural resources industry for the natural resources industry in 2026?

It is valued at USD 1.41 billion in 2026 and is forecast to reach USD 1.63 billion by 2031 at a 2.94% CAGR.

Which service segment holds the highest share in this field?

Testing services lead with a 53.25% share in 2025 owing to indispensable laboratory requirements across exploration and production phases.

Why is Asia-Pacific expanding faster than other regions?

Massive infrastructure projects, critical-mineral processing growth, and increasingly stringent local environmental regulations push Asia-Pacific to a 3.78% CAGR through 2031.

What drives outsourcing in verification tasks?

Rising regulatory complexity and costly specialized equipment encourage operators to outsource 66.15% of all TIC activities so they can focus capital on core extraction.

How is digitalization changing service demand?

Cybersecurity audits, IoT device validation, and real-time sensor verification are creating high-margin niches that shift the industry from episodic testing to continuous monitoring.

Page last updated on: