Industrial Radiography Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

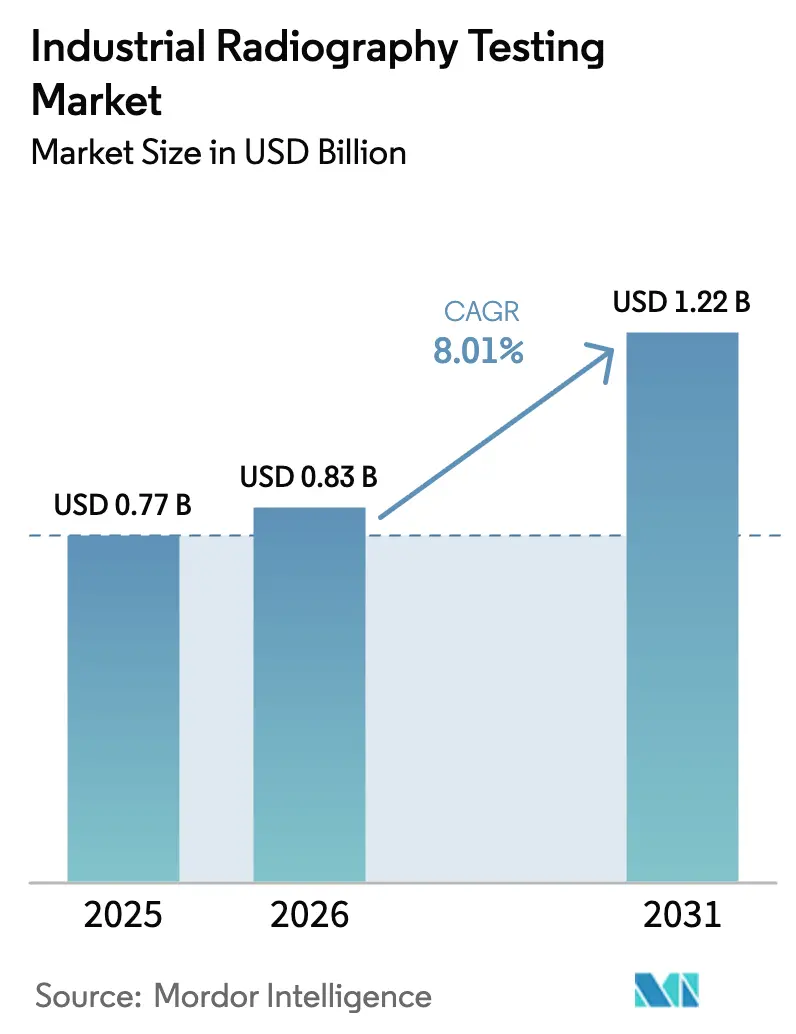

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Radiography Testing Market Analysis by Mordor Intelligence

The Industrial radiography testing market size is expected to increase from USD 0.77 billion in 2025 to USD 0.83 billion in 2026 and reach USD 1.22 billion by 2031, growing at a CAGR of 8.01% over 2026-2031. Demand is advancing as end users replace film with digital flat-panel detectors, shrinking inspection cycles and lowering consumable costs. Inline computed-tomography (CT) scanners are moving from R&D cells into high-volume aerospace, additive-manufacturing, and battery-pack lines, where volumetric data validates structural integrity in minutes. Pipeline operators are expanding use of crawler-mounted X-ray systems to satisfy stricter API 1104, ASME B31.3, and ISO 17636-2 mandates, while electronics assemblers adopt micro-focus units that reveal sub-micron voids in silicon-carbide power modules. Software-centric revenue is rising as artificial-intelligence (AI) algorithms cut radiographer review times and unlock outcome-based service contracts, even as capital-expenditure headwinds temper uptake among small service firms. Competitive pressure revolves around reusability economics, AI-ready detectors, and partnerships that bundle hardware, cloud analytics, and certified interpretation services, signaling a shift toward solution-centric rather than component-centric differentiation.

Key Report Takeaways

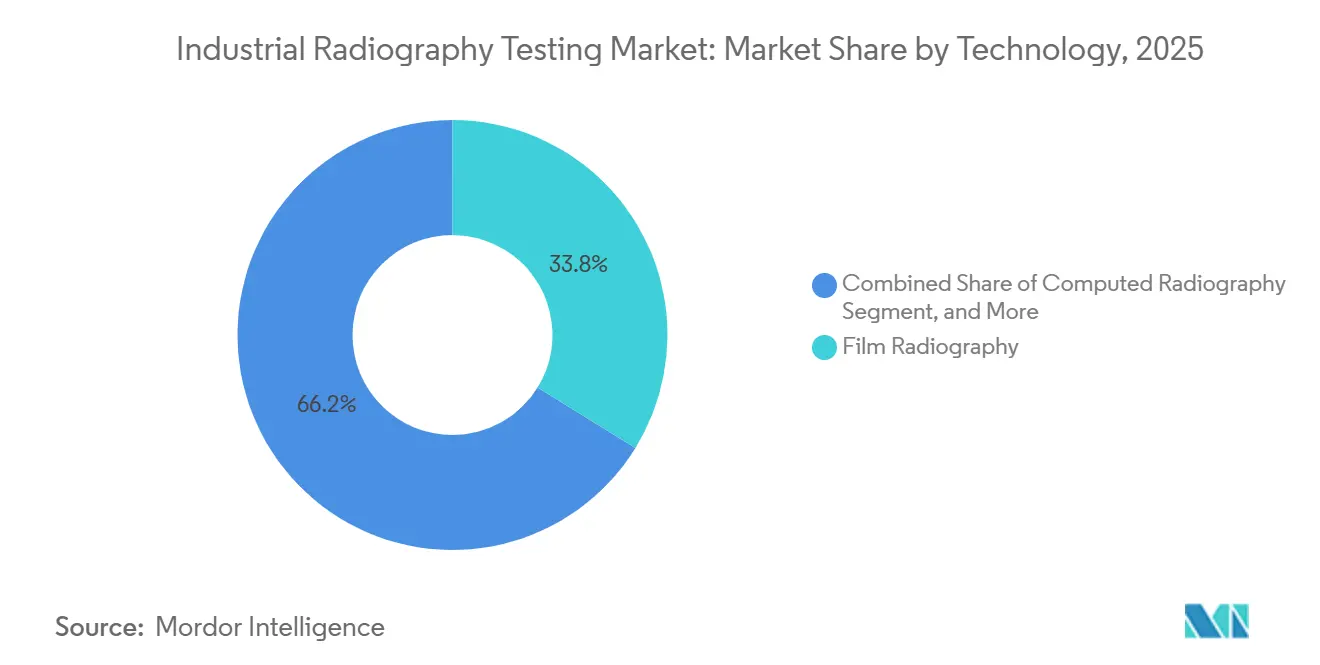

- By technology, film radiography led with 33.81% of Industrial radiography testing market share in 2025, while direct radiography is advancing at an 8.08% CAGR through 2031.

- By imaging technique, X-ray radiography commanded 70.48% revenue share in 2025, and digital X-ray radiography is projected to post an 8.11% CAGR between 2026-2031.

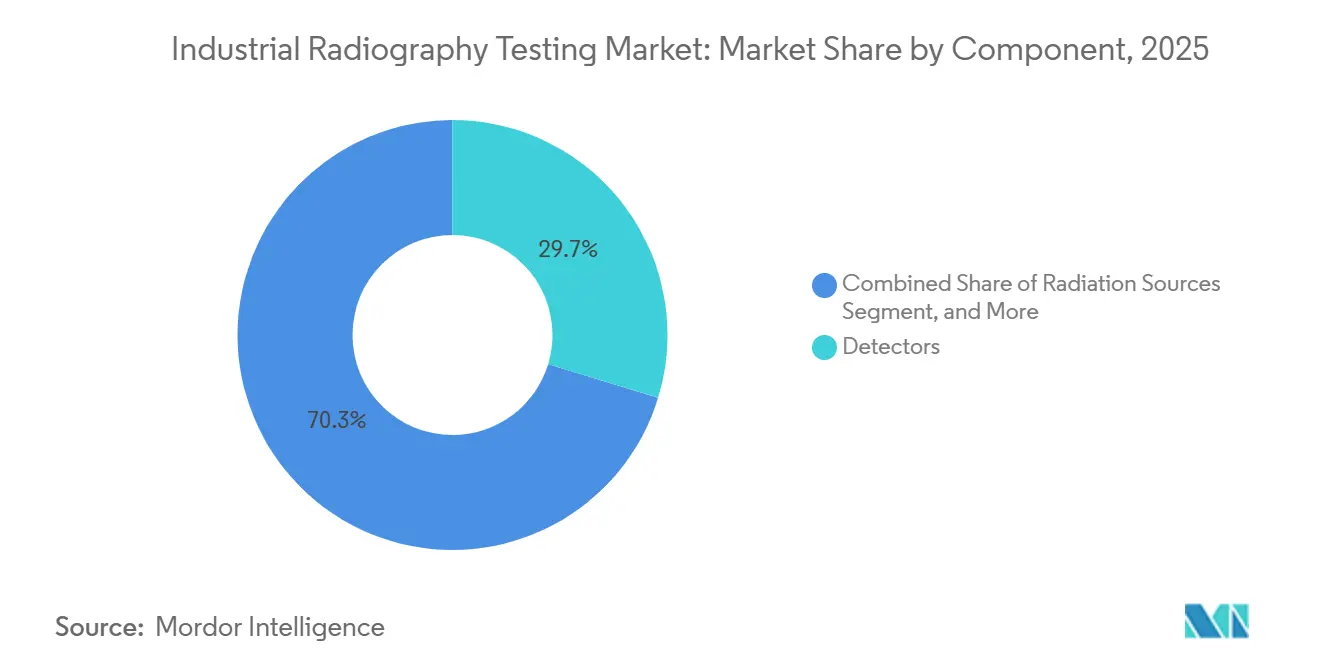

- By component, detectors captured 29.72% of 2025 revenue, whereas software and services are forecast to expand at an 8.05% CAGR during 2026-2031.

- By end-user industry, oil and gas and petrochemical applications accounted for 23.93% of 2025 demand, while electronics and semiconductors are expected to grow fastest at an 8.15% CAGR to 2031.

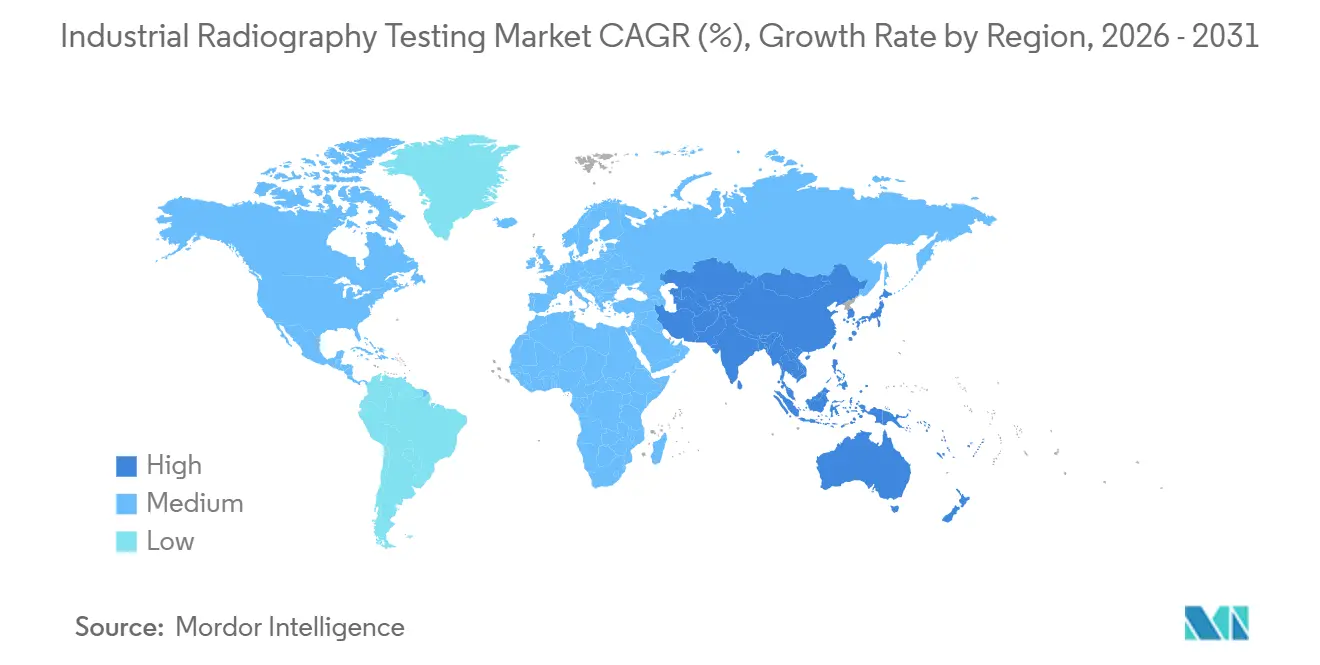

- By geography, Asia-Pacific held 32.64% of 2025 revenue and is projected to rise at an 8.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Radiography Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Volumetric Inspection in Aerospace and Automotive Lightweight Assemblies | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Stringent Safety Regulations for Oil and Gas Pipeline Integrity | +1.5% | Global, concentration in Middle East, North America | Long term (≥4 years) |

| Migration from Film to Digital Radiography Accelerating Inspection Throughput | +1.4% | Global | Short term (≤2 years) |

| Renewable-Energy Build-Out Driving Wind-Blade and Pressure-Vessel Testing | +1.2% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Inline CT for Additive-Manufacturing Production Quality Assurance | +1.0% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Micro-Focus X-Ray for SiC Power-Electronics Packaging in EV Factories | +0.9% | Asia-Pacific, Europe, North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Volumetric Inspection in Aerospace and Automotive Lightweight Assemblies

Composite airframes and battery-electric vehicle platforms require three-dimensional mapping of porosity, delaminations, and weld defects that two-dimensional film cannot reveal. Inline CT units delivering sub-100-micrometer voxel resolution are now on final assembly lines, enabling real-time go/no-go decisions. Automotive battery-pack makers use microfocus X-ray to validate aluminum-to-copper ultrasonic welds in bus bars, thereby averting thermal-cycle-induced cracking. Detector vendors respond with larger flat-panel arrays and faster reconstruction algorithms, cutting scan-to-report times from hours to minutes. These productivity gains reinforce the 8.08% growth trajectory of direct radiography systems.

Stringent Safety Regulations for Oil and Gas Pipeline Integrity

API 1104 mandates 100% radiographic examination of girth welds on sour-gas lines, and ASME B31.3 extends volumetric testing to Category M fluids where leaks pose immediate hazards.[1]American Petroleum Institute, “API 1104 – Welding of Pipelines and Related Facilities,” api.org Saudi Aramco’s USD 10 billion Master Gas System Phase 3 is the marquee example fueling crawler-based automated radiography across 4,000 km of new pipe. Harmonized digital standards such as ISO 17636-2 unlock cross-border equipment qualification, lowering re-inspection risk and supporting global adoption. These rules sustain long-term demand despite oil price swings.

Migration from Film to Digital Radiography Accelerating Inspection Throughput

Film’s wet-chemistry workflow and single-use consumables cap daily shot volume, clashing with lean-manufacturing imperatives. Flat-panel detectors capture images in seconds, eliminate darkrooms, and integrate with DICONDE archives that maintain regulatory traceability. Reusable panels rated for up to 1 million exposures deliver payback inside two years at mid-volume sites, according to GE Vernova cost models. Global codes that equate ISO 17636-2 digital acceptance criteria with film have erased regulatory friction, propelling rapid conversion.

Renewable-Energy Build-Out Driving Wind-Blade and Pressure-Vessel Testing

Offshore and onshore wind programs specify radiography for composite blades exceeding 80 m, where ultrasonic coupling falters, and defects such as wrinkles or dry spots degrade performance.[2]International Electrotechnical Commission, “IEC 61400-5 – Wind Turbine Blades,” iec.ch Hydrogen-storage vessels built to ASME Section VIII-2 also require radiographic weld verification before entering cyclic pressure service. Portable battery-powered X-ray sets now operate in remote wind farms, expanding addressable field applications and reinforcing digital X-ray’s 8.11% growth rate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex and Total Cost of Ownership of Digital Flat-Panel Detector Systems | -1.2% | Global, acute in price-sensitive emerging markets | Short term (≤2 years) |

| Radiation-Safety Compliance Downtime | -0.8% | North America, Europe, regulated markets | Medium term (2-4 years) |

| Shortage of Certified Level-III Radiographers | -0.7% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Competition from Phased-Array UT and Terahertz in Composites | -0.5% | North America, Europe aerospace and automotive hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex and Total Cost of Ownership of Digital Flat-Panel Detector Systems

Detector prices ranging from USD 50,000 to USD 150,000 slow adoption among small contractors, stretching payback to three years or more when annual shot counts are low. Computed radiography plates offer a cheaper interim step but lack the instantaneous readout that high-throughput plants require. Vendors are piloting lease and subscription models, yet the absent secondary-market liquidity and fluctuating import duties deter many emerging-market buyers. As a result, film persists in low-volume, price-sensitive geographies.

Radiation-Safety Compliance Downtime

North American and European regulators require exclusion zones, dosimetry, and periodic leak testing, which can idle inspection crews for hours each shift.[3]Nuclear Regulatory Commission, “Radiation Safety Requirements for Industrial Radiography,” nrc.gov Although electrically switchable X-ray tubes reduce the risk of continuous exposure, site permitting, badge monitoring, and quarterly audits still add non-productive time. Service firms offset by integrating AI-based screening to compress human review, but compliance downtime remains a fixed overhead that squeezes margins, particularly for field jobs with tight turnaround windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Direct Radiography Gains as Reusability Economics Favor Digital Detectors

Direct radiography captured incremental share from film in 2025 as organizations realized that reusable panels slashed consumable outlays, helping the Industrial radiography testing market size for digital workflows accelerate at an 8.08% CAGR. Capital costs remain higher than computed radiography plates, yet lean lines prize the real-time feedback that only direct systems provide. Aerospace integrators now specify flat-panel detectors rated for at least 100 kV, 1,000,000 shot lifetimes, and DICONDE compliance, ensuring uniform data trails across fleets. In additive manufacturing, CT extensions of direct radiography generate volumetric defect maps that validate powder bed builds layer by layer, a capability film cannot match.

Film retains relevance in remote field work where power is scarce and single-use cassettes prove simpler to deploy, but its Industrial radiography testing market share is eroding steadily. ISO 17636-2’s equivalence to film-based ISO 17636-1 eliminated regulatory hurdles, triggering a wave of film darkroom decommissioning. Computed radiography plates sit between film and direct panels as a migration bridge, though their 60-second plate scans fall short in high-throughput auto and electronics plants. Looking forward, neural-network-assisted reconstruction will further compress scan-to-report loops, strengthening direct radiography’s hold on growth applications and widening the performance gap over legacy workflows.

By Imaging Technique: Digital X-Ray Radiography Outpaces Gamma-Ray as Regulatory Burden Intensifies

X-ray techniques accounted for 70.48% of 2025 revenue, and the Industrial radiography testing market size tied to digital X-ray tubes is projected to expand briskly through 2031 as users avoid the licensing and disposal headaches of Iridium-192 and Cobalt-60. Modern 450 kV tubes penetrate 100 mm steel plates once reserved for gamma sources, rendering isotopes non-essential outside select deep-field pipeline sites. National regulators aligned with the IAEA code have raised the paperwork bar, nudging service firms toward tube-based alternatives that switch off instantly and curb safety zones.

Gamma-ray retains a foothold in off-grid pipeline construction because portable isotopes sidestep generator logistics, yet its industrial radiography market share is drifting lower each year. Micro-focus X-ray, a high-end subset, is booming in semiconductor fabs, where sub-micron focal spots reveal voids in system-in-package solder joints. Meanwhile, CT, sitting atop the X-ray hierarchy, wins programs that demand volumetric quantification, think composite wing boxes and rocket turbopump castings. Together, these trends place digital X-ray on a strategic growth arc, while gamma moves toward niche status under tightening safety regimes.

By Component: Software and Services Expand as AI Automates Defect Classification

Detectors remained the single largest hardware line in 2025, but the revenue pool tied to software subscriptions, cloud analytics, and predictive-maintenance packages is expanding at an 8.05% CAGR. AI classifiers cut Level-III review hours by flagging less than 0.1% false positives, freeing scarce experts to focus on borderline calls. As a result, outcome-based contracts that guarantee detection probability rather than time-and-material billing are gaining favor, shifting value from hardware to integrated platforms.

X-ray tubes and generators still anchor capital budgets, yet refurbishment programs delay full-system refresh cycles. Radiation sources, mainly gamma, are declining for reasons noted above, while film and consumables shrink as direct panels proliferate. Vendors bundle five-year cloud licenses with detector sales, capturing annuity revenue even when hardware margins compress. This pivot toward services ensures steady cash flows and embeds customers longer, reshaping competitive playbooks across the Industrial radiography testing market.

By End-User Industry: Electronics and Semiconductors Surge on Advanced Packaging Inspection Needs

Oil and gas weld testing provided 23.93% of demand in 2025, however fabs chasing 3 nm nodes and silicon-carbide power devices now fuel the fastest gains. Inline CT stations sit beside wafer-grinding and die-bonding lines, scanning each package for voids that trigger electrical failure, a need driving an 8.15% CAGR within the Industrial radiography testing market. Aerospace and defense continue ordering multi-MeV CT gantries to validate composite fuselages and additive-manufactured turbine blades, while nuclear operators rely on periodic radiography to meet ASME Section XI codes.

Automotive battery-pack makers deploy micro-focus tubes to audit ultrasonic welds linking copper tabs to aluminum bus plates. Construction crews still use film to check post-tensioned cables, yet digital portability is encroaching here as well. Medical-device and cultural-heritage users form smaller but technically demanding niches, valuing ultra-low energy settings and high-contrast capture. Collectively, these verticals ensure diversified revenue streams that cushion cyclical swings in any single sector.

Geography Analysis

Asia-Pacific anchored 32.64% of 2025 revenue, and the region’s Industrial radiography testing market size is projected to grow at an 8.22% CAGR, the fastest worldwide. China’s infrastructure pipeline and gigafactory build-outs demand crawler-mounted digital systems that meet ISO 17636-2, while India expands technician training under ISO 9712 to feed aerospace offsets. Japan and South Korea invest in micro-focus X-ray for vehicle electrification and shipyard weld audits, and Australia’s LNG terminals favor battery-powered sets for remote field work. Local price sensitivity keeps film alive in smaller workshops, yet tier-one exporters are moving full-speed toward digital compliance.

North America’s mature code environment, spanning API 1104, ASME B31.3, and ASME Section XI, secures baseline demand even as a graying workforce caps throughput. University apprenticeships, online courses, and AI pre-screeners aim to fill the gap, but certifications require years to accrue. Europe mirrors this demographic pinch, yet its nuclear-life-extension and offshore wind programs sustain CT orders. Germany’s auto suppliers add micro-focus lines for battery packs, and the United Kingdom’s PCN scheme backs skilled labor mobility within the bloc.

Middle East projects such as Saudi Aramco’s Master Gas System Phase 3 inject sizeable crawler volumes, while the United Arab Emirates trials robotic radiography to minimize worker dose. South America’s mining belts in Brazil and Argentina deploy ruggedized X-ray sets, contending with currency swings that delay fleet upgrades. Africa sees pockets of growth in South African mining and Egyptian gas networks, but scarcity of training centers slows certification pipelines. Across these varied backdrops, regulators’ convergence around ISO 17636-2 and DICONDE archives supports cross-border equipment reuse, reinforcing the global integration of the Industrial radiography testing market.

Competitive Landscape

The Industrial radiography testing market exhibits moderate fragmentation as global detector OEMs, X-ray tube makers, and regional service companies vie for share. Multinationals bundle detectors, tubes, and AI software into multi-year service contracts that lock in consumables and cloud fees. Baker Hughes’ 2024 purchase of Quest Integrity pivoted its portfolio toward outcome-based inspection, guaranteeing defect-detection probability instead of merely selling scans. Comet Group booked CHF 741.8 million (USD 838.8 million) in 2024, underscoring the resilience of diversified X-ray, RF power, and CT offerings. Waygate Technologies introduced the Phoenix Micromex micro-CT in March 2024, targeting electronics packaging, and followed with the long-life XLG 3501 tube in October 2024, lowering per-shot costs for high-volume lines.

Specialists chase white-space niches such as battery-cell weld CT, offshore wind-blade bond-line mapping, and hydrogen-tank weld inspection, areas where legacy methods struggle. Oak Ridge National Laboratory’s Simurgh AI framework, created with ZEISS, slashes CT scan counts by 40% via neural reconstructions, a leap that early adopters use to pitch inline CT for additive manufacturing. Vendors differentiate on panel durability- some warrant up to 1 million shots- scan speed, and AI integration depth. Workforce shortages push automation, Level-II techs now clear most images after AI triage, reserving scarce Level-III sign-off for edge cases.

Price competition intensifies in emerging markets where film remains entrenched, prompting OEMs to offer entry-level CT such as ZEISS Metrotom 1 OS launched in May 2024. Subscription models that bundle detectors with cloud analytics spread cap-ex over time, easing adoption barriers. Regulatory convergence on DICONDE and ISO 17636-2 means interoperability is no longer a lock-in moat, so players race to embed predictive analytics and remote-assistance tools that raise switching costs. Overall, the top five suppliers command a considerable share of global revenue, indicative of a balanced mix of global brands and regional challengers.

Industrial Radiography Testing Industry Leaders

Fujifilm Holdings Corporation

Nikon Corporation

Waygate Technologies GmbH

Comet Holding AG

Baker Hughes Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mistras Group, Inc. continued expansion of its digital radiography service offerings across North American oil and gas pipeline projects, leveraging automated defect-recognition software to address the shortage of certified Level-III radiographers.

- January 2026: Nikon Corporation announced enhancements to its industrial metrology portfolio, integrating artificial-intelligence algorithms into computed-tomography reconstruction workflows.

- December 2025: Shimadzu Corporation expanded its X-ray inspection system production capacity at its Kyoto manufacturing facility, responding to growing demand from electronics and semiconductor customers requiring inline inspection of advanced packaging assemblies.

- November 2025: Fujifilm Holdings Corporation launched an upgraded digital radiography detector featuring enhanced cesium-iodide scintillator technology, delivering improved image quality at lower radiation doses.

Global Industrial Radiography Testing Market Report Scope

Industrial radiographic testing (RT) is a nondestructive examination (NDE) technique that uses X-rays or gamma rays to inspect the internal structure of a component. It is extremely reproducible, can be used with various materials, and the data collected can be stored for later analysis. Radiography is an effective and efficient tool that requires minimal surface preparation. Furthermore, many radiographic systems are portable, allowing use in the field and at elevated positions.

The Industrial Radiography Testing Market Report is Segmented by Technology (Film Radiography, Computed Radiography, Direct Radiography, and Computed Tomography), Imaging Technique (X-Ray Radiography, and Gamma-Ray Radiography), Component (Detectors, X-Ray Tubes and Generators, Software and Services, Radiation Sources, and Imaging Plates/Films and Consumables), End-User Industry (Aerospace and Defense, Oil and Gas and Petrochemical, Energy and Power Generation, Automotive and Transportation, Manufacturing and Industrial Machinery, Construction and Infrastructure, Electronics and Semiconductors, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Film Radiography |

| Computed Radiography |

| Direct Radiography |

| Computed Tomography |

| X-Ray Radiography |

| Gamma-Ray Radiography |

| Detectors |

| X-Ray Tubes and Generators |

| Software and Services |

| Radiation Sources |

| Imaging Plates/Films and Consumables |

| Aerospace and Defense |

| Oil and Gas and Petrochemical |

| Energy and Power Generation |

| Automotive and Transportation |

| Manufacturing and Industrial Machinery |

| Construction and Infrastructure |

| Electronics and Semiconductors |

| Othe End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | Film Radiography | |

| Computed Radiography | ||

| Direct Radiography | ||

| Computed Tomography | ||

| By Imaging Technique | X-Ray Radiography | |

| Gamma-Ray Radiography | ||

| By Component | Detectors | |

| X-Ray Tubes and Generators | ||

| Software and Services | ||

| Radiation Sources | ||

| Imaging Plates/Films and Consumables | ||

| By End-User Industry | Aerospace and Defense | |

| Oil and Gas and Petrochemical | ||

| Energy and Power Generation | ||

| Automotive and Transportation | ||

| Manufacturing and Industrial Machinery | ||

| Construction and Infrastructure | ||

| Electronics and Semiconductors | ||

| Othe End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the industrial radiography testing market in 2026?

The industrial radiography testing market size is USD 0.82 billion in 2026.

What CAGR is forecast for industrial radiography testing through 2031?

The market is projected to expand at an 8.25% CAGR from 2026 to 2031.

Which technology segment is growing fastest?

Computed tomography is advancing at 8.98% CAGR, driven by additive-manufacturing and aerospace demand.

Which region shows the most rapid growth?

Asia-Pacific posts the highest CAGR at 9.18% through 2031, led by China and India.

What is a key restraint facing adoption of digital radiography?

High capital expenditure for flat-panel detectors, ranging from USD 150,000 to USD 500,000, slows uptake among smaller service firms.

Page last updated on: