Food And Agriculture Testing, Inspection, And Certification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

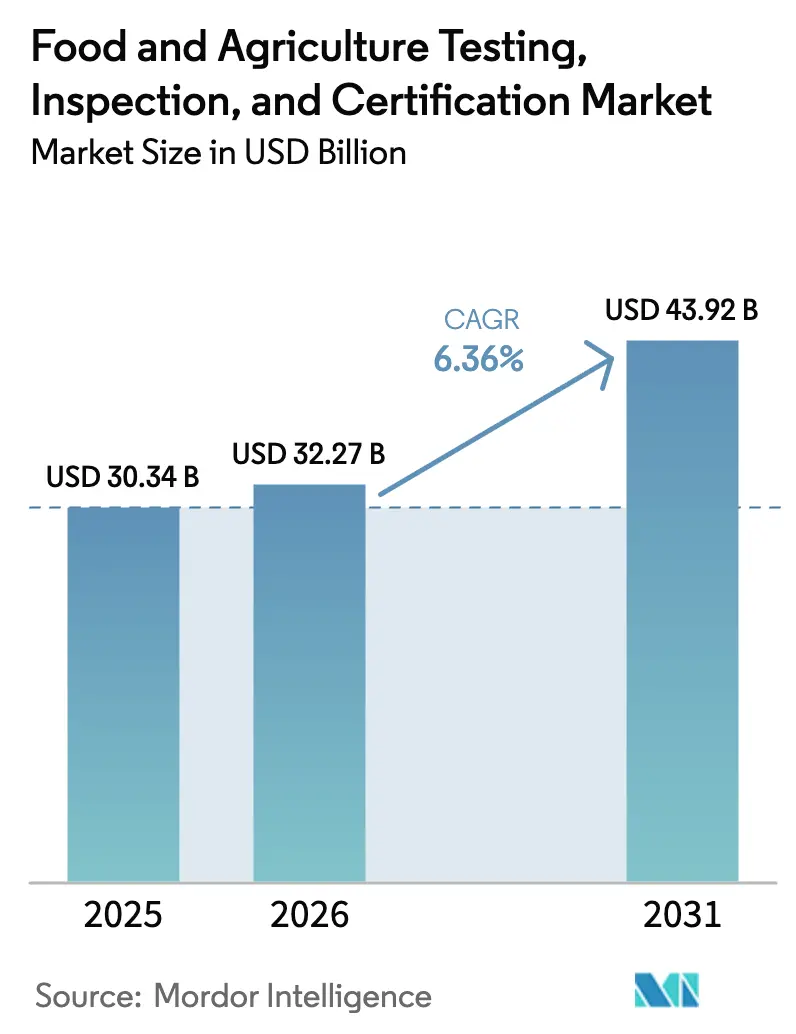

| Market Size (2026) | USD 32.27 Billion |

| Market Size (2031) | USD 43.92 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food And Agriculture Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The food and agriculture testing, inspection, and certification market size is expected to grow from USD 30.34 billion in 2025 to USD 32.27 billion in 2026 and is forecast to reach USD 43.92 billion by 2031 at 6.36% CAGR over 2026-2031. Heightened regulatory scrutiny, rapid expansion of cross-border food trade, and the shift toward outsourced compliance verification propel this upward trajectory. Demand remains resilient because testing and certification are legal requirements rather than discretionary quality upgrades. Advances in artificial intelligence and blockchain strengthen predictive risk profiling and traceability, enabling faster detection of contaminants and tighter supply-chain oversight. Consolidation among third-party laboratories continues as players scale analytical capacity, pursue multi-standard accreditations, and invest in next-generation sequencing and LC-MS/MS platforms.

Key Report Takeaways

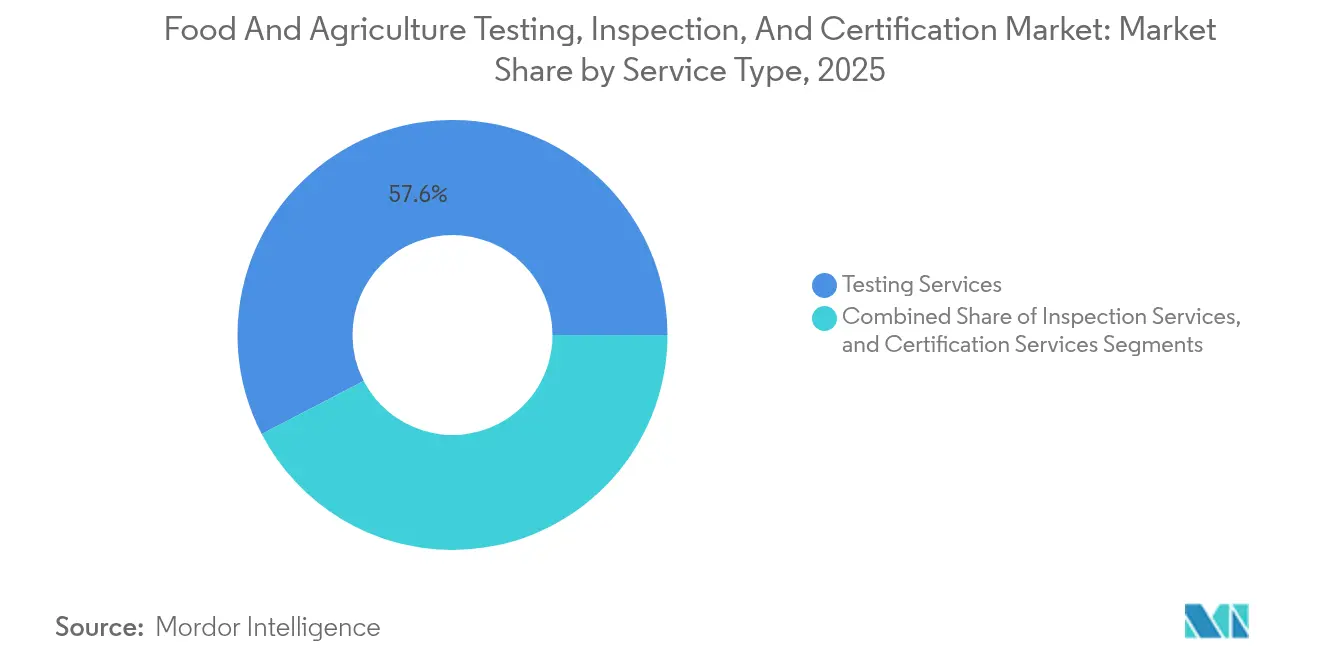

- By service type, testing services commanded 57.62% of the food and agriculture testing, inspection, and certification market share in 2025; certification services are forecast to expand at a 6.72% CAGR through 2031.

- By sourcing type, outsourced providers accounted for 72.34% of 2025 revenue; this channel is expected to grow at a 6.62% CAGR through 2031.

- By geography, Asia-Pacific held 43.12% of 2025 revenue and is projected to grow at a 6.98% CAGR through 2031, the highest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food And Agriculture Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing stringency of global food-safety regulations | +1.8% | Global, with the strongest impact in North America and the EU | Medium term (2-4 years) |

| Rising cross-border agri-food trade volumes | +1.2% | Asia-Pacific core, spill-over to MEA and Americas | Long term (≥ 4 years) |

| Expansion of retail private-label food brands | +0.9% | North America and the EU primarily, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Consolidation of third-party laboratories | +0.7% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| AI-driven predictive risk profiling of farms | +0.5% | North America and the EU are early adoption, and Asia-Pacific is following. | Long term (≥ 4 years) |

| Blockchain-enabled end-to-end traceability mandates | +0.4% | EU leading, North America and Asia-Pacific gradual adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing stringency of global food-safety regulations

The United States FSMA LAAF program became fully operational in 2024 and requires laboratories to secure specific accreditations for designated analyses, increasing compliance costs and pushing food companies toward accredited third-party providers.[1]U.S. Food and Drug Administration, “Laboratory Accreditation for Analyses of Foods (LAAF) Program,” fda.gov Comparable tightening is visible in the European Union, where EFSA broadens risk-assessment frameworks and enforces stricter maximum residue limits, thereby expanding mandatory test panels. ISO 22000 and GFSI-benchmarked schemes such as BRCGS, IFS, and FSSC 22000 reduce regulatory fragmentation, yet they simultaneously elevate the minimum technical bar. As a result, smaller producers that once relied on basic in-house tests must now outsource more complex analyses, enlarging the food safety testing, inspection, and certification market. The requirement for multi-standard compliance turns safety verification into a fixed operating expense, insulating spending from normal economic cycles. Consolidated laboratory networks leverage their accreditation breadth to win long-term contracts and secure price premiums.

Rising cross-border agri-food trade volumes

Global food trade exposes single shipments to multiple regulatory regimes, multiplying the number of required assays per product. An exporter shipping processed seafood from Vietnam to the European Union must satisfy origin and destination pesticide, heavy-metal, microbiological, and labeling standards in parallel, creating incremental testing demand.[2]Baker McKenzie, “Asia-Pacific Food Law Guide 2024,” bakermckenzie.com Laboratories with multi-jurisdictional accreditations are well-positioned as exporters consolidate work with providers that deliver certificates accepted worldwide. Asia-Pacific anchors the growth because it is simultaneously a manufacturing base and a consumer market, leading to bidirectional flows that require verification at both ends. Mutual recognition agreements streamline some documentation yet paradoxically raise total assay counts by lowering barriers for smaller producers to reach new destinations. This dynamic sustains double-digit volume growth for regional laboratories, particularly in hubs such as Thailand and Vietnam.

Expansion of retail private-label food brands

Major retailers increasingly specify proprietary safety protocols, shifting responsibility for verification away from suppliers. Walmart, Carrefour, and Tesco require third-party confirmation that products meet brand-specific criteria, generating incremental test panels that go beyond statutory minima. Laboratories add value by bundling authenticity checks and supply-chain audits with classic pathogen and residue tests. Smaller manufacturers must navigate distinct retail requirements, often commissioning separate test programs for identical products. Retailers adopt blockchain QR codes that expose certification data to consumers at the point of sale, reinforcing transparency and consumer trust. As private-label penetration climbs in packaged foods, recurring testing volume expands, further enlarging the food safety testing, inspection, and certification market.

Consolidation of third-party laboratories

Mérieux NutriSciences acquired Bureau Veritas’ food testing business for EUR 360 million (USD 390 million) in January 2025, creating a network of more than 140 laboratories across 32 countries. Consolidated groups achieve economies of scale in accreditation maintenance, capital equipment utilization, and geographic reach. They can pool sample loads across facilities, introduce integrated data hubs, and negotiate higher volumes with equipment suppliers. Smaller labs face escalating capital requirements for advanced LC-MS/MS or next-generation sequencing platforms and therefore either specialize or seek acquisition. The concentration trend strengthens competitive moats for large incumbents and accelerates the shift to outsourced models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented compliance regimes across emerging markets | -0.8% | Emerging markets in Asia-Pacific, MEA, and Latin America | Medium term (2-4 years) |

| High cost of multi-standard accreditations for SMEs | -0.6% | Global, particularly affecting developing economies | Short term (≤ 2 years) |

| Shortage of qualified food toxicologists and auditors | -0.4% | Global, most acute in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Climate-driven volatility in sampling representativeness | -0.3% | Global, with regional variations in severity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented compliance regimes across emerging markets

Country-specific rules in emerging economies diverge from international standards, forcing exporters to navigate overlapping and sometimes conflicting test requirements. Vietnam and Nigeria, for example, introduced new residue limits and certification frameworks that are not yet harmonized with GFSI schemes, driving repeat sampling and duplicate documentation. Laboratories must maintain multiple accreditations, raising operating costs and lengthening turnaround times. Food companies adjust by limiting product lines or avoiding certain destinations, temporarily suppressing testing growth in those corridors until regulatory alignment improves.

High cost of multi-standard accreditations for SMEs

Securing ISO 17025 plus programs such as FSSC 22000 often requires initial outlays above USD 100,000 and recurring expenses near USD 50,000 per year, levels that strain the budgets of smaller processors and regional laboratories. Without accreditation, SMEs cannot access premium export channels, curbing the volume of outsourced work they generate. The financial hurdle is most acute in developing regions where profit margins are slim and credit availability is limited. While collaborative initiatives such as bioMérieux’s Trusted Third Party reduce some data costs, they do not eliminate upfront accreditation fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Services Lead Despite Certification Growth

Testing Services accounted for 57.62% of the food and agriculture testing, inspection, and certification market in 2025, reflecting mandated pathogen, chemical residue, and nutritional analyses that every producer must complete. Certification Services grow faster at a 6.72% CAGR because brands use third-party stamps to differentiate on supermarket shelves. Inspection Services remain a smaller component, constrained by labor intensity yet indispensable for facility audits and process validation. Within Testing Services, demand for next-generation sequencing and LC-MS/MS drives premium pricing, while integrated data portals such as SGS SMART support value-added analytics. Over the forecast period, convergence between testing and certification will create bundled compliance solutions that lock in recurring revenue streams for providers.

Testing Services retain a critical mass because every new regulation, from allergen cross-contact thresholds to microplastic contamination limits, lengthens the assay checklist. Certification’s momentum stems from private-label retailers seeking consumer-visible assurances. Laboratories that invest in both categories can cross-sell, secure long contracts, and maintain utilization rates above 80%. SGS’s SMART illustrates how real-time dashboards integrate lab data and audit findings, establishing a single compliance narrative for clients. This end-to-end visibility reinforces the importance of outsourcing to large, tech-enabled providers.

By Sourcing Type: Outsourced Model Dominance Reflects Specialization Trends

Outsourced providers generated 72.34% of 2025 revenue and are set to expand at a 6.62% CAGR to 2031, cementing their lead. Complex regulations, rapid technology turnover, and high capital expenditure tilt the cost-benefit equation toward third-party labs except for the highest-throughput processors. In-house facilities survive where immediate line-release decisions are vital, yet even these plants outsource confirmatory tests for legal defensibility. The Trusted Third Party program launched by bioMérieux and Mérieux NutriSciences illustrates the network advantages of the outsourced model: pooled anonymized data generates supplier risk scores unavailable to isolated labs.

Companies discover that outsourcing not only supplies accredited results but also reduces liability because responsibility transfers to the certifier. Large laboratories further sweeten the proposition by offering subscription plans that bundle routine assays, unannounced audits, and traceability dashboards. As cross-border trade intensifies, producers prefer single points of service that carry global accreditations, a status unattainable for most in-house labs.

Geography Analysis

Asia-Pacific posted 43.12% of global revenue in 2025 and is forecast to grow at a 6.98% CAGR through 2031. China, India, and Southeast Asia expand both processing capacity and consumer demand, prompting investments in accredited laboratories. The Government of India funded 100 new NABL-accredited labs in the 2024 budget to support domestic safety oversight and export competitiveness. North America remains a center of regulatory innovation with the FDA’s LAAF program driving accreditation upgrades and increasing outsourced sample flows. Europe, while mature, shows steady demand for novel contaminant screening and premium certification services anchored on sustainability and animal-welfare criteria.

The Middle East and Africa represent the fastest emerging opportunity due to rising food imports and infrastructure development. The Philippines set up its first food quality lab in Cagayan Valley with PHP 5 million DOST funding to improve regional safety oversight. Countries in the Gulf Cooperation Council implement unified residue limits modeled on Codex Alimentarius, stimulating assay harmonization. Latin America benefits from soybean and meat export volumes that require multi-jurisdiction certificates, yet fragmented domestic regulations temper growth rates.

Regional comparison highlights divergent drivers. Asia-Pacific’s expansion originates from manufacturing scale and export orientation, whereas North America and Europe rely on stringent enforcement and private-label uptake. Africa’s growth is tied to donor-funded capacity building and import surveillance. Providers with global lab footprints and digital data networks can arbitrage these regional nuances and maintain high utilization.

Competitive Landscape

The top seven companies account for a majority of global revenue, indicating moderate concentration. SGS, Eurofins, Intertek, Bureau Veritas, and Mérieux NutriSciences compete on geographic coverage, accreditation scope, and technology adoption rather than on price. M&A remains the fastest route to capability expansion as demonstrated by Mérieux NutriSciences’ EUR 360 million purchase of Bureau Veritas’ food testing assets in 2025. Eurofins widened its U.S. footprint by opening a microbiology lab in Louisville, enabling faster turnaround times for regional processors.[4]Eurofins, “Signing of MOU between CDC and Eurofins,” eurofins.vnSGS strengthened its analytics suite by acquiring RTI Laboratories and 41% of Aster Global Environmental Solutions in January 2025.

Technology integration shapes the next competitive phase. SGS SMART delivers real-time dashboards that fuse lab data, blockchain traceability, and AI-powered risk alerts. Digital-native entrants deploy IoT sensors for continuous line monitoring, bypassing batch sampling cycles. Incumbents respond by partnering with sensor firms or integrating cloud platforms. Consolidation lowers unit costs for accreditation upkeep and accelerates innovation adoption, yet also raises regulatory scrutiny over market power.

White-space opportunities appear in novel food ingredient testing, cell-cultured protein verification, and carbon-footprint certification. Large incumbents allocate R&D budgets to these niches while forming alliances with start-ups. Competitive intensity stays moderate because accreditation and audit credentials act as barriers; nonetheless, digitally enabled challengers can win share in rapid growing niches.

Food And Agriculture Testing, Inspection, And Certification Industry Leaders

Bureau Veritas SA

SGS SA

Intertek Group Plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Eurofins opened a microbiology laboratory in Louisville, Kentucky, expanding North American capacity.

- February 2025: Eurofins Vietnam signed an MOU with Community Development Company to strengthen local compliance services.

- January 2025: Mérieux NutriSciences completed the EUR 360 million (USD 390 million) purchase of Bureau Veritas’ food testing business.

- January 2025: SGS acquired 78% of RTI Laboratories and 41% of Aster Global Environmental Solutions.

Global Food And Agriculture Testing, Inspection, And Certification Market Report Scope

The Testing, Inspection, and Certification (TIC) services help improve the standards of agricultural and packaged food products, along with related manufacturing processes, by conducting tests, inspections, and certifications by global regulations. This allows the companies operating in the agricultural & food industry to produce quality and safe products.

The scope of the study includes a detailed analysis of TIC services in the agricultural and food sectors. The study analyzes factors, such as market characteristics and growth trends of the Agriculture Food Testing, Inspection, and Certification industry, based on segments by Service Type (Testing and Inspection Service, Certification Service), Sourcing Type (Outsourced, In-House), and Geography. The report also includes an analysis of the impact of COVID-19 on the industry. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the food and agriculture testing, inspection, and certification market in 2026?

It is valued at USD 32.27 billion in 2026, with a projected 6.36% CAGR to 2031.

Which region leads revenue today?

Asia-Pacific generated 43.12% of 2025 revenue and is also the fastest-growing at 6.98% CAGR.

What segment shows the quickest growth?

Certification Services are forecast to expand at a 6.72% CAGR through 2031 as brands leverage third-party verification.

Why do companies favor outsourced testing?

Outsourcing offers broader accreditations, specialized expertise, and lower per-sample costs than maintaining in-house labs.

What technologies influence future demand?

Artificial intelligence, blockchain traceability, next-generation sequencing, and LC-MS/MS drive accuracy and speed, expanding testing scope.

Page last updated on: