Certification And Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

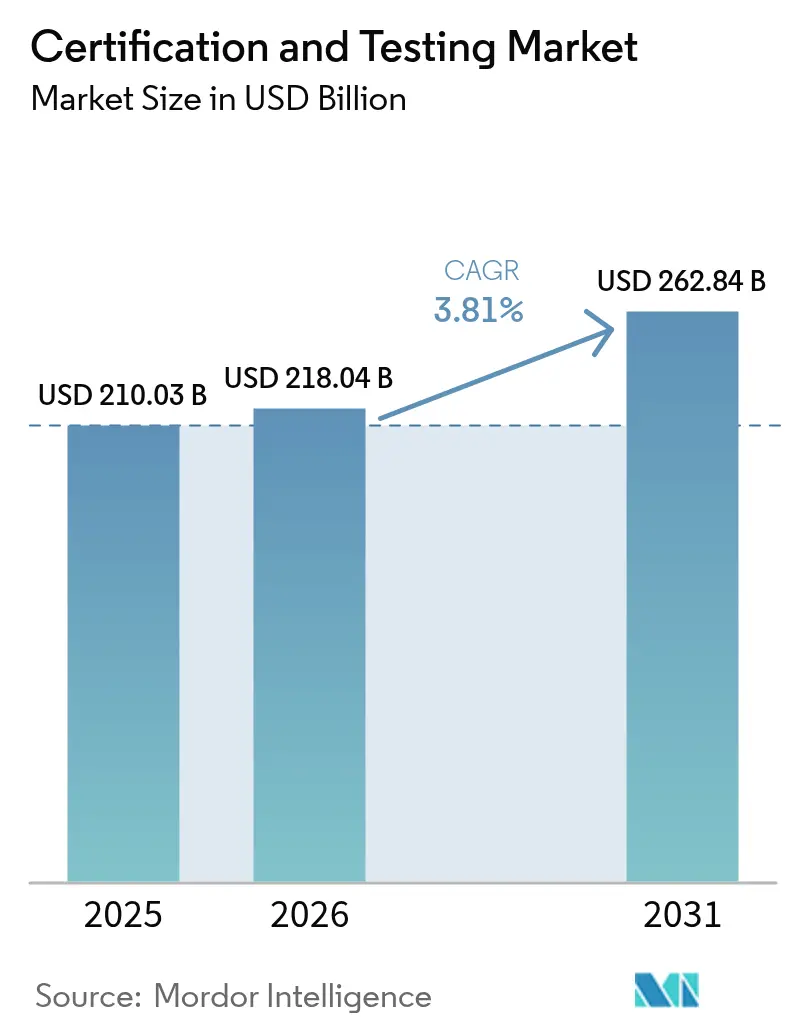

| Market Size (2026) | USD 218.04 Billion |

| Market Size (2031) | USD 262.84 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

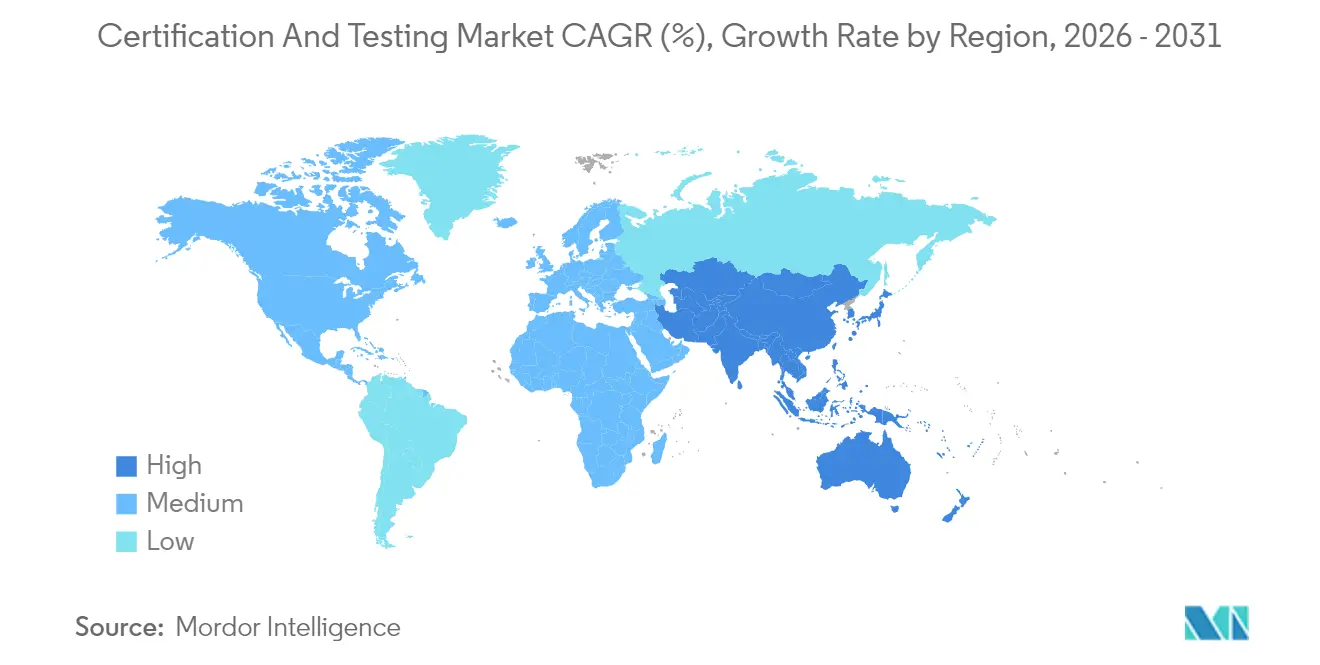

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Certification And Testing Market Analysis by Mordor Intelligence

The certification and testing market size was valued at USD 210.03 billion in 2025 and estimated to grow from USD 218.04 billion in 2026 to reach USD 262.84 billion by 2031, at a CAGR of 3.81% during the forecast period (2026-2031). Outsourced providers already handle two-thirds of all compliance work, and their share is widening as manufacturers shift budgets from laboratory infrastructure to R&D. Digital platforms such as the U.S. Customs and Border Protection’s eCERT portal shorten origin-certificate processing from days to minutes, pointing to faster cross-border turnaround times. Demand is also rotating toward management system audits, with ISO 27001 cybersecurity and ISO 50001 energy certifications expanding more quickly than traditional product testing. The Asia-Pacific region remains the growth engine, aided by China’s expanded CCC catalog and India’s broader BIS mandates. Meanwhile, food and healthcare companies dominate volume, yet transportation is the fastest-rising vertical as UN Regulations 155 and 156 reshape automotive cyber-risk rules.

Key Report Takeaways

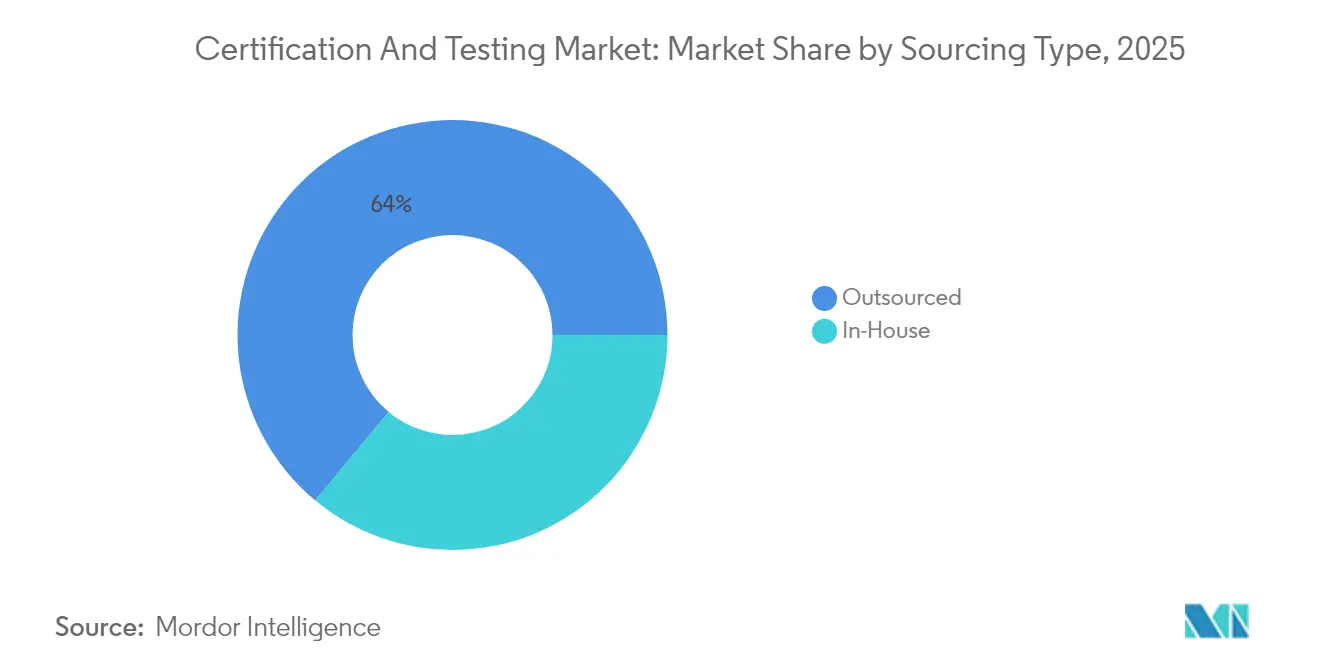

- By sourcing type, outsourced testing captured a 63.98% certification and testing market share in 2025 and is projected to advance at a 4.42% CAGR through 2031.

- By end-user vertical, the food and healthcare sectors held 28.15% of the certification and testing market size in 2025, while the transportation sector is expected to expand at a 5.28% CAGR through 2031.

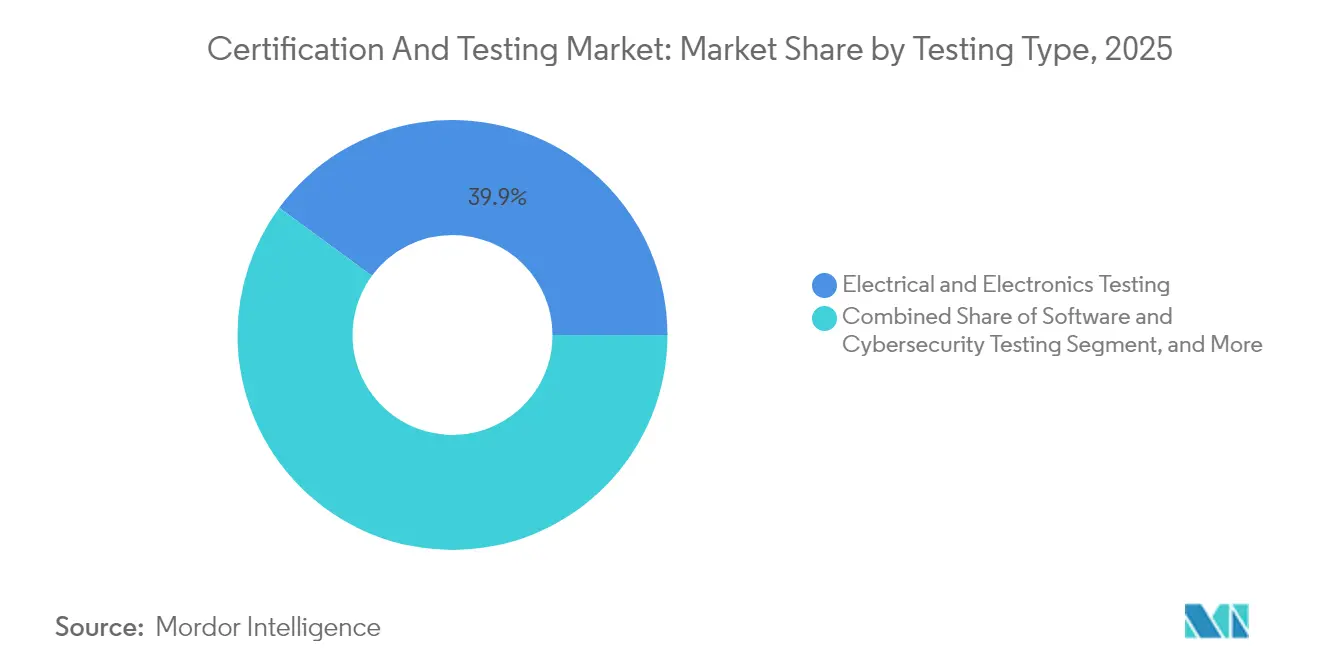

- By testing type, electrical and electronics testing led with 39.92% share of the certification and testing market in 2025. However, software and cybersecurity testing are projected to expand at a 5.03% CAGR between 2026 and 2031.

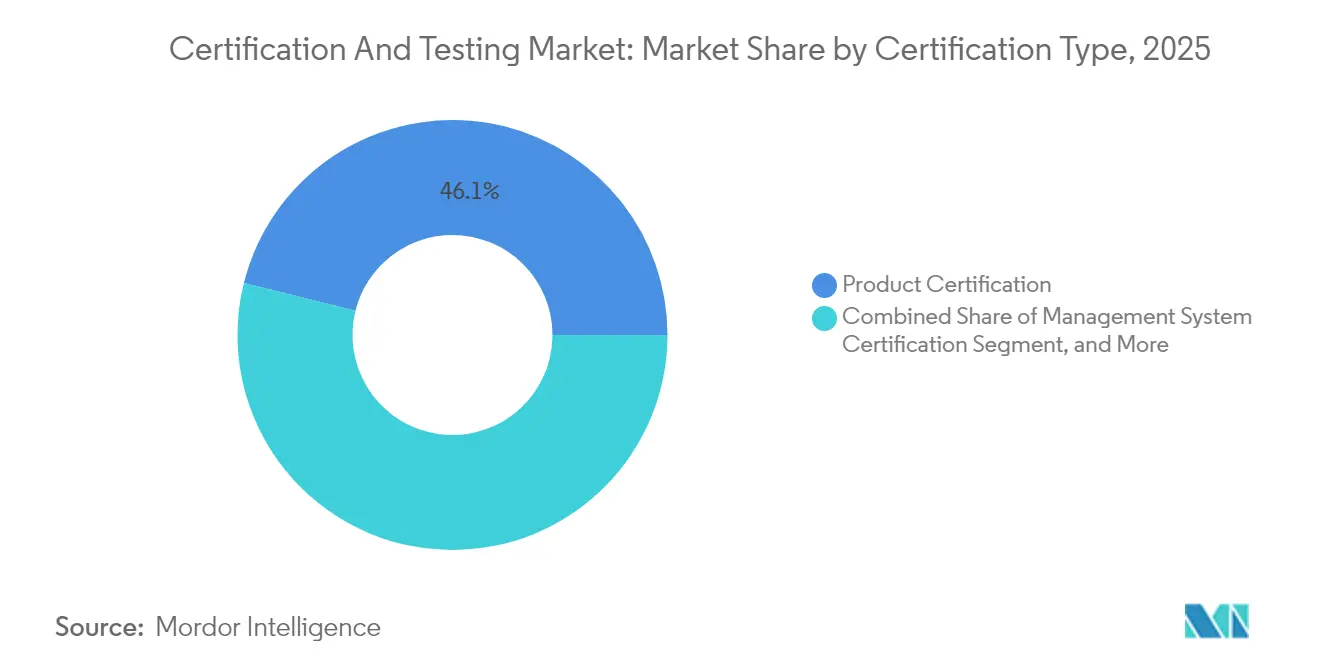

- By certification type, management system certification accounted for the fastest growth, recording a 5.62% CAGR versus product certification’s 3.41% baseline.

- By service type, testing services represented 52.31% of 2025 revenue, while certification services are projected to rise at a 4.69% CAGR through 2031.

- By geography, Asia-Pacific generated 39.88% of 2025 revenue and is forecast to grow at a 4.21% CAGR, nearly double the global pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Certification And Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Global Trade Compliance Mandates | +0.9% | Global, concentrated in North America, EU, APAC export hubs | Medium term (2-4 years) |

| Rapid Expansion of Cross-Border E-Commerce | +0.7% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Proliferation of IoT and Smart Devices | +0.6% | Global, early adoption in North America, EU, East Asia | Medium term (2-4 years) |

| Rising Focus on Product Safety and Quality | +0.5% | Global, especially North America, EU, Japan | Long term (≥ 4 years) |

| Growing Adoption of Digital Twin-Based Remote Certification | +0.4% | North America and EU, gradual APAC uptake | Long term (≥ 4 years) |

| Emergence of Sustainability-Linked Certification Schemes | +0.3% | EU leading, followed by North America and select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Global Trade Compliance Mandates

Governments continue to tighten origin-verification and conformity documentation. The World Customs Organization issued digital certificate guidelines in 2024, prompting exporters to provide accredited laboratory data that matches treaty annexes.[1] World Customs Organization, “Guidelines on Certificates of Origin,” Wcoomd.org The EU’s Registered Exporter scheme now requires ISO 17025 test reports on select goods, doubling certification queues from Southeast Asian suppliers since mid-2024.[2]European Commission, “Registered Exporter System,” Trade.ec.europa.eu The United States added third-party test evidence for dual-use items under updated Export Administration Regulations. Large multi-accredited labs, therefore, win volume as their certificates travel globally, while regional providers rush to secure International Accreditation Forum recognition.

Rapid Expansion of Cross-Border E-Commerce

Major marketplaces have imposed stricter pre-listing protocols. Amazon requires ISO 17025 reports for electronics, toys, and personal-care items in the United States, the EU, and Japan, thereby excluding untested goods.[3]U.S. Department of Commerce, “Export Administration Regulations,” Bis.doc.gov Alibaba’s Tmall Global auto-delists products lacking FCC, CE, or CCC marks, resulting in a 40% surge in certification inquiries from Chinese exporters in 2024. The EU Digital Services Act makes platforms jointly liable for unsafe products, reinforcing these rules. Smaller brands, therefore, outsource compliance work to external labs, accelerating the shift toward asset-light operations in the certification and testing market.

Proliferation of IoT and Smart Devices Requiring Certification

Connected products face a range of tests, including layered radio, cybersecurity, and privacy assessments. NIST finalized the 8259 series in 2024 for federal IoT procurements. Europe followed with ETSI EN 303 645, now a harmonized Radio Equipment Directive standard that mandates secure boot and encrypted communication for consumer IoT. Certification cycles can stretch three to six months for non-compliant designs, prompting a rush to security-ready chipsets. PSA Certified logged more than 200 approvals by end-2024, signaling pre-silicon convergence. Labs with deep cybersecurity benches, therefore, gain share as device counts climb.

Rising Focus on Product Safety and Quality Among Consumers

Social media amplifies recalls, driving brands toward voluntary marks that exceed statutory minimums. The Global Food Safety Initiative recorded 400 new scheme adoptions in 2024, led by FSSC 22000 and SQF. Europe’s Medical Device Regulation expanded audits to many Class I devices, resulting in a tripling of testing backlogs in Germany and the Netherlands. UL Solutions launched a voluntary smart-home cybersecurity seal in 2024, with adopters reporting double-digit price premiums in North American retail channels. As quality credentials become marketing levers, demand rises beyond mandatory compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Industrial Capex Cycles | -0.5% | Global, large swings in APAC and North America manufacturing hubs | Short term (≤ 2 years) |

| Complex and Fragmented Regulatory Standards | -0.4% | Global, most acute for multi-jurisdiction exporters | Medium term (2-4 years) |

| Talent Shortage in Specialized Disciplines | -0.3% | Global, acute in North America and EU | Medium term (2-4 years) |

| Cybersecurity Concerns Over Remote Platforms | -0.2% | Global, heightened in regulated sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Industrial Capex Cycles

Testing volume tracks new-product launches and plant startups. India’s statistical office documented a 66.3% increase in private-sector capital expenditure (capex) between fiscal 2021-22 and 2024-25, temporarily boosting laboratory demand. When global PMI indices dipped in Q2 2024, certification queues thinned within two quarters, leaving spare capacity. In-house labs feel the squeeze more acutely because they carry fixed overhead, which hastens the move to outsourcing. Regional providers often cut prices during downturns, squeezing margins across the certification and testing market.

Complex and Fragmented Regulatory Standards Across Regions

Despite harmonization efforts, duplicate testing continues to persist. China’s CCC scheme covers 17 product groups, yet it seldom accepts foreign test results, forcing re-tests in CNCA-approved labs. India’s BIS extension to electronics and telecom equipment introduced similar hurdles, as few bilateral agreements exist. In the Middle East, SASO and ESMA run overlapping but non-identical programs, adding weeks to product launches. Compliance costs thus rise 20-30% for global rollouts, restraining growth for resource-constrained exporters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sourcing Type: Outsourcing Extends Its Lead

Outsourced providers controlled 63.98% certification and testing market share in 2025 and will climb at a 4.42% CAGR through 2031, well above the headline rate. This dominance stems from the significant investment required to keep ISO 17025 labs current, a cost that most manufacturers now treat as variable rather than fixed. UL Solutions’ 8.1% revenue jump in Q3 2024 demonstrates how large networks capture flows as clients exit captive facilities.

Hybrid models still matter. Pharmaceutical and semiconductor firms maintain in-house labs to protect IP, yet 60% now outsource at least 30% of test volume, chiefly for peak loads or niche disciplines. Digital-twin standards under ISO 23247 could blur boundaries further by allowing internal simulation to screen designs before external confirmation. Overall, outsourced specialists set the pace, and their scale unlocks the analytics and automation budgets required to maintain high efficiency in the certification and testing market.

By End-User Vertical: Transportation Surges Ahead

Food and healthcare accounted for 28.15% of 2025 revenue, as the FDA FSMA Rule 204 and GFSI schemes tightened traceability and hygiene demands. The certification and testing market size for these verticals remains resilient because audits occur across planting, processing, and distribution.

Transportation, however, registers the fastest 5.28% CAGR. UN Regulations 155 and 156 compel cybersecurity and software-update audits for every new vehicle type sold in the EU and Japan, expanding laboratory pipelines for penetration tests and over-the-air update validation. IATF 16949 certifications increased by 12% in 2024, indicating a cascading pressure on supply chains. Battery safety work adds another layer, with Intertek and UL constructing dedicated centers to meet UN 38.3 and IEC 62133 demands. As electrification and autonomy advance, transportation becomes the primary driver of growth within the certification and testing market.

By Certification Type: Management Systems Gain Momentum

Product marks still represented 46.12% of 2025 turnover, reflecting their gatekeeper role in CE, CCC, and FCC approvals. Yet management system audits are the growth engine, advancing at 5.62% CAGR as firms seek ISO 9001, ISO 14001, ISO 45001, and ISO 27001 credentials to satisfy ESG-minded investors. ISO 27001:2022 attracted a 25% jump in new sign-ups after addressing cloud and AI governance.

Integrated audits now combine multiple standards under a single cycle, reducing downtime and costs for mid-sized firms. Service certification and personnel qualification remain smaller but steady contributors. The International Accreditation Forum’s mutual recognition arrangement, covering over 100 economies, eases global acceptance of management certificates, helping to widen the market size for certificates and testing in this category.

By Service Type: Certification Margins Outperform Testing

Testing accounted for 52.31% of 2025 revenue, largely due to its equipment-intensive nature. Still, certification services log a 4.69% CAGR through 2031, slightly ahead of the market, because bundled audits spread cost across multiple standards and deepen client lock-in.

Commodity tests such as textile flammability face price erosion, but high-skill niches 5G electromagnetic compatibility, battery thermal-runaway modeling, and IoT penetration tests command premium rates. Remote auditing cuts travel time 40% under ISO 27001 safeguards, while digital-twin validation halves prototype cycles under ISO 23247. Large providers absorb the software spend required to deliver these tools, reinforcing their edge in the certification and testing market.

By Testing Type: Electrical and Electronics Dominate as Cybersecurity Accelerates

Electrical and electronics testing accounted for 39.92% of the certification and testing market size in 2025, the highest market share among all testing categories. Mandatory safety marks such as UL, CE, CCC, and PSE make this service a non-negotiable gatekeeper for global product launches, driving a steady stream of high-volume work. SGS added new anechoic chambers to its Munich laboratory in May 2024 to handle 5G and IoT electromagnetic-compatibility loads, underscoring its sustained capital commitments to this core segment. Electrical and electronics testing also benefits from adjacent demand in environmental, mechanical, and chemical evaluations, because batteries, power supplies, and printed circuit boards must clear performance, endurance, and restricted-substance screens before reaching the market.

Software and cybersecurity testing is the fastest-growing category, advancing at a 5.03% CAGR between 2026 and 2031. UN Regulations 155 and 156 require every new vehicle type sold in the EU and Japan to undergo penetration and software update validation, shifting new volume toward specialized cyber labs. DEKRA’s Stuttgart cybersecurity center, opened in March 2024, performs vulnerability assessments and ISO 27001 audits for automotive and industrial clients, illustrating how providers build dedicated capacity for this frontier service. In the United States, the NIST 8259 framework and CTIA’s annual certification program extend similar pressure to IoT handsets and wearables, ensuring recurring demand for third-party validation.

Geography Analysis

Asia-Pacific contributed 39.88% of 2025 turnover and is advancing at a 4.21% CAGR, almost double the global clip. China’s widened CCC catalog now spans chargers and industrial robots, lifting local laboratory volume 15% year-over-year. India’s BIS move into electronics and telecom equipment created processing backlogs and spurred capacity additions in Bangalore and Pune.

North America expands near the market average. FCC equipment authorization and OSHA safety marks remain evergreen requirements, while Inflation Reduction Act incentives for batteries introduce new test categories. Canada’s Standards Council upholds ISO 17025 accreditation, sustaining cross-border equivalence.

Europe exhibits steady demand under CE marking rules, although Brexit necessitates dual certification for suppliers selling into both the EU and the United Kingdom. The Middle East is tightening rules as Saudi Arabia’s SASO and the UAE’s ESMA implement distinct conformity assessment schemes, creating parallel pathways that lengthen launch cycles. South America and Africa remain modest contributors, yet Brazil’s INMETRO and South Africa’s SABS are expanding lists of compulsory items, hinting at gradual upside.

Competitive Landscape

The top players include SGS, Intertek, Bureau Veritas, DEKRA, and TÜV SÜD. The strategy revolves around adding accredited scope, expanding the geographic reach, and digitizing workflows. UL Solutions deployed AI-assisted textile defect detection in 2024 and opened a 50,000-square-foot Fire Science Center in 2025 to address bottlenecks in battery and EV infrastructure. SGS expanded its Munich EMC capacity for 5G and IoT equipment. while Bureau Veritas rolled out an AI-enhanced remote audit portal that trims certification cycles to 10 days.

White-space opportunities lie in cybersecurity for IoT, sustainability-linked claims, and digital-twin validation. MET Laboratories focuses on battery testing from U.S. hubs, and Element Materials Technology serves aerospace composites near production clusters.

Merger activity is modest because relationship networks and asset intensity limit scale synergies, so leaders pursue tuck-in buys and greenfield labs instead. The competitive dynamic should persist as the certification and testing market rewards providers that marry multi-standard scope with fast, transparent digital delivery.

Certification And Testing Industry Leaders

Intertek Group plc

Bureau Veritas S.A.

Underwriters Laboratories (UL)

SGS S.A.

Eurofins Scientific SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UL Solutions inaugurated a 30,000 square-foot IoT and connectivity laboratory in Songshan Lake, China, equipped for 5G emulation and penetration tests.

- February 2025: UL Solutions opened a 50,000 square-foot Fire Science Center in Northbrook, Illinois, to serve battery energy storage and EV charging projects.

- August 2024: TÜV SÜD introduced a sustainability certification service for construction materials aligned with the EU Taxonomy Regulation.

- June 2024: DNV launched a digital-twin validation service for offshore wind turbines under ISO 23247 frameworks.

Global Certification And Testing Market Report Scope

Certification and testing are the regular procedures by which an accredited or approved person or agency evaluates and verifies (and attests in writing by issuing a certificate) the properties, features, quality, requirements, or status of individuals or corporations, procedures or processes, goods or services, or events or situations, in accordance with authorized requirements or standards.

The Certification and Testing Market Report is Segmented by Sourcing Type (In-House, and Outsourced), End-User Vertical (Construction and Engineering, Chemicals, Food and Healthcare, Energy and Commodities, Transportation, Products and Retail, Industrial, Other End-User Verticals), Testing Type (Mechanical, Electrical and Electronics, Chemical, Environmental and Climatic, NDT, EMC and Radio, Software and Cybersecurity), Certification Type (Product, Management System, Personnel, and Service), Service Type (Testing, and Certification), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| In-House |

| Outsourced |

| Construction and Engineering |

| Chemicals |

| Food and Healthcare |

| Energy and Commodities |

| Transportation |

| Products and Retail |

| Industrial |

| Other End-User Verticals |

| Mechanical Testing |

| Electrical and Electronics Testing |

| Chemical Testing |

| Environmental and Climatic Testing |

| Non-Destructive Testing (NDT) |

| EMC and Radio Testing |

| Software and Cybersecurity Testing |

| Product Certification |

| Management System Certification |

| Personnel Certification |

| Service Certification |

| Testing |

| Certification |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Sourcing Type | In-House | ||

| Outsourced | |||

| By End-User Vertical | Construction and Engineering | ||

| Chemicals | |||

| Food and Healthcare | |||

| Energy and Commodities | |||

| Transportation | |||

| Products and Retail | |||

| Industrial | |||

| Other End-User Verticals | |||

| By Testing Type | Mechanical Testing | ||

| Electrical and Electronics Testing | |||

| Chemical Testing | |||

| Environmental and Climatic Testing | |||

| Non-Destructive Testing (NDT) | |||

| EMC and Radio Testing | |||

| Software and Cybersecurity Testing | |||

| By Certification Type | Product Certification | ||

| Management System Certification | |||

| Personnel Certification | |||

| Service Certification | |||

| By Service Type | Testing | ||

| Certification | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current global value of the certification and testing market?

The certification and testing market size is USD 218.04 billion in 2026 and should reach USD 262.84 billion by 2031.

Which region grows fastest in certification and testing through 2031?

Asia-Pacific leads with a 4.21% CAGR, driven by China’s wider CCC scope and India’s BIS expansion.

Why are management system audits expanding more quickly than product marks?

Enterprises pursue integrated ISO 9001, ISO 14001, ISO 45001, and ISO 27001 certificates to meet ESG and cybersecurity demands, raising management system audit demand at a 5.62% CAGR.

How large is outsourced participation in certification and testing?

Outsourced providers ran 63.98% of the global compliance workload in 2025, and their share is still climbing.

Which end-user vertical is set to grow the fastest?

Transportation posts a 5.28% CAGR to 2031 due to UN cybersecurity and software-update regulations for new vehicles.

What factors restrain market growth despite rising compliance needs?

Industrial capex volatility and fragmented regional rules impose cost and timing hurdles that subtract up to 0.9 percentage points from forecast CAGR.

Page last updated on: