Size and Share of Testing, Inspection, And Certification Market For The Transportation Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

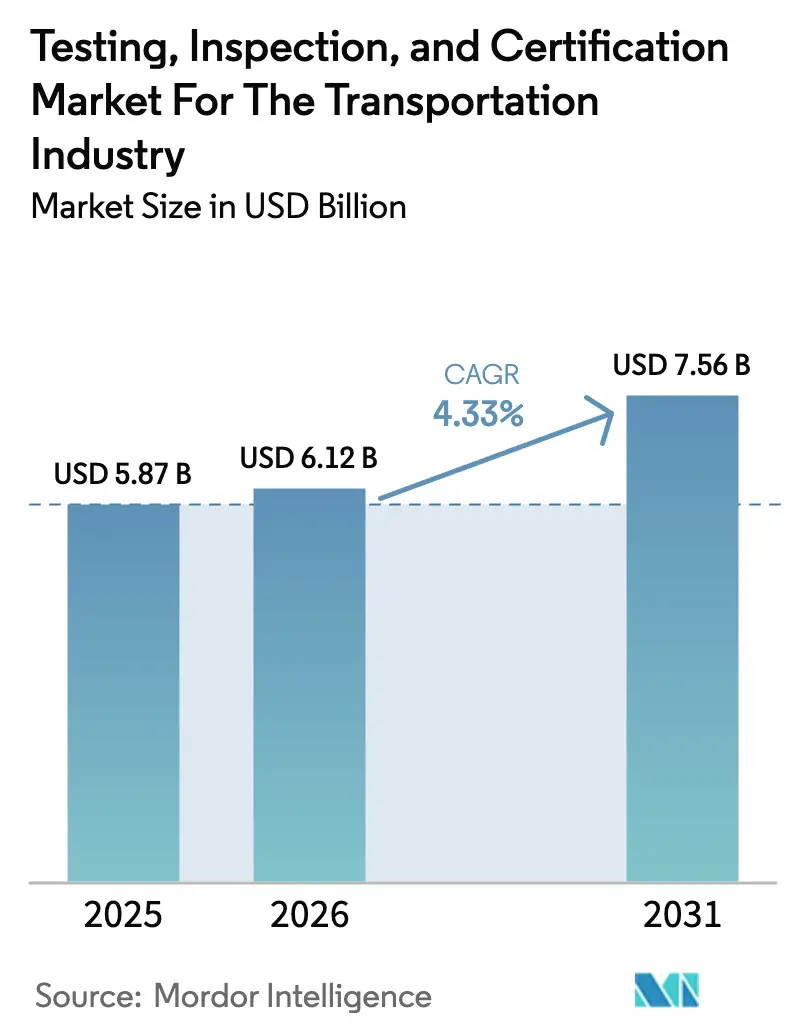

| Market Size (2026) | USD 6.12 Billion |

| Market Size (2031) | USD 7.56 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

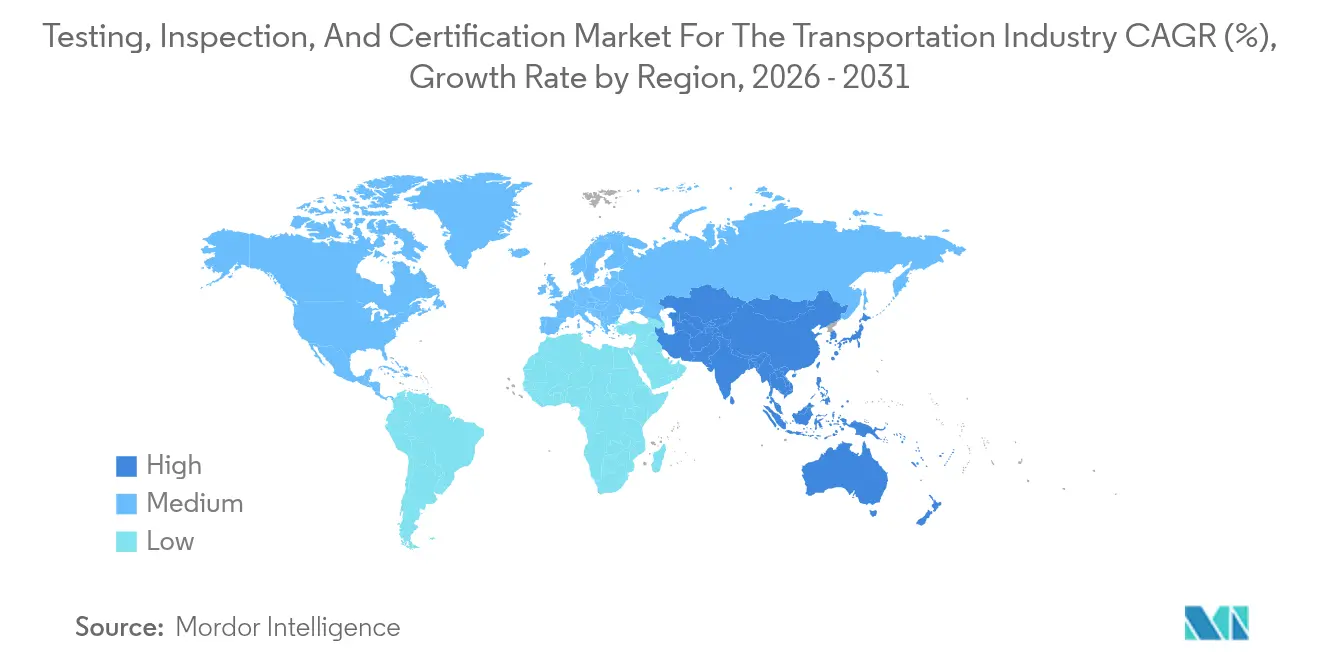

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

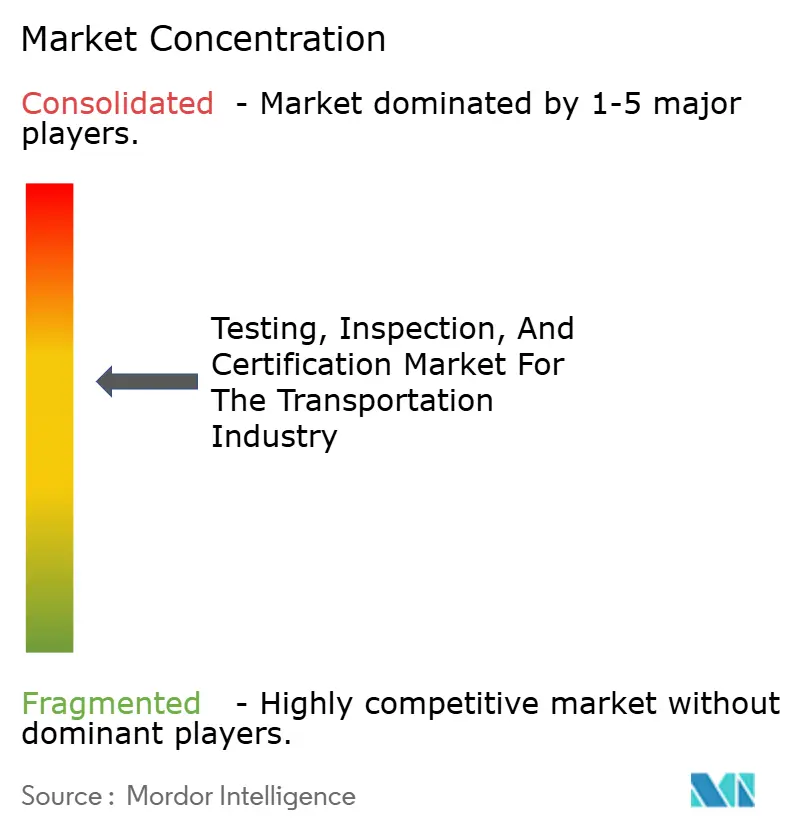

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Testing, Inspection, And Certification Market For The Transportation Industry by Mordor Intelligence

The testing, inspection, and certification market size for the transportation industry was valued at USD 5.87 billion in 2025 and estimated to grow from USD 6.12 billion in 2026 to reach USD 7.56 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031). Growing regulatory alignment, rapid electrification, and the emergence of data-rich validation technologies are reshaping how mobility stakeholders pursue compliance. The transition from discrete mechanical checks to fully digital validation suites now encompasses battery safety, autonomous driving algorithms, and cybersecurity for connected vehicles. Regulatory convergence, emphasized by the European Union’s Euro 7 standards and China’s updated GB series, continues to provide a durable demand floor, even during cyclical fluctuations in vehicle production. Asia-Pacific held the leading 39.6% revenue share in 2024, propelled by China’s zero-emission targets and India’s Bharat NCAP 2.0 rollout, and the region is projected to compound at 5.4% through 2030. Testing services accounted for 59.4% of 2024 spending, while certification services are expanding at the fastest rate, with a 5.1% CAGR, illustrating a shift toward outcome-based validation. Outsourced models already capture a 66.5% share and are expected to expand at a 4.8% CAGR as automakers and fleet operators focus on core engineering while delegating compliance to specialized partners. Consolidation pressures persist most visibly in the proposed SGS-Bureau Veritas merger, but moderate concentration (top four at 20-25% of revenue) still leaves room for regional and digital-native disruptors.

Key Report Takeaways

- By service type, testing services led with 58.92% revenue share of the testing, inspection, and certification market for the transportation industry in 2025; certification services are set to grow at a 4.88% CAGR through 2031.

- By sourcing type, the outsourced segment accounted for 65.82% of the testing, inspection, and certification market share in the transportation industry in 2025, while recording the highest projected CAGR of 4.63% through 2031.

- By geography, the Asia-Pacific region captured 39.12% of the 2025 revenue of the testing, inspection, and certification market for the transportation industry and is projected to advance at a 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Testing, Inspection, And Certification Market For The Transportation Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory stringency for transportation safety and emissions | +1.2% | Global, with the EU and China leading implementation | Medium term (2-4 years) |

| Growth in global trade is boosting vehicle inspection demand | +0.8% | Global, concentrated in major shipping corridors | Long term (≥ 4 years) |

| Rapid adoption of EVs and autonomous vehicles needs new test protocols | +1.5% | Asia-Pacific core, spill-over to North America and the EU | Short term (≤ 2 years) |

| Aging transport infrastructure requires regular inspection | +0.6% | North America and the EU primarily | Long term (≥ 4 years) |

| Emergence of digital twins enabling continuous remote inspection | +0.7% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Rise of fleet-as-a-service models, outsourcing compliance | +0.9% | Urban centers globally, strongest in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Stringency For Transportation Safety And Emissions

Worldwide emissions and safety rules adopted in 2024 tightened compliance thresholds, notably Euro 7’s real-world emissions monitoring scheme and China’s GB 9743-2024 and GB 9744-2024 tire standards. The UN Economic Commission for Europe’s WP.29 forum accelerated harmonization so that manufacturers can certify across multiple jurisdictions via a single test suite.[1]UN Economic Commission for Europe, “World Forum for Harmonization of Vehicle Regulations,” unece.org Outcome-based metrics now dominate, letting laboratories design innovative test procedures that capture real-life duty cycles. Global uptake of ISO 26262 functional safety for autonomous driving raised demand for highly specialized validation-often priced at a premium because liability risk is significant.

Rapid Adoption Of EV And Autonomous Vehicles Needing New Test Protocols

UL 2580 revisions added thermal-runaway benchmarks, and ISO 6469 broadened its scope to solid-state batteries planned for release after 2027. Autonomous standards under SAE J3018 and ISO/TS 5083:2025 mandate multi-layered sensor, algorithm, and cybersecurity tests, lengthening validation cycles but driving higher revenue per project. Vehicle-to-grid interface testing became a standalone service line in 2024 as utilities demanded proof of bidirectional safety.

Emergence Of Digital Twins Enabling Continuous Remote Inspection

IoT-connected sensors feed virtual replicas that identify anomalies in near real time, cutting physical site visits by as much as 40% in early deployments from SGS.[2]SGS, “IoT-Enabled Remote Monitoring Services,” sgs.com Cloud data sharing lets regulators approve standardized certifications in days rather than weeks, while AI-assisted pattern detection speeds report turnaround and enhances accuracy. Remote inspection also supports sustainability goals by lowering travel-related emissions during compliance audits.

Rise Of Fleet-As-A-Service Models Outsourcing Compliance

Federal Motor Carrier Safety Administration updates in 2024 expanded inspection frequency for commercial fleets, prompting operators to adopt subscription-based compliance packages. Third-party testing partners assume regulatory risk and deliver predictable monthly costs, freeing logistics providers to focus on freight efficiency. Outcome-based contracts are emerging, shifting incentives toward continuous compliance rather than episodic checks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High compliance testing costs for SMEs | -0.8% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Fragmented regulatory frameworks across regions | -0.6% | Global, with the highest impact in cross-border operations | Long term (≥ 4 years) |

| AI-based self-diagnostics reducing third-party testing reliance | -0.5% | Developed markets initially, expanding globally | Long term (≥ 4 years) |

| Shortage of qualified NDT professionals | -0.7% | Global, most severe in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Compliance Testing Costs For SMEs

European Commission studies found that small suppliers now spend EUR 50,000-100,000 (USD 53,500-107,000) each year on vehicle testing, an outlay that strains working capital. Battery laboratories cost USD 2-5 million to build, raising entry barriers for new providers. Lengthy certification timelines lock up cash before product launch, forcing many SMEs to adopt collaborative or subscription models.

Shortage Of Qualified NDT Professionals

The American Society for Non-destructive Testing projects a 35,700-technician gap by 2030.[3]American Society for Nondestructive Testing, “NDT Workforce Shortage Analysis,” asnt.org Dual skill sets, mechanical methods, and digital diagnostics are scarce, and 18 to 24-month certification pathways cannot keep pace. Wage inflation of 8-12% annually compresses margins for service providers, particularly smaller firms that compete with aerospace and energy sectors for talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Services Lead While Certification Gains Momentum

Testing services generated the largest share, reflecting mandatory multi-stage validation from component to full-vehicle homologation. Within the testing, inspection, and certification market for the transportation industry size, testing captured 58.92% in 2025, thanks to battery abuse tests and ADAS verification. Certification, however, is set to accelerate at a 4.88% CAGR as outcome-based standards spur demand for digital certificates that regulators can audit remotely. The shift also boosts margins because ISO 26262 and ISO 21434 cybersecurity sign-offs command premium fees.

Inspection remains a steady but slower-growing line. Remote monitoring and automated camera systems cut repetitive physical checks, depressing growth relative to testing and certification. Providers are retooling inspection portfolios around exception-based models where algorithms flag only non-conforming vehicles for manual review, preserving relevance while controlling cost.

By Sourcing Type: Outsourcing Dominance Reflects Strategic Focus

The outsourced model captured 65.82% of 2025 revenue, underscoring industry preference to rent rather than own validation assets. Manufacturers gain rapid access to climatic chambers, shaker rigs, and cybersecurity labs without sinking capital. Fleet operators likewise employ subscription contracts that bundle periodic checks, incident investigations, and regulatory filings. This segment will outpace in-house facilities through 2031, growing 4.63% annually.

In-house laboratories persist at scale OEMs but are increasingly supplemented by external experts for niche areas such as over-the-air update security or V2X electromagnetic compatibility. Cross-border compliance complexities further favor outsourcing because global providers hold multi-jurisdictional accreditations, minimizing duplicate tests and speeding market entry.

Geography Analysis

Asia-Pacific dominated the testing, inspection, and certification market for the transportation industry in 2025, with 39.12% revenue, and is poised for the fastest 5.18% CAGR through 2031. China’s GB 38031-2020 battery safety and aggressive NEV quotas generate steady lab utilization, while India’s move toward advanced driver assistance system testing under Bharat NCAP 2.0 attracts foreign TIC investment. Japan and South Korea add high-value demand tied to solid-state batteries and autonomous shuttles, though their mature vehicle bases temper volume growth.

North America follows with stringent Federal Motor Vehicle Safety Standards and heightened emphasis on connected-car cybersecurity, creating specialty test demand at premium rates. U.S. fleet operators account for sizeable, outsourced inspection volumes after the 2024 FMCSA update tightened commercial vehicle oversight.

Europe remains robust, benefiting from WP.29 harmonization and the imminent Euro 7 rollout that necessitates real-world emissions verification. Laboratories there tout large capacity for portable emissions measurements and battery fire-containment tests that serve both domestic and trans-Atlantic manufacturers.

The Middle East and Africa, and South America are emerging theaters. Gulf Cooperation Council states are aligning rules with UN regulations, while Brazil’s domestic production base and Mercosur trading bloc encourage regional providers to scale. Currency volatility and infrastructure gaps still limit near-term penetration but offer a long-run upside as standards converge.

Competitive Landscape

Market concentration is moderate: SGS, Bureau Veritas, Intertek, and DEKRA account for a significant share of global revenue. The proposed SGS-Bureau Veritas merger, valued at USD 30-35 billion, seeks scale to fend off digital natives that offer AI-driven diagnostics and remote validation. Incumbents emphasize IoT monitoring, cloud analytics, and autonomous-vehicle simulation to differentiate.

Strategic investments include Bureau Veritas’s USD 25 million autonomous-vehicle test center in Michigan, Intertek’s ISO 26262 accreditation for self-driving systems, and DEKRA’s V2X partnership with chip manufacturers. Regional specialists such as Nordic Inspekt are expanding via acquisitions-Testpartner Gruppen for USD 4.6 million added battery abuse expertise and broadened Scandinavian reach.

White-space niches revolve around vehicle-to-grid certification, hydrogen fuel cell validation, and solid-state battery thermosafety. Providers holding ISO 17025 and ISO/IEC 17020 accreditations are better positioned because many regulators require these credentials before recognizing test results.

Leaders of Testing, Inspection, And Certification Market For The Transportation Industry

Bureau Veritas SA

Intertek Group PLC

SGS SA

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Intertek received ISO 26262 accreditation for autonomous vehicle safety testing.

- August 2024: TÜV SÜD rolled out mobile EV charger testing units for on-site validation.

- August 2024: SGS expanded IoT-enabled remote monitoring across Europe, reducing site visits by 40% while retaining ISO/IEC 17020 approval.

- July 2024: TCS launched a digital cockpit testing platform integrating cybersecurity and user-experience checks under ISO 21434.

Scope of Report on Testing, Inspection, And Certification Market For The Transportation Industry

The report on the Testing, Inspection, and Certification Market for the Transportation Industry segments the market by Service Type, including Testing, Inspection, and Certification Services. It also categorizes by Sourcing Type, distinguishing between In-House and Outsourced services. Geographically, the report spans North America (covering the United States., Canada, and Mexico), South America (including Brazil, Argentina, and others), Europe (with a focus on Germany, the United Kingdom, France, Italy, Spain, Russia, and more), Asia-Pacific (highlighting China, Japan, India, South Korea, Southeast Asia, and others), and the Middle East and Africa (featuring Saudi Arabia, the U.A.E., Turkey, and more). All market forecasts are presented in USD value.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the testing inspection and certification market for the transportation industry?

The market is valued at USD 6.12 billion in 2026 and is projected to reach USD 7.56 billion by 2031.

Which region generates the highest revenue?

Asia-Pacific leads with a 39.12% share in 2025 and is also the fastest-growing region.

Which service type is expanding most rapidly?

Certification services are forecast to post a 4.88% CAGR through 2031 as regulations move toward outcome-based compliance.

Why are companies shifting to outsourced testing?

Outsourcing lets manufacturers access specialized, multi-jurisdictional laboratories without heavy capital investment and supports fleet operators requiring continuous compliance.

How will electrification influence testing demand?

New battery safety, vehicle-to-grid, and autonomous driving protocols are lengthening validation cycles and increasing revenue per test engagement.

What challenges could slow market growth?

High compliance costs for SMEs and a shortage of qualified nondestructive testing professionals remain the key restraints.

Page last updated on: