Automotive TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.28 Billion |

| Market Size (2031) | USD 26.86 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

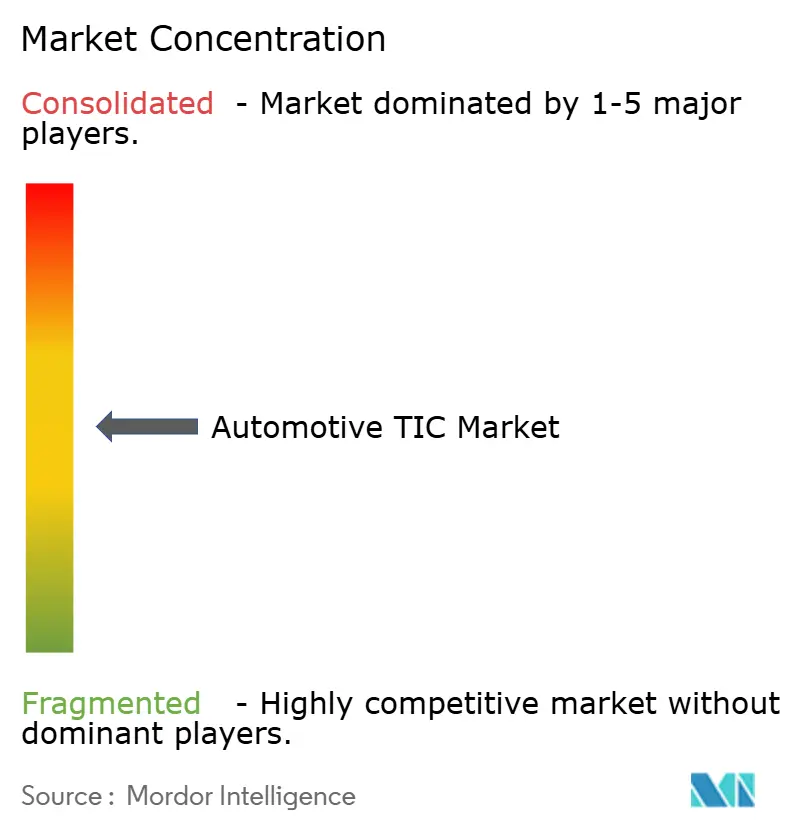

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive TIC Market Analysis by Mordor Intelligence

The automotive testing, inspection, and certification market size was valued at USD 20.31 billion in 2025 and estimated to grow from USD 21.28 billion in 2026 to reach USD 26.86 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). This expansion tracks the sector’s pivot from isolated mechanical evaluations toward end-to-end validation of software-defined vehicles, electrified powertrains, and connected-car ecosystems. Stricter UNECE R155 and R156 mandates have moved cybersecurity from single-event approval to continuous lifecycle oversight, creating stable demand for year-round compliance services. Providers able to blend physical testing with validated virtual simulations are capturing share as development cycles compress from 60–72 months to roughly 40 months. Outsourcing remains the dominant sourcing model because OEMs struggle to keep pace with the rising capital and talent requirements needed to test batteries, over-the-air (OTA) updates, and artificial-intelligence (AI) driving features.

Key Report Takeaways

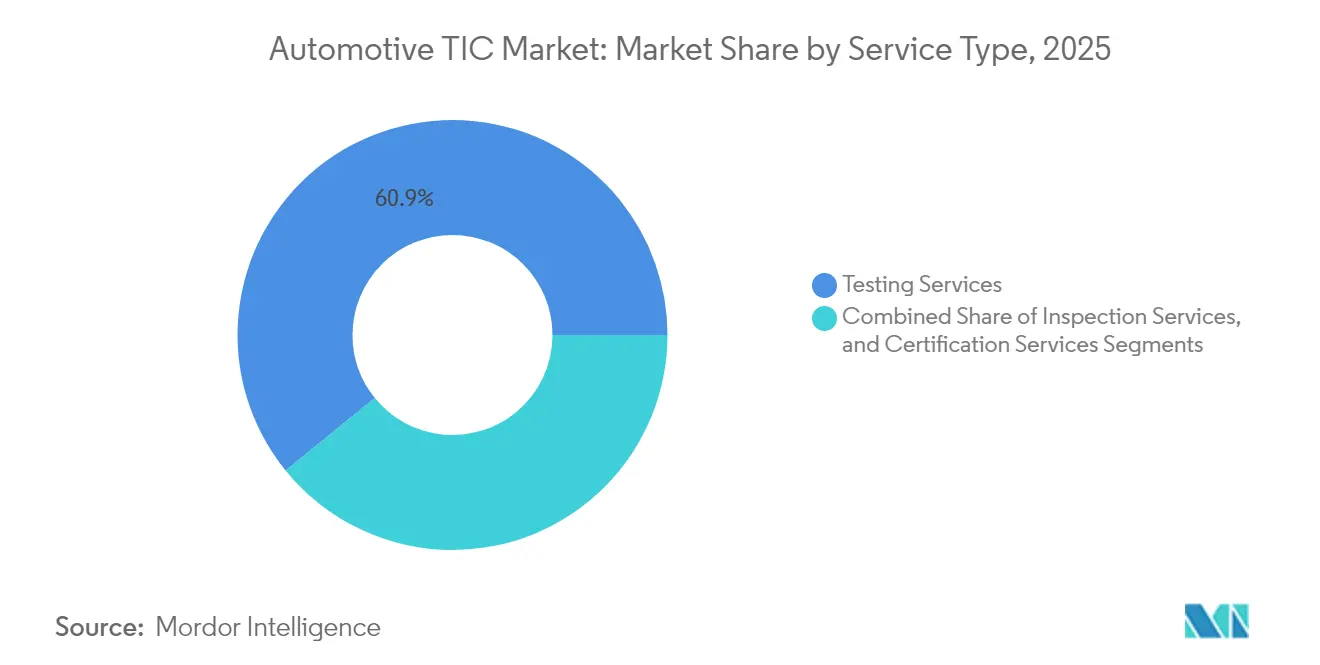

- By service type, testing accounted for 60.85% of the automotive testing, inspection, and certification market share in 2025, while certification is forecast to post the fastest 5.12% CAGR through 2031.

- By sourcing type, outsourced services commanded 74.62% of the automotive testing, inspection, and certification market size in 2025 and are projected to expand at a 4.83% CAGR to 2031.

- By geography, Asia-Pacific held 48.12% revenue share of the automotive testing, inspection, and certification market in 2025 and is set to register the highest 5.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive TIC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter UNECE and ISO Safety Mandates | +1.2% | Global, with the EU and Asia-Pacific leading implementation | Medium term (2-4 years) |

| Growing Outsourcing of Periodic Technical Inspection (PTI) | +0.8% | Europe and North America are primary, expanding to the Asia-Pacific | Short term (≤ 2 years) |

| Electrification Driving Battery and E-Powertrain Testing | +1.5% | Global, with China and the EU driving adoption | Long term (≥ 4 years) |

| Connected-Car Cyber-Security Compliance | +0.9% | North America and the EU core, spill-over to the Asia-Pacific | Medium term (2-4 years) |

| OTA Software-Update Validation Needs | +0.7% | Global, with premium segments leading | Short term (≤ 2 years) |

| Circular-Economy End-of-Life Certification | +0.4% | EU primary, expanding to developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter UNECE and ISO Safety Mandates

UNECE R155 and R156, mandatory for new vehicle types since July 2024, require demonstrable cybersecurity management throughout a vehicle’s lifespan. SGS enlarged its portfolio to include ISO/SAE 21434 training and Common-Criteria evaluations across Germany, the Netherlands, and Singapore, enabling OEMs to meet these continuous-compliance expectations.[1]SGS Integrated Report 2024, “Corporate Profile,” SGS, sgs.com ISO 24089 revisions published in 2024 added tougher automated-driving validation, forcing manufacturers to test sensor fusion, decision algorithms, and human-machine-interface (HMI) performance under a single audit umbrella. Semiconductor suppliers responded quickly; multiple chipmakers achieved ISO 26262 ASIL-D in 2024, proving functional-safety standards now permeate the full supply chain. As a result, providers that can deliver integrated hardware, software, and cybersecurity assessments are winning multi-year contracts tied to model-series refresh cycles.

Growing Outsourcing of Periodic Technical Inspection (PTI)

Governments increasingly delegate PTI activities to specialized firms to access advanced test benches and data analytics platforms without public-sector capital outlay. DEKRA secured 61% of inspection lines in Guadalajara, Mexico, showing how scale and reputation sway public tenders.[2]“DEKRA to Launch Mexican Vehicle Inspection Facilities,” Automotive Testing Technology International, automotivetestingtechnologyinternational.com New PTI scopes now cover brake-particle emissions, battery health, and even cybersecurity checks. Fragmented inspection intervals-some EU nations mandate 12-month cycles while others stretch to 48 months—create opportunities for providers adept at tailoring services to divergent rules. Digital inspection portals enabling real-time data transfer to regulators give large TIC firms an edge, reinforcing the outsourcing trajectory.

Electrification Driving Battery and E-Powertrain Testing

Battery validation has become the fastest-growing revenue stream as regulations now demand thermal-runaway, cycle-life, and recycling-readiness tests. Stellantis’ EUR 4.1 billion (USD 4.63 billion) joint venture with CATL for LFP cell production in Spain requires tiered testing—from single-cell abuse tests to pack-level durability—in both prototype and mass-production phases. Hofer Powertrain’s launch of battery-swelling analysis underscores how electrochemical nuances push TIC expertise past traditional automotive know-how. Providers equipped for electromagnetic-compatibility (EMC) tests, DC-fast-charge validation, and grid-interaction studies offer integrated “one-stop” electrification suites, securing long-term framework agreements with global OEMs.

Connected-Car Cyber-Security Compliance

Cybersecurity testing shifted from optional to compulsory once UNECE R155 took effect. ENX Vehicle Cybersecurity audits now standardize supplier assessments, cutting redundant checks yet raising the baseline competency bar. Keysight’s lab in the Netherlands won technical-service approval in 2024, enlarging the roster of accredited facilities that can certify vehicle software-update processes. V2X modules, cloud gateways, and OTA patch managers must all pass penetration tests before type approval, turning cybersecurity validation into a recurring revenue stream each time firmware is updated. Semiconductor makers such as SK hynix acquired TISAX certification in 2025 to reassure automakers that memory chips meet data-protection criteria, illustrating how cyber-compliance now spans the entire supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Time-to-Market of Homologation | -0.9% | Global, with emerging markets most affected | Medium term (2-4 years) |

| Fragmented Country-Level PTI Regulations | -0.6% | Europe is primary expanding globally | Long term (≥ 4 years) |

| Shortage of EV-Qualified Test Engineers | -0.8% | Global, with Asia-Pacific and North America most impacted | Short term (≤ 2 years) |

| Ethical-AI Audit Gaps for Autonomous Systems | -0.4% | North America and the EU are leading, with limited Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Time-to-Market of Homologation

Divergent U.S. CARB, Euro 7, and Chinese GB standards force OEMs to run parallel validation cycles for identical subsystems. TÜV NORD reports that multiplying rules for pollutant limits, battery durability, and driver-assist functions inflate homologation budgets and add months to launch schedules. Stellantis faced investigations over Opel models that triggered retesting and retrofit campaigns, highlighting reputational exposure when rules are misinterpreted.[3]Stellantis N.V., “Annual Report 2024,” stellantis.com Small suppliers feel the pinch most; certification fees can exceed 10% of annual revenue for niche component makers. The push toward multi-energy platforms intensifies the burden because each propulsion type must satisfy distinct test matrices without cross-credit among regulators.

Fragmented Country-Level PTI Regulations

Lack of harmonization across Europe keeps inspection-interval policies locked in national silos. Vehicles moving from a 12-month jurisdiction to a 48-month one may face redundant checks without measurable safety benefit, undercutting economies of scale for pan-European TIC networks. Each authority mandates its own accreditation path, equipment calibration, and inspector-licensing criteria, driving up compliance costs for service providers. The European Commission’s proposals for uniform PTI standards meet resistance from member states guarding sovereignty, prolonging uncertainty. Until convergence occurs, investors hesitate to fund continent-wide inspection-station upgrades, curbing modernization of brake-particle and battery-health test rigs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Dominates, Certification Accelerates

Testing held a 60.85% share of the automotive testing, inspection, and certification market in 2025, reflecting its indispensability for validating hardware durability, EMI resilience, and safety-critical software. Continued demand for full-vehicle crash tests, battery thermal-runaway chambers, and vehicle-in-the-loop (VIL) simulations anchors the segment’s scale advantage. Certification, though smaller, is growing fastest at 5.12% CAGR because UNECE R155/R156 obligate OEMs to prove cybersecurity and software-update competence before any new model is registered. Each mandatory certificate unlocks downstream testing contracts for periodic audits and OTA re-approvals.

Digital-twin adoption is reshaping revenue composition. dSPACE’s AURELION platform enables Mercedes-Benz to perform sensor-realistic driving scenario validation that regulators accept as equivalent to road miles. Such simulation reduces physical-prototype counts, but it does not diminish testing volume; instead, it shifts spend to high-performance computing clusters and data-validation services. Providers pairing track facilities with certified simulation suites secure multi-phase bookings covering concept, design, and homologation. The automotive testing, inspection, and certification market size tied to software-driven validation is set to widen as developers ask regulators to credit virtual kilometers toward compliance targets.

By Sourcing Type: Outsourcing Momentum Intensifies

Outsourced contracts accounted for 74.62% of the automotive testing, inspection, and certification market size in 2025 and are forecast to expand at a 4.83% CAGR through 2031. OEMs offload specialized tasks—battery nail-penetration, 5G V2X conformance, penetration testing—to avoid capital outlays on single-use rigs and to access scarce talent. In-house labs remain relevant for early-stage R&D where IP sensitivity is high, yet budget constraints and headcount freezes push even proprietary testing outside corporate walls once concept feasibility is proven.

Investor sentiment validates the trend. Spectris’s USD 630 million takeover of Micromeritics in 2024 signaled confidence in materials characterization demand, while FEV continued opening benchmark centers to serve powertrain clients. Predictive-maintenance programs lengthen equipment life at commercial test centers, allowing price structures that undercut internal labs. As regulatory files grow thicker—each Euro 7 prototype requires up to 20 GB of test data—providers able to manage secure data lakes and generate audit-ready dashboards earn preferred-supplier status in global sourcing rosters.

Geography Analysis

Asia-Pacific’s 48.12% share in 2025 and 5.26% CAGR through 2031 confirm the region as the gravitational center of the automotive testing, inspection, and certification market. China’s mandate for enhanced tyre and lighting standards, couples with the world’s highest electric-vehicle adoption, is funneling battery-pack and EMC validation work to domestic TIC zones. India’s NATRAX alliance with TÜV SÜD has cut lead times for ADAS and electromagnetic-compatibility tests, supporting the country’s surge in compact SUV exports. Japan’s advanced autonomous-drive pilots and South Korea’s prominence in automotive semiconductors add layers of software and memory-device certification volume. Yet regulatory harmonization remains modest; labs must hold discrete accreditations for GB, AIS, and J-type standards, reinforcing multiyear project bookings for globally connected providers.

Europe sustains significant weight thanks to rule-making leadership. Euro 7 emissions ceilings and circular-economy directives keep demand robust for powertrain durability, battery recycling, and end-of-life dismantling audits. The region houses dense networks of TÜV, SGS, and Bureau Veritas facilities that possess deep regulators’ trust. Eastern European nations attract new lab investments as cost-effective alternatives to legacy Western European sites, while Brexit complications channel additional certification runs to continental labs. Continued refinement of UNECE and ISO standards ensures steady revenue even as light-vehicle sales stagnate.

North America concentrates on autonomous-vehicle and cybersecurity validations. DEKRA’s USD 22.8 million Michigan expansion in 2024 added climatic chambers and 5G test bays to serve a pipeline of vehicle-software overhauls. U.S. federal and California CARB rules seldom align perfectly, so manufacturers rely on TIC firms to separate and manage dual-path programs. Mexico’s rising role as a manufacturing hub generates cross-border testing demand, especially for NAFTA-compliant emissions and safety certifications. South America and the Middle East, and Africa show emerging, if uneven, promise. Brazil’s PROCONVE L7 and L8 standards increase local powertrain testing needs, while Gulf countries invest in inspection centers tied to growing passenger-car fleets. Infrastructure gaps and technician shortages temper growth but also create first-mover advantages for global providers that partner with local governments.

Competitive Landscape

The automotive testing, inspection, and certification market remains moderately fragmented. Global majors such as SGS, Bureau Veritas, TÜV SÜD, TÜV Rheinland, and Intertek defend their share through dense lab networks, multi-standard accreditations, and deep regulator rapport. SGS operated 2,500 laboratories across 115 nations and 99,500 staff in 2024, reflecting a scale that smaller entrants struggle to replicate. Midsize specialists thrive by focusing on fast-growing niches: battery-abuse testing, ADAS sensor calibration, and V2X conformance. Emerging EV-centric players in China and Europe leverage government subsidies to install high-energy cyclers and thermal-shock chambers within new-energy-vehicle clusters.

Technology partnerships are becoming decisive. Continental aligned with Synopsys to embed vehicle digital twins that cut validation time for software releases.[4]Continental, “Vehicle Digital Twin Cooperation with Synopsys,” continental.com TÜV SÜD collaborates with cloud-simulation vendors to certify scenario libraries acceptable to regulators. Providers racing to integrate virtual and physical test-beds can match the software iteration cadence of modern vehicle programs, winning renewal contracts tied to OTA pipelines rather than model launches.

Price competition remains moderate because accreditations and safety stakes raise switching costs. Yet talent scarcity—especially battery chemists and ethical-AI auditors—raises wage bills across the board. Companies are countering by establishing joint academies with universities and offering remote-testing portals that let OEM engineers watch test runs online, reducing travel expenditure and reinforcing client lock-in.

Automotive TIC Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Continental and Synopsys announced delivery of vehicle digital twin capabilities that blend dSPACE simulation models with NVIDIA DRIVE Sim to accelerate software validation.

- February 2025: Stellantis disclosed USD 314.5 million in BEV sales, expanded its STLA platform family, and confirmed a EUR 4.1 billion (USD 4.63 billion) LFP gigafactory joint venture with CATL in Spain.

- January 2025: SGS TÜV Saar broadened automotive-cybersecurity offerings to include ISO/SAE 21434 training and multi-country Common-Criteria evaluations.

- January 2025: SK hynix earned TISAX certification for South Korean facilities to assure data-security conformity for automotive memory chips.

Global Automotive TIC Market Report Scope

The market is defined by the revenue generated by the third-party TIC service providers globally in the automotive industry. Only testing, inspection, and certification services have been considered for market estimation. Therefore, other services, such as training, auditing, and consulting, are excluded from the scope.

The testing, inspection, and certification market for the automotive industry is segmented by service type (testing, inspection, certification) and geography (Americas (United States, Mexico, Brazil, Rest of Americas), Europe (Germany, Spain, France, Rest of Europe), Asia-Pacific (China, Japan, Korea, India, Rest of Asia-Pacific), Middle East and Africa). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the automotive TIC market and its growth outlook?

The automotive TIC market stands at USD 21.28 billion in 2026 and is projected to reach USD 26.86 billion by 2031, reflecting a 4.78% CAGR.

Which region leads the automotive TIC market and which grows fastest?

Asia-Pacific holds the largest 48.12% share, while Asia-Pacific posts the fastest 5.26% CAGR through 2031.

Which service segment is expanding most rapidly in the automotive TIC market?

Certification services show the strongest momentum, advancing at a 5.12% CAGR as electric and autonomous vehicles increase regulatory complexity.

Why are OEMs increasing outsourcing of automotive TIC services?

Specialized battery, hydrogen and cybersecurity tests require costly infrastructure and expertise, prompting OEMs to outsource work that is non-core yet compliance-critical.

How do new cybersecurity regulations influence demand in the automotive TIC market?

UNECE R155/R156 rules mandate lifecycle cybersecurity certification, turning one-time tests into recurring validation programs and generating steady revenue for TIC providers.

What drives the surge in battery testing within the automotive TIC market?

Stricter safety rules such as China’s “No Fire, No Explosion” standard and global fast-charging adoption elevate demand for advanced thermal-runaway and abuse testing.

Page last updated on: